Sample Category Title

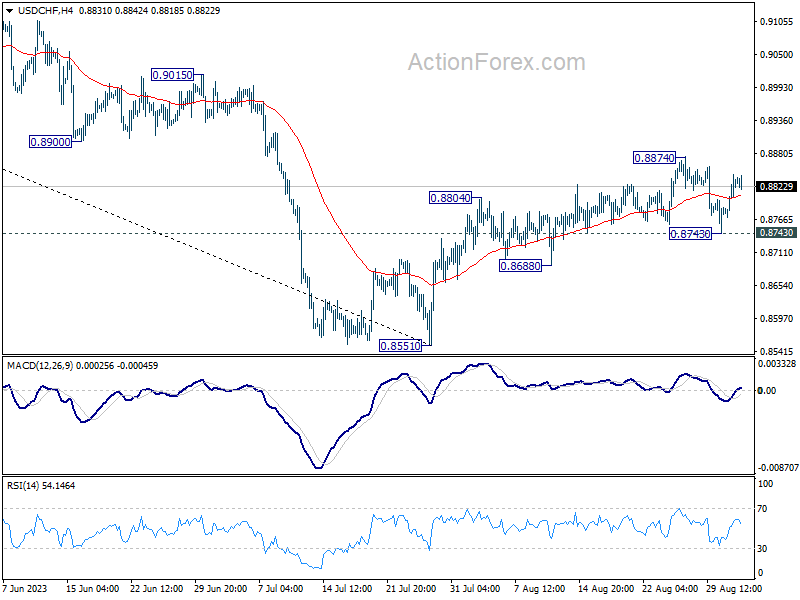

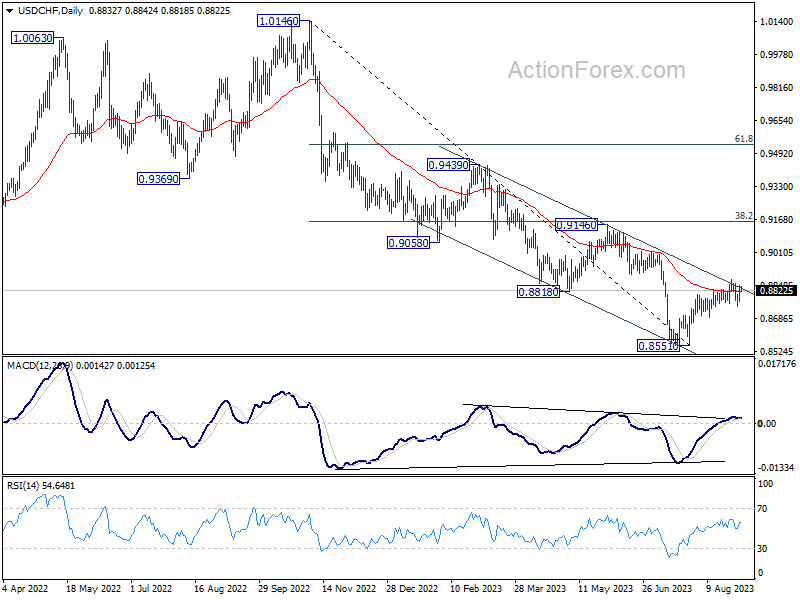

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8752; (P) 0.8778; (R1) 0.8811; More....

Range trading continues in USD/CHF and intraday bias stays neutral at this point. On the upside, firm break of 0.8874 will resume the rise from 0.8551. Next target is 0.9146 cluster resistance. On the downside, though, break of 0.8743 minor support will argue that rebound from 0.8551 has completed, and bring retest of this low.

In the bigger picture, rebound from 0.8551 medium term bottom is currently seen as a correction to the downtrend from 1.0146 (2022 high). Further rally would be seen to 0.9146 cluster resistance (38.2% retracement of 1.0146 to 0.8551 at 0.9160). Strong resistance could be seen there to limit upside, at least on first attempt. Nevertheless, medium term outlook is neutral at best as long as 0.8551 holds, until further developments.

Except in Case of Unexpectedly Weak US data, Dollar Again Might Be Better Protected

Markets

(ECB) speak rather than data was the most important driver for trading yesterday, especially on European markets. ECB’s Schnabel, seen as belonging to the hawkish camp within the ECB, in speech gave quite some weight to recent slowdown in growth. She admitted that underlying price pressures remained too high, but stopped short of making an outright call for an additional ECB interest rate hike at the September 14 meeting. Markets considered it as an indication that chances on a pause in the ECB hiking cycle are growing. In a data-dependent approach, this at least wasn’t conformed by the EMU August inflation print. In line with national data, EMU headline inflation at 0.6% M/M and 5.3% Y/Y (unchanged from July) printed higher than expected. Core inflation eased from 5.5% to 5.3%. In this respect, ECB’s De Guindos also took notice of slower growth, but didn’t expect a big change to the ECB’s inflation forecast. Similar conclusion: the debate on whether to pause or to hike is wide open. As was often the case of late, the market reaction erred to a dovish interpretation. German yields dropped from the open and this trend continued throughout the session, closing between 9.6 bps (5-y) and 5.8 bps (30-y) lower. Contrary to what was the case earlier this week, US data yesterday didn’t leave any room for a dovish interpretation. Weekly jobless claims printed at a lower than expected 228k. July spending data were strong (0.8%) and the PCE deflators printed as expected (core 0.2% M/M; 4.2% Y/Y up from 4.1%). The Chicago PMI expectedly improved from 42.8 to 48.7. Yields still declined between 2.3 bps (2-y) and 0.6 bp (10-y). In this respect, we also keep an eye at oil continuing its recent rebound ($ 87 p/b cf infra). Lower yields this time didn’t really help equities (S&P -0.16%, EuroStoxx -0.42%). Lower EMU yields also caused EUR/USD to (more than) reverse Wednesday’s rebound (close 1.0843 from 1.0923). DXY rebounded to the 103.60 area. However, a modest decline in USD/JPY (145.54 from 146.24) indicated it was mainly euro weakness rather than any big improvement USD momentum. Global euro weakness also pushed the EUR/GBP cross rate further away from the 0.861 area tested earlier this week.

This morning, Asian equites modestly trade with modest gains (Nikkei +0.42%) , supported by further measure from Chinese authorities to support growth and a better than expected Caixin Manufacturing PMI (see infra).

Later today, the focus is on the US payrolls report. US job growth in August is expected to slow down further to 170k from 187K. The unemployment rate is seen unchanged at 3.5%. AHE are expected at to ease slightly further to 0.3% M/M and 4.3% Y/Y. We don’t have a strong arguments to deviate from the consensus. However, the bar for the payrolls isn’t that high and after this week’s repositioning quite some dovishness probably is already discounted. Markets only see a <15% chance of a September Fed rate hike. So, the downside in yields might be better protected. In this respect also keep an eye at the US manufacturing ISM. A minor improvement (47.0) is expected. We don’t expect the report to really be a game-changer, but a positive surprise might temper the recent dovish market bias. Except in case of unexpectedly weak US data, the dollar again might be better protected. In EUR/USD the attempt to break above the downtrend channel top since mid-July is rejected. The 1.0766 correction low is first support. Also keep in mind that US markets are closed for Labour Day on Monday.

News and views

The People Bank of China (PBOC) announced that financial institutions will need to hold 4% of their FX deposits in reserve instead of 6% starting September 15. The FX reserve requirement cut is one of many measures announced this week to prop up the economy (and support the currency). Others include a reduction in down payments for mortgages, higher personal income tax deductions related to care and education and lowered stamp duty for stock trading were the others. The Chinese Caixin manufacturing PMI this morning showed an unexpected increase from 49.2 to 51. The private survey adds to signs that the manufacturing slump could ease after similar signs from the official PMI yesterday (49.7 from 49.3). The Chinese yuan this morning tried to build on yesterday’s gain, with USD/CNY temporary below 7.25. The move didn’t last though (7.2650). Asian stock markets are paring early profits as well.

Brent crude oil prices yesterday closed in on their early August/YTD top above $87/b. Russian deputy PM Novak said that Russia and OPEC+ partners agreed on further export cuts with details to be released next week. Earlier on the day, a bigger than expected drop in US inventories already pointed to tightness on the crude market.

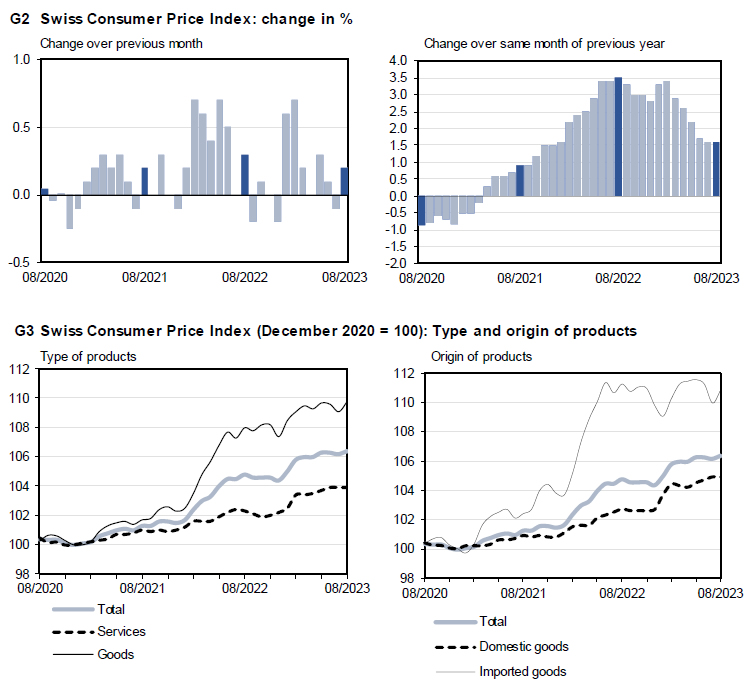

Swiss CPI up 0.2% mom in Aug, unchanged at 1.6% yoy

Swiss CPI rose 0.2% mom in August, matched expectations. Core CPI (excluding fresh and seasonal products, energy and fuel) rose 0.1% mom. Domestic products prices was flat 0.0% mom. Import products prices rose 0.8% mom.

Compared with the same month a year ago, CPI was unchanged at 1.6% yoy, above expectation of 1.5% yoy. Core CPI slowed from 1.7% yoy to 1.5% yoy. Domestic products prices slowed from 2.3% yoy to 2.2% yoy. Imported products prices rose from -0.6% yoy to -0.3% yoy.

GBPJPY Should Extend Lower in Zigzag Correction

Short Term Elliott Wave view in GBPJPY suggests the rally to 186.75 ended wave 1. Pullback in wave 2 is currently in progress as a zigzag Elliott Wave structure. Down from wave 1, wave (i) ended at 185.38 and wave (ii) rally ended at 185.94. The pair extended lower in wave (iii) towards 183.35 and wave (iv) ended at 184.78. Final leg wave (v) ended at 183.34 which completed wave ((a)). Pair then corrected in wave ((b)) as another zigzag in lesser degree. Up from wave ((a)), wave (a) ended at 185.26 and pullback in wave (b) ended at 184.056. Wave (c) higher ended at 186.06 which completed wave ((b)).

Pair then resumed lower in wave ((c)) with subdivision as an impulse. Down from wave ((b)), wave (i) is expected to complete soon. Pair should then rally in wave (ii) to correct the decline from wave ((b)) high at 186.06 before turning lower again in wave (iii). Potential target lower is 100% – 161.8% Fibonacci extension of wave ((a)). The area comes at 180.5 – 182.6 where buyers can appear for at least a 3 waves rally. Near term, as far as pivot at 186.75 high stays intact, expect rally to fail and pair to extend lower.

GBPJPY 60 Minutes Elliott Wave Chart

GBPJPY Elliott Wave ChartGBPJPY Elliott Wave Video

https://www.youtube.com/watch?v=U8pa1dL-66o

Jobs Day

August ended on a downbeat note for the S&P500 and on an upbeat note for the US dollar as, even though the Federal Reserve’s (Fed) favourite gauge of inflation, PCE, came in line with expectations in July for both the core and headline figures – and even though the core PCE posted the smallest back-to-back rise since late 2020, the supercore services inflation – very closely watched by Mr. Powell and team, and that excludes not only energy but also housing, rose by the most on a monthly basis since the year began. Plus, personal spending remained strong – in line with the GDP data released earlier this week.

Digging deeper, the personal income fell slightly, meaning that Americans continue to tap into the reserves to continue spending. But the good news for the Fed is that the consumer spending at this speed could continue as long as the savings are available. And according to the latest data, personal savings in the US fell from 4.3% in June to 3.5% in May. Before the pandemic, the savings level was close to 9%. In conclusion, savings are melting, housing affordability is falling, mortgage rates are up, low-income Americans reportedly fall behind their important payments like rent, and the main street gives away signs of suffering. But the GDP remains above 2%, above the long-term trend which is thought by the Fed to be around 1.8%, and the scenario of soft landing is what the market is pricing convincedly.

Jobs day

The US jobs data shows signs of loosening but the numbers are still at historically strong levels. Due to be released later today, the US unemployment rate is expected to remain at a multi-decade low of 3.5%, and the US economy is expected to have added around 170K new nonfarm jobs in August. In the last twelve months, the US economy added almost 280K jobs on average. If today’s data comes in line with expectations, the last 12-month average will still remain close to 270K monthly job additions on average. Historically, we expect NFP to fall to around 50K per month a few months into recession. So, to tell you that: we are not there just yet.

Today, a softer than expected NFP figure, a slight deterioration in the unemployment rate, or softer-than-expected wages data could further cement the idea that the Fed will skip a pause at the September meeting, and maybe at the November as well. So far, the US Treasuries have had their best week since mid-July. The US 2-year yield retreated to 4.85%, while the 10-year yield flirted with the 4% mark for the first time in three weeks. But who says a rapid jump, also says a rising possibility of a correction. One thing is sure, we don’t expect any major central banker to call victory on inflation just yet…

European inflation sticks around 5.3% due to rising energy

Latest CPI estimate showed that Eurozone inflation stagnated at 5.3% in August due to the sticky energy costs, versus a fall to 5.1% expected by analysts. Inflation in France for example accelerated at a much faster pace than expected in August, while the latest PMI numbers showed weakness in activity. German retail sales also fell faster than expected in July, whereas inflation in Germany also ticked higher last month. The combination of weak economic data and sticky inflation is a nightmare scenario for the European Central Bank (ECB). The ECB should raise the rates to continue fighting inflation, even though the underlying economies are under pressure. Today, the final PMI figures will likely confirm the ongoing slowdown. The EURUSD gave back most of its weekly advance after yesterday’s inflation data, hinting that the market is worried that further ECB hikes will further damage economic activity. The bears are tempted to retest the 200-DMA support. If they are successful, the next natural bearish target stands at a distant 1.0615, the major 38.2% Fibonacci retracement on past year’s rally, which should distinguish between the continuation of the actual positive trend and a bearish medium term reversal.

More stimulus from China

This week’s PMI data showed that the Chinese manufacturing contracted at a slower pace, and today’s Caixin PMI showed that it stepped into the expansion zone in August, whereas the Chinese services PMI fell short of expectations and the wave of further bad news, like Country Garden announcing an almost $7bn loss in H1, talk of the company’s yuan denominated bond default, Moody’s downgrading of the firm to Ca and Evergrande’s wealth unit saying that it couldn’t make payments on its investment products due to a cash crunch, combined to the existing and worsening property crisis get the People’s Bank of China (PBoC) to announce lower payment requirements for first and second-time house buyers, and to encourage lower rates on existing mortgages. But it won’t improve the situation overnight. The CSI 300 is closing a week PACKED with fresh stimuli on a meagre note.

Crude rallies

The barrel of American crude jumped more than 2% yesterday and is consolidating above the $84pb level. The next bullish targets stand at $85pb, the August peak, and $89pb, in the continuation of an ABCD pattern. But the rally can’t extend above $90 without reviving global inflation expectations and recession worries, which would then start playing against the bulls.

China Steps Up Stimulus

Market movers today

It is non-farm payroll day and markets are geared up for a soft number after disappointing labour market data this week from JOLTS, ADP and the consumer confidence survey. We look for a rise in payrolls of 160k, slightly below consensus of 170k. Also keep an eye on hourly earnings, which were a bit high in July at 0.4% m/m.

In addition, we get US ISM manufacturing, which has been moving sideways at a low level in the past months. Recent manufacturing data such as US and euro PMI manufacturing has been weak, so markets are prepared for a soft reading.

In the Scandies, we get PMI manufacturing in both Norway and Sweden.

The 60 second overview

This morning, China announced a 200bp cut to financial institutions' foreign exchange reserve requirements (from 6 to 4%) with an aim to increase USD liquidity and stabilise renminbi. The move comes after the PBOC yesterday released a statement saying nationwide minimum down payments would be uniformly set at 20% for first-time home buyers, and at 30% for second-time buyers. The statement also encouraged local banks to cut down rates on existing mortgages and deposits. This latest spree of stimulus comes after yesterday's data showed that the value of new home sales by China's 100 largest real estate companies fell 34% compared to a year earlier.

Yesterday, euro area headline inflation came in unchanged compared to last month at 5.3%. Core inflation fell 0.2pp to 5.3%. Also, service inflation edged slightly lower to 5.5% (-0.15pp), which is an important step for ECB to eventually end its hiking cycle. The overall take is that the disinflationary process is underway, but in our view, it is still not enough for ECB to be confident to the timely return to the 2% target. We keep our call for one more hike in September.

Oil prices have climbed this week in the anticipation of production cuts. Yesterday, Russia's deputy prime minister said the country has agreed with OPEC+ countries to reduce exports.

Equities: After a strong week, equities took a breather on Thursday. Macro should not be blamed though, but wait-and-see mode ahead of the US job report today. Equities were lower, with both Stoxx 600 and S&P 500 down -0.2% and Nordics -0.8%. It was not a risk-off session though. Defensives underperformed (utilities and health care) while large cap growth cyclicals rose, most notably in the US but also in the Nordics with EQT and NIBE outperforming. US futures are higher this morning while many Asian markets are closed due to weather conditions.

FI: A strong rally dominated the trading session yesterday from the sub 5y point as markets repriced the expectations of an ECB rate hike at the September meeting. This took the sub 5y point almost 10bp lower on the day. This happened amid headline inflation beating expectations (which country releases earlier had suggested) and staying unchanged from July at 5.3%. Core inflation declined 0.2pp, but still printed at elevated levels at 5.3%. The key takeaway from the August inflation release is that disinflationary forces are underway but the question remains of the pace of decline, which means that the August inflation, report has something for both the doves and the hawks in the Governing Council. Also, moderately hawkish minutes and Schnabel's speech on inflation did not lead to higher yields.

FX: Yesterday's session was primarily characterised by a drop in EUR/USD below the 1.09 mark and a slight outperformance of the commodity FX sphere amid a rise in commodity prices incl. energy.

Credit: Primary activity in the credit market remained high yesterday albeit lower than the red hot market seen at the beginning of the week. Secondary activity stayed muted with iTraxx Main 1bp wider at 70bp while iTraxx Xover was 4bp wider at 396bp.

Nordic macro: The Norwegian unemployment rate has been stable at 1.8% since Easter, but the total number of people out of work - including those on job creation schemes and the partially unemployed - increased by almost 3,000 in July. Job growth also seems to have levelled off somewhat, so we think the unemployment rate may well rise to a seasonally adjusted 1.9% in August.

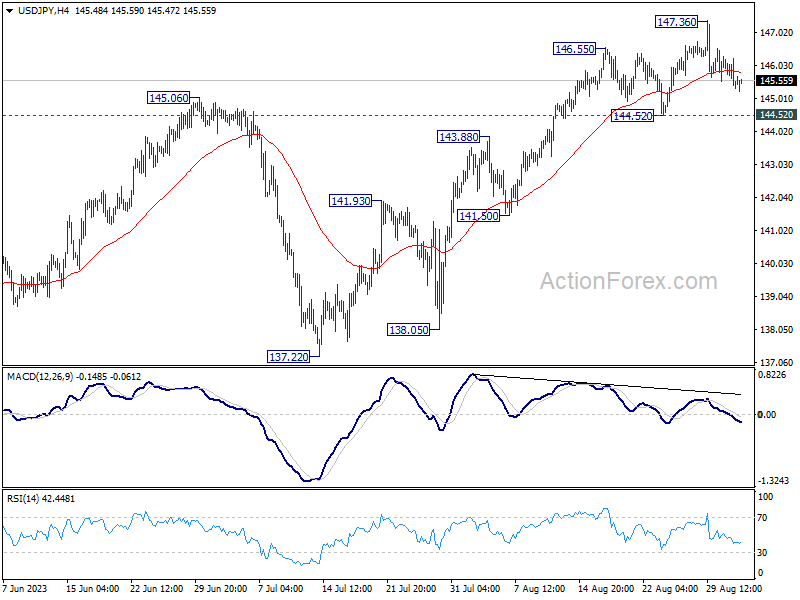

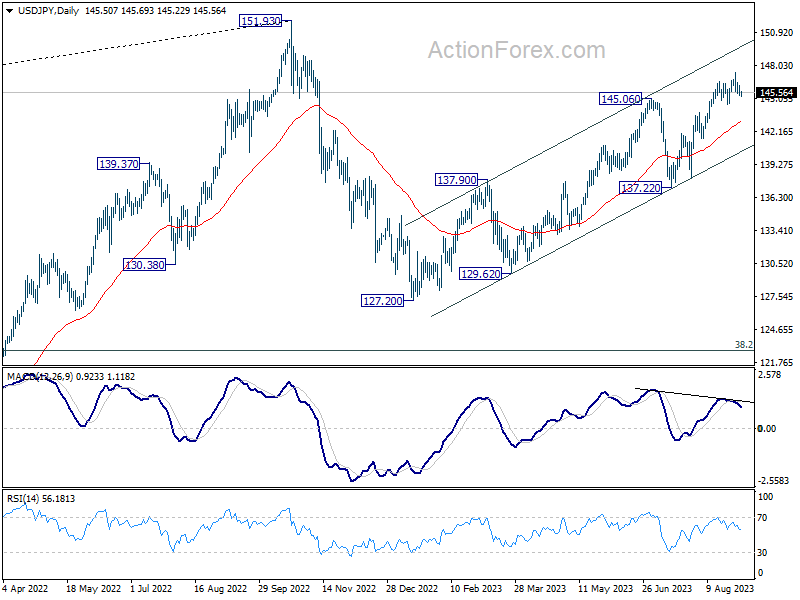

USD/JPY Daily Outlook

Daily Pivots: (S1) 145.17; (P) 145.72; (R1) 146.10; More...

USD/JPY is staying in range of 144.52/147.36 and intraday bias remains neutral. As long as 144.52 support holds, further rally remains in favor. Above 147.36 will resume the rise from 127.20 to retest 151.93 high. On the downside, however, firm break of 144.52 should confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 143.04).

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Rise from 127.20 is seen as the second leg of the pattern and could still be in progress. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.

Forex Markets Awaiting US NFP Data, Bitcoin Reverses Gains

Forex markets are showing unremarkable activity in today's Asian session, with major currency pairs and crosses largely contained within yesterday's trading range. The mood this week has been one of indecision, with sporadic movements failing to evolve into sustained trends. Despite China's intervention to bolster Yuan, the impact was fleeting. Similarly, stronger-than-expected manufacturing data seemed to have little lasting effect on market dynamics. All eyes are now on today's US Non-Farm Payroll data to see if it can be a catalyst for more enduring shifts.

On weekly performance metric, Australian Dollar has been the star, followed closely by New Zealand Dollar and British Pound. Conversely, Dollar sits at the bottom of the performance list, trailed by Swiss Franc, Euro, the Japanese Yen. This composition hints at a risk-on sentiment prevailing in the markets, a mood underscored by a rebound in major US stock indexes a significant retraction in benchmark yields.

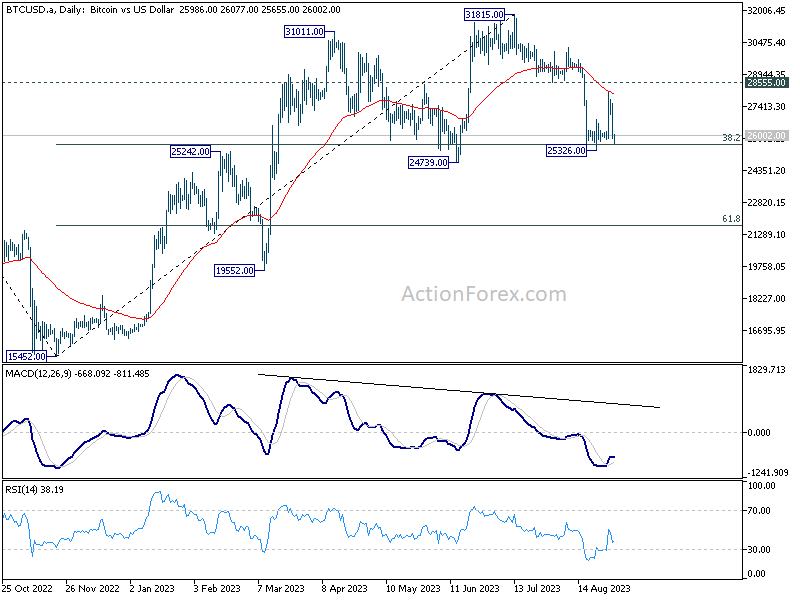

One noteworthy outlier in financial markets has been Bitcoin, which saw a sharp rally to 28146 earlier this week only to relinquish those gains in an overnight selloff. The abrupt reversal followed news that US Securities and Exchange Commission has postponed decisions on approving spot Bitcoin exchange-traded funds from firms like Invesco, WisdomTree, and Valkyrie.

Technically, rejection by 55 D EMA is a bearish sign, suggesting that fall from 31815 is not over yet. The key level now appears to be on 24739 support. Medium term rise from 15452 could still extend higher at a later stage as long as this support holds. Decisive break below this level, however, could open the door to a broader bearish reversal, potentially weighing down sentiment in equities markets, particularly NASDAQ.

In Asia, at the time of writing, Nikkei is up 0.41%. China Shanghai SSE is up 0.39%. Japan 10-year JGB yield down -0.0150 at 0.632. Overnight, DOW dropped -0.48%. S&P 500 dropped -0.16%. NASDAQ rose 0.11%. 10-year yield dropped -0.025 to 4.093.

Japan PMI manufacturing finalized at 49.6, input costs inflation at three-month high

Japan's PMI Manufacturing remained stagnant at 49.6 in August, indicating a third consecutive month of sectoral contraction. According to Usamah Bhatti at S&P Global Market Intelligence, the rate of deterioration was "unchanged from July and only fractional," primarily due to a "slower reduction in new orders."

The report highlighted concerning trends in cost pressures. "Input prices rose at a quicker pace for the first time since September 2022, pushing the rate of input cost inflation to a three-month high," Bhatti stated. The escalation in input costs was specifically attributed to high raw material prices, labor costs, and a weakened yen.

Despite these pressures, the report found that manufacturers increased their selling prices at the "weakest rate in two years," indicating that companies may be absorbing the additional costs instead of transferring them to consumers.

The employment situation also emerged as a point of concern. Bhatti noted, "The rate of job creation broadly stalled, with the latest increase the slowest recorded in the 29-month sequence."

China's Caixin PMI manufacturing rose to 51, output and employment see uptick

China's Caixin PMI for manufacturing defied expectations in August, rising from 49.2 to 51.0 and beating market forecasts of 49.4. This indicates a return to expansionary territory. The report noted several key improvements, including increases in output, new business, and a rebound in employment levels. Significantly, input costs rose for the first time since February, suggesting an easing in deflationary pressures.

Wang Zhe, Senior Economist at Caixin Insight Group, elaborated on the data, stating, "In August, the manufacturing sector showed overall improvement. Apart from sluggish exports, the gauges for supply, total demand, and employment were all in expansionary territory." Wang also noted that the "slight rise in prices buffered the pressure of deflation" and that logistics remained smooth.

However, caution still underlines the market's medium-term outlook. According to Wang, "Looking ahead, seasonal impacts will gradually subside, but the problem of insufficient internal demand and weak expectations may form a vicious cycle for a longer period of time." Wang also warned that "combined with the uncertainty in external demand, the downward pressure on the economy may continue to increase."

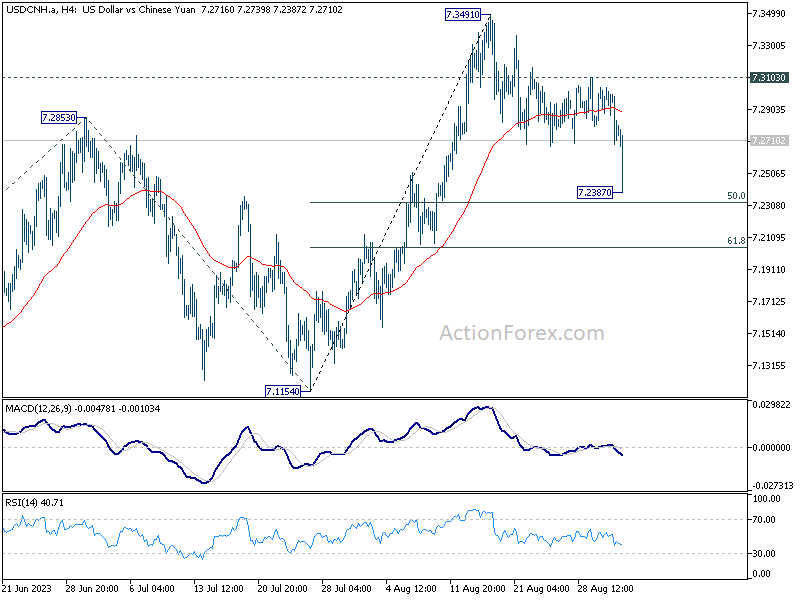

Yuan spikes higher as PBOC slashes FX RRR, but move quickly undone

Chinese Yuan saw a sharp uptick after PBoC announced a substantial 200 bps cut in foreign exchange reserve requirement ratio to 4% from 6%, effective September 15. According to PBoC, the move aims to "improve financial institutions' ability to use foreign exchange funds."

This rate RRR is set to release approximately USD 16.4B in foreign exchange, based on China's FX deposits standing at USD 821.8B as of end-July. Market analysts also note that the FX RRR reduction could have the added effect of lowering dollar funding costs in the interbank market, thereby alleviating some of downward pressure on Yuan.

On the technical front, USD/CNH saw a drop to as low as 7.2387 following the announcement, but it has since recovered most ground. Despite the knee-jerk reaction, the broader uptrend from 6.6971 appears to remain intact. Should it break 7.3103 minor resistance, this would signal completion of the correction from 7.3491 and likely pave the way through 7.3491 for testing 7.3745 high.

However, considering bearish divergence condition in D MACD, strong resistance is likely at 61.8% projection of 6.8100 to 7.2853 from 7.1154 at 7.4091 to limit upside, to complete the five wave sequence from 6.6971.

While technical landscape seems to suggest further upside for USD/CNH, it is crucial to note that these views could be rendered academic at a moment's notice. The Chinese authorities may implement various intervention measures any time, adding an extra layer of unpredictability to the equation.

Downside risks for NFP, yet market impact may be fleeting

Today, the financial markets are keenly focused on US Non-Farm Payrolls data, which is expected to show growth of 170k jobs in August. While unemployment rate is anticipated to remain steady at 3.50%, average hourly earnings are projected to grow by 0.3% mom. However, related data paint a murkier picture, suggesting that risks could be skewed to the downside for the NFP report. Yet, it's unsure if the impact on the markets would last long.

Earlier this week, ADP private job growth came in at 177k, slightly missing expectations and dampening the overall employment outlook. Moreover, JOLTS data showed that job openings have plummeted to their lowest level since March 2021, and consumer confidence took a significant hit, dropping from 114.0 to 106.1. The employment components of ISM Manufacturing and Non-Manufacturing reports are not yet available, leaving a gap in the data to fully assess labor market conditions.

Traders have been notably indecisive recently. While it is almost certain that Fed will pause its tightening this month, the likelihood of a rate hike by year's end seems to be teetering around 50% mark. Market participants are unlikely to get more clarity until the Fed releases its new economic projections and dot plot on September 20, alongside the rate decision.

As for Dollar Index, it's clearly losing upside momentum as seen in D MACD. While another rise cannot be ruled out as long as 102.84 support holds, strong resistance is likely at 38.2% retracement of 144.77 to 99.57 at 105.37 to limit upside. Break of 102.84 will argue that the corrective rally from 99.57 has completed earlier then expected.

Looking ahead

Swiss CPI and PMI manufacturing, Eurozone and UK PMI manufacturing final will be featured in European session. Later in the day, Canada GDP and US non-farm payrolls are the main events, while US will also release ISM manufacturing.

USD/JPY Daily Outlook

Daily Pivots: (S1) 145.17; (P) 145.72; (R1) 146.10; More...

USD/JPY is staying in range of 144.52/147.36 and intraday bias remains neutral. As long as 144.52 support holds, further rally remains in favor. Above 147.36 will resume the rise from 127.20 to retest 151.93 high. On the downside, however, firm break of 144.52 should confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 143.04).

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Rise from 127.20 is seen as the second leg of the pattern and could still be in progress. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Capital Spending Q2 | 4.50% | 7.90% | 11.00% | |

| 00:30 | JPY | Manufacturing PMI Aug F | 49.6 | 49.7 | 49.7 | |

| 01:45 | CNY | Caixin Manufacturing PMI Aug | 51 | 49.4 | 49.2 | |

| 06:30 | CHF | CPI M/M Aug | 0.20% | -0.10% | ||

| 06:30 | CHF | CPI Y/Y Aug | 1.50% | 1.60% | ||

| 07:30 | CHF | PMI Manufacturing Aug | 41.5 | 38.5 | ||

| 07:45 | EUR | Italy Manufacturing PMI Aug | 45.9 | 44.5 | ||

| 07:50 | EUR | France Manufacturing PMI Aug F | 46.4 | 46.4 | ||

| 07:55 | EUR | Germany Manufacturing PMI Aug F | 39.1 | 39.1 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Aug F | 43.7 | 43.7 | ||

| 08:30 | GBP | Manufacturing PMI Aug F | 42.5 | 42.5 | ||

| 12:30 | CAD | GDP M/M Jun | 0.20% | 0.30% | ||

| 12:30 | USD | Nonfarm Payrolls Aug | 170K | 187K | ||

| 12:30 | USD | Unemployment Rate Aug | 3.50% | 3.50% | ||

| 12:30 | USD | Average Hourly Earnings M/M Aug | 0.30% | 0.40% | ||

| 13:30 | CAD | Manufacturing PMI Aug | 49.6 | |||

| 13:45 | USD | Manufacturing PMI Aug F | 47 | 47 | ||

| 14:00 | USD | ISM Manufacturing PMI Aug | 46.6 | 46.4 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Aug | 42.9 | 42.6 | ||

| 14:00 | USD | ISM Manufacturing Employment Index Aug | 44.4 | |||

| 14:00 | USD | Construction Spending M/M Jul | 0.50% | 0.50% |

RBA Board on Hold Next Week – Next Move Will Be Down

The Reserve Bank Board meets next week on September 5.

We are confident that the Board will decide to keep rates on hold at the meeting.

Following the Board's decision to hold rates steady at the August meeting we concluded that rates would remain on hold until the September quarter next year when the first rate cut of 0.25% can be expected.

Since we released that forecast the data flow and the Minutes from the August meeting have provided further support to the view that rates have peaked at 4.1%.

The Minutes once again highlighted that the Board had considered the two options of holding rates steady or raising the cash rate by 0.25%. While in previous Minutes the cases for both options were represented in an even – handed way the preferred case in August seemed to be more clearly favoured than we have seen in past meetings (no reference to "finely balanced").

The Minutes note " the Board had already tightened monetary policy significantly, there were signs that this was working as intended and the Board had time to wait and see how the economy evolves… full effects of the earlier tightening were yet to be recorded… consumption had already slowed significantly, there were early signs that the labour market might be at a turning point and inflation was heading in the right direction."

The Wage Price Index for the June quarter lifted by 0.8% - the same increase we saw in the December and March quarters despite the ongoing record low unemployment rate. There was no significant evidence of an ongoing lift in pressures in either the individual or enterprise bargaining components. Annual growth will increase from the current 3.6% to 3.9% in the September quarter when the 5.9% lift in the minimum wage flows through to the Index but we now expect that 3.9% will be the peak, down from our previous forecast of 4.1%.

The monthly Inflation Indicator showed annual inflation easing to 4.9%yr in July from 5.4%yr in June and 6.7%yr in April. There is volatility in these monthly prints, and we do expect a lift next month due to a greater focus on quarterly services price surveys.

We are forecasting a 0.5% print for the update in August, but this will be offset by a –0.1% decline in September as the new Federal Government child-care rebate kicks in.

Overall, the trend in inflation is clearly "in the right direction." Our current annual growth rate forecast for the CPI in the September quarter is 5.1% down from 6% in June and likely to finish the year at 3.8%.

While there was a sharp jump in the unemployment rate in July from 3.5% to 3.7% the ABS points out the effects of school holidays which are becoming a key issue in determining when people take their leave and start or leave a job. We are expecting a significant lift in jobs growth in August just as we saw in May following the similar lift in the unemployment rate in April (the April survey was conducted during school holidays). Although adding to our case, we don't think the July jobs report will be a swing factor in the Board's decision at the September meeting.

We have argued for some time that the August meeting was likely to be the last opportunity the Board would have to take further insurance against the risk of inflation not reaching the target band by the end of 2025.

Going forward from here the evidence around an ongoing weak economy and slowing inflation will encourage the Board to extend its pause through to the end of the year and into 2024.

So, we expect the debate is now going to evolve towards the timing of the first rate cut.

That does not mean that the Board will abandon the policy of considering "on hold" or "25 bp hike" as the two options but, as we saw in August, the "on hold" case will progressively become dominant.

The Board will also be mindful of the weak AUD – largely a function of the unusual negative yield differential with the US and some market concerns that the policy target of 2.8% inflation by 2025 is too "soft". The recommendations of the RBA Review advocated targeting the middle of the band. That approach may well be adopted by the new Board although, given the better than expected progress on inflation, a revised in the target is unlikely to be a game changer for policy.

One approach to contain some of this AUD negativity is to persist with "members agreed it was possible some further tightening of monetary policy might be required", although markets are likely to become increasingly more dismissive of this practice as we move ahead.

The timing of the first rate cut.

In the note following the August Board meeting we have targeted the September quarter, 2024, for the first cut in this cycle.

Our estimate is that by the time of the August meeting next year the Board will be confronted with unemployment rate of 4.5%; inflation having fallen to 3.2%; and GDP growth of 0.8% for the year to the June quarter 2024 (although, the full update will probably still be, bizarrely the day after the Board meeting.)

While inflation will not have fully returned to the target band of 2–3%, policy will be assessed as being clearly contractionary; the unemployment rate will have risen 1ppt over the previous year with the prospect of further deterioration in the second half of 2024; the economy will be growing at the parlous pace of 0.8% and confidence that inflation will reach the target earlier than the current forecast will be building.

While the RBA will have been hold since June of 2023 the lagged impact of borrowers transitioning from low fixed rate mortgages to much higher floating mortgages, which will intensify in the second half of 2023, leading toa cumulative automatic increase in average mortgage rates right out to the first quarter of 2024 of up to 1 ppt.

Wages growth will also have peaked at 3.9% in the second half of 2023 and slowed to 3.6% with more easing likely through the remainder 2024.

Pressure will have eased on the AUD as we expect the Federal Reserve to have begun its easing cycle by March or June at the absolute latest. Falling US rates will also boost global confidence providing some support for the "risk" currencies, including the AUD.

It is unlikely that the rate cuts can come earlier.

In the first half of 2024 the Board will be facing a tight labour market; potential delays in the beginning of the Fed's easing cycle; and ongoing momentum in house prices. While still falling, inflation will be stickier in the first half of 2024 as the contraction in goods inflation eases and services inflation remains elevated.

That combination is likely to preclude the prospect of rate cuts in the first half of 2024 despite the ongoing evidence that spending remains lack lustre.

Conclusion

2023 has been a difficult year for gauging monthly movements in the cash rate. The Board has varied the weights it gives to the two key themes: risk of not achieving the inflation target on time; and needing to pause to assess the cumulative impact of this very rapid tightening cycle. There has been no clear lead indicator as to how these weights have evolved.

With inflation slowing more rapidly than the Board, and other central banks had expected; evidence of an easing in wage pressures; household spending struggling; and further effective mortgage increases embedded in the system, the policy of moving to the sidelines is now clearly the favoured approach.

We think this should remain the case until the September quarter next year when inflation; growth; and unemployment have established a very clear message that will allow the Board to begin the process of unwinding the rate hikes.

Cliff Notes: Consumer Incomes Remain Under Pressure from Cost of Living

Key insights from the week that was.

Beginning in Australia, the July Monthly CPI Indicator provided further confirmation of the deceleration in inflation’s momentum, easing from 5.4%yr to 4.9%yr. However, the composition still speaks to lingering cost-of-living pressures, as evinced not only by the actual lift in electricity prices (6.0%mth) but also what the lift could have been were it not for the introduction of state energy rebates (19.2%mth). Additionally, the detail around housing still reflects an uncomfortable mix, with rental inflation continuing to accelerate (7.3%yr to 7.6%yr) as the moderation in new dwellings persists (6.6%yr to 5.9%yr). So, while it is constructive to see the current progress in inflation and the improving balance of risks for monetary policy, the detail is a reminder that consumption nonetheless remains under pressure in an environment where both prices and interest rates have risen rapidly.

Therefore, it was somewhat encouraging to see nominal retail sales rise 0.5% (2.1%yr) in July, largely due to a solid contribution from cafés and restaurants associated with school holidays and the 2023 FIFA Women’s World Cup. The influence of population growth and inflation remains substantial however, with retail sales continuing to track a very weak profile on a real per capita basis, in the realm of –3.0%yr to –3.5%yr, a reminder that temporary forces which stimulate aggregate discretionary spending have not significantly altered the underlying trend.

In the lead up to next week’s Q2 GDP report, the ABS also released two partial indicators for investment.

There were some unexpected results around the quarterly profile for construction work done, a modest 0.4% lift in Q2 coupled with a significant upward revision to Q1 (from 1.8% to 3.8%), resulting in construction work being up 9.3%yr. This solid uptrend reflects ongoing momentum in infrastructure investment, public infrastructure up a sizeable 16%yr and private infrastructure +15%yr. Housing experienced mixed fortunes however, with renovation activity down –7.2%yr but new dwelling construction up 5.1%yr.

The Q2 CAPEX survey subsequently delivered an upside surprise, the 2.8% lift in current activity surpassing even Westpac’s top-of-the-range forecast of 2.0%. The 1.9% gain in equipment spending was also constructive and remains consistent with our immediate view for investment. On spending intentions, the third estimate for 2023/24 CAPEX plans remained optimistic, up 7.0% compared to the third estimate a year ago. In our view, this implies a 6.3% rise in CAPEX spending over the financial year. While positive for now, we anticipate a diverging outlook for investment, with equipment spending softening as the impetus from tax incentives fade while capacity expansion via construction work holds firm.

Despite the downside surprise on construction work, our forecast for Q2 GDP remains unchanged at 0.4% (1.8%yr). A detailed breakdown of our forecast can be found on WestpacIQ.

Offshore, the US had the most data to ascertain signal from, with spending, income, and a revised GDP figure released as well as the latest JOLTS survey. Personal spending rose 0.6% in real terms in July after a 0.4% gain in June. Spending well and truly outpaced growth in personal income in the month, 0.2%, and the savings rate fell back near its historic low as a result, highlighting that savings can only be drawn down upon for so long. Given this robust July reading for spending and as Q2 GDP has been revised down from 2.3% to 2.1% annualised, Q3 GDP growth looks set to print materially above trend. That said, with available excess savings dwindling and real incomes recovering slowly, growth looks certain to drop below trend in Q4 and beyond. The latest labour market detail is also supportive of such a view, July's

JOLTS job openings falling by an outsized 338k while the number of unemployed people per job opening increased to 0.7. Hiring and separation rates being little changed and the still historically-high level of job openings are not indicative of recession by any means, but they do point to less opportunity for advancement and nominal wage growth, restricting discretionary demand. In such a climate, a continuation of the current benign inflation trends seems probable. Both headline and core PCE deflators rose by ‘only’ 0.2% in July.

Across the Atlantic, Europe's flash August CPI showed disinflation only at the second decimal place -- August's print coming in at 5.26%yr versus 5.31%yr in July. 'Underlying' inflation cooled to 5.3%yr from 5.5%yr however, giving the ECB the option of extending their pause in September if they perceive the risks faced by the economy as skewed to the downside.

China's NBS manufacturing PMI meanwhile ticked up to 49.7 in August from 49.3 but remains below the 5-year pre-COVID average. Of note, there was a large upswing in main raw material purchase prices and producer prices, although producer price data suggests the starting point was entrenched deflation. The non-manufacturing PMI instead declined from 51.5 to 51.0, continuing the downtrend of recent months. While there was a slight improvement in the employment component for services overall, construction employment’s contraction accelerated.

Overall, the data should be taken as a sign of stabilisation not recovery. The latter is likely some months away, assuming the recent run of policy measures gains traction. Of note this week, the Chinese government announced changes to mortgage lending requirements, with the national minimum deposit requirement to now be 20% for first-time buyers and 30% for second-home buyers (first-time investors). However, required deposits will still vary city by city. How far tier 1 and 2 city deposit requirements for first-time investors are cut towards 30% will dictate how effective the policy is. The additional move to cut mortgage rates for all borrowers will, in time, aid consumption as well as new housing investment. Hopefully, the windfall will be greater than its immediate financial impact. Putting a floor under sentiment such that households feel free to spend down accumulated excess savings could quickly turn Chinese domestic demand. As the changes are due to take effect late-September, it will be a few months before we find out.