Sample Category Title

Week Ahead – RBA rate decision, Fed speak and BoE monetary policy hearing

US

The month started with a bang with the US jobs report but the following week is looking a little more subdued, starting with the bank holiday on Monday. Economic data is largely made up of revisions and tier-three releases. The exceptions being the ISM services PMI on Wednesday and jobless claims on Thursday. That said, revised productivity and unit labor costs on Thursday will also attract attention given the Fed’s obsession with input cost, wages in particular.

We’ll also hear from a variety of Fed policymakers including Susan Collins on Wednesday (Beige Book also released), Patrick Harker, John Williams, and Raphael Bostic on Thursday, and Bostic again on Friday.

Eurozone

Next week is littered with tier-three events despite the large number of releases in that time. Final inflation, GDP and PMIs, regional retail sales figures and surveys, and trade figures make up the bulk of next week’s reports. Not inconsequential, per se, but not typically big market events unless the PMI and CPI reports bring massive revisions. We will hear from some ECB policymakers earlier in the week which will probably be the highlight, including Christine Lagarde, Fabio Panetta, Philip Lane, and Isabel Schnabel.

UK

Next week offers very little on the data front but the Monetary Policy Report Hearing in front of the Treasury Select Committee on Wednesday is usually one to watch. While the committee’s views are typically quite polished by that point, the questioning is intense and can provide a more in-depth understanding of where the MPC stands on interest rates.

Russia

Inflation in Russia is on the rise again and is expected to hit 5.1% on an annual basis in August, up from 4.3% in July. That is why the CBR has started raising rates aggressively again – raised to 12% from 8.5% on 15 August. Even so, the ruble is not performing well and isn’t too far from the August highs just before the superhike. We’ll hear from Deputy Governor Zabotkin on Tuesday, a few days before the CPI release.

South Africa

Further signs of disinflation in the PPI figures on Thursday will have been welcomed by the SARB but they won’t yet be declaring the job done despite the substantial progress to date. The focus next week will be on GDP figures on Tuesday, with 0.2% quarterly growth expected, and 1.3% annual. The whole economy PMI will be released earlier the same day.

Turkey

CPI inflation figures will be eyed next week, with annual price growth seen hitting 55.9%, up from 47.8% in July. The CBRT is all too aware of the risks, hence the surprisingly large rate hike – from 17.5% to 25% – last month. The currency rebounded strongly after the decision but it has been drifting lower since, falling back near the pre-meeting levels. There’s more work to be done.

Switzerland

Another relatively quiet week for the Swiss, with GDP on Monday – seen posting a modest 0.1% quarterly growth – and unemployment on Thursday, which is expected to remain unchanged. Neither is likely to sway the SNB when it comes to its next meeting on 21 September, with markets now favoring no change and a 30% chance of a 25 basis point hike.

China

Two key data to focus on for the coming week; the non-government compiled Caixin Services PMI for August out on Tuesday which is expected at 54, almost unchanged from July’s reading of 54.1. If it turns out as expected, it will mark the eighth consecutive month of expansion in China’s services sector which indicates resilience despite the recent spate of deflationary pressures and contagion risk from the fallout of major indebted property developers that failed to make timely coupon payments on their respective bonds obligations.

Next up will be the balance of trade data for August on Thursday with export growth anticipated to decline at a slower pace of 10% y/y from -14.5% y/y recorded in July. Imports are expected to contract further by 11% y/y from -12.4% y/y in July.

Interestingly, several key leading economic data announced last week have indicated the recent doldrums in China will start to stabilize and potentially turn a corner. The NBS manufacturing PMI for August came in better than expected at 49.7 (consensus 49.4), and above July’s reading of 49.3 which makes it three consecutive months of improvement, albeit still in contraction.

In addition, two sub-components of August’s NBS manufacturing PMI; new orders and production are now in expansionary mode with both rising to hit their highest level since March 2023 at 50.2 and 51.9 respectively. Also, the Caixin manufacturing PMI for August has painted a more vibrant picture with a move back into expansion at 51 from 49.2 in July, and above the consensus of 49.3; its strongest pace of growth since February 2023.

Hence, it seems that the current piecemeal fiscal stimulus measures have started to trickle down positively into China’s economy.

India

The services PMI for August will be released on Tuesday where the consensus is expecting a slight dip in expansion to 61 from 62.3 in July, its highest growth in over 13 years. Capping off the week will be August’s bank loan growth out on Friday.

Australia

The all-important RBA monetary policy decision will be released on Tuesday. A third consecutive month of no change in the policy cash rate is expected, at 4.1%, as the recently released monthly CPI indicator has slowed to 4.9% y/y from 5.4% y/y, its slowest pace of increase since February 2022 and below consensus of 5.2% y/y.

Interestingly, the ASX 30-day interbank cash rate futures on the September 2023 contract have indicated a 14% chance of a 25-basis point cut on the cash rate to 3.85% for this coming Tuesday’s RBA meeting based on data as of 31 August 2023. That’s a slight increase in odds from a 12% chance of a 25-bps rate cut inferred a week ago.

On Wednesday, Q2 GDP growth will be out where consensus is expecting it to come in at 1.7% y/y, a growth slowdown from 2.3% y/y recorded in Q1.

To wrap up the week, the balance of trade for July will be out on Thursday where the consensus is expecting the trade surplus to narrow to A$10.5 billion from a three-month high of A$11.32 billion recorded in June.

New Zealand

Two data to watch, Q2 terms of trade on Monday and the global dairy trade price index on Tuesday.

Japan

A quiet week ahead with the preliminary leading economic index out on Thursday and the finalized Q2 GDP to be released on Friday. The preliminary figure indicated growth of 6% on an annualized basis that surpassed Q1’s GDP of 3.7% and consensus expectations of 3.1%; its steepest pace of increase since Q4 2020 and a third consecutive quarter of annualized economic expansion.

Singapore

Retail sales for July will be out on Tuesday with another month of lackluster growth expected at 0.9% y/y from 1.1% y/y in June; its softest growth since July 2021 as the Singapore economy grappled with a weak external environment. On a monthly basis, a slower pace of contraction is expected for July at -0.1% m/m versus -0.8% m/m in June.

Sunset Market Commentary

Markets

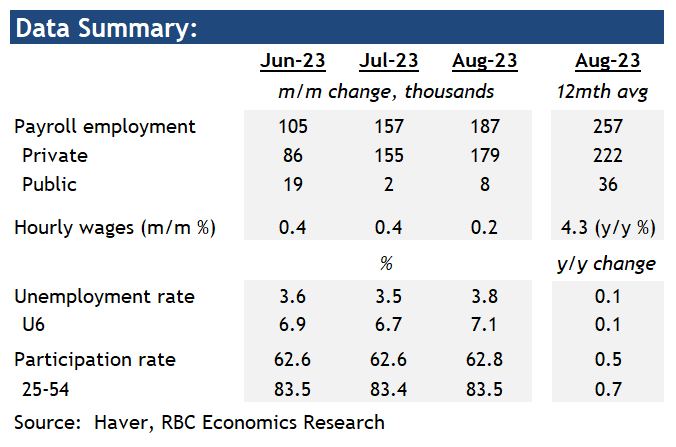

Markets barely budged in the run up to today’s widely anticipated payrolls so we’ll jump straight to it. Job growth amounted to 187k in August. The small consensus beat (170k) fades to nothing when taking into account a net 110k downward revision for the past two months. The unemployment rate unexpectedly jumped 0.3 ppts to 3.8% but a jump in the participation rate from 62.6% to 62.8% as more Americans explore the labour market helps explain the uptick. It’s the highest level since the pandemic erupted in February 2020. Average hourly earnings growth cooled a little more than expected on a monthly basis, from 0.4% to 0.2%, bringing the yearly figure further down to 4.3% (vs 4.4% in July). It’s a decent report, yet one that shows the labour market is moving from extremely tight towards a more balanced one. After the string of other disappointing US data earlier this week (including JOLTS & consumer confidence) it strengthens the markets’ case for Fed tightening effectively having come to an end. The US manufacturing ISM is still due after wrapping up this report though. Money markets yesterday were evenly split whether one more hike will follow or not. The balance today tilts towards a just one in three chance for a final 25 bps move. They also stop short of fully pricing in two full rate cuts as soon as May 2024. The short end of the US yield curve clearly outperforms even though it has left the intraday lows behind. The 2-y yield eases 3 bps. Yields on longer maturities are much more muted. The 10-y yield briefly dipped 5 bps in the wake of the report before paring losses again and even gaining a few bps. In some parts of the curve the inversion disappears for the time being (eg. 30y-5y). German yields followed a similar steepening trend with the 2-y yield first easing a few bps before trading flat on the day and the 30-y yield adding 7 bps on a daily basis.

The dollar is only marginally weaker for the day. DXY falls towards 103.44 but steers clear from the lows seen earlier this week. EUR/USD ran higher but it could have been more given the initial yield differences. The pair is trading around 1.087. USD/JPY is testing minor support around 145. The Canadian loonie underperforms G10 peers after the northern economy unexpectedly contracted in Q2 (-0.2% q/q vs +1.2% expectations).

News & Views

The Czech Finance Ministry published its proposal for the 2024 State Budget. The proposal assumes a budget deficit of CZK 252 bln. Both revenues (CZK 1921.2 bln from 1927.9 bln, -0.3%) and expenditures (CZK 2173.2 bln from 2222.9 bln, -2.2%) are expected to decline. Earlier in the budget process, the Ministry of Finance aimed for a budget deficit of CZK 235 bln. The government for this year the Czech budget assumes a deficit of CZK 295.0 bln. The draft proposes spending cuts in regional development, in the Health Ministry and in the Industry and trade Ministry. Expenses in defense are expected to increase to meet defense spending legislation (2.0% of GDP). The composition of the budget items still might be changed due to debate within the government, but the Finance Ministry indicated that the deficit as such shouldn’t be changed anymore. The budget will be submitted to Parliament by the end of September. Other data today showed that Czech manufacturing PMI tentatively bottoming from 41.1 in July to 42.9 (40.8 bottom in June) still 15th consecutive month contraction. The krona today weakened slightly to EURCZK 24.12.

Swiss August inflation data published this morning showed somewhat of a mixed picture as markets are counting down to the September 21 SNB policy meeting. Headline inflation rose 0.2% M/M (-0.1% in July) keeping the Y/Y measure unchanged at 1.6% (vs 1.5% expected). According to the Swiss Statistical office, the “0.2% increase compared with the previous month is due to several factors including rising prices for fuels and heating oil. Housing rentals and fees for securities accounts also recorded a price increase. In contrast, the hire of private means of transport decreased as well as prices for air transport and international package holidays”. In its June forecast, the SNB expected inflation to decline to 1.7% in Q3, but to regain some ground later this year and next year. At that time the SNB kept the door open for further tightening. Money markets currently see a chance of less than 50% for the SNB to hike rates again in September. After topping out recently, the franc gained marginally to today (EUR/CHF 0.9570).

US Unemployment Rate Higher in August

Job growth in the U.S. remained firm in August at 187k, following downwardly revised 157k and 105k increases in July and June.

The majority of employment growth was again accounted for by services sectors. Health care and leisure and hospitality added the most jobs, by 71k and 40k, respectively in August. Transportation and warehousing continued to show weakness, losing 34k jobs in August. That was also the 5th decline out of 8 months this year.

Separately released household survey showed the unemployment rate rising higher to 3.8% in August from 3.5% in July. The increase was mostly driven by a rise in the participation rate not being offset by higher employment. Labour force participation rate rose to 62.8% in August.

Other indicators have continued to point to slowing labour demand. Job openings in July dropped to the lowest level in almost two and a half years. Quits rates in the U.S. also continued to decline, suggesting that tight labour market conditions are continuing to unwind.

Wage growth is persisting at higher levels, but the 0.2% increase in average hourly earnings in August was relatively small and the year-over-year rate of growth ticked down to 4.3% from 4.4% in July.

Bottom line: The employment growth in August is still historically strong and the increase in the unemployment rate could still be partially reversed in coming months. But signs of flagging labour demand elsewhere mean we can expect conditions to continue to cool. That outlook, together with easing inflation trends should be enough to keep Fed on a “hopeful” pause. We expect the Fed Funds to be held at current range (5.25% - 5.5%) throughout the remainder of 2023.

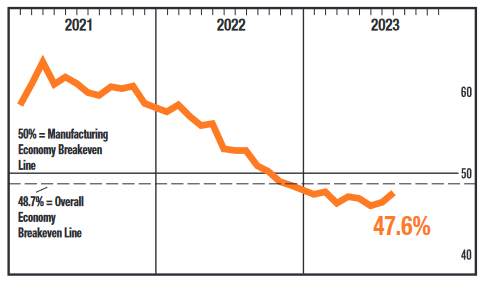

US ISM manufacturing rose to 47.6, corresponds to -0.4% annualized GDP contraction

US ISM Manufacturing PMI rose from 46.4 to 47.6 in August. New orders dropped from 47.3 to 46.8. Production rose from 48.3 to 50.0. Employment rose from 44.4 to 48.5. Prices rose from 42.6 to 48.4.

ISM said: "This is the 10th month of contraction and continuation of a downward trend that began in June 2022. That trend is reflected in the Manufacturing PMI's 12-month average falling to 47.8 percent. Of the five subindexes that directly factor into the Manufacturing PMI, none are in growth territory."

"The past relationship between the Manufacturing PMI and the overall economy indicates that the August reading (47.6 percent) corresponds to a change of minus-0.4 percent in real gross domestic product (GDP) on an annualized basis."

Canada’s GDP Stalls in Second Quarter of 2023

The Canadian economy contracted by 0.2% quarter/quarter annualized (q/q) in 2023 Q2. Furthermore, the flash estimate for July was essentially unchanged. Stripping out external factors, final domestic demand came in at 1% q/q, right on our expectation for positive, but still below trend growth.

Housing was once again a big drag on the economy, down 8.2% q/q. New construction and a lack of renovation activity weighed on the sector, as high interest rates continue to curb activity. While there was a bounce back in real estate transactions during the spring, this wasn't enough to provide an offset.

Canadian consumer spending slowed to 0.2% q/q, from 4.75% q/q in Q1 (also revised lower). Spending on goods increased by 0.6% q/q, as expenditures on new trucks, vans and sport utility vehicles rose enough to offset declines in new passenger cars, furniture, and major durables for outdoor recreation. Spending on services didn't grow at all as Canadians held back on spending abroad and going out to bars.

Trade was also a drag as imports (+1.9% q/q) rose more than exports (0.4% q/q). Imports rose on the back of "unwrought gold, silver and platinum group metals and their alloys, passenger cars and light trucks and aircraft", while exports were slowed by declines in "crude oil and bitumen, wheat and canola".

The incomes of Canadians also rose, as employee compensation surged 9.1% q/q. This caused the savings rate to rise to 5.1%, from 3.7% in the first quarter.

Key Implications

So much for that overheating economy. While Canada's economy was widely expected to slow in the second quarter of 2023, today's report came well under expectations. Various special factors contributed to this, including the multiple worker strike actions and rampant wildfires, which shut down oil & gas production in May and limited consumer activity in June. While federal government transfers in July may result in a short-term boost in the third quarter, we believe Canada has entered a stage of below trend economic growth. This should continue through the rest of this year, as the impact of high interest rates work through the economy to prevent another acceleration in demand.

When the Bank of Canada decided to raise rates in June and July, it did so largely because consumer momentum was so strong in the first quarter of 2023. But with today's weak report and with employment growth decelerating to a 12k pace (three-month average), from 80k in the first quarter, consumer demand should continue to act as a weight on growth. This cooling off is exactly what the BoC wants to see in order to be confident that inflation will keep pushing towards the 2% target. We think it will continue, justifying our call for the BoC to remain on the sidelines for the rest of this year. Markets are taking this cue with the Canada 2-year and 10-year yields falling this morning, and down by approximately 30 basis points over the last two weeks.

Fed Could Not Have Hoped for a Better Week of US Jobs Data

If you're a Federal Reserve official, you'll find it hard not to be very pleased with the way this week's gone from a labor market data perspective.

The JOLTS release at the start of the week was extremely encouraging as it continued a clear trend that brought the number of vacancies back to levels not seen in two years and not far from the pre-pandemic norm. Even without today's report, that will have come as a huge relief for the Fed.

When you consider today's report on top of that, the week couldn't have gone much better. The headline NFP may have been a little stronger than expected but it's still below 200,000 and the beat was more than offset by last month's revision.

Then there's average hourly earnings which fell back to 0.2%, a level far more consistent with the Fed's goal if it can be repeated and again, below market expectations. The cherry on the cake is the participation beat and jump in unemployment, both of which point to more slack appearing in the labor market.

To be clear, the Fed won't get carried away with today's report. It's just one that needs to be repeated on a number of occasions but there's plenty of cause for optimism in there. If there was any doubt that the Fed will pause in September, today's report surely puts an end to that debate.

Gold pares gains but continues to push against resistance

Despite all of this, the reaction to the report has arguably been relatively mild. The dollar is lower but has pared much of the earlier declines, as have US yields. Gold initially broke above $1,950 - a level it's struggled around in recent days - but is now hovering a little below.

Obviously, we should always wait for the dust to settle on this before making a judgment and it will be very interesting to see how the final hours of the week now play out. But on the face of it, this week's labor market figures don't appear to have done gold any harm after what has been a rough few months for the yellow metal.

Oil buoyed by US jobs data to near 2023 highs

Oil prices have seemingly responded positively to the labor market figures, perhaps as they signal interest rates may not rise any further and even fall sooner which is better for the economic prospects of the economy over the medium term. They'd already been on a good run though and Brent is now trading around its highest level this year, with no shortage of momentum.

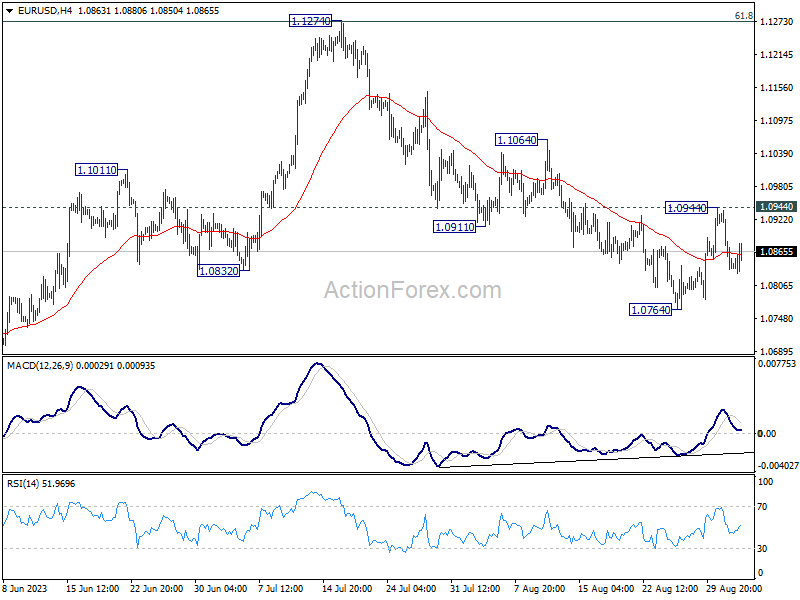

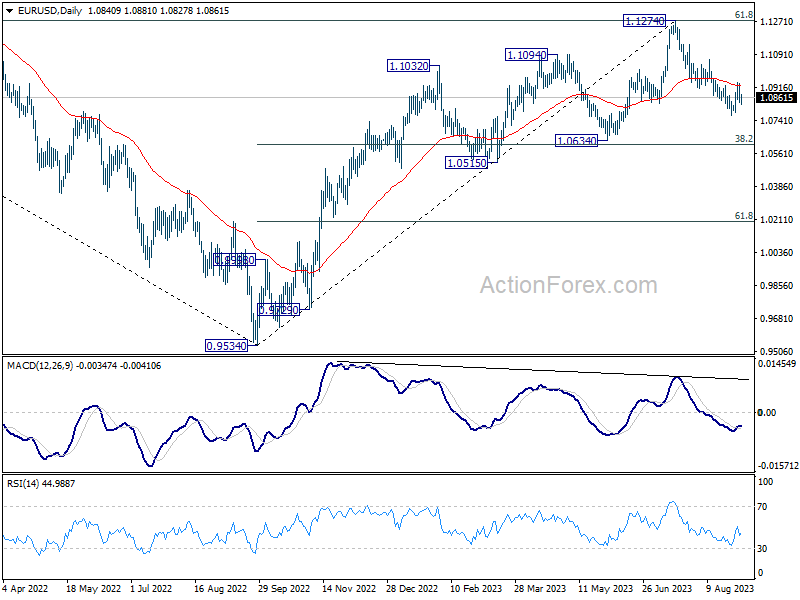

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0806; (P) 1.0873; (R1) 1.0910; More...

Intraday bias in EUR/USD is turned neutral first with current recovery. On the downside, firm break of 1.0764 will resume whole decline from 1.1274 to 1.0609/34 cluster support next. On the upside, however, break of 1.0944 resistance will argue that the corrective fall from 1.1274 has completed with three waves down to 1.0764. Further rally would then be seen to 1.1064 resistance for confirmation.

In the bigger picture, fall from 1.1274 medium term top is seen as a correction to up trend from 0.9534 (2022 low). Deeper decline would be seen to 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609). Strong support could be seen there, at least on first attempt, to bring rebound. Yet, medium term outlook will be neutral for now, as long as 1.1274 resistance holds.

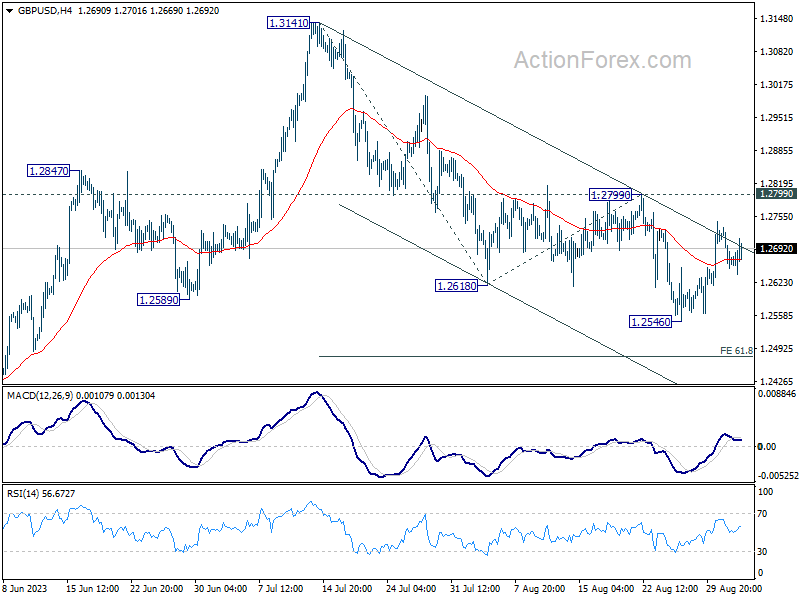

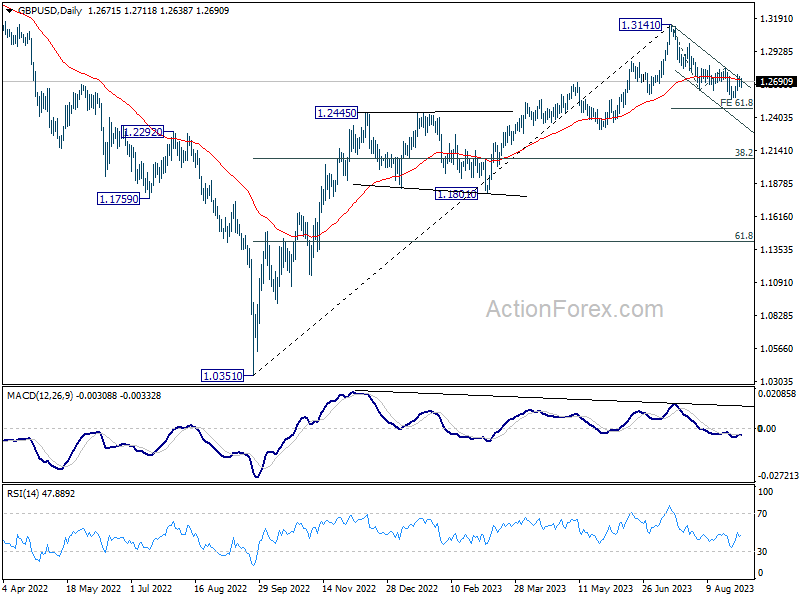

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2639; (P) 1.2687; (R1) 1.2720; More...

Intraday bias in GBP/USD stays neutral as range trading continues. On the downside, break of 1.2546 will resume whole fall from 1.3141 to 61.8% projection of 1.3141 to 1.2618 from 1.2799 at 1.2476. However, on the upside, firm break of 1.2799 will indicate that the correction from 1.3141 has completed with three waves down to 1.2546. Intraday bias will be turned back to the upside for retesting 1.3141.

In the bigger picture, for now, fall from 1.3141 medium term top is seen as a correction to up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3141 at 1.2075. Strong support would be seen there to bring rebound on first attempt. But outlook will be neutral at best as long as 1.3141 resistance holds, and consolidation from there is set to extend, until further development.

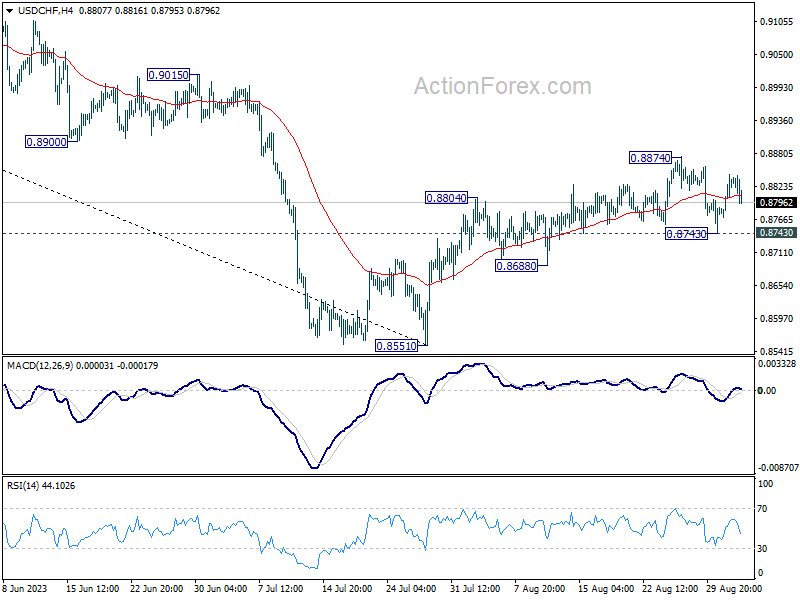

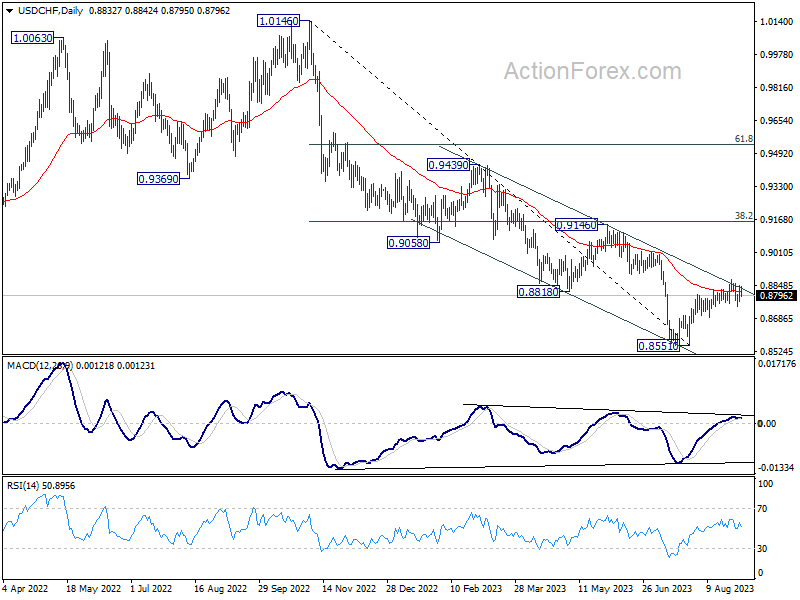

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8752; (P) 0.8778; (R1) 0.8811; More....

Intraday bias in USD/CHF remains neutral at this point, as it's still bounded in range of 0.8743/8874. On the upside, firm break of 0.8874 will resume the rise from 0.8551. Next target is 0.9146 cluster resistance. On the downside, though, break of 0.8743 minor support will argue that rebound from 0.8551 has completed, and bring retest of this low.

In the bigger picture, rebound from 0.8551 medium term bottom is currently seen as a correction to the downtrend from 1.0146 (2022 high). Further rally would be seen to 0.9146 cluster resistance (38.2% retracement of 1.0146 to 0.8551 at 0.9160). Strong resistance could be seen there to limit upside, at least on first attempt. Nevertheless, medium term outlook is neutral at best as long as 0.8551 holds, until further developments.

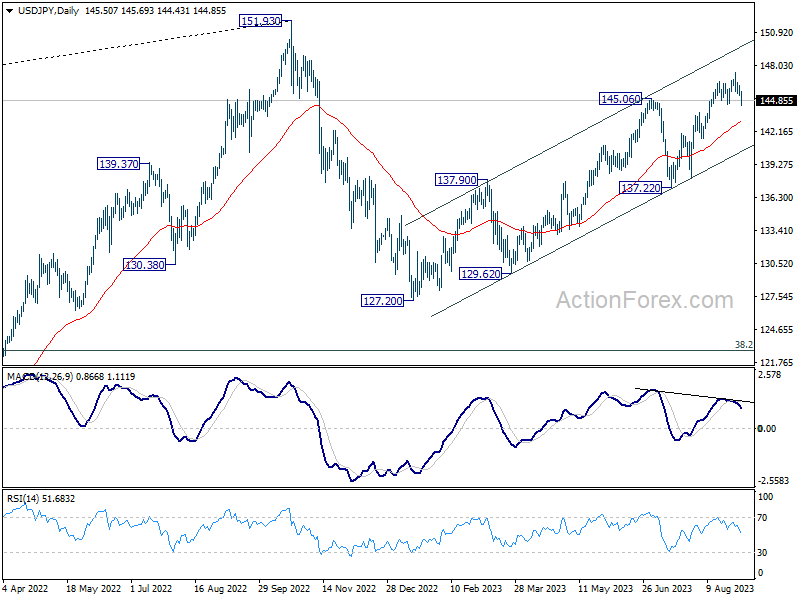

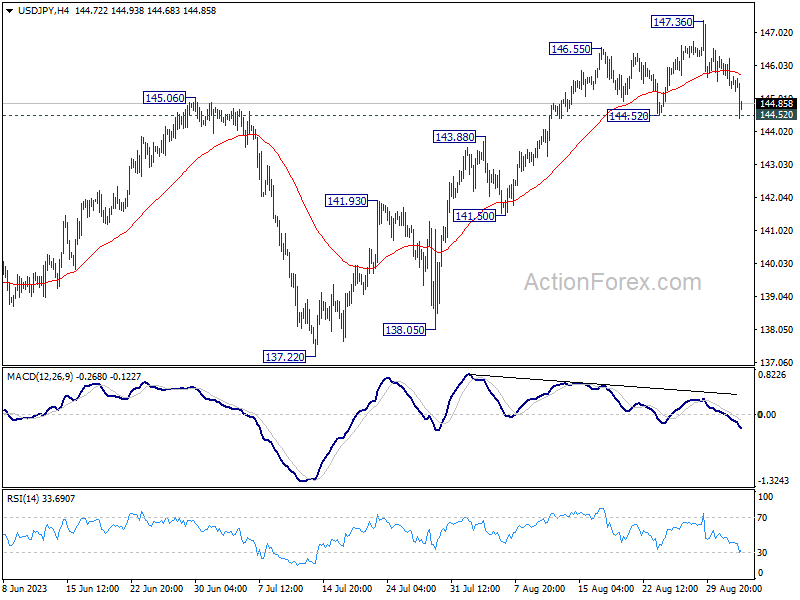

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 145.17; (P) 145.72; (R1) 146.10; More...

USD/JPY falls notably in early US session but it's still trying to defend 144.52 support. Intraday bias stays neutral first. Strong rebound from current level, follow by break of 147.36, will resume the rise from 127.20 to retest 151.93 high. On the downside, however, firm break of 144.52 should confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 143.04) and possibly below.

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Rise from 127.20 is seen as the second leg of the pattern and could still be in progress. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.