Sample Category Title

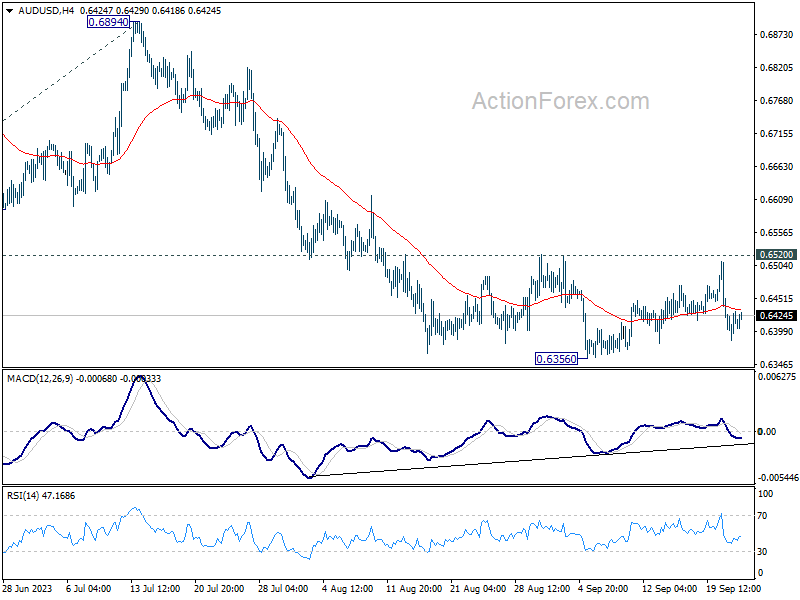

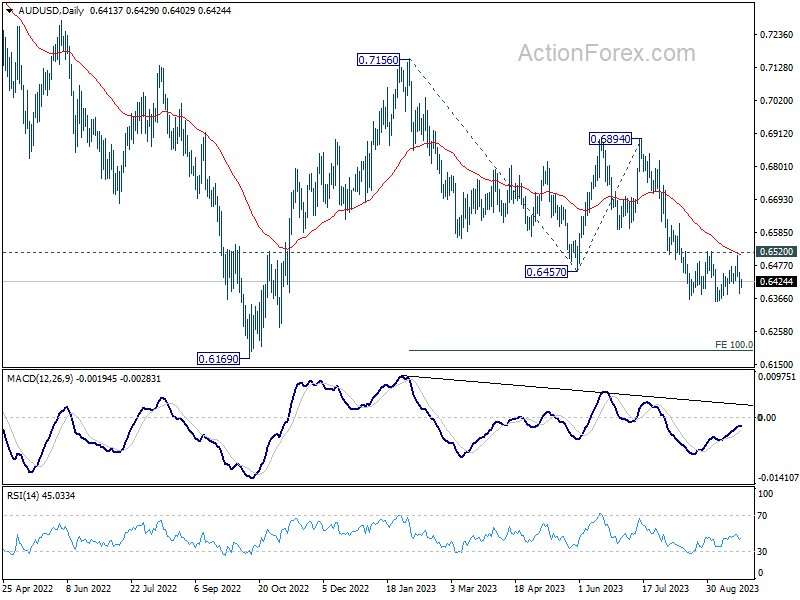

AUD/USD Daily Report

Daily Pivots: (S1) 0.6382; (P) 0.6419; (R1) 0.6453; More...

Intraday bias in AUD/USD stays neutral as range trading continues. Outlook stays bearish with 0.6520 resistance intact. On the downside, break of 0.6356 will resume larger down trend to 100% projection of 0.7156 to 0.6457 from 0.6894 at 0.6195.

In the bigger picture, down trend from 0.8006 (2021 high) is possibly still in progress. Decisive break of 0.6169 will target 61.8% projection of 0.8006 to 0.6169 to 0.7156 at 0.6021. This will now remain the favored case as long as 0.6894, in case of strong rebound.

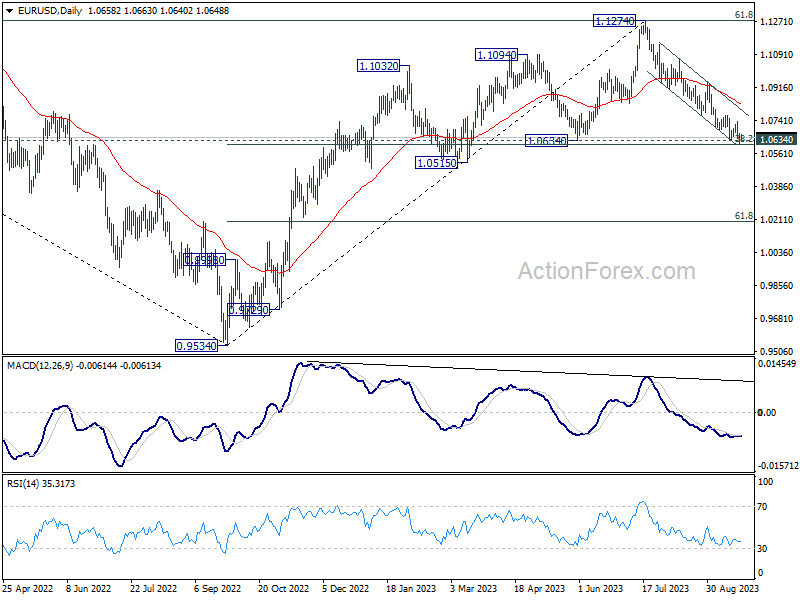

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0627; (P) 1.0651; (R1) 1.0684; More...

Intraday bias in EUR/USD is turned neutral again first. Sustained break of 1.0609/34 support zone will carry larger bearish implication. Fall from 1.1274 should then target target 1.0515 support next. Nevertheless, strong rebound from current level, followed by break of 1.0767 resistance, should confirm short term bottoming. Intraday bias will be back on the upside for 1.0944 resistance.

In the bigger picture, fall from 1.1274 medium term top is seen as a correction to up trend from 0.9534 (2022 low). Strong support could be seen from 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609) to bring rebound, at least on first attempt. However, sustained break of 1.0609/0634 will raise the chance of bearish trend reversal, and target 61.8% retracement at 1.0199.

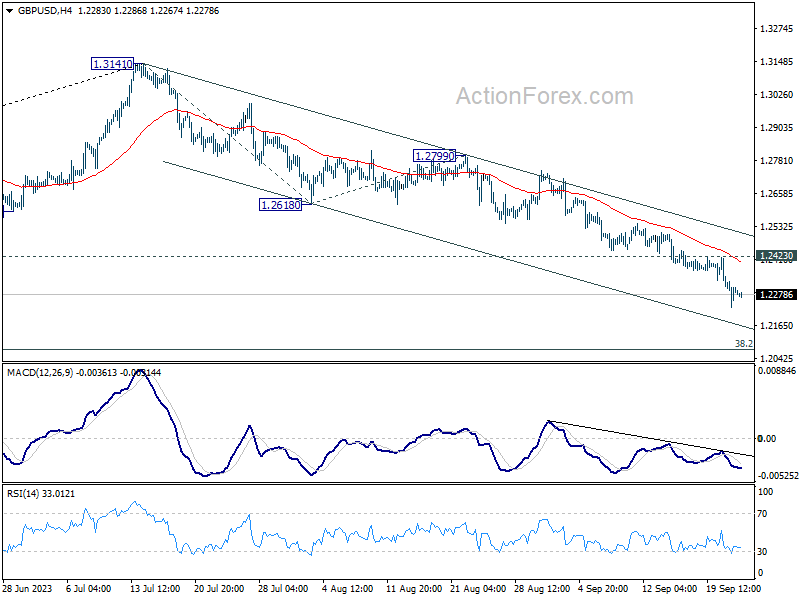

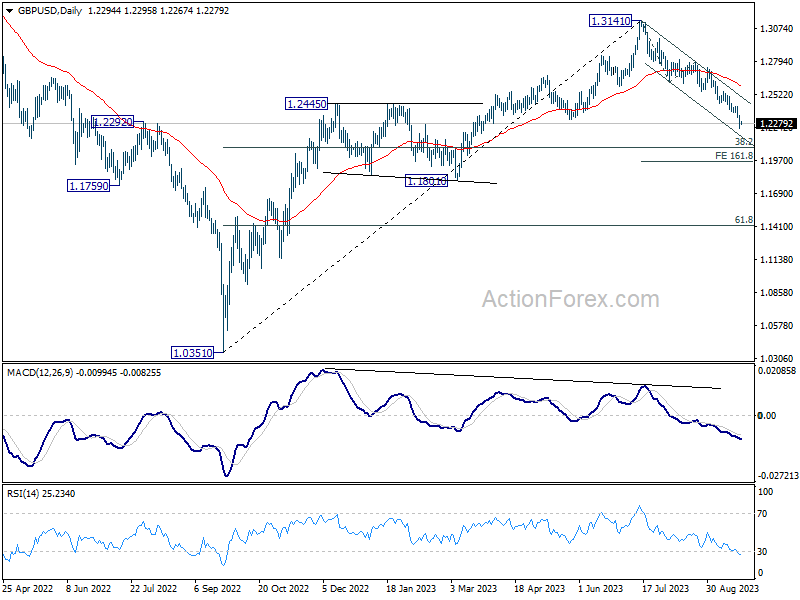

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2237; (P) 1.2293; (R1) 1.2352; More...

Intraday bias in GBP/USD remains on the downside as this point. Current fall from 1.3141 should target 1.2075 fibonacci level. On the upside, above 1.2423 minor resistance will turn intraday bias neutral again. But near term outlook will stay bearish as long as 1.2618 support turned resistance holds, in case of strong recovery.

In the bigger picture, fall from 1.3141 medium term top is seen as a correction to up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3141 at 1.2075. Strong support would be seen there to bring rebound on first attempt. However, sustained break of 1.2075 will raise the chance of bearish trend reversal.

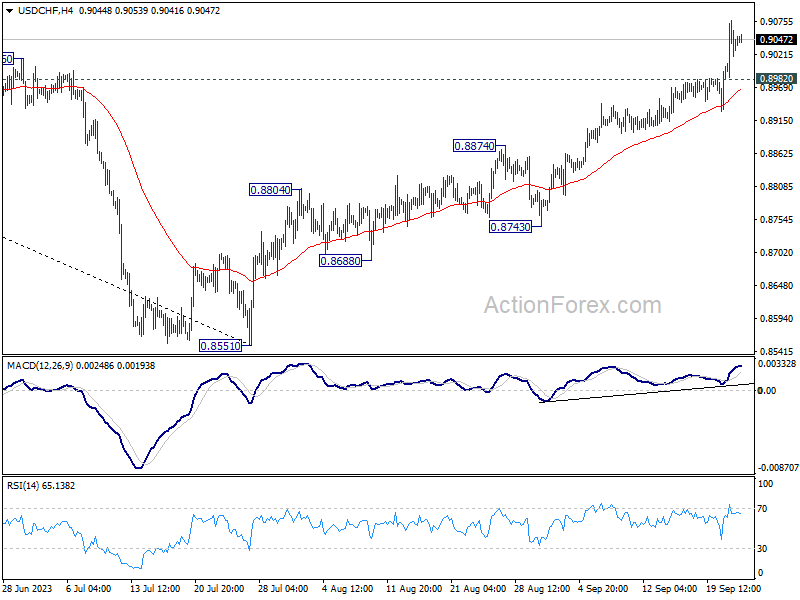

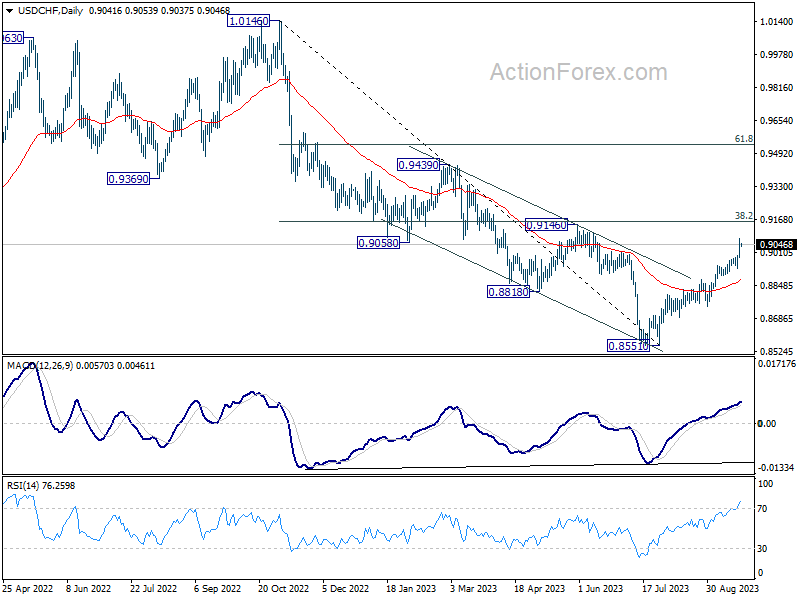

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8991; (P) 0.9035; (R1) 0.9090; More....

Intraday bias in USD/CHF remains on the upside at this point. Current rise from 0.8551 is in progress for 0.9146 cluster resistance. On the downside, break of 0.8982 minor support will turn intraday bias neutral first. But further rally will remain in favor as long as 0.8874 resistance turned support holds, in case of retreat.

In the bigger picture, rebound from 0.8551 medium term bottom is currently seen as a correction to the downtrend from 1.0146 (2022 high). Further rally would be seen to 0.9146 cluster resistance (38.2% retracement of 1.0146 to 0.8551 at 0.9160). Strong resistance could be seen there to limit upside, at least on first attempt.

Hawkish Fed vs Dovish Others

The Swiss National Bank (SNB) and the Bank of England (BoE) surprised by maintaining their rates unchanged at yesterday’s trading session. The Bank of Japan (BoJ) surprised by maintaining its ultra-lose monetary policy stance unchanged. Combined with a hawkish pause earlier this week, the major currencies further sank against the greenback. The USDCHF advanced past the 200-DMA, and Cable slipped to 1.2232, a fresh low since March, and whispers of a potential return to parity against the US dollar sparked, yet again. Reasonably, the pound-dollar could return to 1.20, and below, if the major 38.2% Fibonacci support – which stands at 1.2080 is pulled out and lets the pair slip into a medium-term bearish consolidation zone. But we will likely see the Federal Reserve (Fed) soften its tone before we start talking about parity in Cable.

Now, looking at what the BoE did, you know that I was surprised, and intrigued with the decision. In Switzerland for example, inflation – official inflation – steadied below the SNB’s 2%, target. The latest data shows that the Swiss CPI is at no higher than 1.6% - even though we are expecting a monstrous rise in health insurance costs, and another 20% rise in average in electricity costs that will certainly drill holes in our pockets at the start of next year, but for now inflation is at 1.6%, say the numbers, and alone, it justifies a SNB pause. But in Britain, the no action is quite premature. Inflation in Britain is almost at 7%, the energy prices are rising, the war in Ukraine is nowhere close to being over, sterling pound is now losing value, which means that whatever the Brits will import from now will cost them more than during the last months, when the pound was appreciating. It’s hard to see how, with all these developments, the BoE won’t be obliged to hike, again. The only way is a really bad economic performance.

A bright spot

If there is one bright spot in Britain with all this, it is the FTSE100. First, the rising energy prices are good for the energy-rich FTSE100. Second, softer sterling makes these companies more affordable for international investors, who should of course think of hedging their sterling exposure, and third, more than 80% of the FTSE100 companies’ revenues come from oversees, which means that when they convert their shiny dollar revenues back to a morose sterling, well, they can’t really complain with a stronger dollar. Consequently, if a more dovish BoE is bad for sterling, the combination of a hawkish Fed and a dovish BoE and a pitiless OPEC is certainly good for the FTSE100. The index has been left behind the S&P500 this year, as the tech rally is what propelled the American index to the skies, but that technology wind is now turning direction. The FTSE 100 broke its February to September downtrending trend to the upside and is fundamentally and technically poised to gain further positive traction, whereas, the S&P500 is heaving a rough month, with technology stocks set for their worse performance this year, under the pressure of rising US yields, which make their valuations look even more expensive.

Interestingly, the US 2-year yield peaked at 5.20% after the Fed’s hawkish pause this week and is back headed toward the 5% mark, but the gap between the US 2-year yield and the top range of the Fed funds rate is around 40bp, which is a big gap, and even if the Fed decided not to hike rates, this gap should narrow, in theory. If it does not, it means that bond traders are betting against the Fed’s hawkishness and think that the melting savings, the loosening jobs market, tightening bank lending conditions and strikes, and restart of student loan repayments and a potential government shutdown could prevent that last rate hike to happen before this year ends. And indeed, activity on Fed funds futures gives more than 70% chance for a third pause at the FOMC’s November meeting, and Goldman Sachs now sees the US expansion slow to 1.3% from 3.1% printed in the Q3. KPMG also warned that a prolonged auto stoppage may precipitate contraction. And if no deal is inked by noon today, the strikes will get worse.

One’s bad fortune is another’s good fortune

The Japanese auto exports surged big this year, they were 50% higher in yen terms. The yen is certrainly not doing well, but yes, you can’t have it all. That cheap yen is one of the reasons why the Japanese export so well outside their country. And in case you missed, the BoJ did nothing today to exit their hyper-ultra-loose monetary policy. They didn’t even give a hint of normalization, meaning that the yen will hardly strengthen from the actual levels. In the meantime, Toyota, Mitsubishi and Honda shares are having a stellar year, and the US strikes will only help them do better.

Was that the End of Hiking Cycle?

Market movers today

Today, focus shifts from central banks to economic outlook as we get the latest activity signals from Europe and the US in the form of PMIs.

In August, the euro area PMI print surprised negatively with the service sector falling into contractionary territory for the first time this year indicating that the entire economy is contracting. The weak August print came on top of the already negative July print that surprised markets. We expect to see some stabilisation in the September print given the large declines in the previous months. We look out for the sub-components of employment that indicated that aggregate employment growth was close to a stall in August. The price sub-components will also be closely watched as the service sector is still recording higher prices while goods prices are falling.

In the US, we expect modest weakening driven by the services component. August data has been rather mixed so far, with for example ISM surprising to the upside while retail sales already reflected weaker consumption.

We also have a few ECB and Fed speakers on the wires.

The 60 second overview

Japan: The Bank of Japan kept monetary policy unchanged as expected, including keeping the yield curve control policy. Inflation in Japan did not drop as expected in August. Headline inflation was 3.2% y/y and core inflation 4.3%. PMIs indicate that economic activity slowed further in September. Manufacturing PMI declined to 48.6 and the service PMI to 53.3.

Central banks: Bank of England and the Swiss National Bank surprised us and the market by refraining from raising interest rates further yesterday. The Riksbank and Norges Bank both hiked policy rates 25bp. While the door is still open for more hikes from all four, we think they are all done increasing interest rates.

Oil: The rally in oil prices came to a halt with the price on Brent crude stabilising for now around the USD93-94/bbl level. Prices have come a long way on the back of tighter supply, but negative risk sentiment in global financial markets and a stronger USD may start to weigh on oil demand. In addition, the release of flash PMIs today may put focus back on weakening global growth.

Equities: It was a broad risk-off session amid more hawkish takeaways from the FOMC meeting, which overshadowed the overall dovish rate decisions yesterday. As such, equities were lower on Thursday, with Europe and US selling off 1-2%. The value outperformance was sharp. Value outperformed growth by almost a full percentage yesterday, and a full 2% for the week globally. While it was a risk-off session in the US with all sectors lower, Nordics were more of a rotation story with banks rising at the expense of tech and industrials. Asian equities and especially tech are rebounding this morning. The only exception is Japan, where market is somewhat lower on an unchanged rate decision from the Bank of Japan but higher inflation and weaker PMIs than expected. US futures are a tad higher too.

FI: It was a very mixed picture in the global bond markets after yesterday's monetary policy meetings in UK, Switzerland, Sweden and Norway. Bank of England and SNB kept rates on hold contrary to expectations, while Norway and Sweden raised rates with 25bp as expected and signalled more could come before pausing.

Hence, the Norwegian curve saw a very bearish flattening, while UK and Switzerland saw steepening, where rates rose in the UK while declining in Switzerland. Swedish bond yields rose across the curve. In the US, there was a very bearish steepening of the curve, where 10Y Treasuries rose to 4.5%, the highest level since 2007

FX: EUR/USD has remained range-bound around following the week's Fed decision. USD/JPY rose above 148 once more on slightly dovish comments from the Bank of Japan. Both GBP and CHF weakened on unchanged policy decisions from respective central banks, however the latter retraced some of the move during the day. Volatile trading in Scandies following yesterday's policy decisions, but both closed the day close to unchanged.

Credit: On the back of the hawkish pause announced by the Fed on Wednesday, the credit markets were in risk-off mode yesterday. This left iTraxx main 2.9bp wider to 77.5bp and Xover 13.3bp wider to 419bp.

UK sales volume up 0.4% mom, sales value up 0.8% mom

UK retail sales showed some growth in August, albeit falling short of market expectations. On a month-on-month basis, sales volumes increased by 0.4% mom, slightly under the anticipated 0.5% rise. When removing the impact of fuel, the volume rose by a slightly better 0.6% mom. In terms of the monetary value, sales were up 0.8% mom, with the figures excluding fuel at 0.7% mom.

Taking a step back to analyze a broader timeframe, the three-month period leading up to August 2023 witnessed a 0.3% rise in sales volumes compared to the previous three months. Same growth of 0.3% was observed for volumes that excluded auto sales. In value terms, the increase was more pronounced with a 1.3% growth, and the value excluding fuel sales experienced an even more robust growth of 2.0%.

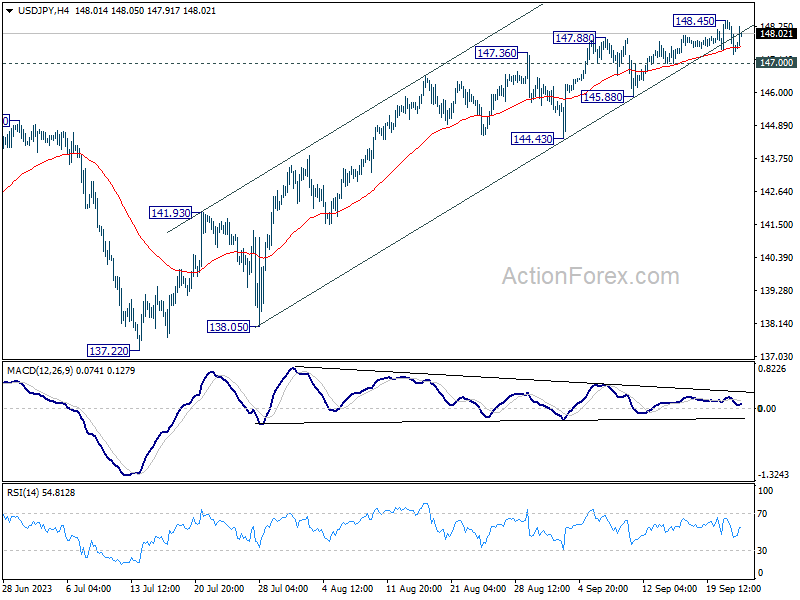

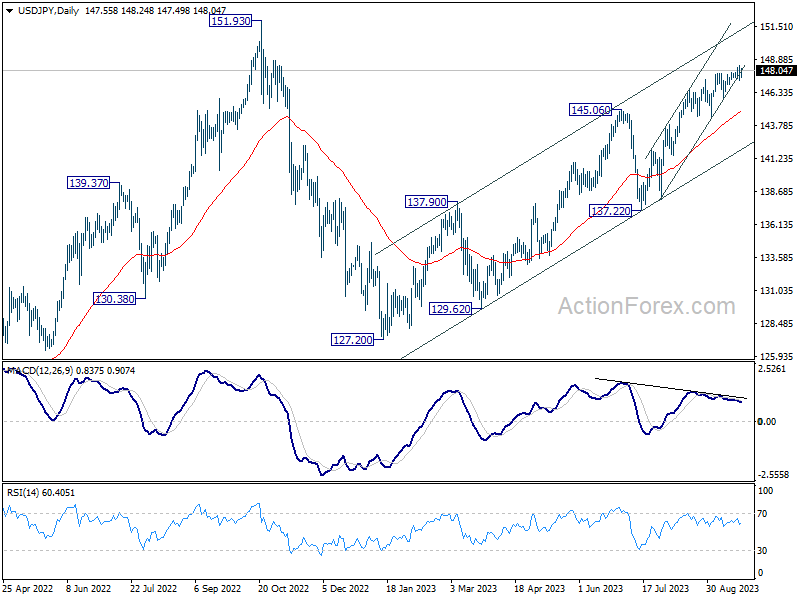

USD/JPY Daily Outlook

Daily Pivots: (S1) 147.10; (P) 147.78; (R1) 148.24; More...

USD/JPY dipped to 147.31 but quickly recovered. Intraday bias is turned neutral first. For now, further rally is in favor as long as 147.00 support holds. Above 148.45 will resume larger rally from 127.20. Next target is 151.93 high. However, firm break of 147.00 will should confirm short term topping, and turn bias to the downside for 145.88 support and below.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by break of 137.22 support will indicate that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

Yen Down on Silent BoJ; DOW Stares at Key Support in Week’s Finale

In a move that left many market observers bemused, Yen declined in Asian trading session after BoJ opted for continuity, leaving its monetary policy untouched. Notably, the bank refrained from dropping any hints about potential alterations in its policy stance in the foreseeable future. With US 10-year yield surging to a remarkable 16-year high, Yen may face further selling pressure in the coming sessions. Meanwhile, attention is shifting to forthcoming PMI releases from major economies, including Eurozone, UK, and US, as the week approaches its end.

Reflecting on the week's performance, both Sterling and Swiss Franc have been the laggards, affected by decisions of BoE and SNB to maintain their policies unchanged. The anticipation is growing that these central banks might have reached the apex of their tightening cycles already. Trailing closely behind in terms of weakness is Yen. New Zealand Dollar has emerged as the top performer, followed by Canadian Dollar and US Dollar. Euro and Australian Dollar are exhibiting a mixed performance.

Technically, in light of Fed's hawkish stance this week, market players are keenly watching for signs of escalating risk aversion. If DOW plunges below 34092.22 support level and wraps up the week beneath it, it would not only signify a renewed decline from 15679.13 but also set a bearish tone that extends into Q4, potentially aiming for 31429.82 support.

In Asia, at the time of writing, Nikkei is down -0.43%. Hong Kong HSI is up 0.86%. China Shanghai SSE is up 0.67%. Singapore Strait Times is up 0.05%. Japan 10-year JGB yield is down -0.0037 at 0.750. Overnight, DOW dropped -1.08%. S&P 500 dropped -1.64%. NASDAQ dropped -1.82%. 10-year yield surged 0.131 to 4.480.

BoJ stands pat, drops no hint on future adjustment

BoJ maintains a steady course today and keeps monetary policy unchanged. It also chooses choosing not to make any adjustments in the statement that would suggest a departure from its existing negative interest rate stance or the yield curve control measures. The central bank even retains the pledge that it "will not hesitate to take additional easing measures if necessary."

In unanimous decisions, short-term policy interest rate is held at -0.10%. 10-year JGB yield target is held at 0%, with a band of plus and minus 0.5%. Moreover, the bank's offer to purchase 10-year JGBs at a rate of 1.0% daily through fixed-rate market operations remains unchanged.

BoJ anticipates the Japanese economy to maintain a moderate recovery in the near term. However, it has also flagged concerns, noting that the economy is "under downward pressure stemming from a slowdown in the pace of recovery in overseas economies." Beyond this phase, the central bank is optimistic that the economy will exhibit growth "at a pace above its potential growth rate" due to the strengthening of a "virtuous cycle from income to spending."

Regarding inflation, BoJ foresees the year-on-year core CPI to "decelerate" owing to diminishing import price effects. Nevertheless, in the subsequent period, the CPI is projected to "accelerate again moderately", spurred by an improving output gap, along with rising medium-to-long-term inflation expectations and wage growth.

Released earlier, Japan headline CPI slowed slightly from 3.3% yoy to 3.2% yoy in August. CPI core (ex-food) was unchanged at 3.1% yoy. CPI core-core (ex food and energy) was unchanged at 4.3% yoy.

Japan's PMI manufacturing fell to 48.6, slackening demand and lower employment

Japan's Manufacturing PMI further declined from 49.6 to 48.6 in September, falling short of the anticipated 49.9, marking the most pronounced contraction since February. PMI Services also receded from 54.3 to 53.3. PMI Composite, which gives a holistic view of the broader economy, tapered off from 52.6 to 51.8.

Usamah Bhatti, an Economist at S&P Global Market Intelligence, noted that the future doesn't seem particularly rosy, with forward-looking indicators hinting at a possible slackening of demand and activity. While service firms did experience a rise, manufacturing segment reported a sharp decline in new orders, the most pronounced in seven months.

Another worrisome development is the reduced employment levels in the private sector. Bhatti stated, "As pressure on capacity eased, there was a renewed reduction in employment levels." This trend was "the first since the start of the year and the quickest since August 2020." He attributed this to companies not replacing those who voluntarily exited, often as a strategy "amid elevated cost burdens."

Australia PMI composite back to expansion, risk of "no land" for the economy

In September, Australia's Manufacturing PMI slipped to a 3-month low, declining from 49.6 to 48.2. In contrast, PMI Services showcased resilience, rising from 47.8 to a 4-month high of 50.5. PMI Composite also surged from 48.0 to 50.2, a 4-month peak, signaling a return to expansion in the broader economy.

Warren Hogan, Chief Economic Advisor at Judo Bank,said that "demand in the economy is holding up, and business activity remains on a sound footing." He further remarked that, contrary to some expectations, the present economic scenario isn't about choosing between a "hard or soft landing." Instead, he proposed that the real risk is of "no landing" for the economy.

Hogan further touched upon the inflation concerns that have been a pivotal discussion in financial circles. "The inflation indicators remain elevated at levels pointing to above-target CPI over the next 6-9 months," he stated. He pointed out that input prices remained unchanged in September, hinting at continued cost pressures. However, the final prices index experienced a slight dip in the September flash report. Despite this marginal decline, Hogan suggested that "inflation over the second half of 2023 could be higher than desired."

This latest PMI data follows a trend of stronger-than-predicted figures emerging from Australia in recent weeks. While this demonstrates economic stamina and persisting inflation, all eyes are on RBA's next steps. Hogan postulates that the RBA Board, under leadership of the new Governor Michele Bullock, will likely adopt a patient stance. However, he doesn't rule out further monetary tightening, possibly "in early November on Melbourne Cup day," should the economic indicators not align with RBA's projections of a slowdown.

New Zealand's trade data sees China dominates decline in exports and imports

In August, New Zealand observed a dip in both its goods exports and imports compared to the previous year, leading to a monthly trade deficit of NZD -2.3B.

Compared to figures from August 2022, goods exports saw a reduction of NZD -296m, marking a -5.6% yoy drop, settling at NZD 5.0B. On the other hand, goods imports displayed an even steeper decline, shrinking by NZD -639m or -8.1% yoy, amounting to NZD 7.3B.

A deeper dive into the export figures revealed China as the major contributor to the monthly dip. Exports to China fell sharply by NZD -262m, representing an -18% yoy decline. Other notable declines were witnessed in exports to Australia, which dipped by NZD -71m (-9.0% yoy), and Japan, with a decrease of NZD -34m (-11% yoy). However, there was some silver lining with US and EU. Exports to the USA grew by NZD 62m, marking a 9.6% yoy increase, and those to the EU surged by NZD 28m, a 7.7% yoy rise.

China also took the lead in the contraction in imports. Imports from China plummeted by NZD -363m, a stark -19% yoy decline. Other significant reductions in imports were observed from Australia, down by NZD -92m (-9.7% yoy), South Korea with a drop of NZD -74m (-13% yoy), and US decreasing by NZD -36m (-5.4% yoy). In contrast, imports from EU displayed a robust growth, climbing by NZD 120m or 12% yoy.

ECB's Lane: 4% deposit rate can bring inflation back to target within projection horizon

ECB's Chief Economist, Philip Lane, offered insights into last week's rate hike during a speech overnight. He noted that "the choice between holding at 375 and moving to 400 was finely balanced," referring to the deposit rate. Lane went on to express that opting for an additional hike was a safer decision "at a margin".

He believed that 4% deposit rate should be "consistent with a return of inflation to target within the projection horizon." The condition is that it's to be " maintained for a sufficiently long duration".

Looking to the future, Lane cautioned about the extended phase of uncertainty that looms regarding the disinflation process. Highlighting the intricacies of the present economic climate, Lane pointed to the "initial inflation shock, the lagged nature of wage adjustment in the euro area, [and] the considerable sectoral rebalancing" as contributors to the prolonged period of inflation uncertainty.

Looking ahead

UK retail sales and PMIs will be featured in European session together with Eurozone PMIs. Later in the day, Canada will release retail sales while US will publish PMIs too.

USD/JPY Daily Outlook

Daily Pivots: (S1) 147.10; (P) 147.78; (R1) 148.24; More...

USD/JPY dipped to 147.31 but quickly recovered. Intraday bias is turned neutral first. For now, further rally is in favor as long as 147.00 support holds. Above 148.45 will resume larger rally from 127.20. Next target is 151.93 high. However, firm break of 147.00 will should confirm short term topping, and turn bias to the downside for 145.88 support and below.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by break of 137.22 support will indicate that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Aug | -2291M | -1107M | -1177M | |

| 23:00 | AUD | Manufacturing PMI Sep P | 48.2 | 49.6 | ||

| 23:00 | AUD | Services PMI Sep P | 50.5 | 47.8 | ||

| 23:01 | GBP | GfK Consumer Confidence Sep | -21 | -27 | -25 | |

| 23:30 | JPY | National CPI Y/Y Aug | 3.20% | 3.30% | ||

| 23:30 | JPY | National CPI ex-Fresh Food Y/Y Aug | 3.10% | 3.00% | 3.10% | |

| 23:30 | JPY | National CPI ex Food Energy Y/Y Aug | 4.30% | 4.30% | ||

| 00:30 | JPY | Manufacturing PMI Sep P | 48.6 | 49.9 | 49.6 | |

| 02:52 | JPY | BoJ Interest Rate Decision | -0.10% | -0.10% | -0.10% | |

| 06:00 | GBP | Retail Sales M/M Aug | 0.50% | -1.20% | ||

| 07:15 | EUR | France Manufacturing PMI Sep P | 46 | 46 | ||

| 07:15 | EUR | France Services PMI Sep P | 46 | 46 | ||

| 07:30 | EUR | Germany Manufacturing PMI Sep P | 39.5 | 39.1 | ||

| 07:30 | EUR | Germany Services PMI Sep P | 47.1 | 47.3 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Sep P | 44 | 43.5 | ||

| 08:00 | EUR | Eurozone Services PMI Sep P | 47.5 | 47.9 | ||

| 08:30 | GBP | Manufacturing PMI Sep P | 43 | 43 | ||

| 08:30 | GBP | Services PMI Sep P | 49 | 49.5 | ||

| 12:30 | CAD | Retail Sales M/M Jul | 0.40% | 0.10% | ||

| 12:30 | CAD | Retail Sales ex Autos M/M Jul | 0.50% | -0.80% | ||

| 13:45 | USD | Manufacturing PMI Sep P | 47.8 | 47.9 | ||

| 13:45 | USD | Services PMI Sep P | 50.3 | 50.5 |

Cliff Notes: Policy Takes Effect, But Global Risks Remain

Key insights from the week that was.

The September RBA meeting minutes presented a detailed account of the Board’s deliberations and their assessment of risks. In recent months, the Board has stopped describing its considerations for policy – the choice between remaining on hold and a rate hike – as “finely balanced”. Rather, it has become increasingly clear that the Board view the case for remaining on hold as the “stronger” argument, in step with their growing confidence in navigating a soft landing. While the Board still conclude that “some further tightening in policy may be required should inflation prove more persistent than expected”, the hurdle for the Q3 CPI report or interim Monthly CPI Indicators to raise alarm is high. Westpac remains of the view that the RBA will remain on hold until August 2024 when we see the next rate cutting cycle begin, to restore balance to demand conditions and support growth’s return towards trend.

The Q3 Westpac-ACCI Survey of Industrial Trends demonstrated that the RBA’s rapid tightening cycle is having a material impact on Australian industry. At 51.3, the Westpac-ACCI Actual Composite signals conditions are approaching stall speed. Indeed, that new orders growth held flat for a second consecutive quarter and is now the number one concern of manufacturers is consistent with the marked slowing of the Australian economy. Within this context, firms report there is little incentive to grow their workforce or lift their investment intentions despite an easing in labour and material shortages. Overall, the tone of the survey remains broadly downbeat, with expectations for future activity in the sector subdued – adding to the case for the RBA to remain on hold.

Central bank meetings dominated the news offshore.

The FOMC kept the fed funds rate at 5.375%; however, the dot plot suggests most members expect the data to justify one last hike before the end of the year. During Q&A, Chair Jerome Powell said 'we need to see more progress' when speaking to why they felt a further hike could be on the cards. On balance, the FOMC expects the upside surprise to growth currently being experienced in 2023 to persist into 2024, the GDP forecast for next year revised up from 1.1% to 1.5%. The unemployment rate is also only expected to lift at the margin from now to end-2024, from 3.8% to 4.1%, while PCE inflation is expected to only slowly trend down to 2.5% at end-2024. Consequently, the FOMC now expects only 50bps of cuts in 2024 from 5.625% at end-2023.

While they do anticipate a further reduction in inflation and the fed funds rate in 2025 and 2026, it is again expected to be slow going and still leaves the fed funds rate above their longer run estimate of neutral, 2.5%. We see the US economy disappointing the FOMC’s expectations in coming months and so anticipate an earlier and larger start to the cutting cycle, pencilling in 100bps of rate cuts in 2024 versus the FOMC's 50bps. However, we also perceive greater inflation risks in the out years and so, at 3.375%, our end-2025 fed funds forecast is also materially above the FOMC’s 2.5% ‘longer run’ figure. In our view, these inflation risks are likely to primarily be structural rather than cyclical, limiting the effectiveness of policy and, at the margin, creating greater risk for activity growth and the labour market. Highlighting this, through 2025, we see the unemployment rate holding around 5.0% and GDP growth remaining below trend.

Overnight, the Bank of England paused for the first time since they started hiking in 2021 in a divided vote -- five voted to remain on hold, while four voted to hike. The pause came as a surprise to economists, but market pricing had drawn much closer to the final result after the last CPI release. In August, annual inflation growth fell to 6.7%yr as the monthly gain only partially made up for July’s fall, bringing the three-month average to flat. The contribution from services nudged down to 3.2% -- just under half of total CPI. Goods also decelerated further, much to the surprise of the BoE. August was the second month that headline CPI undershot the BoE's forecast of 6.93% for Q3 (July's print was an undershoot at the second decimal place). Higher fuel costs have been observed in inflation prints in US and Europe, but they did not add as much pressure to the headline print for the UK in monthly terms and were a dampening influence in the annual print. Reports suggest this may be a result of a more delayed response to the spike in oil prices. Overall, the percentage of the CPI basket running above the BoE's 2% target has trickled down to 81% over July and August.

In addition to the weaker-than-expected CPI, the Committee was concerned about the growth outlook following a 0.5%mth decline in GDP in July. This followed other indicators which suggest weaker growth can be expected in the near term. Strong wages growth had seen economists anticipate further hikes. However, while the Average Weekly Earnings figures continue to overshoot the Bank's forecasts, they were characterised as “difficult to reconcile with other indicators of pay growth”. The Decision Maker Panel data, frequently referenced by Governor Andrew Bailey, suggests wages growth has been stable at 5%. As such, the Committee will be looking at broader measures of wages ahead.

The statement noted that the current stance was “restrictive” and that “Further tightening in monetary policy would be required if there were evidence of more persistent inflationary pressures”. Before the November meeting, we will get two CPI prints and another wages read which may allay or fuel the hawks' fears. Hawk Sir Jon Cunliffe will also be leaving and BoE internal Sarah Breeden arriving. Breeden has said she will have a more 'balanced' approach to monetary policy.

Across the Tasman, New Zealand's Q2 GDP rose 0.9%qtr, materially above the market’s and RBNZ’s expectation but in line with our New Zealand team’s view. The technical recession through December and March quarters was also revised away and puts the economy 0.5% larger than the RBNZ expected in August. Given the revisions and Q2 GDP print, we continue to expect the RBNZ to hike once more by year end. The market is also coming to this view, although it is currently priced for this last hike to occur in early-2024.