Sample Category Title

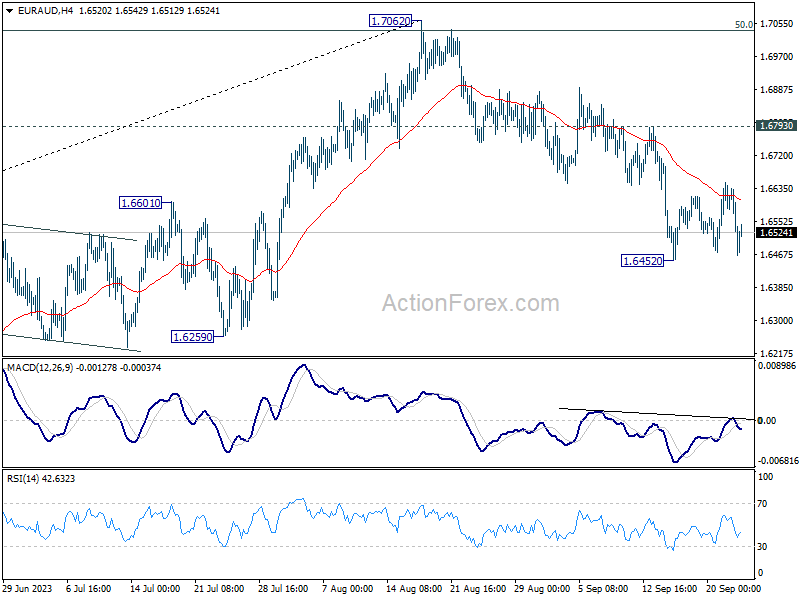

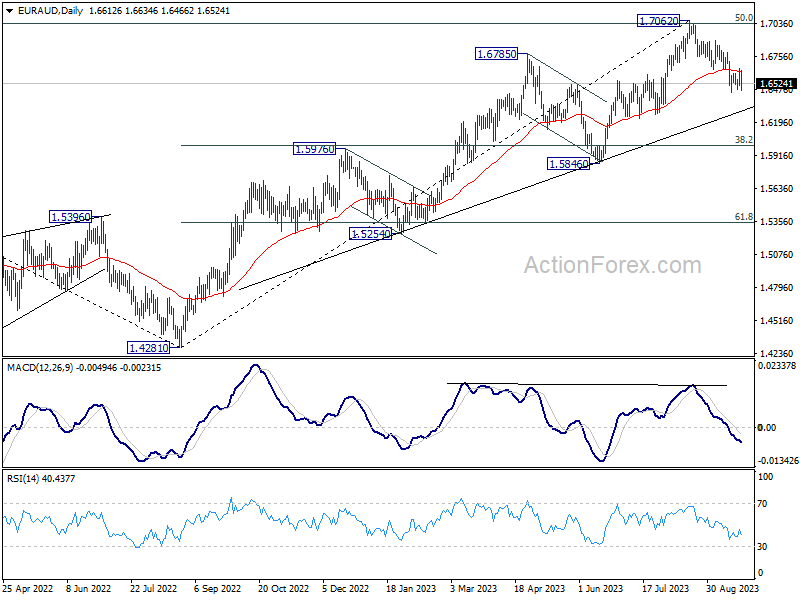

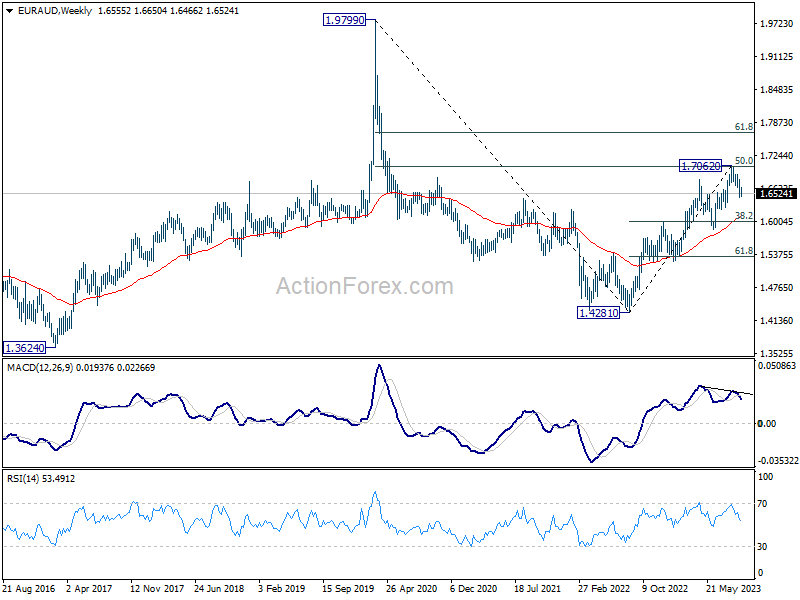

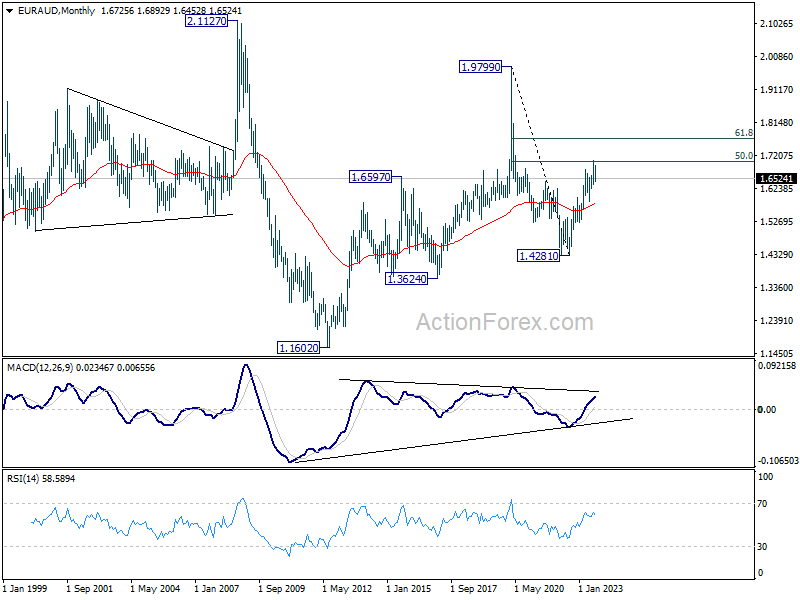

EUR/AUD Weekly Outlook

EUR/AUD turned into sideway trading above 1.6452 last week, but upside is capped well below 1.6793 resistance. Initial bias remains neutral this week first and outlook stays bearish. On the downside, break of 1.6452 will resume the fall from 1.7062, as a larger scale correction, to 1.6000 fibonacci level. Nevertheless, firm break of 1.6793 will dampen this view and bring retest of 1.7062 instead.

In the bigger picture, fall from 1.7062 is probably correcting whole up trend from 1.4281 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.4281 to 1.7062 at 1.6000. Strong support should be seen there to bring rebound, at least on first attempt.

In the longer term picture, it's still early to decide if rise from 1.4281 is resuming whole up trend from 1.1602 (2012 low). But in either case, further rally is in favor as long as 1.5846 support holds. Next target is 61.8% retracement of 1.9799 to 1.4281 at 1.7691.

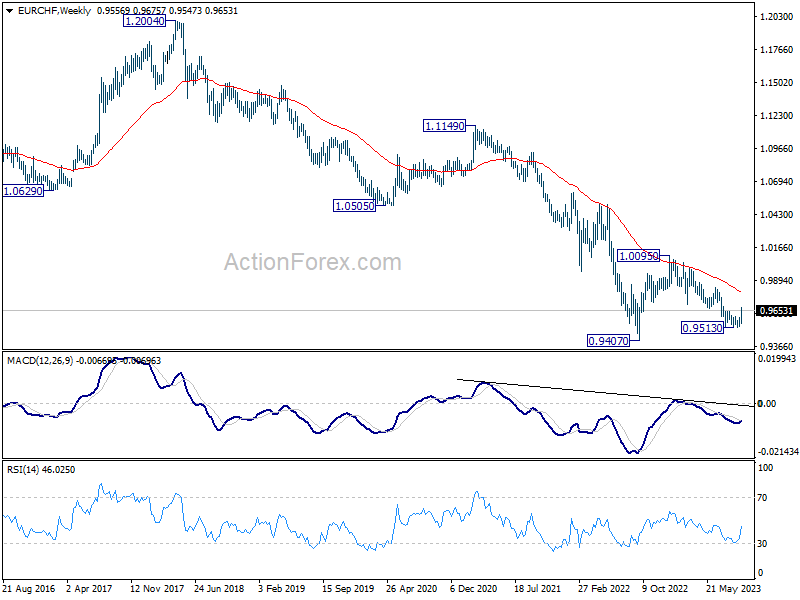

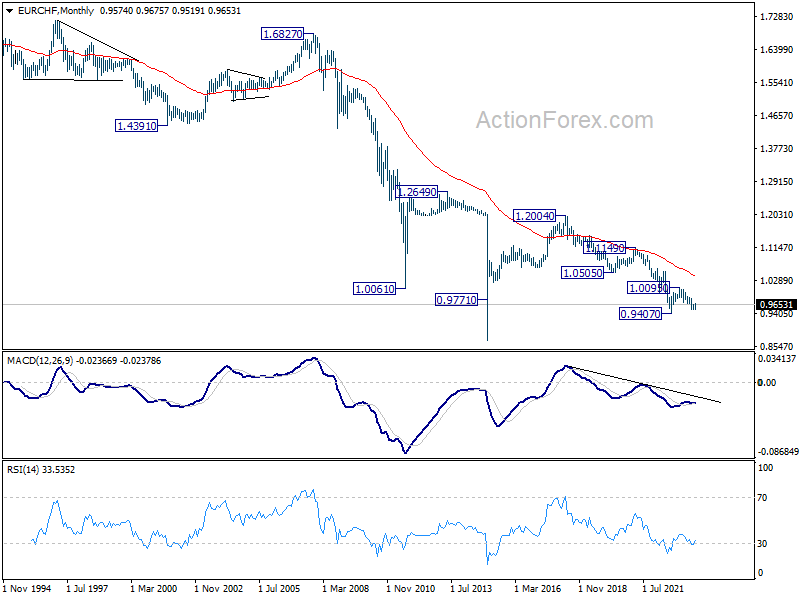

EUR/CHF Weekly Outlook

EUR/CHF's strong rebound last week argues that a medium term bottom could be in place at 0.9513, on bullish convergence condition in D MACD. Initial bias stays on the upside this week for further rally to 38.2% retracement of 1.0095 to 0.9513 at 0.9735. Sustained break there will target 61.8% retracement at 0.9873. On the downside, however, below 0.9602 minor support will dampen the bullish case and turn intraday bias neutral first.

In the bigger picture, medium term outlook will stay bearish as long as the cross is capped well below falling 55 W EMA (now at 0.9809). That is, down trend from 1.2004 (2018 high) could still resume through 0.9407 (2022 low). However, sustained trading above the 55 W EMA will raise the chance that 0.9470 is already a long term bottom. Further rise would then be seen to 1.0095 resistance to indicate bullish trend reversal.

In the long term picture, outlook remains bearish as it's staying well below 55 M EMA (now at 1.0391). Break of 1.0095 resistance is needed to be the first sign of bottoming, or the multi-decade down trend is expected to continue.

The Weekly Bottom Line: Inflation Testing the Bank of Canada’s Hand

U.S. Highlights

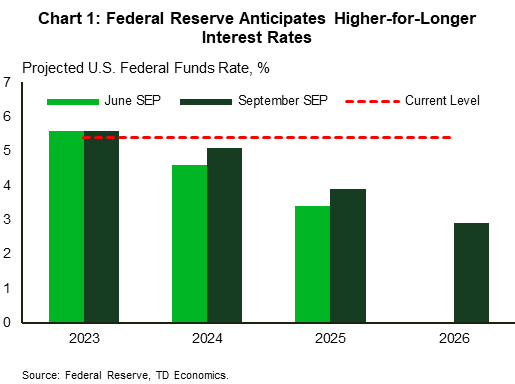

- The Federal Reserve held rates unchanged at its September meeting, but updated projections showed that the median FOMC member expects rates to remain above 5% through 2024, reinforcing the higher for longer message.

- The economy is likely to feel some drag from the UAW strike, which announced additional action at 38 parts and distribution facilities across 20 states, as contract negotiations continue to progress slowly.

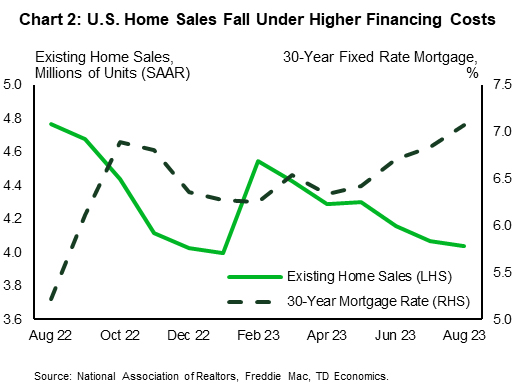

- The theme of “higher-for-longer” had pushed mortgage rates higher, which weighed on both homebuilding activity and existing home sales in August.

Canadian Highlights

- The economic data headline this week was a faster than expected acceleration in inflation in August. Markets are now positioned for another Bank of Canada (BoC) interest rate hike in the next six months.

- The BoC is at a crossroads as nascent signs of renewed inflation pressures collide with an economy that is losing its heat. We see enough bending in the Canadian economy to allow the BoC to hold the policy rate at 5.00% in October.

- Retail spending is one example of cooling demand. While sales rebounded modestly in July, they fell in real terms, a trend expected to continue into August. Overall, the consumer is showing signs of losing steam.

U.S. – Higher for Longer

Over the past eighteen months the Federal Reserve has raised interest rates eleven times, bringing the policy rate 5¼ percentage points (ppts) higher. On Wednesday, the FOMC opted to hold rates steady for the second time in the past three meetings, as it fine-tunes its approach to the level it deems sufficiently restrictive to return price stability to the economy. The Fed adopted the same policy decision it implemented in June - a hawkish pause if you will - indicating their expectation that one further rate hike is in the cards for 2023. In response, Treasury yields jumped to their highest level since 2007, with the ten-year yield rising by 12 basis points (bps) on the week to 4.4%, while equities fell with the S&P 500 down 2.3% as of the time of writing.

Accompanying the FOMC decision on Wednesday, the updated summary of economic projections (SEP) showed that the median FOMC member is projecting a de-facto soft landing for the U.S. economy. The median member expects the unemployment rate to rise only 0.3ppts by the end of next year. For reference, the U.S. unemployment rate just rose by 0.3ppts in August alone. The Fed’s expectation that inflation will be at 2.5% by the end of 2024 remained unchanged. However, the number of rate cuts for next year was pulled in, with the median FOMC member expecting the policy rate to be only 25bps below the current level at the end of 2024 - 50 basis points higher than in the June SEP (Chart 1). While these projections are decidedly hawkish, Chair Powell continued to emphasize that the Fed’s future decisions will depend on incoming data and its implications for the trajectory of inflation.

On that front, we saw in the housing data released this week that the interest rate sensitive sector continues to feel the strain of higher rates, as homebuilding activity faltered in August on slowing demand for new homes. With mortgage rates back above 7%, a similar curtailment of demand was seen in existing home sales in August, which declined for a third consecutive month (Chart 2). Price growth, however, has continued to push higher, as the highest mortgage rates in 22 years has left many would-be sellers locked-in to their lower rates, limiting resale supply. This dynamic is being monitored by the Fed but is unlikely to influence monetary policy discussions due to the lagged and proxied measurement of shelter costs in the CPI and PCE indexes.

Looking ahead, there is no shortage of upcoming events that will be on the Federal Reserve’s radar. This includes the UAW strike, which was extended to an additional 38 parts and distribution facilities this morning as negotiations continue to progress slowly. In the most recent round of strike action, the UAW has targeted General Motors and Stellantis, citing negotiation progress with Ford as the reason for the company’s exclusion. This is expected to create additional disruptions on top of the roughly 7.5% hit to U.S. production stemming from the first round of strike action. Also on the horizon is a looming shutdown of the federal government, with only a few days left before the October 1st deadline. Adding to the impacts expected from the end of the moratorium on student debt repayment, it is clear that the Federal Reserve’s data-dependency approach is set to become more challenging over the near-term.

Canada – Inflation Testing the Bank of Canada's Hand

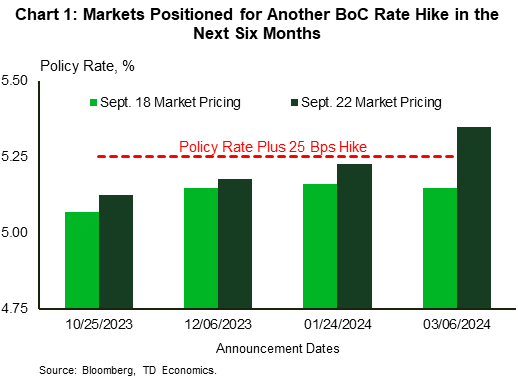

Summer may be coming to an end, but Canada's inflation report just offered up some unwelcome heat. Headline CPI accelerated for a second straight month in August reaching 4.0% year-on-year (y/y). On top of that, core inflation measures increased, which surely rang some alarm bells at the Bank of Canada (BoC). Whether the inflation data is hot or just uncomfortably warm is up for debate, but markets have raised their bets for another interest rate hike down the road. Prior to Tuesday's inflation release, markets were pricing a roughly 20% chance of another quarter-point hike at the October 25th policy meeting. Those odds swiftly increased to 50% post-data, with a full quarter-point hike fully priced by the first quarter of next year (Chart 1). As interest rate expectations rise, the 5-year Government of Canada yield rose to 4.25%, its highest level in 16 years.

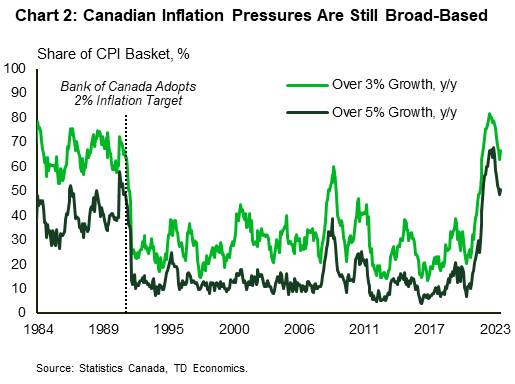

Soaring energy prices over the month of August were expected to drive an increase to headline inflation. But it was more than this, as shelter costs accelerated for both renters and homeowners facing higher mortgage payments. There was finally some relief on food prices, which fell for the first time in two years, but still sport the highest year-on-year increase across major CPI categories. On core readings, the average of the BoC's CPI-Trim and CPI-Median measures has moved back to 4.0%, the highest reading since April this year. Any way you slice it, inflation pressures remain broad-based. As shown in Chart 2, the share of components in the CPI basket running at higher than 3% and 5% y/y are considerably higher than pre-pandemic levels, and the highest since the pre-inflation targeting days of the BoC.

The BoC faces a difficult road ahead, as nascent signs of renewed inflation pressures collide with an economy that is losing its heat. Our base case is for the BoC to keep the overnight rate on hold at 5.00% next meeting. However, the BoC will need to see evidence of further slowing in upcoming data to feel comfortable staying on the sidelines. The first such data point was today's pulse check on the consumer. Retail sales for July (+0.3% m/m) came in a touch weaker than Statistics Canada's advance estimate, and broadly in line with our own internal spending data which pointed to a rebound. However, controlling for price effects, retail spending edged down, with further deceleration expected in August. This aligns with our view that the resiliency of the consumer is beginning to fade and will continue to do so into next year.

We see enough bending in the Canadian economy to support a cooling in inflation pressures ahead, with enough time to allow the lagged impacts of monetary policy to continue working through the system. The Bank does have over a month to see how the data unfolds before it's next announcement in late October. The data to watch the most closely include another inflation report, plus data on jobs and wages and the BoC’s surveys of consumers and businesses including measures of inflation expectations. Stay tuned.

Summary 9/25 – 9/29

Monday, Sep 25, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 08:00 | EUR | Germany IFO Business Climate Sep | 85.2 | 85.7 |

| 08:00 | EUR | Germany IFO Current Assessment Sep | 88.0 | 89.0 |

| 08:00 | EUR | Germany IFO Expectations Sep | 82.8 | 82.6 |

| 23:50 | JPY | Corporate Service Price Index Y/Y Aug | 1.80% | 1.70% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 08:00 | EUR | Germany IFO Business Climate Sep | |

| Forecast: 85.2 | Previous: 85.7 | ||

| 08:00 | EUR | Germany IFO Current Assessment Sep | |

| Forecast: 88.0 | Previous: 89.0 | ||

| 08:00 | EUR | Germany IFO Expectations Sep | |

| Forecast: 82.8 | Previous: 82.6 | ||

| 23:50 | JPY | Corporate Service Price Index Y/Y Aug | |

| Forecast: 1.80% | Previous: 1.70% | ||

Tuesday, Sep 26, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Jul | -0.50% | -1.20% |

| 13:00 | USD | Housing Price Index M/M Jul | 0.10% | 0.30% |

| 14:00 | USD | Consumer Confidence Sep | 105.9 | 106.1 |

| 14:00 | USD | New Home Sales Aug | 700K | 714K |

| 23:50 | JPY | BoJ Minutes |

| GMT | Ccy | Events | |

|---|---|---|---|

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Jul | |

| Forecast: -0.50% | Previous: -1.20% | ||

| 13:00 | USD | Housing Price Index M/M Jul | |

| Forecast: 0.10% | Previous: 0.30% | ||

| 14:00 | USD | Consumer Confidence Sep | |

| Forecast: 105.9 | Previous: 106.1 | ||

| 14:00 | USD | New Home Sales Aug | |

| Forecast: 700K | Previous: 714K | ||

| 23:50 | JPY | BoJ Minutes | |

| Forecast: | Previous: | ||

Wednesday, Sep 27, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Monthly CPI Y/Y Aug | 4.90% | |

| 06:00 | EUR | Germany Gfk Consumer Confidence Oct | -25.5 | -25.5 |

| 08:00 | CHF | Credit Suisse Economic Expectations Sep | -38.6 | |

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Aug | -1.00% | -0.40% |

| 12:30 | USD | Durable Goods Orders Aug | -0.40% | -5.20% |

| 12:30 | USD | Durable Goods Orders ex Transportation Aug | 0.20% | 0.40% |

| 14:30 | USD | Crude Oil Inventories | -2.1M |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Monthly CPI Y/Y Aug | |

| Forecast: | Previous: 4.90% | ||

| 06:00 | EUR | Germany Gfk Consumer Confidence Oct | |

| Forecast: -25.5 | Previous: -25.5 | ||

| 08:00 | CHF | Credit Suisse Economic Expectations Sep | |

| Forecast: | Previous: -38.6 | ||

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Aug | |

| Forecast: -1.00% | Previous: -0.40% | ||

| 12:30 | USD | Durable Goods Orders Aug | |

| Forecast: -0.40% | Previous: -5.20% | ||

| 12:30 | USD | Durable Goods Orders ex Transportation Aug | |

| Forecast: 0.20% | Previous: 0.40% | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -2.1M | ||

Thursday, Sep 28, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:00 | NZD | ANZ Business Confidence Sep | -3.7 | |

| 01:30 | AUD | Retail Sales M/M Aug | 0.30% | 0.50% |

| 08:00 | EUR | ECB conomic Bulletin | ||

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Sep | 92.5 | 93.3 |

| 09:00 | EUR | Eurozone Industrial Confidence Sep | -10.5 | -10.3 |

| 09:00 | EUR | Eurozone Services Sentiment Sep | 3.5 | 3.9 |

| 09:00 | EUR | Eurozone Consumer Confidence Sep F | -17.8 | -17.8 |

| 12:00 | EUR | Germany CPI M/M Sep P | 0.30% | |

| 12:00 | EUR | Germany CPI Y/Y Sep P | 6.10% | |

| 12:30 | USD | Initial Jobless Claims (Sep 22) | 200K | 201K |

| 12:30 | USD | GDP Annualized Q2 F | 2.30% | 2.10% |

| 12:30 | USD | GDP Price Index Q2 F | 2.00% | 2.00% |

| 14:00 | USD | Pending Home Sales M/M Aug | 0.20% | 0.90% |

| 14:30 | USD | Natural Gas Storage | 64B | |

| 23:30 | JPY | Tokyo CPI Y/Y Sep | 2.90% | |

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Sep | 2.60% | 2.80% |

| 23:30 | JPY | Tokyo CPI ex Food Energy Y/Y Sep | 4% | |

| 23:30 | JPY | Unemployment Rate Aug | 2.60% | 2.70% |

| 23:50 | JPY | Industrial Production M/M Aug P | -0.80% | -1.80% |

| 23:50 | JPY | Retail Trade Y/Y Aug | 6.40% | 6.80% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:00 | NZD | ANZ Business Confidence Sep | |

| Forecast: | Previous: -3.7 | ||

| 01:30 | AUD | Retail Sales M/M Aug | |

| Forecast: 0.30% | Previous: 0.50% | ||

| 08:00 | EUR | ECB conomic Bulletin | |

| Forecast: | Previous: | ||

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Sep | |

| Forecast: 92.5 | Previous: 93.3 | ||

| 09:00 | EUR | Eurozone Industrial Confidence Sep | |

| Forecast: -10.5 | Previous: -10.3 | ||

| 09:00 | EUR | Eurozone Services Sentiment Sep | |

| Forecast: 3.5 | Previous: 3.9 | ||

| 09:00 | EUR | Eurozone Consumer Confidence Sep F | |

| Forecast: -17.8 | Previous: -17.8 | ||

| 12:00 | EUR | Germany CPI M/M Sep P | |

| Forecast: | Previous: 0.30% | ||

| 12:00 | EUR | Germany CPI Y/Y Sep P | |

| Forecast: | Previous: 6.10% | ||

| 12:30 | USD | Initial Jobless Claims (Sep 22) | |

| Forecast: 200K | Previous: 201K | ||

| 12:30 | USD | GDP Annualized Q2 F | |

| Forecast: 2.30% | Previous: 2.10% | ||

| 12:30 | USD | GDP Price Index Q2 F | |

| Forecast: 2.00% | Previous: 2.00% | ||

| 14:00 | USD | Pending Home Sales M/M Aug | |

| Forecast: 0.20% | Previous: 0.90% | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 64B | ||

| 23:30 | JPY | Tokyo CPI Y/Y Sep | |

| Forecast: | Previous: 2.90% | ||

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Sep | |

| Forecast: 2.60% | Previous: 2.80% | ||

| 23:30 | JPY | Tokyo CPI ex Food Energy Y/Y Sep | |

| Forecast: | Previous: 4% | ||

| 23:30 | JPY | Unemployment Rate Aug | |

| Forecast: 2.60% | Previous: 2.70% | ||

| 23:50 | JPY | Industrial Production M/M Aug P | |

| Forecast: -0.80% | Previous: -1.80% | ||

| 23:50 | JPY | Retail Trade Y/Y Aug | |

| Forecast: 6.40% | Previous: 6.80% | ||

Friday, Sep 29, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Private Sector Credit M/M Aug | 0.30% | 0.30% |

| 05:00 | JPY | Housing Starts Y/Y Aug | -8.90% | -6.70% |

| 05:00 | JPY | Consumer Confidence Index Sep | 36.2 | 36.2 |

| 06:00 | EUR | Germany Import Price Index M/M Aug | 0.50% | -0.60% |

| 06:00 | GBP | GDP Q/Q Q2 F | 0.20% | 0.20% |

| 06:00 | EUR | Germany Retail Sales M/M Aug | 0.50% | -0.80% |

| 06:00 | GBP | Current Account (GBP) Q2 | -14.0B | -10.8B |

| 06:30 | CHF | Real Retail Sales Y/Y Aug | -2.20% | |

| 06:45 | EUR | France Consumer Spending M/M Aug | -0.40% | 0.30% |

| 07:00 | CHF | KOF Economic Barometer Sep | 90.5 | 91.1 |

| 07:55 | EUR | Germany Unemployment Change Aug | 14K | 18K |

| 07:55 | EUR | Germany Unemployment Rate Aug | 5.70% | 5.70% |

| 08:30 | GBP | Mortgage Approvals Aug | 48K | 49K |

| 08:30 | GBP | M4 Money Supply M/M Aug | 0.20% | -0.50% |

| 09:00 | EUR | Eurozone CPI Y/Y Sep P | 4.50% | 5.20% |

| 09:00 | EUR | Eurozone CPI Core Y/Y Sep P | 4.80% | 5.30% |

| 12:30 | USD | Personal Income M/M Aug | 0.40% | 0.20% |

| 12:30 | USD | Personal Spending Aug | 0.50% | 0.80% |

| 12:30 | USD | PCE Price Index M/M Aug | 0.50% | 0.20% |

| 12:30 | USD | PCE Price Index Y/Y Aug | 3.30% | |

| 12:30 | USD | Core PCE Price Index M/M Aug | 0.20% | 0.20% |

| 12:30 | USD | Core PCE Price Index Y/Y Aug | 3.90% | 4.20% |

| 12:30 | USD | Goods Trade Balance (USD) Aug P | -91.2B | -90.9B |

| 13:45 | USD | Chicago PMI Sep | 47.6 | 48.7 |

| 14:00 | USD | Michigan Consumer Sentiment Index Sep F | 67.7 | 67.7 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Private Sector Credit M/M Aug | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 05:00 | JPY | Housing Starts Y/Y Aug | |

| Forecast: -8.90% | Previous: -6.70% | ||

| 05:00 | JPY | Consumer Confidence Index Sep | |

| Forecast: 36.2 | Previous: 36.2 | ||

| 06:00 | EUR | Germany Import Price Index M/M Aug | |

| Forecast: 0.50% | Previous: -0.60% | ||

| 06:00 | GBP | GDP Q/Q Q2 F | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 06:00 | EUR | Germany Retail Sales M/M Aug | |

| Forecast: 0.50% | Previous: -0.80% | ||

| 06:00 | GBP | Current Account (GBP) Q2 | |

| Forecast: -14.0B | Previous: -10.8B | ||

| 06:30 | CHF | Real Retail Sales Y/Y Aug | |

| Forecast: | Previous: -2.20% | ||

| 06:45 | EUR | France Consumer Spending M/M Aug | |

| Forecast: -0.40% | Previous: 0.30% | ||

| 07:00 | CHF | KOF Economic Barometer Sep | |

| Forecast: 90.5 | Previous: 91.1 | ||

| 07:55 | EUR | Germany Unemployment Change Aug | |

| Forecast: 14K | Previous: 18K | ||

| 07:55 | EUR | Germany Unemployment Rate Aug | |

| Forecast: 5.70% | Previous: 5.70% | ||

| 08:30 | GBP | Mortgage Approvals Aug | |

| Forecast: 48K | Previous: 49K | ||

| 08:30 | GBP | M4 Money Supply M/M Aug | |

| Forecast: 0.20% | Previous: -0.50% | ||

| 09:00 | EUR | Eurozone CPI Y/Y Sep P | |

| Forecast: 4.50% | Previous: 5.20% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Sep P | |

| Forecast: 4.80% | Previous: 5.30% | ||

| 12:30 | USD | Personal Income M/M Aug | |

| Forecast: 0.40% | Previous: 0.20% | ||

| 12:30 | USD | Personal Spending Aug | |

| Forecast: 0.50% | Previous: 0.80% | ||

| 12:30 | USD | PCE Price Index M/M Aug | |

| Forecast: 0.50% | Previous: 0.20% | ||

| 12:30 | USD | PCE Price Index Y/Y Aug | |

| Forecast: | Previous: 3.30% | ||

| 12:30 | USD | Core PCE Price Index M/M Aug | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 12:30 | USD | Core PCE Price Index Y/Y Aug | |

| Forecast: 3.90% | Previous: 4.20% | ||

| 12:30 | USD | Goods Trade Balance (USD) Aug P | |

| Forecast: -91.2B | Previous: -90.9B | ||

| 13:45 | USD | Chicago PMI Sep | |

| Forecast: 47.6 | Previous: 48.7 | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Sep F | |

| Forecast: 67.7 | Previous: 67.7 | ||

Weekly Economic & Financial Commentary: Higher for Longer

Summary

United States: U.S. Economy Still Resilient, but Headwinds Building

- It was a relatively light week on the U.S. economic data front. A slate of housing data offered additional evidence that high mortgage rates and limited inventory are weighing on housing market activity. Jobless claims remained low, but a still-declining LEI and a further climb in Treasury yields and oil prices suggest economic growth will slow in the months ahead.

- Next week: New Home Sales (Tue.), Durable Goods (Wed.), Personal Income and Spending (Fri.)

International: Central Banks Here, There and Everywhere

- It was a particularly active week for international central banks across the G10 and emerging markets, with several institutions delivering differing decisions and differing messages. Emerging market central banks saw a combination of rate hikes, rate holds and rate cuts. G10 central banks saw some rate hikes and some rate holds, with differing messages also on the likelihood of further monetary tightening in the months ahead.

- Next week: Mexico Policy Rate Decision (Thu.), Eurozone CPI (Fri.), China PMIs (Sat.)

Interest Rate Watch: Higher for Longer

- The Federal Open Market Committee (FOMC) held the target range for the federal funds rate at 5.25%-5.50% this week. While rates were left unchanged, the Committee retained a hawkish bias. The median projection for the midpoint of the target range at the end of 2024 rose to 5.125%, up from 4.625% in June.

Topic of the Week: Oil Prices Complicate the Fed's Efforts to Reduce Inflation

- The climb in oil prices to a 10-month high has created a new challenge to corralling inflation. While having a bigger effect on headline inflation, the increase, if sustained, could also pass through to core prices and slow progress in returning inflation to 2%.

Week Ahead – US and Eurozone Inflation, Fed Speak, Bank of Japan Minutes

US

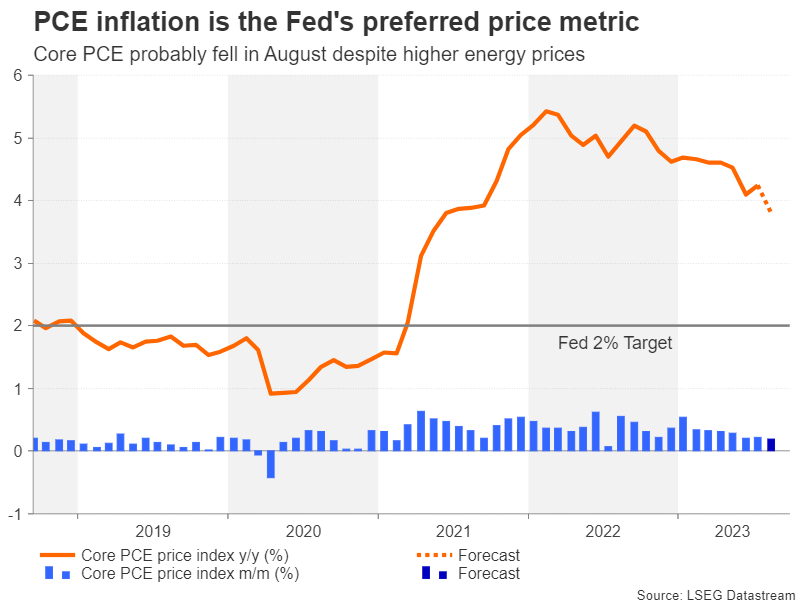

It will be a busy week filled with a wide range of economic releases, with the focus falling on the consumer and the Fed’s preferred inflation gauge. August personal income is expected to rise given the strong labor market while spending cooled given the end of summer vacations. The bond market will pay extremely close attention to the next round of inflation readings. Headline PCE will likely heat up given the surge in energy prices, while the core reading should maintain the 0.2% monthly pace.

Wall Street will also pay close attention to the UAW strike and if government shutdown odds grow. It will also be a busy week filled with central bank speak. On Monday, the Fed’s Kashkari speaks at Wharton School. Tuesday contains Bowman’s welcoming remarks at a FedCommunities event on rental housing affordability. Thursday contains four events, with Chair Powell hosting a town hall with educators and speeches from Goolsbee, Cook, and Barkin. Williams speaks on monetary policy on Friday.

Eurozone

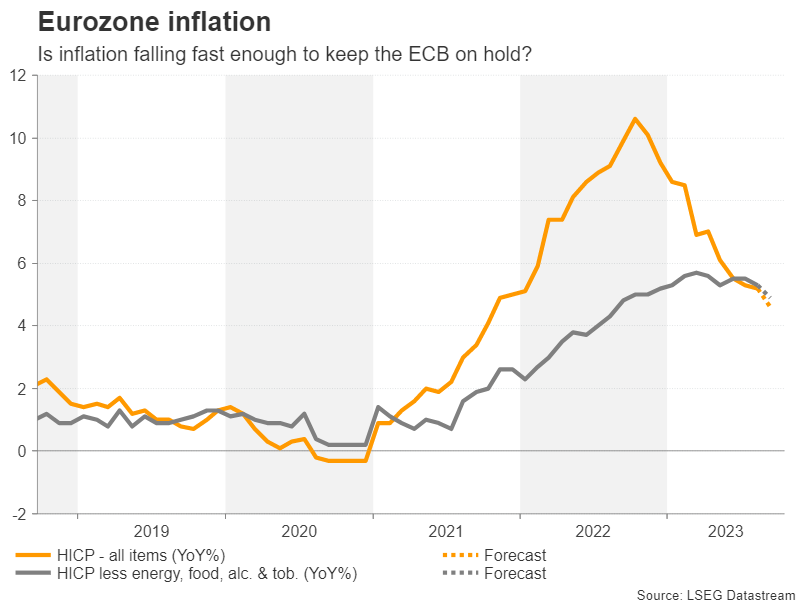

The ECB signaled after its September meeting that its tightening cycle was likely at an end, barring any nasty surprises on the data front. Next week could be the first test of that, with flash HICP inflation data due on Friday. Substantial progress has already been made and much more is expected over the remainder of the year, while a cooling economy and threat of recession is clearly making policymakers nervous.

As always, a number of individual countries will release their inflation numbers in the days leading up to the eurozone release so we could have a pretty good idea of what we’re in for by the time the Friday release happens. That aside, there are some surveys released over the course of the week among other tier two and three data. Central bank speak will also be monitored, most notably President Christine Lagarde’s comments as she makes an appearance on the same day as the inflation report is released.

UK

The Bank of England surprised markets this past week in choosing to hold the Bank Rate at 5.25, with those backing it taking the vote by the finest of margins 5-4. That doesn’t necessarily mark the end of the tightening cycle but if the data improves as the MPC expect, it may well be. Any negative data surprises between now and the early November meeting though may tip the balance the other way. There’s going to be even more pressure on the data now, not that there’s really anything of note next week. The final GDP reading for the second quarter is the only one that stands out in any way.

Russia

There’s a selection of data due next week although I’m not sure any will hold much sway when it comes to upcoming monetary policy announcements unless they’re particularly shocking. Industrial output, retail sales, GDP, unemployment, and real wages are among the releases. Russia’s issues with inflation and the currency are much bigger than all of these, although it will be interesting to see how the economy is holding up amid these additional pressures.

South Africa

The SARB held rates steady at its September meeting, as expected, with headline and core inflation sitting comfortably within its 3-6% target. The central bank continued to warn about risks to the inflation outlook and hasn’t declared the end of the tightening cycle just yet. PPI figures next week may be of interest.

Turkey

The Turkish central bank raised interest rates by 5% on Thursday, taking the Key Rate to 30% amid a plunging lira and soaring inflation. The move didn’t help lift the currency which still sits near record lows. Next week doesn’t have much to offer beyond a few tier-three data releases.

Switzerland

The SNB opted against raising interest rates in September as their new forecasts showed inflation below 2% over the forecast horizon, meaning no more tightening is necessary. The decision obviously came with warnings that hikes could be considered in the future if the data warrants it, as the SNB attempted to put itself into hawkish hold territory, which markets didn’t buy. The SNB is done with rate hikes and the focus now will shift to when the first cut will come. Next week has a few things of note, with the KOF indicator and investor sentiment surveys, and the SNB quarterly bulletin being released.

China

The only data to watch will be total industrial profits for August which are forecasted to contract at a slower pace of -10% y/y from -15.5% y/y in July.

India

Q2 current account and external debt data will be released on Friday. The current account deficit is expected to shrink marginally to $1 billion from $-1.3 billion recorded in Q1.

The Indian rupee has been resilient against the strength of the US dollar against other emerging currencies in the past three months. The USD/INR has been trading in a tight range of 175 pips and capped below its October 2022 high of 83.28.

Australia

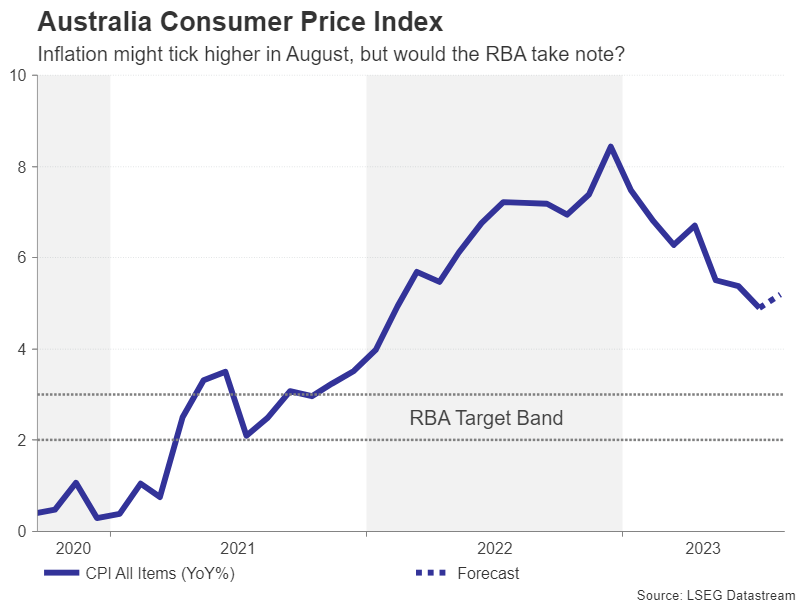

Two key data releases to be aware of this week. Firstly, the monthly CPI for August will be out on Wednesday, and after a deceleration to 4.9% in the year to July, marking the lowest inflation rate since February 2022, a slight uptick to 5.2% is expected in August.

Secondly, preliminary retail sales for August on Thursday are expected to show a dip to 0.3% m/m from 0.5% in July.

New Zealand

Business confidence data for September is due on Thursday with an improvement to 5 from -3.7 in August expected. That would put an end to 26 consecutive months of negative readings.

Consumer confidence on Friday is expected to slow to 81.5 for September from 85 previously.

Japan

Bank of Japan (BoJ) monetary policy meeting minutes will be out on Wednesday and market participants will scrutinize the BoJ official’s remarks or expressed views on the state of inflation in Japan as well as any debate on bringing forward the end of negative interest rate policy.

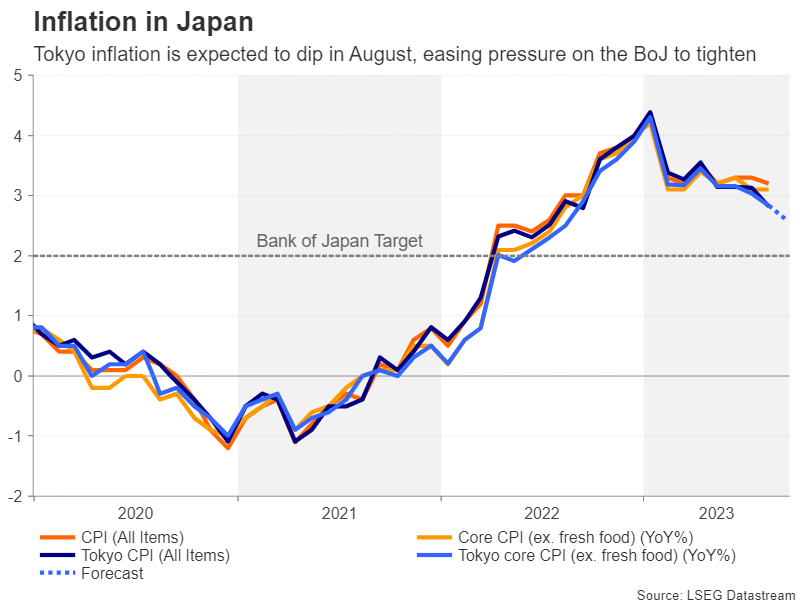

A busy Friday with a slew of data releases. The leading Tokyo core inflation reading (excluding fresh food) is expected to dip to 2.6% y/y from 2.8%. That would be the third straight month of deceleration in Tokyo’s core inflation. However, the core-core inflation rate (excluding fresh food and energy) is forecasted to remain the same at 2.6% y/y for September, a 31-year high.

Retail sales for August are expected to dip slightly to 6.6% y/y from 6.8% in July, Consumer confidence in September is expected to improve to 37 from 36.2 in August.

Singapore

Inflation data for August will be out on Monday and the core inflation rate is expected to decelerate further to 3.5% y/y from 3.8% in July. That would be the fourth consecutive month of slowdown. Meanwhile, the headline inflation rate is expected to be almost unchanged at 4% y/y in August versus 4.1% in July.

August’s industrial production figures will be released on Tuesday with another month of contraction expected at a higher magnitude of -3.1% y/y from -0.9% in July. That would mark eleven straight months of contraction suggesting a sticky weak external demand environment.

Economic Calendar

Saturday, Sept. 23

Economic Data/Events

- 78th session of the UN General Assembly (plenary) continues

- German Chancellor Scholz attends SPD campaign events in Nuremberg and Hesse

Sunday, Sept. 24

Economic Data/Events

- Austrian Chancellor Nehammer opens Salzburg Europe Summit

Monday, Sept. 25

Economic Data/Events

- Germany IFO business climate

- Singapore CPI

- IAEA General Conference starts in Vienna

- RBA Assistant Governor Jones speaks on financial technology and climate change

- Fed’s Kashkari participates in Q&A at the University of Pennsylvania’s Wharton School.

- ECB’s Villeroy speaks on monetary policy and macroeconomics at the Paris conference

- EU industry ministers meet in Brussels

- German Chancellor Scholz and Economy Minister Habeck attend the national aerospace conference

- European Budget Commissioner Hahn and Austrian Finance Minister Brunner speak at the Salzburg Europe Summit

Tuesday, Sept. 26

Economic Data/Events

- US new home sales, Conference Board consumer confidence

- Mexico international reserves

- Singapore industrial production

- ECB’s Holzmann speaks at Bloomberg event in Vienna

- ECB’s Lane speaks on monetary policy and macroeconomics at the Paris conference

- Spanish Parliament begins debate on the new prime minister. Vote to occur on Sept. 27th

- German Chancellor Scholz speaks at the annual meeting of the German Society for International Cooperation

- German Economy Minister Habeck speaks at the BDI climate conference

Wednesday, Sept. 27

Economic Data/Events

- US durable goods

- China industrial profits

- Mexico trade

- Russia unemployment, industrial production

- Thailand rate decision: Expected to raise rates 25bps to 2.50%

- Bank of Japan issues minutes of July’s policy meeting

- French government reveals 2024 budget

- Foreign ministers of Austria, Slovenia, Slovakia, Czechia, and Hungary hold a briefing in Vienna

Thursday, Sept. 28

Economic Data/Events

- US initial jobless claims, GDP

- Australia retail sales

- Eurozone economic confidence, consumer confidence

- Germany CPI

- Mexico unemployment, rate decision

- Spain CPI

- Fed Chair Jerome Powell hosts town hall meeting

- Fed’s Barkin dinner speech on monetary policy outlook at Money Marketeers of NYU

- Fed’s Goolsbee speaks at Peterson Institute for International Economics in Washington

- South African Reserve Bank issues quarterly bulletin

- German Chancellor Scholz, Belgian Prime Minister De Croo, Bank of America CEO Brian Moynihan, and BlackRock CEO Larry Fink attend the Berlin Global Dialogue

- Riksbank Deputy Governor Flodén speaks at Svenska Kreditföreningen’s autumn conference

- IEA’s Critical Minerals and Clean Energy Summit in Paris

- Austrian energy regulator’s gas chief Millgramm speaks at the Montel Energy Day conference

Friday, Sept. 29

Economic Data/Events

- US consumer spending, wholesale inventories, University of Michigan consumer sentiment

- China Caixin manufacturing PMI, Caixin services PMI

- Czech Republic GDP

- Eurozone CPI

- France CPI

- Germany unemployment

- Hong Kong retail sales

- Italy CPI

- Japan unemployment, Tokyo CPI, industrial production, retail sales

- Poland CPI

- South Africa trade balance

- Thailand trade

- UK GDP

- China’s ‘Golden Week’ holiday begins from Sept. 29 to Oct. 8

- ECB President Lagarde speaks in Paris at an event on the energy transition

- Fed’s Williams speaks at the Long Island Association

- Helsinki Security Forum begins

Sovereign Rating Updates

- Portugal (Fitch)

- Turkey (S&P)

Canadian GDP to mark a lacklustre start to Q3

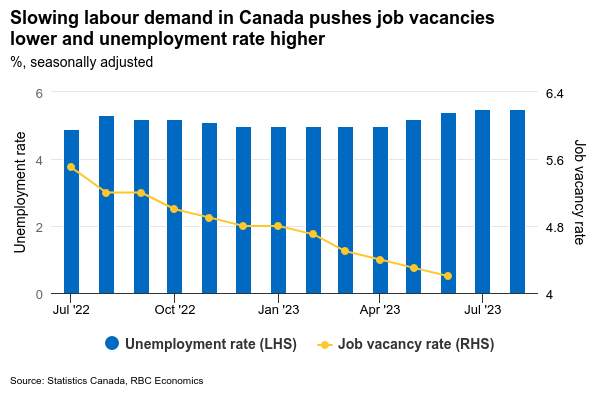

There was a surprise contraction in Canada’s economy in Q2. Despite estimates for a 1% increase, GDP fell by 0.2% (at an annualized rate) and with most of the decline coming from a 0.2% drop in June. And an early estimate for July suggests GDP was ‘essentially unchanged’ from the month before. Data releases have been broadly consistent with that estimate. Employment edged lower in July (down 6,000 positions) and the unemployment rate ticked higher amid a broader pullback in labour demand. Next week’s Survey of Employment, Payrolls and Hours should continue to show a slowdown in the number of job vacancies in July. Manufacturing sales rose 0.9% (excluding price impacts) in July, but that increase was drawn from existing inventories rather than new production. Wholesale sales volumes were little changed (+0.2%) outside of a surge in the large (and volatile) petroleum component. And retail sales continued to soften, with volumes declining by 0.2% after posting an already-large 3.3% annualized drop in Q2.

Part of the weakness in Q2 output can be attributed to ‘transitory’ factors, including the federal government workers’ strike in April and wildfire-related disruptions to mining sector output. But the softening momentum looks to have been extended into Q3, where a flat reading in July GDP would leave output running at roughly 0.4% (annualized) below the Q2 average. That’s broadly in line with our forecast for output to decline by 0.5% in Q3. Notably, the unemployment rate (which is much less affected by those transitory disruptions) has increased by half a percentage point over the last four months. To be sure, the preliminary estimate for August output (also to be released next week) could read better—given both employment and hours worked bounced back in that month. But housing markets also cooled further as resales declined outright for a second consecutive month in August. And spending on discretionary items also continued to flag, with motor vehicle sales continuing on its downward trend in August.

Meantime, our own tracking of RBC debit and credit spending data flagged less spending on hotels and restaurants, as the busy summer travel season comes to an end. Overall, we believe elevated interest rates are putting a tighter squeeze on households’ buying power. That will drive inflation pressures lower still, despite the upside surprise in August.

Week ahead data watch

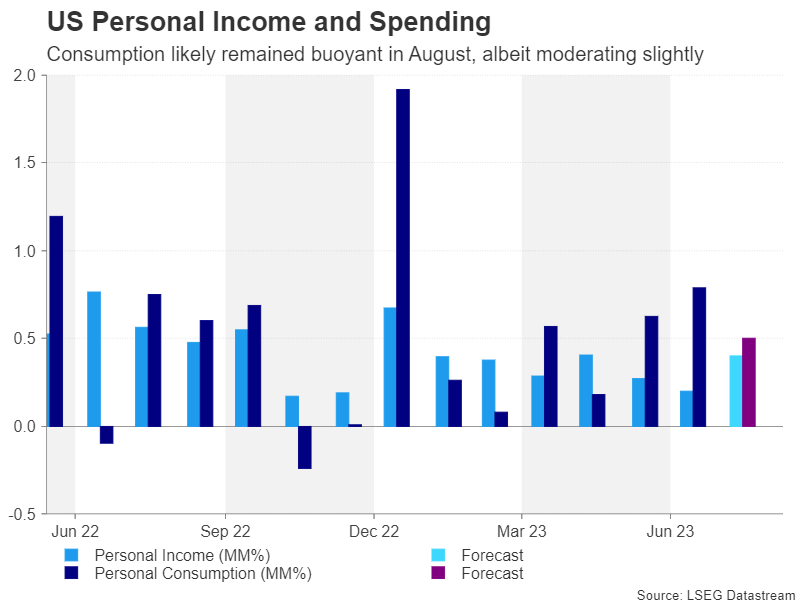

U.S. personal consumption expenditure is likely to edge up 0.5% in August, supported by strong retail sales data (+0.6%). Personal income is likely to rise by 0.3%, supported by slower but still elevated wage gain in the same month (+0.2%).

The July job vacancy and employment growth numbers (from SEPH) are out next week. The former will likely confirm a further slowdown in labour demand. The latter will be watched for any divergence in employment accounts from the earlier-reported 6,000 position drop in July in the more timely Labour Force Survey.

Q2 Canadian population estimates will be watched closely after Q1 saw the strongest year-over-year increase since the 1950s. The release could, reportedly, include new details on the composition of non-permanent resident arrivals, that have driven much of the upward surprise in population growth in recent quarters, and potentially also revisions to prior total population counts.

Canadian auto producers may have avoided a strike. But U.S. strikes (currently targeting a small number of motor vehicle production facilities) will still impact Canadian motor vehicle production—particularly if those disruptions escalate. Auto trade is exceptionally integrated across the border. Auto production and retail combined to account for 1.5% of Canadian GDP in 2022.

Week Ahead – US Core PCE and Eurozone Flash CPIs Eyed After Rate Pause Signals

- PCE inflation to grab attention on Friday as Fed signals higher for longer

- But markets might be more worried about a government shutdown

- Eurozone flash CPIs will also be the in the spotlight on Friday

- Chinese PMIs to be watched for recovery signs

Will core PCE add to second inflation wave worries?

The latest spike in oil prices is causing some headaches for policymakers as energy costs are on the rise again just as they’ve started to see the result of their hard-fought battle to get inflation down. In the United States, higher gasoline prices have already started to push headline inflation back up. But as long as the oil surge turns out to be temporary, the trend in underlying price metrics should remain downwards.

That is what investors are hoping to see on Friday when the latest PCE inflation numbers are published. The core PCE price index is expected to have increased by 0.2% month-on-month in August, taking the annual figure down to 3.8% from 4.2% in July. For the Fed that’s mindful of overtightening, such a print would likely be low enough to give it second thoughts about hiking rates in November or December.

But resurgent energy prices aren’t the Fed’s only concern. Exceptionally strong consumption has been another incentive for policymakers to keep the door open to further hikes. Personal spending is forecast to have increased by 0.5% m/m, moderating slightly from 0.8% previously, while personal income is expected to have risen by 0.4% m/m.

Any upside surprise in either or both personal consumption and core PCE would boost the odds of one final hike, pushing up Treasury yields and the US dollar.

Looming government shutdown could rattle markets

Ahead of Friday’s data, traders will also keep an eye on some housing numbers on Tuesday, which will include new home sales for August, as well as the September consumer confidence index. Durable goods orders are out on Wednesday, while on Thursday, the final estimate of Q2 GDP will be doing the rounds together with pending home sales.

However, a potentially bigger concern for investors is a possible government shutdown as time is running out for Congress before the midnight deadline on September 30 to agree to a stopgap spending bill. Republicans have already torpedoed three attempts by House Speaker Kevin McCarthy to bring to the floor a defence spending bill amid GOP opposition to further aid for Ukraine. But even if McCarthy manages to get a funding bill through the House, it’s unlikely that the Democrat-controlled Senate would pass legislation that contains spending cuts proposed by hardline Republicans.

Falling inflation could be positive for the euro

In the euro area, higher energy prices also pose a problem for the European Central Bank and could determine whether rates stay on hold for the foreseeable future or rise further. Unlike the Fed, the ECB has to factor in a much weaker economy into its decision making, hence, the bar for a further hike is higher.

For the moment at least, Eurozone inflation is falling, removing any urgency for policymakers to respond pre-emptively to any new inflationary threat. The September flash estimates of the harmonised indices of consumer prices (HICP) are due on Friday and should they show a further decline in price pressures as expected, the outlook might brighten a little amid ongoing recession risks.

In this respect, a downside surprise in inflation might not necessarily be bad for the euro, as easing stagflation fears could offset diminishing expectations of further ECB rate hikes.

In other data, some business surveys might also capture the euro’s attention. Germany’s Ifo business climate index is due on Monday, and the Eurozone economic sentiment indicator will follow on Thursday.

Aussie likely to get caught between domestic CPI and Chinese PMIs

Another economy suffering a bit of a wobble lately is China’s. After the post-pandemic recovery unexpectedly faltered earlier this year, Chinese authorities have been busy devising various measures to boost growth. The problem is that a lot of the policy responses have been half measures, leaving investors exasperated by the lack of more substantive stimulus announcements.

However, the drip-feed stimulus has kept on coming and there are encouraging signs that they’ve started to have some effect. The PMI surveys for September will provide fresh clues if the economy is indeed stabilizing. The government will report its manufacturing and non-manufacturing PMI prints on Saturday, and the S&P Global/Caixin equivalent is due next Sunday.

The tepid improvement in the economic picture appears to have helped China-sensitive currencies such as the Australian dollar establish a floor under their recent slide. Whilst the aussie remains one of the worst performing currencies of the year, a Chinese economic revival could yet spur an end of year rally.

One major obstacle, though, for the aussie bulls is an increasingly neutral Reserve Bank of Australia. With inflation in Australia falling to just below 5% in July, RBA tightening has potentially reached the end of the road. However, despite the cautious rhetoric, the RBA did reveal in its meeting minutes that a rate increase was discussed in September. Therefore, Australian CPI figures for August released on Wednesday might pressure the RBA to hike again should the headline figure edge up as forecast.

Tokyo CPIs unlikely to provide much relief to the yen

The Tokyo CPI readings will be watched on Friday for any signs that inflation in Japan isn’t about to drop to 2% in a quick manner. The Tokyo stats are published in advance of the nationwide numbers so they are seen as a forward looking indicator.

The Bank of Japan has yet to be convinced that high inflation is here to stay and that the country isn’t about to fall back into deflation. A sustained rise in wages is a key criterion for policymakers, but even if this isn’t achieved anytime soon, the longer that CPI stays above the 2% target, the more difficult it will be for the Bank of Japan to justify maintaining ultra-loose monetary policy.

Thus, there could be some modest gains for the yen if the data is slightly stronger-than-expected. Also on the agenda in Japan are retail sales and preliminary industrial production figures for August, both on Friday.

Weekly Focus – Taking Stock of Central Bank Week

This week was all about central banks with monetary policy meetings around the globe. In the US, the Fed maintained the policy rate unchanged at 5.25%-5.50% as widely anticipated, but surprised hawkishly with higher median rate projections (dot plots). The median 'dots' were revised up by 50bp for both 2024 (to 5.1%) and 2025 (to 3.9%) which moved treasury yields higher. The higher projected policy rate was due to a large upward revision of the growth outlook for 2023 to 2.1% (from 1.0%) and 1.5% (from 1.1%) for 2024, while inflation forecasts only received minor adjustments. For more details, see Fed review: Upbeat on growth, 20 September.

Bank of England (BoE) decided to leave the policy rate unchanged at 5.25% and step up QT as five members voted for a pause and four for a hike. The outcome of the meeting was more uncertain than usual as inflation figures released a day before the meeting showed a significantly larger decline in both in headline and core figures than expected. For more details, see BoE review: End to the hiking cycle, but not GBP headwinds, 21 September.

The Bank of Japan kept its QQE with yield control unchanged as expected. The policy rate stayed at -0.1% and the 10-year yield target around 0% with +/- 0.50% tolerance band and a firm cap at 1.0%. The central bank of Turkey increased the policy rate as expected while the Swiss National Bank surprised both analysts and markets by leaving the policy rate unchanged. For details on Sveriges Riksbank and Norges Bank, see Scandi Update section.

The September PMIs showed that the euro area and UK economy ended Q3 in contraction as waning demand lead to a further decline in activity. The service sector surprised positively in the euro area and negatively in the UK but both remain below 50. Price pressures are still large in the service sectors as wages push up input costs.

Focus next week will be on inflation in both the US and euro area on Friday. Inflation drivers continue to paint a mixed picture, as price pressures from food and energy ease while underlying inflation still remains uncomfortably high for the Fed and ECB. In the US core PCE inflation is expected to print around 0.2% m/m as in August while headline is expected to increase to 0.4% m/m from 0.2% m/m. In the euro area, we expect a decline in headline HICP to 4.4% from 5.3% in August driven by negative energy inflation, lower food prices, and a downtick in core inflation from 5.3% to 4.8%.

In China, we receive the September Caxin PMIs for both manufacturing and services on Friday. After a decent rebound in manufacturing PMIs in August from 49.2 to 51.0 we see downside risks to the September print and expect a decline to 50.5. The series is quite erratic and last month's increase seemed a bit too strong relative to the releases on retail sales and housing.

Other relevant data releases next week are US jobless claims, durable goods orders and conference board consumer sentiment. We expect US real private consumption growth volume to land around zero or even slightly negative. In the euro area, we receive money supply (M3) figures and Ifo figures from Germany. Finally, plenty of focus will also be Fed comments after this week's meeting.

Sunset Market Commentary

Markets

Global PMI’s took center stage today. The eurozone composite measure increased from 46.7 to 47.1 (vs 46.5 expected). The minor increase ended a 4-month decline which took the PMI from a solid 54.1 in April to current contraction levels. The EMU services PMI followed a similar path, gently rebounding from 47.9 to 48.4. The EMU manufacturing PMI stabilized around 43.4, marking the 15th consecutive <50 print. Details showed a further deterioration in the order situation with companies still reducing the stock of purchased goods. However, the destocking process may bottom out over the next few months in line with the worldwide trend, which is an important precondition for the expected recovery of the manufacturing sector at the beginning of 2024. Details of the services PMI showed shrinking business and orders as well, but companies keep hiring. Input and output prices keep rising and should remain top of mind at the ECB. Especially the risk of a wage-price spiral is high. S&P global, responsible for the PMI survey together with Hamburg Commercial Bank, estimates euro zone growth to have dropped by 0.4% Q/Q in Q3 based on the outcome of July/August/September PMI’s. On a national level, France significantly underperformed linked to a deterioration in the luxury goods business and services industry overall.

Markets were wrongfooted by the disappointing French data, published first. They sent German yields over 5 bps lower at the start of European trading. The move didn’t last though with markets recovering as Germany/EMU PMI’s bucked the French trend and with the huge US Treasury sell-off since Wednesday’s FOMC meeting in mind. At the time of writing, German yields add 0.5 bps (2-yr) to 3.5 bps (30-yr). The German 10-yr yield is again testing the cycle top at 2.77%. The German 30-yr yield exceeds 2.9% for the first time since end 2011. EUR/USD followed this intraday pattern, spiking to 1.0620, before rebounding to 1.0650. So far, key support at 1.0611/34 survives. US Treasuries take a breather after this week’s beating with yields 2 to 3 bps lower ahead of in line with consensus September US PMI’s. EUR/GBP tested 0.87 resistance as September UK PMI’s fell short of expectations. The composite gauge declined from 48.6 to 46.8 (vs 48.7) strengthening BoE Bailey’s dovish hold yesterday. UK Gilts outperform with Gilt yields falling up to 5 bps at the front end (2-yr). European and US stock markets test key support levels (EuroStoxx50: 4175, S&P 500: 4335, Nasdaq: 13162) , but avoid a drop lower for now.

News & Views

Governor Ueda spoke after the Bank of Japan this morning kept the policy rate unchanged at -0.1% and the 10-y yield target at 0%. The reason for doing so despite inflation turning out to be sticky well above the 2% target, is “Because we aren’t in a state where inflation accompanied by wage growth — sustainable and stable inflation — is in sight.” Ueda admitted price growth had been faster than expected but sticks to the view that it would start to slow more clearly in coming months. The ultra-easy monetary policy stance has pressured the Japanese yen against the likes of the euro and the dollar. The BoJ governor did not comment on recent moves but said that he was looking at the FX market closely and is in close communication with the government (which carries out FX interventions if they decide to). USD/JPY inches higher today to north of the 148 barrier. The 150 level at which interventions took place in October last year remains in clear sight.

Hungary’s minister for economic development Nagy said the central bank should avoid keeping interest rates too high as inflation slows. The former central bank deputy governor said that excessive real rates could hurt consumption and thwart Hungary’s recovery process. He forecasts CPI inflation to drop from 16.4% in August to below 10% in November and to 8% in December. This compares to a current shadow policy rate of 14%, which in all likelihood is to be lowered to 13% next week to match the regular base rate again. Nagy expects the economy to exit its now one-year long recession in Q3. The forint together with other CE currencies including the CZK and especially PLN strengthened today but pared gains after Nagy’s comments hit the screen. EUR/HUF is currently changing hands around 387.53, marginally down from an 388 open but higher than the 386 intraday low.