Sample Category Title

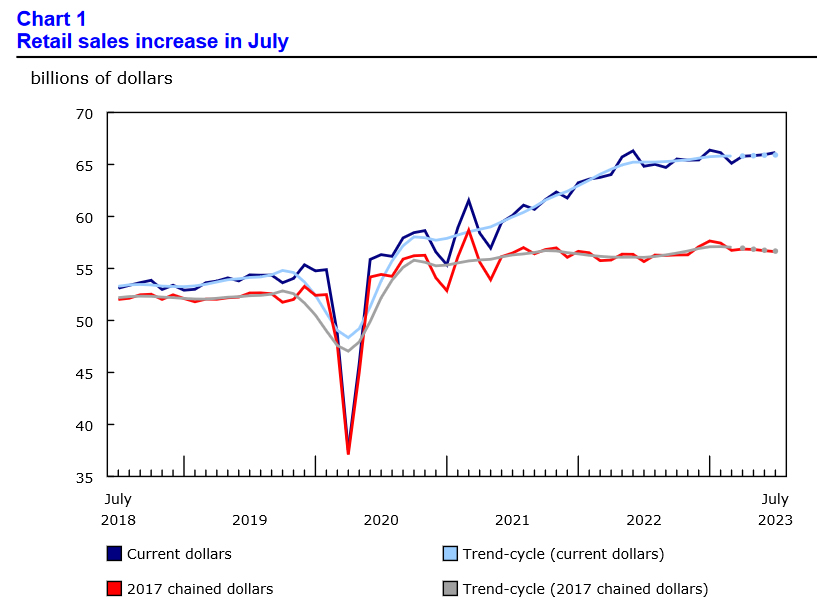

Canadian Retail Sales Rebounded in July, But Declined in Real Terms

Retail sales rose 0.3% month-on-month (m/m) in July, coming in a tad weaker than 0.4% m/m reported in Statistics Canada's advance estimate. June's print remained unchanged at 0.1% m/m.

Adjusting for inflation, the volume of retail sales was 0.2% lower on the month.

Sales at motor vehicle and parts dealers fell by 1.6% m/m – the first decline in four months. But this weakness comes on the back of a 1.4% gain on average over the past three months.

Sales growth at gasoline stations and fuel vendors were 0.7% lower relative to June. In volumes terms, receipts were down 1.0% m/m in July. We expect to see a reversal in August as gas prices accelerated recently.

Excluding sales at car dealerships and gas stations, core retail sales rebounded strongly in July with a reading of 1.3% m/m that exceeded the consensus estimate of 0.5% m/m. However, the three month average remained at 0.1% in July

Strength in core sales was broad-based and led by food and beverage stores (+1.3% m/m) and general merchandise retailers (+1.8% m/m).

No core category reported losses in July, but Statistics Canada reports that approximately 17% of Canadian retailers were affected by the strike at the ports in British Columbia.

E-commerce sales gained a whopping 2.4% m/m in July on the back of an upwardly revised gain of 3.4% m/m in June (from 1.1% m/m reported earlier).

The advanced estimate for the month of August points to a decline of 0.3% m/m. This is in line with our own estimate of consumer activity based on TD debit/credit card spending.

Key Implications

Retail trade entered the third quarter on a decent footing with solid gains in core categories – revealing a reacceleration in spending momentum from an essentially flat second quarter. But that pick up is modest by historical standards, with real consumer spending tracking 1.4% quarter-on-quarter (annualized) for the third quarter, as outlined in our recent Quarterly Economic Forecast.

Monetary policy's long and variable lags are leaving a permanent mark on the Canadian consumer. By the Bank of Canada's estimates, roughly 50% of mortgages that were initiated before they started raising interest rates last year will face higher rates by the end of this year. Meanwhile, families who rely on a more interest-rate sensitive consumer credit have already fully experienced the bitterness of higher rate medicine, and retail sales in real terms are softening. We think that weaker demand will translate into cooler inflation in the coming months, enabling the BoC to will remain on hold for the rest of the year.

Canadian Dollar Edges Higher as Retail Sales Rebound

- Canada retail sales climb 2%

The Canadian dollar has posted losses on Friday. In the European session, USD/CAD is trading at 1.3446, down 0.28%.

Canada’s retail sales jump

Canada’s retail sales rebounded in impressive fashion on Friday. Retail sales in July jumped 2% y/y, following a -0.6% reading in June and beating the 0.5% consensus estimate. On a monthly basis, retail sales rose 0.3%, up from 0.1% in June but shy of the consensus estimate of 0.4%. The good news was tempered by the August estimate, which stands at -0.3% m/m and would be the first decline since March. The Canadian dollar showed little reaction to the retail sales release.

The Bank of Canada doesn’t meet again until October 25th and policy makers will have plenty of data to monitor in the meantime. The BoC has been walking a tightrope that will be familiar to most central banks, that of trying to balance the risks of over and under-tightening. The difficulty in finding the right balance was highlighted in the BoC summary of deliberations of the policy meeting earlier this month.

The BoC decided to hold the benchmark rate at 5.0% after concluding that earlier rate hikes were having an effect and slowing economic growth. The summary indicated that policy makers were concerned that a pause might send the wrong message that rate cuts might be on the way. With inflation still above the BOC’s target, the central bank is not looking at rate cuts and stressed at the September meeting that rate hikes were still on the table and that inflation remained too high.

USD/CAD Technical

- USD/CAD is testing resistance at 1.3468. The next resistance line is 1.3553

- 1.3408 and 1.3323 are the next support lines

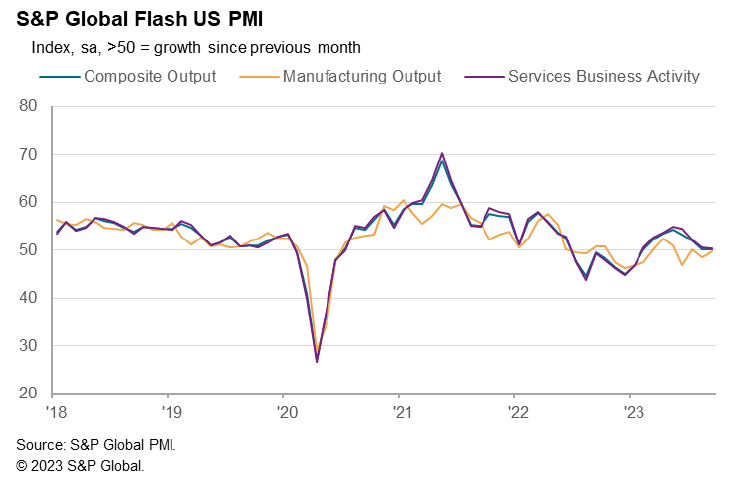

US PMI composite ticks down to 50.1, broad stagnation in total activity

US PMI Manufacturing rose from 47.9 to 48.9 in September. PMI Services fell from 50.5 to 50.2, an 8-month low. PMI Composite fell from 50.2 to 50.1, a 7-month low.

Siân Jones, Principal Economist at S&P Global Market Intelligence said:

"PMI data for September added to concerns regarding the trajectory of demand conditions in the US economy following interest rate hikes and elevated inflation. Although the overall Output Index remained above the 50.0 mark, it was only fractionally so, with a broad stagnation in total activity signalled for the second month running. The service sector lost further momentum, with the contraction in new orders gaining speed.

"Subdued demand did not translate into overall job losses in September as a greater ability to find and retain employees led to a quicker rise in employment growth. That said, the boost to hiring from rising candidate availability may not be sustained amid evidence of burgeoning spare capacity and dwindling backlogs which have previously supported workloads.

"Inflationary pressures remained marked, as costs rose at a faster pace again. Higher fuel costs following recent increases in oil prices, alongside greater wage bills, pushed operating expenses up. Weak demand nonetheless placed a barrier to firms' ability to pass on greater costs to clients, with prices charged inflation unchanged on the month."

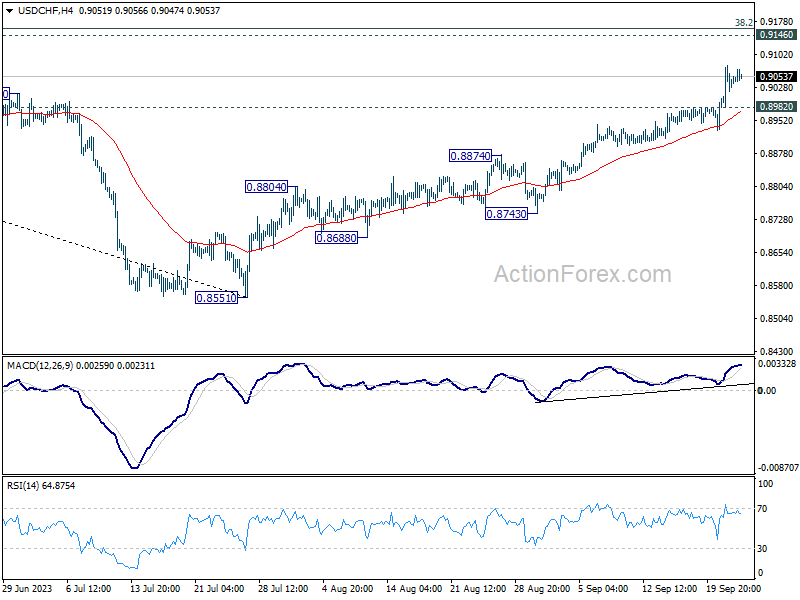

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8991; (P) 0.9035; (R1) 0.9090; More....

USD/CHF's rise from 0.8551 is still in progress. Intraday bias remains on the upside for 0.9146 cluster resistance. On the downside, break of 0.8982 minor support will turn intraday bias neutral first. But further rally will remain in favor as long as 0.8874 resistance turned support holds, in case of retreat.

In the bigger picture, rebound from 0.8551 medium term bottom is currently seen as a correction to the downtrend from 1.0146 (2022 high). Further rally would be seen to 0.9146 cluster resistance (38.2% retracement of 1.0146 to 0.8551 at 0.9160). Strong resistance could be seen there to limit upside, at least on first attempt.

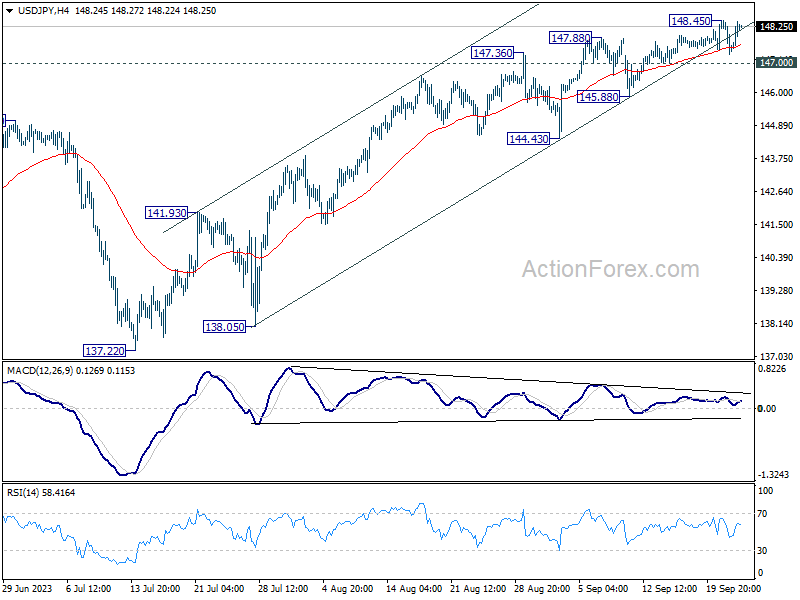

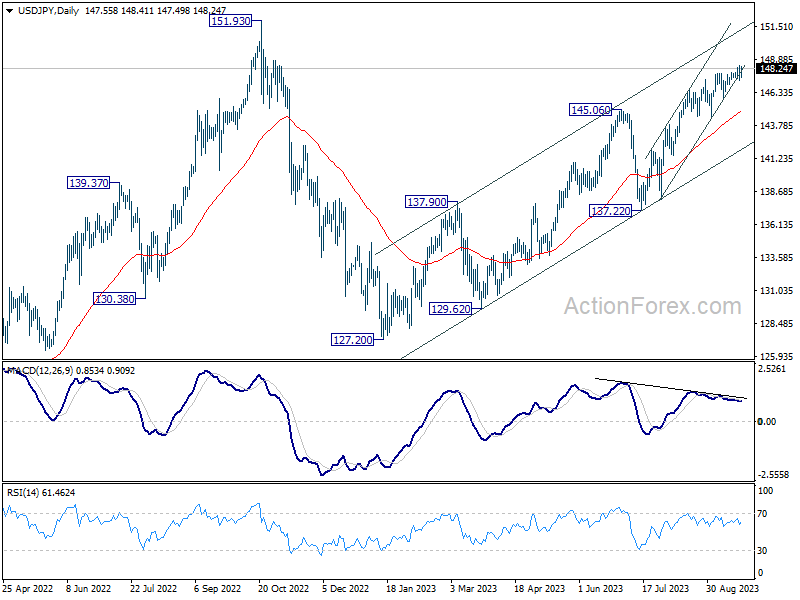

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.10; (P) 147.78; (R1) 148.24; More...

Intraday bias in USD/JPY remains neutral but further rally is in favor with 147.00 support intact. Above 148.45 will resume larger rally from 127.20. Next target is 151.93 high. However, firm break of 147.00 will should confirm short term topping, and turn bias to the downside for 145.88 support and below.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by break of 137.22 support will indicate that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

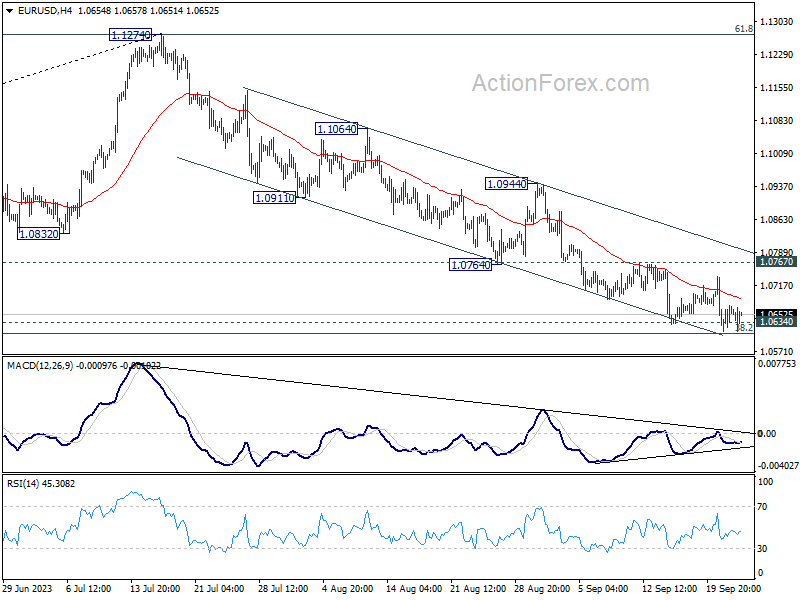

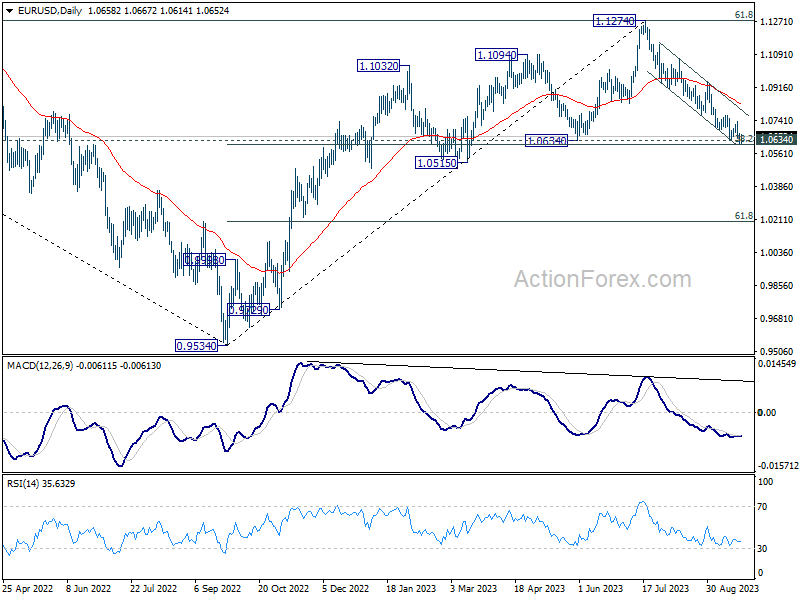

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0627; (P) 1.0651; (R1) 1.0684; More...

No change in EUR/USD's outlook and intraday bias stays neutral for the moment. On the downside, sustained break of 1.0609/34 support zone will carry larger bearish implication. Fall from 1.1274 should then target target 1.0515 support next. Nevertheless, strong rebound from current level, followed by break of 1.0767 resistance, should confirm short term bottoming. Intraday bias will be back on the upside for 1.0944 resistance.

In the bigger picture, fall from 1.1274 medium term top is seen as a correction to up trend from 0.9534 (2022 low). Strong support could be seen from 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609) to bring rebound, at least on first attempt. However, sustained break of 1.0609/0634 will raise the chance of bearish trend reversal, and target 61.8% retracement at 1.0199.

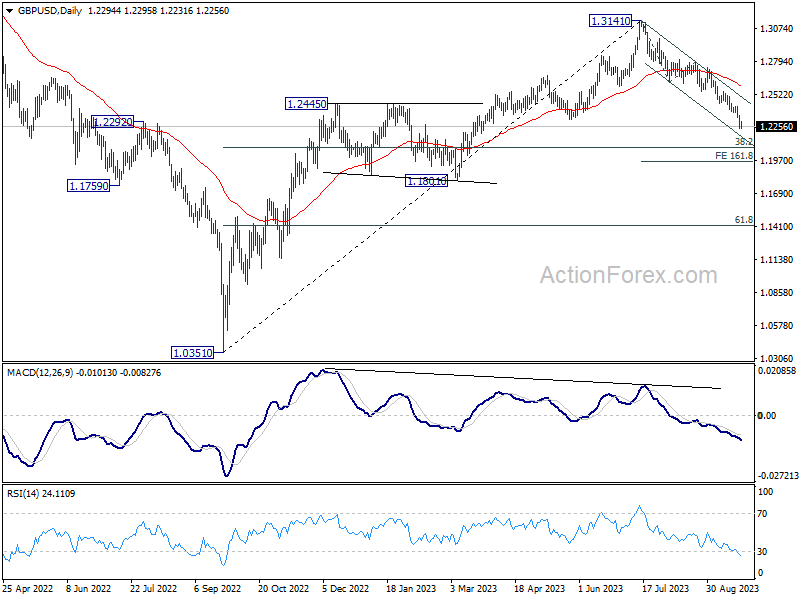

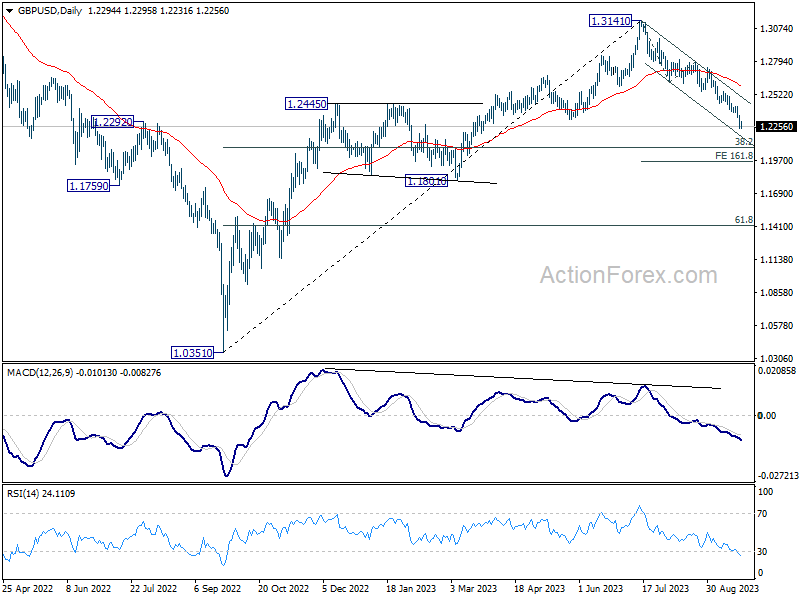

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2237; (P) 1.2293; (R1) 1.2352; More...

GBP/USD's decline continues today and intraday bias stays on the downside. Current fall from 1.3141 should target 1.2075 fibonacci level. On the upside, above 1.2369 minor resistance will turn intraday bias neutral and bring consolidations. But near term outlook will stay bearish as long as 1.2618 support turned resistance holds, in case of strong recovery.

In the bigger picture, fall from 1.3141 medium term top is seen as a correction to up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3141 at 1.2075. Strong support would be seen there to bring rebound on first attempt. However, sustained break of 1.2075 will raise the chance of bearish trend reversal.

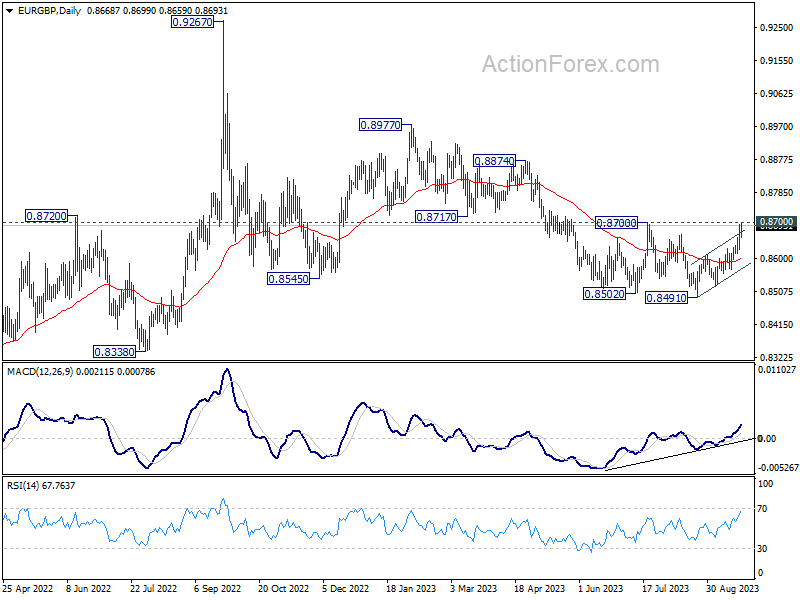

Euro and Pound Feel PMI Squeeze, While Yen’s Descent Continues

Yen languishes as the day's worst performer, with sentiments taking a hit due to BoJ's silence on potential policy tweaks. European majors aren't faring much better, as subpar PMI data from both Eurozone and UK echo the sentiment that further tightening might not be on the cards for ECB and BoE. The Swiss Franc also feels the pressure, even if the pace of its earlier slide has decelerated.

Conversely, commodity currencies are flexing their muscles, spearheaded by the New Zealand Dollar. The notable rebound in Hong Kong stocks could be providing a boost to both Aussie and Kiwi. Enthusiasm is mounting over the possibility of China's economic recovery picking up pace during the latter part of the year. Meanwhile, Dollar offers a mixed performance, battling to re-establish its momentum against the likes of the Yen and the Euro.

Technically, as the week comes to a close, a focus will be on whether EUR/GBP could close above 0.8700 resistance. If realized, that would be an indication what fall from 0.8977 has completed, as well as the three wave down trend from 0.9267. That would set the stage for more medium term rally back to 0.8977 resistance levels.

In Europe, at the time of writing, FTSE is up 0.65%. DAX is up 0.00%. CAC is down -0.41%. Germany 10-year yield is up 0.013 at 2.752. Earlier in Asia, Nikkei dropped -0.52%. Hong Kong HSI rose 2.28%. China Shanghai SSE is rose 1.55%. Singapore Strait Times dropped -0.33%. Japan 10-year JGB yield dropped -0.0041 to 0.749.

Canada retail sales rose 0.3% mom in Jul, missed expectations

retail sales rose 0.3% mom to CAD 66.1B in July, below expectation of 0.4% mom. Core retail sales—which exclude gasoline stations and fuel vendors and motor vehicle and parts dealers—were up 1.3% mom. In volume terms, retail sales was down -0.2% mom.

Advance estimate suggests that sales declined -0.3% mom in August.

Eurozone PMIs point to -0.4% GDP contraction in Q3

Eurozone Manufacturing PMI was slightly disappointing in September, dipping from 43.5 to 43.4, failing to meet expectations set at 44.0. On the other hand, Services PMI indicated a slight revival, progressing from 47.9 to 48.4, surpassing the anticipated 47.5. Composite PMI reflected this marginal uplift, moving from 46.7 to 47.1.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank predicts a contraction for Eurozone in the third quarter, with a potential decrease of -0.4% relative to the previous quarter.

In services sector, "the heat on input prices shows that the risk of a wage-price spiral must remain very much on the radar of the ECB." Manufacturing continues to be a drag. But "destocking process" may bottom out over the next few months, which is crucial for the manufacturing sector's recovery for the beginning of next year.

Making a comparison between the two European giants, de la Rubia pointed out that while the French manufacturing sector "catching up" with Germany's weaknesses. When it comes to services, France's sector is "in a much worse state".

Germany PMI Manufacturing saw a slight climb from 39.1 to 39.8. Similarly, PMI Services edged up from 47.3 to just below the 50 mark at 49.8. Composite PMI experienced an uptick, moving from 44.6 to 46.2.

France PMI Manufacturing slumped to 43.6 in September, marking a 40-month low. PMI Services and Composite figures too painted a grim picture, both plummeting to a 34-month low, with values of 43.9 and 43.5, respectively.

UK PMI composite fell to 46.0, heightened recession risk supports BoE pause

UK PMI Manufacturing sector had a slight uptick in September, moving from 43.0 to 44.2, surpassing expectations set at 43.0. Services PMI disappointed, recording a drop from 49.5 to 47.2, underperforming against the forecasted 49.0, marking a 32-month low. Consequently, PMI Composite followed suit, declining from 48.6 to 46.8, also registering a 32-month low.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, stated, "The disappointing PMI survey results for September mean a recession is looking increasingly likely in the UK."

The current PMI data aligns with a potential GDP contraction of over -0.4% on a quarterly basis. Williamson mentioned, "September's downturn is the steepest since the height of the global financial crisis in early 2009 barring only the pandemic lockdown months."

A significant point of apprehension in the inflation framework remains wage growth. However, with the survey indicating the most significant employment decline since 2009, wage negotiation leverage appears to be dwindling swiftly.

Williamson believes the unsettling indications of heightened recession risk coupled with diminishing inflationary pressures are likely to have "added to calls to halt rate hikes" by BoE.

UK sales volume up 0.4% mom, sales value up 0.8% mom

UK retail sales showed some growth in August, albeit falling short of market expectations. On a month-on-month basis, sales volumes increased by 0.4% mom, slightly under the anticipated 0.5% rise. When removing the impact of fuel, the volume rose by a slightly better 0.6% mom. In terms of the monetary value, sales were up 0.8% mom, with the figures excluding fuel at 0.7% mom.

Taking a step back to analyze a broader timeframe, the three-month period leading up to August 2023 witnessed a 0.3% rise in sales volumes compared to the previous three months. Same growth of 0.3% was observed for volumes that excluded auto sales. In value terms, the increase was more pronounced with a 1.3% growth, and the value excluding fuel sales experienced an even more robust growth of 2.0%.

BoJ stands pat, drops no hint on future adjustment

BoJ maintains a steady course today and keeps monetary policy unchanged. It also chooses choosing not to make any adjustments in the statement that would suggest a departure from its existing negative interest rate stance or the yield curve control measures. The central bank even retains the pledge that it "will not hesitate to take additional easing measures if necessary."

In unanimous decisions, short-term policy interest rate is held at -0.10%. 10-year JGB yield target is held at 0%, with a band of plus and minus 0.5%. Moreover, the bank's offer to purchase 10-year JGBs at a rate of 1.0% daily through fixed-rate market operations remains unchanged.

BoJ anticipates the Japanese economy to maintain a moderate recovery in the near term. However, it has also flagged concerns, noting that the economy is "under downward pressure stemming from a slowdown in the pace of recovery in overseas economies." Beyond this phase, the central bank is optimistic that the economy will exhibit growth "at a pace above its potential growth rate" due to the strengthening of a "virtuous cycle from income to spending."

Regarding inflation, BoJ foresees the year-on-year core CPI to "decelerate" owing to diminishing import price effects. Nevertheless, in the subsequent period, the CPI is projected to "accelerate again moderately", spurred by an improving output gap, along with rising medium-to-long-term inflation expectations and wage growth.

Released earlier, Japan headline CPI slowed slightly from 3.3% yoy to 3.2% yoy in August. CPI core (ex-food) was unchanged at 3.1% yoy. CPI core-core (ex food and energy) was unchanged at 4.3% yoy.

Japan's PMI manufacturing fell to 48.6, slackening demand and lower employment

Japan's Manufacturing PMI further declined from 49.6 to 48.6 in September, falling short of the anticipated 49.9, marking the most pronounced contraction since February. PMI Services also receded from 54.3 to 53.3. PMI Composite, which gives a holistic view of the broader economy, tapered off from 52.6 to 51.8.

Usamah Bhatti, an Economist at S&P Global Market Intelligence, noted that the future doesn't seem particularly rosy, with forward-looking indicators hinting at a possible slackening of demand and activity. While service firms did experience a rise, manufacturing segment reported a sharp decline in new orders, the most pronounced in seven months.

Another worrisome development is the reduced employment levels in the private sector. Bhatti stated, "As pressure on capacity eased, there was a renewed reduction in employment levels." This trend was "the first since the start of the year and the quickest since August 2020." He attributed this to companies not replacing those who voluntarily exited, often as a strategy "amid elevated cost burdens."

Australia PMI composite back to expansion, risk of "no land" for the economy

In September, Australia's Manufacturing PMI slipped to a 3-month low, declining from 49.6 to 48.2. In contrast, PMI Services showcased resilience, rising from 47.8 to a 4-month high of 50.5. PMI Composite also surged from 48.0 to 50.2, a 4-month peak, signaling a return to expansion in the broader economy.

Warren Hogan, Chief Economic Advisor at Judo Bank,said that "demand in the economy is holding up, and business activity remains on a sound footing." He further remarked that, contrary to some expectations, the present economic scenario isn't about choosing between a "hard or soft landing." Instead, he proposed that the real risk is of "no landing" for the economy.

Hogan further touched upon the inflation concerns that have been a pivotal discussion in financial circles. "The inflation indicators remain elevated at levels pointing to above-target CPI over the next 6-9 months," he stated. He pointed out that input prices remained unchanged in September, hinting at continued cost pressures. However, the final prices index experienced a slight dip in the September flash report. Despite this marginal decline, Hogan suggested that "inflation over the second half of 2023 could be higher than desired."

This latest PMI data follows a trend of stronger-than-predicted figures emerging from Australia in recent weeks. While this demonstrates economic stamina and persisting inflation, all eyes are on RBA's next steps. Hogan postulates that the RBA Board, under leadership of the new Governor Michele Bullock, will likely adopt a patient stance. However, he doesn't rule out further monetary tightening, possibly "in early November on Melbourne Cup day," should the economic indicators not align with RBA's projections of a slowdown.

New Zealand's trade data sees China dominates decline in exports and imports

In August, New Zealand observed a dip in both its goods exports and imports compared to the previous year, leading to a monthly trade deficit of NZD -2.3B.

Compared to figures from August 2022, goods exports saw a reduction of NZD -296m, marking a -5.6% yoy drop, settling at NZD 5.0B. On the other hand, goods imports displayed an even steeper decline, shrinking by NZD -639m or -8.1% yoy, amounting to NZD 7.3B.

A deeper dive into the export figures revealed China as the major contributor to the monthly dip. Exports to China fell sharply by NZD -262m, representing an -18% yoy decline. Other notable declines were witnessed in exports to Australia, which dipped by NZD -71m (-9.0% yoy), and Japan, with a decrease of NZD -34m (-11% yoy). However, there was some silver lining with US and EU. Exports to the USA grew by NZD 62m, marking a 9.6% yoy increase, and those to the EU surged by NZD 28m, a 7.7% yoy rise.

China also took the lead in the contraction in imports. Imports from China plummeted by NZD -363m, a stark -19% yoy decline. Other significant reductions in imports were observed from Australia, down by NZD -92m (-9.7% yoy), South Korea with a drop of NZD -74m (-13% yoy), and US decreasing by NZD -36m (-5.4% yoy). In contrast, imports from EU displayed a robust growth, climbing by NZD 120m or 12% yoy.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2237; (P) 1.2293; (R1) 1.2352; More...

GBP/USD's decline continues today and intraday bias stays on the downside. Current fall from 1.3141 should target 1.2075 fibonacci level. On the upside, above 1.2369 minor resistance will turn intraday bias neutral and bring consolidations. But near term outlook will stay bearish as long as 1.2618 support turned resistance holds, in case of strong recovery.

In the bigger picture, fall from 1.3141 medium term top is seen as a correction to up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3141 at 1.2075. Strong support would be seen there to bring rebound on first attempt. However, sustained break of 1.2075 will raise the chance of bearish trend reversal.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Aug | -2291M | -1107M | -1177M | |

| 23:00 | AUD | Manufacturing PMI Sep P | 48.2 | 49.6 | ||

| 23:00 | AUD | Services PMI Sep P | 50.5 | 47.8 | ||

| 23:01 | GBP | GfK Consumer Confidence Sep | -21 | -27 | -25 | |

| 23:30 | JPY | National CPI Y/Y Aug | 3.20% | 3.30% | ||

| 23:30 | JPY | National CPI ex-Fresh Food Y/Y Aug | 3.10% | 3.00% | 3.10% | |

| 23:30 | JPY | National CPI ex Food Energy Y/Y Aug | 4.30% | 4.30% | ||

| 00:30 | JPY | Manufacturing PMI Sep P | 48.6 | 49.9 | 49.6 | |

| 02:52 | JPY | BoJ Interest Rate Decision | -0.10% | -0.10% | -0.10% | |

| 06:00 | GBP | Retail Sales M/M Aug | 0.40% | 0.50% | -1.20% | -1.10% |

| 07:15 | EUR | France Manufacturing PMI Sep P | 43.6 | 46 | 46 | |

| 07:15 | EUR | France Services PMI Sep P | 43.9 | 46 | 46 | |

| 07:30 | EUR | Germany Manufacturing PMI Sep P | 39.8 | 39.5 | 39.1 | |

| 07:30 | EUR | Germany Services PMI Sep P | 49.8 | 47.1 | 47.3 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Sep P | 43.4 | 44 | 43.5 | |

| 08:00 | EUR | Eurozone Services PMI Sep P | 48.4 | 47.5 | 47.9 | |

| 08:30 | GBP | Manufacturing PMI Sep P | 44.2 | 43 | 43 | |

| 08:30 | GBP | Services PMI Sep P | 47.2 | 49 | 49.5 | |

| 12:30 | CAD | Retail Sales M/M Jul | 0.30% | 0.40% | 0.10% | |

| 12:30 | CAD | Retail Sales ex Autos M/M Jul | 1.00% | 0.50% | -0.80% | -0.70% |

| 13:45 | USD | Manufacturing PMI Sep P | 47.8 | 47.9 | ||

| 13:45 | USD | Services PMI Sep P | 50.3 | 50.5 |

Canada retail sales rose 0.3% mom in Jul, missed expectations

Canada retail sales rose 0.3% mom to CAD 66.1B in July, below expectation of 0.4% mom. Core retail sales—which exclude gasoline stations and fuel vendors and motor vehicle and parts dealers—were up 1.3% mom. In volume terms, retail sales was down -0.2% mom.

Advance estimate suggests that sales declined -0.3% mom in August.

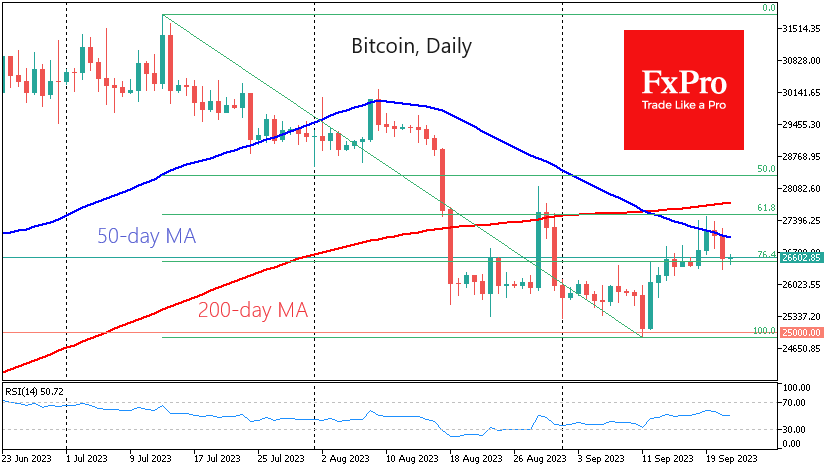

Ethereum and Bitcoin Ready to Dive

Market picture

The crypto market capitalisation has fallen to $1.056 trillion, losing around 0.9% in the last 24 hours. The main pressure on the market came from outside, as equity indices fell, with the US market losing a further 1.8% on the Nasdaq, returning to August lows. It should be noted that against such an unfavourable external backdrop, the consolidation of cryptocurrencies near the levels seen at the beginning of the week looks like a vote of confidence from crypto enthusiasts.

The bitcoin price has returned to $26.6, erasing the mini pump at the beginning of the week. The ability to hold on to last week’s support looks like a positive signal. On the other hand, we saw earlier this week that bears control the market. But they aren’t in a hurry yet.

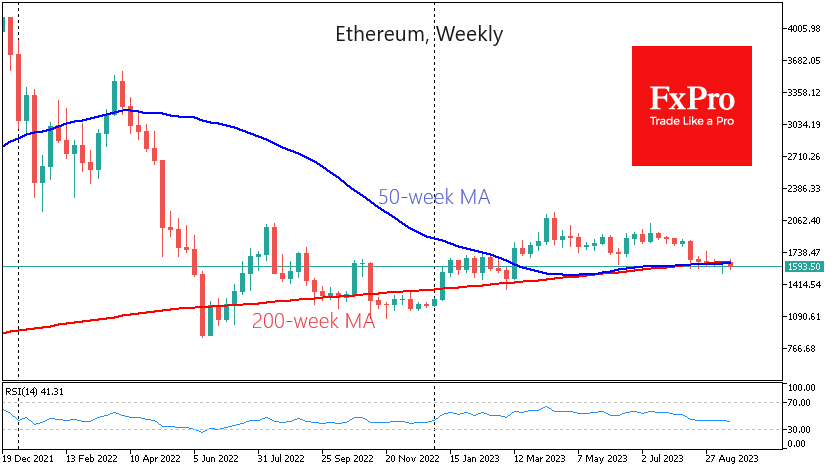

Ethereum looks weak. After five weeks of trying to stay above its 50- and 200-week moving averages, the digital silver is in danger of closing below these lines and $1600 this week. The following essential lines of defence look to be the $1500 and $1200 levels, where buyers came to the coin’s rescue in March and December last year.

News Background

Bloomberg notes that Bitcoin continues to evolve as a global payment network while carbon emissions fall. That’s what’s needed to increase adoption of the world’s first cryptocurrency.

The court allowed bankrupt cryptocurrency exchange MtGox to extend its deadline to repay creditors until 31 October 2024. These reports supported bitcoin exchange rates earlier in the week, removing a potential overhang of crypto assets from the market. MtGox’s creditors have been expecting repayment for nearly a decade, and the deadline has been pushed back several times.

According to the Wall Street Journal, Tether has increased its USDT lending again despite promising investors it would reduce it to zero by 2024. According to the paper, Tether’s inconsistent lending policy is causing serious concern among crypto investors.

Binance has warned of a possible delisting of stablecoins in Europe. This is because the exchange’s lawyers have not yet found a way to meet the requirements of the new MiCA rules adopted in the European Union.