Sample Category Title

RBA Bullock sets eyes on inflation, signals possibility of further rate hikes

Incoming RBA Governor Michele Bullock made clear her primary focus would be tackling the country's persistently high inflation. As Bullock prepares to take the helm of RBA on September 18, replacing her current role as deputy governor, her comments carry considerable weight for markets and policymakers alike.

"My first priority is to keep very focused on inflation. Inflation is still too high in Australia. It is coming down and we're forecasting it to continue to come down, but it's still too high," said Bullock.

While she stopped short of providing a timeline for how long interest rates may remain elevated, Bullock did hint at the possibility of additional hikes in the future.

"I'm reluctant to give any sort of predictions on how long interest rates might have to stay high. In Australia's case, all I can say is that we might have to raise interest rates again, but we're watching the data very carefully," she said.

Additionally, Bullock clarified that rate-setting decisions would, for the time being, be made on a "month-by-month"" basis until at least next year.

USD/JPY Rate Updates the High of the Year

Yesterday, USD/JPY hit 146.74 for the first time since November 2022. The rise in the rate is facilitated by the growing gap in the policies of central banks: while the Bank of Japan has kept the rate below zero since 2016, the Fed has been raising rates since the spring of 2022.

Moreover, on Friday, Powell said the Fed is ready to continue to remain tough in the fight against inflation. According to CME's FedWatch tool, there is now a 62% chance of a rate hike at the Fed's November meeting, up from 42% a week earlier.

However, the limiting factor for the USD/JPY rate is the power of the Japanese Ministry of Finance. Last year, when the market was at current levels, the authorities intervened in the foreign exchange market, lowering the rate to 140 yen per US dollar.

The USD/JPY chart shows that:

→ the price continues to move within the ascending channel;

→ on Friday, during Powell's speech, the median line was tested, confirming its influence as a support;

→ former resistance at 144.8 also provides support;

→ if the trend continues, the rate may reach the upper limit of the channel — that is, the psychological mark of 150 yen per US dollar.

However, if we analyze the progress of the bulls when reaching the tops, then we can assume that the bullish momentum is depleted: after all, bullish candles do not have a wide body when they reach the highs, but on the contrary, they shrink. For sure, the strength of buyers is limited by fears of new interventions. Therefore, it is possible that a series of cautious renewal of the highs of the year may be interrupted when the Japanese authorities have their say.

According to analysts at Goldman Sachs, the yen may weaken to 155 per US dollar if the Bank of Japan continues to adhere to its ultra-soft position.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

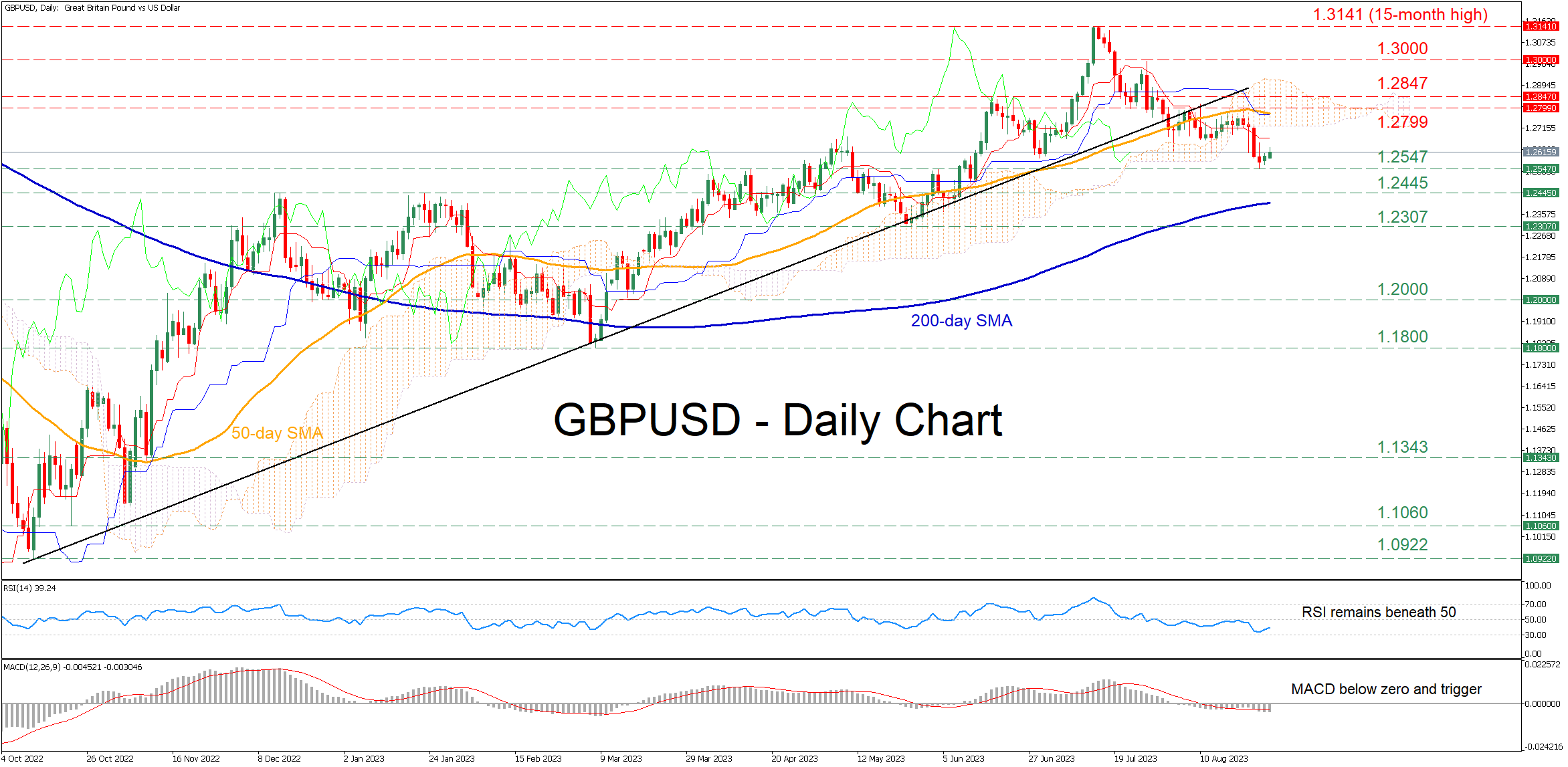

GBPUSD Attempts Rebound from 2-month Low

GBPUSD had been in a prolonged uptrend since October 2022, storming to a fresh 15-month high of 1.3141 on July 14. However, since then, the pair has been experiencing a prolonged downside correction, with the price falling to a fresh two-month low of 1.2547 last Friday before recouping some losses.

The short-term oscillators currently suggest that near-term risks are tilted to the downside. Specifically, the RSI is positively charged but remains well within the negative zone, while the MACD is found below both zero and its red signal line.

Should the bears attempt to push the price lower, the recent two-month bottom of 1.2547 could act as immediate support. Failing to halt there, the pair might extend its retreat towards the December-January resistance zone of 1.2445, which could serve as support in the future. Even lower, the May bottom of 1.2307 may provide downside protection.

On the flipside, if the pair manages to halt its retreat and storm back higher, the bulls could attack the recent resistance of 1.2799. Breaking above that zone, the pair could advance towards the June peak of 1.2847 before the 1.3000 psychological mark appears on the radar. A violation of territory could pave the way for the 15-month peak of 1.3141.

In brief, it seems that the GBPUSD’s pullback is starting to lose steam, but it’s too early to call for a reversal. Nevertheless, the short-term decline could accelerate in the case that the pair records a fresh lower low.

EURJPY Eyes Recent Peak, But Will the Uptrend Resume?

EURJPY climbed back above its 20-day simple moving average (SMA), aiming to push its 2023 uptrend above last week’s high of 159.47.

The upward-sloping SMAs promote the positive trend in the market, but the technical oscillators can't warrant stronger bullish momentum in the coming sessions. The RSI is maintaining a negative trajectory above its 50 neutral mark despite pivoting higher recently, while the MACD keeps hovering below its red signal line, indicating some skepticism in the market.

Nevertheless, if the bulls take over the 159.50 bar and the short-term resistance line from June, the price might revisit the 161.35-162.50 zone, where it struggled at the end of August 2008 and peaked in August-October 1998. A close higher could then target the tentative ascending line from January 2023 seen around 163.80-164.00.

Alternatively, a pullback below the 20- and 50-day SMAs at 157.85 and 156.80, respectively, may confirm additional losses towards the tentative support trendline at 154.45. An extension lower may stabilize somewhere between 151.30 and 152.00. If the sell-off continues, the door will open for the 150.00 psychological number.

In brief, EURJPY's short- and medium-term bullish structure provides safeguard, but it's still uncertain if there are enough buyers to upgrade the market's outlook above the 159.50 ceiling.

EUR/USD Forming a Wedge

EURUSD came down as expected to a new low after wave 4 corrective rise so price is now seen in late stages of a leading diagonal in (A). Therefore, Euro can see limited weakness and slow price action in days ahead but only if that's a throw-over formation. In either case, we think that a higher degree of bearish correction is still underway and that pair can trade much lower after wave B rally which can retest higher resistance, near 1.0930-1.1060. However, we will once again turn bullish on the euro once the corrective A-B-C drop comes to an end, but at the moment that's clearly not the case yet.

USD Holds Steady

USD/CAD tests major ceiling

The US dollar remains firm as traders expect resilient data later this week. On the daily chart, the price is probing last May’s double top near 1.3650, a major ceiling that so far has capped the greenback’s advance. Its breach would signal that the bulls are back in the game and stronger than ever, with October 2022’s peak of 1.3900 as a potential target later on. As the daily RSI shows an overextension, a pullback would be a test of the bulls’ resolve with 1.3570 as the first support and 1.3500 on the 20-day SMA as a second layer.

AUD/USD seeks to bottom out

The Australian dollar clawed back some losses after July’s retail sales exceeded expectations. The pair is looking to stabilise around its 9-month lows near 0.6370 with a preliminary bounce above 0.6480 pushing a few short interests out of the way. The former demand zone 0.6490-0.6500 from May’s low coincides with the 20-day SMA and is a major resistance to lift to instil confidence and open the door to a broader rebound to 0te.6610. On the flip side, a slip below 0.6370 would trigger a new round of sell-off towards 0.6200.

UK 100 probes resistance

The FTSE 100 recoups some losses as commodity prices register some upticks. The index so far has found support in the demand zone near the July low of 7240, offering the bulls some relief. Still, they are not out of the woods yet as the latest bounce could be due to short-term sellers’ profit-taking with support of a little bargain hunting. The demand-turned-supply zone of 7420 next to the 20-day SMA would be their first real test and a bullish breakout may extend gains to 7550. But a fall below 7300 may cause a reversal to 7000.

Dollar Taking a Breather on its Protracted Rally

Markets

With little economic data in the way, the first trading session post-Jackson Hole mainly yielded order-driven and technically inspired trading. Fed Chair Powell reiterating the ‘higher for longer mantra’ didn’t change investors’ assessment in any profound way. At the short end of the curve, the US 2-y touched 5.10% at the start of US dealings, but the cycle top (5.1175%) was left intact. Bonds gradually rebounded. The intra-day price dynamics was reinforced by a solid $ 46 bln 2-y US Treasury action. The subsequent 5-y note auction was ok. At the end of the day, US yields ceded between 3.75 bps (5-y) and 0.7 bps (30-y). German yields added between 3.1 bps (2-y) and 0.3 bps (10-y). ECB Holzmann advocated a front-loading approach to reach the peak cycle rate sooner rather than later. However, his comments had limited impact on trading. EMU inflation data to be published later this week will be key to guide the debate whether or not the ECB should consider a pause in its hiking cycle at the September 14 meeting. Equity investors apparently felt comfortable with the post-Jackson Hole status quo on interest rate markets. The S&P500 gained 0.63%. After a poor post-PMI performance last week, the Eurostoxx 50 yesterday even outperformed, gaining 1.36%. On FX markets, the dollar is taking a breather on its protracted rally since mid-July. The DXY index yesterday closed just north of the 104 big figure (open 104.17). For now, a real attack/break of the 104.7 end May top apparently is difficult without additional strong US data and/or markets pricing in a bigger chance for a 25 bps September 21 Fed rate hike than is currently the case (+/-25%). EUR/USD (1.0819) succeeded a close north of 1.08 after testing the 1.0766 area last week. Still the picture remains fragile. The yen for now still isn’t able to profit from any USD softness with USD/JPY still closing at 146.54 after setting a minor YTD top earlier yesterday. London markets were closed.

Asian equity markets mostly trade in positive territory joining yesterday’s WS rebound. Measures to support markets announced in China yesterday maybe also still play a role. US Treasuries show a tentative bid. Dollar is losing slightly (DXY 103.94; EUR/USD 1.0825). The calendar in Europe still only contains second tier data. The US is more interesting with house price data, JOLTS job openings, consumer confidence (Conference Board) and a $35 bln 7-y Treasury auction. We don’t expect markets to break any important levels with key US data (ADP, payrolls, manufacturing ISM) and EMU inflation data to be published later this week. 4.89% is first support for the US 2-y yield. On FX the picture stays USD constructive as long as the DXY 103 area holds. Also keep an eye at the ongoing topside test in USD/JPY.

News and views

The British Retail Consortium-Nielsen’s shop price index eased further in August. Prices rose 6.9% y/y, down from 7.6% in July and the 9% series high in May this year. Food led the decline, in particular meat, potatoes and cooking oils. While grocery prices still rose 11.5%, it was less than the 13.4% last month and the slowest since September 2022. “The unpredictable weather of recent weeks has dampened consumer demand with some high street retailers increasing promotional activity and food retailers continuing to extend price cuts,” head of retailer and business insight at NielsenIQ Mike Watkins said. Today’s numbers are a welcome development for the Bank of England though offer no room for complacency with official inflation still being well over triple the 2% target. UK money markets currently price in at least two more hikes to 5.75%. Sterling this morning ekes out a small gain (EUR/GBP 0.8575).

The Japanese government in its annual economic white paper said the country finds itself at an “inflection point” in its battle with 25 years of deflation. It referred to signs of broadening price and wage rises in an echo of the Bank of Japan, which said that price- and wage-setting behaviour was changing. In last year’s edition, the government said inflation was modest except for some food and energy-related goods. Now, it pointed to a “still moderate pace” of service price increases while at the same time highlighting the importance of it since they reflect domestic demand and wages more than goods prices do. Official Japanese inflation numbers hit 3.1-4.3% depending on the gauge in July, the highest in four decades. For the government to officially declare an end to the in 2001 introduced state of deflation, it not only needs to see underlying price rises but also clear signs that Japan won’t return to periods of price drops.

Euro Underperforms Amid Weak German Consumer Sentiment; Gold Gains Momentum

Euro is trading lower across the board today, additionally dragged down by weaker-than-expected consumer sentiment data out of Germany. This latest indicator has added fuel to concerns that Eurozone's largest economy may become a drag on the broader region, heightening risk of a looming recession. Meanwhile, Dollar and Swiss Franc also demonstrated weakness, but this appears to be more related to a mildly positive risk sentiment permeating the market.

In contrast, Australian and New Zealand Dollars are holding their ground as relatively better performers, followed by British Pound. Yen displayed mixed performance; although Japan's unemployment rate rose, the currency hasn't shown any clear recovery momentum.

Market participants should expect subdued trading conditions to continue for the day, particularly due to an empty economic calendar in Europe. However, upcoming US consumer confidence data could serve as a potential catalyst to awaken market activity.

On the technical side, Gold is attempting to build momentum for an extension of its rebound from 1884.83. For now, further upside appears likely as long as 1902.57 minor support holds. Sustained trading above falling trendline resistance (now at 1949) would strengthen the case that whole correction from 2062.95 has completed, and bring further rally to 1987.22 resistance confirmation.

Based on current market developments, extended rally in Gold might not necessarily mean selloff in Dollar. But that could still be seen as a sign of capped momentum for the greenback.

In Asia, Nikkei closed up 0.18%. Hong Kong HSI is up 2.00%. China Shanghai SSE is up 1.12%. Singapore Strait Times is up 0.34%. Japan 10-year JGB yield is down -0.0139 at 0.654. Overnight, DOW rose 0.62%. S&P 500 rose 0.63%. NASDAQ rose 0.84%. 10-year yield dropped -0.0027 to 4.212.

German consumer sentiment slides to -25.5, dashing hopes for a late-year recovery

Consumer sentiment in Germany continues to languish as the GfK Consumer Sentiment Index for September slipped to -25.5, missing market expectations of -24.3 and marking a decline from last month's -24.6.

"The consumer sentiment is currently not showing a clear trend, neither downward nor upward – and that at a very low level overall," stated Rolf Bürkl, consumer expert at GfK.

Adding to the gloom, Bürkl warned, "The chances that consumer sentiment can sustainably recover before the end of this year are dwindling more and more."

He cited "persistently high inflation rates, especially for food and energy supplies," as the main obstacles hindering any meaningful advance in consumer sentiment.

The sub-components of the index painted an equally disheartening picture. Economic expectations in August plummeted from 3.7 to a worrying -6.2, marking the lowest level since last December's -10.3. Meanwhile, income expectations saw a significant drop from -5.1 to -11.5. The propensity to buy, another crucial sub-index, also declined, falling from -14.3 to -17.0.

Japan's unemployment rate up to 2.7%, first rise in four months

Japan's job market showed unexpected signs of weakening in July, as the unemployment rate rose to 2.7%, defying expectations of remaining steady at June's 2.5% level. This marks the first uptick in unemployment in four months. The data reveals that the number of employed workers decreased by -100k during the month, while the ranks of those without jobs swelled by 110k.

Adding to the concern, jobs-to-applicants ratio—a leading indicator of labor market health—dipped to 1.29 in July from 1.30. This is the third consecutive monthly decline, counter to median economist forecasts that predicted the ratio would remain flat. These figures indicate that there were only 129 job openings for every 100 applicants, a metric that is closely watched for signs of labor market tightness or slack.

Looking ahead

US house price index and consumer confidence will be released later in the day.

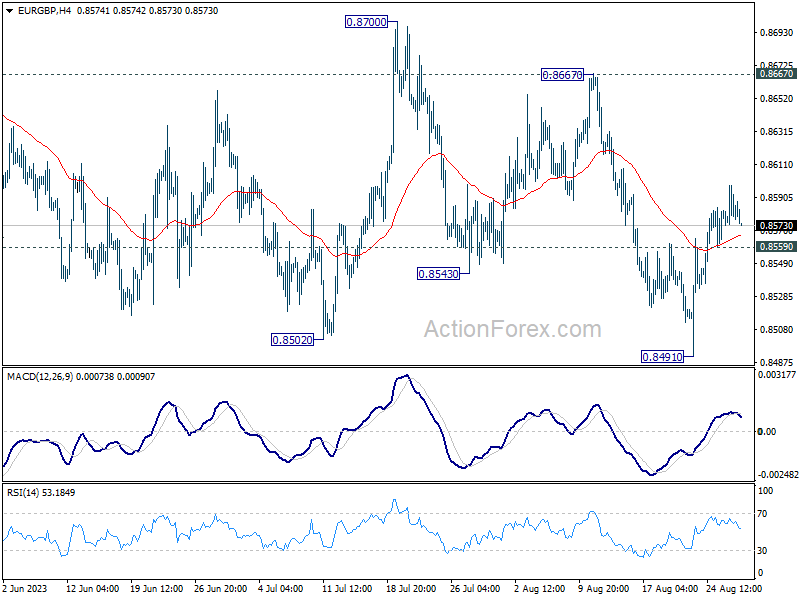

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8548; (P) 0.8573; (R1) 0.8586; More...

Intraday bias in EUR/GBP is turned neutral first with 4H MACD crossed below signal line. Overall outlook stays bearish with 0.8667 resistance holds. On the downside, below 0.8559 minors support will turn bias to the downside for retesting 0.8491 low first. Firm break there will resume larger down trend.

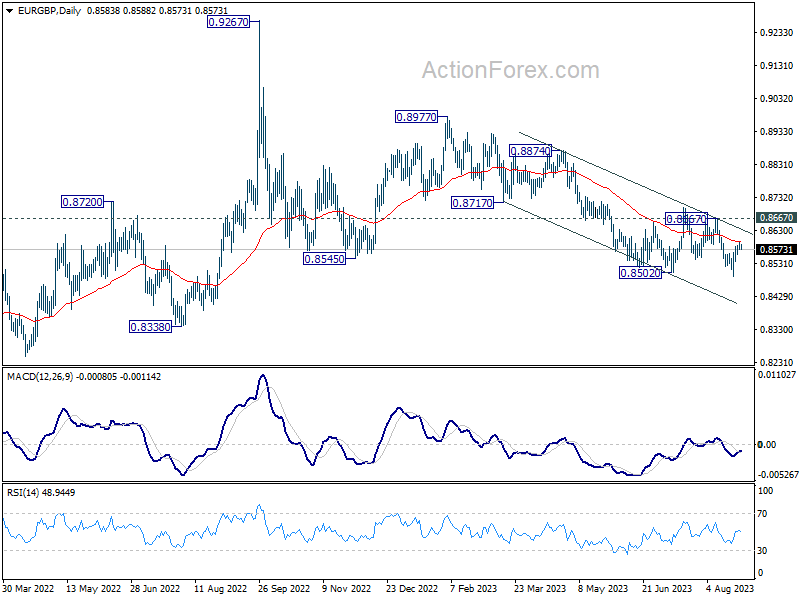

In the bigger picture, the down trend from 0.9267 (2022 high) is seen as part of the long term range pattern from 0.9499 (2020 high). Further decline is in favor as long as 0.8667 resistance holds. Break of 0.8502 will resume the fall towards 0.8201 (2022 low).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Unemployment Rate Jul | 2.70% | 2.50% | 2.50% | |

| 06:00 | EUR | Germany Gfk Consumer Sentiment Sep | -25.5 | -24.3 | -24.4 | -24.6 |

| 13:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y Jun | -1.50% | -1.70% | ||

| 13:00 | USD | Housing Price Index M/M Jun | 0.20% | 0.70% | ||

| 14:00 | USD | Consumer Confidence Aug | 116.5 | 117 |

Calm Before the Storm?

The week started in a relatively good mood. The S&P 500 posted its first back-to-back gains this month, even though the US 2-year yield advanced to a fresh high since July with the 2 and 5-year treasury auctions hitting the highest yields since before the 2008 crisis. One would think that the Chinese stimulus measures have lifted up the sentiment across global equities, but the CSI 300 closed yesterday just around 1% higher. In this sense, yesterday was just another day the Chinese stimulus measures didn’t get the attention Chinese officials were hoping for. And that’s the new normal. Before 2020, any stimulus news from China would move oceans, but now, China can cut rates, inject liquidity, half stamp duty, prevent big names from becoming net sellers… nothing is enough to bring investors back apart from a massive fiscal stimulus. And the chances are that, China won’t do that, because Xi doesn’t want to explode the national debt levels – which are already alarmingly high – to kick start another unsustainable growth in China. That’s not bad in the long run, but it sure costs China a lot of investment. MSCI’s EM ex-China ETF has outperformed the MSCI China since the beginning of the year and the trend in Chinese equities, and the latest surveys hint at around 5% growth in 2023, in line with the government’s growth target, but not enough to bring money on board.

Focus on US growth and jobs data

The softer US dollar gave some breathing room to other currencies yesterday. The EURUSD bulls won a battle near the 200-DMA, and the pair is slightly above that level this morning, while the USDJPY is steady around 146.50. Crude oil steadied above the $80pb with the news that the tropical storm Idalia could interrupt crude production in the Gulf Coast and put an additional short-term pressure on oil prices. Gold is better bid above the $1900 thanks to a retreat in the US 10-year yield.

Today, the US JOLTS data is expected to post a third month below 10mio job openings. A number lower than expectations would point to loosening jobs market and could soften the hawkish Federal Reserve (Fed) expectations, while a strong figure will keep the economists and the Fed officials in a state of confusion. It is now increasingly certain that the Covid disruption in jobs market has largely passed, which means that the fact that the jobs figures remain resilient to rate hikes is due to another reason! And that reason could be the aging population. Looking at the CBO projections, the participation rate in the US is not at shocking levels compared to the long-term projections. On the contrary, the actual participation rate (62.6%) is even higher than the long-term projection (62.4%).

Strong jobs figures have potential to boost Fed hawks as tightness of the jobs market means people ask for more money for doing the same job than they would otherwise.

Slow Start to a Busy Week

Market movers today

We get some interesting US data today. The JOLTS data will provide more key information on the labour market and so will the consumer confidence numbers from Conference Board, which contain the jobs plentiful vs. hard to get indices.

US house prices are also due and have been surprisingly strong lately. However, we may see prices cool down again following the recent sharp increases in mortgage rates.

In the Nordics we get Swedish GDP (see more below).

The 60 second overview

Markets. While this week will bring plenty of key data releases - most notably the US non-farm labour market report on Friday and Eurozone inflation on Thursday - markets have been off to a slow start since the weekend. Stabilisation in Chinese markets on the back of a stamp duty reduction seems to have calmed global risk appetite. That said, global equity indices still look set for the worst calendar-month this year.

Overnight most Asian equity indices are trading in green while US yields have come a little lower leaving 2Y treasury yields now just below 5.00%. Japanese unemployment showed a slightly surprising increase although from very low levels. The Japanese labour market remains very tight and we still think Japanese authorities underestimate the underlying inflation pressures.

In the near-term, we expect US activity data to perform better than those in the Eurozone. Markets will hope for a sweet spot in economic releases. That is, on the one hand, the global economy must not do too well as this is likely to trigger additional monetary tightening. On the other hand, it must also avoid an outright recession or sharp growth slowdown for risky assets not to suffer. Following last week's PMI releases the balance of risk for now seems skewed towards a higher recession probability.

We maintain the call that we have seen the peak in US policy rates whilst we still lean - not much more than that - towards a final 25bp rate hike from the ECB in September.

Equities: Investors continued in a buoyant manner on Monday. Jackson Hole lingered in focus, as the macro agenda was thin and hence the drivers were the same as Friday. Equities grinded higher in US and Europe caught up. S&P500 rose 0.6%, Stoxx 600 0.9% and Nordics bounced a full 1.4%, on track to recoup some of last months' losses. It was a risk-on session, with growth, cyclicals and small caps outperforming. In the Nordics, this translated into EQT, Volvo and Sandvik being the stocks on top, after being the worst performing stocks the last month. Asian markets are a notch higher this morning and US futures indicate a mildly positive opening too.

FI: US Treasury yields ended Monday with a modest decline in yields across the yield curve. This has continued this morning in the Asian trade and the 2Y US Treasury yield is now below 5%. There was also a modest decline in the longer-dated European government bond yields, where the periphery outperformed the core-EU government bonds.

FX: Yesterday's session was dominated by a relief rally to China and industrials exposed currencies such as SEK, AUD and EUR. EUR/USD rebounded slightly above 1.08 while EUR/SEK dropped back below the 11.90 mark. EUR/NOK remains in the 11.50s range while EUR/GBP keeps hovering around the 0.858-mark. USD/JPY remains at yearly highs just above 146.

Credit: Credit markets started the week with a significant number of new primary deals announced throughout Europe. In Scandi space Danske Bank acted as lead manager on Länsförsäkringar Bank AB's new Senior Non-Preferred Green bond as well as on Lifco AB's Senior Unsecured issue. Overall, we expect a continued busy primary market in the coming days. Due to the high primary activity the secondary market was relatively muted with iTraxx Main 1bp tighter at 74bp while iTraxx Xover was 2bp tighter at 413bp.

Nordic macro

Sweden: Today focus is on Q2 GDP (released 08.00 CET) and market expectations are very depressed (-1.3 % qoq sa) which is very close to the reading of the (non-official) GDP indicator (-1.5 % qoq sa). We expect a less negative -0.5 % as consumption appears to have bottomed out and employment has continued its upward trend. As shown in the most recent issue of Reading the Markets Sweden, 25 August, the GDP indicator is very volatile and often revised significantly. We also find it strange that Sweden should deviate to such an extent form positive GDP reading in other Nordic and export markets. To be sure, residential construction remains a severe drag on growth. July trade balance and retail sales are also released this time.

Deputy Governor Bunge speaks about the economic outlook and monetary policy 09.30 CET. Expect a similar message as Flodén's yesterday, i.e. more hikes coming (we anticipate one more though).