Sample Category Title

Franc Weakens as SNB’s Logical Move Surprises Markets

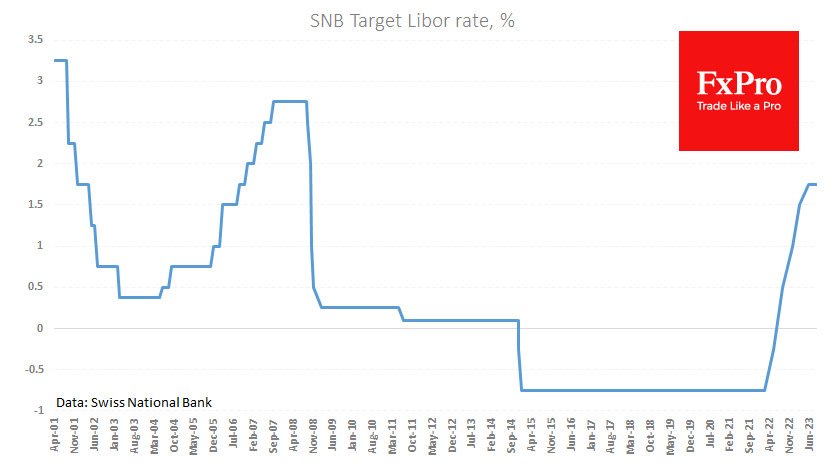

The Swiss National Bank left its key interest rate unchanged at 1.75%. On average, markets had been predicting a 25-basis point hike, contrary to our expectations.

Most likely, market participants’ forecasts were influenced by the ECB rate hike a week earlier. In addition, policy tightening expected in Sweden and Norway indeed took place. But there are a couple of things that set Switzerland apart from other European countries.

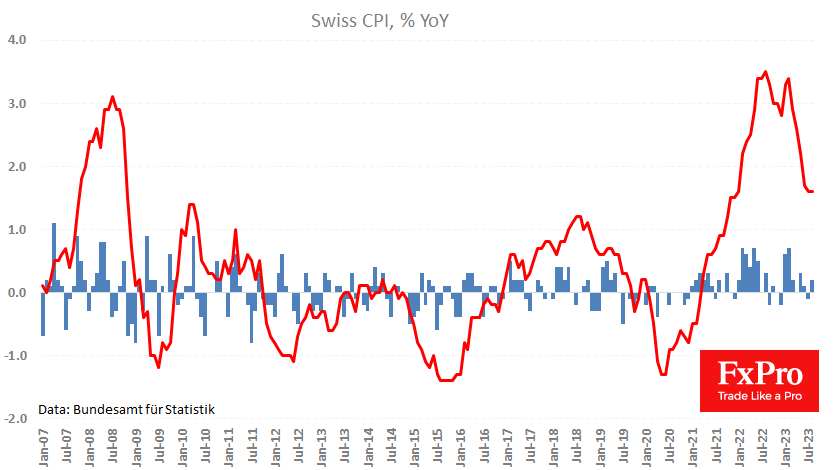

First is inflation. The annual rate of price increases has been below 2% for the past three months, and this is not a high-base effect. Monthly price increases have averaged 0.09% over the past six months and half that over the past three months, bringing annual inflation to 1.1% and 0.55%, respectively.

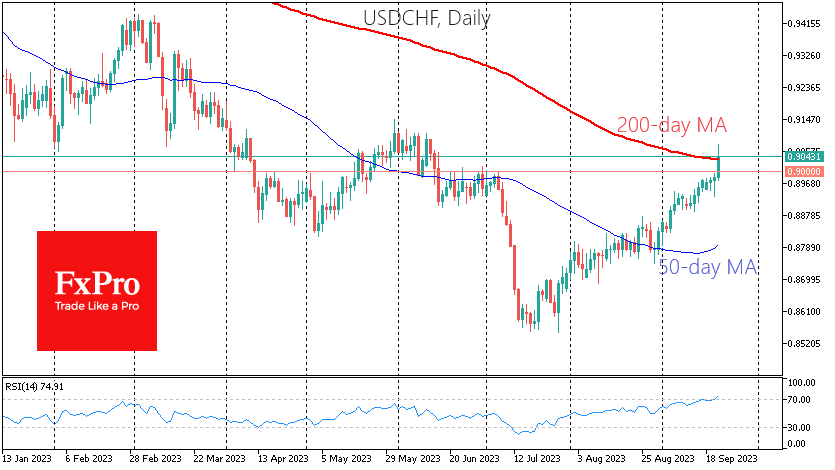

Second is the Swiss franc exchange rate. In July, the USDCHF fell to 0.8550. It was briefly lower in 2015 and from May to September 2011. By comparison, the yen – another example of a safe haven – is testing multi-month lows. Neither the euro nor the pound can boast high levels relative to historical prospects.

The Swiss franc lost 1.5% against the dollar in response to the Fed’s hawkish pause and a “surprise” from the SNB. The USDCHF pair has risen above 0.9050, its highest level in over three months, after moving slowly but smoothly upwards for the past two months.

If the pair holds these levels for the rest of the day, or even better, for the rest of the week, we will have signalled a change in the long-term trend, as the USDCHF has crossed the 200-day moving average.

However, we should expect a severe fight at current levels as the pair looks overbought. The pair’s upward momentum on Thursday could be the last mile before broad profit-taking begins on the previous gains.

The Franc has likely run out of fuel for further declines. A corrective pullback to 0.9850-0.9000 may be needed to make selling the Franc attractive again in the medium term. On the bearish side, risk aversion in global markets could return in the coming days if it leads to deleveraging.

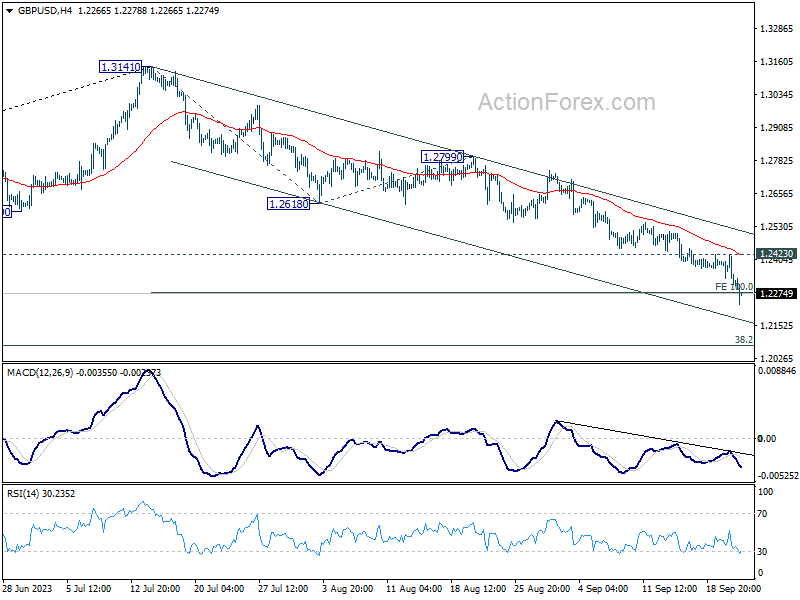

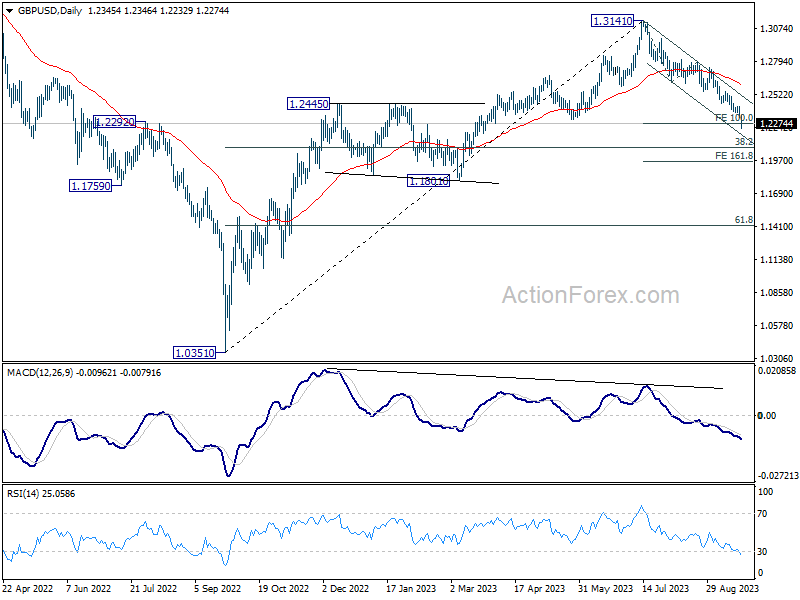

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2310; (P) 1.2366; (R1) 1.2399; More...

GBP/USD falls to as low as 1.2232 so far today and intraday bias stays on the downside. 100% projection of 1.3141 to 1.2618 from 1.2799 at 1.2276 is already met but there is no sign of bottoming. next target would be 1.2075 fibonacci level. On the upside, above 1.2423 minor resistance will turn intraday bias neutral again. But near term outlook will stay bearish as long as 1.2618 support turned resistance holds, in case of strong recovery.

In the bigger picture, fall from 1.3141 medium term top is seen as a correction to up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3141 at 1.2075. Strong support would be seen there to bring rebound on first attempt. However, sustained break of 1.2075 will raise the chance of bearish trend reversal.

Sterling and Franc Stumble on BoE and SNB; Yen Rises ahead BoJ

The currency markets faced significant shifts today, notably with Sterling and Swiss Franc, which are enduring considerable selloffs. Both BoE and SNB opted to maintain their current interest rates, prompting speculation that these institutions might have peaked in their tightening cycles. However, Australian Dollar bore the brunt of today's market sentiment, emerging as the day's biggest loser, possibly due to escalating risk aversion. This sentiment has been echoed in major global indexes, most likely influenced by Fed hawkish hold yesterday coupled which also triggered soaring treasury yields.

On the flip side, Japanese Yen is shining as the day's top performer. This strength is, in part, attributed to 10-year JGB yield surpassing 0.75% mark. Market participants are also possibly adjusting their positions in anticipation of a potentially hawkish surprise from BoJ in the upcoming Asian trading session. Following closely,Dollar maintains its robust position, though USD/JPY pair continues to show signs of strain ahead of 150 mark. Euro is also gaining a bit traction, but only benefiting from trades against the beleaguered Swiss Franc and Sterling. Meanwhile, Canadian Dollar's performance is mixed, retracting much of the gains driven by this week's CPI data.

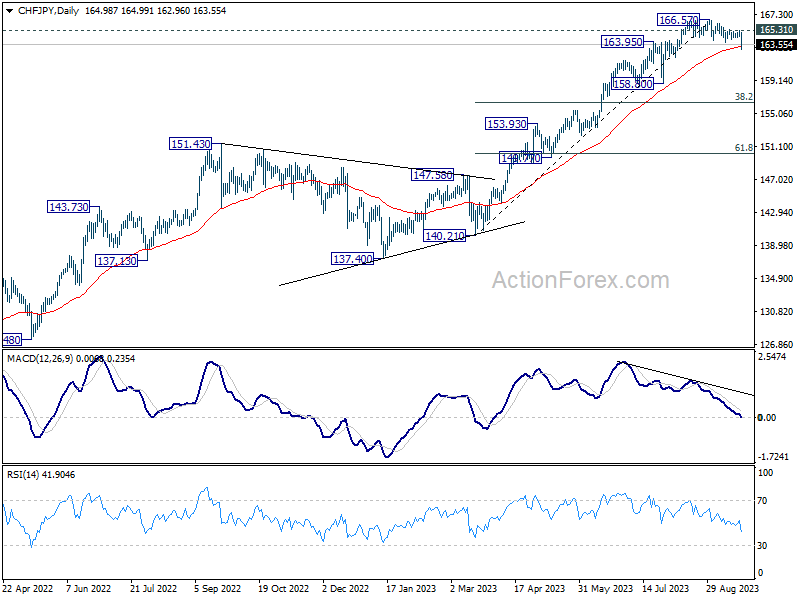

Technically, CHF/JPY's fall from 166.57 resumes today on broad-based Swiss Franc weakness. Considering bearish divergence condition in D MACD, this decline is probably corrective whole rise from 140.21. Sustained trading below 55 D EMA (now at 163.27) will add more credence to this case. Deeper fall should then be seen to 158.80 support, or possibly further to 38.2% retracement of 150.21 to 166.57 at 156.50.

In Europe, at the time of writing, FTSE is down -0.43%. DAX is down -1.39%. CAC is down -1.72%. Germany 10-year yield is up 0.0658 at 2.771. Earlier in Asia, Nikkei fell -1.37%. Hong Kong HSI fell -1.29%. China Shanghai SSE fell -0.77%. Singapore Strait Times fell -1.21%. Japan 10-year JGB yield rose 0.0285 to 0.754.

In Europe, at the time of writing, FTSE is down -0.43%. DAX is down -1.39%. CAC is down -1.72%. Germany 10-year yield is up 0.0658 at 2.771. Earlier in Asia, Nikkei fell -1.37%. Hong Kong HSI fell -1.29%. China Shanghai SSE fell -0.77%. Singapore Strait Times fell -1.21%. Japan 10-year JGB yield rose 0.0285 to 0.754.

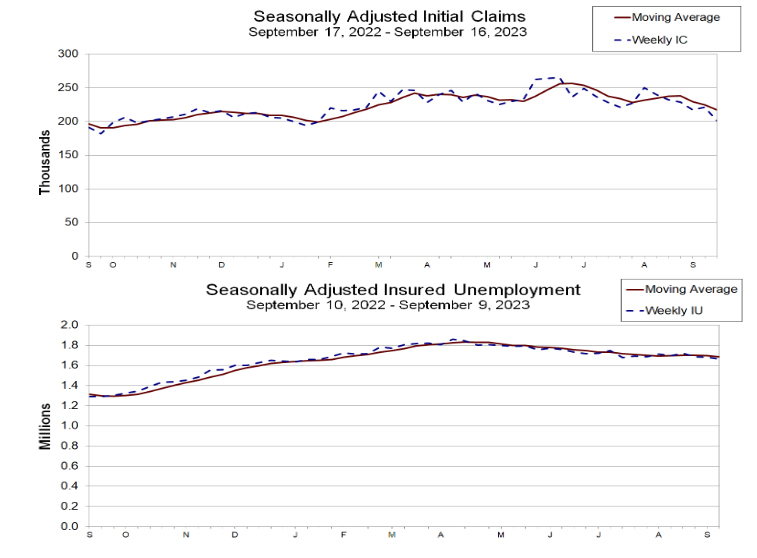

US initial jobless claims drop to 201k, vs exp 222k

US initial jobless claims fell -20k to 201k in the week ending September 16, well below expectation of 222k. Four-week moving average of initial claims dropped -8k to 217k. Continuing claims fell -21k to 1662 in the week ending September 9. Four-week moving average of continuing claims fell-9k to 1687k.

BoE on hold at 5.25%, heavyweights win tight vote

BoE opts to keep its Bank Rate unchanged at 5.25%. The decision, however, came after a razor-thin 5-4 vote that showed divisions within the central bank's ranks. Notably, the influential figures - Governor Andrew Bailey, Deputies Ben Broadbent and Dave Ramsden, along with Chief Economist Huw Pill, sided with Swait Dhingra in favour of retaining the rate at its current level.

In its accompanying statement, BoE underscored the need for a vigilant approach, stating, "Monetary policy will need to be sufficiently restrictive for sufficiently long". Furthermore, the central bank emphasized its readiness to consider more rate hikes, signaling that "Further tightening in monetary policy would be required if there were evidence of more persistent inflationary pressures."

Amid these cautions, Bank's staff adjusted their growth outlook, expecting only a slight uptick in GDP for the third quarter of 2023. They also anticipate that the underlying growth for the second half of the year will likely underperform previous expectations.

On the inflation front, the bank projected a notable decline in CPI in the near future. Despite recent spikes in oil prices, the central bank expects this drop due to "lower annual energy inflation" and anticipated further reductions in food and core goods prices.

Yet, the BoE warned that the services sector could buck this trend, foreseeing that "Services price inflation, however, is projected to remain elevated in the near term, with some potential month-to-month volatility."

Also, in a unanimous decision, the MPC agreed to reduce the stockpile of UK government bond purchases, cutting it down by GBP 100B over the coming year, bringing the total to GBP 658B.

SNB bucks expectations and keeps interest rate steady

In an unexpected move that diverged from the market's anticipations, SNB held its policy rate steady at 1.75%, side-stepping the anticipated hike to 2.00%. The conditional inflation projections have undergone downward revision. While inflation could surge above 2% target in upcoming quarters, it's projected to retract back to 1.9% in 2025 based on current interest rate, without further tightening.

Despite this, SNB did not completely distance itself from a hawkish tone, and maintained the further tightening "may become necessary". It also reiterated the willingness to intervene in the market with focus on "selling foreign currency

Delving into the specifics of the conditional inflation projections, based on steady 1.75% policy rate, inflation is forecasted to ascend to 2.0% by the end of this year. It will scale up to its apex at 2.2% in the second quarter of 2024, before experiencing a slight dip to 1.9% at the onset of 2025, maintaining that level thereafter.

On the economic growth front, SNB's projections lean towards the cautious side, forecasting tepid growth for the remainder of the year. The annual growth is projected to hover around a modest 1%.

ECB's Nagel uncertain if rate plateau is reached

ECB Governing Council, Joachim Nagel, Bundesbank head, posed a crucial question in his speech in Frankfurt, "Have we reached the plateau" on interest rates? He answered by stating that it "cannot yet be clearly predicted". He continued, elaborating that "the forecasts still only show a slow decline toward the target level of 2%."

Nagel's comments hinted at the continuous monitoring of economic indicators, suggesting that while borrowing costs are expected to "remain at a sufficiently high level for a sufficiently long time," the exact interpretation hinges on the incoming data.

Addressing concerns about Germany's economic health, he remarked that characterizing Germany as the 'sick man' "seems exaggerated." He attributed the present sluggish growth to specific influences such as the global economic deceleration, Russia's conflict with Ukraine, and reduced public expenditure. Offering a silver lining, Nagel projected, "Once we get past the worst of these special factors, the weak growth should also ease. We expect the economy to grow again in 2024."

On the other hand, Latvia's central bank chief, Martins Kazaks, highlighted the structural nature of recent oil price hikes. He pointed out, "The recent oil price increase in my view is not a temporary or transitory, it's very much a structural issue." Such dynamics, according to Kazaks, present heightened inflation risks. Regarding the anticipated rate cuts, he expressed skepticism about their timing, asserting, "I think expecting rate cuts mid next year is somewhat too early."

New Zealand's Q2 GDP outperforms expectations with 0.9% qoq growth

New Zealand's GDP surged by 0.90% qoq in Q2, doubling the expected growth rate of 0.4%. This notable growth is significantly attributed to substantial boost in the business services sector, specifically within the realm of computer system design.

Despite a setback in the primary industries, which contracted by 1.9%, goods-producing industries and service sectors pulled their weight, recording a growth of 0.7% and 1.0% respectively. The service sector emerged as a strong pillar of economic advancement.

The quarter also saw manufacturing sector shake off its lethargy, reversing a trend of decline sustained over five consecutive quarters to contribute positively to the economic pie.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2310; (P) 1.2366; (R1) 1.2399; More...

GBP/USD falls to as low as 1.2232 so far today and intraday bias stays on the downside. 100% projection of 1.3141 to 1.2618 from 1.2799 at 1.2276 is already met but there is no sign of bottoming. next target would be 1.2075 fibonacci level. On the upside, above 1.2423 minor resistance will turn intraday bias neutral again. But near term outlook will stay bearish as long as 1.2618 support turned resistance holds, in case of strong recovery.

In the bigger picture, fall from 1.3141 medium term top is seen as a correction to up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3141 at 1.2075. Strong support would be seen there to bring rebound on first attempt. However, sustained break of 1.2075 will raise the chance of bearish trend reversal.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | GDP Q/Q Q2 | 0.90% | 0.40% | -0.10% | 0.00% |

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Aug | 10.8B | 9.8B | 3.5B | |

| 07:30 | CHF | SNB Interest Rate Decision | 1.75% | 2.00% | 1.75% | |

| 11:00 | GBP | BoE Interest Rate Decision | 5.25% | 5.50% | 5.25% | |

| 11:00 | GBP | MPC Official Bank Rate Votes | 4--0--5 | 8--0--1 | 8--0--1 | |

| 12:30 | CAD | New Housing Price Index M/M Aug | 0.10% | 0.00% | -0.10% | |

| 12:30 | USD | Initial Jobless Claims (Sep 15) | 201K | 222K | 220K | 221k |

| 12:30 | USD | Philadelphia Fed Survey Sep | -13.5 | -0.7 | 12 | |

| 12:30 | USD | Current Account (USD) Q2 | -212B | -220B | -219B | |

| 14:00 | USD | Existing Home Sales Aug | 4.10M | 4.07M | ||

| 14:00 | EUR | Eurozone Consumer Confidence Sep P | -16.5 | -16 | ||

| 14:30 | USD | Natural Gas Storage | 65B | 57B |

US initial jobless claims drop to 201k, vs exp 222k

US initial jobless claims fell -20k to 201k in the week ending September 16, well below expectation of 222k. Four-week moving average of initial claims dropped -8k to 217k.

Continuing claims fell -21k to 1662 in the week ending September 9. Four-week moving average of continuing claims fell-9k to 1687k.

A Surprisingly Dovish BoE But Another Rate Hike Still Possible

We're certainly seeing plenty of different approaches from central banks as they wrap up their tightening cycles, with the Bank of England today surprising with a hold while not adopting a particularly hawkish tone alongside it.

That said, more important than the tone is just how close the vote was, with five policymakers - including Governor Bailey - voting to hold and four others backing a hike. That arguably puts this in into hawkish hold territory but what is interesting is the wide range of views within the committee that comes across in the statement.

I expect we'll see a similarly tight vote at the next meeting, the outcome of which will be even more heavily driven by the data as there's clearly no overriding consensus on the committee.

Two things that particularly stood out in the statement were the view that inflation has fallen a lot and is expected to continue to do so, and the choice of words with respect to how long rates will stay high - "sufficiently restrictive for sufficiently long". While you could argue it's just a bit cryptic, it's far from the message that rates will stay higher for longer that we're getting from the Fed, ECB, and others. I suspect a number of policymakers see the potential for rate cuts earlier in 2024 if data performs as expected.

An attempted hawkish hold from the SNB but markets not buying it

The SNB refrained from raising interest rates earlier today, instead signaling that sufficient tightening has taken place in order to get inflation back to below 2% over the forecast horizon. While inflation is already well below 2%, there was an expectation that the central bank would hike again and in effect mirror the actions of the ECB before calling it a day.

The decision did see the Swiss franc weaken against the euro, as you'd expect, despite Chair Jordan's attempts to strike a hawkish tone in warning rates could still rise again if they deemed it necessary. That seems very unlikely now though, instead, it will soon become a question of when we can expect rate cuts rather than hikes.

Profit-taking continues in Oil after the Fed's hawkish hold

Oil prices are trending lower for a third day, with the Fed's hawkish hold on Wednesday seemingly compounding fears that appeared to build in the run-up to the decision. The central bank was always likely to position itself as hawkish but perhaps the dot plot was more so than many anticipated.

And ultimately, while the US economy showing resilience may be viewed as a positive in the short term as it supports demand, if that then prompts the Fed to tighten further and hold rates higher for longer, it risks tipping the economy over the edge and into recession. And it seems it's those fears that are now weighing on crude prices after such a powerful rally over the last four weeks.

I'm not convinced that will be enough to trigger a significant reversal in crude prices, but rather provide an excuse for some profit-taking after such a huge rally. The fact remains that the market is tight and running a large deficit. Until that changes, prices could remain elevated, and talk of $100 Brent won't go away.

Gold pares gains but are traders convinced by Fed forecasts?

The Fed's hawkish hold didn't prove too popular with gold bulls either despite some apparent optimism ahead of the release. Gold rallied toward $1,950 in the run-up to the decision, in line with the highs from earlier this month, before giving all of the day's pre-release gains back and ending it in the red.

It's trading a little lower once more and, depending on how seriously traders are taking the Fed's dot plot, could be at risk of testing last week's lows around $1,900. Ultimately, until we get more data, that's what it all comes down to. Will traders accept the forecasts or do they view them as a hawkish move to manage expectations, the latter of which could continue to support the yellow metal until we have more data.

Bitcoin edges lower but there are bigger things to focus on

Bitcoin is trending a little lower, roughly aligned with how other risk assets have performed in the aftermath of the Fed decision. Broadly speaking though not a lot has changed for bitcoin recently. There's been some bursts of volatility but price-wise, it's just fluctuating primarily between $25,000 and $27,500. Perhaps it's simply a case of traders awaiting more ETF news, or other catalysts within the space, as the post-Fed move wasn't particularly significant.

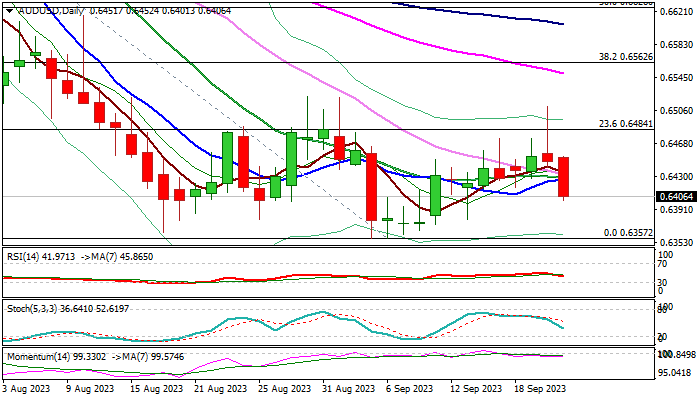

AUD/USD: Aussie Dollar Falls On Post-Fed Risk Aversion

AUDUSD was down 0.7% in Asian/European trading on Thursday, extending post-Fed drop (falling in total 1.6% since FOMC announcement).

Fed’s hawkish hold, in which the central bank kept interest rates unchanged but signaled one more hike until the end of the year and likelihood of keeping high interest rates through 2024, sparked fresh risk aversion, prompting traders into dollar.

Technical structure on daily chart is weakening, following Wednesday’s strong upside rejection and formation of bull-trap pattern, as fresh acceleration lower already retraced over 61.8% of the recent 0.6357/0.6511 bull-leg).

Daily moving averages returned to bearish setup and 14-d momentum is heading deeper into negative territory, contributing to negative near-term signals.

Daily close below broken10DMA (0.6426) is needed to keep bears intact for renewed attack at near-term base at 0.6360 zone (2023 lows), violation of which would signal an end of a multi-week congestion and continuation of larger downtrend from 0.6894 (July 14 high).

Res: 0.6426; 0.6452; 0.6484; 0.6511.

Sup: 0.6380; 0.6357; 0.6272; 0.6210.

BoE on hold at 5.25%, heavyweights win tight vote

BoE opts to keep its Bank Rate unchanged at 5.25%. The decision, however, came after a razor-thin 5-4 vote that showed divisions within the central bank's ranks. Notably, the influential figures - Governor Andrew Bailey, Deputies Ben Broadbent and Dave Ramsden, along with Chief Economist Huw Pill, sided with Swait Dhingra in favour of retaining the rate at its current level.

In its accompanying statement, BoE underscored the need for a vigilant approach, stating, "Monetary policy will need to be sufficiently restrictive for sufficiently long". Furthermore, the central bank emphasized its readiness to consider more rate hikes, signaling that "Further tightening in monetary policy would be required if there were evidence of more persistent inflationary pressures."

Amid these cautions, Bank's staff adjusted their growth outlook, expecting only a slight uptick in GDP for the third quarter of 2023. They also anticipate that the underlying growth for the second half of the year will likely underperform previous expectations.

On the inflation front, the bank projected a notable decline in CPI in the near future. Despite recent spikes in oil prices, the central bank expects this drop due to "lower annual energy inflation" and anticipated further reductions in food and core goods prices.

Yet, the BoE warned that the services sector could buck this trend, foreseeing that "Services price inflation, however, is projected to remain elevated in the near term, with some potential month-to-month volatility."

Also, in a unanimous decision, the MPC agreed to reduce the stockpile of UK government bond purchases, cutting it down by GBP 100B over the coming year, bringing the total to GBP 658B.

(BOE) Bank rate maintained at 5.25%

Monetary Policy Summary, September 2023

The Bank of England's Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. At its meeting ending on 20 September 2023, the MPC voted by a majority of 5–4 to maintain Bank Rate at 5.25%. Four members preferred to increase Bank Rate by 0.25 percentage points, to 5.5%. The Committee also voted unanimously to reduce the stock of UK government bond purchases held for monetary policy purposes, and financed by the issuance of central bank reserves, by £100 billion over the next twelve months, to a total of £658 billion.

In the MPC's August most likely, or modal, Monetary Policy Report projections, conditioned on a market-implied path for Bank Rate that averaged just under 5½% over the three-year forecast period, CPI inflation was expected to return to the 2% target by 2025 Q2. It was then projected to fall below the target in the medium term, as an increasing degree of economic slack was expected to reduce domestic inflationary pressures, alongside declining external cost pressures. The Committee had continued to judge that the risks around the modal inflation forecast were skewed to the upside, albeit by less than in May, reflecting the possibility that the second-round effects of external cost shocks on inflation in wages and domestic prices take longer to unwind than they did to emerge. The mean projection for CPI inflation, which incorporated these risks, was 2.0% and 1.9% at the two and three-year horizons respectively.

Since the MPC's previous meeting, global growth has evolved broadly in line with the August Report projections, albeit with some differences across regions. Spot oil prices have risen significantly, while underlying inflationary pressures have remained elevated across advanced economies.

UK GDP is estimated to have declined by 0.5% in July and the S&P Global/CIPS composite output PMI fell in August, although other business survey indicators remain consistent with positive GDP growth. While some of this news could prove erratic, Bank staff now expect GDP to rise only slightly in 2023 Q3. Underlying growth in the second half of 2023 is also likely to be weaker than expected.

There have been some further signs of a loosening in the labour market, although it remains tight by historical standards. The vacancies-to-unemployment ratio has continued to decline, reflecting both a steady fall in the number of vacancies and rising unemployment. The Labour Force Survey unemployment rate rose to 4.3% in the three months to July, higher than expected in the August Report. Indicators of employment have generally softened against the backdrop of subdued activity.

Annual private sector regular Average Weekly Earnings (AWE) growth increased to 8.1% in the three months to July, 0.8 percentage points above the August Report projection. The recent path of the AWE is, however, difficult to reconcile with other indicators of pay growth. Most of these have tended to be more stable at rates of growth that are elevated but not quite as high as the AWE series.

Twelve-month CPI inflation fell from 7.9% in June to 6.7% in August, 0.4 percentage points below expectations at the time of the Committee's previous meeting, and triggering the exchange of open letters between the Governor and the Chancellor of the Exchequer that is being published alongside this monetary policy announcement. Core goods CPI inflation has fallen from 6.4% in June to 5.2% in August, much weaker than expected in the August Report. Services CPI inflation rose from 7.2% in June to 7.4% in July but declined to 6.8% in August, 0.3 percentage points lower than expected in the August Report. Some of those movements are linked to services such as airfares and accommodation that tend to be volatile over the summer holiday period. Excluding these travel-related components, services inflation has been more stable at continued high rates, albeit slightly weaker than expected.

CPI inflation is expected to fall significantly further in the near term, reflecting lower annual energy inflation, despite the renewed upward pressure from oil prices, and further declines in food and core goods price inflation. Services price inflation, however, is projected to remain elevated in the near term, with some potential month-to-month volatility.

The MPC's remit is clear that the inflation target applies at all times, reflecting the primacy of price stability in the UK monetary policy framework. The framework recognises that there will be occasions when inflation will depart from the target as a result of shocks and disturbances. Monetary policy will ensure that CPI inflation returns to the 2% target sustainably in the medium term.

Developments in key indicators of inflation persistence have been mixed, with the recent acceleration in the AWE not apparent in other measures of wages and with some downside news on services inflation. There are increasing signs of some impact of tighter monetary policy on the labour market and on momentum in the real economy more generally. Given the significant increase in Bank Rate since the start of this tightening cycle, the current monetary policy stance is restrictive. At this meeting, the Committee voted to maintain Bank Rate at 5.25%.

The MPC will continue to monitor closely indications of persistent inflationary pressures and resilience in the economy as a whole, including the tightness of labour market conditions and the behaviour of wage growth and services price inflation. Monetary policy will need to be sufficiently restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term, in line with the Committee's remit. Further tightening in monetary policy would be required if there were evidence of more persistent inflationary pressures.

The MPC committed in the minutes of its August 2022 meeting to review the reduction in the Asset Purchase Facility annually and, as part of that, to set an amount for the reduction in the stock of purchased UK government bonds over the subsequent 12-month period. At this meeting, the Committee voted to reduce the stock of UK government bond purchases held for monetary policy purposes, and financed by the issuance of central bank reserves, by £100 billion over the period from October 2023 to September 2024, to a total of £658 billion.

Minutes of the Monetary Policy Committee meeting ending on 20 September 2023

1: Before turning to its immediate policy decisions, the Committee discussed: the international economy; monetary and financial conditions; demand and output; and supply, costs and prices.

The international economy

2: UK-weighted global GDP was estimated to have increased by 0.5% in 2023 Q2, broadly in line with the August Monetary Policy Report projection. Global GDP growth of 0.3% was expected for Q3, also in line with the August Report, but with some differences across regions.

3: Euro-area GDP had increased by 0.1% in 2023 Q2 but was expected to contract in Q3, weaker than expected in the August Report. Manufacturing and services output PMIs had both entered contractionary territory, with weakness in German manufacturing output particularly pronounced.

4: In the United States, GDP had increased by 0.5% in 2023 Q2, and growth was expected to increase further in Q3, stronger than projected in the August Report for both quarters. In contrast to developments in the euro area, the manufacturing output PMI had stopped contracting and the services output PMI had remained in expansionary territory.

5: The Committee discussed some possible factors behind the recent relative strength of US activity. Real incomes had increased more strongly in the United States, uplifted partly by significant fiscal policy actions during the pandemic and a smaller deterioration in the terms of trade, whereas government support in Europe had abated as energy prices had fallen back. US households had also appeared relatively more willing to spend any excess savings, possibly due to higher consumer confidence.

6: Growth appeared to have slowed in China, with the NBS manufacturing PMI having remained below the neutral 50 level since April. Consumption and industrial production growth were similarly weak, alongside softer investment and falling exports. There had been notable headwinds from the property sector, with property prices falling and a major developer narrowly avoiding technical default. Taken together, these indicators pointed to Chinese growth slowing further in 2023 Q3, weaker than had been expected in the August Report.

7: Energy prices had increased since the MPC's previous meeting. The Dutch Title Transfer Facility spot price, a measure of European wholesale gas prices, had risen by 26%, owing in part to strike action at Australian liquefied natural gas facilities, although the gas futures curve had been broadly unchanged. Brent spot oil prices had risen by 17%, to $93 per barrel, following supply cuts by the OPEC+ group, as well as oil inventories falling globally.

8: Headline consumer price inflation in the United States and euro area had continued to follow a downward trend from the peak rates recorded in 2022, although the impact of volatile energy prices had affected recent data. Annual euro-area HICP inflation had decreased slightly to 5.2% in August. In the United States, headline CPI inflation had increased to 3.7% in August from 3.2% in July, largely accounted for by a reduced drag from annual energy price inflation.

9: Underlying inflationary pressures had remained elevated across advanced economies. US annual core CPI inflation had fallen to 4.3% in August from 4.7% in July. Annual core inflation in the euro area had fallen to 5.3% in August from 5.5% in July. Outturns in pay growth in these regions had continued to be strong. Labour markets had remained tight though had shown some signs of easing. The vacancies-to-unemployment ratio had decreased in the United States and had been broadly flat in the euro area.

Monetary and financial conditions

10: Market pricing suggested that policy rates in major advanced economies were expected to be nearing their peaks. At its meeting ending on 14 September, the ECB Governing Council had raised its key policy rates by 25 basis points, while market expectations were for the Federal Open Market Committee to leave the federal funds rate unchanged at its forthcoming meeting ending on 20 September. In the United Kingdom, Bank Rate expectations implied by market pricing had fallen in the immediate run-up to the MPC's meeting, following the August CPI release. That had left market expectations for the September Bank Rate decision finely balanced between a 25 basis point increase and no change.

11: There had also been a reduction in market expectations for the path of Bank Rate beyond the September MPC decision. Market pricing in the immediate run-up to the MPC's meeting suggested a peak in Bank Rate of around 5.5%, held for around three quarters. Since the MPC's previous meeting, the one-year overnight index swap (OIS) rate, one year forward had decreased by around 70 basis points. The market implied path for Bank Rate now averaged a little under 5% over the next three years.

12: Ten-year government bond yields in the United Kingdom were down a little relative to the MPC's August meeting, in contrast to global peers, for whom rates at this horizon had risen somewhat. The Committee noted that the level of UK and US 10-year government bond yields had converged over the recent period.

13: There had continued to be evidence that interest rates in financial markets had been more sensitive to economic data outturns, particularly in the United Kingdom, than had been usual over the past decade. Nevertheless, these data outturns could be volatile from month to month. Overall, the sensitivity of UK interest rates to data releases relating to the nominal environment had remained greater than to releases relating to real activity, although there had been some reductions in market rates in response to both the August flash PMI and July GDP data releases.

14: As the MPC had previously communicated, it would vote at this meeting on the reduction in the stock of gilts held in the Bank's Asset Purchase Facility for monetary policy purposes over the 12-month period from October 2023 to September 2024. According to the Market Participants Survey (MaPS), the median market expectation for the MPC's pace of gilt stock reduction over the year ahead was £100 billion.

15: Medium-term inflation compensation measures in the United Kingdom were little changed relative to the MPC's previous meeting. Although interpreting the level of these measures continued to be challenging, they had remained lower than their peak in March 2022, but above their average levels of the previous decade. The median MaPS respondent's expectation for CPI inflation three years ahead was 2.0% in the latest survey, down slightly relative to the previous survey. The distribution of survey responses had, however, remained skewed to the upside.

16: Aggregate growth in sterling net lending by banks had continued to slow. Within that, new mortgage lending had continued to decline. While quoted mortgage rates had fallen somewhat since the MPC's August meeting, largely reflecting pass-through of reductions in risk-free reference rates, they had remained substantially higher than at the start of the Bank Rate tightening cycle. Over that period, corporate credit conditions had also tightened and, consistent with that, and with subdued demand for credit, corporate lending growth had been weak.

17: The annual growth rate in aggregate sterling broad money had slowed further to 0% in July. The pass-through of increases in Bank Rate to instant-access savings accounts, which had previously been much slower than pass-through to time deposit accounts, had increased since the Committee's previous meeting. The overall increase in such sight deposit rates had, however, remained substantially smaller than the increase in Bank Rate since the end of 2021.

Demand and output

18: According to the ONS's first quarterly estimate, real GDP had increased by 0.2% in 2023 Q2, marginally stronger than had been expected in the August Monetary Policy Report. Household consumption had risen by 0.6% and business investment by 3.4%, stronger than expected in the August Report. Housing investment had continued to fall, down by 2.3% on the quarter and by 7.7% on a year earlier.

19: Monthly GDP was estimated to have fallen by 0.5% in July, following a rise of 0.5% in June. The July outturn was weaker than had been expected in the August Report, particularly within the services sector. Measured government health services output had fallen sharply in part reflecting the impact of strikes, and poor weather had also appeared to have dampened activity in some sectors. Weakness in private services activity had otherwise been concentrated in transport and other business services sectors.

20: The S&P Global/CIPS UK composite output PMI had fallen in August, to 48.6, which was consistent with a fall in GDP based on past historical relationships. The future output PMI series had risen slightly, however, and remained close to its long-run average. Other business survey indicators of activity, including the Lloyds Business Barometer, had also remained consistent with positive GDP growth. The latest intelligence from the Bank's Agents suggested that activity had remained subdued and that there were growing concerns about the economic outlook, most notably from contacts in consumer-facing businesses but also from some in the business services sector.

21: Combining the signals from official data and business surveys, Bank staff now expected GDP to rise by only 0.1% in 2023 Q3, compared with the 0.4% increase incorporated in the August Report. Although some of this downside news could prove erratic, underlying growth was also likely to be weaker than the ¼% per quarter built into the August projection for the second half of 2023.

22: The Committee discussed the factors behind a slowing in GDP growth, including the impact of the significant tightening in monetary policy since the end of 2021. The clearest signs of weakness continued to be in the housing sector, with housing investment and most measures of house prices falling somewhat, alongside a low level of property transactions. Recent consumer spending indicators had shown fewer signs of softening, with consumer confidence recovering in August and real labour incomes now rising. Corporate spending indicators had generally weakened over recent months, however, with an increasing number of firms responding to the ONS Business Insights and Conditions Survey noting concerns about interest rates. The manufacturing export orders PMI had also fallen quite sharply recently, in part reflecting global developments.

23: Since the MPC's previous meeting, the ONS had published some estimates of the impact of Blue Book 2023. GDP had been revised nearly 2% higher by 2021 Q4, although almost all of this news had been accounted for by stronger public sector output, largely reversing the revisions in Blue Book 2022. The Committee would consider the implications of revisions for supply as well as demand in its November forecast round discussions, by which time the Blue Book dataset beyond 2021 would also be available.

Supply, costs and prices

24: There had been further signs of a loosening in the labour market, although it remained tight by historical standards. Contacts of the Bank's Agents had reported an easing in recruitment difficulties, but also persistent skills shortages in some sectors. The vacancies-to-unemployment ratio had continued to decline, reflecting both a steady fall in the number of vacancies and rising unemployment. The Labour Force Survey (LFS) unemployment rate had risen to 4.3% in the three months to July, higher than expected in the August Monetary Policy Report forecast. The latest quarterly data had shown an increase in flows from inactivity into unemployment, indicative of some of the increase in unemployment having been associated with individuals that were previously inactive beginning to look for work, as well as a gradual increase in flows from employment into unemployment.

25: Indicators of employment had generally softened against a backdrop of subdued activity. LFS employment had fallen by 0.6% in the three months to July, but that had been preceded by a 0.8% increase in the previous non-overlapping three months. This series often fluctuated from one period to another and sample sizes and response rates to the LFS had been declining. The Bank's Agents had reported that companies were expecting to keep staff numbers broadly stable, with few active plans to make redundancies. The KPMG/REC Report on Jobs was, however, pointing to a fall in companies hiring new staff. The S&P Global/CIPS composite employment PMI had also fallen in August, albeit only to around its historical average.

26: The Committed discussed what to infer from the latest developments in indicators of pay. Annual private sector regular Average Weekly Earnings (AWE) growth had been 8.1% in the three months to July, 0.8 percentage points above the August Report projection, with the news largely due to upward revisions to previous months' data. Three-month-on-three-month growth for the same AWE measure had increased in recent months, with that strength seen across a number of different sectors.

27: The latest path of the AWE was, however, difficult to reconcile with other pay indicators, including measures using HMRC payrolls, the LFS and the Decision Maker Panel (DMP), which had tended to be more stable at rates that were elevated but not quite as high as the AWE series. The Bank's Agents were continuing to report that average annual pay settlements were in the region of 6 to 6½%, with contacts expecting settlements to begin to drift down and for there to be fewer additional payments provided to compensate for a higher cost of living. Only the measures within the KPMG/REC Report were signalling a clear decrease in pay growth but, puzzlingly, their relationship with the AWE data had been less strong over the recent past.

28: Twelve-month CPI inflation had fallen to 6.8% in July, before edging down to 6.7% in August, 0.4 percentage points below the August Report forecast. The latest CPI release had triggered the exchange of open letters between the Governor and the Chancellor of the Exchequer that was being published alongside these minutes.

29: While declines in CPI inflation had been largely driven by lower energy prices up to July, the fall in August had been driven by other components. A combination of past falls in petrol pump prices dropping out of the annual comparison and increases on the month had resulted in a higher rate of energy price inflation in August. In contrast, core CPI inflation, excluding energy, food, beverages and tobacco, had fallen to 6.2%, having been relatively stable at just under 7% in preceding months.

30: Lower core goods price inflation had accounted for just under two-thirds of the downside surprise in CPI inflation since the August Report. Some of the latest news had been confined to the more idiosyncratic used cars component. Downside news elsewhere in core goods, however, suggested that the recent easing in input cost pressures, evident in a flattening in non-petroleum producer prices, was feeding through to consumer goods prices more quickly than had been anticipated previously. There had been relatively modest and offsetting news in food and energy prices up to August. If sustained, recent significant increases in oil prices would, however, mean that the energy contribution to CPI inflation would be higher than assumed in the August Report forecast over coming months.

31: The remainder of the downside surprise in CPI inflation since August had been in services prices. Services CPI inflation had unexpectedly risen back to a 31-year high of 7.4% in July before falling more sharply than had been expected to 6.8% in August. Some of the increase in July and the subsequent unwind, along with the corresponding news, was linked to services such as airfares and accommodation that tended to be volatile over the summer holiday period. Excluding travel-related components such as these, services inflation had been more stable at continued high rates. Nevertheless, there had also been some downside news across this wider part of the consumer basket for services.

32: An underlying measure of services inflation produced by Bank staff, which was determined by the co-movement of price changes across services components, had begun to decline. The S&P Global/CIPS UK services input and output price PMIs had continued to fall towards their past averages, while Agents' contacts were reporting that, although pay pressures had remained intense for consumer-facing services companies, other cost pressures were easing.

33: Abstracting from these underlying trends, the path of services inflation was likely to be volatile in coming months, in part reflecting potential noise in the prices of travel-related services. A temporary sharp upward spike was also anticipated in January 2024, as large and unusual falls in a number of services prices at the beginning of 2023 were not expected to be repeated, resulting in a positive base effect early next year.

34: Inflation expectations for the year ahead had remained at elevated levels. Businesses responding to the DMP were expecting their own prices to increase by around 5% over the next twelve months. Measures of household inflation expectations were broadly unchanged in both the Bank/Ipsos and Citi/YouGov surveys, within which the medium-term measures were closer to their historical averages.

The immediate policy decisions

35: The MPC sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment.

36: In the MPC's August most likely, or modal, Monetary Policy Report projections, conditioned on a market-implied path for Bank Rate that had averaged just under 5½% over the three-year forecast period, CPI inflation had been expected to return to the 2% target by 2025 Q2. It had then been projected to fall below the target in the medium term, as an increasing degree of economic slack had been expected to reduce domestic inflationary pressures, alongside declining external cost pressures. The Committee had continued to judge that the risks around the modal inflation forecast were skewed to the upside, albeit by less than in May, reflecting the possibility that the second-round effects of external cost shocks on inflation in wages and domestic prices took longer to unwind than they did to emerge. The mean projection for CPI inflation, which incorporated these risks, had been 2.0% and 1.9% at the two and three-year horizons respectively.

37: The Committee discussed the news in recent UK economic data outturns. Past increases in Bank Rate were expected to weigh increasingly on the economy, with the impact of tighter monetary policy likely to be apparent earlier for indicators of demand and labour market tightness than for indicators of domestically generated inflation, such as wage growth and services CPI inflation, which were at a later stage in the monetary transmission mechanism.

38: While some of the weakening in recent activity data could prove erratic, Bank staff now expected GDP to rise only slightly in 2023 Q3. Underlying growth in the second half of 2023 was also likely to be weaker than had been expected. Ahead of its final meeting, the Committee was made aware of the flash S&P Global/CIPS UK composite PMI for September that would be released publically on Friday 22 September.

39: There had been some further signs of a loosening in the labour market, although it had remained tight by historical standards. The vacancies-to-unemployment ratio had continued to decline, reflecting both a steady fall in the number of vacancies and a greater than expected rise in unemployment.

40: Annual private sector regular Average Weekly Earnings (AWE) growth had increased to 8.1% in the three months to July, 0.8 percentage points above the August Report projection. Most other indicators of pay had tended to be more stable at rates of growth that were elevated but not quite as high as the AWE series.

41: Twelve-month CPI inflation had fallen to 6.7% in August, 0.4 percentage points below expectations at the time of the Committee's previous meeting. Services CPI inflation had declined to 6.8% in August, 0.3 percentage points lower than had been expected in the August Report. Some of those movements were linked to services such as airfares and accommodation that tended to be volatile over the summer holiday period. Excluding these travel-related components, services inflation had been more stable at continued high rates, albeit slightly weaker than had been expected.

42: The MPC's remit was clear that the inflation target applied at all times, reflecting the primacy of price stability in the UK monetary policy framework. The framework recognised that there would be occasions when inflation would depart from the target as a result of shocks and disturbances. Monetary policy would ensure that CPI inflation returned to the 2% target sustainably in the medium term. Monetary policy was also acting to ensure that longer-term inflation expectations were anchored at the 2% target.

Bank Rate decision

43: The Committee turned to its immediate decision on Bank Rate. Developments in key indicators of inflation persistence had been mixed, with the recent acceleration in the AWE not apparent in other measures of wages and with some downside news on services inflation. There were increasing signs of some impact of tighter monetary policy on the labour market and on momentum in the real economy more generally. Given the significant increase in Bank Rate since the start of this tightening cycle, the current monetary policy stance was restrictive. This meant that the decision on whether to increase or to maintain Bank Rate at this meeting had become more finely balanced between the risks of not tightening policy enough when underlying inflationary pressures could still prove persistent, and not placing sufficient weight on the impact of the previous tightening that was still to come through on activity and inflation.

44: Five members judged that maintaining Bank Rate at 5.25% was warranted at this meeting. There were signs that the labour market was loosening. The recent acceleration in the AWE was noteworthy but was not apparent in other measures of wages. Although it was important not to put too much weight on a single data point, headline and services CPI inflation had fallen back and were lower than had been expected. Regarding activity, contacts of the Bank's Agents had become more downbeat, and the output PMI in August was now consistent with falling GDP. For most members within this group, the latest developments meant that the judgement to keep Bank Rate unchanged at this meeting rather than increase it was finely balanced. Conditions were likely to warrant a restrictive policy stance being maintained until material progress had been made in returning inflation to the 2% target sustainably. For one member, however, the risks of overtightening policy had continued to build, increasing the likelihood of output losses and volatility that would require sharper reversals of policy. Lags in the effects of monetary policy meant that sizeable impacts from past rate increases were still to come through.

45: Four members judged that a 0.25 percentage point increase in Bank Rate, to 5.5%, was warranted at this meeting. Although there were now some signs of weakening economic activity, consumer sentiment appeared to be holding up, real household incomes had started to rise, and forward-looking indicators of output had remained positive. The labour market was still relatively tight, consistent with a possible rise in the medium-term equilibrium rate of unemployment, and the pace of loosening had been slow. Measures of wage growth and services inflation had remained at rates above those consistent with meeting the 2% target sustainably in the medium term. While services CPI inflation had fallen by more than had been expected in the latest data release, this appeared to have been driven mainly by volatile components and had followed recent upside surprises. These members judged that overall there was evidence of more persistent inflationary pressures. Although the monetary stance was weighing increasingly on economic activity, a 0.25 percentage point increase in Bank Rate at this meeting was necessary to address the risks of more deeply embedded inflation persistence and bring inflation back to the 2% target sustainably in the medium term.

46: The MPC would continue to monitor closely indications of persistent inflationary pressures and resilience in the economy as a whole, including the tightness of labour market conditions and the behaviour of wage growth and services price inflation. Monetary policy would need to be sufficiently restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term, in line with the Committee's remit. Further tightening in monetary policy would be required if there were evidence of more persistent inflationary pressures.

Decision on the annual pace of reduction in the stock of UK government bond purchases held for monetary policy purposes

47: As set out in the minutes of its August 2022 meeting, the MPC had committed to review the reduction in the Asset Purchase Facility (APF) annually and, as part of that, to set an amount for the reduction in the stock of purchased UK government bonds (gilts) over the subsequent 12-month period. Box A of the August 2023 Monetary Policy Report had set out an assessment of the process of quantitative tightening over the previous year.

48: The Committee judged that reducing the size of the APF had the important benefit of reducing the risk of a ratchet upwards in the size of the central bank balance sheet over time if successive policy cycles encountered the effective lower bound on interest rates. That in turn should increase the headroom and flexibility for the central bank to be able to use its balance sheet in the future should that be needed.

49: The appropriate pace of gilt stock reduction would continue to be guided by a set of key principles, which the MPC had first outlined in the August 2021 Monetary Policy Report. First, the Committee intended to use Bank Rate as its active policy tool when adjusting the stance of monetary policy. Second, sales would be conducted so as not to disrupt the functioning of financial markets. Third, to help achieve that, sales would be conducted in a gradual and predictable manner over a period of time.

50: As set out in the Box in the August 2023 Report, the Committee judged that quantitative tightening was going smoothly. There was no evidence of a negative impact of gilt sales on market functioning across a range of financial market measures. APF reduction was likely to have had some tightening effect on yields, which, while difficult to measure precisely, was judged to have been modest. That was in line with the MPC's prior expectations, but the Committee would continue to learn from monitoring developments as the process progressed.

51: The tightening impact of the reduction in the APF on activity and inflation also appeared to have been, and was expected to be, modest. While it was hard to measure precisely the marginal effect of quantitative tightening, the MPC's economic forecasts were conditioned on asset prices that incorporated announced and expected APF reduction alongside other factors. The MPC would therefore take this effect into account when setting the desired monetary policy stance using Bank Rate. Any tightening effect from the reduction in the APF would lead to a slightly lower path for Bank Rate, all else equal. Given that the impact of APF reduction was judged to have been modest, this was unlikely to have made a material difference to the appropriate path for Bank Rate over the past year.

52: Drawing on the experience of the first year of quantitative tightening, the Committee considered a number of factors which supported a modest increase in the pace of gilt stock reduction from £80 billion over the previous year to £100 billion over the 12 months ahead. First, an assessment of market conditions, and of market capacity to absorb the pace of gilt sales implied by a £100 billion gilt stock reduction, suggested that this pace was unlikely to disrupt the functioning of financial markets. Second, the Committee noted that a £100 billion gilt stock reduction over the year ahead would leave the pace of gilt sales broadly unchanged relative to the previous year, given some increase in APF gilt maturities. As set out in the August 2023 Report, the focus of the MPC was on total gilt stock reduction, comprising both maturing gilts and sales, such that variation in the profile of redemptions might also lead to variation in the pace of sales over time. Notwithstanding that, the Committee placed some weight on continuity in the pace of sales. Third, the Committee noted that over the previous year the £80 billion reduction in APF gilt holdings had been accompanied by the near-complete unwind of the £20 billion corporate bond portfolio, such that the overall reduction in the size of the APF over the past year had also been around £100 billion. Taken together, these factors supported a small increase in the pace of reduction in the stock of gilts relative to the previous year.

53: In the immediate run-up to this meeting, Bank staff had briefed the MPC on the current state of economic and market conditions. Current conditions were judged appropriate for the Committee to proceed with its preferred pace of gilt stock reduction. The Financial Policy Committee (FPC) had also been briefed.

54: All members of the MPC agreed at this meeting that the Bank of England should reduce the stock of UK government bond purchases held for monetary policy purposes, and financed by the issuance of central bank reserves, by £100 billion over the 12-month period from October 2023 to September 2024, comprising both maturing gilts and sales.

55: The MPC also reaffirmed that there would be a high bar for amending the planned reduction in the stock of purchased gilts outside a scheduled annual review. That was in order to remain consistent with the principles that Bank Rate should be the active policy tool when adjusting the stance of monetary policy, and that APF reduction should be predictable. In judging whether that bar was met, the FPC would also have a role through its assessment of financial stability.

56: The Chair invited the Committee to vote on the propositions that:

- Bank Rate should be maintained at 5.25%;

The Bank of England should reduce the stock of UK government bond purchases held for monetary policy purposes, and financed by the issuance of central bank reserves, by £100 billion over the next twelve months, to a total of £658 billion.

57: Five members (Andrew Bailey, Ben Broadbent, Swati Dhingra, Huw Pill and Dave Ramsden) voted in favour of the first proposition. Four members (Jon Cunliffe, Megan Greene, Jonathan Haskel and Catherine L Mann) voted against the proposition, preferring to increase Bank Rate by 0.25 percentage points, to 5.5%.

58: The Committee voted unanimously in favour of the second proposition.

Operational considerations

59: On 20 September 2023, the total stock of assets held for monetary policy purposes was £759 billion, comprising £759 billion of UK government bond purchases and £0.6 billion of sterling non‐financial investment‐grade corporate bond purchases.

60: At its September 2022 meeting, the MPC had voted to reduce the stock of UK government bond purchases by £80 billion over the 12-month period from October 2022 to September 2023. The Bank of England had set out in a Market Notice on 1 September how the 2023 Q3 gilt sales programme would be adjusted in order to meet the MPC's target.

61: At this meeting, the MPC had voted to reduce the stock of UK government bond purchases held for monetary policy purposes by £100 billion over the 12-month period from October 2023 to September 2024. The details of the first quarter of the associated gilt sales programme, covering 2023 Q4, were set out in a Market Notice accompanying these minutes. The Bank would continue to set auction sizes each quarter, to meet the MPC's annual target as closely as practicable.

62: The following members of the Committee were present:

- Andrew Bailey, Chair

- Ben Broadbent

- Jon Cunliffe

- Swati Dhingra

- Megan Greene

- Jonathan Haskel

- Catherine L Mann

- Huw Pill

- Dave Ramsden

James Bowler was present as the Treasury representative.

Sarah Breeden was present as an observer.

63: On behalf of the Committee, the Chair expressed his appreciation to Jon Cunliffe for his contributions to the work of the MPC since becoming a member in 2013 and for his role in establishing the monetary policy framework.

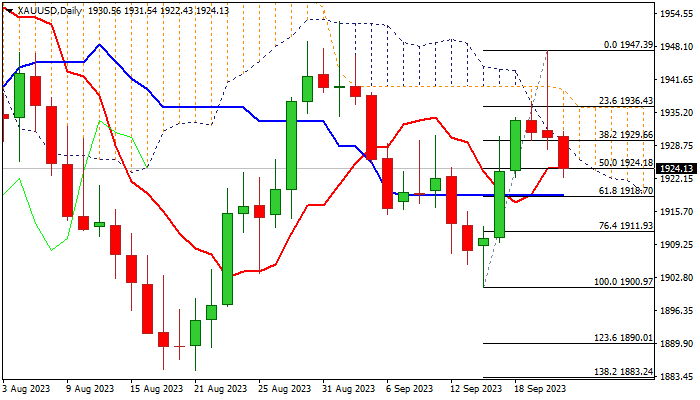

XAU/USD: Gold Loses Ground After Hawkish Signals from Fed

Gold fell further on Thursday, deflated by hawkish stance of the US Federal Reserve, as the central bank kept interest rates on hold in its September’s policy meeting which ended on Wednesday, but signaled another hike by the end of the year and likely to keep high interest rates through 2024.

Hawkish Fed’s posture on interest rates renewed demand for dollar and increased pressure on metal’s price.

Fresh weakness contributes to formation of reversal pattern on daily chart after the action on Wednesday was strongly rejected above daily cloud top, leaving daily Doji candle with long upper shadow and forming a bull-trap pattern.

Today’s acceleration lower hit over 50% retracement of $1900/$1947 upleg, adding to signals that near-term bull-phase is likely over.

Close below 50% retracement ($1924, reinforced by 200DMA) is needed to confirm signal and risk deeper drop towards Fibo targets at $1918/11 (Fibo 61.8% / 76.4% respectively) and expose key near-term support at $1900 (Sep 14 higher low).

The 14-d momentum indicator remains in negative territory and RSI/Stochastic are heading south, reinforcing negative near-term outlook.

The base of daily cloud ($1929) marks solid resistance, with today’s close below here needed to keep the action biased lower.

Res: 1929; 1936; 1939; 1947.

Sup: 1918; 1911; 1905; 1900.

The Battle for Oil. OPEC Strikes Back

The past several weeks have been a real triumph for the bulls in the oil market. The Brent spot price grew by 8.5% during the last month.

The energy market is currently becoming especially important for both blocs of countries. BRICS+ countries represent the Eastern bloc, while the Western bloc is G7 countries. A severe confrontation over price continues. The oil market is the key to the future global geopolitical and economic configuration.

Prerequisites for a price war in the oil market

According to money supply ratios, 80% of all money entering the American system occurred between 2020 and 2023. All available channels were used to pump in liquidity: QE, Helicopter Money, and low rates. The situation in G7 countries was more or less controlled in 2021, with an inflation level of 5%. By February 2022 (the beginning of the Russia-Ukraine conflict), the CPI in the States reached 7.5%. The Fed-targeted Personal Consumption Expenditure (PCE) approached 6%. However, by the time of the price shock in the oil market, the Fed had still not begun the cycle of monetary policy tightening, leaving the real rate in a deeply negative zone.

The oil market’s price shock, provoked by the conflict in Ukraine, required the Fed to make tough decisions. Firstly, the FOMC began to raise the rate quite aggressively - the increase step at each meeting was at least 50 bp. Secondly, in April 2022, the Fed balance sheet began to decline (QT) for the first time in quite a long time.

However, this was not enough. Since full control over inflation was possible only if oil prices were controlled.

G7 countries win the first round

The first thing the United States did after the start of the conflict in Ukraine was to cut Russia from the European energy market. Although this was done to the detriment of the national interests of the allies, the United States became the largest beneficiary of the process. The American energy sector made a significant breakthrough. By October 2022, the S&P Energy sector had almost reached its 2014 historical highs, testing 724.74 points.

To solve this problem, the United States significantly increased oil production (up to 12.8 million barrels per day) and continued to sell oil from its strategic reserves. Strategic oil reserves in the United States over the past two years (i.e., since the COVID crisis) have decreased from 635 million to 350 million barrels. This means that by releasing liquidity into the markets, the States simultaneously began active actions in the energy market, preventing price growth. Thus, monetary control in 2020–2022 gradually passed into energy control. By the way, strategic reserves are strategic because they serve to solve longer-term US goals. Commercial reserves are for short-term tactical use.

In 2023, this US control of the energy market was strengthened by the inclusion of WTI Midland in the Brent DTD, thus gradually squeezing out the British grade of oil from key grades in the derivatives market.

The United States expected another energy shock to occur but did not think this shock would be so strong. Otherwise, the FOMC would likely have begun a tightening cycle before the Russian-Ukrainian conflict started.

Then, the United States tried to increase oil production by reaching agreements with the largest oil producers, Iran (9th in the world) and Venezuela (20th). From January to July 2023, oil production in Iran increased from 2.5 million barrels per day to 2.8 million barrels (an increase of 12%) in Venezuela from 732 thousand barrels to 810 thousand barrels.

As a result, oil prices dropped below $80 per barrel in the second half of 2022 and the first half of 2023. The correction in the energy market with the simultaneous monetary policy tightening decreased consumer inflation by 500 bp – 8.2% to 3.2%.

The opening of China that never took place this year was a gift for oil-consuming countries. The Chinese economy reached a plateau and did not generate additional impetus for growth in oil prices.

OPEC+ Response

The countries of the Eastern bloc responded by reducing oil production. Saudi Arabia reduced production to 9 million barrels per day (in 2022, the country produced about 11 million), and Russia reduced production not so significantly - to 10 million barrels (production in July 2022 was 10.3 million). According to OPEC's latest report, the cartel's members cut production by 836 thousand barrels from June to July this year – to 27.3 million per day.

Their actions pushed the price up from $74 to $93 per barrel. This will later lead to higher inflation in the consumer countries and start a new cycle of inflationary pressure. Geopolitical tensions are likely to rise.

Technical Analysis

The price broke several resistance levels.

At first, it broke $87.75 and moved to $91. The bears gave up this level, too. The nearest resistance level is at $97.50.

According to the Elliott wave theory, the movement up may be a third impulse wave. It means that after the correction, the asset may overcome $97.50 and move directly to $100.

Let’s sum up:

- The price of oil and control over it has always been the main goal in the confrontation between countries on the world stage. This goal is becoming even more important, given the almost complete exhaustion of resources to control inflation (rates in developed countries have been kept at a high level for quite a long time; SPR in the United States has decreased significantly).

- Oil prices will most likely continue to rise. Consequently, it becomes impossible for the developed economies to switch to monetary easing fast – rates will remain high for a long time.

- Geopolitical risks are on the rise, so safe-haven allocations should increase.

- Market volatility will increase, and speculative strategies may be more attractive in the medium term than the classic “buy and hold” approach.