Sample Category Title

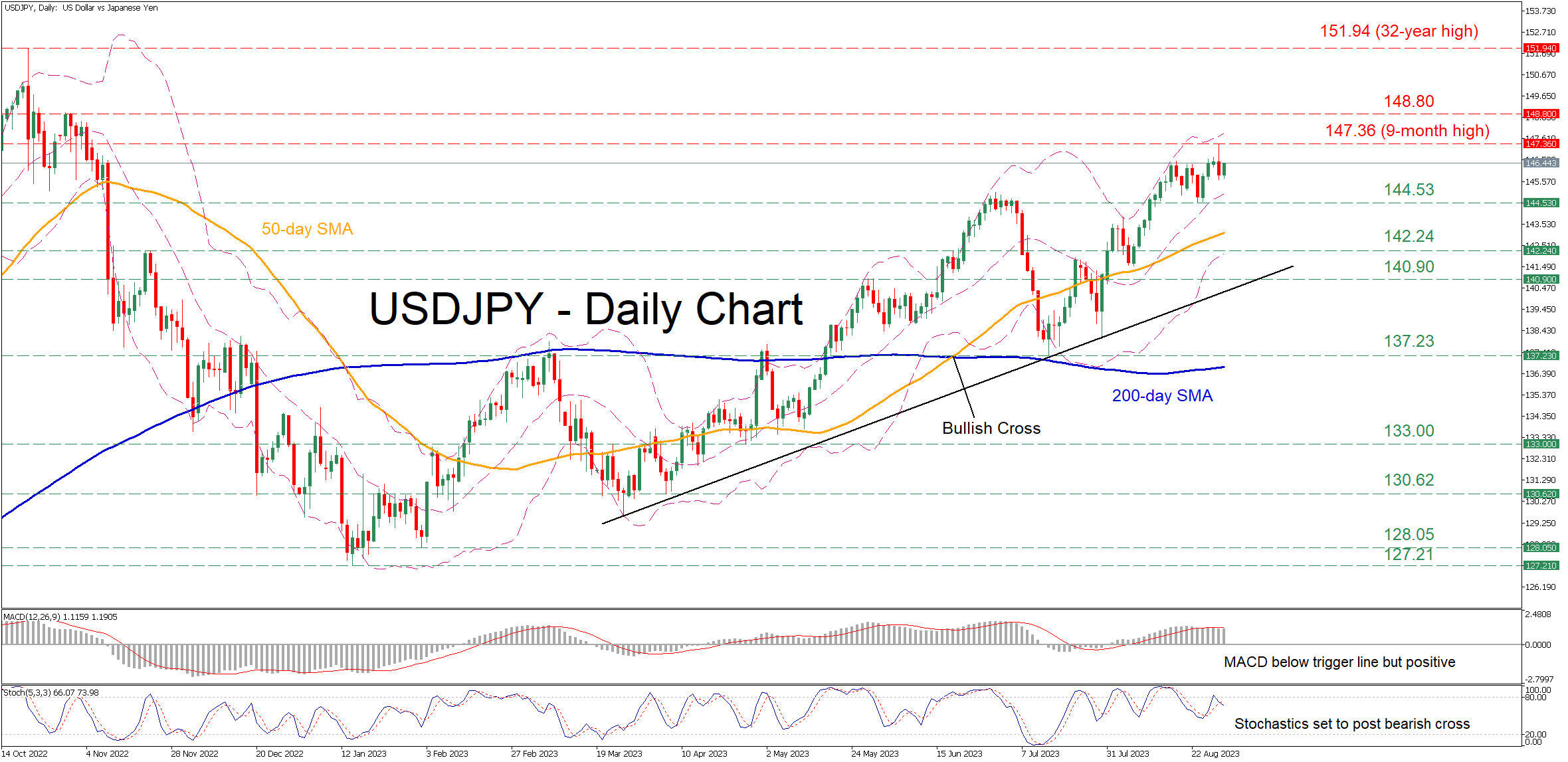

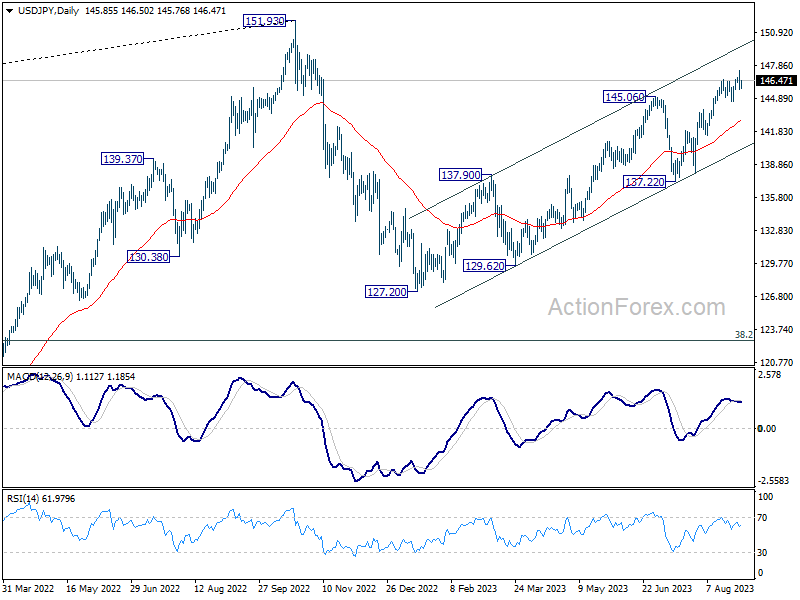

USDJPY Posts 9-month High Increasing Odds of Intervention

USDJPY has been in a steady uptrend since the beginning of the year, posting a fresh nine-month high of 147.36 on Tuesday before paring some gains. Undoubtedly, the probability of an impending pullback appears to be heightening as the pair has surpassed the level around where the first round of intervention by the Japanese authorities took place.

The momentum indicators currently suggest that the bullish forces are fading. Specifically, the MACD is hovering below its red signal line in the positive zone, while the stochastic oscillator is set to post a bearish cross.

If buying interest wanes, the recent support of 144.53 could prove to be the first barrier for sellers to claim. Sliding beneath that floor, the price could descend towards previous resistance zones such as 142.24 and 140.90, which could now serve as support levels. Further declines could then cease at the July low of 137.23.

Alternatively, if the relentless year-to-date rally extends, the pair could initially face the recent nine-month peak of 147.36. A break above that zone could trigger an advance towards the 148.80 resistance territory observed in November 2022. Should that obstacle fail, the spotlight could turn to the 32-year high of 151.94.

Overall, USDJPY seems to be stuck in a steep uptrend, but the price has reached levels that in previous occasions the Japanese policymakers were willing to protect. Will this scenario play out again?

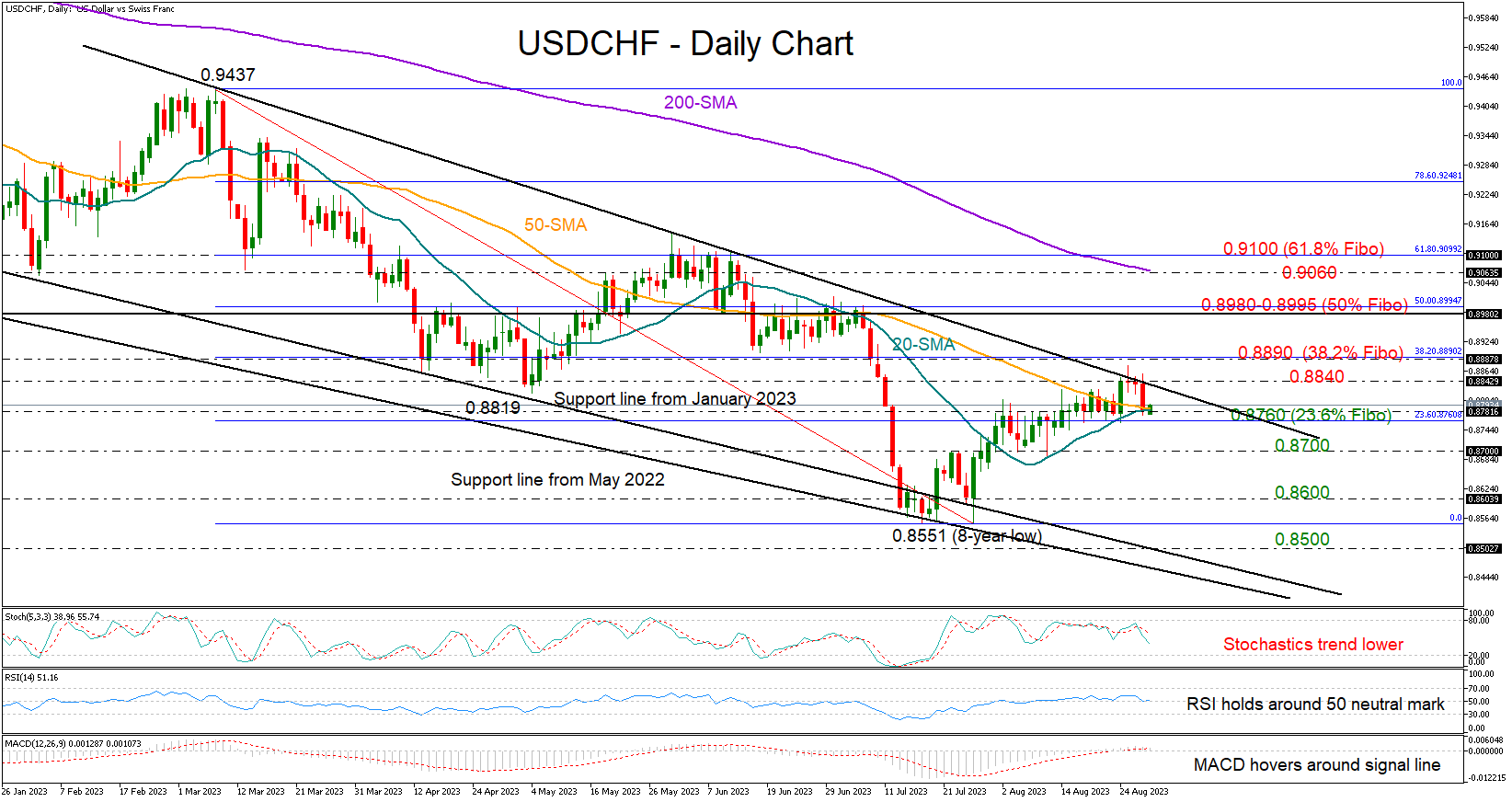

Has the USDCHF Bull Wave Peaked?

USDCHF reversed on Tuesday after six weeks of gains, as the bulls became tired near the resistance trendline at 0.8840 from March.

The 20- and 50-day simple moving averages (SMAs) came immediately to defend the upleg that started from the eight-year low of 0.8515 in mid-July. Traders might also keep a close eye on the 23.6% Fibonacci mark of the March-July downfall, slightly lower at 0.8760. If that base cracks, they may press the price towards the 0.8700 constraining area. Then, another deep negative correction could follow to 0.8600 if sellers stay in the driver’s seat.

Technically, a rebound in the price cannot be excluded as the RSI has not crossed below its 50 neutral mark yet, while the MACD is still hovering around its red signal line.

Still, it’s uncertain whether the pair will find sufficient buying interest to advance sustainably above the descending trendline and the 0.8840 area. The 38.2% Fibonacci mark of 0.8890 could be another headache for the bulls. If the latter gives way, the price could rise exponentially towards the 0.8980 crucial barrier and the 50% Fibonacci, while an extension above 0.9000 could clear the way towards the 200-day SMA.

In brief, USDCHF is testing a potential support zone with scope to force its way back to the important 0.8840 resistance bar. Hopes for a bullish revival could stay intact unless the price dives below 0.8760.

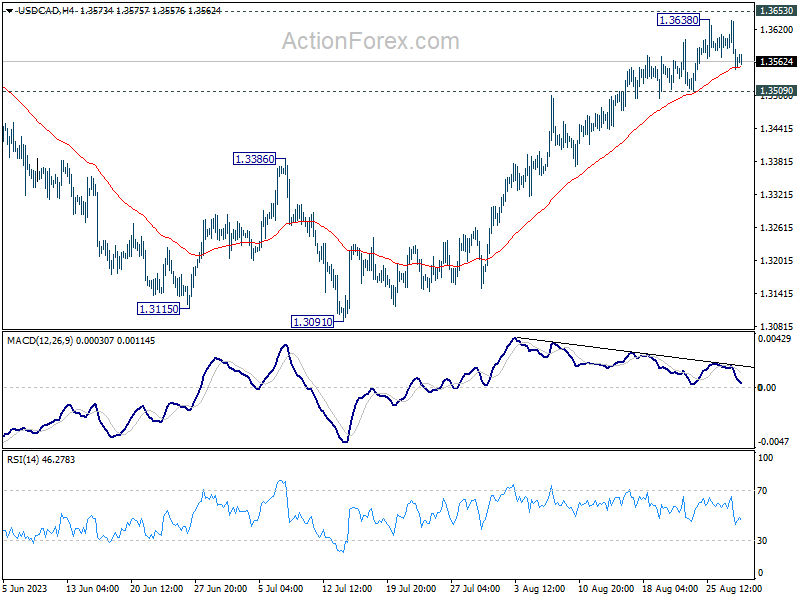

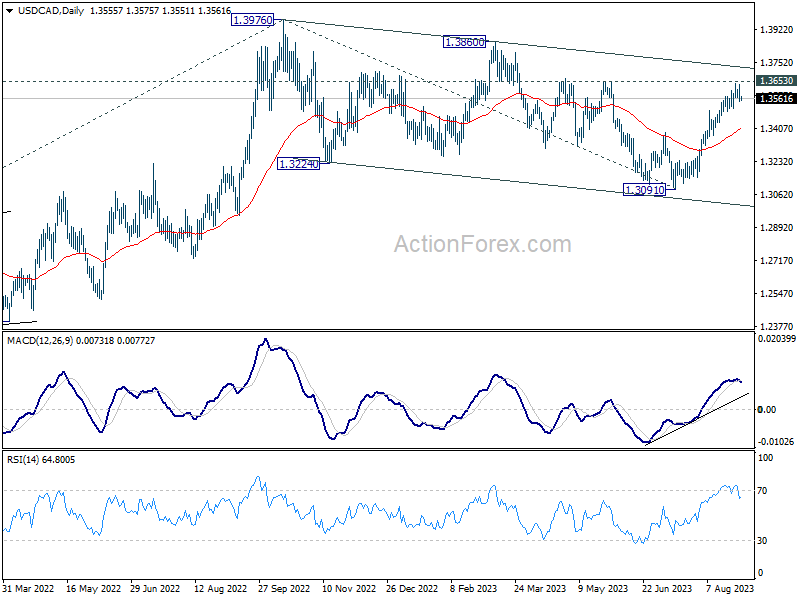

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3521; (P) 1.3580; (R1) 1.3609; More....

Intraday bias in USD/CAD is turned neutral first with current retreat. But further rally is expected as long as 1.3509 support holds. On the upside, decisive break of 1.3653 resistance there will confirm that correction from 1.3976 has completed, and target a test on this high. On the downside, however, break of 1.3509 support will indicate short term topping, and turn bias to the downside for some correction first.

In the bigger picture, price actions from 1.3976 are viewed as a corrective pattern only. Upon completion, rise from 1.2005 (2021 low) would resume through 1.3976. Next target is 61.8% projection of 1.2005 to 1.3976 from 1.3091 at 1.4309. For now, this will remain the favored case as long as 55 D EMA (now at 1.3387) holds.

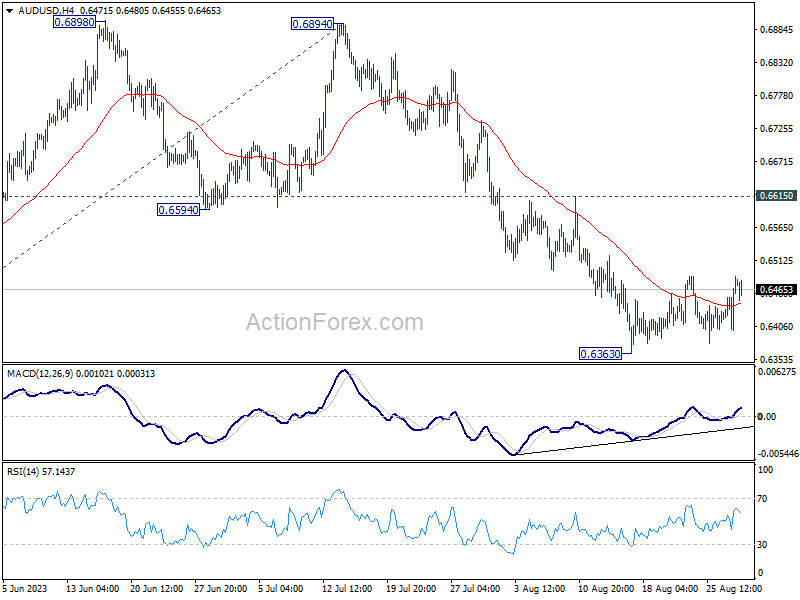

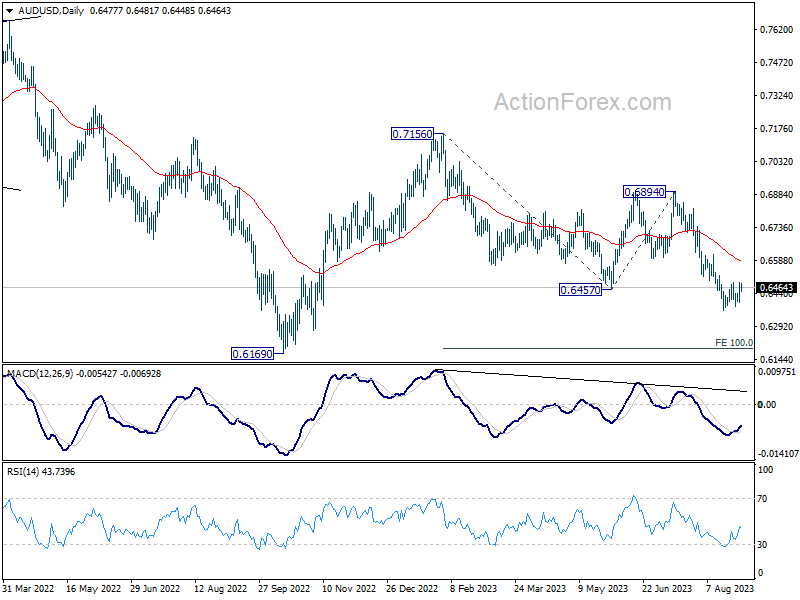

AUD/USD Daily Report

Daily Pivots: (S1) 0.6425; (P) 0.6456; (R1) 0.6511; More...

Intraday bias in AUD/USD remains neutral for the moment as consolidation from 0.6363 is still extending. Another recovery cannot be ruled out, but upside should be limited by 0.6615 resistance. Break of 0.6363 will resume larger fall from 0.7156 to 100% projection of 0.7156 to 0.6457 from 0.6894 at 0.6195.

In the bigger picture, current development argues that the down trend from 0.8006 (2021 high) is still in progress. Decisive break of 0.6169 will target 61.8% projection of 0.8006 to 0.6169 to 0.7156 at 0.6021. This will now remain the favored case as long as 0.6894, in case of strong rebound.

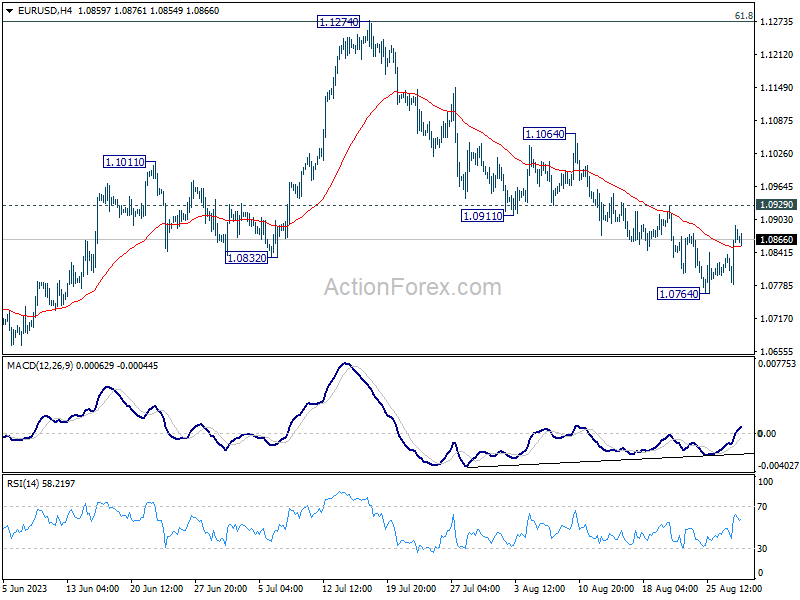

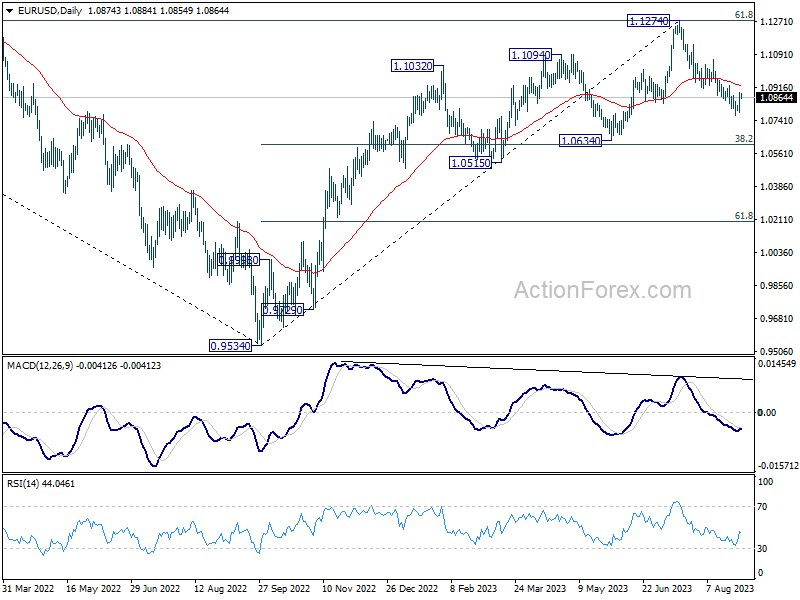

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0810; (P) 1.0851; (R1) 1.0920; More...

EUR/USD's recovery from 1.0764 extends higher today but stays below 1.0929 resistance. Intraday bias remains neutral first, and further decline is in favor. On the downside, break of 1.0764 will resume the fall from 1.1274 to 1.0609/34 cluster support next. Nevertheless, firm break of 1.0929 will turn bias back to the upside for 1.1064 resistance instead.

In the bigger picture, fall from 1.1274 medium term top is seen as a correction to up trend from 0.9534 (2022 low). Deeper decline would be seen to 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609). Strong support could be seen there, at least on first attempt, to bring rebound. Yet, medium term outlook will be neutral for now, as long as 1.1274 resistance holds.

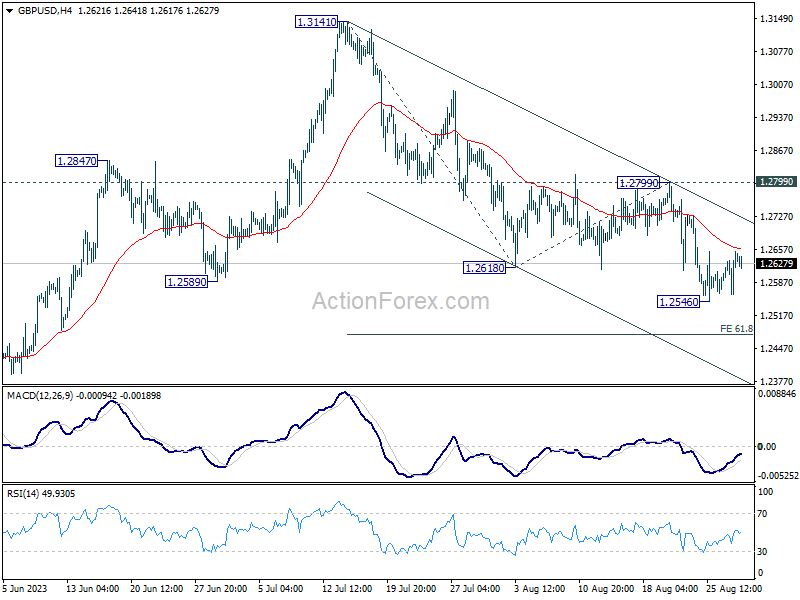

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2586; (P) 1.2621; (R1) 1.2678; More...

GBP/USD is still extending the consolidation above 1.2546 and intraday bias bias stays neutral. Also, near term outlook remains mildly bearish as long as 1.2799 resistance holds. On the downside, break of 1.2546 will resume whole fall from 1.3141 to 61.8% projection of 1.3141 to 1.2618 from 1.2799 at 1.2476. Firm break there could prompt downside acceleration to 100% projection at 1.2276.

In the bigger picture, for now, fall from 1.3141 medium term top is seen as a correction to up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3141 at 1.2075. Strong support would be seen there to bring rebound on first attempt. But outlook will be neutral at best as long as 1.3141 resistance holds, and consolidation from there is set to extend, until further development.

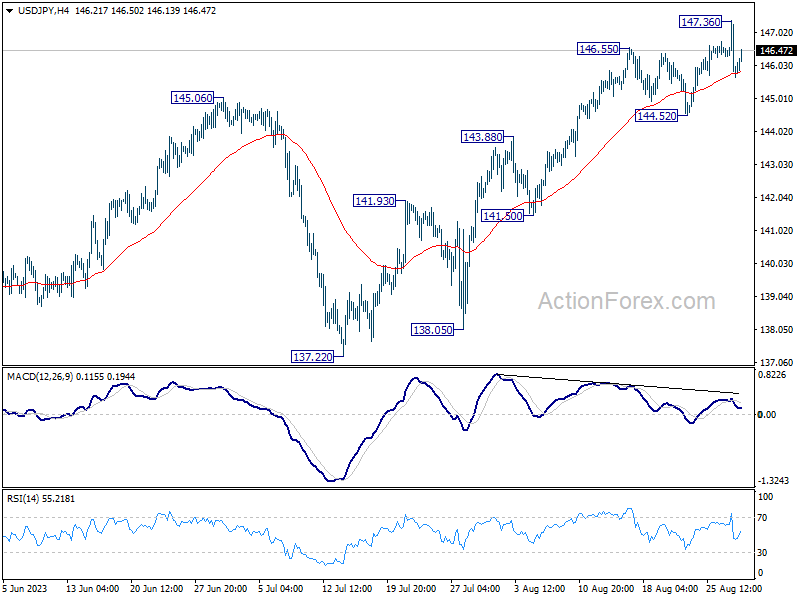

USD/JPY Daily Outlook

Daily Pivots: (S1) 145.24; (P) 146.31; (R1) 146.94; More...

USD/JPY retreated after spiking higher to 147.36 and intraday bias is turned neutral first. Further rally remains in favor as long as 144.52 support holds. Above 147.36 will resume the rise from 127.20 to retest 151.93 high. On the downside, however, firm break of 144.52 should confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 142.86).

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Rise from 127.20 is seen as the second leg of the pattern and could still be in progress. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.

DYX Dropped Below 104 (Close 103.5)

Markets

US and EMU markets yesterday initially held to the guarded technical trading as was the case on Monday. However, with central banks working under the highest the degree of data dependency, things can move quickly. Both US JOLTS job openings (8827k from 9165k, lowest since March 2021) and consumer confidence (106.1 from 114) showed an unexpected tumbling, causing markets to raise the odds for a pause in the Fed hiking cycle at the September meeting, despite chair Powell and other central bankers holding to the higher for longer narrative at Jackson Hole just a few days ago. In a perfect re-steepening the US 2-y yield dropped 15.4 bps leaving behind the 5.0%+ area (4.90%).The 30-y eased 4.7 bps. The decline was mainly driven by the real yields (10-y minus 6.4 bps). The spill-over to European markets was modest. The focus in the EMU is on inflation data to be published today (Germany) and tomorrow (EMU). German yields lost between 2.3 bps (2-y) and 5.7 bps (30-y). The sharp decline in US yields propelled equities (S&P 500 +1.45%, Nasdaq 1.74%). Important support levels that were at risk only a week ago look again relatively safe now. The lost of (real) interest rate support and the risk rebound broke the USD’s momentum. The DYX dropped below 104 (close 103.5). A potential test of the 104.7 end May top is called off for now. EUR/USD jumped to the high 1.08 area (close 1.088). Even the yen received some breathing space after USD/JPY initially jumped well north of 147 (close 145.88). Even so, the USD/JPY uptrend remains intact for now.

Asian equities mostly open in green but gains could have been bigger give the price action on WS yesterday evening. Persistent uncertainty on Chinese growth and on the country’s property sector are tempering sentiment. US ADP private job growth later today is expected to decline from a very strong 324k in July to 195k in August. Markets are sensitive to negative surprises, but after yesterday’s repositioning expectations for a September Fed rate hike have already become low going into Friday’s payrolls report (0.15%). So the room for a further sharp decline in ST US yields probably isn’t that big anymore. The reaction of European interest rate markets to the German August CPI data could be more interesting. Headline HICP inflation is expected to slow down further to 0.3% M/M and 6.5% Y/Y (from 0.5%M/M and 6.5% Y/Y in July). With markets discounting a close to even chance between a rate hike and a pause at the September 14 ECB meeting, there is room for a market reaction either way in case of a surprise. The EUR/USD decline over the previous month was mainly driven by overall USD strength. After yesterday’s rebound, the pair is now closing in the ST downtrend line marking the decline since mid-July (coming near 1.09). The payrolls will have the final say on the overall USD performance. Even so, higher than expected EMU inflation data might help to put a floor the euro short term.

News and views

Headline Australian inflation rose by 0.3% M/M in July following a 0.7% gain in June. The Y/Y figure dropped more than forecast, from 5.4% to 4.9%, matching the lowest level since February 2022. Declines in holiday travel and accommodation (-3.3%), fruit and vegetable prices (-2.9%) and automotive fuel (-0.2%) weighed on headline CPI while price for rents (0.7%), electricity (6%) and gas and other household fuels (2.3%) increased. Government energy rebates prevented a 19.2% increase in electricity prices, according to the Australian Bureau of Statistics. CPI excluding volatile items remained higher at 5.8% Y/Y (vs 6.1% Y/Y in June). The Aussie dollar briefly ticked lower on the release, but already returns towards yesterday’s 0.6480 top (USD weakness). Incoming RBA governor Bullock yesterday said that inflation is still too high in Australia and that the RBA may have to raise interest rates again. For the time being and at least until next year, the central bank will be taking decisions month by month. She’s reluctant to give any sort of predictions on how long interest rates may have to stay high.

People familiar with the matter told news agency Bloomberg that China’s largest banks are preparing to cut interest rates on existing mortgages (loans on first homes) and deposits as soon as today in the latest bid to revamp consumer spending. In separate news, the China Securities Journal reports, citing analysts, that the country’s currency will receive government support to prevent excessive volatility awaiting pro-growth measures to take effect. USD/CNY is camping around 7.30, matching the weakest CNY level since end 2007.

Bad News is Good News for Markets – For Now

Market movers today

Today we get the first August CPI releases in the euro area with both Germany and Spain reporting numbers ahead of the Flash Euro CPI tomorrow.

In the US ADP employment for August is due. It may get extra attention after the weak job openings data and consumer confidence yesterday but remember the ADP release is rarely a good guide for the non-farm payrolls due on Friday.

In Scandi, Sweden will release the monthly batch of survey data for consumers and businesses.

Overnight China will release August PMI for both manufacturing and services from NBS.

The 60 second overview

US releases. The US session yesterday saw the release of the monthly JOLTS job opening statistics which showed a sharp decline from 9.2m in June to 8.8m in July. This is a clear indication that demand for labour is beginning to level off and that wage growth pressures are easing with the JOLTS report having many coinciding features with other US labour market compensation measures. Hence the release should be encouraging news for the Federal Reserve as it suggests that the last years' monetary tightening is beginning to feed through to the labour market. We will get the important non-farm payrolls report on Friday.

In addition, the Conference Board Consumer survey release for August - also released yesterday - showed beginning signs of weakening US consumer sentiment. Consumer expectations declined following some improvement over the summer, while the assessment of job opportunities being 'plentiful' fell to the lowest level since April 2021. For the consumer confidence indices there were signs of weakness both in the current situation assessment as well as in the future expectations component - similar to earlier signals from University of Michigan and the PMIs. Inflation expectations in this report ticked ever so slightly higher (5.8%; from 5.7%), although we would be careful reading too much into this amid the summer rise in gasoline prices.

Markets. Overall softer US consumer sentiment combined with signs of declining nominal wage growth eases the pressure on the Federal Reserve to deliver more monetary tightening. Indeed, rates markets reacted sharply to the releases with 2 Y US yields moving more than 10bp lower driving a general bullish steepening of the US yield curve. In turn the drop in yields added relief in financial markets with risky assets across asset classes performing strongly. This shows that we are currently in a "bad news is good news"-regime for markets with investors fretting the potential for additional monetary tightening.

Norway. Also in Norway we got data yesterday on unfilled vacant positions in the job market which showed a drop from 131K to 118K bringing the vacancy rate from 4.1% to 3.7%. The release supports the signals from other recent indicators that the labour market remains tight, but is weakening moderately as growth is slowing down. While not weak enough to stop Norges Bank from delivering another 25bp hike in September, we do believe that a weaker labour market increasingly suggests that the peak in policy rates will be hit next month.

Equities were notably higher on Tuesday as the soft landing narrative was reinforced by new job data. This especially spurred US equities as yields fell, with S&P500 gaining 1.5%, but also Europe rose 1%. Sector performance differed between the two regions. European and Nordic outperformance was driven by value cyclicals, such as Stora Enso and Nokia among the top performers, while big tech led the gains in the US (consumer discretionary, communication and tech all up 2%). Buoyant tones are continuing this morning with Asia and US futures in green.

FI: Global fixed income markets have had a strong performance following the US data releases described above. 2-year US Treasury yields have fallen by a significant 12bp, while the 10-year Treasury yield is down 9bp. The tailwind to US bond markets spilled over to European markets, where 10-year yields fell 5-7bp. The 10-year Italian yield spread to Germany tightened by a few basis points. The market pricing of the expected peak ECB rate was close to unchanged, while the implied probability of further rate hikes from the FOMC subsided a bit.

FX: Yesterday's FX session was dominated by a boost to risk and cyclically sensitive currencies following the sharp decline in USD yields. Unsurprisingly, the USD had a poor session with EUR/USD moving close to one full big figure higher after having moved below the 1.08 mark earlier in the session. Both NOK and SEK have enjoyed the rally in risk appetite with EUR/NOK and EUR/SEK moving back to the low 11.50s and low 11.80s, respectively. The decline in global yields has contributed to sending USD/JPY a full big figure lower toward the 146 mark while EUR outperformance vis-à-vis GBP has sent EUR/GBP back above the 0.86 mark for the first time in two weeks.

Credit: The red hot primary credit market continued Tuesday with a number of high profile deals announced. In Scandi space this included among others Securitas, Molnlycke, Klaveness Combination Carriers, Eurofins and Sydbank. Once again, the high primary activity took most of the attention leaving the secondary credit market activity subdued. That said, iTraxx Main ended 4bp tighter at 70bp while iTraxx Xover was 18bp tighter at 395.

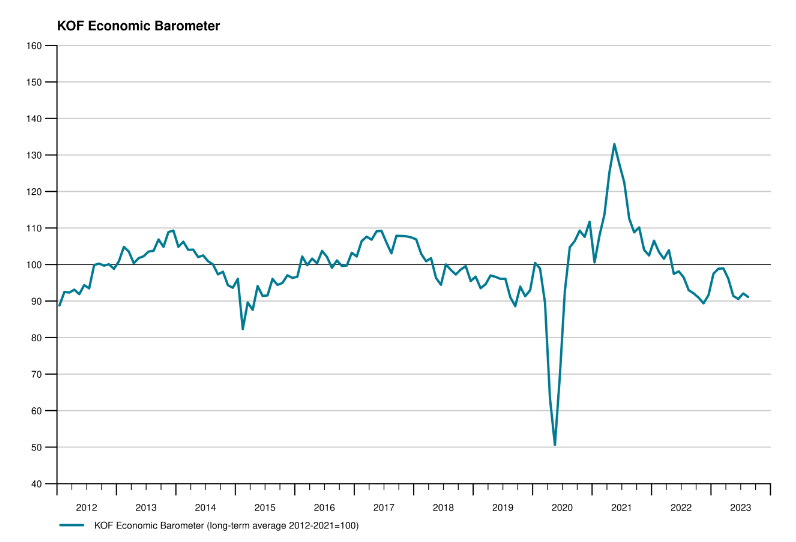

Swiss KOF falls to 91.1, signals sluggish economy ahead

Swiss KOF Economic Barometer, a leading indicator for the Swiss economy, declined from 92.1 to 91.1 in August, missing market expectation of 91.3. The barometer continues to hover below the average mark, signaling that Swiss economy is likely to face challenging conditions in the near term.

According to KOF, almost all sectoral indicators contributed to the lower reading except for construction and domestic consumption, which exhibited slight positive developments.

The most notable downturn in sentiment was observed in the services sector, affecting both real and financial services. This was closely followed by export-oriented businesses, as well as the hotel and restaurant industries.