Sample Category Title

BoE Joins the ‘Done With Hikes’ Team

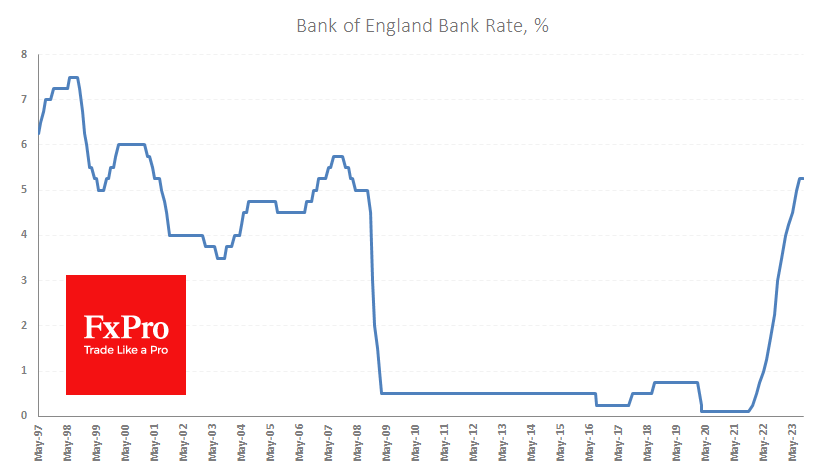

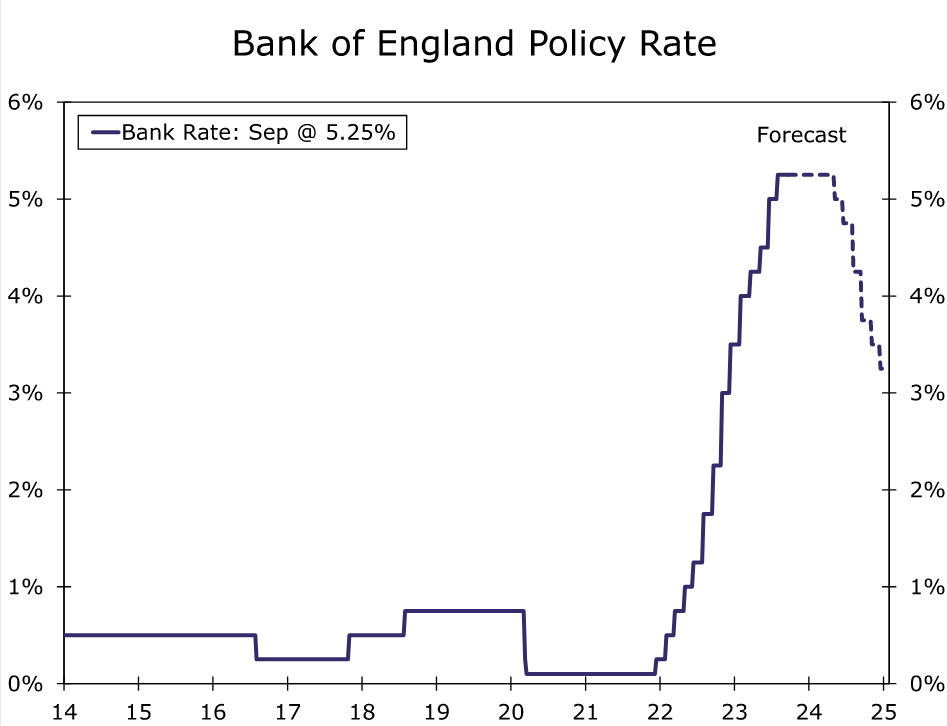

The Bank of England has left its key interest rate unchanged at 5.25%. The likelihood of such an outcome was actively priced into Pound quotes following yesterday’s UK inflation report.

The accompanying commentary noted the Bank of England’s worsening outlook for GDP growth and signs of deterioration in the labour market. In addition, the central bank expects inflation to slow significantly in the near term.

This is a much softer stance than we had expected, given the return of higher energy prices, the turnaround in producer prices and the still very high level of consumer inflation.

Today’s decision has raised expectations that the Bank of England has reached an interest rate ceiling. A similar scenario is now the main one for the Fed, the ECB and the SNB.

The Bank of England’s focus on the economy rather than inflation briefly sent GBPUSD to 1.2250, its lowest level since March, bringing the pair’s overall decline from its July peak to 6.8%.

The British Pound fell below its 200-day moving average this week, returning to a bearish trend. On the other hand, the pair has accumulated a short-term oversold condition over the past two months, which increases the chances of a corrective bounce in the coming days, paving the way for further declines.

Except for the US, September seems to be a turning point for the G7’s central banks. The Fed yesterday signalled the greatest willingness to raise rates soon and to keep them on hold for an extended period. In contrast, many opted to signal that they are comfortable with the current level of interest rates. This divergence is fuelling the strengthening of the US currency, albeit at a high cost to the US government, whose nominal debt servicing costs have risen to unprecedented levels.

WTI Oil Futures Turn Positive Again After Pullback from 10-month High

- Slide in oil doesn’t last long as bulls remain in control

- But further gains will depend on whether 50% Fibonacci can be overcome

WTI oil futures (cash) are heading higher on Thursday, reversing an earlier decline to a one-week low of 88.96. The price brushed a 45-week peak of 93.08 on Tuesday, extending the year-to-date gains to more than 15%.

The pullback was to be expected as both the RSI and stochastics had crossed into their respective overbought zones. The stochastics remain tilted downwards, heading towards the neutral level, but the RSI is attempting to re-enter the overbought region. This could be a sign that some further upside action is possible before a more sizeable correction is triggered.

That trigger could be the 50% Fibonacci retracement of the June 2022-May 2023 downtrend at 93.91. The significance of the 50% Fibonacci is underscored by the upper Bollinger band, which is flatlining just above it. A break above this crucial resistance area would green-light a sustained recovery in oil, clearing the path for the 61.8% Fibonacci of 101.04.

But should it succeed in capping gains, the price could retreat towards the 38.2% Fibonacci of 86.77, which corresponds with the 20-day simple moving average (SMA). The 50-day SMA lies not that much lower at 82.75, while further down, the 23.6% Fibonacci of 77.95 could next provide support as it did in August. However, a sharper selloff that pushes the price below the 200-day SMA in the 77.00 region would risk turning the bullish medium-term outlook to neutral.

Overall, this latest fall appears to have been only a minor setback for WTI oil futures and there’s not enough indication at this stage suggesting the uptrend is in danger. However, the 50% Fibonacci will be an important test, while a drop below the 20-day SMA would further weaken the short-term positive bias.

Bank of England Review: End to the Hiking Cycle, But Not GBP Headwinds

- The BoE today decided to keep the policy rate unchanged at 5.25% with forward guidance remaining broadly unchanged.

- We think that this marks the peak in the Bank Rate of 5.25%, although wage growth and service inflation remain a joker.

- We stay negative on GBP and continue to see relative rates as a moderate positive for EUR/GBP from here.

The Bank of England (BoE) decided to keep the the Bank Rate (key policy rate) unchanged at 5.25%. Five members voted for an unchanged decision while four members voted for an increase of 25bp. On gilt stock reduction, the BoE set a target of a reduction of GBP 100bn for the next 12 months (up from 80bn the past 12 months).

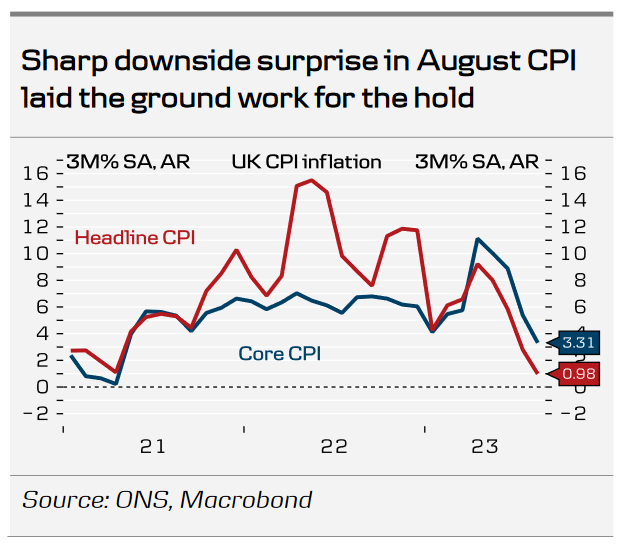

The majority of the Monetary Policy Committee (MPC) voted to keep the Bank Rate unchanged, citing the recent downside surprise to august inflation and further signs that the labour market was loosening. The BoE now expects GDP to rise only slightly in 2023 Q3 and underlying growth in the second half of 2023 also likely to be weaker than expected. Likewise, the BoE expects CPI inflation to "fall significantly further" while noting that service inflation is projected to remain elevated in the near-term. The BoE reiterated that "the current monetary policy stance is restrictive" and that "Monetary policy will need to be sufficiently restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term, in line with its remit". The BoE retained its forward guidance repeating that "further tightening in monetary policy would be required if there were evidence of more persistent inflationary pressures". While there is potential for a hike further out, only further amplified by the tight vote split, we do not believe that data will prove sufficiently strong for this to be the case. We expect the UK economy to show further signs of weakness, inflation to level off and a peak in private sector wage growth. Likewise, data releases are rather limited before the next meeting on 2 November, where we only get one job market report and inflation data for September.

Rates. Overall, the reaction in rates markets was relatively muted. Initially, rates markets rallied on the decision and statement and sent 2Y Gilt yields lower, but largely retraced the move during the afternoon. Markets are pricing in 10bp for the November meeting and a peak in the Bank Rate of 5.45%.

FX. EUR/GBP initially moved higher but partly retraced the move later on. On balance, we continue to see relative rates as a moderate positive for EUR/GBP, although GBP has been largely decoupled from moves in relative rates the past month. We expect the relative performance of the euro area and UK economy to be a driver, targeting a moderate rise in EUR/GBP to 0.88 the next year.

Our call. We expect the peak in the Bank Rate to have been reached. In order for BoE to opt for a 25bp instead of an unchanged decision at the next meeting we believe that we would have to see data releases, most notably wage growth and core inflation, prove considerably better than what we currently pencil in. Our call is less than current market pricing (20bp until March 2024). We still believe that the first rate cuts will not be delivered before Q2 2024.

Bank of England Pauses Monetary Tightening

Summary

- In what was a finely balanced decision, Bank of England (BoE) policymakers held their policy rate steady at 5.25% at today's monetary policy announcement. In a significant change, the BoE said there were mixed developments on indicators of inflation's persistence, noting slower varied signals on wage growth and slower services inflation.

- We believe today's interest rate pause could also represent an interest rate peak. The BoE said it views the current level of interest rates as restrictive, and that monetary policy would need to be sufficiently restrictive for sufficiently long to return inflation towards target.

- We do not anticipate an initial 25 bps rate cut until the May 2024 meeting, and see the BoE's policy rate ending next year at 3.25%. Today's decision also represents a loss of interest rate support for the pound. In that context, we view the risks as tilted towards further U.K. currency weakness through early 2024, and cannot rule out a move towards $1.2000 or below.

Bank of England Holds Rates Steady

In what was a finely balanced decision, Bank of England (BoE) policymakers held their policy rate steady at 5.25% at today's monetary policy announcement. BoE policymakers voted 5-4 to keep interest rates unchanged, with four policy committee members favoring a 25 bps increase. Separately, the BoE continued with its quantitative tightening, saying it would reduce the size of its balance sheet by £100 billion over the next 12 months.

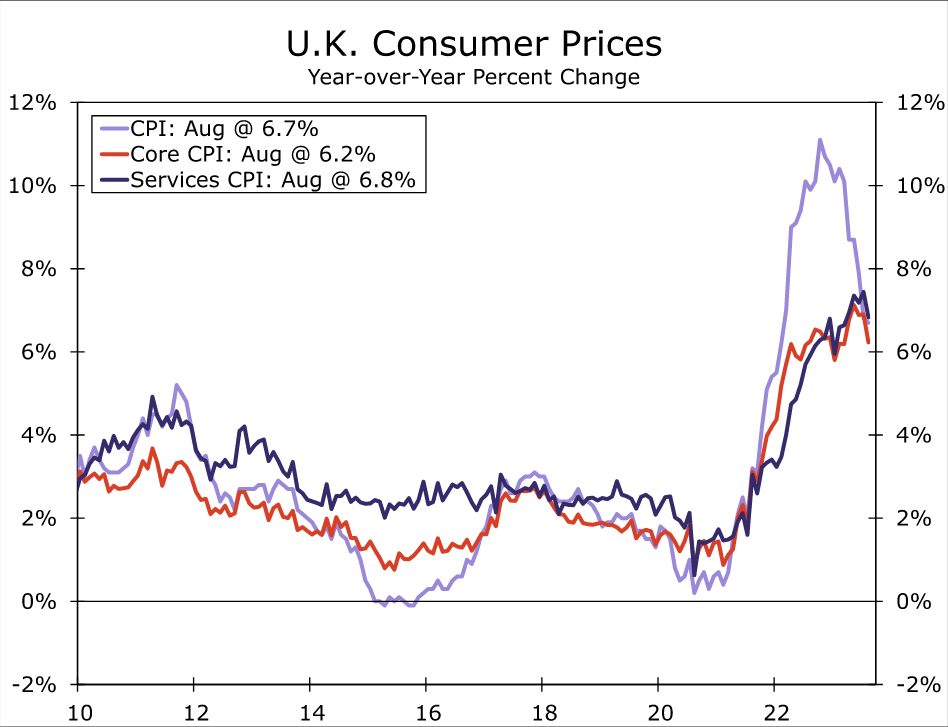

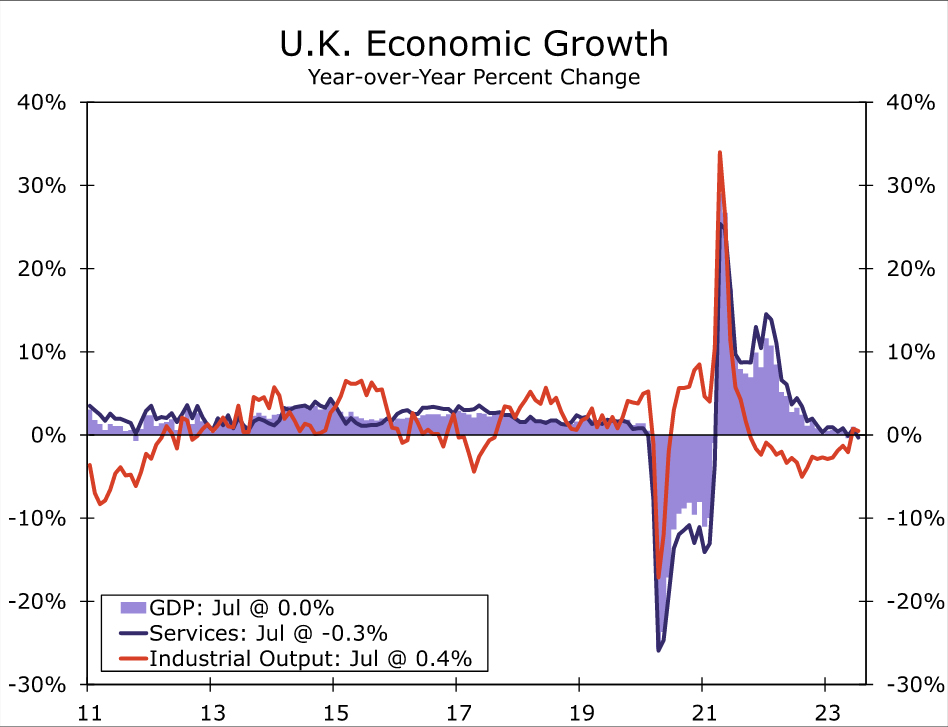

In holding interest rates steady, the Bank of England in a key change noted mixed developments on indicators of inflation's persistence. The central bank said the recent acceleration of average weekly earnings is not consistent or apparent in other wage measures, while also noting downside news on services inflation, which slowed to 6.8% year-over-year in August. Separately, the Bank of England also said core goods inflation is much weaker than had been expected. Finally, the Bank of England also said there are increasing signs of some impact of tighter monetary policy on the labor market and on momentum in the real economy more generally. On that front, we note that July GDP fell 0.5% month-over-month, while the unemployment rate rose to 4.3% in the three months to July.

Policy Rate Pause Could Also Be A Policy Rate Peak

In our opinion, there are also indications that today's policy rate pause could be a policy rate peak. The BoE said "given the significant increase in Bank Rate since the start of this tightening cycle, the current monetary policy stance is restrictive”, while adding that “monetary policy will need to be sufficiently restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term.” We view that language as consistent with the Bank of England keeping rates at the current level for an extended period. The central bank did leave the door open to further rate hikes, saying a further tightening in monetary policy would be required if there were to be evidence of more persistent inflation pressures. However, given the weakening in the economy to date and the mild U.K. recession we forecast, along with the more significant deceleration of inflation that now appears to be underway, we believe such rates hikes are unlikely to eventuate.

As a result, we now forecast that the current policy rate of 5.25% will be the peak for this cycle. We do expect rates to remain at that level for some time and, following a mild recession beginning from late this year and as CPI inflation moves closer the 2% target, forecast an initial modest 25 bps rate reduction only by the time of the May 2024 policy meeting. We expect the pace of rate cuts to gather momentum through the rest of next year, and see the Bank of England policy rate to end next year at 3.25%. From a currency perspective, today's decision to pause and the probable end to policy tightening represents a loss of interest rate support. As a result and even though the GBP/USD exchange rate has already moved below our medium-term target of $1.2300, we think the risks remain tilted toward further sterling weakness through early 2024. In that context, a move to $1.2000 or below cannot be ruled out.

Sunset Market Commentary

Markets

A slew of central bank meetings kept markets busy all day. From the Turkish central bank (+500 bps to 30%) over the Riksbank & the Norges Bank (+25 bps to 4% and 4.25%) to the Swiss national bank and the Bank of England (status quo). A summary for most of them can be found below while we discuss the BoE here. The central bank’s decision to leave rates unchanged at 5.25% was a close 5-4 call. Inflation, though still too high, dropped more than expected with the central bank specifically pointing to services inflation finally easing. The labour market, meanwhile is showing early signs of easing (eg. lower employment rates and higher unemployment rates) and economic growth is expected to be lower following disappointing PMI’s and several other business indicators. Market pricing going into the meeting (about 50-50) suggests there was an equally solid case to be made for another hike. But the ECB’s and Fed’s pause probably (though not officially) helped to tilt the balance in favour of a hold. The BoE retains the possibility of further hikes should inflation prove more persistence but we think the bar is high. Governor Bailey’s appearance before parliament two weeks ago once again made that clear. The pound slips. EUR/GBP is testing 0.8678 resistance. Cable (GBP/USD) loses 1.2308 support (May low) to trade at 1.2262, the lowest since mid-March. UK yields in a kneejerk reaction dropped before quickly paring losses again. Current changes vary between 7.5-12.4 bps with the belly underperforming.

Core bonds are spared no respite after yesterday’s hawkish Fed meeting. And if it weren’t enough, once again bumper US jobless claims (201k vs 225k) just came in today. US yields extend gains with changes varying from -1.7 bps (2-y, after briefly hitting new cycle high) to +8 bps (30-y). German yields rally 4-5.9 bps. The 10-y yield is testing the previous cycle high at 2.77% in a move largely driven by real yields. The one in the US meanwhile moves further north of the 2% barrier to the highest since 2008. The dollar gets another push in the back, including from a dire risk environment (stocks down 1.4% in Europe, 1% on WS). EUR/USD temporarily lost 1.0635 support and went for 1.0611 before paring losses. DXY gapped above 105.38 resistance at the open trade at 105.57 currently. USD/JPY is the exception to the rule (147.9) with the yen banking on its safe haven status going into tomorrow’s BoJ meeting.

News & Views

The Swiss National Bank (SNB) unexpectedly left its policy rate at 1.75%. A wide majority of analysts expected an increase to 2%. Governor Jordan said that the battle on inflation isn’t over yet, but the SNB is able to wait for the December review to see whether previous tightening was sufficient to keep inflation within 0-2% on a sustainable basis. Further tightening remains possible. Inflation in Switzerland in August eased to 1.6% Y/Y. The SNB expects 2.0% at the end of this year and an average of 2.2% next year before returning to 1.9% in 2025. The lower inflation trajectory compared to June is due to lower economic growth and slightly lower inflationary pressure from abroad. For the second half of this year, SNB expects annual growth of about 1.0% for 2023. The SNB remains prepared to sell foreign currency if needed. However, given recent CHF-strength, that’s probably not the case right now. EUR/CHF initially rallied from 0.957 to 0.9675, but the franc gradually recouped part of the loss (currently 0.963).

The Norges Bank and the Swedish Riksbank raised policy rates by 25 bps to respectively 4.25% and 4.0%. Swedish inflation is falling, for an important part due to lower energy prices. Still CPIF inflation at 4.7% is still too high and well above the 2% target. Core inflation excluding energy even stands at 7.2%. The RB sees CPIF and core inflation in 2024 respectively at 2.5% and 2.9% and at 1.8% and 2.1% in 2025. Growth for this year was downward revised to -0.8% (from -0.5%) and to -0.1% in 2024. The (“unjustifiable”) weak krone adds to inflationary risks. The policy rate can therefore still be raised further. The krone briefly gained after the decision, but with the Fed reinforcing its higher for longer mantra, the krone (EUR/SEK 11.96) again nears its all-time low against the euro. The Norwegian central bank acknowledges that inflation stays markedly above the 2.0% target. Headline inflation in August eased more than expected to 4.8% Y/Y but underlying inflation still was 6.3%. In its new projections the NB expects underlying inflation well above target through 2026. Growth is seen slowing to 0.4% next year. Despite this, the NB sees the policy rate being raised further to about 4.5% to stay there throughout 2024. The krone since June strengthened modestly from about EUR/NOK 12+ to currently trade near 11.52. A rebound attempt after the NB rate hike failed.

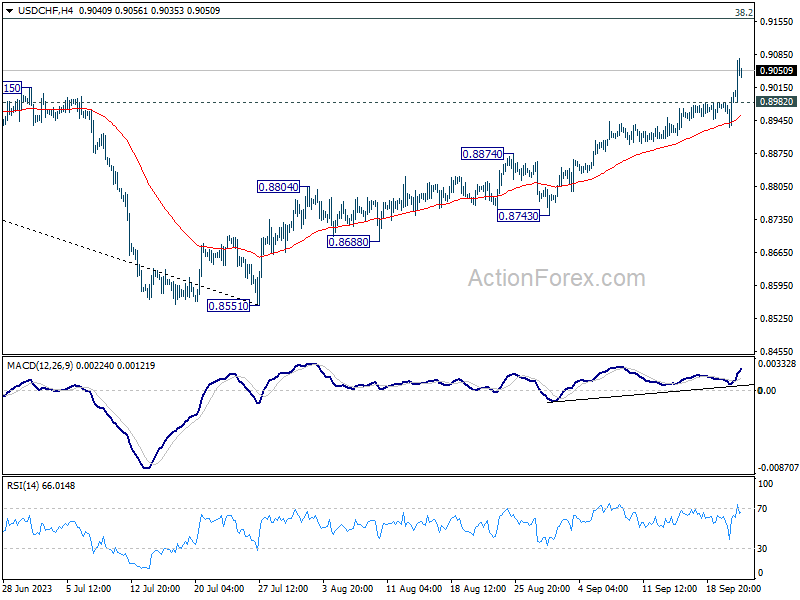

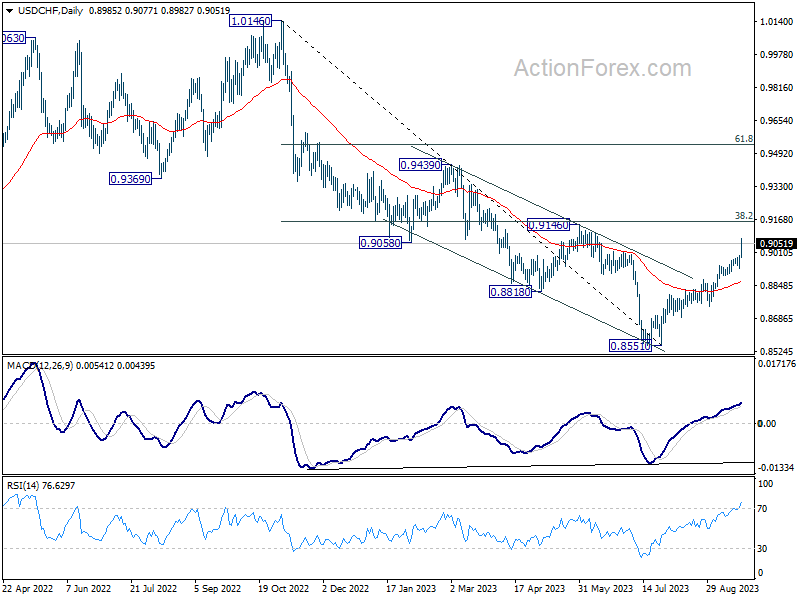

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8947; (P) 0.8972; (R1) 0.9011; More....

USD/CHF's accelerates to as high as 0.9077 so far today. Intraday bias stays on the upside and current rise from 0.8551 should target 0.9146 cluster resistance. On the downside, break of 0.8982 minor support will turn intraday bias neutral first. But further rally will remain in favor as long as 0.8874 resistance turned support holds, in case of retreat.

In the bigger picture, rebound from 0.8551 medium term bottom is currently seen as a correction to the downtrend from 1.0146 (2022 high). Further rally would be seen to 0.9146 cluster resistance (38.2% retracement of 1.0146 to 0.8551 at 0.9160). Strong resistance could be seen there to limit upside, at least on first attempt.

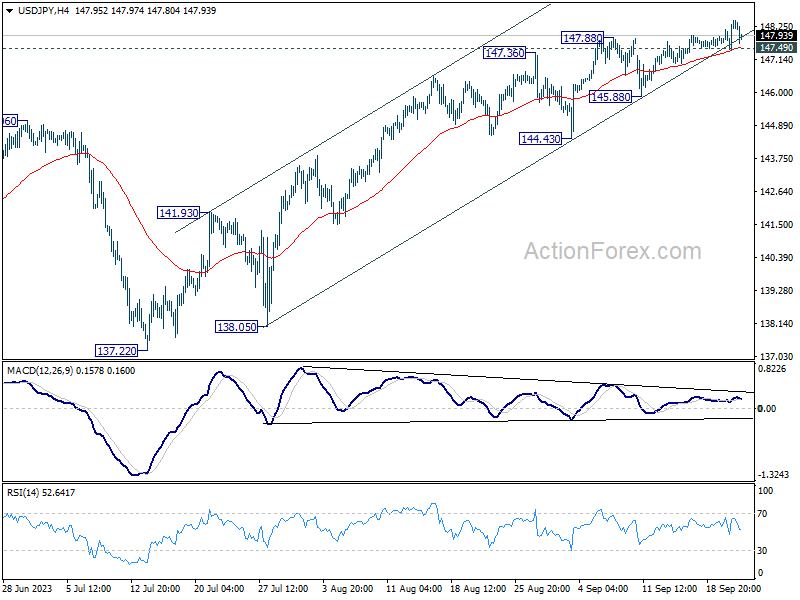

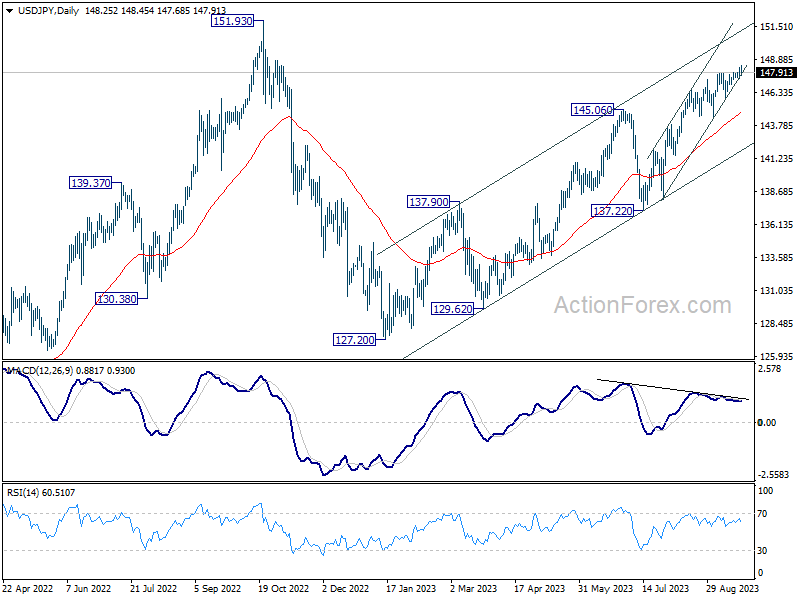

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.76; (P) 148.06; (R1) 148.65; More...

Further rise is mildly in favor in USD/JPY as long as 147.49 minor support intact. Current rally would target 151.93 high. However, break of 147.49 will argue that a short term top is already formed. intraday bias will be turned to the downside for 145.88 support instead.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by break of 137.22 support will indicate that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

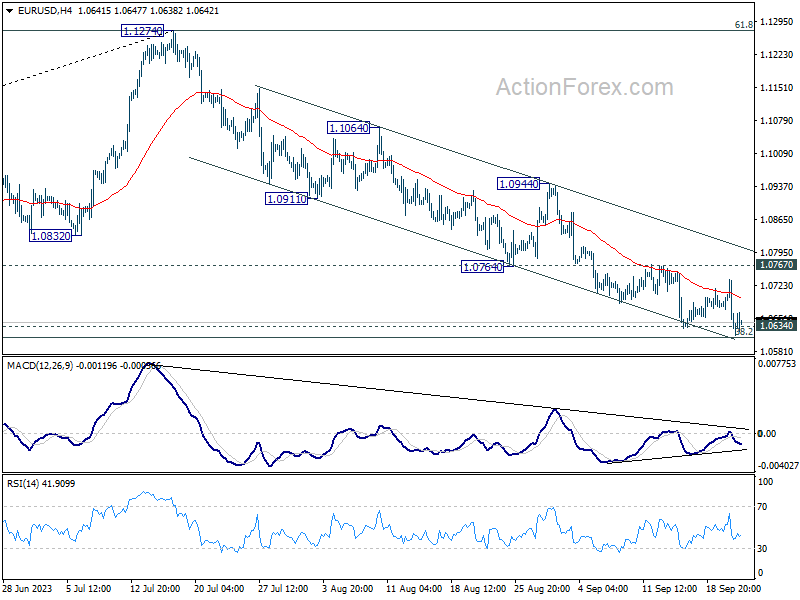

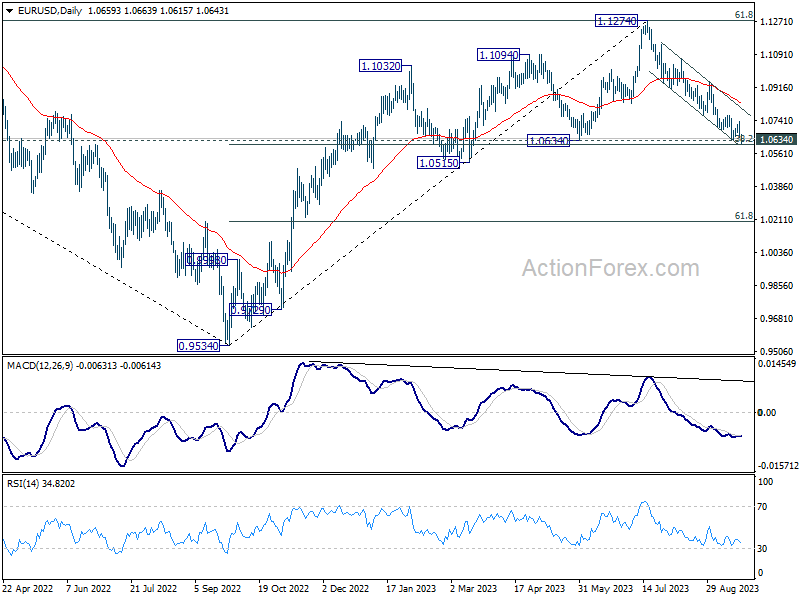

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0628; (P) 1.0683; (R1) 1.0715; More...

Intraday bias in EUR/USD remains on the downside for the moment. Sustained break of 1.0609/34 support zone will carry larger bearish implication. Fall from 1.1274 should then target target 1.0515 support next. Nevertheless, strong strong rebound from current level, followed by break of 1.0767 resistance, should confirm short term bottoming. Intraday bias will be back on the upside for 1.0944 resistance.

In the bigger picture, fall from 1.1274 medium term top is seen as a correction to up trend from 0.9534 (2022 low). Strong support could be seen from 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609) to bring rebound, at least on first attempt. However, sustained break of 1.0609/0634 will raise the chance of bearish trend reversal, and target 61.8% retracement at 1.0199.

Swiss Sinks on SNB Surprise, Fed Pauses

- SNB surprises and holds interest rates

- Fed delivers a ‘hawkish hold’

The Swiss franc has fallen sharply on Thursday. In the European session, USD/CHF is trading at 0.9060, up 0.80%. Earlier, USD/CHF hit a high of 0.9078, its highest level since June 13th.

The driver behind the Swiss franc’s downturn was the Swiss National Bank’s decision to hold rates at 1.75%, after five consecutive rate hikes. This surprised the markets which had expected a quarter-point increase. The SNB policy assessment noted that significant tightening had curbed inflation, but that further tightening could not be ruled out.

Have interest rates peaked in Switzerland? The answer appears to be yes, unless inflation rises unexpectedly. Inflation was unchanged in August at 1.6%, within the SNB’s target of 0%-2%. The assessment noted that Swiss growth has been weak and there is a risk that the global economic slowdown will worsen.

The assessment also noted the SNB is “willing to be active in the foreign exchange market as necessary”. The SNB hasn’t been shy about intervention in order to stabilize the exchange rate, which has helped to control external inflationary pressures. At the same time, the central bank doesn’t want the Swiss franc to appreciate to such an extent that it weighs on the crucial export sector.

Fed holds rates as expected

The Federal Reserve paused rates for the second time in three months, maintaining the benchmark rate at 5.5%. The decision was a ‘hawkish pause’, as the Fed signaled that it would hold rates higher for longer.

The dot plot indicated that the Fed expects to raise rates once more before the end of the year and is projecting trimming rates by 50 basis points in 2024. In June, the dot plot indicated one more hike before the year’s end and rate cuts of 100 basis points. The Fed also revised its growth forecast for 2023 to 2.1%, up from 1% in June, indicating that the Fed is confident it can guide the economy to a soft landing and avoid a recession.

USD/CHF Technical

- USD/CHF pushed above resistance at 0.9033 and is putting pressure on resistance at 0.9087

- 0.8985 and 0.8910 are providing support