Sample Category Title

Weekly Focus – ECB on Course for Rate Hikes

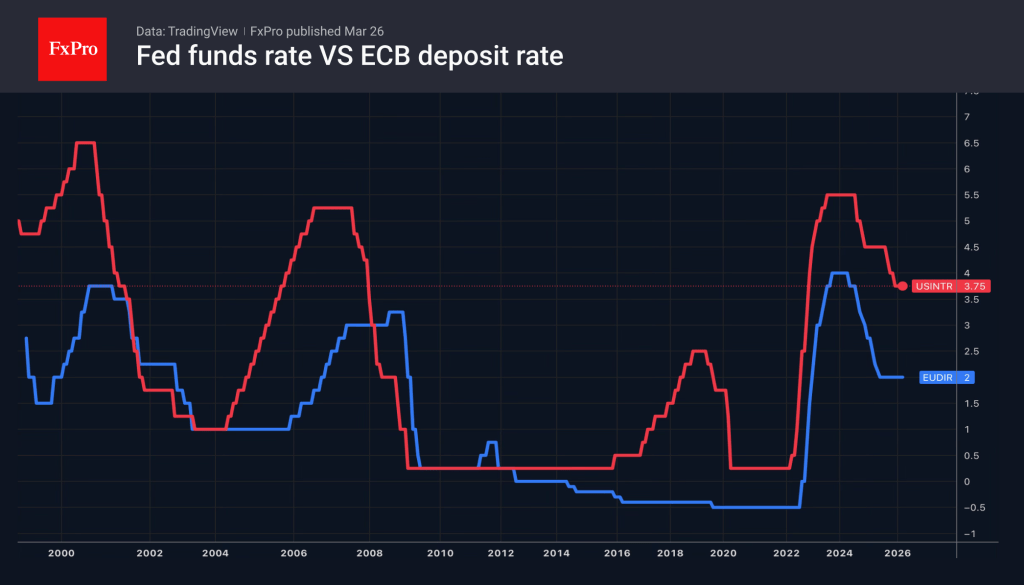

We have changed our ECB call and now expect two 25bp hikes delivered in April and June, respectively, bringing the deposit rate to 2.50%. The comments from the ECB's GC members have been significantly more hawkish compared to Lagarde's view at the last monetary policy meeting. This makes the call for a total of 50bp hikes by YE 2026 more likely than ECB remaining at 2.00% although the latter can certainly not be ruled out. Our call is highly contingent on the developments of the war in Iran, so we present three scenarios for the ECB's deposit rate path in 2026 and 2027 in Reading the Markets EUR - New call: two 25bp hikes in April and June, 27 March.

This week provided the first hints that US President Donald Trump is starting to look for an exit of the Iran war. But also, that he is still considering "a final decisive blow". The mixed news left markets in another rollercoaster pattern. Trump said on Monday, US would not hit Iranian energy infrastructure for five days and was talking with Iran, which caused oil prices to drop below USD100 per barrel after hitting close to USD120 per barrel last week. On Thursday he prolonged the deadline by 10 days referring to good talks. Axios reported during the week that US is weighing options for a "final blow" in Iran that may include ground forces and a major bombing campaign. However, WSJ also reported that Trump had told advisers he wanted an end to the war soon, and he announced new dates for his trip to China, 14-15 May. The trip was supposed to take place next week but was delayed due to the war. Trump's approval rating is declining by the day, and high gasoline prices is starting to hurt. Even if Trump is looking for an exit and does not escalate further it is not clear that Iran is willing to back down and reopen the Strait of Hormuz. And should Trump decide on putting 'boots on the ground' the probability of escalation goes up significantly.

We see a risk that the conflict drags out beyond the 4-6 weeks that Trump has aimed for from the outset. Uncertainty is of course unusually high, and many scenarios are in play, both for the war and the global economy. Oil markets are currently priced for a fairly quick resolution of the war with oil futures pricing a decline from just below USD110 per barrel at the time of writing to USD 90 by late summer and USD85 by the end of the year.

Financial markets have generally followed the ebbs and flows in the Iran war with equities higher on Monday when oil prices dropped but moving broadly sideways in a see-saw pattern for the rest of the week. Bond yields and the USD have followed a similar pattern.

On the data front PMIs for March were in the spotlight, not least as a first sign of the impact of the Iran war. Euro PMIs were mixed with manufacturing holding up well while services took a hit with a decline from 51.9 to 50.1. The price indices moved sharply higher lifted by the rise in energy prices.

Next week, developments in the Iran war will continue to be the main market driver but we also get key US labour market data with the JOLTS job openings, Challenger job cuts ahead of the main release, non-farm payrolls on Friday. In the euro zone, Flash CPI for March, released Tuesday, will be in focus. Germany will publish March CPI numbers on Monday.

EUR/USD Mid-Day Outlook

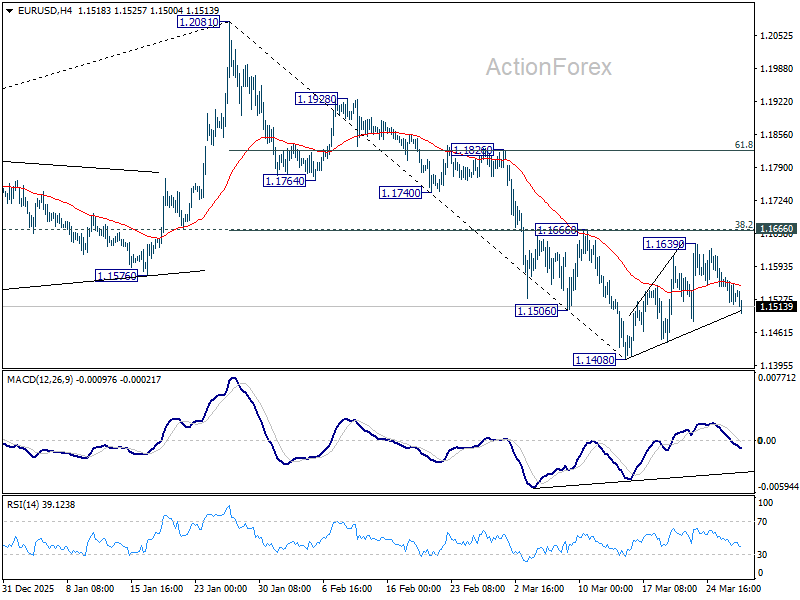

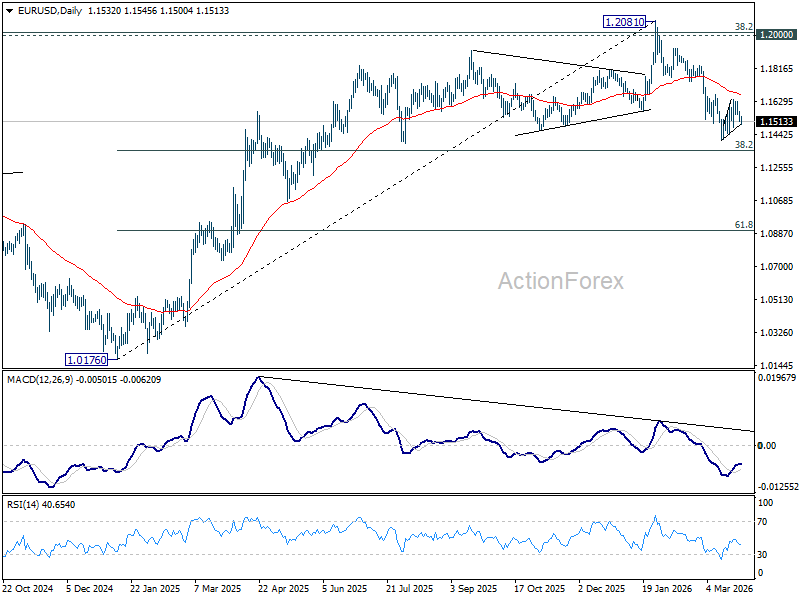

Daily Pivots: (S1) 1.1508; (P) 1.1541; (R1) 1.1562; More….

EUR/USD dips lower today but stays in range above 1.1408 low. Intraday bias remains neutral at this point. With 1.1666 cluster resistance (38.2% retracement of 1.2081 to 1.1408 at 1.1665) intact, further decline is in favor. On the downside, below 1.1408 will resume the fall from 1.2081 to 38.2% retracement of 1.0176 to 1.2081 at 1.1353. However, decisive break of 1.1666 will argue that the fall from 1.2081 has completed, and turn bias back to the upside for 61.8% retracement of 1.2081 to 1.1408 at 1.1824.

In the bigger picture, prior break of 55 W EMA (now at 1.1501) should confirm rejection by 1.2 key cluster resistance level. The whole up trend from 0.9534 (2022 low) might have completed as a three wave corrective rise too. Deeper fall is expected to long term channel support (now at 1.0528). Meanwhile, risk will stay on the downside as long as 1.2081 holds, even in case of strong rebound.

GBP/USD Mid-Day Outlook

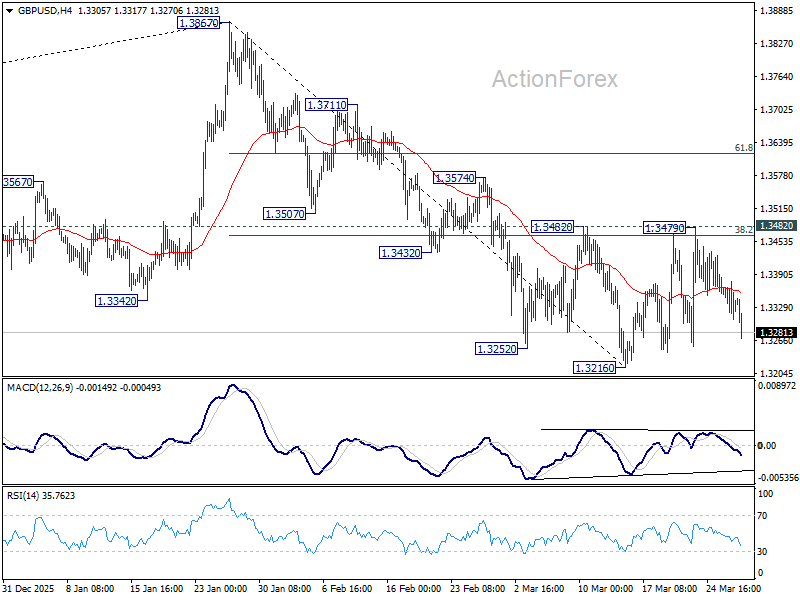

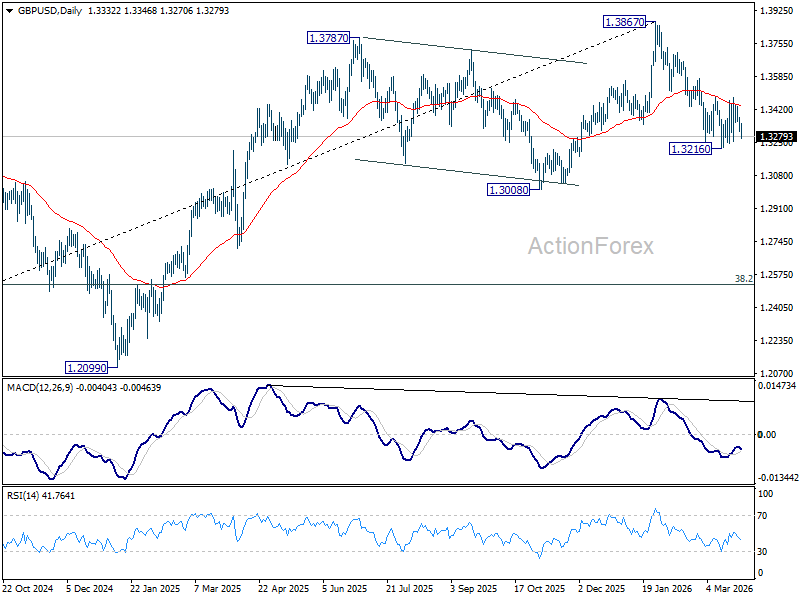

Daily Pivots: (S1) 1.3301; (P) 1.3340; (R1) 1.3369; More...

GBP/USD accelerates lower today but it's still holding above 1.3216 support. Intraday bias remains neutral at this point. With 1.3482 resistance intact, further decline is in favor. On the downside, below 1.3216 will resume the fall from 1.3867 to 1.3008 structural support. However, decisive break of 1.3482 will argue that the fall from 1.3867 has completed, and turn bias back to the upside for 61.8% retracement of 1.3867 to 1.3216 at 1.3618.

In the bigger picture, considering bearish divergence condition in both D and W MACD, a medium term top should be in place at 1.3867. Firm break of 1.3008 support will argue that fall from 1.3867 is at least correcting the rise from 1.0351 (2022 low) with risk of bearish reversal. That would open up further decline to 38.2% retracement of 1.0351 to 1.3867 at 1.2524. For now, medium term outlook will be neutral at best as long as 1.3867 resistance holds, or until further development.

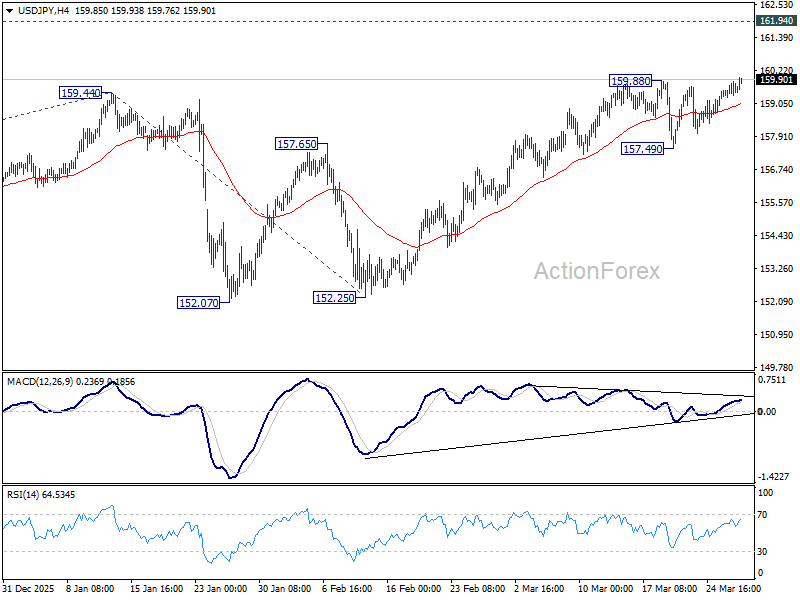

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 159.42; (P) 159.64; (R1) 159.98; More...

Intraday bias in USD/JPY is back on the upside with breach of 159.88 resistance. Rise from 152.52 is resuming and further rally should be seen to retest 161.94 high. For now, outlook will remain bullish as long as 157.49 support holds, in case of retreat.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.70) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

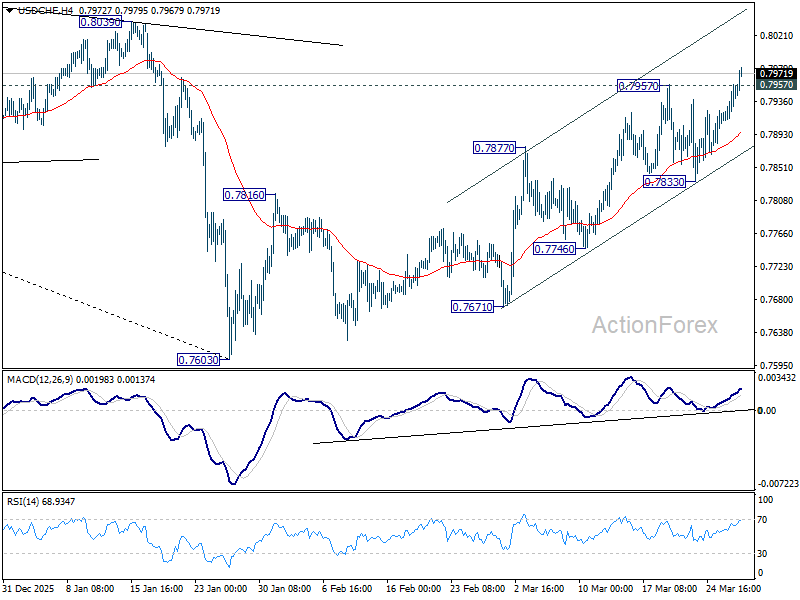

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7924; (P) 0.7942; (R1) 0.7972; More….

USD/CHF's break of 0.7957 suggests that rebound from 0.7603 is resuming. Intraday bias is now the upside. As a correction to the whole down trend from 0.9200, next target is 38.2% retracement of 0.9200 to 0.7603 at 0.8213. For now, further rise is expected as long as 0.7833 support holds, in case of retreat.

In the bigger picture, a medium term bottom should be in place at 0.7603 on bullish convergence condition in D MACD. Rebound from there is seen as correcting the fall from 0.9200 only. However, decisive break of 55 W EMA (now at 0.8085) will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high). On the other hand, rejection by the 55 W EMA will setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage.

Dollar Breakout as Markets Front-Run Weekend Escalation Wildcard Risks

Risk-off sentiment has returned to the fore as the US session approaches, with Dollar breaking out against Yen and Swiss Franc while Brent crude rebounds to $108. While US President Donald Trump has extended the Iran strike pause to April 6, markets are increasingly viewing this as a "thin veil" for a tactical realignment rather than true de-escalation.

A key concern is that the “pause” does not cover several major escalation channels. Traders are actively positioning for a high-risk weekend characterized by "Wildcard" threats—specifically unilateral Israeli strikes and Trump's own "Pearl Harbor" obsession with surprise. This front-running suggests a growing belief that the diplomatic window could be scrapped well before the Monday open.

The most immediate risk comes from Israel, which is not bound by the US framework and has signaled intentions to escalate operations. Any strike that impacts high-value infrastructure or strategic assets could quickly invalidate the pause and trigger retaliation from Iran.

Beyond that, the buildup of US ground capabilities suggests a broader strategic shift. Markets are increasingly considering scenarios where the US could move to secure key chokepoints such as the Strait of Hormuz or seize strategic islands if diplomacy fails. While these actions may not occur immediately, the preparation itself raises the probability of a larger conflict.

At the same time, Iran’s response function is evolving. As pressure intensifies, the risk is shifting from controlled proxy actions to more direct and asymmetric strikes, including potential attacks on US military assets in the region. Such a move would likely trigger a rapid escalation, bypassing the current pause framework entirely.

Regional spillover risks are also rising. Interceptions of drones over Saudi Arabia and the UAE, along with warnings issued by Iranian forces, point to an increasingly fragile environment where miscalculations could draw additional players into the conflict. A single incident involving a neutral or regional actor could quickly broaden the scope of the war.

Adding to the uncertainty is the risk tied to strategic unpredictability. Trump’s recent comparisons of his strategy to "the element of surprise" at Pearl Harbor signal that he views diplomatic pauses as tools to keep an enemy off-balance. The risk is that the administration, sensing Iranian stalling, could unilaterally scrap the April 6 deadline this weekend to order a "shock and awe" strike on Iran's power grid. While a tail-risk, it is something that the markets wouldn't ignore.

In currency markets, Dollar is the strongest performer for the week so far, followed by Sterling and Yen. In contrast, growth-sensitive currencies such as the Australian and New Zealand Dollars remain under pressure, while Euro and Canadian Dollar sit in the middle of the pack.

In Europe, at the time of writing, FTSE is down -0.44%. DAX is down -1.43%. CAC is down -0.80%. UK 10-year yield is up 0.103 at 5.019. Germany 10-year yield is up 0.038 at 3.114. Earlier in Asia, Nikkei fell -0.43%. Hong Kong HSI rose 0.38%. China Shanghai SSE rose 0.63%. Singapore Strait Times rose 0.21%. Japan 10-year JGB yield rose 0.106 to 2.380.

UK Retail Sales Slip -0.4% as Discount-Driven Demand Fades

UK retail sales slipped -0.4% in February after a strong January, as earlier discount-driven demand faded. Spending appears to have been pulled forward, leaving softer activity in the latest data. While three-month growth remains positive, the figures highlight uneven consumer momentum and sensitivity to pricing. Read More

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7924; (P) 0.7942; (R1) 0.7972; More….

USD/CHF's break of 0.7957 suggests that rebound from 0.7603 is resuming. Intraday bias is now the upside. As a correction to the whole down trend from 0.9200, next target is 38.2% retracement of 0.9200 to 0.7603 at 0.8213. For now, further rise is expected as long as 0.7833 support holds, in case of retreat.

In the bigger picture, a medium term bottom should be in place at 0.7603 on bullish convergence condition in D MACD. Rebound from there is seen as correcting the fall from 0.9200 only. However, decisive break of 55 W EMA (now at 0.8085) will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high). On the other hand, rejection by the 55 W EMA will setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage.

Chart Alert: WTI Crude Oil Minor Pullback Over, Start of New Bullish Leg for Breakout Above $102.25

Key takeaways

- Pullback complete, bullish structure emerging: WTI corrected 17% from $102.25 to $85.50 but has stabilised above its 20-day moving average, reclaimed $93.70, and is now positioned to retest the $102.25 resistance.

- Fundamentals support upside pressure: Deepening backwardation (-21.74) signals tightening near-term supply amid escalating US–Iran tensions, reinforcing upward pressure on crude prices.

- Breakout levels to watch: A sustained move above $102.25 could trigger a fresh bullish leg toward $111–$124, while a break below $85.50 would invalidate the bullish view and expose downside toward the $81–$73 zone.

The price actions of the West Texas Oil CFD (a proxy of the WTI crude oil futures) have staged the expected minor corrective pullback of 17% from its key $102.25 near-term range resistance after a retest on Monday, 23 March 2026, at the start of the London session to hit an intraday low of $85.50 at mid-London session on the same day due US President Trump’s “optimistic claims” that US and Iran are in the process of negotiating an immediate ceasefire deal.

Thereafter, the West Texas Oil CFD traded sideways above its 20-day moving average as Iran rejected the US’s ceasefire proposal and continued to strike the Gulf states’ key installations as the US-Iran war entered its 28th day.

In addition, conflicting messages are being sent out from the US White House Administration. US President Trump has extended by 10 days his pledge to refrain from attacks on Iranian energy-producing sites and added that the “negotiation talks are going very well”.

On the other hand, the Wall Street Journal has reported that the Pentagon is considering sending additional troops, as many as 10,000, to the Middle East, on top of the already deployed 2,000 soldiers from the 82nd Airborne Division. Hence, increasing the odds of a US ground invasion into Iranian soil as soon as this weekend.

Right now, several technical factors are suggesting the potential start of a new bullish up move sequence for West Texas crude oil at this juncture.

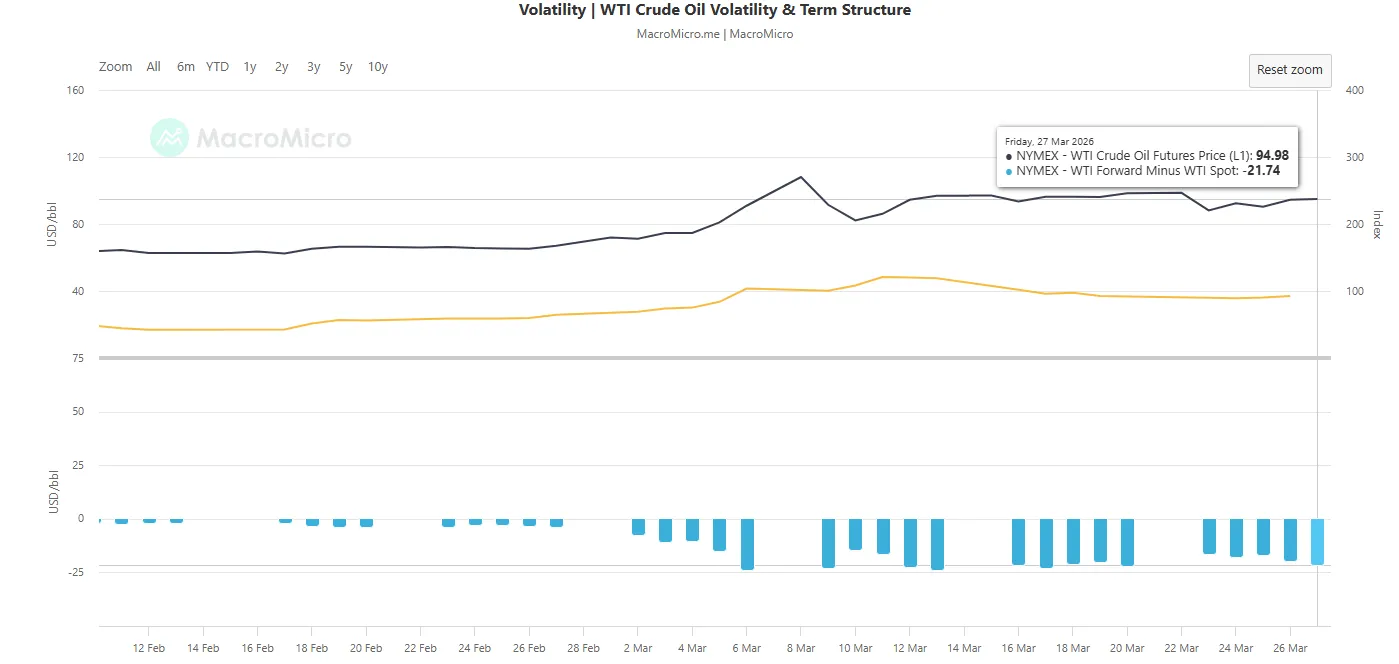

WTI calendar spread remains in negative territory

Fig. 1: WTI crude oil term structure (12-month forward minus spot rate) as of 27 Mar 2026 (Source: MacroMicro)

The WTI crude oil calendar spread, defined as the difference between the 12-month forward price and the spot price, serves as a gauge of the market’s structural conditions.

A positive spread (contango) reflects a typical environment where futures trade at a premium to spot, factoring in storage and transportation costs.

In contrast, a negative spread (backwardation) signals near-term supply tightness, with strong prompt demand pushing spot prices above futures.

At the time of writing, the spread has deepened into backwardation at -21.74, marking its most negative level since 6 March 2026 (-23.92) on the onset of the ongoing US-Iran war (see Fig. 1).

Hence, near-term prices of WTI crude oil are likely to face further upside pressure.

Let’s switch our attention to the potential short-term trajectory (1 to 3 days) of WTI crude oil.

WTI Crude Oil – Imminent potential bullish breakout above $102.25 minor range top

Fig. 2: West Texas Oil CFD minor trend as of 27 Mar 2026 (Source: TradingView)

The minor price structure of the West Texas Oil CFD (a proxy for WTI crude oil futures) has turned more constructive over the past four sessions, supported by its ability to hold above a rising 20-day moving average.

On Thursday, 26 March 2026, it has cleared above its $93.70 near-term resistance and is en route to retest its $102.25 minor range resistance in place since 16 March 2026.

Watch the $88.36/85.50 key short-term pivotal support to maintain the current bullish momentum, and a clearance above $102.25 increases the odds of a fresh bullish impulsive up move sequence to seek out the next intermediate resistances at $111.28, $116.56/119.54, and $124.40 (see Fig. 2).

However, a break and an hourly close below $85.50 invalidates the bullish scenario for an extension of the minor corrective decline to expose the next intermediate supports at $81.85, $77.26/76.83, and $73.38 (also the 50-day moving average).

Key elements to support the bullish bias on WTI crude oil

- Price actions remain above its rising 20-day and 50-day moving averages, which indicates that the medium-term uptrend phase remains intact.

- The hourly MACD trend indicator has just flashed out a bullish crossover condition above its centreline. This latest positive observation has occurred above its prior bullish breakout above its former key descending resistance on Thursday, 26 March 2026. An indication of a change of trend in the West Texas Oil CFD, from sideways to a minor bullish trend.

ECB Rate Hikes May Backfire on Europe

- Japan is exploring options for intervening in the oil market.

- The OECD considers the risks of stagflation in the eurozone to be higher than in the US.

Christine Lagarde’s statement that the ECB is ready to raise interest rates should, in theory, support the euro. However, a tightening of monetary policy could shock the eurozone. The surge in energy prices raises short-term inflation risks but deteriorates the medium-term growth outlook, potentially forcing the ECB to shift towards policy easing.

The OECD sees a higher risk of stagflation in the eurozone than in the US. The Paris-based organisation has revised its GDP forecast for the United States this year upwards from 1.7% to 2% and lowered its forecast for the eurozone from 1.2% to 0.8%. Inflation estimates have been increased by 1.2 percentage points and 0.7 percentage points, respectively. They also suggest that the market’s expectations of 2-3 ECB rate hikes this year are overstated, whilst investors are justified in expecting more from the Fed than merely pausing the rate-cut cycle.

According to Federal Reserve Vice-Chair Philip Jefferson, the duration of the conflict in the Middle East and its impact on energy prices will be decisive for the central bank’s future decisions. His FOMC colleague, Lisa Cook, believes that the war in Iran and the associated oil market shock make fighting inflation the Fed’s top priority, requiring rates to remain on hold for longer.

Meanwhile, markets have raised the probability of a Fed rate hike in 2026 from 20% to 45%, signalling confidence in the US economy’s resilience. Alongside the OECD’s revised forecasts and geopolitical tensions in the Middle East, this is contributing to downward pressure on EURUSD.

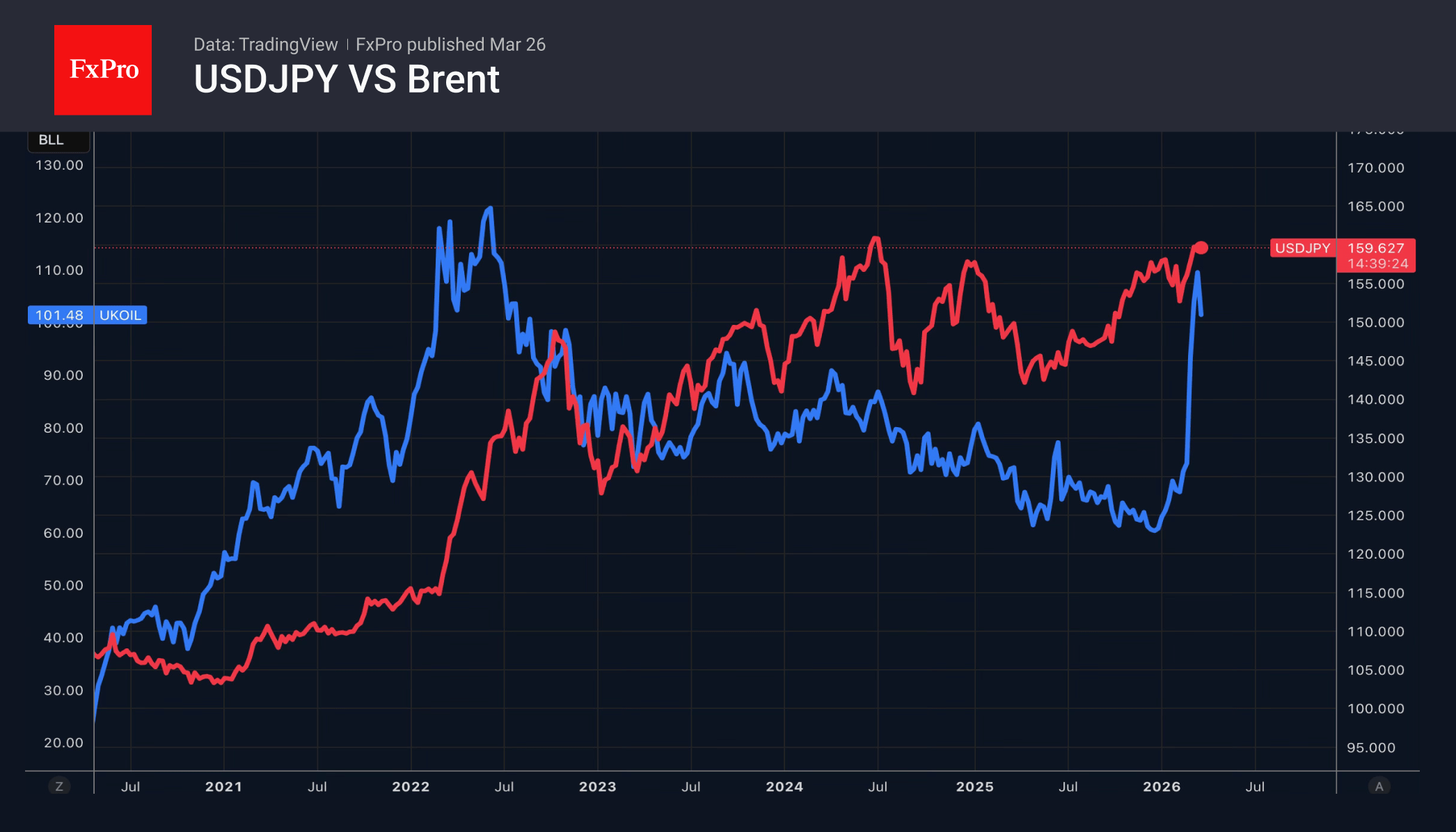

The approach of USDJPY to the psychologically significant 160 level is prompting the Japanese government to intensify its verbal interventions. According to Finance Minister Satsuki Katayama, the time has come for bold action. In 2024, Tokyo intervened in the forex market near current levels. However, this time, the US dollar’s strength may act as a limiting factor.

The rise in the USD is supported by the surge in Brent. Rumours are circulating that Japan has decided to address the root cause of the USDJPY rally. Using $1.4 trillion in reserves to intervene in the oil futures market could help ease pressure on both the economy and financial markets by lowering prices.

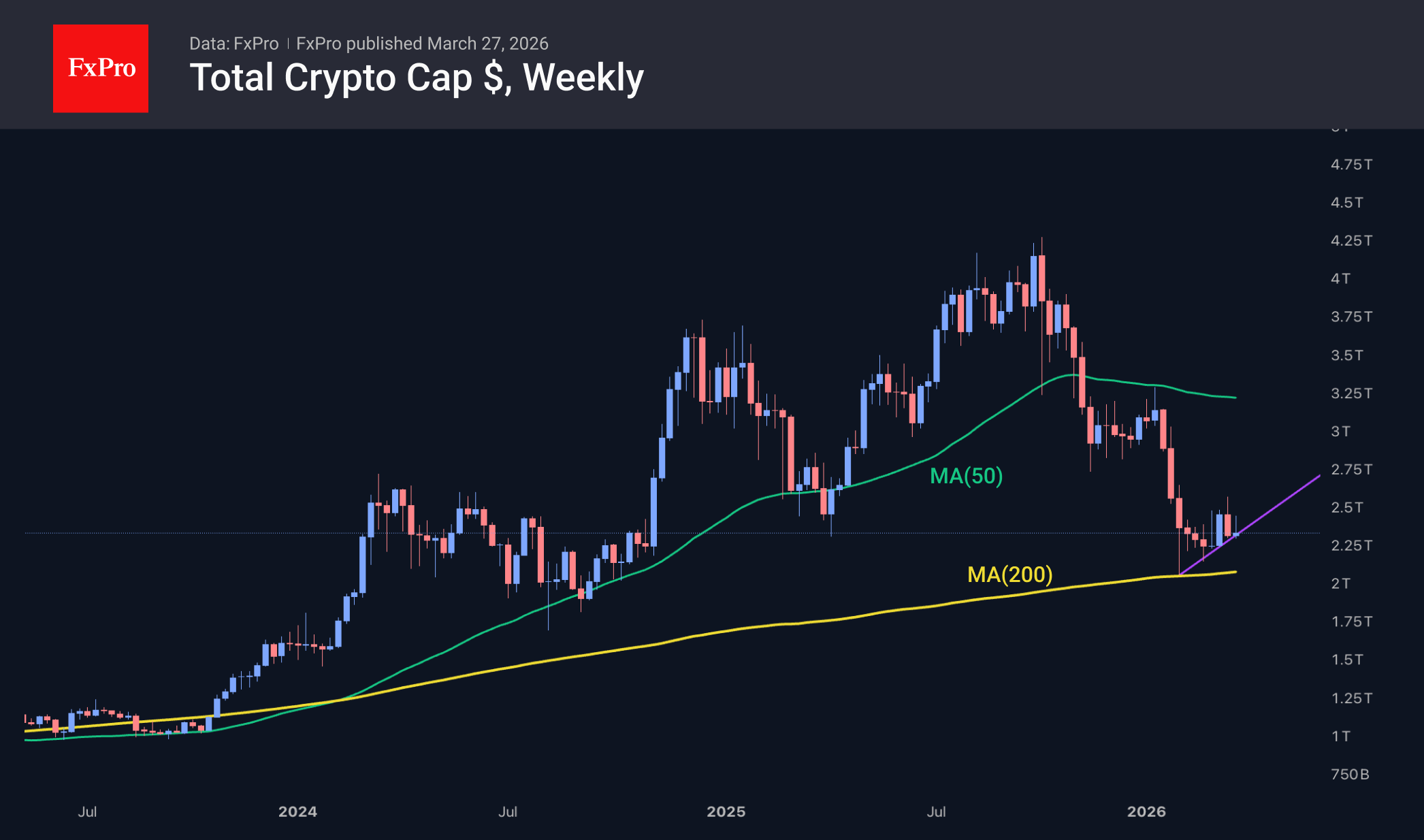

Crypto Has Pulled Back, But Appears Stronger Than Stocks

Market Overview

The crypto market’s capitalisation fell by 3.4% over the past 24 hours to $2.36 trillion, remaining close to the uptrend line. The downward momentum was once again driven by stock indices, which returned to their lows at the start of the week. However, whilst the Nasdaq 100 has shown a steady downward trend on weekly charts since late January, cryptocurrencies have been forming a sequence of higher local lows since early February, when the market touched the 200-week moving average – a key long-term trend line.

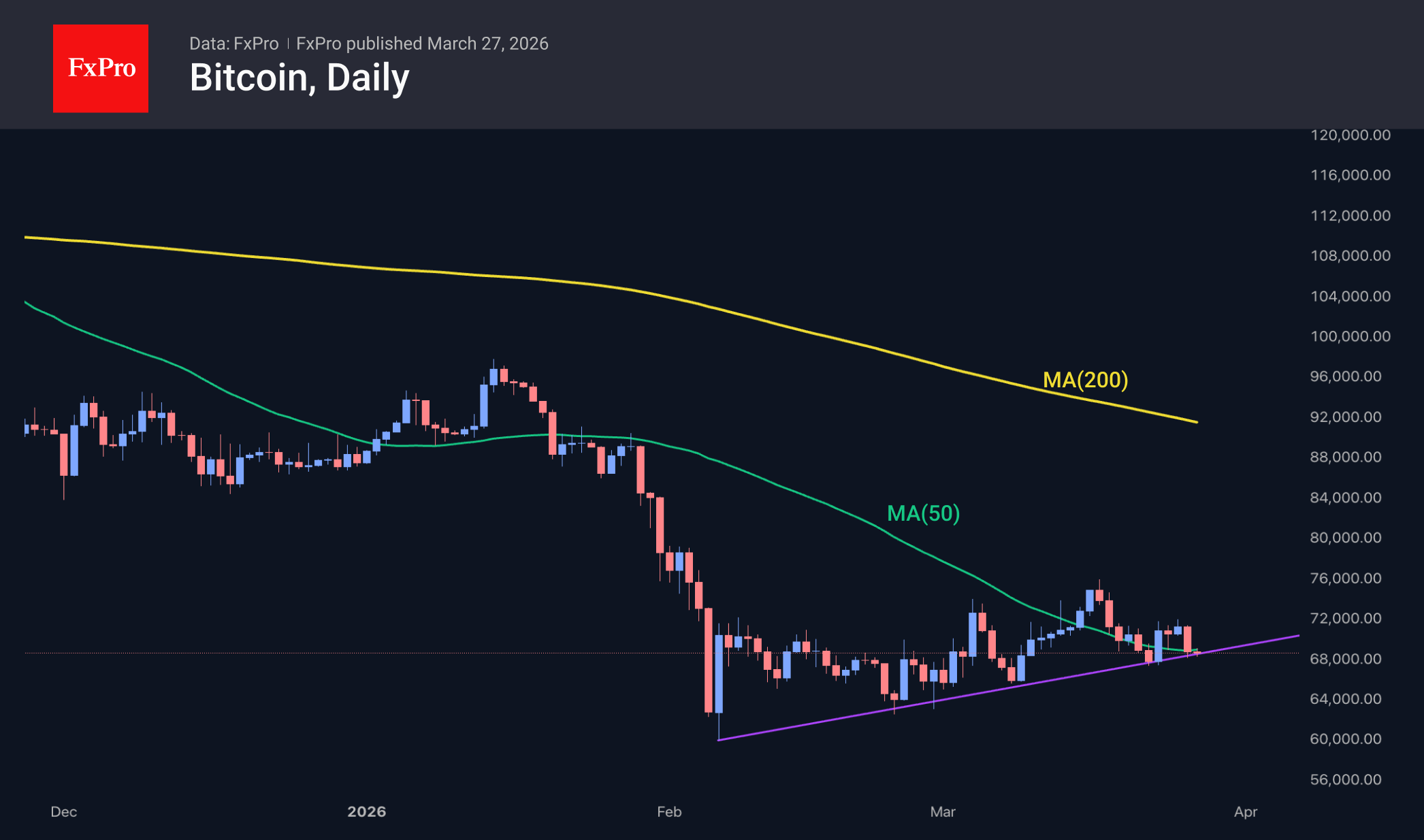

Bitcoin has fallen below $69K, testing the strength of the 50-day MA and the support of the upward trend of the last two months. The nervous mood in the financial markets makes cryptocurrencies, and Bitcoin in particular, vulnerable in the event of a large-scale sell-off. For BTC, the 200-week MA has historically been the most important long-term support level. It currently sits near $60K. However, it is worth remembering that in 2022–2023, the price fell more than 30% below this line before finding structural support for many weeks.

News Background

Bitcoin miner MARA has sold 15,133 BTC for $1.1 billion since the start of the month. The company intends to use the proceeds to buy back its own bonds. The miner’s remaining reserves are estimated at 38,689 BTC.

The cost of Bitcoin mining for public companies has reached $80K and, for some miners, exceeded $100K, according to CoinShares. The fourth quarter of 2025 has been the most challenging for Bitcoin miners since the last halving. The US (38%), Russia (17%), and China (12%) continue to dominate global Bitcoin mining, collectively accounting for around 68% of the world’s hash rate.

Adam Livingston, an analyst and author of the book ‘The Great Harvest: AI, Labor, and the Bitcoin Lifeline’, believes the risk of a Bitcoin crash, as seen in 2022, is minimal due to the market’s more mature structure. According to his calculations, BTC volatility has been steadily declining over the past 11 years.

US investment firm Franklin Templeton, in partnership with Ondo Finance, will launch tokenised versions of its ETFs, accessible directly via crypto wallets.

Gold Steadies After Declines: Strait of Hormuz Back in Focus

Gold prices stabilised near 4,400 USD per ounce on Friday following a sharp decline the previous day. The market found support from Donald Trump's decision to postpone the deadline for reaching a deal with Iran to end the conflict.

The US has pledged to hold off on striking Iran's energy infrastructure until 6 April, offering some relief to market tensions. Trump also stated that Iran had allowed 10 oil tankers to pass through the Strait of Hormuz as a gesture towards the US.

Meanwhile, Tehran confirmed it had rejected the 15-point plan proposed by the US and put forward its own conditions, including recognition of its control over the Strait of Hormuz.

Gold lost nearly 3% the previous day amid doubts over the prospects for an imminent truce. Overall, the metal remains under pressure, with rising energy prices continuing to heighten inflationary risks and reinforce expectations of tighter policy from major central banks.

Technical Analysis

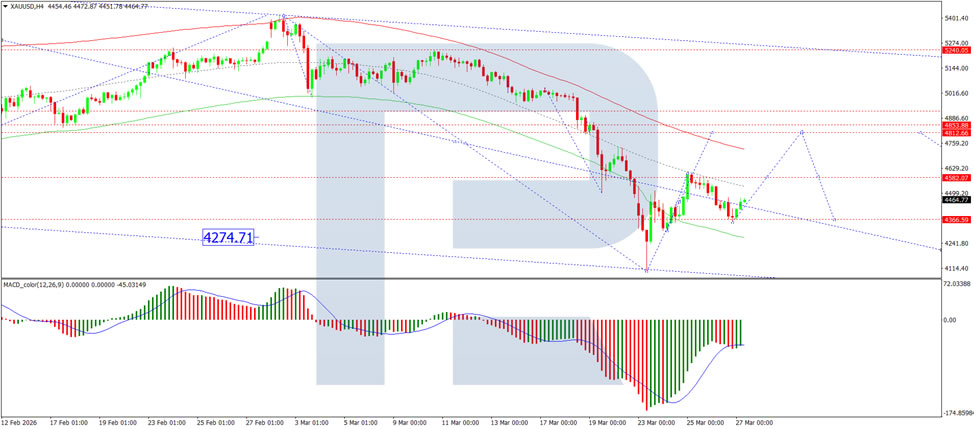

On the H4 XAU/USD chart, the market is forming a consolidation range around 4,353 USD. An upside breakout would pave the way for a correction to 4,820 USD, while a downside breakout could extend the downward wave to 4,272 USD. The MACD indicator confirms the current momentum, with its signal line currently below the centre line but pointing firmly upwards.

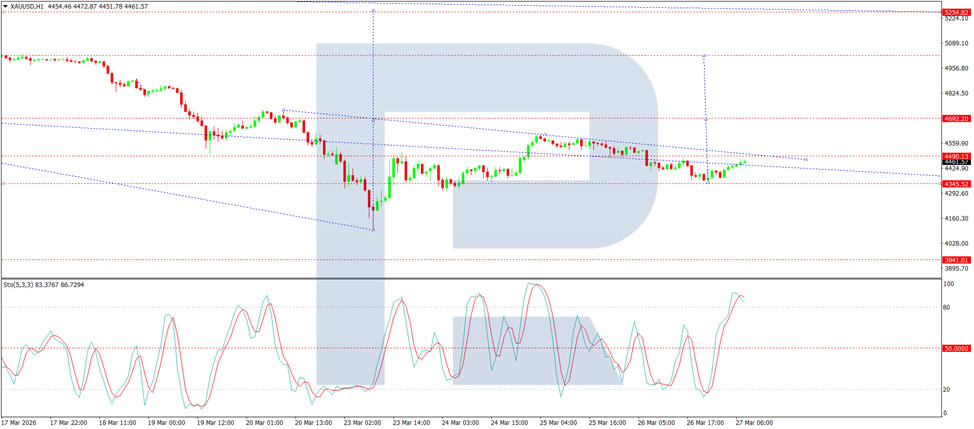

On the H1 chart, the market broke above 4,414 USD and completed a wave to 4,474 USD. Looking ahead, a corrective move back to 4,414 USD is likely, followed by a renewed advance towards 4,690 USD. The Stochastic oscillator supports this scenario, with its signal line remaining above 80 and showing continued upward pressure.

Conclusion

Gold has found a temporary respite following the US decision to delay strikes on Iranian energy infrastructure, easing immediate geopolitical tensions. However, Tehran's rejection of the US proposal and insistence on maintaining control over the Strait of Hormuz underscores how fragile the situation is. While the postponement offers a short-term reprieve, the underlying drivers – elevated energy prices, persistent inflation risks, and expectations of tighter central bank policies – remain. With technical indicators pointing to a potential corrective bounce, gold's broader trajectory will likely hinge on whether diplomatic efforts gain traction or tensions reignite after the 6 April deadline.