Sample Category Title

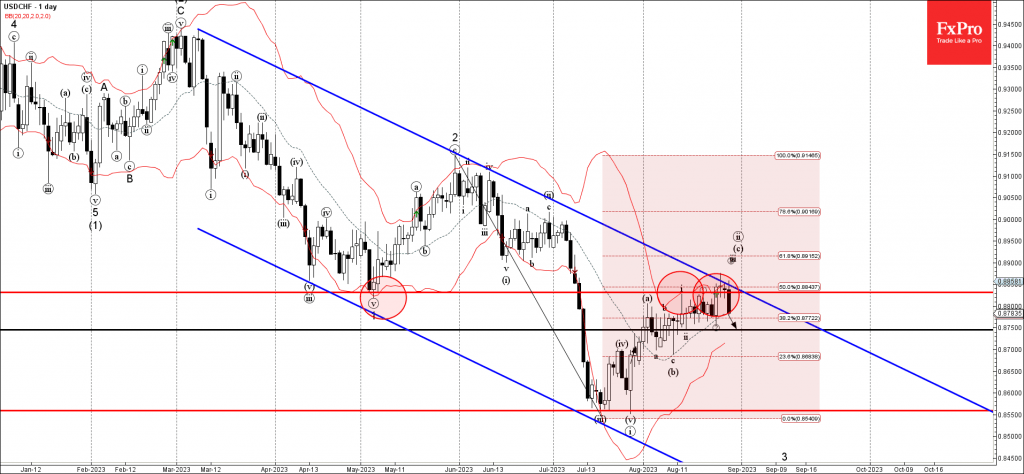

USDCHF Wave Analysis

- USDCHF reversed from pivotal resistance level 0.8830

- Likely to fall to support level 0.8750

USDCHF currency pair recently reversed down from the pivotal resistance level 0.8830 (former multi-month low from May), intersecting with the upper daily Bollinger Band and the 50% Fibonacci correction of the downward impulse from May.

The resistance level 0.8830 was further strengthened by the resistance trendline of the wide daily down channel from the start of May.

Given the clear daily downtrend, USDCHF currency pair can be expected to fall further toward the next support level 0.8750.

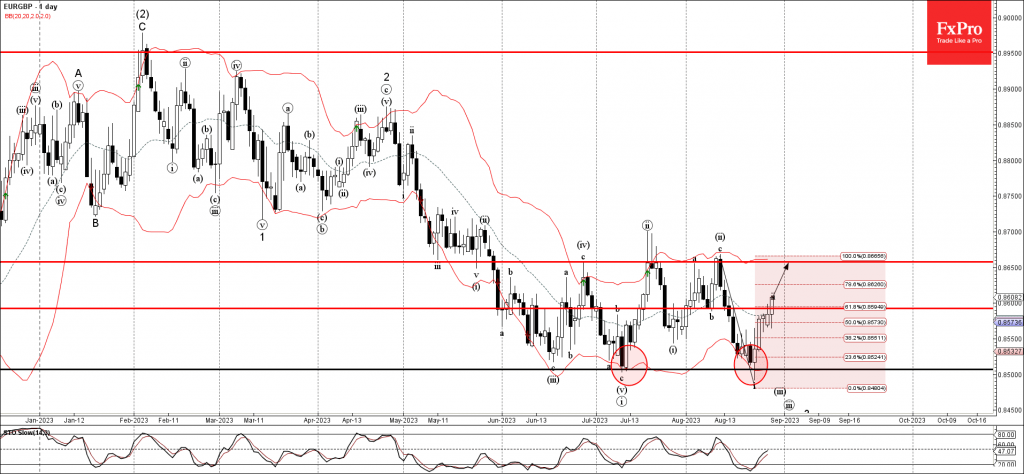

EURGBP Wave Analysis

- EURGBP broke resistance level 0.8590

- Likely to test resistance level 0.8655

EURGBP currency pair recently broke above key resistance level 0.8590, intersecting with the 61.8% Fibonacci correction of the downward impulse from the start of August.

The breakout of the resistance level 0.8590 accelerated the active short-term correction ii.

Given the strong sterling sales across the FX markets, EURGBP currency pair can be expected to rise further toward the next resistance level 0.8655 , which has been reversing the pair since June.

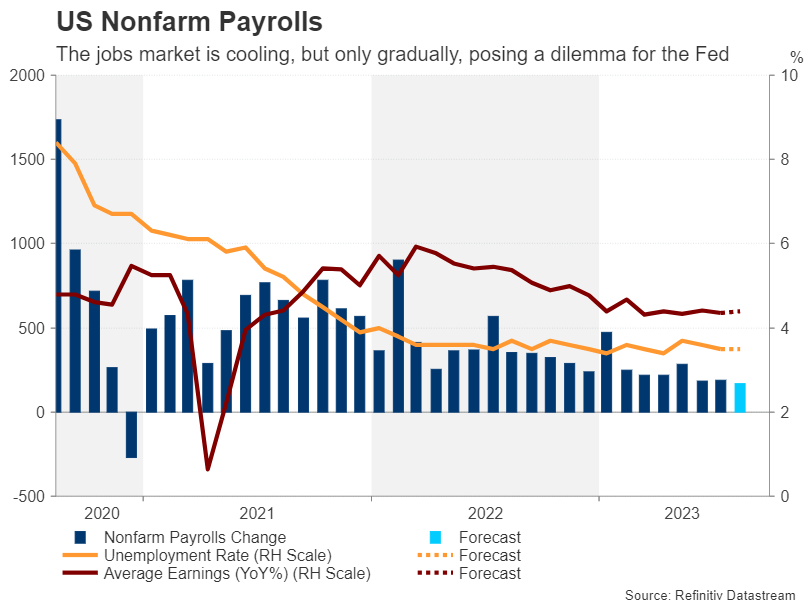

US Nonfarm Payrolls and PCE Inflation Awaited for Vital Clues after a Neutral Powell

A crucial data week lies ahead as the latest PCE inflation figures are due on Thursday, while on Friday, the August NFP report will mark the end of summer. Both reports will be released at 12:30 GMT. The upcoming numbers look set to attract even more attention than usual this time after Fed Chair Jerome Powell struck a finely balanced tone when he addressed the Kansas City Fed’s economic symposium at Jackson Hole, Wyoming, on Friday. With the US dollar trading near 12-week highs, will the data bolster expectations for further rate hikes or dampen them?

Above-trend growth

The Fed’s current round of tightening has been widely characterized as one of the most aggressive in its history. Yet, the US economy is on course to expand by almost 6% annualized rate in the third quarter – quite remarkable for this late stage of the tightening cycle and an acceleration on the second quarter’s 2.4% pace. Revised estimates for Q2 GDP growth are due on Wednesday. Powell told audiences at Jackson Hole that a continuation of this “above-trend growth” could warrant some further policy tightening.

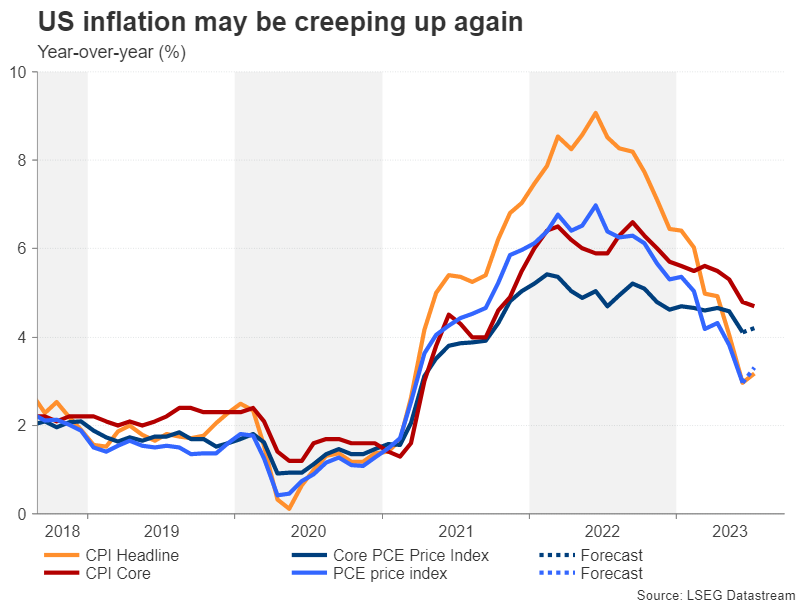

Will core PCE follow CPI higher?

On inflation, Powell repeated that it remains “too high” despite the recent declines. Non-housing services inflation in particular is a big concern, saying “some further progress here will be essential to restoring price stability”.

Overall services prices were 4.9% higher from a year ago in June according to the PCE measure. That’s notably higher than the core PCE price index reading of 4.1% y/y. For July, core PCE is forecast to have edged up to 4.2%. This would be in line with the rise in headline CPI during the same period, underlining the slow path to achieving 2% inflation.

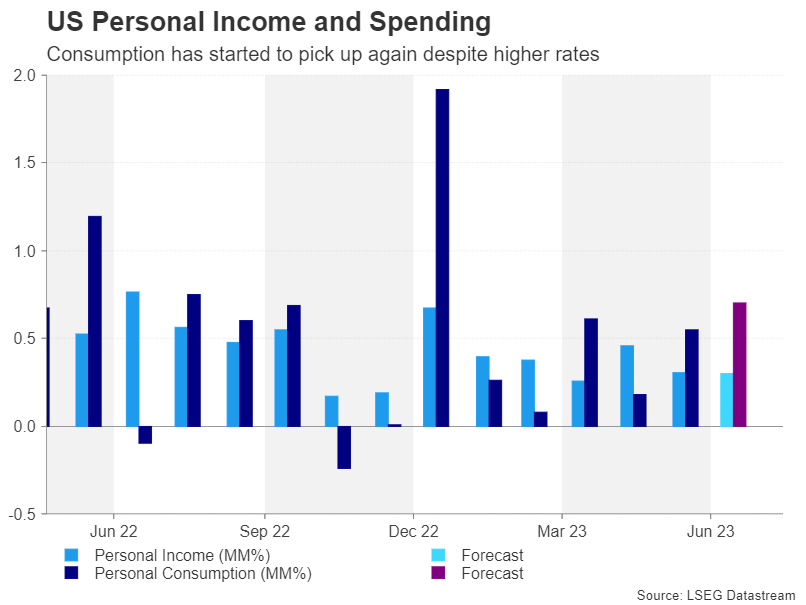

Real wages are boosting consumption

With upward pressure on wages from a very tight labour market and consumer spending rebounding rather than slowing, it’s no wonder services inflation is elevated. Personal consumption is projected to have jumped by 0.7% over the month in July after increasing by 0.5% in June.

Personal income has also been growing steadily this year and it’s expected to have ticked up by 0.3% m/m in July.

Although higher borrowing costs have started to inflict some pain on many households, what’s likely boosting the consumer is the pickup in real wages in recent months as the rate of inflation falls below the rate of nominal wage growth. That trend looks set to continue for a while longer as wage increases are showing no sign of slowing amid a still hot jobs market.

Average hourly earnings are expected to have risen by 4.4% on a yearly basis in July, unchanged from the prior month.

Strikes could stoke wage-price spiral

However, that figure might only be headed higher in the coming months as there’s been a number of major strikes during the summer across America, many of which are ongoing, and firms have had to offer big pay deals to reach a settlement. American Airlines for example bumped pilots’ pay by as much as 46% over several years and UPS agreed a 17% pay hike for its drivers.

Headlines about double digit wage offers are bound to keep Fed policymakers awake at night. But for August at least, the latest strike actions, including the actors and writers strike in Hollywood, likely had a negative impact on employment.

Payrolls increases are moderating

Nonfarm payrolls are forecast to have gained by 170k in August, down from 187k previously. The strikes pose a downside risk to the headline print so any positive surprises would probably shock markets and push up the odds for a 25-bps rate hike in September or November.

The unemployment rate is expected to remain steady at 3.5%.

Overall, the labour market does appear to be cooling and there was further confirmation of this after the Bureau of Labor Statistics reduced its estimate of the number of people on payrolls in March by 306,000 in its preliminary benchmark revision for 2023.

Excluding the wage pressures stemming from the labour disputes, the outlook for the jobs market has become somewhat gloomier, particularly in the manufacturing sector. The deepening economic slowdowns in China and the euro area, which come against a backdrop of tighter credit conditions at home, are some of the factors businesses have to consider before hiring new workers.

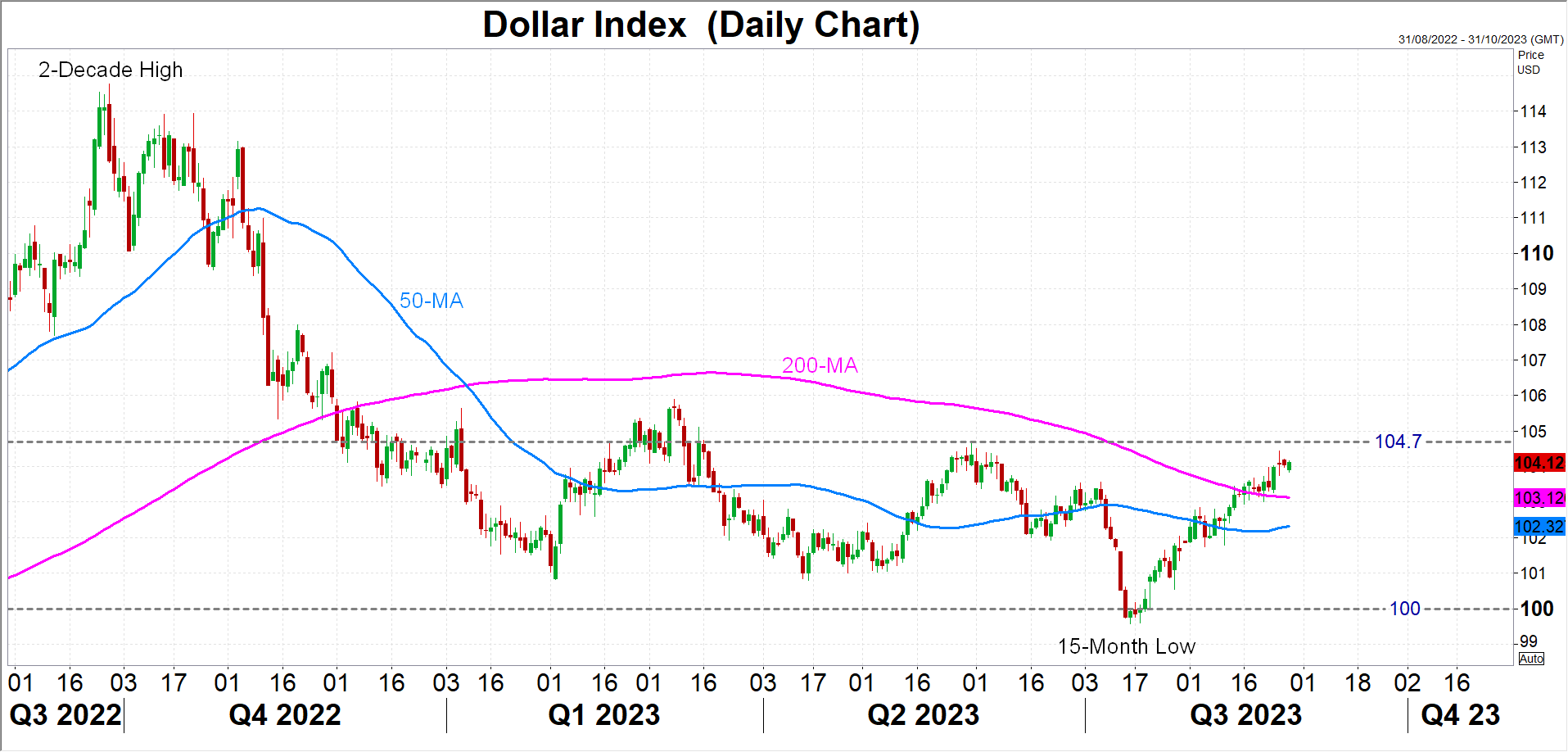

Dollar bulls hoping for September hike

For the US dollar, which is at a critical juncture against major pairs such as the yen, euro and pound, the data could determine whether its six-week-old rebound has more ground to cover. Whilst its gains have been impressive, the dollar index has yet to surpass its previous peak of 104.70 from May 31 and until it does, its medium-term outlook will stay neutral.

Powell has set the bar high for a September rate rise, making it clear that the Fed will “proceed carefully” when deciding on further tightening. Nevertheless, should both the core PCE and payrolls data beat expectations, it will be hard to justify a pause. However, if the week ends with a mixed batch of readings, policymakers are more likely to wait until November to get a clearer picture on what’s happening to prices and the economy.

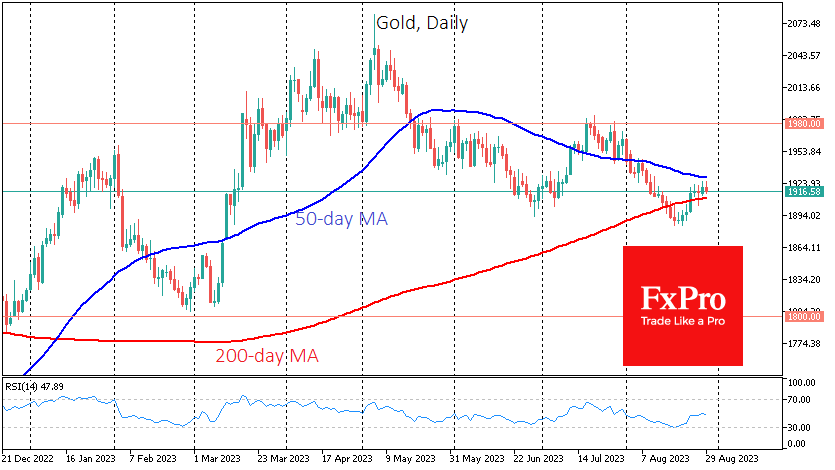

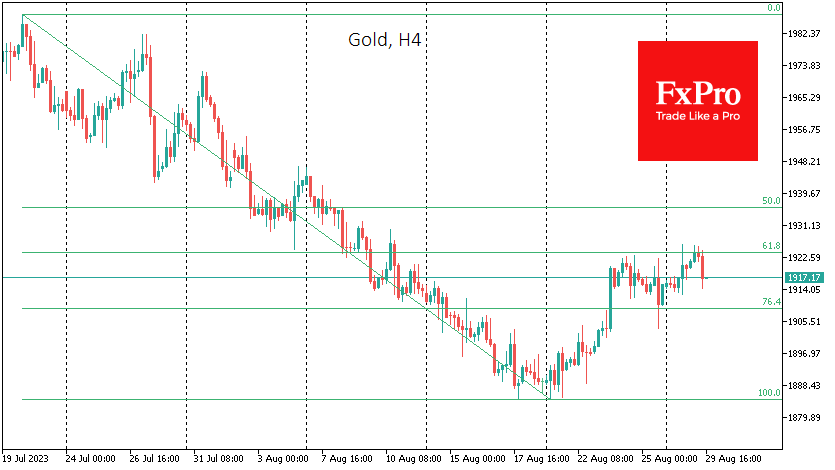

Gold Probably Ending a Short-term Bounce

Gold’s rally appears to be running out of steam after a 2% rally since the beginning of last week.

Gold has been at the mercy of sellers for a month since the 20th, losing over 5.2% from peak to trough. Gold began to look oversold in the short term after falling below $1885.

The price fell below the 50-day and then the 200-day moving averages in August. The rally in recent days has brought the price back above the long moving average, but the short moving average is effectively acting as resistance. The last time we saw this dynamic was in May last year, followed by five months of declines before a reversal to the upside.

The situation could repeat itself this time around. At the end of last week, the rally slowed considerably, and since the start of the day on Tuesday, gold is down 0.2%, having fallen to $1915 an ounce in the spot market.

The rally since the beginning of last week fits into the Fibonacci retracement pattern, having lost upward momentum as it approached the 61.8% level of the initial decline.

Confidence in gold’s further decline will be boosted by a quick return below the 200-day average, now above $1910. The final confirmation of this pattern would be a return to August’s local lows at $1885, opening the way to $1820.

Separately, it is worth noting that gold has temporarily returned to a direct correlation with the equity market. In contrast, in the spring of this year and last, it was the other way round: equity sell-offs were accompanied by frenzied gold buying.

Last year, it was geopolitics, and this spring, it was fears about bank capital retention. The latter has fallen off the radar but is hardly exhausted, and it would not be surprising to see it back on the front pages of the financial press in September-October. This could be an essential pivot point for growth for gold, but no earlier.

Euro Dips Below 1.08 But Bounces Back After Soft US Data

- Euro slips below 1.08 but recovers

- German GfK consumer climate falls

- US consumer confidence and job openings decelerate

The euro fell below the 1.08 line on Tuesday after a weak German consumer confidence report but has recovered in the North American session after soft US data. EUR/USD is currently trading at 1.0840, up 0.20%.

Germany is the eurozone’s largest economy and is considered the powerhouse of the bloc. That has changed dramatically as the German economy is looking more like a dead weight than a locomotive. With the economy sputtering, it’s no surprise that German business and consumer confidence is in the doldrums.

Germany’s GfK Consumer Climate is forecasting a reading of -25.5 for September, down from the revised downward figure of -24.6 in August and below the consensus estimate of -24.3. This was the lowest reading since May, with consumers pointing to high inflation and concern about potential unemployment as key reasons for concern. Last week, German Ifo Business Climate fell in August for a fourth straight month to 85.7, down from an upwardly revised 87.4 and shy of the market consensus of 86.7 points.

German CPI expected to fall to 6.0%

Germany will release the July inflation report on Wednesday. Inflation is currently at 6.2% and is expected to dip to 6.0%, considerably higher than eurozone inflation which is at 5.3%. The ECB is committed to bringing inflation back to the 2% target but it’s unclear if the central bank will raise rates for an eighth straight time or take a pause and monitor how the economy is performing. The benchmark rate is relatively low at 3.75%, but the eurozone and German economies aren’t in the best shape and higher interest rates would raise the likelihood of a recession.

In the US, it was a bad day at the office. The Conference Board Consumer Confidence Index fell sharply to 106.1 in July, compared to 116.0 in August. JOLTS Jobs Openings slowed to 8.82 million in July, down from 9.16 million in June and well off the estimate of 9.46 million. The data is further evidence that the US economy is slowing as high rates continue to filter through the economy.

EUR/USD Technical

- EUR/USD is testing support at 1.0830. The next support line is 1.0731

- There is resistance at 1.0896 and 1.0996

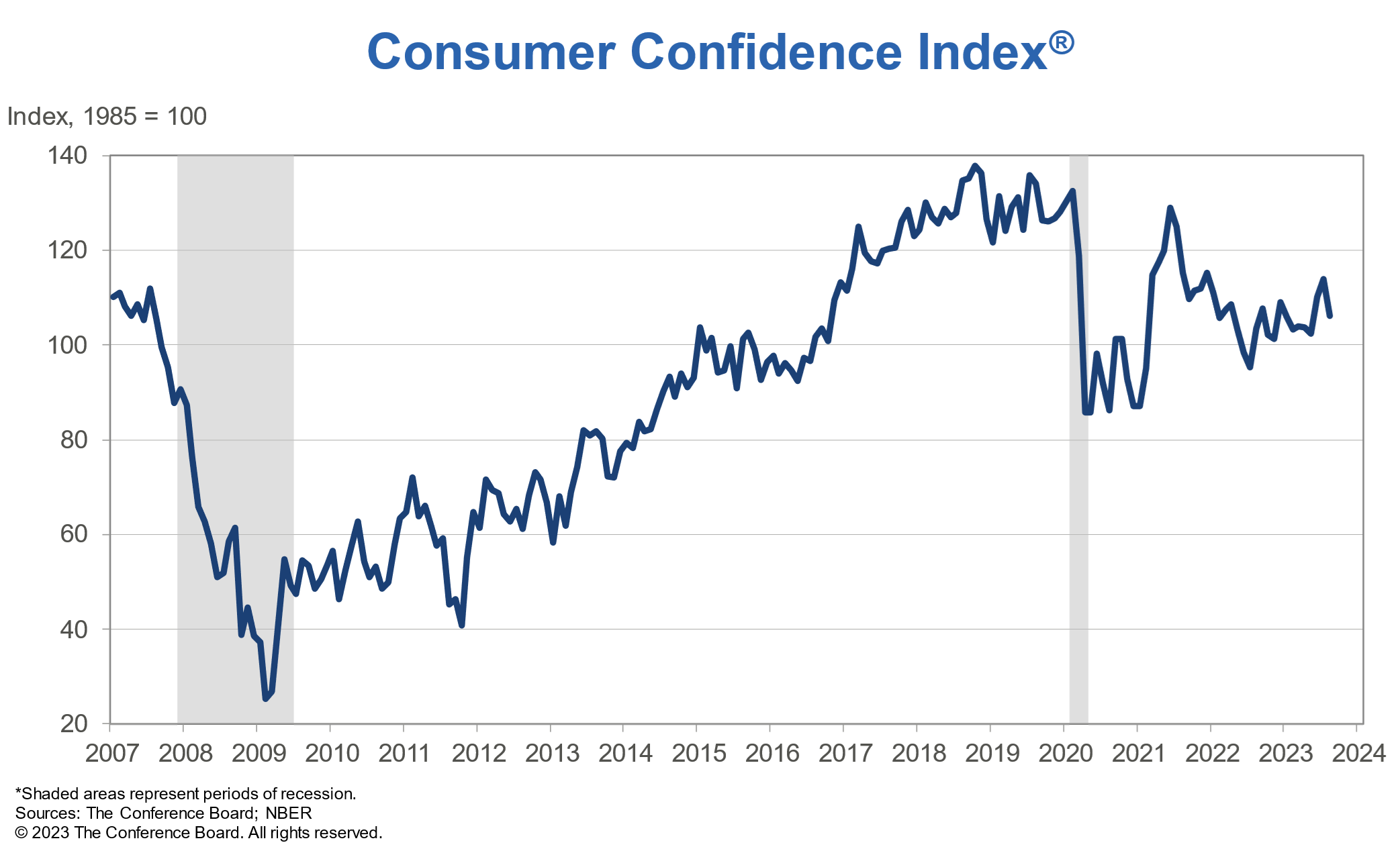

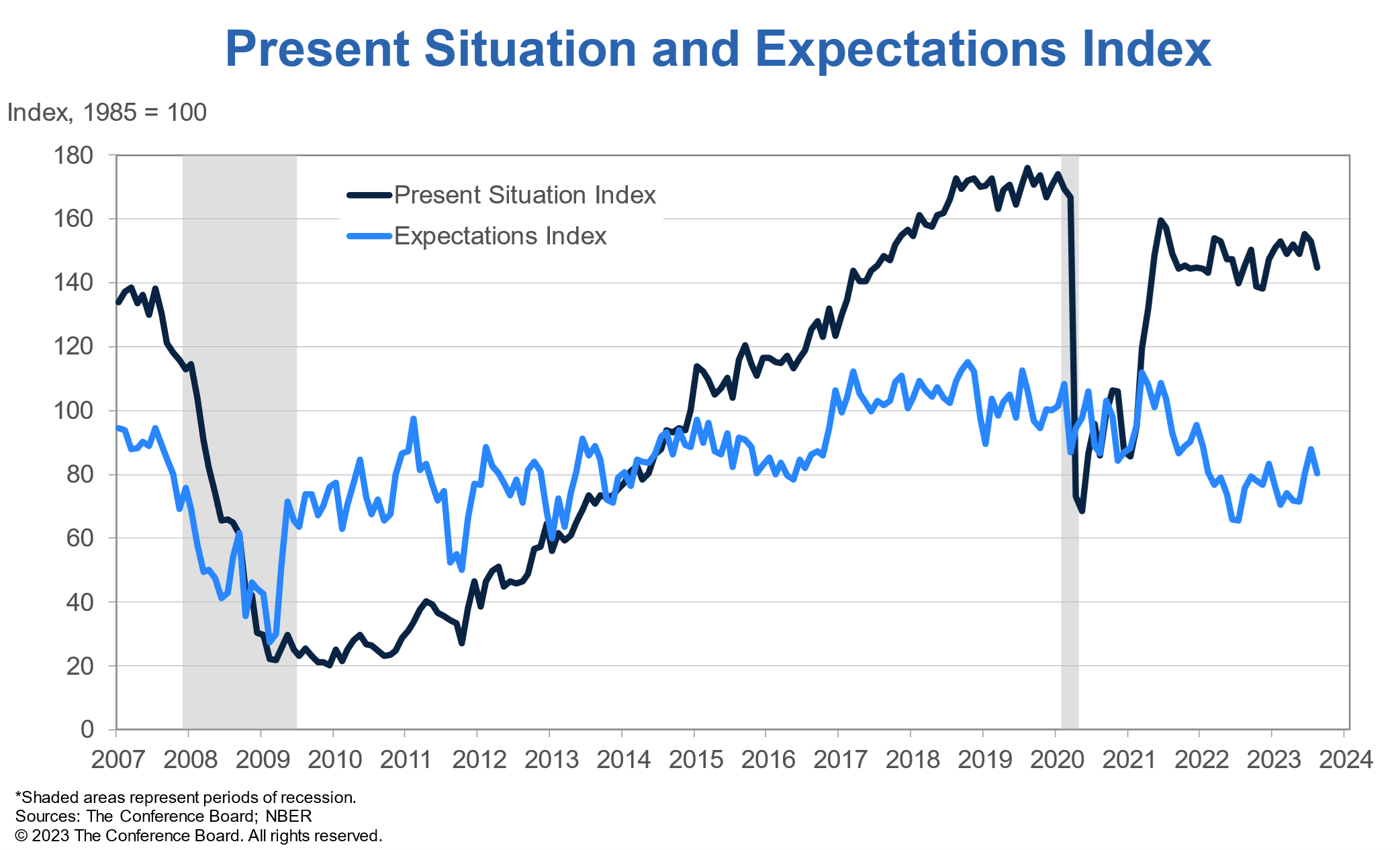

US consumer confidence fell to 106.1, expectations near recession threshold

US Conference Board Consumer Confidence fell from 114.0 to 106.1 in August, well below expectation of 116.5. Present Situation Index fell from 153.0 to 144.8. Expectations Index fell from 88.0 to 80.2.

Dana Peterson, Chief Economist at The Conference Board:

- "Consumer confidence fell in August 2023, erasing back-to-back increases in June and July."

- "Write-in responses showed that consumers were once again preoccupied with rising prices in general, and for groceries and gasoline in particular.

- "Assessments of the present situation dipped in August on receding optimism around employment conditions

- "Expectations for the next six months tumbled back near the recession threshold of 80, reflecting less confidence about future business conditions, job availability, and incomes."

Sunset Market Commentary

Markets

The economic calendar turned somewhat more interesting today but the most critical data points (US JOLTS job openings and Conference Board consumer confidence) unfortunately are scheduled for release after this report. We did receive the June US house prices in time. They rose for a fifth month in a row by 0.92% m/m, more than the 0.80% expected. The yearly measure still stood at a negative -1.17% but that was less than the -1.73% in May, thereby snapping a protracted decline that started in April 2022. Some German data is definitely worth mentioning as well, even as markets didn’t quite pick it up. The federal statistical office said wages in the country grew 6.6% in the second quarter, up from 5.6% in Q1 and the fastest pace since data collection began in 2008. With the latest inflation number (July) coming in at 6.5%, real wage growth was positive for the first time since 2021. With every further inflation deceleration (6.3% in August, according to consensus for Thursday’s publication), real wage growth turns more positive … potentially helping consumer spending to rebound … which could thwart the disinflationary process. It’s a catch 22 that requires a restrictive monetary policy for long enough to escape from.

Turning to FI and FX markets now. US yields dipped lower in Asian dealings with the front end again outperforming before hitting a bottom early in the European session. The 2-y yield, even though still losing about 2.7 bps, holds north of the symbolic 5% barrier. Other tenors moved higher before paring gains as the US entered. German yields showed a similar pattern with early (yet minor) losses being erased to trade more or less unchanged compared to yesterday’s close. The front underperforms. Gilts underperform global peers with UK yields adding 3.1-5.8 bps across the curve on the first UK trading day of the week. Sterling doesn’t profit with EUR/GBP hovering around opening levels in the 0.858 area. The dollar is trading with a minor strengthening bias, gaining against all G10 peers. EUR/USD flipped opening gains for losses to trade near the recent lows of 1.0786. The trade-weighted index rises from 103.95 to 104.33 and seems to be preparing for a new attack on the May high (104.7). USD/JPY already broke beyond previous resistance of 146.63, surging to 147.24.

News & Views

Czech GDP in the April-June quarter rose by 0.1% Q/Q, a more refined estimate of the Czech statistical office showed. Activity was still 0.4% lower Y/Y. Quarterly growth was supported by a 3.4% Q/Q growth in fixed capital formation as investments in transport equipment, ICT and other machinery and equipment gained rebounded. Dwelling investment and other buildings and structures decreased. Inventories contributed negatively. Final consumption expenditure rose 0.3% Q/Q. It was the first time in six quarters for this factor to contribute positively. Government consumption rose 0.3% Q/Q. Exports (-0.5% Q/Q) and imports (-1.2% Q/Q) both declined. The CNB on its website said that Q2 growth was slightly stronger than its latest projection (-0.7% Y/Y expected). It indicated that the modest quarter consumption growth was fostered by gradually decreasing inflation. Also gross fixed capital formation was better than CNB expected. The CNB states that the economy already emerged from a shallow recession. The koruna today trades little changed near 24.15. Czech money market rates hardly reacted. The Czech 2-y yield even eases marginally further to 5.38% as the market still sees a potential start of the CNB easing cycle in Q4. Czech Central bank governor Michl today reiterated that inflation is still at unacceptable high levels.

The National Bank of Hungary today as expected further reduced to overnight deposit rate to 14%. The official base rate was left unchanged at 13% as is this is seen as keeping monetary conditions sufficiently tight. MNB still expects that domestic CPI inflation and core inflation will continue to decrease at a rapid pace in coming months. It also sees real interest rates to move in positive territory soon. The NMB stressed the faster an expected improvement in the external balance. Looking ahead, the bank repeated that that financial market stability is key to achieving price stability. In the current environment, a cautious and gradual approach is warranted. At the press conference, Deputy Governor Virag also said that the MNB will simplify the MNB toolkit when the 1 day rate will be aligned with the base rate. The forint gains modestly after the decision to currently trade near EUR/HUF 382.15.

USD/JPY Breaks Above 147

The Japanese yen continues to lose ground on Tuesday. In the North American session, USD/JPY is trading at 147.26, up 0.50%. The yen broke above the 147 level for the first time since November 2022.

Tokyo says battle with inflation has reached turning point

Just a few days after Bank of Japan Governor Kazuo Ueda’s speech at the Jackson Hole summit, the Japanese government released a potentially significant white paper. To say that the two events were contradictory might be a stretch, but they appeared to present a very different stance towards inflation.

At Jackson Hole, Ueda stuck to the BoJ’s well-worn script that underlying inflation remains lower than the BoJ’s target of 2%. As a result, the BoJ has insisted it will stick with the current ultra-easy policy until there is evidence that inflation remains sustainably above target. The white paper sounded a different tone, noting that “Japan has seen price and wage rises broaden since the spring of 2022. Such changes suggest the economy is reaching a turning point in its 25-year battle with deflation” and “a window of opportunity may be opening to exit deflation.”

Could this be a turning point that leads to a tightening in policy? The government hasn’t acknowledged that deflation is over, despite the fact that core inflation has remained above the 2% target for 16 successive months. Wages are also on the rise after companies significantly bumped up employee wages earlier in the year.

The white paper spoke of the need to “eradicate the sticky deflationary mindset besetting households and companies”, but I wonder if the BoJ also suffers from the same mindset, even with inflation remaining above target month after month. Investors should remain on guard for a shift in central bank policy, especially if the yen continues to head towards the key 150 level.

USD/JPY Technical

- There is resistance at 147.19 and 147.95

- 146.30 and 145.10 are providing support

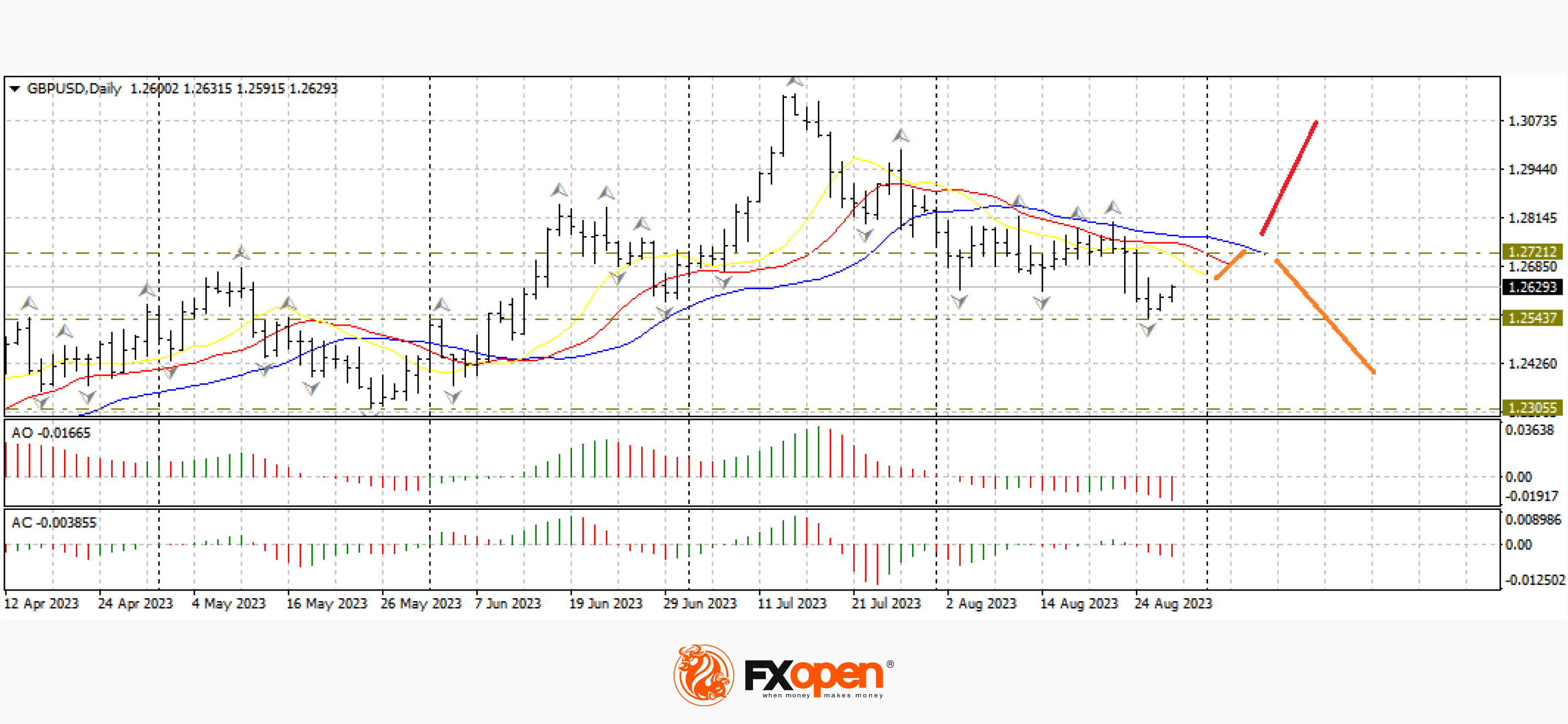

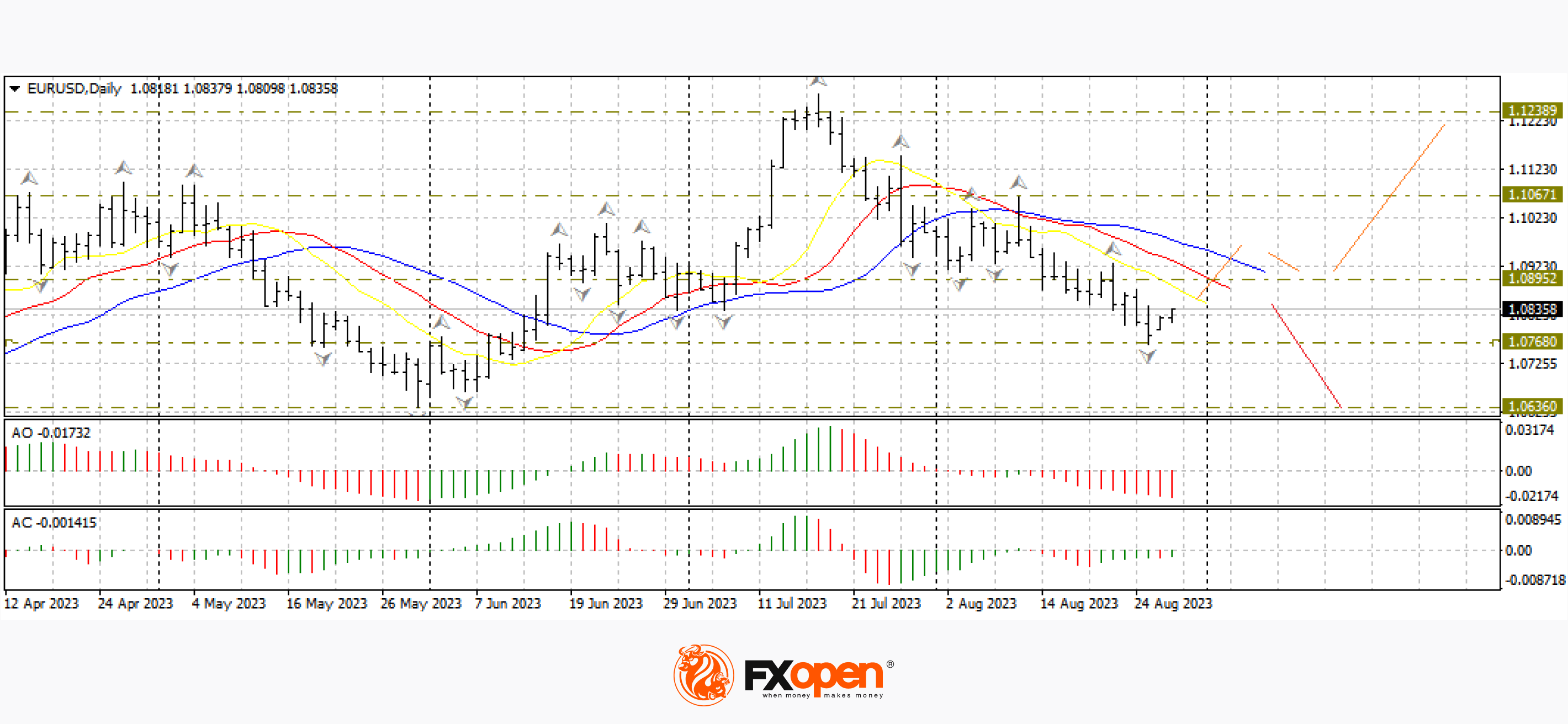

European Currencies Hit New Lows, Precious Metals on the Rise

European currencies, along with the yen and commodity currencies, came under pressure again last week. After Jerome Powell's hawkish talk at the Jackson Hole symposium, GBP/USD fell below 1.2600, EUR/USD broke support at 1.0800, and USD/JPY came close to 2023 extremes near 147. In the event of a breakout of these levels, the upward movement of the USD may increase sharply, which will lead to exponential growth. Conversely, a rebound from current levels could lead to a full-blown correction in almost all directions.

GBP/USD

The British currency, which is sensitive to the risky mood of market participants, broke through important support at 1.2600 last week and set a new August low at 1.2540. Jerome Powell's statements about the Fed's readiness to further raise the rate, if necessary, sharply strengthened the dollar, contributing to the collapse of GBP/USD. Nevertheless, at the beginning of the current five-day trading period, buyers of the pound managed to return the pair above 1.2600 and at the moment they intend to test 1.2700. If bulls meet serious resistance near the range of 1.2600-1.2700, another downward impulse may occur, the target of which will be a test of 1.2400-1.2200. If the pair gains a foothold above 1.2700, the resumption of growth to 1.3000-1.3100 may happen.

EUR/USD

The EUR/USD currency pair managed to get back above 1.0800 despite the break of this support last week. The pair's downward momentum is not as strong as in the case of the pound, and if the current situation does not change, euro buyers may be able to seize the initiative and test 1.0900 again. This level is very important for further pricing of the pair. A sharp rebound from this resistance could help bears break 1.0700 and move down towards 1.0600-1.0500.

From the point of view of fundamental analysis, today at 13:00 GMT+3, we are waiting for the publication of economic forecasts for the European Union. At 17:00 GMT+3, traders will pay attention to the data on the US CB consumer confidence for August.

XAU/USD

Despite a sharp increase in the US dollar last week, precious metals managed to find significant support and form reversal bullish combinations on higher timeframes. So, in the XAU/USD pair, we observe a bullish reversal bar near 1,900.00. The behaviour of the price at the nearest resistance, which is located near the alligator lines on the daily timeframe, will be important for the development of a further upward correction.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.