Sample Category Title

AUD/USD Daily Report

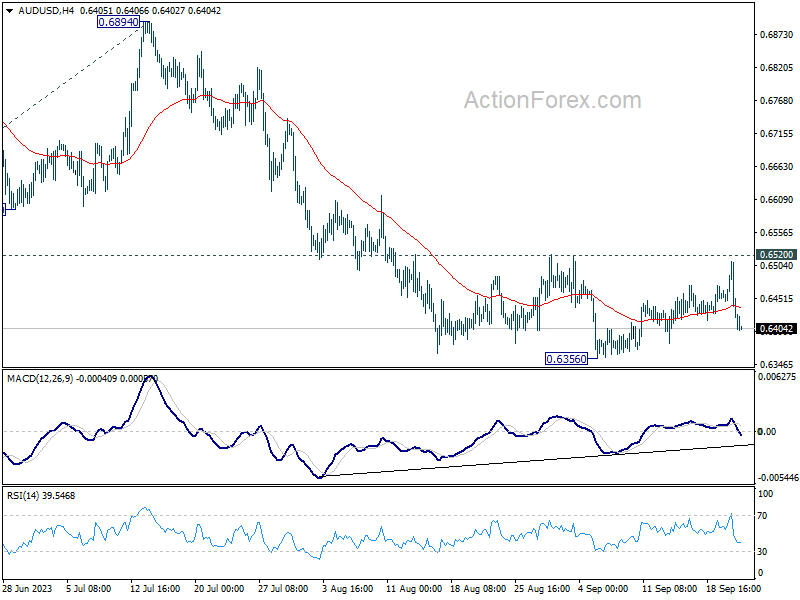

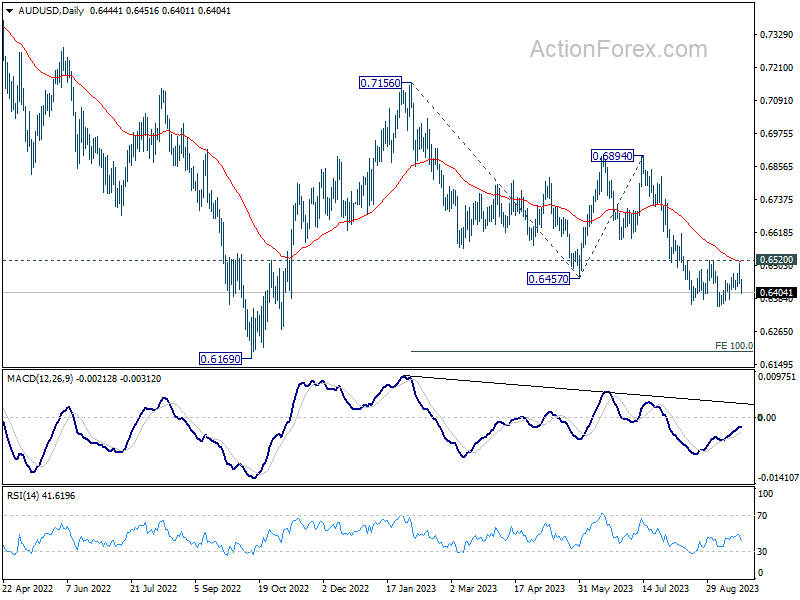

Daily Pivots: (S1) 0.6422; (P) 0.6466; (R1) 0.6493; More...

AUD/USD is holding in range of 0.6356/6520 despite near term volatility. Intraday bias stays neutral for the moment. Outlook stays bearish with 0.6520 resistance intact. On the downside, break of 0.6356 will resume larger down trend to 100% projection of 0.7156 to 0.6457 from 0.6894 at 0.6195.

In the bigger picture, down trend from 0.8006 (2021 high) is possibly still in progress. Decisive break of 0.6169 will target 61.8% projection of 0.8006 to 0.6169 to 0.7156 at 0.6021. This will now remain the favored case as long as 0.6894, in case of strong rebound.

ECB’s Nagel uncertain if rate plateau is reached

ECB Governing Council, Joachim Nagel, Bundesbank head, posed a crucial question in his speech in Frankfurt, "Have we reached the plateau" on interest rates? He answered by stating that it "cannot yet be clearly predicted". He continued, elaborating that "the forecasts still only show a slow decline toward the target level of 2%."

Nagel's comments hinted at the continuous monitoring of economic indicators, suggesting that while borrowing costs are expected to "remain at a sufficiently high level for a sufficiently long time," the exact interpretation hinges on the incoming data.

Addressing concerns about Germany's economic health, he remarked that characterizing Germany as the 'sick man' "seems exaggerated." He attributed the present sluggish growth to specific influences such as the global economic deceleration, Russia's conflict with Ukraine, and reduced public expenditure. Offering a silver lining, Nagel projected, "Once we get past the worst of these special factors, the weak growth should also ease. We expect the economy to grow again in 2024."

On the other hand, Latvia's central bank chief, Martins Kazaks, highlighted the structural nature of recent oil price hikes. He pointed out, "The recent oil price increase in my view is not a temporary or transitory, it's very much a structural issue." Such dynamics, according to Kazaks, present heightened inflation risks. Regarding the anticipated rate cuts, he expressed skepticism about their timing, asserting, "I think expecting rate cuts mid next year is somewhat too early."

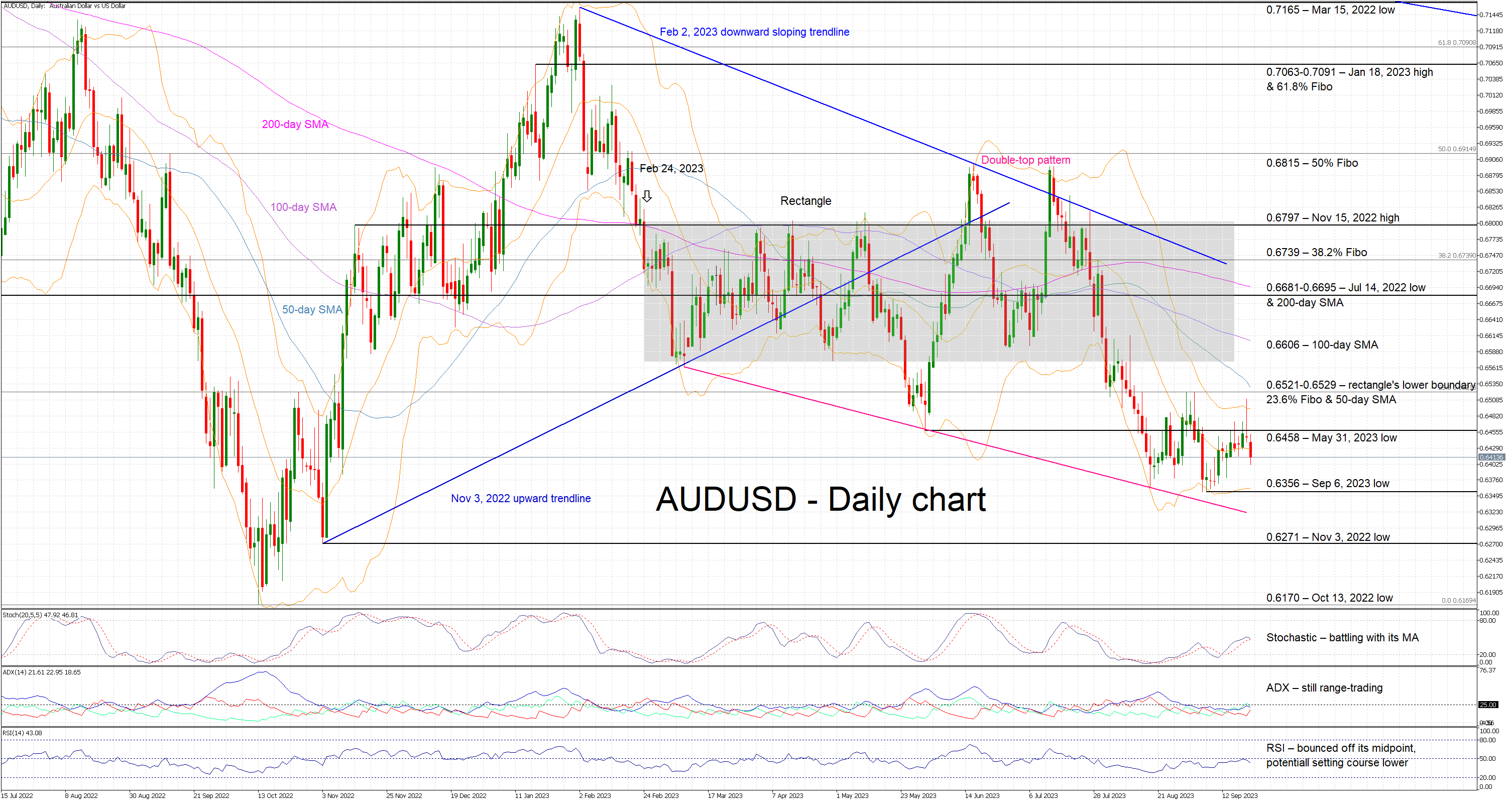

AUDUSD Edges Lower, Bearish Sentiment Lingers

- AUDUSD is edging lower today, reacting to yesterday’s key event

- The pair remains very close to the new 2023 low registered on September 6

- The momentum indicators appear to support the downleg at this juncture

AUDUSD is experiencing its second straight red candle, canceling out most of the upleg recorded since the September 6 low. The overall sentiment remains bearish despite the aggressive sell-off that took place after the formation of the double top pattern in July. Therefore, all eyes are on the momentum indicators at this stage for any clues on the next likely leg in AUDUSD.

In more detail, the RSI continues to hover below its 50-midpoint and now appears to be heading lower. More interestingly, the stochastic oscillator is currently battling with its moving average. The outcome of this battle could play a key role in the next AUDUSD move. On the other hand, the Average Directional Movement Index (ADX) seems uninterested in the recent price action and is stuck below its 25-threshold.

Mixing up the technical picture, an inverse head-and-shoulders pattern appears to be forming with the neckline set at the 0.6521 region. However, a move above this level is necessary for this bullish pattern to become valid.

Should the bulls decide to react to the current pullback, they would try to overcome the May 31, 2023 low at 0.6458, and then set course for the 0.6521-0.6529 region. This is populated by the 23.6% Fibonacci retracement level of the April 5, 2022 – October 13, 2022 downtrend, the rectangle’s lower boundary and the 50-day simple moving average (SMA). Even higher, the 100-day SMA stands at 0.6606.

On the flip side, the bears probably want to capitalize on the current move and gradually test the September 6, 2023 low at 0.6356. They could then possibly set sail for the November 3, 2022 low at 0.6271, with the main target being the October 13, 2022 low at 0.6170.

To sum up, the renewed bearish pressure supported by most momentum indicators appears to bear fruits for the bears but the battle for the next move in AUDUSD has just begun.

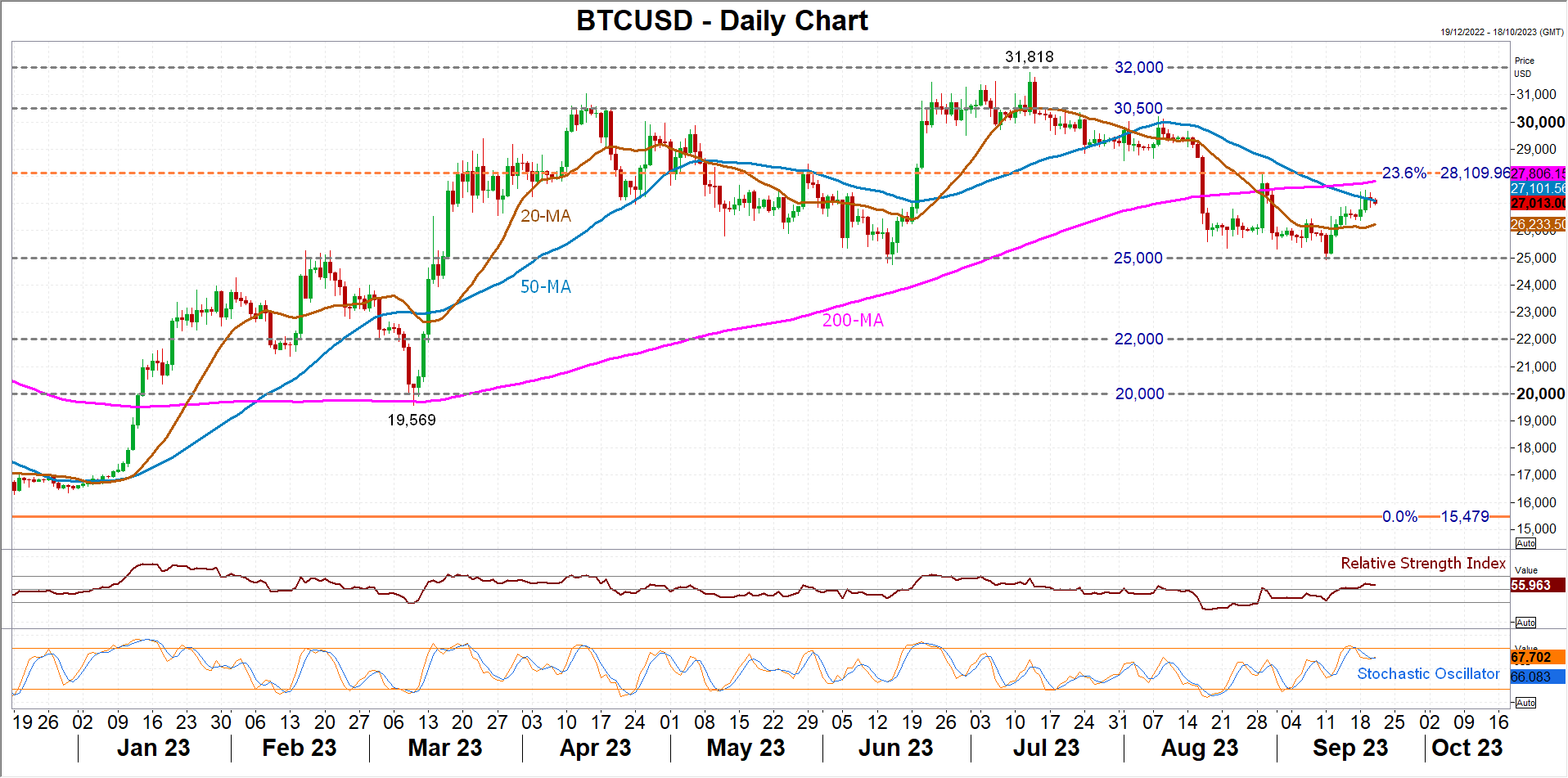

BTCUSD Rebound Tested by 50-day SMA

- BTCUSD remains perky after bouncing off 25,000 support

- But 50-SMA proving to be a difficult obstacle to overcome

- Can Bitcoin maintain its recovery?

BTCUSD (Bitcoin) has extended its rebound from the September 11 low of 24,920. However, the upside pressure has started to wane after coming into contact with its 50-day simple moving average.

The momentum indicators are in the bullish zone but are pointing to some deterioration in the positive bias in the near term. The RSI has started to edge lower, though it remains above the 50-neutral mark for now, while the stochastic oscillator has eased back after briefly entering the overbought region.

If BTCUSD is to stage a sustained recovery, it is critical that it not only conquers the 50-day SMA near 27,100, but also the 200-day SMA just above the 27,800 level, as well as the 23.6% Fibonacci retracement of the November 2021-November 2022 downtrend at 28,110. A break above this strong resistance area would pave the way for the July top of 31,818, although there might be some friction around 30,500 too.

However, if the bullish momentum subsides further and the price turns lower, immediate support should be provided by the 20-day SMA at 26,234. Failing to halt the decline, Bitcoin could then head back towards the 25,000 level. If breached, there could be some support around 22,000. Otherwise, a revisit of the March low of 19,569 would become inevitable.

In brief, there are a number of hurdles standing in the way of Bitcoin’s latest rebound attempt. Only a climb above the July peak of 31,818 would shift the neutral medium-term outlook to a bullish one, while a drop below the 20-day SMA would turn the focus back to the downside.

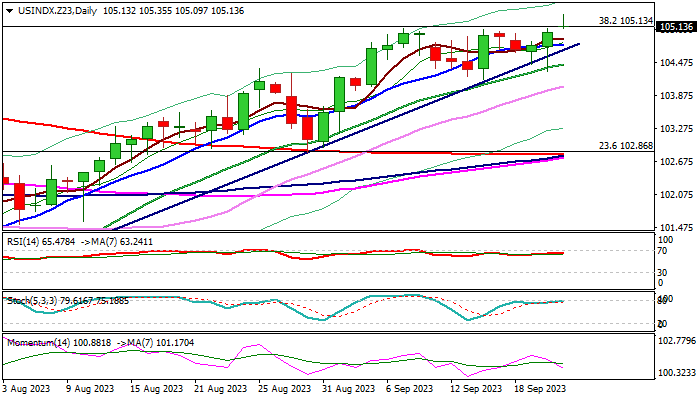

DXY Looking Towards March Highs, to Complete the Higher Degree Recovery

Markets are in risk-off mode after the Fed left its policy rate unchange. The USD extended the gains across the board with DXY catching the March highs. Interesting, Aussie and kiwi are again one of the weakest while MXN is not down much, so for dollar shorts I still faovur to look at USDMXN pairs, while dollar longs can be the best vs NZD and AUD.

Dollar Index Lifted by Fed’s Hawkish Pause

The dollar index rose to new multi-month high in early Thursday, boosted by Fed’s decision to keep rates on hold at September’s meeting but signaling another hike by the end of the year, which markets saw as hawkish rate pause.

The US central bank left its policy rate unchanged at 5.25%-5.50%, in line with expectations, but left the door open for one more hike, expecting interest rate to peak at 5.50%-5.75% range this year.

The policymakers see the overall economic conditions as satisfactory for now that will allow them to keep restrictive policy for extended period, without high risk of significantly harming the economy.

In addition, the Fed signaled it will continue fight with inflation even if prices decline further in coming months, with first rate cuts expected the earliest in mid-2024, if conditions continue to improve, though they downgraded initial projection for 100 basis points cut next year to 50 basis points.

Fresh rise of dollar index price generated initial signal of bullish continuation, after larger bulls paused under pivotal Fibo resistance in past almost three weeks.

Bulls cracked 105.13 barrier (Fibo 38.2% of 114.72/99.20 descend) with close above here seen as a minimum requirement to keep fresh bulls intact for attack at another strong obstacle provided by weekly Ichimoku cloud (spanned between 105.47/106.22).

Firm break above the cloud (which will continue to thicken in coming weeks) is needed to confirm bullish signal.

Daily studies remain bullish overall but fading positive momentum and stochastic about to enter overbought territory, add to headwinds and require caution.

Near-term action should stay above 104.80 zone (10DMA / bull-trendline off 99.20, July 18 low) to keep bullish bias, while increased downside risk to be expected on break below 104.44/17 (20DMA / Sep 14 trough).

Res: 105.47; 105.60; 106.22; 106.96.

Sup: 105.00; 104.80; 104.44; 104.17.

Markets Heed Hawkish Fed

Risk sentiment was forced to turn lower as the Fed delivered its higher-for-longer messaging to markets, projecting fewer-than-anticipated rate cuts for 2024. With potentially one more rate hike to come this year, the US dollar moved back closer to its year-to-date high while global equities tumbled, though spot gold was able to mitigate its losses.

Following the Fed’s latest commentary, markets have now pared bets for US rate cuts in 2024, with next year’s median rate in the dot plot revised up by 50 basis points higher than June’s projections. Chair Powell admitted that a rate cut “will come” but refrained from saying when.

US rates that are kept higher for longer are set to erode an expected tailwind for US stocks and spot gold over the coming year; even a soft landing may not be in the best interests of the bulls. Furthermore, the threat of $100 oil could revive the need for additional rate hikes, further delaying central bankers’ victory lap against still-stubborn inflation.

However, an erosion of US economic resilience, perhaps via the UAW strikes, government shutdown, or a steep drop in consumer spending, may hasten the Fed’s eventual rate cut while potentially providing some year-end cheer for risk-taking activities across global financial markets.

BOE decision on knife’s edge

Markets have slashed bets for another 25-basis point hike by the Bank of England today, with such odds now standing at 48%, in stark contrast to the 80% chance priced in this time last week.

Yesterday’s lower-than-expected August inflation prints are expected to bind the hands of MPC hawks. A rate hike today may even confirm that UK rates have peaked for this cycle.

Dovish signals out of the BOE today, even if it were accompanied by a rate hike, could see GBPUSD bears potentially gunning for the 1.20 psychological level.

SNB bucks expectations and keeps interest rate steady

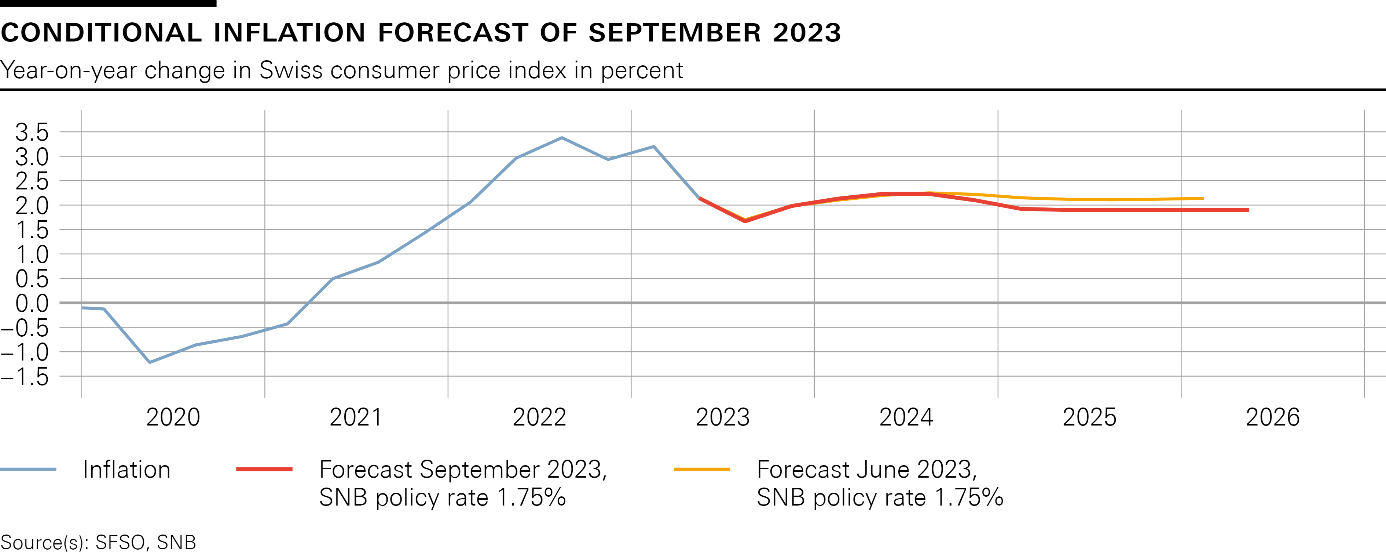

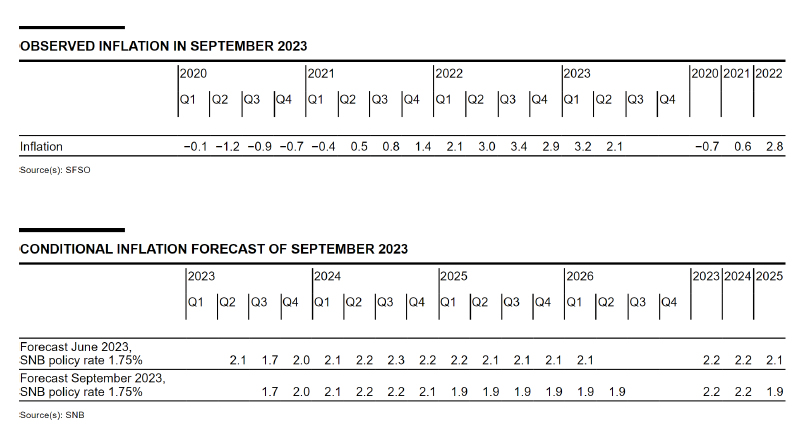

In an unexpected move that diverged from the market's anticipations, SNB held its policy rate steady at 1.75%, side-stepping the anticipated hike to 2.00%. The conditional inflation projections have undergone downward revision. While inflation could surge above 2% target in upcoming quarters, it's projected to retract back to 1.9% in 2025 based on current interest rate, without further tightening.

Despite this, SNB did not completely distance itself from a hawkish tone, and maintained the further tightening "may become necessary". It also reiterated the willingness to intervene in the market with focus on "selling foreign currency

Delving into the specifics of the conditional inflation projections, based on steady 1.75% policy rate, inflation is forecasted to ascend to 2.0% by the end of this year. It will scale up to its apex at 2.2% in the second quarter of 2024, before experiencing a slight dip to 1.9% at the onset of 2025, maintaining that level thereafter.

On the economic growth front, SNB's projections lean towards the cautious side, forecasting tepid growth for the remainder of the year. The annual growth is projected to hover around a modest 1%.

(SNB) Swiss National Bank leaves SNB policy rate unchanged at 1.75%

The Swiss National Bank is leaving the SNB policy rate unchanged at 1.75%. The significant tightening of monetary policy over recent quarters is countering remaining inflationary pressure. From today's perspective, it cannot be ruled out that a further tightening of monetary policy may become necessary to ensure price stability over the medium term. The SNB will therefore monitor the development of inflation closely in the coming months. To provide appropriate monetary conditions, the SNB is also willing to be active in the foreign exchange market as necessary. In the current environment, the focus is on selling foreign currency.

Banks' sight deposits held at the SNB will continue to be remunerated at the SNB policy rate of 1.75% up to a certain threshold. Sight deposits above this threshold will be remunerated at an interest rate of 1.25%, and thus still at a discount of 0.5 percentage points relative to the SNB policy rate.

Inflation has declined further in recent months, and stood at 1.6% in August. This decrease was above all attributable to lower inflation on imported goods and services.

The new conditional inflation forecast is based on the assumption that the SNB policy rate is 1.75% over the entire forecast horizon (cf. chart 1). In the medium term, the new forecast is somewhat below that of June, mainly due to the economic slowdown and slightly lower inflationary pressure from abroad. The inflation forecast puts average annual inflation at 2.2% for 2023 and 2024, and at 1.9% for 2025 (cf. table 1). It is thus just within the range of price stability at the end of the forecast horizon.

Global economic growth was moderate in the second quarter of this year. Although inflation continued to decline in many countries, it remains clearly above the respective targets. Against this background, numerous central banks tightened their monetary policy further during the last quarter, albeit at a slower pace than in the previous quarters.

The growth outlook for the global economy in the coming quarters remains subdued. At the same time, inflation is likely to remain elevated worldwide for the time being. Over the medium term, however, it should return to more moderate levels, not least due to more restrictive monetary policy.

This scenario for the global economy remains subject to large risks. In particular, the high inflation in some countries could be more persistent than expected, necessitating a further tightening of monetary policy there. Equally, the energy situation in Europe could deteriorate again in Q4 2023 and Q1 2024. A pronounced slowdown in the global economy therefore cannot be ruled out.

Swiss GDP stagnated in the second quarter of 2023. The services sector once again grew solidly, while value added in manufacturing contracted significantly. The labour market remained robust, and utilisation of overall production capacity continued to be above average, albeit only slightly.

Growth is expected to remain weak for the rest of the year. Subdued demand from abroad, the loss of purchasing power due to inflation, and more restrictive financing conditions are having a dampening effect. Overall, Switzerland's GDP is likely to grow by around 1% this year. In this environment, unemployment will probably continue to rise slightly, and the utilisation of production capacity is likely to decline somewhat.

The forecast for Switzerland, as for the global economy, is subject to high uncertainty. The main risk is a more pronounced economic slowdown abroad.

Momentum on the mortgage and real estate markets has weakened noticeably in recent quarters. However, the vulnerabilities in these markets remain.

What Will the BoE Do?

The Federal Reserve (Fed) maintained interest rates unchanged, as expected. It revised its growth forecast higher, as expected. The peak unemployment rate was revised to 4.1%, down from 4.5% as a result of a resilient jobs market. The Fed President Jerome Powell said that they are getting close to where they want to be and that the bank must ‘proceed carefully’ on the last mile. He also said that the positive pressure on yields was due to strong growth prospects and an abundance of Treasury issuance rather than higher inflation. And the dot plot showed one more rate hike before the end of this year, and less cuts next year.

So yes, the Fed announcement was hawkish, without much surprise. The market reaction was smooth and unsurprising, as well. The US 2-year yield spiked to 5.20%, the 10-year yield reached 4.45%. Both the S&P500 and Nasdaq slipped below their ascending base building since October, while the US dollar index extended gains and pulled out the all-important Fibonacci resistance. The index now trades above the major 38.2% Fibonacci retracement on past year’s rally, potentially marking the end of the last year’s bearish trend. The next bullish targets stand at 107 than 109 levels.

The only thing that could slow down the US dollar’s appreciation is a hawkish shift in other major central bank’s policies. But with the European Central Bank (ECB) preparing to pause rate hikes as soon as next meeting, and the Bank of England (BoE) expected to announce its last rate hike today, we can only rely on the Bank of Japan (BoJ) to make a change. And well… I wouldn't place my bets on a hawkish BoJ even if the universe handed me a lucky horseshoe. The USDJPY is now above the 148 mark, and if the BoJ does or says nothing tomorrow, the pair could be propelled to 155. The only risk in a long USDJPY trade is a direct FX intervention from Japan. And that’s just turning the mill with carried water…

Fifty-fifty

Up until yesterday, the expectation was an almost certain 25bp hike from the BoE at today’s meeting, but yesterday’s shocker inflation data has shaken these expectations. In fact, no one, and even less the BoE Chief Bailey himself, was expecting to see softer inflation in Britain last month, when oil prices spiked and sterling fell. Therefore, the surprising nature of yesterday’s data release should prevent the BoE from announcing a surprise rate pause today. Because:

- Rising energy prices, and falling sterling hint at potentially higher inflation in the foreseeable future,

- At 6.2%, core inflation is still more than three times the BoE’s 2% inflation target.

In summary, the BoE is not there yet. And if sterling continues to fall – which is the most plausible outcome if the BoE softens its policy stance more than necessary today, inflation in Britain will become harder to contain. As a result, a - maybe - last 25bp rate hike is on today’s menu to limit losses in sterling so that energy costs wouldn’t spike as a result of a happy CPI report, that’s happiness would remain short-lived.

Speaking of energy, the barrel of US crude fell below the $90pb on Wednesday even though the US crude inventories fell more than 2-mio barrel last week, more than a 1.3-mio-barrel fall expected by analysts. This week’s retreat from above the $93pb is due to profit taking. The downside correction that could reasonably extend toward $86/87 range.