Sample Category Title

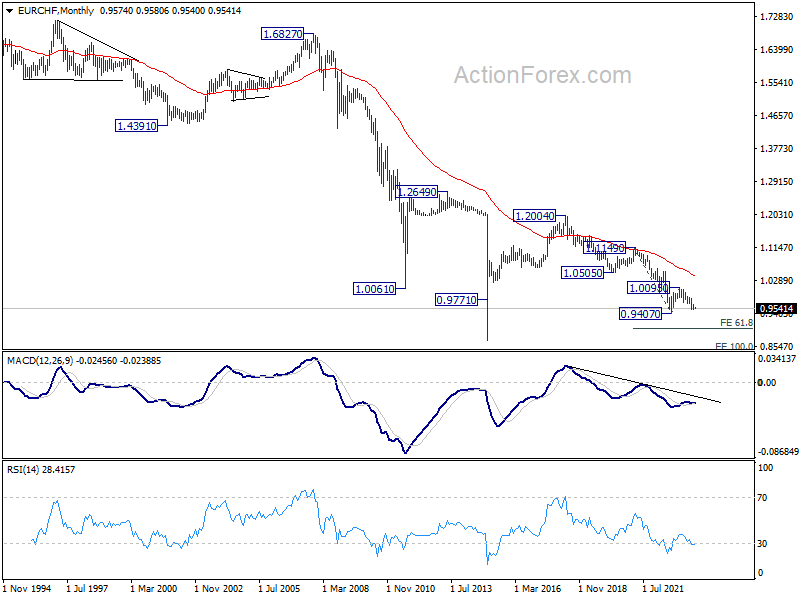

EUR/CHF Weekly Outlook

EUR/CHF recovered to 0.9601 last week but reversed from there. Initial bias stays neutral this week and larger down trend is still in favor to continue. Break of 0.9513 support will confirm this bearish case and target 0.9407 low. Nevertheless, break of 0.9601 resistance will turn bias back to the upside for stronger rebound to 0.9646 resistance and above.

In the bigger picture, medium term outlook is staying bearish as the pair is capped well below falling 55 W EMA (now at 0.9839). Down trend from 1.2004 (2018 high) is in favor to continue. Sustained break of 0.9407 will target 61.8% projection of 1.1149 to 0.9407 from 1.0095 at 0.9018. For now, this will remain the favored case as long as 0.9670 support turned resistance holds, in case of strong rebound.

In the long term picture, outlook remains bearish as it's staying well below 55 M EMA (now at 1.0421). Break of 1.00095 resistance is needed to be the first sign of bottoming, or the multi-decade down trend is expected to continue.

Dollar Stays Resilient after Volatile Week, Euro Falters as Worst Performer

In a week marked by high volatility, Dollar proved resilient, closing within its established range against other major currencies after intra-week selloff. This performance quells, at least for now, fears of bearish reversal for the greenback. Indeed, sentiment has shifted to favor near-term upside for Dollar, which is likely to maintain its strength at least until Fed releases new economic projections later this month.

Contrastingly, Euro emerged as the week's weakest performer amid rising expectations that ECB will hit the pause button on interest rate changes this month. Weakness in Euro has also dragged down Swiss Franc, which ended as the week's second-worst performer. British Pound lingered not far behind, showing vulnerability against the resilient Dollar.

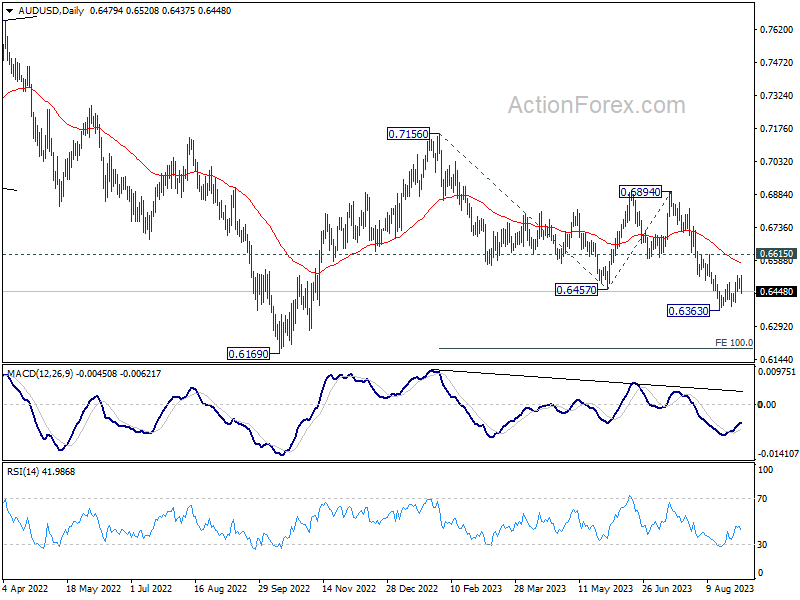

Australian Dollar was the best performer of the week, buoyed by improving sentiment towards China's economy. However, this rally appears to be in corrective mode only, lacking decisive momentum needed to confirm a sustained uptrend. Consequently, renewed wave of selling could emerge at any moment, particularly if optimism about China's economic outlook starts to wane. Following closely behind was New Zealand Dollar, which also enjoyed a strong week. Yen ended mixed as the pull back in major benchmark yields didn't last long.

Dollar's volatile week ends on a high note

Dollar faced significant volatility last week, flirting with the risk of a near-term bearish reversal before making a sharp U-turn on Friday. This renewed bullishness keeps the prospect for more upside in the greenback alive, albeit not without hurdles.

The eagerly watched non-farm payroll data gave investors a balanced view of the US economy: the labor market showed just enough loosening to deter immediate Fed rate action, but not so much as to raise concerns about a recession. Supplementing this positive outlook, recovering ISM manufacturing data offered a glimmer of hope that the worst may be over for that sector.

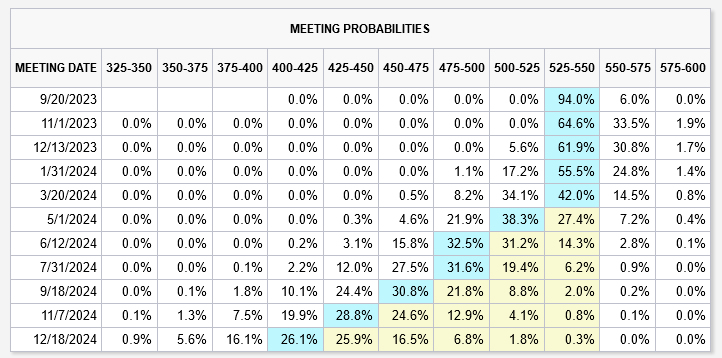

Market expectations for Fed to maintain its current rate held steady, with Fed fund futures now pricing in 94% chance of a hold this month. The likelihood of another rate hike this year has dipped to below 36%. There's a 65% probability being priced in for a rate cut by May of next year—a projection that appears overly optimistic given that overall economic growth is outpacing the trend and inflation is well above Fed's target.

All eyes will now be on Fed's new set of economic projections and dot plot, scheduled for release on September 20. These could potentially recalibrate market expectations and pricing metrics significantly.

On the technical front, Dollar Index successfully defended its near-term support at 102.84, bouncing to close the week at 104.23. Near term bullishness is maintained for extending the rally from 99.57 through 104.44. But loss of upside momentum, as seen in D MACD, could limited upside at 38.2% retracement of 114.77 to 99.57 at 105.37.

Should the index break 102.84 support level, it would signify that the recent rebound has run its course. Conversely, sustained break of 105.37 could argue that Dollar Index is on track to reverse the downtrend from 2022 high of 114.77, altering the broader market narrative.

Euro stumbles as ECB pause gains traction amid recession risks

Euro emerged as the week's worst-performing currency, reflecting growing market sentiment that ECB may hold off on policy changes in its upcoming meeting. Money markets are currently pricing in more than 70% chance that ECB will stay put on September 14, a stark contrast to last week when odds of a rate hike stood at 60%.

Starkly contrasting the US, economic landscape in Eurozone is becoming increasingly fraught, caught between the dual pressures of recession and inflation. Recent PMI data offered little comfort, particularly with disconcerting trends emerging from Germany, the "sick man of Europe". ECB Executive Board member Isabel Schnabel, traditionally a hawkish voice, has also turned cautious in her recent speech, signaling downside risks to economic growth and refraining from taking a firm stance on the September meeting. Inflation data for August further complicated the picture; while the flash CPI remained stable at 5.5%, core CPI eased to 5.3%.

Minutes from ECB's July meeting offered no clarity either, painting a divided stance among the central bank's members. While some argued for a rate hike in September, should inflation not recede as expected, others countered that new ECB staff projections could show a downward revision in the inflation path, rendering another rate hike unwarranted.

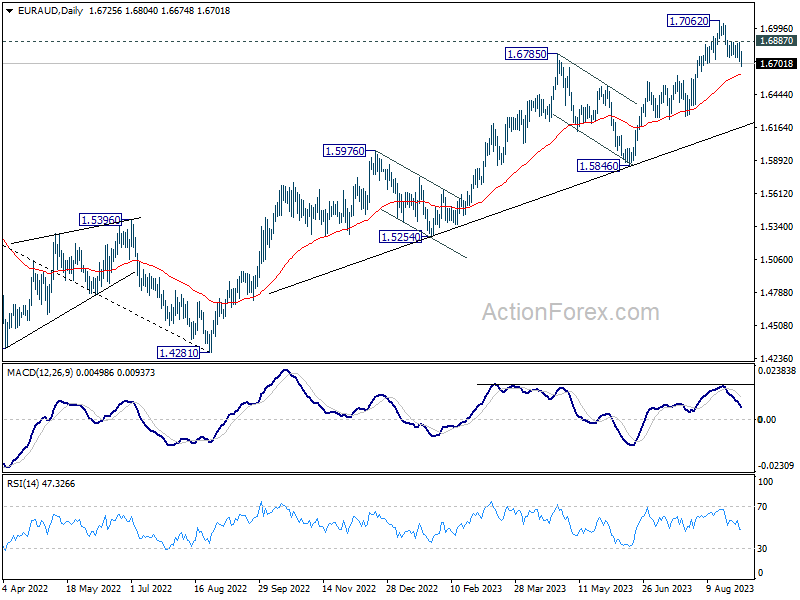

EUR/AUD was the top mover last week, closing down -0.93%. For now, the fall form 1.7062 is still seen as a near term correction only. While deeper decline is in favor as long as 1.6887 resistance holds, strong support could be seen from 55 D EMA (now at 1.6612) to contain downside to complete the fall. However, sustained break of the EMA will raise the change that the cross is in a larger scale correction, and prompt deeper fall to medium term trend line support (now at 1.6177).

Australian dollar rides higher on Chinese policy moves

Talking about Australian Dollar, it ended as the strongest one for the week, buoyed by a series of encouraging developments from China and a rebound in copper prices. However, Aussie's recent upswing appears more of a corrective move than a sustainable rally, suggesting downside risk remains for an extension of its recent downtrend.

China began the week by slashing stamp duty on stock trading by half, aimed at revitalizing its capital markets and bolstering investor sentiment. This was followed by a significant 200 basis point cut in the foreign exchange reserve requirement ratio by the People's Bank of China on Friday, reducing it from 6% to 4% in a bid to alleviate downward pressure on the Yuan. In between, official PMI Manufacturing data for August showed a marginal rise, while Caixin PMI Manufacturing Index advanced turned back into expansion.

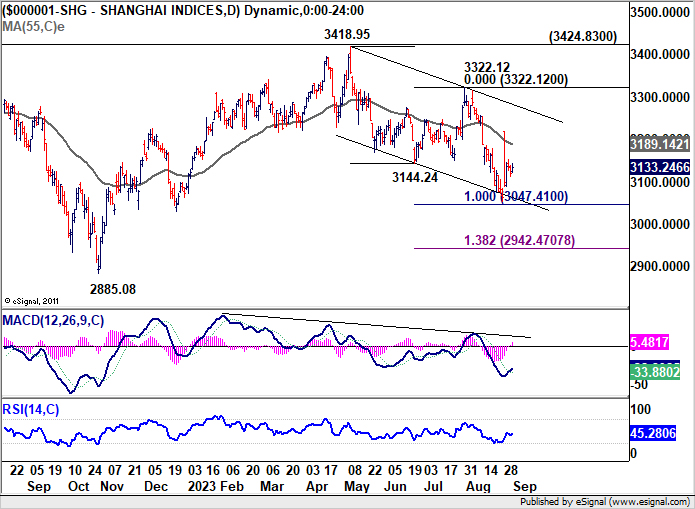

Though these developments led Shanghai SSE to close higher, the lackluster upside momentum just mixed up the near term outlook, rather than turning it bullish. On the one hand, fall from 3148.95 could have completed as a three-wave correction, slightly ahead of 100% projection of 3418.95 to 3144.24 from 3322.12 at 3047.41. However, sustained break above 55 D EMA (now at 3819.14) is needed to instill greater confidence. Conversely, firm break below 3047.31 could resume the descent to 138.2% projection level at 2924.47.

As for AUD/USD, the structure of the recovery from 0.6363 is corrective looking. Upside is capped below falling 55 D EMA (now at 0.6573). Near term outlook is staying bearish for another fall through 0.6363, to resume the whole decline from 0.7156, to 1% projection of 0.7156 to 0.6457 from 0.6894 at 0.6195.

Surge in oil prices could cloud global disinflation path

Last week saw oil prices surging to their highest levels in 10 months, creating a complex scenario for global disinflation efforts and complicating central bank policies. The development has triggered a sense of unease in the markets and could potentially disrupt the delicate balancing act central banks are performing amid inflationary pressures and economic uncertainties.

Several factors are contributing to this rally in oil prices. Most notably, Saudi Arabia is expected to extend its voluntary oil production cut of 1 million barrels per day into October. This move is in addition to production cuts already instituted by OPEC+. The cuts could even potentially last through the end of 2023. Meanwhile, in US, oil stockpiles have fallen by 10.6 million barrels to their lowest levels since December of last year.

From a technical perspective, WTI crude oil prices have broken through 84.91 resistance, confirming resumption of the rally that began at 63.67. Strong support from rising 55 D EMA is clearly a bullish sign. Next target is 61.8% projection of 66.94 to 84.91 from 77.95 at 89.05. This is close to 38.2% retracement of 131.82 to 63.67 at 89.70.

Market participants should keep an eye on 90 level as strong resistance is anticipated to cap upside and possibly complete the current uptrend. However, any powerful move through 90 could suggest underlying drastic developments and unsettle the markets.

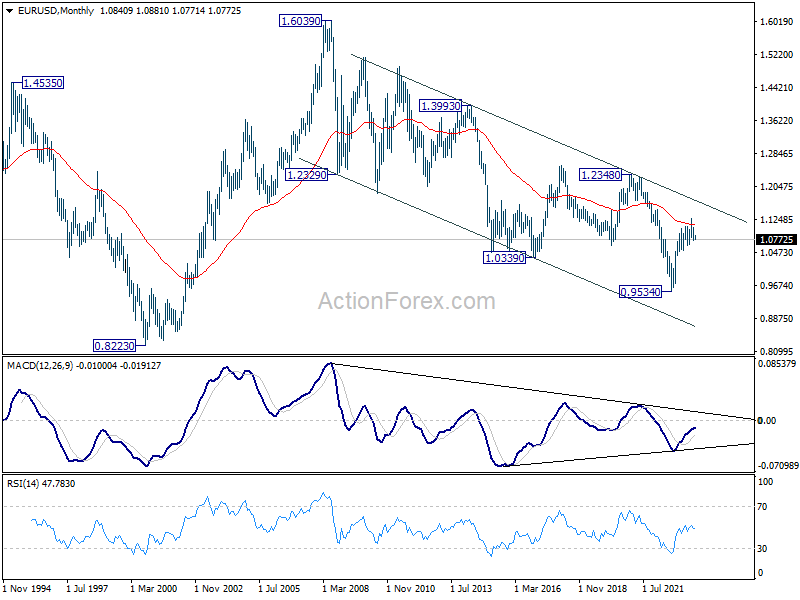

EUR/USD Weekly Outlook

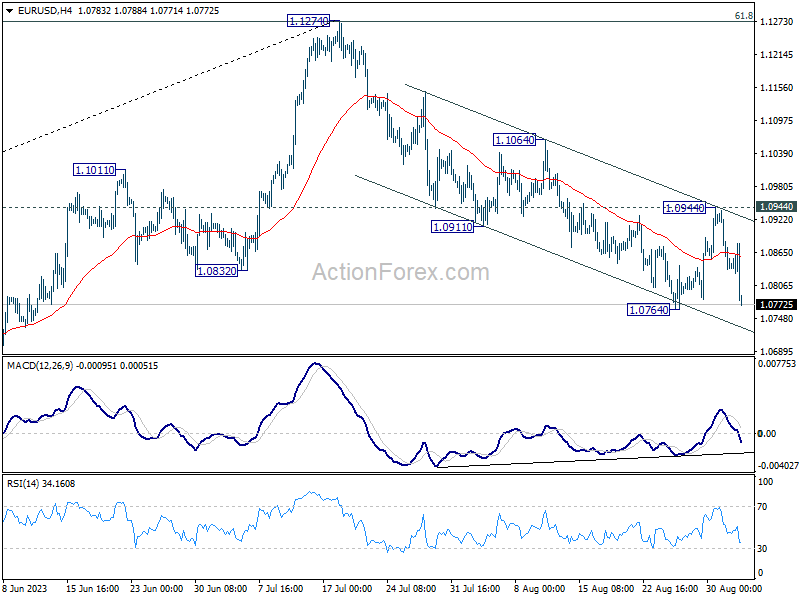

EUR/USD's rebounded to 1.0944 last week, but was rejected by 55 D EMA (now at 1.0924) and fell sharply since then. The development keeps near term outlook bearish. Immediate focus is now on 1.0764 support this week, firm break there will resume whole decline from 1.1274 to 1.0609/34 cluster support next. Meanwhile, further decline will be in favor as long as 1.0944 resistance holds, in case of recovery.

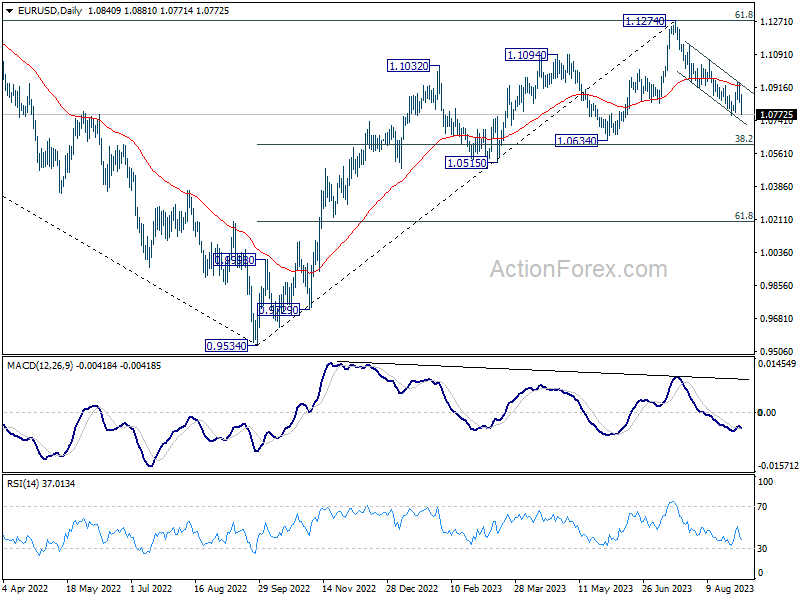

In the bigger picture, fall from 1.1274 medium term top is seen as a correction to up trend from 0.9534 (2022 low). Deeper decline would be seen to 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609). Strong support could be seen there, at least on first attempt, to bring rebound. Yet, medium term outlook will be neutral for now, as long as 1.1274 resistance holds.

In the long term picture, focus stays on 55 M EMA (now at 1.1124). Rejection by this EMA will revive long term bearishness. However, sustained break above here will be affirm the case of long term bullish reversal and target 1.2348 resistance for confirmation.

Summary 9/4 – 9/8

Monday, Sep 4, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 22:45 | NZD | Terms of Trade Index Q2 | -1.30% | -1.50% |

| 23:50 | JPY | Monetary Base Y/Y Aug | -0.70% | -1.30% |

| 01:00 | AUD | TD Securities Inflation M/M Aug | 0.80% | |

| 06:00 | EUR | Germany Trade Balance (EUR) Jul | 17.6B | 18.7B |

| 07:00 | CHF | GDP Q/Q Q2 | 0.10% | 0.30% |

| 08:30 | EUR | Eurozone Sentix Investor Confidence Sep | -19.6 | -18.9 |

| 23:01 | GBP | BRC Like-For-Like Retail Sales Y/Y Aug | 2.20% | 1.80% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 22:45 | NZD | Terms of Trade Index Q2 | |

| Forecast: -1.30% | Previous: -1.50% | ||

| 23:50 | JPY | Monetary Base Y/Y Aug | |

| Forecast: -0.70% | Previous: -1.30% | ||

| 01:00 | AUD | TD Securities Inflation M/M Aug | |

| Forecast: | Previous: 0.80% | ||

| 06:00 | EUR | Germany Trade Balance (EUR) Jul | |

| Forecast: 17.6B | Previous: 18.7B | ||

| 07:00 | CHF | GDP Q/Q Q2 | |

| Forecast: 0.10% | Previous: 0.30% | ||

| 08:30 | EUR | Eurozone Sentix Investor Confidence Sep | |

| Forecast: -19.6 | Previous: -18.9 | ||

| 23:01 | GBP | BRC Like-For-Like Retail Sales Y/Y Aug | |

| Forecast: 2.20% | Previous: 1.80% | ||

Tuesday, Sep 5, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Current Account Balance (AUD) Q2 | 8.1B | 12.3B |

| 01:45 | CNY | Caixin Services PMI Aug | 53.6 | 54.1 |

| 04:30 | AUD | RBA Interest Rate Decision | 4.10% | 4.10% |

| 07:45 | EUR | Italy Services PMI Aug | 50.2 | 51.5 |

| 07:50 | EUR | France Services PMI Aug F | 46.7 | 46.7 |

| 07:55 | EUR | Germany Services PMI Aug F | 47.3 | 47.3 |

| 08:00 | EUR | Eurozone Services PMI Aug F | 48.3 | 48.3 |

| 08:30 | GBP | Services PMI Aug F | 48.7 | 48.7 |

| 09:00 | EUR | Eurozone PPI M/M Jul | -0.60% | -0.40% |

| 09:00 | EUR | Eurozone PPI Y/Y Jul | -7.60% | -3.40% |

| 14:00 | USD | Factory Orders M/M Jul | -2.50% | 2.30% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Current Account Balance (AUD) Q2 | |

| Forecast: 8.1B | Previous: 12.3B | ||

| 01:45 | CNY | Caixin Services PMI Aug | |

| Forecast: 53.6 | Previous: 54.1 | ||

| 04:30 | AUD | RBA Interest Rate Decision | |

| Forecast: 4.10% | Previous: 4.10% | ||

| 07:45 | EUR | Italy Services PMI Aug | |

| Forecast: 50.2 | Previous: 51.5 | ||

| 07:50 | EUR | France Services PMI Aug F | |

| Forecast: 46.7 | Previous: 46.7 | ||

| 07:55 | EUR | Germany Services PMI Aug F | |

| Forecast: 47.3 | Previous: 47.3 | ||

| 08:00 | EUR | Eurozone Services PMI Aug F | |

| Forecast: 48.3 | Previous: 48.3 | ||

| 08:30 | GBP | Services PMI Aug F | |

| Forecast: 48.7 | Previous: 48.7 | ||

| 09:00 | EUR | Eurozone PPI M/M Jul | |

| Forecast: -0.60% | Previous: -0.40% | ||

| 09:00 | EUR | Eurozone PPI Y/Y Jul | |

| Forecast: -7.60% | Previous: -3.40% | ||

| 14:00 | USD | Factory Orders M/M Jul | |

| Forecast: -2.50% | Previous: 2.30% | ||

Wednesday, Sep 6, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | GDP Q/Q Q2 | 0.30% | 0.20% |

| 06:00 | EUR | Germany Factory Orders M/M Jul | -4.30% | 7.00% |

| 08:30 | GBP | Construction PMI Aug | 49.8 | 51.7 |

| 09:00 | EUR | Eurozone Retail Sales M/M Jul | -0.20% | -0.30% |

| 12:30 | CAD | Labor Productivity Q/Q Q2 | -0.10% | -0.60% |

| 12:30 | CAD | Trade Balance (CAD) Jul | -3.5B | -3.7B |

| 12:30 | USD | Trade Balance (USD) Jul | -67.9B | -65.5B |

| 12:30 | USD | Goods Trade Balance Jul | $-91.2B | |

| 13:45 | USD | Services PMI Aug F | 51.0 | 51.0 |

| 14:00 | USD | ISM Services PMI Aug | 52.6 | 52.7 |

| 14:00 | CAD | BoC Interest Rate Decision | 5.00% | 5.00% |

| 18:00 | USD | Fed's Beige Book | ||

| 22:45 | NZD | Manufacturing Sales Q2 | -2.80% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | GDP Q/Q Q2 | |

| Forecast: 0.30% | Previous: 0.20% | ||

| 06:00 | EUR | Germany Factory Orders M/M Jul | |

| Forecast: -4.30% | Previous: 7.00% | ||

| 08:30 | GBP | Construction PMI Aug | |

| Forecast: 49.8 | Previous: 51.7 | ||

| 09:00 | EUR | Eurozone Retail Sales M/M Jul | |

| Forecast: -0.20% | Previous: -0.30% | ||

| 12:30 | CAD | Labor Productivity Q/Q Q2 | |

| Forecast: -0.10% | Previous: -0.60% | ||

| 12:30 | CAD | Trade Balance (CAD) Jul | |

| Forecast: -3.5B | Previous: -3.7B | ||

| 12:30 | USD | Trade Balance (USD) Jul | |

| Forecast: -67.9B | Previous: -65.5B | ||

| 12:30 | USD | Goods Trade Balance Jul | |

| Forecast: | Previous: $-91.2B | ||

| 13:45 | USD | Services PMI Aug F | |

| Forecast: 51.0 | Previous: 51.0 | ||

| 14:00 | USD | ISM Services PMI Aug | |

| Forecast: 52.6 | Previous: 52.7 | ||

| 14:00 | CAD | BoC Interest Rate Decision | |

| Forecast: 5.00% | Previous: 5.00% | ||

| 18:00 | USD | Fed's Beige Book | |

| Forecast: | Previous: | ||

| 22:45 | NZD | Manufacturing Sales Q2 | |

| Forecast: | Previous: -2.80% | ||

Thursday, Sep 7, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Trade Balance (AUD) Jul | 10.05B | 11.32B |

| 03:00 | CNY | Trade Balance (USD) Aug | 68.0B | 80.6B |

| 03:00 | CNY | Trade Balance (CNY) Aug | 494B | 576B |

| 05:00 | JPY | Leading Economic Index Jul P | 107.9 | 109.1 |

| 05:45 | CHF | Unemployment Rate Aug | 2.10% | 2.10% |

| 06:00 | EUR | Germany Industrial Production M/M Jul | -0.40% | -1.50% |

| 06:45 | EUR | France Trade Balance (EUR) Jul | -6.8B | -6.7B |

| 07:00 | CHF | Foreign Currency Reserves (CHF) Aug | 698B | |

| 08:00 | EUR | Italy Retail Sales M/M Jul | 0.20% | -0.20% |

| 09:00 | EUR | Eurozone GDP Q/Q Q2 | 0.30% | 0.30% |

| 12:30 | CAD | Building Permits M/M Jul | 7.50% | 6.10% |

| 12:30 | USD | Initial Jobless Claims (Sep 1) | 235K | 228K |

| 12:30 | USD | Nonfarm Productivity Q2 | 3.50% | 3.70% |

| 12:30 | USD | Unit Labor Costs Q2 | 1.80% | 1.60% |

| 14:00 | CAD | Ivey PMI Aug | 49.2 | 48.6 |

| 14:00 | CAD | Ivey Purchasing Managers Index s.a Aug | 48.6 | |

| 14:30 | USD | Natural Gas Storage | 32B | |

| 15:00 | USD | Crude Oil Inventories | -10.6M | |

| 23:30 | JPY | Labor Cash Earnings Y/Y Jul | 2.40% | 2.30% |

| 23:30 | JPY | Overall Household Spending Y/Y Jul | -4.20% | |

| 23:50 | JPY | Bank Lending Y/Y Aug | 2.80% | 2.90% |

| 23:50 | JPY | GDP Q/Q Q2 F | 1.40% | 1.50% |

| 23:50 | JPY | GDP Deflator Y/Y Q2 F | 3.40% | 3.40% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Trade Balance (AUD) Jul | |

| Forecast: 10.05B | Previous: 11.32B | ||

| 03:00 | CNY | Trade Balance (USD) Aug | |

| Forecast: 68.0B | Previous: 80.6B | ||

| 03:00 | CNY | Trade Balance (CNY) Aug | |

| Forecast: 494B | Previous: 576B | ||

| 05:00 | JPY | Leading Economic Index Jul P | |

| Forecast: 107.9 | Previous: 109.1 | ||

| 05:45 | CHF | Unemployment Rate Aug | |

| Forecast: 2.10% | Previous: 2.10% | ||

| 06:00 | EUR | Germany Industrial Production M/M Jul | |

| Forecast: -0.40% | Previous: -1.50% | ||

| 06:45 | EUR | France Trade Balance (EUR) Jul | |

| Forecast: -6.8B | Previous: -6.7B | ||

| 07:00 | CHF | Foreign Currency Reserves (CHF) Aug | |

| Forecast: | Previous: 698B | ||

| 08:00 | EUR | Italy Retail Sales M/M Jul | |

| Forecast: 0.20% | Previous: -0.20% | ||

| 09:00 | EUR | Eurozone GDP Q/Q Q2 | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 12:30 | CAD | Building Permits M/M Jul | |

| Forecast: 7.50% | Previous: 6.10% | ||

| 12:30 | USD | Initial Jobless Claims (Sep 1) | |

| Forecast: 235K | Previous: 228K | ||

| 12:30 | USD | Nonfarm Productivity Q2 | |

| Forecast: 3.50% | Previous: 3.70% | ||

| 12:30 | USD | Unit Labor Costs Q2 | |

| Forecast: 1.80% | Previous: 1.60% | ||

| 14:00 | CAD | Ivey PMI Aug | |

| Forecast: 49.2 | Previous: 48.6 | ||

| 14:00 | CAD | Ivey Purchasing Managers Index s.a Aug | |

| Forecast: | Previous: 48.6 | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 32B | ||

| 15:00 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -10.6M | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y Jul | |

| Forecast: 2.40% | Previous: 2.30% | ||

| 23:30 | JPY | Overall Household Spending Y/Y Jul | |

| Forecast: | Previous: -4.20% | ||

| 23:50 | JPY | Bank Lending Y/Y Aug | |

| Forecast: 2.80% | Previous: 2.90% | ||

| 23:50 | JPY | GDP Q/Q Q2 F | |

| Forecast: 1.40% | Previous: 1.50% | ||

| 23:50 | JPY | GDP Deflator Y/Y Q2 F | |

| Forecast: 3.40% | Previous: 3.40% | ||

Friday, Sep 8, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 06:00 | EUR | Germany CPI M/M Aug F | 0.30% | 0.30% |

| 06:00 | EUR | Germany CPI Y/Y Aug F | 6.10% | 6.10% |

| 06:45 | EUR | France Industrial Output M/M Jul | 0.20% | -0.90% |

| 12:30 | CAD | Net Change in Employment Aug | 20.0K | -6.4K |

| 12:30 | CAD | Unemployment Rate Aug | 5.60% | 5.50% |

| 12:30 | CAD | Capacity Utilization Q2 | 82.50% | 81.90% |

| 14:00 | USD | Wholesale Inventories Jul F | -0.10% | -0.10% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 06:00 | EUR | Germany CPI M/M Aug F | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 06:00 | EUR | Germany CPI Y/Y Aug F | |

| Forecast: 6.10% | Previous: 6.10% | ||

| 06:45 | EUR | France Industrial Output M/M Jul | |

| Forecast: 0.20% | Previous: -0.90% | ||

| 12:30 | CAD | Net Change in Employment Aug | |

| Forecast: 20.0K | Previous: -6.4K | ||

| 12:30 | CAD | Unemployment Rate Aug | |

| Forecast: 5.60% | Previous: 5.50% | ||

| 12:30 | CAD | Capacity Utilization Q2 | |

| Forecast: 82.50% | Previous: 81.90% | ||

| 14:00 | USD | Wholesale Inventories Jul F | |

| Forecast: -0.10% | Previous: -0.10% | ||

Weekly Economic & Financial Commentary: What Is the Yield Curve Saying about Recession?

Summary

United States: Labor Market Slowly Losing Its Swagger

- This week's data continue to demonstrate an underlying resiliency in the economy, but with flickers of moderation. Employers added 187K net new jobs in August. The cooling labor market makes another rate hike this cycle unlikely in our view, yet with the labor market still tight and wage growth elevated, cuts are a ways off.

- Next week: Trade Balance (Wed.), ISM Services Index (Wed.)

International: Moderating Global Growth and Moderating Global Inflation

- This week's key international data continued the trend of slowing global growth and gradual easing of inflation pressures. China's August services PMI fell for a fifth straight month to 51.0, while in Canada the economy unexpectedly contracted in Q2. In the Eurozone, the August headline CPI held steady at 5.3% year-over-year, but core inflation moderated to 5.3%.

- Next week: Reserve Bank of Australia Policy Rate (Tue.), Bank of Canada Policy Rate (Wed.), Mexico CPI (Thu.)

Interest Rate Watch: What Is the Yield Curve Saying about Recession?

- Many financial market indicators seem consistent with the rising odds of a soft landing. The S&P 500 is up nearly 18% year-to-date, and corporate bond spreads have narrowed since the start of the year. However, one market indicator continues to flash some warning signs about the economic outlook: the shape of the yield curve.

Credit Market Insights: Middle-Upper Income Households Increasingly Relying on Credit Cards

- The Household Pulse survey has been showing an increasing trend of middle-to-upper income households using credit cards and other loans to meet their weekly spend. These data come on the heels of data released earlier this month that showed consumers racked up an outstanding balance of over $1 trillion for the first time ever.

Topic of the Week: The State of U.S. Agriculture 2023

- The nation's farmers have endured tough economic and climate conditions over the past few years. Fortunately, the tide seems to be turning, with easing cost inflation and supply chain frictions.

The Weekly Bottom Line: Soft GDP Data Take Pressure off BoC

U.S. Highlights

- The U.S. economy added 187k jobs in August, but revisions to the two prior months subtracted a notable 110k jobs from the previous reported tally.

- Both total and core PCE inflation rose by 0.2% month-on-month in July, equal to the monthly change seen in June for both measures.

- Hurricane Idalia, the first of the season to make landfall in the U.S., caused widespread flooding and wind damage through Florida’s Big Bend region and up through Georgia and the Carolinas.

Canadian Highlights

- Payrolls and GDP data show the economy coming off the boil, reflecting a year and a half’s worth of rate hikes doing their job to cool economic momentum.

- Markets pricing for another rate hike by year-end has come in noticeably, following the string of softening data.

- The job’s not quite done yet, but the Bank of Canada can feel better about how far they’ve come in reaching the target state.

U.S. – The Labor Market Takes a Holiday

The U.S. almost managed to escape August without a major hurricane, but unfortunately those hopes were dashed when Hurricane Idalia made landfall as a category 3 hurricane on Wednesday in Florida. Strong winds, rain, and storm surges caused widespread flooding and property damage, leaving hundreds of thousands of Americans without power across the Southeast. Although the extent of the damage is still being assessed, insurance and clean-up costs are expected to be well over a billion dollars.

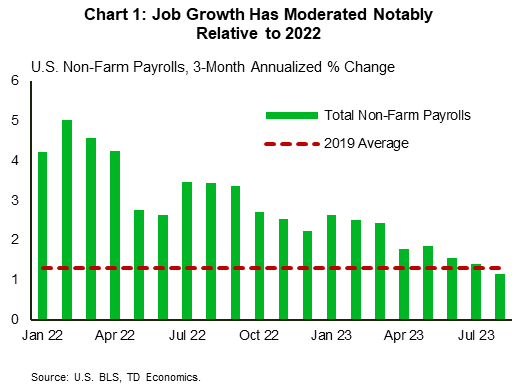

Fortunately for the national economy, sunnier skies could be found in this week’s economic data, including the 187k new jobs added in August. While this reading, in addition to the downward revisions to the previous two months, marks a continued moderation in the pace of hiring, it indicates that supply and demand in the labor market are coming into a more sustainable alignment (Chart 1). This was further evidenced by the decline in job openings in July, with the job opening to unemployed ratio falling to 1.5. While the unemployment rate did rise to 3.8%, this mostly resulted from a boost in labor force growth which could be considered a net positive if it helps to offset labor shortages. On aggregate, this progress will come as positive news for the Federal Reserve, however the most recent data on inflation was slightly more mixed.

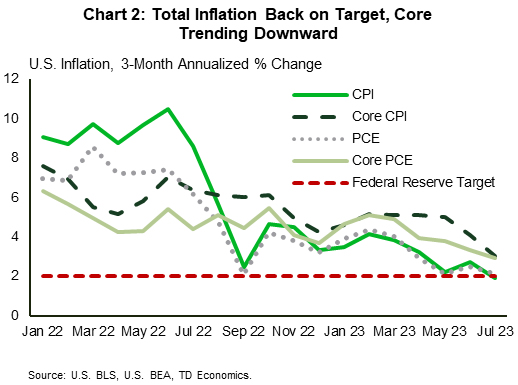

On Thursday, we saw that PCE inflation rose by 3.3% year-on-year (y/y) in July, up from 3.0% in June. This was driven by a moderation in the negative base effects resulting from the spike in energy prices last year in addition to a moderate uptick in services inflation – driven entirely by Powell’s ‘supercore’ component. Looking at the 3-month annualized trend (Chart 2), we can see that total inflation is pushing closer to the Fed’s 2% target, though this is likely to be short lived given the recent move up in energy prices. In addition, while core inflation is moving in the right direction, non-housing core services have barely budged from their cyclical highs and continue to run at an elevated annualized pace. Until we see a meaningful cooling here, core inflation will likely remain north of 3%.

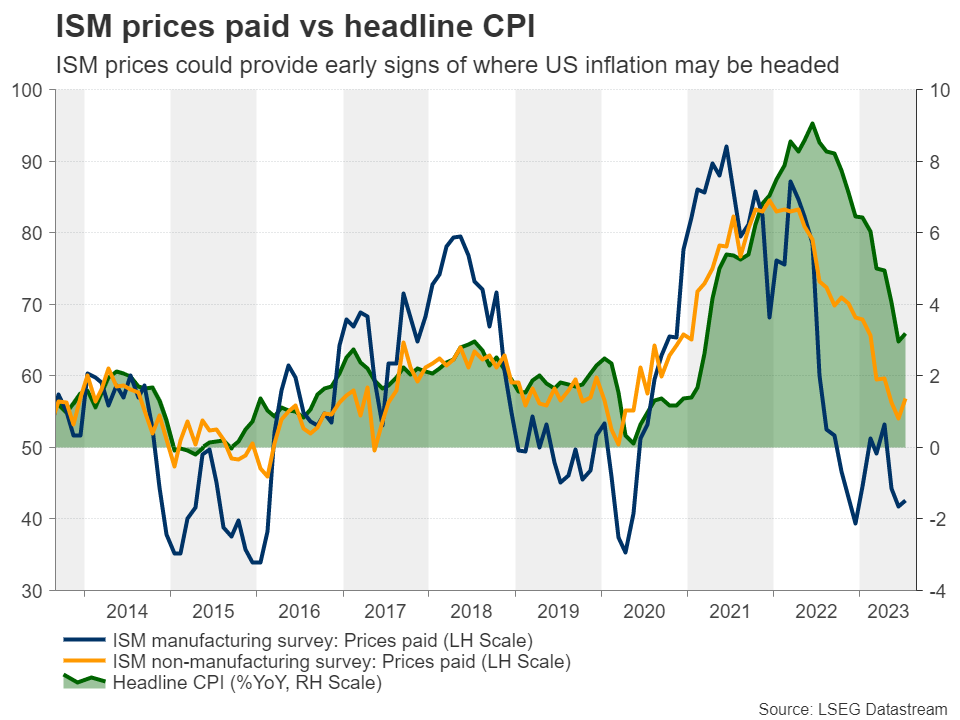

Some offset to inflationary pressures continues to be provided by the goods sector, with the ISM Manufacturing Purchasing Managers’ Index (PMI) showing manufacturing activity contracted for a tenth consecutive month in August. Ten out of sixteen industries reported lower input prices, which is likely factoring in downstream to the consumer. Price growth in the services sector has been more stubborn, so next week’s update on the ISM Services PMI will offer insight into how resilient the sector remains.

With the Labor Day holiday on Monday, next week will be short both in length and in the volume of economic data that we receive. However, the release of the Fed’s Beige Book will be one item to watch, as it will feed into the viewpoints that FOMC members bring to the upcoming meeting. We expect that the progress on inflation and job market cooling up to this point will be sufficient to warrant a hold in 2 weeks’ time, but the tone will likely remain hawkish to guard against the potential for pre-mature easing in financial conditions.

Canada – Soft GDP Data Take Pressure off BoC

And just like that, concerns about the need for another Bank of Canada (BoC) rate hike have cooled substantially. Payrolls and GDP data that show the economy coming off the boil, reflect a year and a half's worth of rate hikes doing their job to cool economic momentum. The job's not quite done yet, but with the data coming in soft this week, the BoC can feel better about how far they've come in reaching the target state.

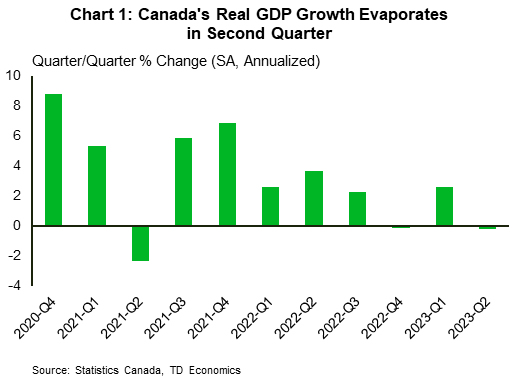

This week came as a bit of a bad news is good news moment. GDP growth in the first quarter was revised downward, easing some concerns that growth had accelerated substantially above-trend in early 2023. With a healthy hand-off from the first quarter, market consensus was that momentum in the second quarter would see the economy expand at a 1.2% quarter-on-quarter (q/q, annualized) rate. What happened was a loud thud, with the economy shrinking marginally (-0.2% q/q) amid a steep drop-off in consumption growth and a host of extreme events (Chart 1). Striking workers and a horrific fire season acted as a drag on activity – bringing the economy to a standstill.

Looking forward, there doesn't appear to be much relief. The third quarter looks to be getting off on the wrong foot as Statistics Canada's flash estimate shows the economy failed to grow in July. This is in line with our view that overall economic momentum will remain weak over the rest of this year. With rates set to remain well in restrictive territory for the coming months, the prospect of strong growth in the second half of 2023 seems far-off.

The news has palpably shifted investor sentiment. Market pricing that had started the week with roughly six-in-ten odds of a hike by the end of this year has pulled back to a much more moderate one-in-ten as of this morning. On cue, bonds are rallying as investors look to lock-up solid yields. Ten-year yields that started the week at roughly 3.7% have shaved off about 15 basis points as of the time of writing. The five-year yield is down nearly 25 basis points over the same time span.

That said, while the economy is cooling, it's not cold. The labour market is still churning out jobs. This week's Survey of Employment, Payrolls and Hours (SEPH) showed fixed weight wages still growing at 3.9% year-on-year (y/y). While the fixed weight wage gains are slightly lower than the 5% y/y print from the Labour Force Survey, they both reflect a labour market that, despite recent setbacks, still has a healthy appetite to hire – a fact supported by job vacancies that are still roughly 250k positions higher than before the pandemic.

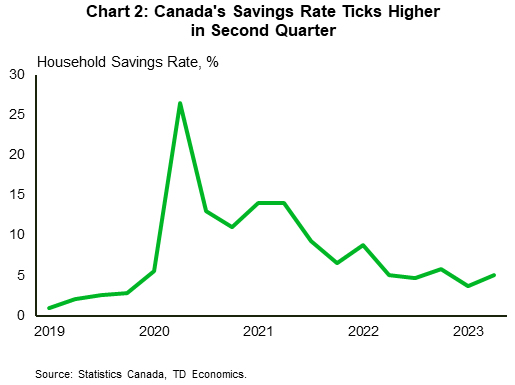

For the BoC, the totality of this week's data suggest that things are still trending in the right direction to meet its mandate. Sure, the labour market suggests that underlying pressures persist, but spending data show consumers aren't freely spending their wage gains – as the savings rate ticked up 1.4 percentage points (Chart 2). In totality, the case for further hikes weakened this week, helping lift hopes of a soft landing.

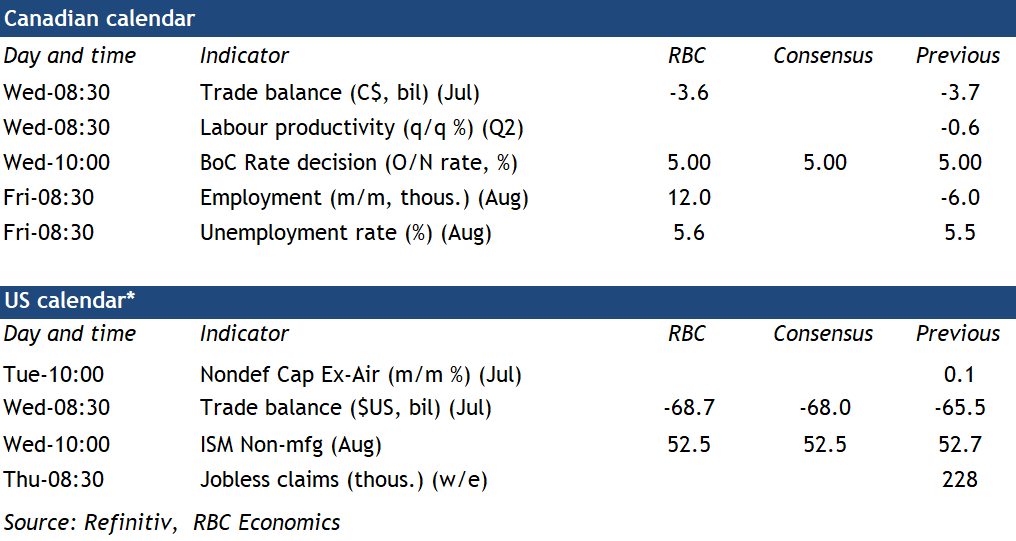

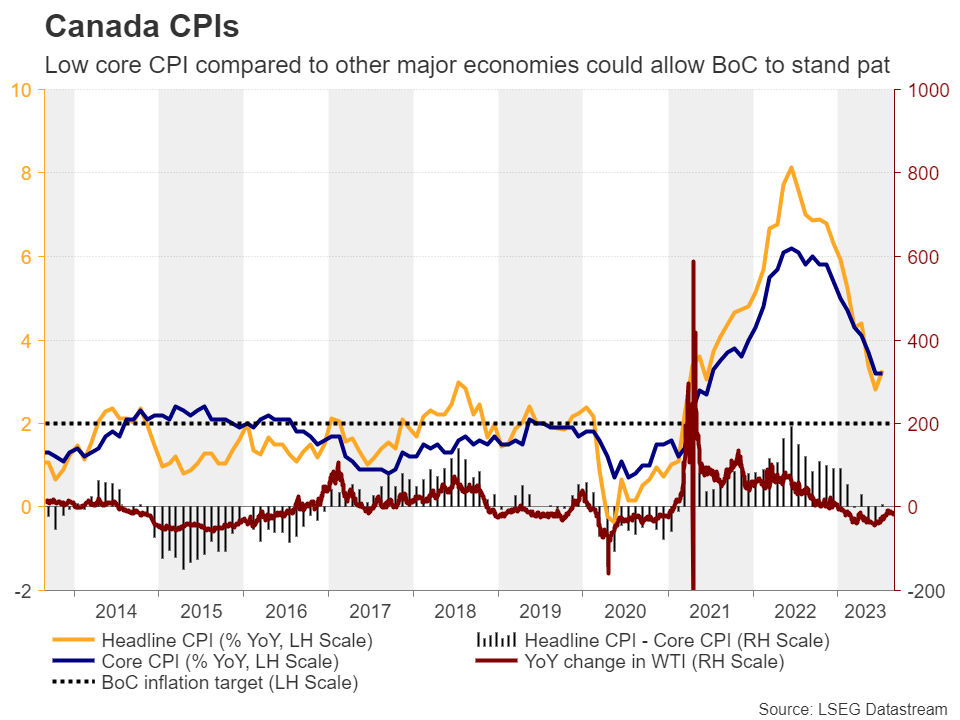

Bank of Canada to Pause Rate Hikes Ahead of Key Jobs Data

We expect the Bank of Canada to move back to the sidelines Wednesday, foregoing another interest rate hike. But it’ll keep its options open in case more increases are necessary down the road.

Broader price growth is still running above the BoC’s 2% inflation target despite slower headline CPI growth. But the BoC is more interested in where prices are going than where they’ve been. And softer economic growth numbers suggest headwinds from earlier interest rate hikes are gaining strength.

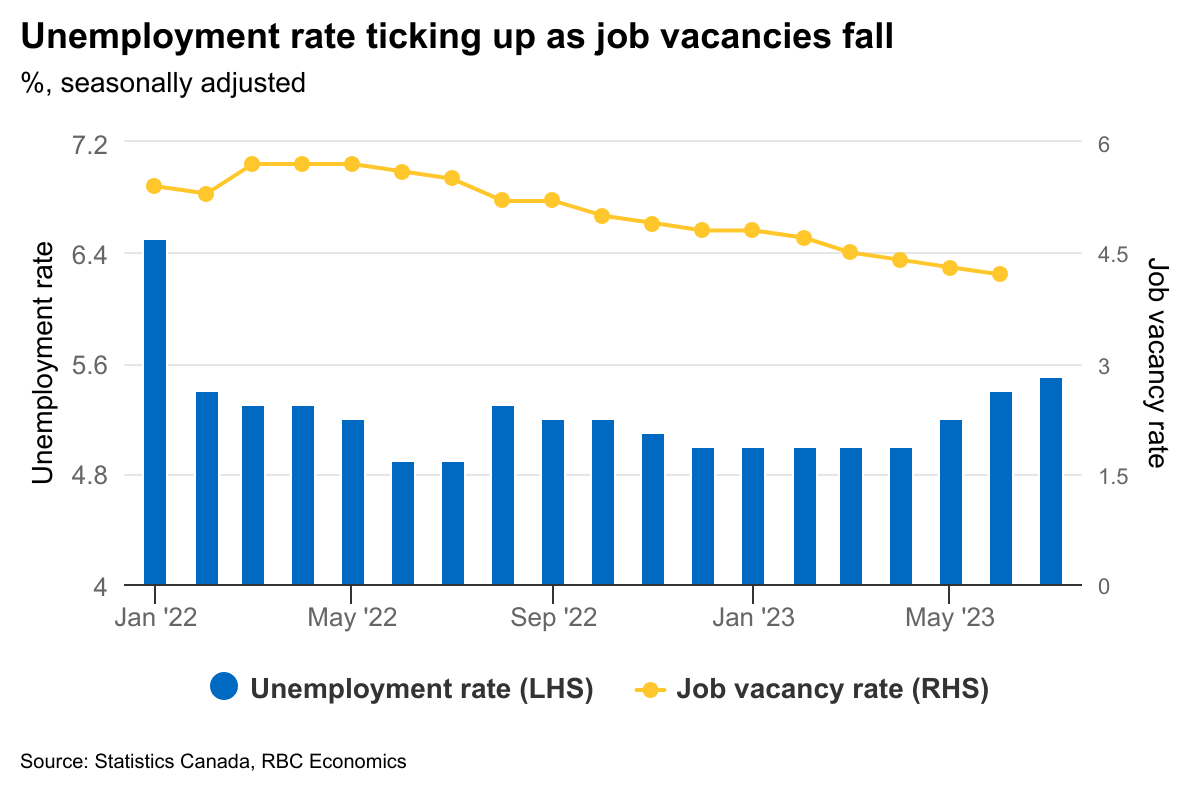

GDP growth has softened with a 0.2% decline (at an annualized rate) in Q2 that was substantially softer than the 1.5% increase the BoC previously assumed. Most of the Q2 weakness came from a decline in June GDP with a flat preliminary estimate for July leaving growth tracking potentially another negative GDP print in Q3 – well below the BoC’s 1.5% (annualized) forecast. And the 0.5 percentage point increase in the unemployment rate over the last three months is the largest rise (outside of the pandemic) since the 2008/09 recession. Canadian labour market data is notoriously volatile, but we think there is more than enough evidence of cooling for the BoC to hold rates steady for now.

The August job numbers—released next Friday—will arrive too late to influence the BoC's interest rate decision. But they’ll help determine how long this next expected pause in rate hikes will last. For our part, we expect a small increase in August employment (12,000.) That wouldn’t be large enough to prevent a fourth consecutive tick higher in the unemployment rate given surging population growth, and would be further evidence that labour market headwinds are building. The job switching rate has been trending lower, something that typically happens when labour markets weaken. The share of involuntary part-time workers has inched up since early 2023. And labour demand is continuing to slow, with June job vacancies dropping to their lowest level in 2 years.

Week ahead data watch

According to the advance economic indicators report, the U.S. goods deficit likely widened to $68.7 billion in July. Much of that was driven by rising consumer goods imports and a 10.3% jump in motor vehicle exports.

July Canadian trade data likely showed declines for both exports and imports with a strike at B.C. ports disrupting ocean trade flows in the month. Higher oil prices likely boosted the energy trade balance, but we look for the trade deficit to be $3.6 billion in July, close to June’s $3.7 billion level.

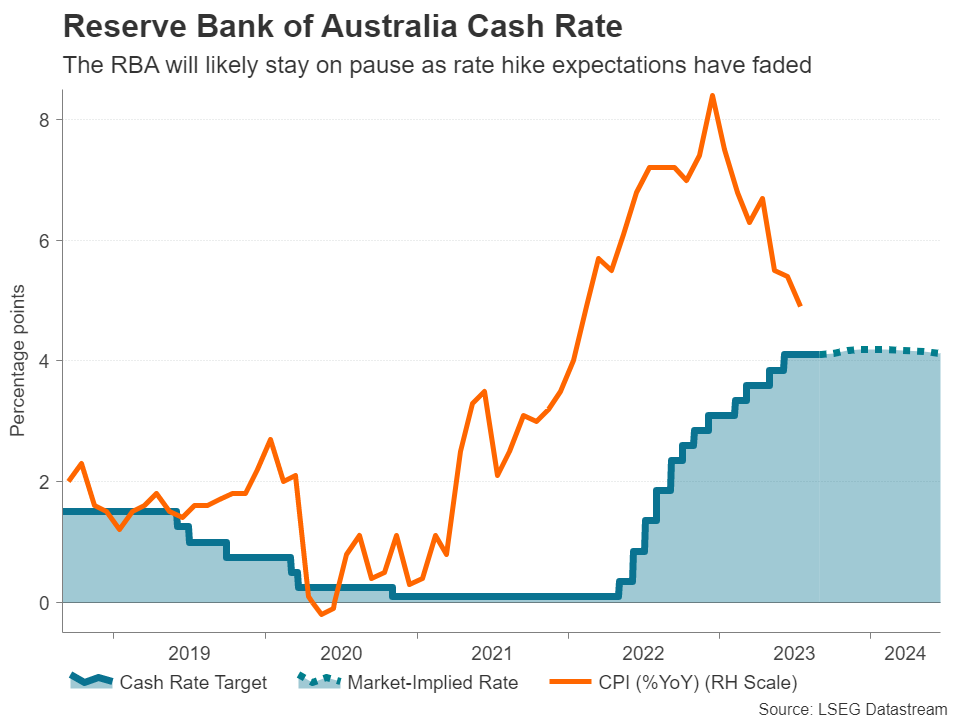

RBA Set to Stay on Pause as Inflation and Economy Cool

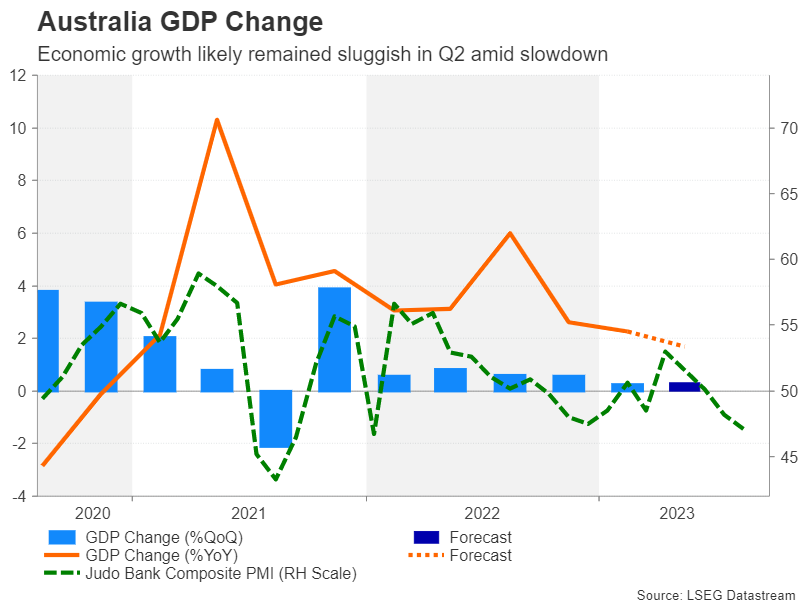

The Reserve Bank of Australia will decide on interest rates on Tuesday (04:30 GMT), likely keeping them on hold for the third straight month. One reason for the RBA’s increased caution lately is weaker economic growth. GDP data due on Wednesday (01:30 GMT) will reveal whether growth remained sluggish or improved in the second quarter. The Australian dollar is vulnerable to further losses amid mounting worries about China on top of a less hawkish RBA.

Inflation threat is receding

As policymakers continue their battle against high inflation, there is good news and bad news for the Australian economy. The good news is that inflation is well on the way down. The consumer price index eased to 4.9% y/y in July – the lowest since February 2022. Underlying measures of inflation are also falling, with weighted CPI declining from 5.4% to 4.9% y/y. In a further encouraging sign, wage growth appears to have peaked.

For a central bank that is highly conscious about the cumulative effects from the 400-bps-worth of tightening that have yet to be felt, leaving the cash rate unchanged in September seems like a sensible move. Analysts and markets both concur, and no change is almost fully priced in by investors.

Is Australia headed for recession?

The bad news, however, is that growth has slowed substantially this year amid a number of headwinds, higher rates being the main one. The housing market was the first to feel the heat from rising borrowing costs and was a significant drag on growth in 2022. However, this year, higher rates are taking their toll on consumption, as households are being forced to rein in their spending.

But that’s not the only trouble spot. Exports have slumped in the past few months as China’s economy has hit a stumbling block. China is Australia’s largest trading partner so any slowdown there would have a material impact on local exporters.

GDP growth moderated to just 0.2% q/q in the first three months of the year and it likely quickened slightly to 0.3% in the second quarter. But if the S&P Global PMI surveys are any indication, a worse figure is possible and the economy could be headed for a small contraction in Q3.

Some green shoots

However, even if a poor GDP reading adds to the slew of data supporting a prolonged pause by the RBA, that might be an assumption too far as there are some positive developments as well. The labour market remains tight even if there has been a slight cooling off lately, and that should support consumption. There are already some early signs that consumer spending is picking up.

What is more incredible is that house prices have started to rebound again, countering the argument that further rate hikes could cause a crash in the housing market.

Moreover, all the evidence at the moment is that inflation globally is proving to be a lot stickier than anticipated so even if the economy continues to lose steam, the RBA may have to provide an extra nudge for CPI to fall sustainably within its 2-3% target band. Hence, there’s a risk some investors are too readily dismissing policymakers’ warnings about the need for further rate hikes. After all, the outlook could easily change if the economic situation in China starts to improve.

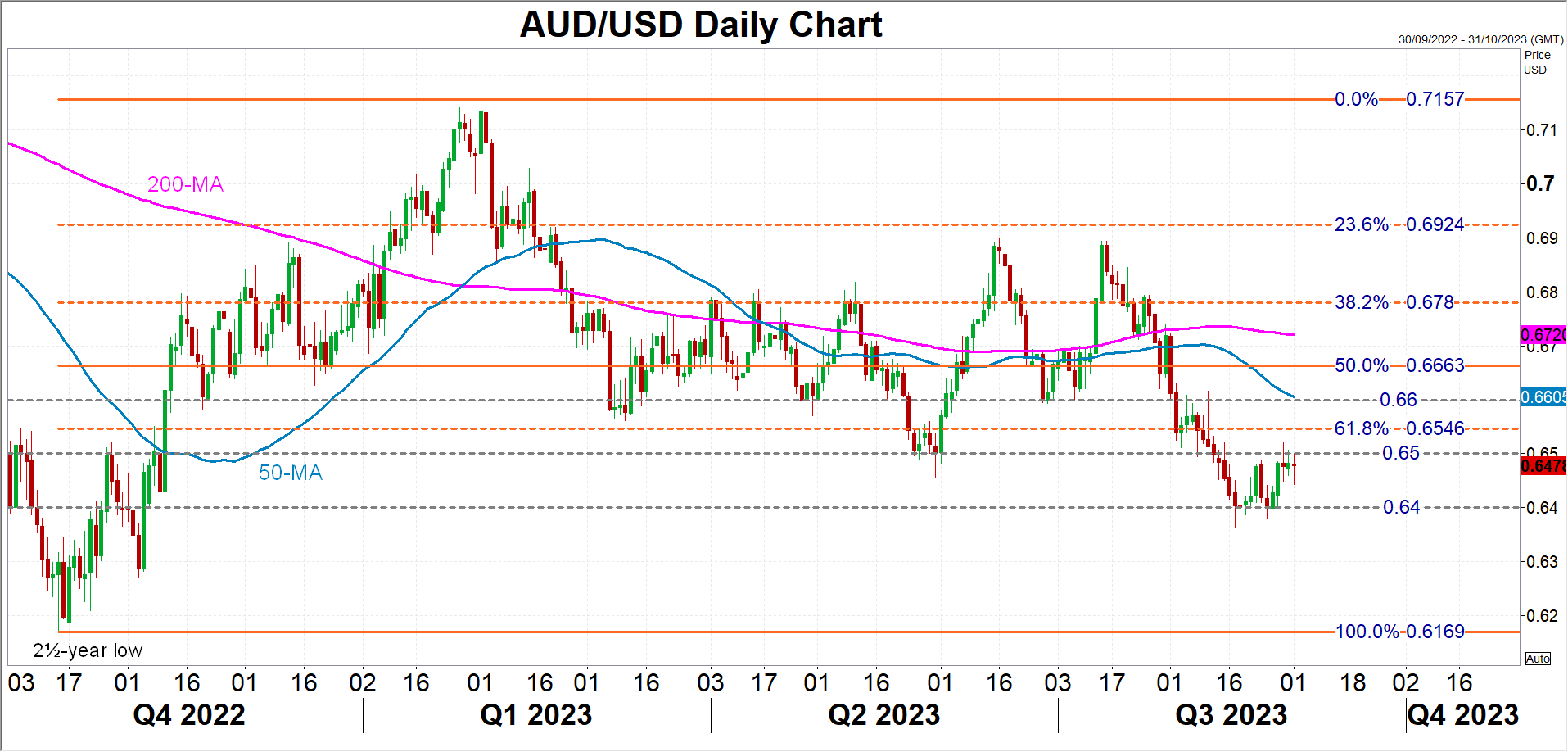

Aussie slide may have more to go

This applies to the Australian dollar too. While a relatively more hawkish Fed and stronger American economy go some way in explaining the aussie’s weakness against the US dollar this year, the main factor behind the extent of this underperformance is all the gloom surrounding China in recent months.

In the near term, however, a neutral RBA won’t be enough to stem the aussie’s losses and a breach of the October 2022 low of $0.6169 is possible. But in the event that the RBA stresses the upside risks to inflation or the incoming US data keeps surprising to the downside, the aussie could rebound towards its 50-day moving average just above the $0.66 level.

Week Ahead – RBA and BoC to Kick-Start Key Round of Central Bank Meetings

After a barrage of US data hurt the dollar this week, with investors having second thoughts as to whether another Fed hike may be needed, the US agenda will become lighter next week with the spotlight turning to the ISM non-manufacturing PMI. Elsewhere, the RBA and the BoC are holding their interest rate decisions, kick-starting a round of pivotal meetings by major central banks, which could well impact forthcoming directions of major currency pairs.

Light US agenda, focus on ISM non-mfg PMI

The US dollar pulled back this week as several US data forced investors to reconsider the likelihood of another hike by the Fed before the end credits of this tightening crusade roll, and to add more basis points worth of rate cuts for next year.

Just after Fed Chair Powell kept the prospect of more rate increases alive at Jackson Hole, investors lifted slightly their implied path, but on Tuesday, job openings for July hit their lowest since March 2021 and consumer sentiment for August deteriorated, while on Wednesday, the ADP employment report revealed that the US private sector added less jobs than expected during August.

Investors had second thoughts after the data and currently, they are evenly split on whether another hike by November is warranted. The US agenda will be light in the coming week, with Monday being a holiday due to Labor Day, but there is a data point that could well impact expectations regarding the Fed’s plans, and this is the ISM non-manufacturing PMI on Wednesday.

The preliminary manufacturing and services PMIs from S&P Global both confounded market expectations of largely unchanged points and instead declined in August. With that in mind, the risks surrounding the ISM index may be tilted to the downside. That said, whether the probability of another Fed hike will further decline may also depend on the new orders and prices subindices. If there are declines there as well, the dollar and Treasury yields could stay under pressure and equities may continue drifting higher as expectations of lower interest rates could keep the net present value (NPV) of high-growth firms elevated.

Aussie awaits RBA and Chinese data

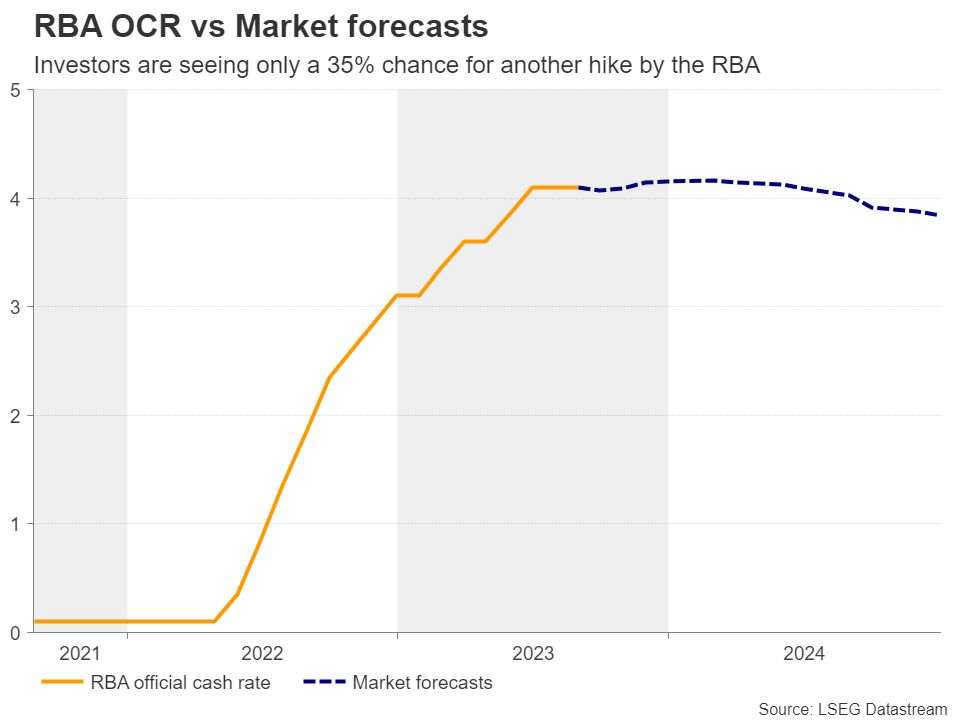

On Tuesday, the Reserve Bank of Australia begins a series of central bank meetings that could prove very important in guiding market expectations regarding the future of monetary policy in the major economies. At their last meeting, officials stood pat, disappointing expectations of a rate hike, but leaving the door open to more action by saying that some further tightening of monetary policy may be required, but also that this will depend upon the data and the evolving assessment of risk.

Since then, the employment data for July revealed that the economy has lost jobs instead of gaining, with the unemployment rate rising to 3.7% from 3.5%. On top of that, CPI numbers for the month of July showed that headline inflation in Australia dropped to 4.9% y/y from 5.4%, which eliminated any speculation with regards to a potential hike at this gathering.

Currently, investors are nearly certain that policymakers will keep their hands off the hike button at this meeting, while they are assigning around only a 35% probability for another quarter-point increase to be delivered by the end of the year.

Having said that though, with the core monthly CPI rate sliding only to 5.8% y/y from 6.1%, still well above the Bank’s inflation target range of 2-3%, closing the door to more hikes may be an unwise choice. Therefore, if policymakers reiterate the guidance that some further tightening may be required, even if they stand pat at this meeting, the probability for another hike before the end of this year could rise, helping the aussie extend its latest recovery.

That said, monetary policy developments on their own may not be enough to save the risk-linked currency, which has been sensitive also to developments and expectations surrounding China, Australia’s main trading partner.

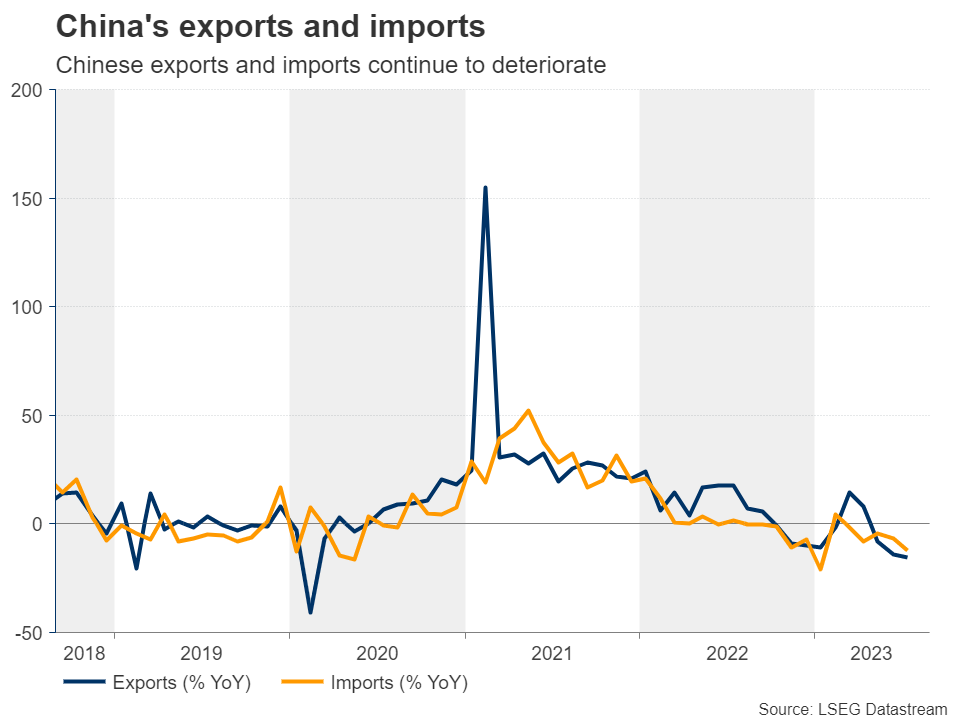

China has been in the spotlight lately, with data pointing to deepening economic wounds and responses by authorities not convincing market participants that they could have the desired effect. With that in mind, China’s trade data on Thursday, as well as the CPI and PPI numbers on Friday, could attract special attention. Further weakness in Chinese exports and imports, as well as another month of deflation could prompt traders to sell the aussie, which could erase any RBA decision-related gains.

Australia’s own trade data are also due to be released on Thursday, while the day before, the nation releases its GDP numbers for Q2.

BoC seen holding fire, guidance and jobs data in focus

Besides the aussie, another risk-linked currency will enter the limelight next week and that’s the loonie, with the Bank of Canada holding its own interest rate decision on Wednesday.

At the July gathering, this Bank decided to push the hike button, lifting interest rates by 25bps, but refrained from clearly telegraphing future moves. Officials just noted that they will continue to assess the dynamics and the outlook for inflation and that they remain committed to restoring price stability.

Inflation data for June revealed a notable slowdown in both headline and core terms, but the July numbers pointed to some stickiness, with the headline rate rebounding to 3.3% y/y from 2.8%, and the core one holding steady at 3.2%.

This may have prompted market participants to keep the option of another hike by the end of the year firmly on the table. Although they see only a 20% chance for action next week, they are assigning around a 50% probability for another 25bps hike by December.

Yes, inflation is above the Bank’s 2% objective, but with Canada’s core rate being closer to that number than underlying inflation rates in other major economies, and with the BoC maintaining a flexibility range around that target between 1-3%, officials may have the luxury to stay sidelined now and wait to see whether past hikes are still exerting downside pressure on prices.

That said, similarly to the RBA, closing the door to future hikes before the objective is met may be a premature choice. Thus, even if they stand pat, Canadian policymakers could keep alive the possibility of more action if deemed necessary. This will confirm the view of those assigning decent chances for another move in the coming months and thus, it may allow the loonie to gain some ground.

However, whether the currency could have a sustained and decent post-meeting recovery may largely depend on Friday’s employment report for August. The July numbers pointed to some weakness, with the economy losing some jobs and the unemployment rate rising further. Should next week’s data reveal deeper wounds, those expecting another BoC rate increase may start having second thoughts. For the probability of further action to keep rising and take the loonie higher, improving labor-market conditions may be required.

Weekly Focus – Risk Back On Amid Chinese Support

After a few volatile weeks, equity markets stabilised this week on the back of Chinese authorities cutting stamp duties on stock trades in half. The VIX volatility index was back at the lowest levels since early August. US job openings took a sharp decline in July and the jobs plentiful index declined indicating more people have a hard time finding a job. Consumer sentiment also took a turn for the worse, which all weighed on the dollar and took US yields lower.

European yields moved lower as well, fuelled by some small promising signs that core inflation is moving lower in the euro area. ECB pricing went a couple of basis points lower as this could be the first signs that the decline in activity we have seen so far in Q3 is feeding through to companies' price setting. Headline inflation was unchanged at 5.3%, though, which remains a big headwind to consumers.

July German retail sales confirmed service sector weakness with a 0.8% MoM decline, much worse than expected. Germans are being compensated for lost purchasing power, though, and wages increased at a record annual pace of 6.6% in Q2, giving a much-needed boost to consumers' spending power but also fuelling inflation concerns. The unemployment rate in the euro area did not budge in July and remained at 6.4%, a record low. Strong data for the labour market in Q3 is not much of a surprise, though. Labour markets should be the last to react to the slowdown in activity.

In Japan, the labour market surprisingly loosened somewhat in July with an increase in the unemployment rate to 2.7% from 2.5% in June. This looks like a bump on the road and does not change the fact that the Japanese labour market remains tight. Even so, it will probably only trigger an even more cautious Bank of Japan (BoJ) at the policy meeting later this month.

Elsewhere in Asia, Chinese data is watched closely by financial markets these days considering the recent weakness in the economy. Overall, both private and national PMIs were better than expected indicating the economy has not fallen completely out of the bed. Authorities came with a range of stimulating measures to the economy this week with a reduction of the required down payment for home-buyers as particularly important given the increasing risk stemming from the housing market.

Next week brings more important data from the euro area ahead of the ECB meeting with compensation per employee for Q2. We already saw negotiated wage growth spike, but the data next week is ECB's preferred measure of labour costs.

In China the most important event will be whether the developer Country Garden defaults. This might cause renewed stress in Chinese markets. We also get trade balance figures where weak exports have caught attention lately. In Japan, we will look out for July wage growth, which is important information ahead of the next BoJ meeting. In the US, we will look out for ISM services. Leading data indicates they will be on the weak side.

In Danske Bank we publish our Nordic Outlook on Tuesday with an update of our views on the Nordics and the global economy.

Week Ahead – RBA rate decision, Fed speak and BoE monetary policy hearing

US

The month started with a bang with the US jobs report but the following week is looking a little more subdued, starting with the bank holiday on Monday. Economic data is largely made up of revisions and tier-three releases. The exceptions being the ISM services PMI on Wednesday and jobless claims on Thursday. That said, revised productivity and unit labor costs on Thursday will also attract attention given the Fed’s obsession with input cost, wages in particular.

We’ll also hear from a variety of Fed policymakers including Susan Collins on Wednesday (Beige Book also released), Patrick Harker, John Williams, and Raphael Bostic on Thursday, and Bostic again on Friday.

Eurozone

Next week is littered with tier-three events despite the large number of releases in that time. Final inflation, GDP and PMIs, regional retail sales figures and surveys, and trade figures make up the bulk of next week’s reports. Not inconsequential, per se, but not typically big market events unless the PMI and CPI reports bring massive revisions. We will hear from some ECB policymakers earlier in the week which will probably be the highlight, including Christine Lagarde, Fabio Panetta, Philip Lane, and Isabel Schnabel.

UK

Next week offers very little on the data front but the Monetary Policy Report Hearing in front of the Treasury Select Committee on Wednesday is usually one to watch. While the committee’s views are typically quite polished by that point, the questioning is intense and can provide a more in-depth understanding of where the MPC stands on interest rates.

Russia

Inflation in Russia is on the rise again and is expected to hit 5.1% on an annual basis in August, up from 4.3% in July. That is why the CBR has started raising rates aggressively again – raised to 12% from 8.5% on 15 August. Even so, the ruble is not performing well and isn’t too far from the August highs just before the superhike. We’ll hear from Deputy Governor Zabotkin on Tuesday, a few days before the CPI release.

South Africa

Further signs of disinflation in the PPI figures on Thursday will have been welcomed by the SARB but they won’t yet be declaring the job done despite the substantial progress to date. The focus next week will be on GDP figures on Tuesday, with 0.2% quarterly growth expected, and 1.3% annual. The whole economy PMI will be released earlier the same day.

Turkey

CPI inflation figures will be eyed next week, with annual price growth seen hitting 55.9%, up from 47.8% in July. The CBRT is all too aware of the risks, hence the surprisingly large rate hike – from 17.5% to 25% – last month. The currency rebounded strongly after the decision but it has been drifting lower since, falling back near the pre-meeting levels. There’s more work to be done.

Switzerland

Another relatively quiet week for the Swiss, with GDP on Monday – seen posting a modest 0.1% quarterly growth – and unemployment on Thursday, which is expected to remain unchanged. Neither is likely to sway the SNB when it comes to its next meeting on 21 September, with markets now favoring no change and a 30% chance of a 25 basis point hike.

China

Two key data to focus on for the coming week; the non-government compiled Caixin Services PMI for August out on Tuesday which is expected at 54, almost unchanged from July’s reading of 54.1. If it turns out as expected, it will mark the eighth consecutive month of expansion in China’s services sector which indicates resilience despite the recent spate of deflationary pressures and contagion risk from the fallout of major indebted property developers that failed to make timely coupon payments on their respective bonds obligations.

Next up will be the balance of trade data for August on Thursday with export growth anticipated to decline at a slower pace of 10% y/y from -14.5% y/y recorded in July. Imports are expected to contract further by 11% y/y from -12.4% y/y in July.

Interestingly, several key leading economic data announced last week have indicated the recent doldrums in China will start to stabilize and potentially turn a corner. The NBS manufacturing PMI for August came in better than expected at 49.7 (consensus 49.4), and above July’s reading of 49.3 which makes it three consecutive months of improvement, albeit still in contraction.

In addition, two sub-components of August’s NBS manufacturing PMI; new orders and production are now in expansionary mode with both rising to hit their highest level since March 2023 at 50.2 and 51.9 respectively. Also, the Caixin manufacturing PMI for August has painted a more vibrant picture with a move back into expansion at 51 from 49.2 in July, and above the consensus of 49.3; its strongest pace of growth since February 2023.

Hence, it seems that the current piecemeal fiscal stimulus measures have started to trickle down positively into China’s economy.

India

The services PMI for August will be released on Tuesday where the consensus is expecting a slight dip in expansion to 61 from 62.3 in July, its highest growth in over 13 years. Capping off the week will be August’s bank loan growth out on Friday.

Australia

The all-important RBA monetary policy decision will be released on Tuesday. A third consecutive month of no change in the policy cash rate is expected, at 4.1%, as the recently released monthly CPI indicator has slowed to 4.9% y/y from 5.4% y/y, its slowest pace of increase since February 2022 and below consensus of 5.2% y/y.

Interestingly, the ASX 30-day interbank cash rate futures on the September 2023 contract have indicated a 14% chance of a 25-basis point cut on the cash rate to 3.85% for this coming Tuesday’s RBA meeting based on data as of 31 August 2023. That’s a slight increase in odds from a 12% chance of a 25-bps rate cut inferred a week ago.

On Wednesday, Q2 GDP growth will be out where consensus is expecting it to come in at 1.7% y/y, a growth slowdown from 2.3% y/y recorded in Q1.

To wrap up the week, the balance of trade for July will be out on Thursday where the consensus is expecting the trade surplus to narrow to A$10.5 billion from a three-month high of A$11.32 billion recorded in June.

New Zealand

Two data to watch, Q2 terms of trade on Monday and the global dairy trade price index on Tuesday.

Japan

A quiet week ahead with the preliminary leading economic index out on Thursday and the finalized Q2 GDP to be released on Friday. The preliminary figure indicated growth of 6% on an annualized basis that surpassed Q1’s GDP of 3.7% and consensus expectations of 3.1%; its steepest pace of increase since Q4 2020 and a third consecutive quarter of annualized economic expansion.

Singapore

Retail sales for July will be out on Tuesday with another month of lackluster growth expected at 0.9% y/y from 1.1% y/y in June; its softest growth since July 2021 as the Singapore economy grappled with a weak external environment. On a monthly basis, a slower pace of contraction is expected for July at -0.1% m/m versus -0.8% m/m in June.