Sample Category Title

Crude Oil Price Remains In Uptrend Unless This Level Gives Way

Key Highlights

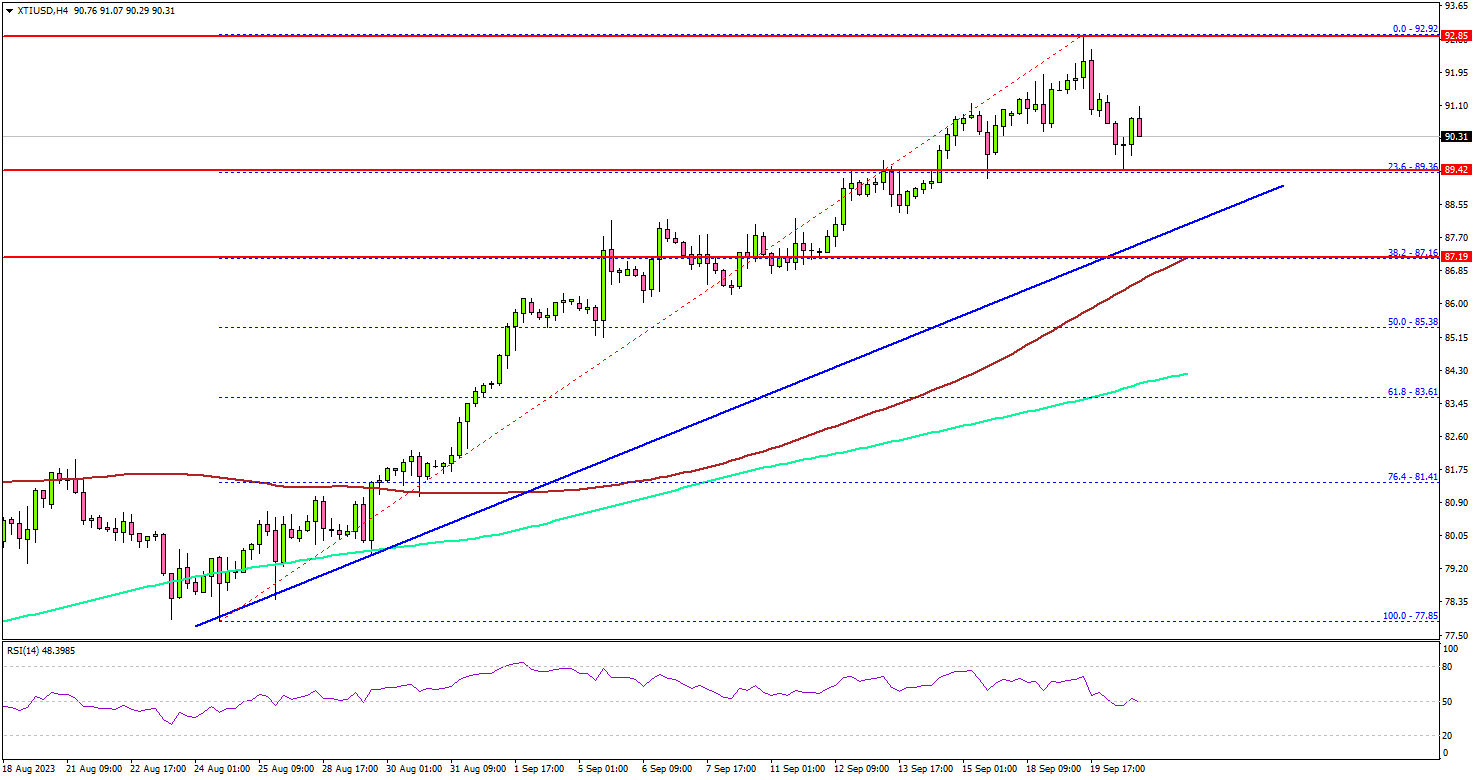

- Crude oil price rallied above the $90 and $92.50 resistance levels.

- A key bullish trend line is forming with support near $88.00 on the 4-hour chart.

- Gold prices failed to clear the $1,950 resistance.

- EUR/USD could recover if it clears the 1.0720 resistance.

Crude Oil Price Technical Analysis

Crude oil price started a fresh increase after a close above $88 against the US Dollar. The price rallied above the $90 and $90.50 resistance levels.

Looking at the 4-hour chart of XTI/USD, the price settled well above the $90 level, the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour).

Finally, it traded to a new multi-week high at $92.92. Recently, there was a minor downside correction below the $91.20 level. However, the bulls seem to be active above the $89.40 level. The 23.6% Fib retracement level of the upward move from the $77.85 swing low to the $92.92 high is also near $89.40.

The next major support sits near the $88.00 zone. There is also a key bullish trend line forming with support near $88.00 on the same chart.

Any more losses might call for a test of the $87.15 support zone or a trend change and drop toward the $82.00 support zone.

On the upside, the price might face resistance near the $92.50 level. The next major resistance is near the $93.20 level, above which the price may perhaps accelerate higher. In the stated case, it could even visit the $95 resistance.

Looking at gold prices, there was a decent increase and the price was able to surpass the $1,935 resistance zone.

Economic Releases to Watch Today

- BoE Interest Rate Decision - Forecast 5.5%, versus 5.25% previous.

- US Initial Jobless Claims - Forecast 225K, versus 220K previous.

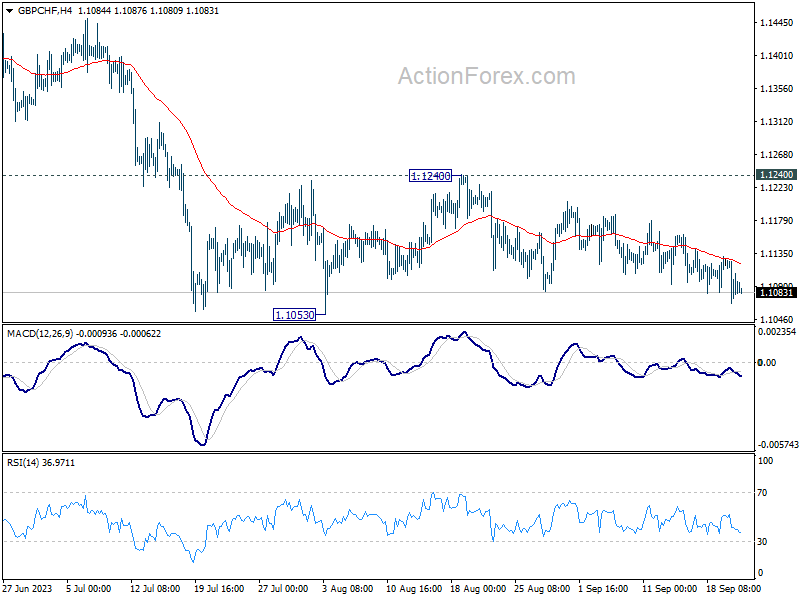

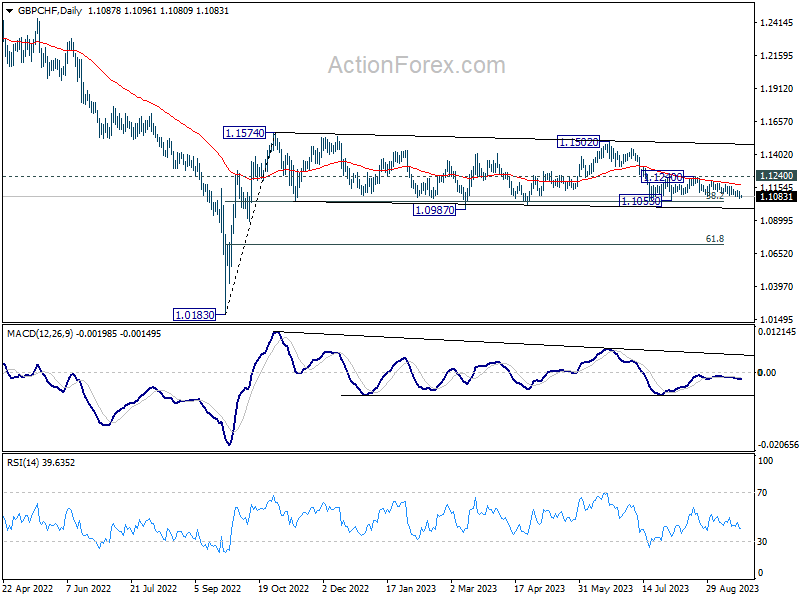

BoE and SNB looms as GBP/CHF awaits Clarity

Today, all eyes are firmly fixed on BoE and SNB rate decisions, which are poised to offer directional cues for the GBP/CHF, hopefully. The pair has been bounded in a constrained range for some time, hungry for a catalyst to redefine its movement.

On one hand, BoE is grappling with the aftermath of lackluster UK inflation data, leaving its imminent rate decision hanging in a delicate balance. The central bank faces two potential paths: embracing a hawkish hold akin to Fed, hence deferring a rate hike while keeping it in the future playbook, or mirroring ECB's strategy with a dovish hike, signaling a peak in the tightening cycle. This undetermined stance has metamorphosed the rate decision into somewhat of a coin toss.

Meanwhile, the consensus among analysts is leaning towards a 25bps hike by SNB, setting the interest rate at a neat 2.00%, thereby drawing the current cycle to a close. This perspective, held by a substantial majority of economists surveyed by Bloomberg, finds reinforcement in the upward revision of the 2024 inflation forecasts tabled by SECO yesterday.

Casting an eye on GBP/CHF, it is currently oscillating within a short-term range between 1.1053 and 1.1240. Presently, its trajectory is hard to pin down. The bearish sentiment is palpable with the pair capped below by 55 D EMA at 1.1709. However, this is offset by the steadfast support at 38.2% retracement of 1.0183 to 1.1574 at 1.1043.

For a clear bearish momentum to materialize, the cross would need to break the 1.1053 support, and then ensuring it sustainably trades below 1.1043 – a weekly close below this fibonacci level would solidify this stance. Yet, a spike lower, followed a substantial rebound could indicate a bullish reversal, hinting at a potential rise past 1.1240 resistance later, to extend the medium term range trading from 1.1574.

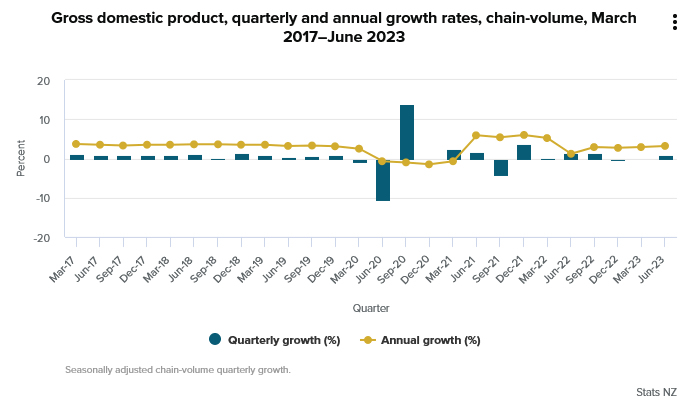

New Zealand’s Q2 GDP outperforms expectations with 0.9% qoq growth

New Zealand's GDP surged by 0.90% qoq in Q2, doubling the expected growth rate of 0.4%. This notable growth is significantly attributed to substantial boost in the business services sector, specifically within the realm of computer system design.

Despite a setback in the primary industries, which contracted by 1.9%, goods-producing industries and service sectors pulled their weight, recording a growth of 0.7% and 1.0% respectively. The service sector emerged as a strong pillar of economic advancement.

The quarter also saw manufacturing sector shake off its lethargy, reversing a trend of decline sustained over five consecutive quarters to contribute positively to the economic pie.

S&P 500 dips on Fed’s definitive hawkish stance

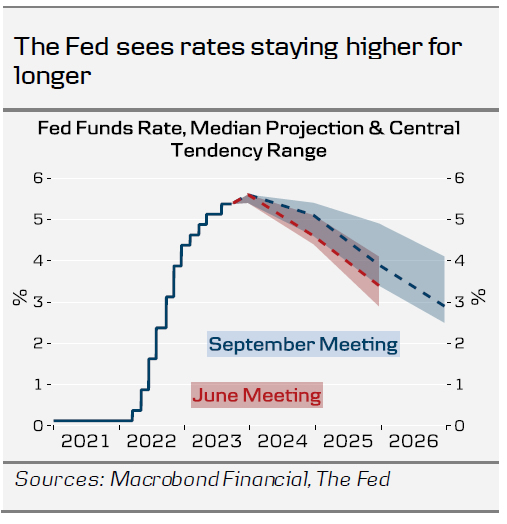

US equities ended their trading session in the red, following a definitive hawkish stance from Fed, even though interest rate was kept unchanged as expected. Fed sent a clear signal that another rate hike is still on the cards this year, and interest rate is going to stay higher for longer. Fed Chair Jerome Powell confirmed in the post meeting press conference, "We're in a position to proceed carefully in determining the extent of additional policy firming."

The new batch of economic projections divulged a prevailing sentiment among 12 of 19 Fed officials in favor of one more rate hike within this year. Investors were taken by surprise not by the rate hike anticipation but by the foreseeing of lesser rate cuts in 2024, a strategic shift attributed largely to the resilient labor market.

Furthermore, the projections hinted at a steeper path for interest rates in the years ahead. Median outlook for federal funds rate was adjusted upwards, settling at 5.1% for 2024, from a prior 4.6%, and 3.9% for 2025, up from 3.4%. This suggests that monetary policy will lean on the tighter side stretching into 2026. A 2.9% funds rate is projected for 2026, marking a divergence from the long-run neutral rate, which remains pegged at 2.5%.

More on Fed:

- Fed Review: Upbeat on Growth

- Message from FOMC Meeting: Higher for Longer

- Fed React: Dollar Pares Earlier Losses after Fed's Attempt of a Hawkish Skip

- Fed stands part, 12 members see one more hike

Reflecting these developments, S&P 500 took a dip, shedding -0.94% or -41.75 points to conclude at 4402.20. In a technical context, S&P 500's movements stemming from 4607.07 are perceived a correction pattern. D deeper slide is on the cards to 4335.31 or even lower.

However, robust support levels are anticipated around the 38.2% retracement of 3491.58 to 4607.07 at 4180.95. This is expected to limit further losses, at least at first attempt. Meanwhile, a close above 55 D EMA (now at 4438.25) will neutralize the bearish outlook.

NZ First Impressions: GDP June Quarter 2023

New Zealand's GDP rebounded 0.9% in the June quarter and there were small upward revisions to the prior two quarters. This suggests more pressure on resources than the RBNZ has been estimating.

NZ GDP, June quarter 2023

- Quarterly change: +0.9% (last: 0.0%, Westpac f/c: +0.8%, market f/c: 0.4%, RBNZ +0.5%)

- Annual change: +1.8% (Last +2.4%, Westpac f/c +1.5%, RBNZ +1.2%)

- Annual average change: +3.2% (Last: +2.9%)

As widely anticipated, New Zealand’s GDP rebounded in the June quarter. Indeed, Statistics NZ reported a 0.9% lift in production – an outcome was well above the market forecast of 0.4% and the Reserve Bank’s most recent forecast of 0.5%. However, it was just 0.1ppts firmer than Westpac’s top of the market estimate of 0.8%.

Adding to today’s surprise were small upward revisions to prior quarters, with the recent December and March quarters revised to -0.5% and 0.0% respectively from -0.7% and -0.1% previously (i.e., the technical recession has been revised away, at least for now). As a result, annual growth in the year through to June stands at 1.8%, which is 0.6ppts above the RBNZ’s forecast and 0.3ppts above our estimate. After allowing for all revisions, the overall size of the economy in the June quarter is 0.5% larger than the RBNZ had estimated in the August MPS.

A portion of that forecast error will likely feed into the RBNZ’s estimate of the output gap, at the margin lifting the Bank’s estimate of the degree of inflation pressure that remained in the economy during that quarter. Given the ongoing uncertainty surrounding these figures – including the likelihood of future revisions – we think that the RBNZ will also choose to draw inference from a wider array of economic indicators in assessing how excess demand and inflation pressures are evolving, including developments in the labour market. Even so, we think that today’s data adds to the likelihood that the RBNZ will, at some point, feel the need to act on the slight tightening bias that it indicated last month.

Stepping back from the recent volatility in quarterly GDP outcomes, momentum in the economy is slowing with annual growth of 1.8% in the year to June down from the (upwardly revised) 2.4% growth recorded in the year to March. The economy is growing at a below trend pace, as reflected in the gradual increase in the unemployment rate over the past year. While rapid population growth is supporting demand, it is also helping to boost the economy’s productive capacity, and over the past three quarters cumulative output has declined in per capita terms. So despite today’s data, with past monetary policy tightening steadily gaining traction as mortgages are refinanced, and low commodity prices now weighing on rural incomes, we expect the economy will continue to flirt with recession over the coming quarters. Indeed, the BNZ-BusinessNZ PMIs suggest that the economy may be contracting in the current quarter, and annual growth in the year to September is likely to be close to nil.

As a result, we expect that the unemployment rate will remain on an upward trajectory, contributing to a gradual easing of inflation pressures. However, especially after today’s release, it remains to be seen whether inflation pressures will dissipate quickly enough to satisfy the RBNZ. On that score, attention will now turn to the various cost and pricing indicators in next month’s QSBO business survey and in the September quarter CPI report.

Detail

There were no huge surprises in the industry detail of today’s GDP report, which was broadly in line with what had been signalled by the various partial indicators released in recent weeks. As we had expected growth was driven by the services sector, with especially strong growth recorded in the public administration and safety sector (+2.8%) and business services sector (+2.1%). The education and training sector, transport and storage, and utility sectors also reported strong growth this quarter.

On the negative side, as expected growth was weighed down by lower activity in the retail trade and accommodation (-1.0%) and wholesale trade (-0.5%) and sectors. There were also declines in the forestry, fishing and construction sectors.

The expenditure-based measure of GDP, which is a slightly more volatile measure of activity, increased 1.3% in the June quarter and 1.9% in the year to June. This measure indicated a strong rebound in exports and strong growth in business investment and government consumption spending.

Fed Review: Upbeat on Growth

- The Fed maintained Fed Funds Rate target unchanged at 5.25-5.50% as widely anticipated, but surprised hawkishly with clearly more optimistic projections.

- Median growth forecasts were revised higher for 2023-2024, warranting a 50bp upward revision to both 2024 & 2025 median rate projections.

- We remain more pessimistic on the economic outlook, and make no changes to our Fed call. We still expect no further rate hikes, and quarterly 25bp cuts starting from Q1 2024.

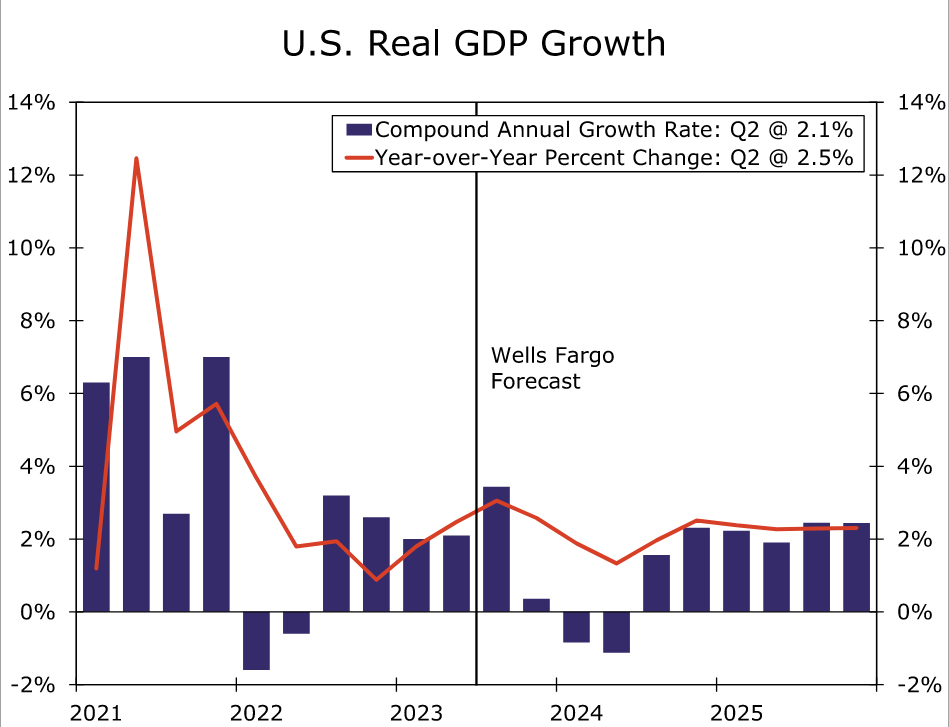

Powell delivered a 'hawkish hold', as the updated economic projections outlined an optimistic path towards soft(-er) landing. Real GDP forecasts were revised up to 2.1% (from 1.0%) for 2023 and 1.5% (from 1.1%) for 2024, while inflation forecasts only received minor adjustments. Median forecast for unemployment rate was also revised higher, with the peak now seen at only 4.1% in 2024-2025 (from 4.5%).

Powell underscored that the more optimistic growth outlook warrants rates remaining higher for longer, and the median 'dots' were revised up by 50bp for both 2024 (5.1%) and 2025 (3.9%). Markets erased some of the cuts priced in for 2024, with 2y UST yield rising some 12bp. Powell mentioned solid realized data and recovering real income growth as factors lifting the outlook, and while the looming government shutdown and UAW strike were seen as downside risks, they have not materially impacted the baseline view for now.

The FOMC statement was mostly unchanged, economic growth was described as 'solid' rather than 'moderate' while job gains were seen 'slowing' rather than 'robust'. Powell also maintained strong emphasis on data-dependency.

A key factor driving the renewed hawkish market reaction during the press conference was Powell's surprisingly open view regarding potentially higher neutral rate. While the longer-term Fed Funds Rate estimate was unchanged at 2.5%, Powell mentioned that it does not necessarily suggest that neutral rate could not be higher, which in turn would suggest monetary policy is not as restrictive as previously thought. While not our base case, we discussed the idea and potential drivers back in August, see Research US - Could investment boom pave the way for a soft landing?, 22 August.

In any case, the Fed anticipates that the economy is going to remain more resilient to the effects of restrictive monetary policy than we do. In our Fed preview, 15 September, we highlighted recent tightening in financial conditions and already restrictive level of real rates are key headwinds for the economy, and ever since the latest University of Michigan consumer survey confirmed a further decline in inflation expectations. Powell explicitly mentioned that higher real rates due to declining inflation could warrant earlier rate cuts, and we still stick to our view of quarterly 25bp cuts starting from Q1 2024.

Also, while the 'dots' were 7-12 in favour of one more rate hike later in the year, we doubt it will materialize. This would imply downward pressure on UST yields going forward, but if we will be proven too pessimistic on our macro outlook by incoming data, rates are likely to remain higher for longer than what we assume.

FX: Near-term USD tailwinds could be fading

EUR/USD moved lower around a half figure on the hawkish hold from the Fed. The outcome was about as hawkish as the Fed could have engineered without actually delivering a surprise hike. Despite the ongoing USD strength, we think there could be some potential for some EUR/USD tailwinds in the near-term. We think that peak policy rates, improving manufacturing sector relative to the service sector and/or easing pessimism priced on China could add some support to EUR/USD within the next month. On the longer horizon, however, we maintain our strategic case for a lower EUR/USD, expecting the cross at 1.03 in 12M.

Message from FOMC Meeting: Higher for Longer

Summary

- As widely expected, the FOMC kept its target range for the federal funds rate unchanged at 5.25%-5.50% at today's policy meeting. The decision to keep rates unchanged was unanimously supported by all twelve voting members of the Committee.

- The statement noted that job gains remain strong, and it continued to characterize inflation as "elevated." The Committee also reiterated in the statement that "additional policy firming may be appropriate."

- The Summary of Economic Projections, which highlights the macroeconomic forecasts of the Committee members, was more optimistic than in June. Specifically, median forecasts of GDP growth for this year and 2024 were revised higher, while forecasts of the unemployment rate were revised lower.

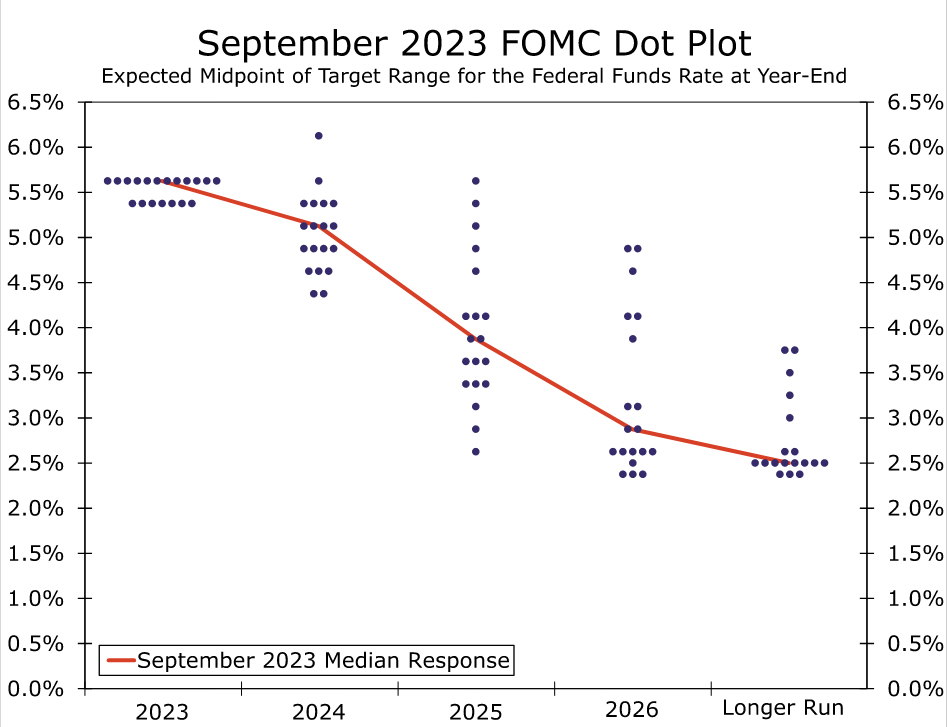

- The so-called "dot plot" showed that 12 of the 19 Committee members believe that another 25 bps of rate hikes would be appropriate by the end of this year. Furthermore, the dot plot shows that only 50 bps of policy easing would be appropriate next year, considerably less than the 100 bps of rate cuts that were forecasted in June.

FOMC Remains on Hold but Continues to Think Further Policy Tightening May Be Appropriate

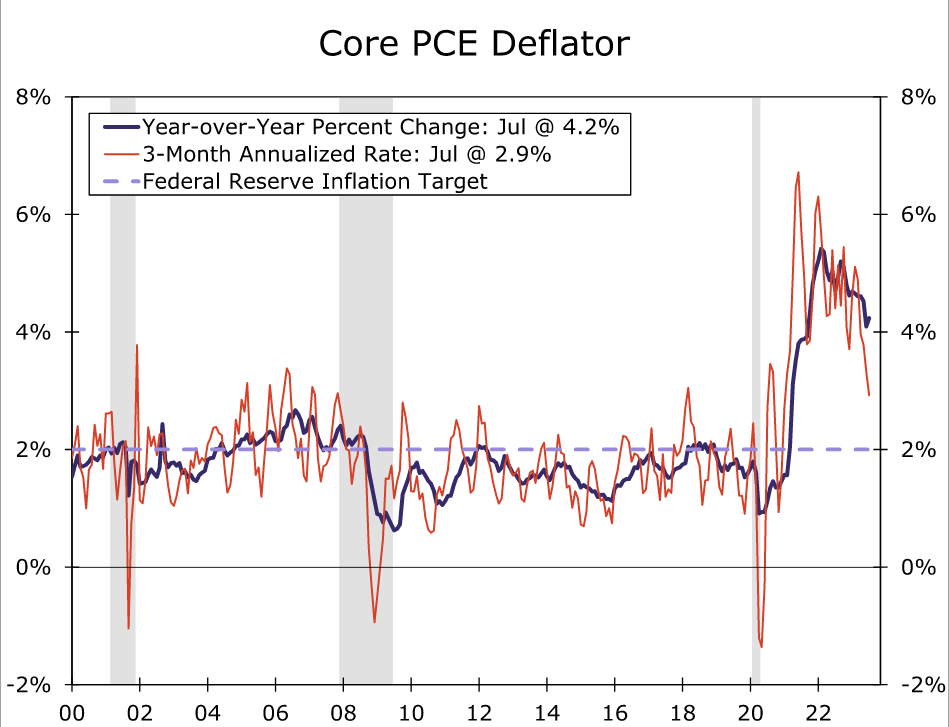

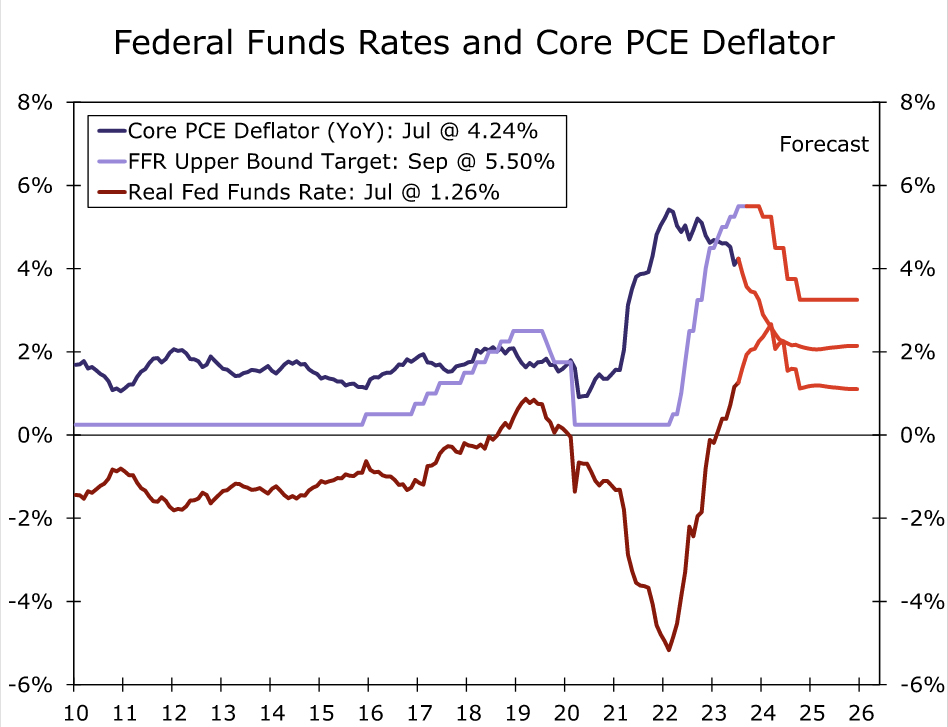

As universally expected, the Federal Open Market Committee (FOMC) decided at today's meeting to keep its target range for the federal funds rate unchanged at 5.25%-5.50%. All twelve voting members of the Committee supported today's decision to keep rates unchanged. In the statement that announced the decision, the FOMC said that "economic activity has been expanding at a solid pace." Although "job gains have slowed in recent months," they "remain strong." The Committee continued to characterize inflation as "elevated." Indeed, the year-over-year rate of core PCE inflation, which is the Fed's preferred measure of the underlying rate of consumer inflation, printed at 4.2% in July, although the 3-month annualized change slipped below 3% (Figure 1). Nevertheless, core PCE inflation remains above the FOMC's 2% target.

As has become standard boilerplate, the Committee said that it "will continue to assess additional information and its implications for monetary policy." In that regard, the FOMC retained a hawkish bias by re-iterating that "additional policy firming may be appropriate to return inflation to 2 percent over time." As we will discuss further below, this bias was represented in the so-called "dot plot."

Median Dot for 2024 Revised Higher

Following its usual quarterly procedure, the Committee released an update to its Summary of Economic Projections (SEP), in which each FOMC member outlines his or her macroeconomic forecasts. As we anticipated in our recent report that outlined our expectations for the FOMC meeting, the median GDP growth forecast for 2023 rose from 1.0% in the June SEP to 2.1% today. This revision reflects the run of stronger-than-expected economic data that have been released since the June 14 meeting. At the same, the median projection for the unemployment rate at the end of this year fell to 3.8% from 4.1% previously, reflecting the continued resilience of the labor market. The FOMC also seems to think that a "soft landing" for the economy is increasingly likely. The median forecast for real GDP growth in 2024 was revised up to 1.5% from 1.1% in the June SEP, while the forecast for the unemployment rate fell to 4.1% from 4.5%.

The median forecast for core PCE inflation at the end of this year edged down to 3.7% from 3.9% in the June SEP. Notably, all FOMC members forecast that PCE inflation, whether measured by the overall rate or by the core rate, will remain above 2% at the end of next year.

These macroeconomic forecasts undoubtedly influence the placement of the dots in the dot plot. The median dot for the end of 2023 remains at 5.625% (i.e., the midpoint of a 5.50%-5.75% target range), which is unchanged from the June SEP. In other words, 12 of the 19 members of the FOMC think it would be appropriate to hike rates by 25 bps at either the November 1 meeting or at the final meeting of the year on December 13. Furthermore, there was an important change for next year. In June, the median dot for 2024 stood at 4.625%, which indicated 100 bps of rate cuts next year would likely be appropriate. The median dot today stands at 5.125%. If the FOMC does indeed raise rates by 25 bps by the end of this year, then the Committee would cut rates by only 50 bps in 2024. Although the median dot for 2025 currently stands at 3.875%, there is a wide dispersion in the forecasts, which should be expected of a forecasted variable more than two years from now. In sum, the message from the FOMC today is higher for longer, in terms of interest rates (Figure 2).

We tend to side with the seven FOMC members who believe that no further rate hikes are needed this year, although we acknowledge the risk that the Committee could indeed hike one more time. As we outlined in our most recent U.S. Economic Outlook, monetary policy will tighten passively in coming months (Figure 3). That is, even with the FOMC on hold, the real fed funds rate will creep higher in coming months if, as we forecast, inflation continues to recede. This rise in real interest rates will exert stronger headwinds on the economy, which we believe will lead to a modest contraction in economy activity next year (Figure 4). We then look for the FOMC to cut rates by more than the market (and most Committee members) currently expect. Not only will lower rates be appropriate if the economy weakens, but the FOMC will need to cut rates just to prevent an upward creep in the real fed funds rate.

Fed React: Dollar Pares Earlier Losses after Fed’s Attempt of a Hawkish Skip

- Fed kept rates steady; target range remained at 5.25%-5.50% (as expected)

- Dot plots showed 12 of 19 expected policymakers (12 also called for one more hike in June)

- Fed projections saw rate cut bets halved from June’s 5.10% to 4.60%

US stocks dropped and king dollar returned after the Fed kept rates unchanged and signaled one more rate hike will happen this year. The US economy is too strong and this rate hiking cycle will last a lot longer than Wall Street wants.

It is clear that higher-for-longer will be the Fed’s theme for a while given the summary of economic projections (SEP) revisions. The slowing economy will happen, but the growth and unemployment targets that the Fed is setting is concerning. The FOMC statement noted that “Tighter credit conditions for households and businesses are likely to weigh on economic activity, hiring, and inflation. The extent of these effects remains uncertain.”

If we continue to see an extended period of time that the economy performs well, the growth/inflation mix will lead to a harder hitting lag from their rate hiking cycle.

The Fed still believes the soft landing will happen, but a few more stickier inflation reports and that will make those 2024 rate cut bets disappear. Higher rates are not going away as it seems US economic resiliency is here to stay. The 2-year Treasury yield initially surged on the release of the statement and SEP, rising 4bps to over 5.14%.

Fed Chair Powell’s opening emphasized a long list of reasons on why they will need to keep up the hawkish rhetoric: The economy has been expanding faster than expected this year. Consumer spending has been “particularly robust.” Housing has “picked up somewhat.”

The path of policy will adjust meeting by meeting, but it seems the incoming data might support additional tightening by year-end. Powell’s comment that the Fed is in a position to proceed carefully on firming rates took away some of their hawkishness.

Powell wants convincing evidence that inflation is under control and that won’t be happening anytime soon given the gas price trajectory and the current state of the labor market.

Dollar firmer post Powell (EUR/USD 5-minute chart):

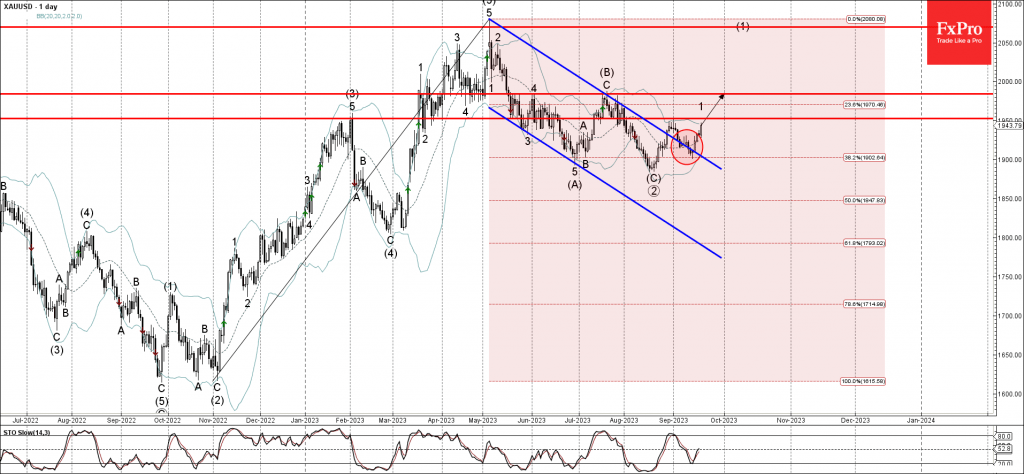

Gold Wave Analysis

- Gold rising inside minor impulse wave 1

- Likely to reach resistance at 1985.00

Gold continues to rise inside the minor impulse wave 1, which reversed earlier from the upper trendline of the recently broken down channel from May.

The active impulse wave 1 belongs to the intermediate impulse wave (1) from the end of August.

Given the strong daily uptrend, Gold can be expected to break the next resistance at 1950.00 and to rise further toward the next resistance level 1985.00.

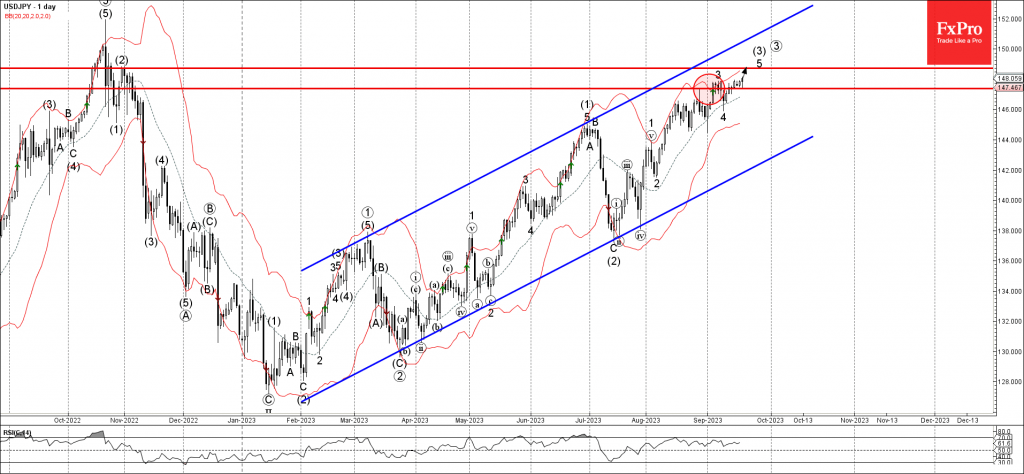

USDJPY Wave Analysis

- USDJPY broke the resistance level 147,40

- Likely to riseW to resistance level 147.70

USDJPY currency pair recently broke the resistance level 147,40 (which has been reversing the price from the start of September).

The breakout of the resistance level 147,40 accelerated the active impulse wave 5 of the intermediate impulse wave (3) from the middle of July.

Given the clear daily uptrend, USDJPY currency pair can be expected to rise further toward the next resistance level 147.70.