Sample Category Title

Gold Holds Steady Within Fresh Range Near 4,500

- Gold pares gains below uptrend line on softer Dollar.

- Dip‑buyers emerge, but upside remains limited.

- Momentum signals maintain a neutral‑to‑bearish stance.

Gold is holding steady near 4,500 on Monday, attempting to build on last session’s 2.5% rebound as a softer dollar offsets fading rate‑cut expectations. Still, the precious metal struggles to attract strong dip‑buying interest amid a bearish technical backdrop after falling more than 15% this month.

Price action remains range‑bound in a bearish consolidation phase below the medium‑term ascending trendline and the 100‑day SMA. Momentum indicators reinforce this hesitation – the MACD remains in negative territory, showing persistent downward pressure, while the RSI is flatlining just above oversold levels, suggesting bearish momentum is easing but not reversing. Last week’s rebound from the 200‑day SMA near 4,000 therefore remains on fragile footing.

Initial resistance sits at 4,600, the 38.2% Fibonacci retracement of the March 2-23 pullback, aligning with the 100‑day SMA. A break above could open the way to the 50% Fibonacci level at 4,758, followed by the 20‑day SMA, currently in a bearish crossover with the 50-day SMA, near 4,850.

Support emerges near 4,375, where recent lows have held, followed by deeper support around 4,300 if sellers regain control. Below that, the 200‑day SMA in the 4,000-4,150 zone remains critical.

Summing up, Gold has snapped a three‑week losing streak, but the modest recovery from multi‑month lows remains volatile. A sustained move back above the uptrend line is needed to shift the precious metal onto more stable ground.

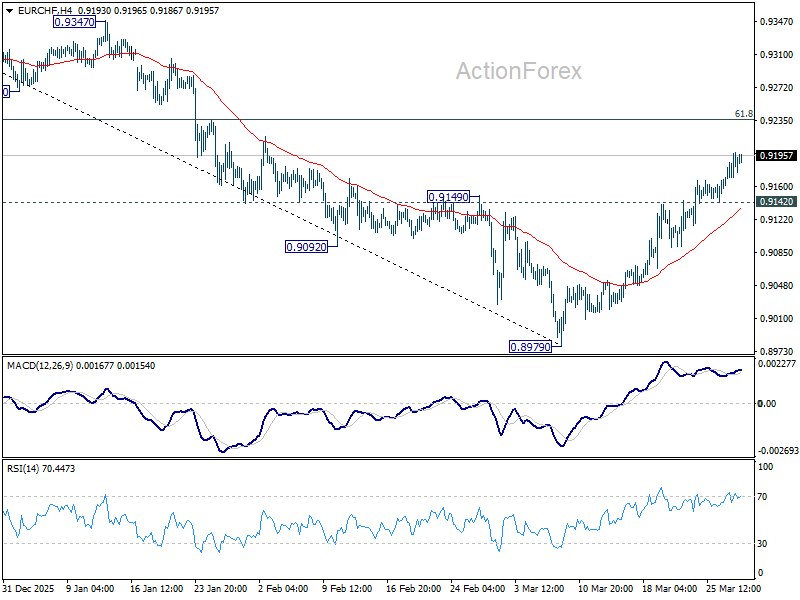

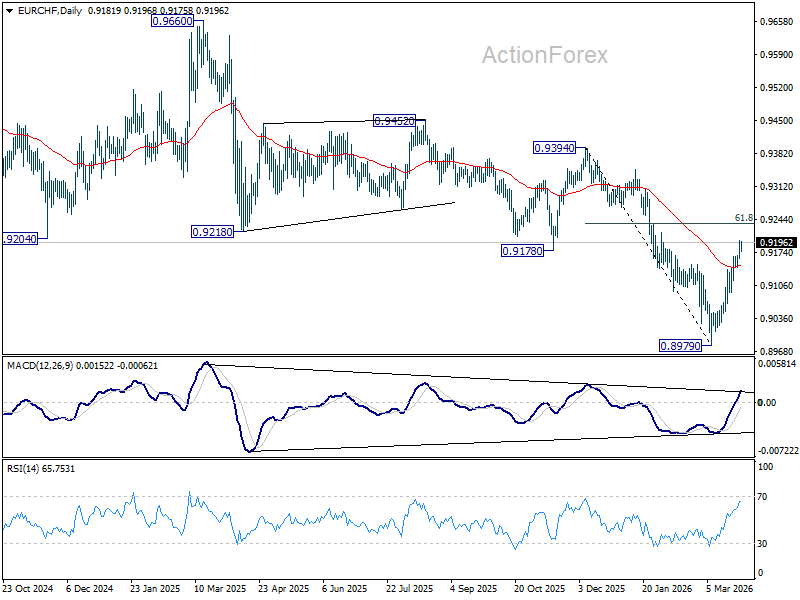

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9168; (P) 0.9186; (R1) 0.9214; More....

Intraday bias in EUR/CHF stays on the upside at this point. Rise from 0.8979 short term bottom is in progress to 61.8% retracement of 0.9394 to 0.8979 at 0.9235. Sustained break there will pave the way to 0.9394 key resistance next. On the downside, below 0.9142 minor support will turn intraday bias neutral again first.

In the bigger picture, as long as 55 W EMA (now at 0.9286) holds, the larger down trend from 0.9928 (2024 high) is still expected to continue through 0.8979 at a later stage. However, sustained break of 55 W EMA should confirm medium term bottoming, and bring stronger rise through 0.9394 resistance, even as a corrective move.

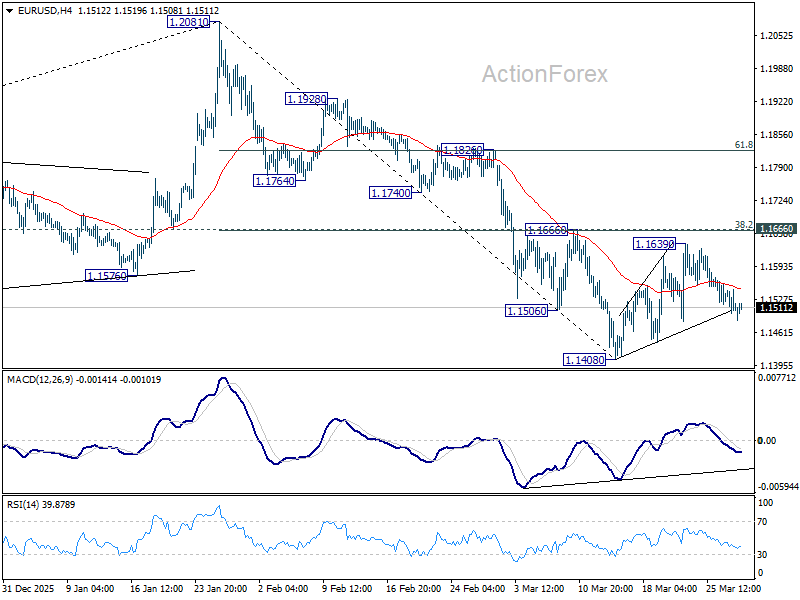

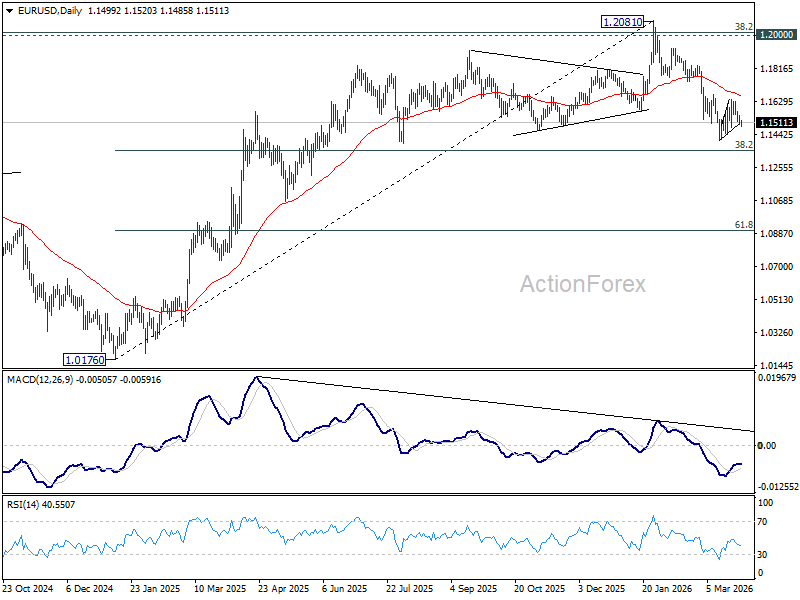

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1491; (P) 1.1520; (R1) 1.1537; More….

Range trading continues in EUR/USD and intraday bias remains neutral. Further decline is expected with 1.1666 cluster resistance (38.2% retracement of 1.2081 to 1.1408 at 1.1665) intact. On the downside, firm break of 1.1408 will resume the fall from 1.2081 to 38.2% retracement of 1.0176 to 1.2081 at 1.1353. However, decisive break of 1.1666 will argue that the fall from 1.2081 has completed, and turn bias back to the upside for 61.8% retracement of 1.2081 to 1.1408 at 1.1824.

In the bigger picture, prior break of 55 W EMA (now at 1.1497) should confirm rejection by 1.2 key cluster resistance level. The whole up trend from 0.9534 (2022 low) might have completed as a three wave corrective rise too. Deeper fall is expected to long term channel support (now at 1.0535). Meanwhile, risk will stay on the downside as long as 1.2081 holds, even in case of strong rebound.

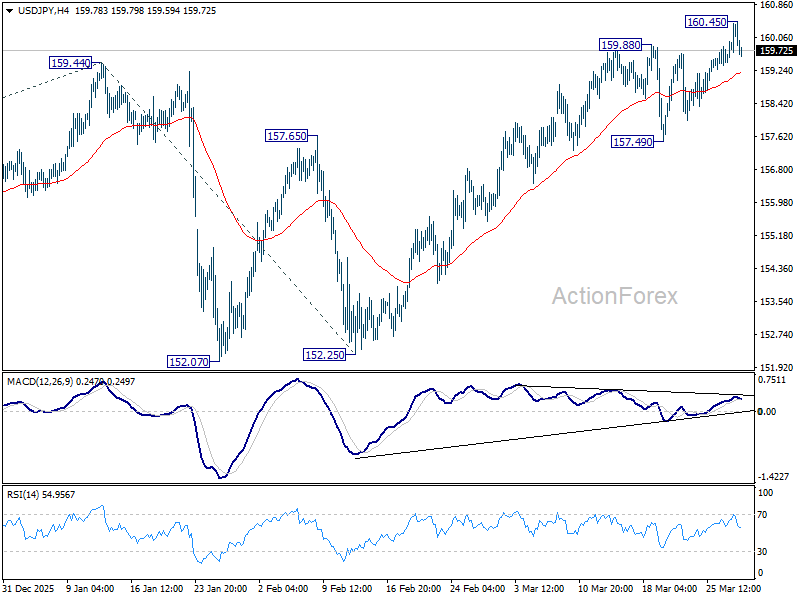

USD/JPY Daily Outlook

Daily Pivots: (S1) 159.70; (P) 160.05; (R1) 160.65; More...

Intraday bias in USD/JPY is turned neutral with current retreat. Some consolidations would be seen but further rally is still in favor. Above 160.45 will bring retest of 161.94 high. Nevertheless, considering bearish divergence condition in 4H MACD, sustained break of 55 4H EMA will indicate short term topping, and turn bias to the downside for 157.94 support instead.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.97) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

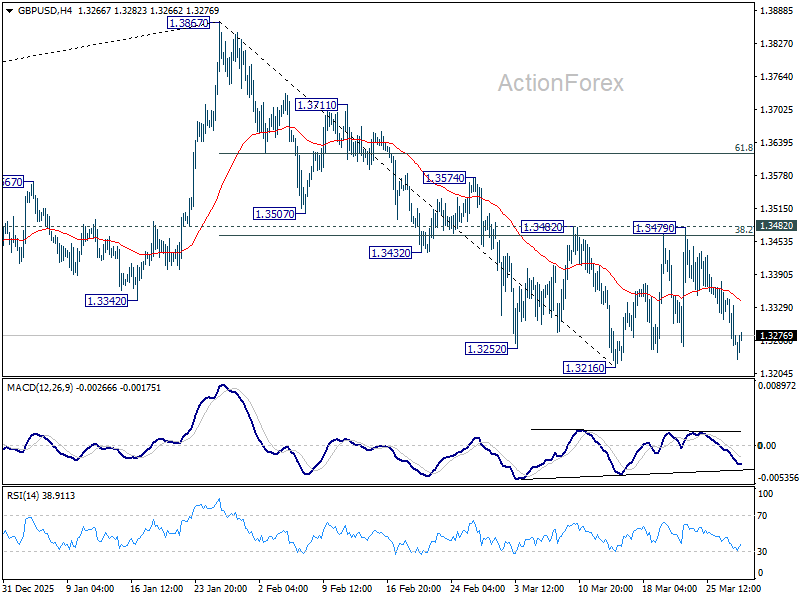

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3229; (P) 1.3289; (R1) 1.3318; More...

GBP/USD recovers mildly ahead of 1.3216 support as range trading continues. Intraday bias stays neutral first. Further decline is expected with 1.3482 resistance intact. On the downside break of 1.3216 will resume the fall from 1.3867 to 1.3008 structural support. However, decisive break of 1.3482 will argue that the fall from 1.3867 has completed, and turn bias back to the upside for 61.8% retracement of 1.3867 to 1.3216 at 1.3618.

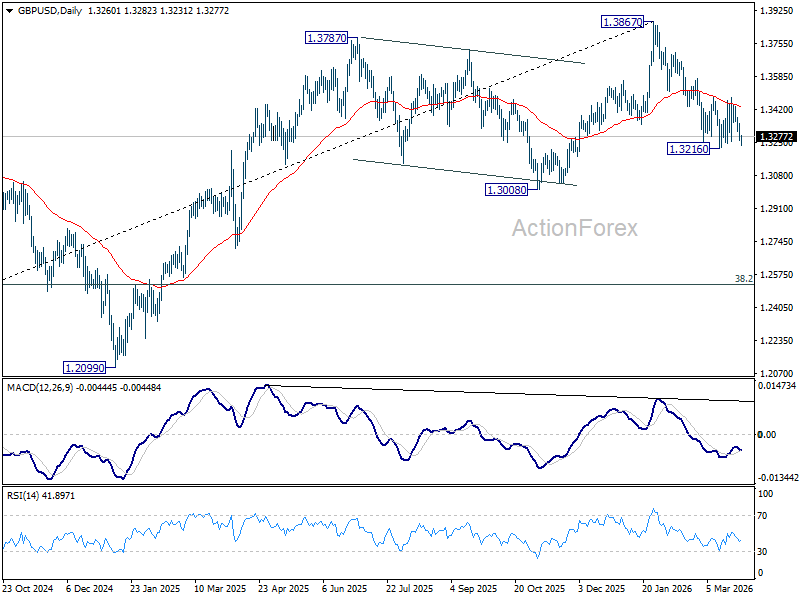

In the bigger picture, considering bearish divergence condition in both D and W MACD, a medium term top should be in place at 1.3867. Firm break of 1.3008 support will argue that fall from 1.3867 is at least correcting the rise from 1.0351 (2022 low) with risk of bearish reversal. That would open up further decline to 38.2% retracement of 1.0351 to 1.3867 at 1.2524. For now, medium term outlook will be neutral at best as long as 1.3867 resistance holds, or until further development.

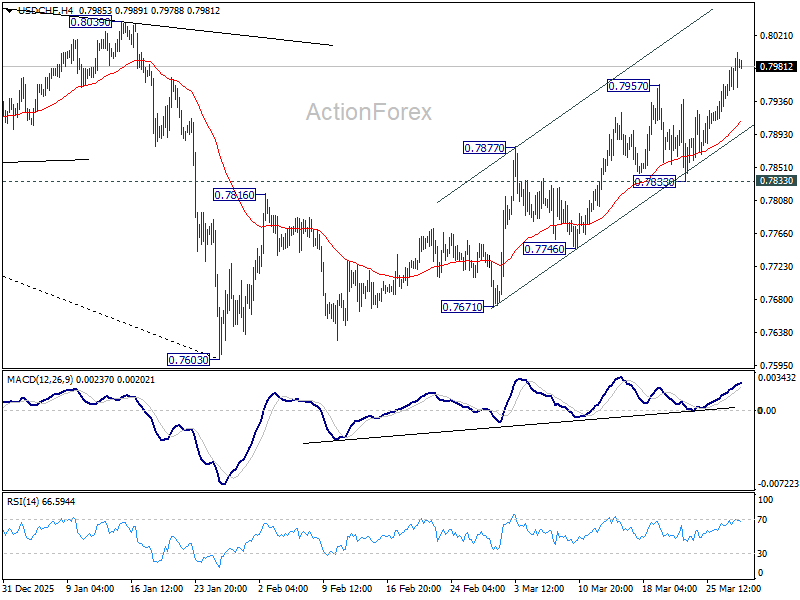

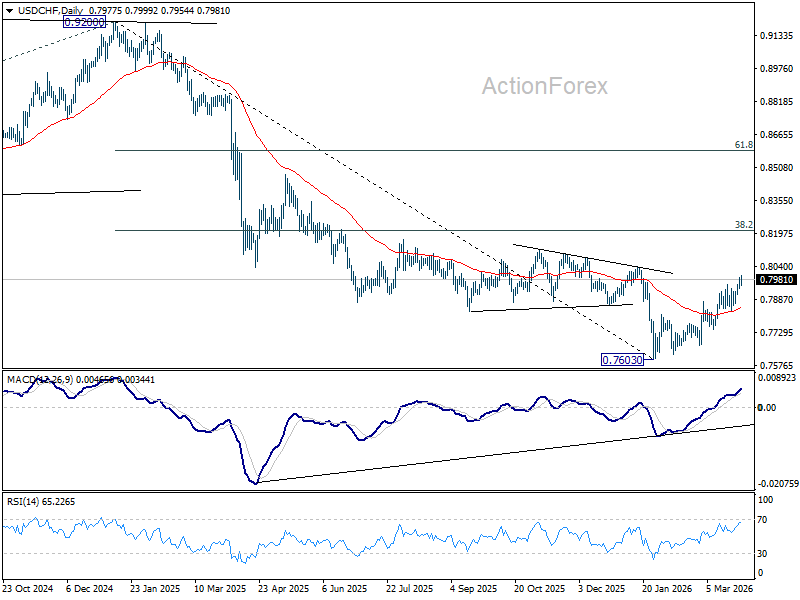

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7955; (P) 0.7974; (R1) 0.8009; More….

Intraday bias in USD/CHF remains on the upside at this point. Current rise from 0.7603 should target 38.2% retracement of 0.9200 to 0.7603 at 0.8213. For now, further rally is expected as long as 0.7833 support holds, in case of retreat.

In the bigger picture, a medium term bottom should be in place at 0.7603 on bullish convergence condition in D MACD. Rebound from there is seen as correcting the fall from 0.9200 only. However, decisive break of 55 W EMA (now at 0.8088) will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high). On the other hand, rejection by the 55 W EMA will setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage.

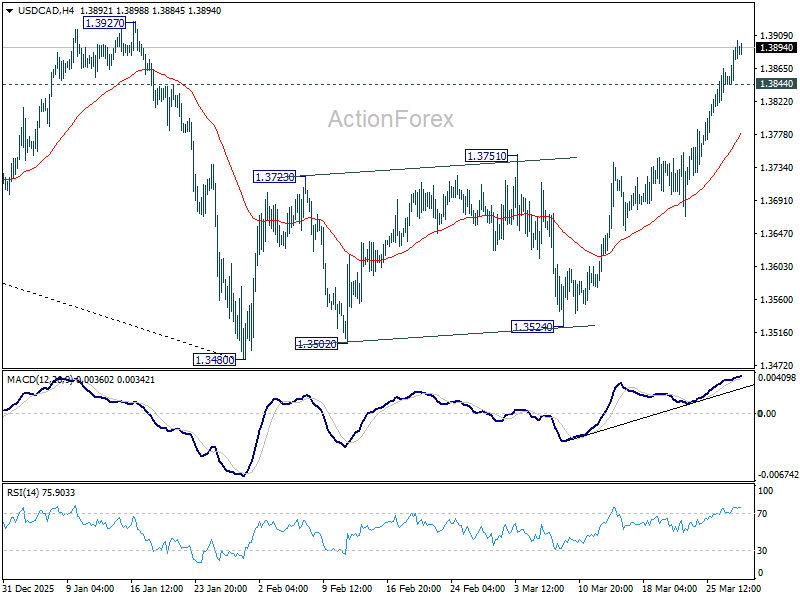

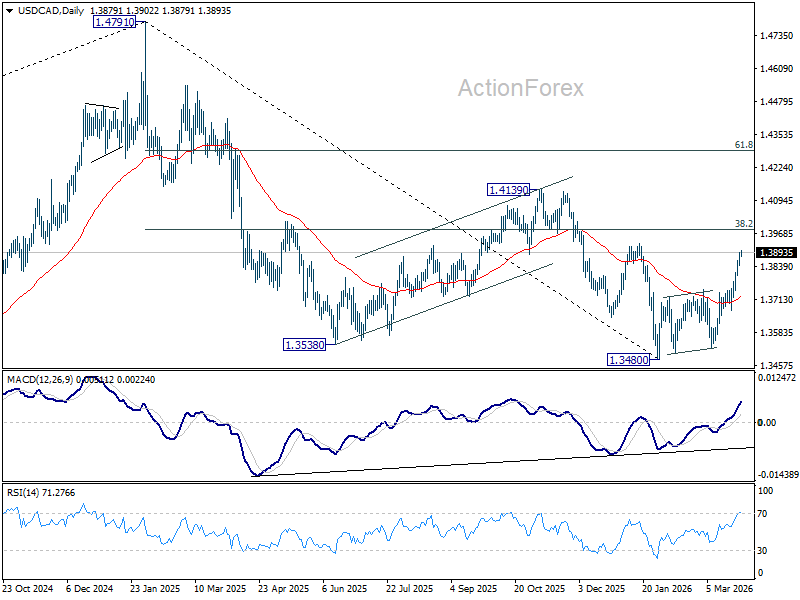

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3860; (P) 1.3880; (R1) 1.3915; More...

Intraday bias in USD/CAD remains on the upside for the moment. Current rally from 1.3480 is in progress for 38.2% retracement of 1.4791 to 1.3480 at 1.3981. Decisive break there will argue that it's already reversing the whole down trend from 1.4791, and target 61.8% retracement at 1.4290. On the downside, below 1.3844 minor support will turn intraday bias neutral first. But risk will stay on the upside as long as 1.3751 resistance turned support holds, in case of retreat.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, break of 1.3927 resistance will argue that the correction has completed with three waves down to 1.3480 already. Further break of 1.4139 will confirm and bring retest of 1.4791 high.

The TACO-Trade Met It’s Maker

Markets

The TACO-trade met it’s maker. “Iran Never Chickens Out” pushed the US tech-heavy Nasdaq index into correction territory last week, trading around 12.50% off the all-time high reached in January (20948 close vs 24020). From a technical point of view, we rapidly approach 38% retracement on the rally that followed the early Liberation Day mess (20492), the 2024 high (resistance-turned-support) at 20205 and the target of the double top formation that formed during Q4 2025 and Q1 2026 (19776). The S&P 500 is currently 9% below its record (6356 close vs 7002) with more or less similar technical references at 6174 (38% retracement), 6147 (2025 high) and 6102 (target double top). The Eurostoxx 50 trades already 13.3% below the all-time high (5506 close vs 6200) and narrowly closed above 5500 support last week. The next line of defense stands at 5370 which is 50% retracement on the post Liberation Day rally. From a momentum point of view, the pace of the equity sell-off especially started accelerating in the US last week. Weekly differences on bond markets were more limited last week, thanks to a strong rebound of US Treasuries during Friday’s US session. Volatility remains extremely high though. After the initial hawkish front end repositioning, more and more harm is being done at the longer end of the curve as inflation risk premia start drifting away. The dollar stands its ground in FX space. The trade-weighted dollar closed last week above the 100-mark (100.36 March high), EUR/USD ended just above 1.15 (1.1411 March low) and USD/JPY broke the 160-mark for the first time since July 2024, prompting direct verbal intervention treats by Japanese officials.

The first marker on our market-dashboard continues to signal escalation risks and keeps above-mentioned momentum trades going. Brent crude moves above $115/b, approaching the highest level since the start of the war ($119.5). Rumours of a US ground invasion, either seizing the strategic Khargh (oil) island or even trying to extract Iran’s uranium go in the mix with Houthi’s joining Iranian war efforts (first attacks on Israel) and Iranian strikes on aluminum plants in Abu Dhabi and Bahrain. The latter pushed futures on the London Metal Exchange up by the most since 2024 (+4-6%) as they disrupt stretched supply chains even more. Today’s eco calendar contains EC economic confidence indicators and German March inflation numbers. Spanish figures at the end of last week reflected the energy supply shock though rose slightly less than consensus (+1% M/M and 3.3% Y/Y from 2.3% Y/Y; core stable at 2.7% Y/Y). US Fed Chair Powell participates in a moderated discussion at Harvard University, but don’t expect him to elaborate as much as for example the ECB on the Fed’s reaction function. Steady remains the key principle for the Federal Reserve.

News & Views

The European Commission proposed some general principles in trying to coordinate EU countries’ response to the energy price surge. Such coordination is deemed essential to prevent market fragmentation and leverage economies of scale. The EC has also learned from 2022 in that many of the measures back then were broad and untargeted, leading to inefficiencies and a huge fiscal price tag. The EC’s preferred option is to support only the most vulnerable households because that would not distort the price signal too much. EU countries could also lower electricity taxes but the Commission warns for the hole it could punch in budget revenues at a time when deficits and debt are already high. The EC is also suggesting a form of two-tier pricing for electricity and/or natural gas as a way to blunt the impact for vulnerable households and firms. Whatever measure taken, the EC said it should have a clear end-date.

Rating agency Fitch affirmed Israel’s rating steady at A with a negative outlook. The rating itself balances a “diversified, resilient and high value-added economy and strong external finances against a high public debt/GDP ratio, still high security risks, and a record of unstable governments that has hindered policymaking”. The negative outlook is a reflection of a projected continued rise in public debt on deficits nearing 6% of GDP this year, which is already well above the A median, as well as war-related tail risks that may weaken Israel’s growth prospects and its fiscal trajectory. The latter could remain unaddressed due to the fractious domestic political environment. Fitch forecasts debt to rise from 71.4% this year to 72.5% in 2027 with further increases in subsequent years. Growth is projected to pick up from 2.9% last year to 3.5% in 2027 with inflation remaining close to the mid-point of the 1-3% central bank target through 2027.

Escalation Continues

Middle East tensions escalated over the weekend as around 3’500 US troops came to the region – increasing the chances of a ground operation that will likely last weeks – and Iran-backed Houthis joined the war. That’s a big deal as their inclusion brings new uncertainty regarding trade through the Red Sea, at a time when disruption in the Strait of Hormuz is taking a toll on global energy and other essential goods flows – including fertilizers. Saudi, remember, had redirected its oil exports to the Yanbu port on the Red Sea and was able to export around 5mbpd of oil – a bit less than the roughly 7mbpd export capacity through the Strait of Hormuz. So now, shipping through the Red Sea is also becoming risky.

Escalation and expansion of the Middle East conflict sent crude oil and aluminium up at the open. Aluminium prices jumped more than 5% in Asia after Iran struck aluminium producers in Bahrain and the UAE over the weekend. US crude approached the $105pb level before retreating slightly to just below $103pb at the time of writing, while Brent crude flirted with the $110pb mark. There are bets that crude could rise to $150 and even to the $200pb level if the war doesn’t end quickly. I believe that demand would be heavily hit if prices go that high. Above $120–130pb, global recession odds would take the upper hand and tame upside pressure.

What’s certain, however, is that the persistent rise in oil prices continues to fuel global inflation and stagflation bets, as tighter monetary policies from global central banks could slow down demand, but not fully reverse an external inflation shock – leaving many economies with high inflation and rising unemployment. That’s the definition of stagflation.

The latter will – at some point – ease the latest hawkish shift in central bank expectations: a sharp economic slowdown could convince central banks to act less aggressively.

The Japanese 10-year yield opened the week at a fresh multi-year high, near 2.38%, but slightly eased, while the US 2-year yield is softer this morning. This slight rebound in sovereign bonds could explain why S&P 500 futures have slightly turned positive this morning, but there is no doubt that the unideal geopolitical and macroeconomic backdrop will continue to weigh on risk appetite.

The S&P 500 fell more than 2% last week – it was the fifth consecutive week of losses – while the Nasdaq 100 sank more than 3%. Losses since the January peak have now surpassed 10%, meaning that the index has entered correction territory, with risks only building for a deeper pullback. The VIX index ended last week above the 30 level, while volatility across sovereign bonds has also reached eye-watering levels. High volatility in both stocks and bonds has led to one of the largest monthly declines in 60/40 portfolios since 2022. Last week’s weak Treasury auctions only came as confirmation that investors remain worried.

Inside tech, CrowdStrike has become the latest victim of AI anxiety. The stock price fell nearly 6% on Friday after Anthropic’s Mythos AI model advanced cyber capabilities, decreasing the need for certain security services. Meta also tanked 4%. The selloff followed ongoing legal problems regarding the addictive nature of the platforms harming young users, but the latter is likely a trigger and not the main cause. Investors have been growing uncomfortable with massive AI spending (increasingly financed by debt), and indeed we have seen a similar drop across other Magnificent 7 stocks, for companies that are not involved in legal issues like Amazon.

So this week, investors will continue to watch Middle East developments, oil and energy prices, and their impact on inflation and central bank expectations.

The US dollar has pushed above the 100 level, helped by safe-haven demand and higher oil prices. But gains have been limited as the USDJPY bounced lower after shortly trading above the critical 160 level – a level that makes Japanese authorities uncomfortable and highly likely to act. And indeed, the country’s FX chief said that they could take bold action in the FX markets if the yen depreciation continues. This confirms that there is no juice left to be squeezed out of the USDJPY as speculative positions don’t have enough margin to tolerate a currency intervention. Of course, the yen will remain under pressure against the dollar, but any intervention – or threat of intervention – will keep speculative shorts in check.

Elsewhere, the Indian rupee also posted a strong gain on central bank intervention.

FX interventions to curb the dollar’s strength, at a time when oil prices have taken a lift, could slow the dollar’s appreciation, but what could eventually reverse it is: 1) de-escalation in the Middle East and 2) the hawkish divergence between the Fed and the other major central banks.

Remember, the Federal Reserve (Fed) has a dual mandate: it must ensure price stability but also a healthy jobs market. So any further softening in the jobs market could help ease hawkish Fed expectations.

This week, the US will reveal its latest jobs data. And even though Western markets will be closed for Good Friday, the data will still come out on Friday and is expected to show around 56K new nonfarm payroll additions in the US economy. A soft – or softer-than-expected – figure, or revisions, could help lift some of the hawkish pressure off the market’s shoulders and help ease yields. But the data will obviously remain secondary to Middle East headlines.

Middle East Tensions Rise as Trump Hints at Move on Iran’s Kharg Island Oil Hub

In focus today

In the euro area, focus turns to the German flash inflation print and the seller price expectations in the EU Commissions' business surveys for March. German inflation is projected to rise to 2.7% y/y from 1.9% y/y, driven entirely by energy prices. As the data does not fully reflect the war's impact, the EU Commission's survey on selling price expectations, which the ECB is closely monitoring as noted by President Lagarde, will also be critical.

Also in the euro area, ECB's Stournaras is giving a speech today and markets will be looking for comments on monetary policy and inflation.

In Sweden, retail sales figures for February are likely to hold limited significance, given recent developments in the Middle East. That said, recent months have shown a disconnect between retail sales and consumer confidence. Notably, January saw a 4.1% y/y rise in retail sales, despite weak consumer confidence.

In the US, Fed chair Powell and Fed's Williams are scheduled to speak.

In Japan, Tokyo March CPI data will be released overnight, providing an early glimpse into the energy shock's impact on Japanese consumer prices. February data on retail sales, unemployment, and industrial production will also be released, offering largely outdated insights.

Overnight, China will release NBS PMIs for manufacturing and services. NBS manufacturing PMI fell to 49.0 in February, but March signals from the Emerging Industries PMI and Yicai's high-frequency indicator suggest a rebound, though the Iran war introduces some uncertainty.

During the week, we get key US labour market data with the JOLTS job openings, Challenger job cuts ahead of the main release, non-farm payrolls on Friday. In the euro zone, Flash CPI for March, released Tuesday, will be in focus.

Economic and market news

What happened over the weekend

Middle East tensions have escalated sharply as Trump, in a Financial Times interview, suggested seizing Iran's Kharg Island, which handles 90% of its oil exports, a potential shift from airstrikes to direct resource control. US ground deployment considerations significantly elevate tail risks, given Iran's advanced missile and drone capabilities alongside the vulnerability of fixed assets. The Pentagon is also intensifying its presence, deploying approx. 10,000 troops trained for territorial operations. Amid these developments, Trump disclosed direct and indirect talks with Iran, describing its new leaders as "very reasonable," even as Tehran warned against humiliation. Pakistan is preparing to mediate talks to end the month-long Iran war. Brent Crude rose to around 115 USD/bbl during early Asian trading.

What happened Friday

In Norway, the seasonally adjusted unemployment rate stayed at 2.1% in March, slightly above Norges Bank's forecast (2.0%) but unlikely to impact markets due to the minimal deviation. A marginal rise in unemployed persons suggests a slightly looser labour market. Retail sales fell 1.1% m/m in February, roughly as anticipated. Higher electricity bills may have dampened spending. Despite monthly volatility, retail activity has shown an upward trend since early 2025, supported by strong wage growth and easing mortgage rates.

In the euro area, Spanish HICP inflation rose to 3.3% y/y in March (below 3.8% consensus), with core inflation unchanged at 2.7%. Note that it is still early days in the impact of the war on the economy. Spain's faster energy price passthrough and a high base effect contributed to the print. Hence euro area inflation expected to rise less than Spain on Tuesday, with consensus currently expecting a rise to 2.7% y/y from 1.9% y/y in February. A dovish signal for the ECB.

ECB's Schnabel, typically a hawk, adopted a more dovish tone late Friday, emphasising caution. She stated the ECB "must be vigilant, but no need to rush" and should avoid overreacting to energy price shocks, highlighting the importance of assessing data for second-round effects and demand conditions. While this suggests she is not pushing for immediate hikes in April, her pre-war hawkish stance and optimism on the economic outlook indicate she may still align with the consensus, which appears tilted towards a hike.

In the US, the Final UMich 1-year inflation expectations were revised to 3.8% in March (prelim: 3.4%), reflecting rising gas prices. Long-term 5-year inflation expectations remained steady at 3.2%, suggesting anchored longer-term views.

Fed's Barkin and Paulson, Barkin emphasised prudence in holding rates steady amid uncertainty, noting risks of stalled inflation progress even before the oil shock. He highlighted a fragile labour market with low unemployment but multiple applicants per job and limited wage pressure, consistent with current market pricing. Philly Fed's Paulson echoed a cautious and balanced tone, highlighting that the Iran war poses risks to both growth and inflation.

Equities: Equities had a rough end to last week, extending the drop from Thursday by another 1.4%. S&P500 declined 1.7%, with Nasdaq down 2.2%, Russell 2000 -1.8% and Stoxx600 down 1%. Concerns over the growth implications for the continued rise in oil prices dominated discussions, in an almost textbook risk off session due to demand destruction concerns. Defensives, led by Energy companies being up 1.9%, outperformed cyclicals. Overnight, futures as well as Asian equities are down, amid the Houthi's strike during the weekend.

FI and FX: The combination of energy prices taking another leg higher on renewed escalation risks in Iran and the fact that it increasingly looks likely that central banks will hike policy rates into a slowing economy sets the tone in FI and FX markets. After a nervous end to the last week cyclically sensitive assets are also opening in red territory this morning albeit FX spot moves have been fairly modest compared to recent Mondays. US yields are slightly lower this morning while precious metals are little changed from Friday's close.