Sample Category Title

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0773; (P) 1.0801; (R1) 1.0812; More...

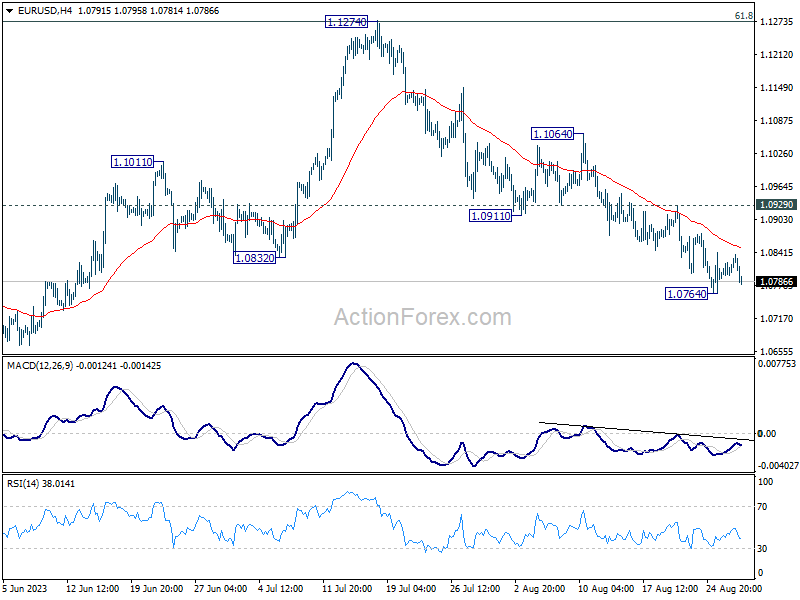

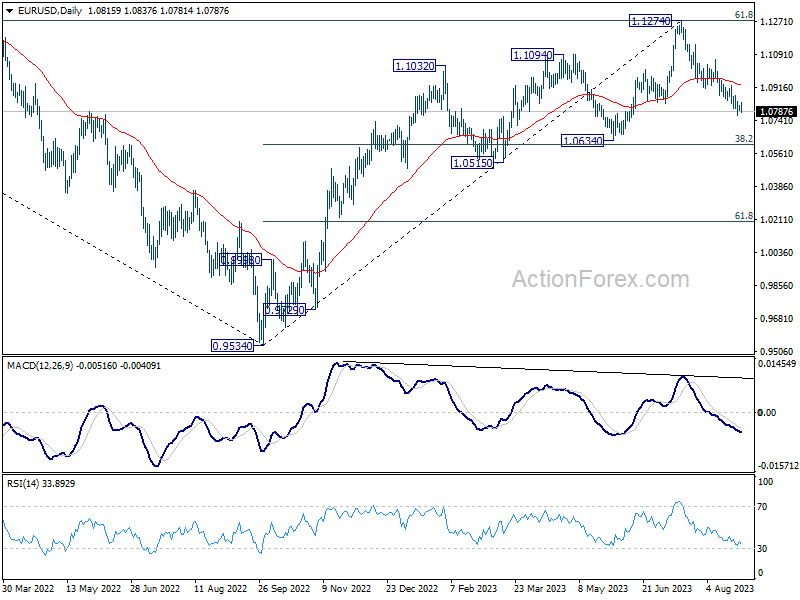

EUR/USD is still bounded in consolidation above 1.0764 and intraday bias stays neutral. Outlook stays mildly bearish as long as 1.0929 resistance holds. Below 1.0764 will resume the fall from 1.1274 to 1.0609/34 cluster support next.

In the bigger picture, fall from 1.1274 medium term top is seen as a correction to up trend from 0.9534 (2022 low). Deeper decline would be seen to 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609). Strong support could be seen there, at least on first attempt, to bring rebound. Yet, medium term outlook will be neutral for now, as long as 1.1274 resistance holds.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2531; (P) 1.2576; (R1) 1.2593; More...

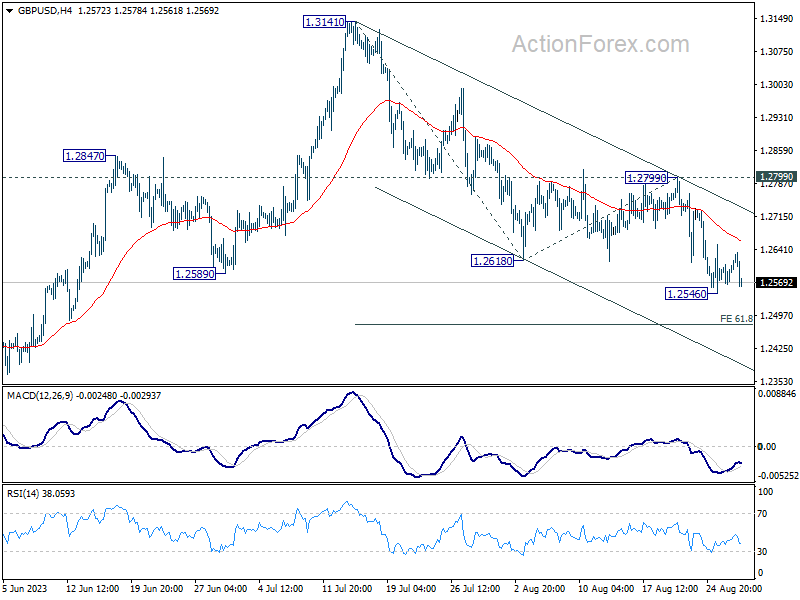

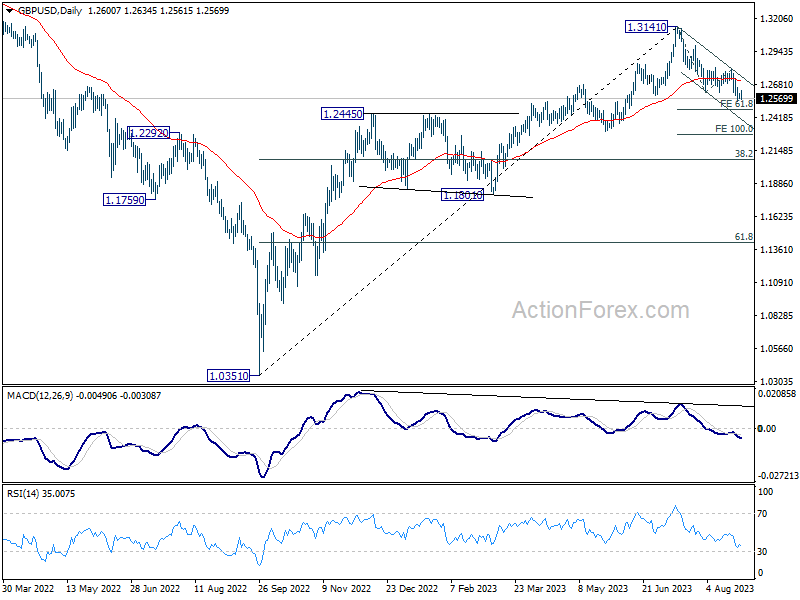

Intraday bias in GBP/USD stays neutral as consolidation continues above 1.2546. Near term outlook remains mildly bearish as long as 1.2799 resistance holds. On the downside, break of 1.2546 will resume whole fall from 1.3141 to 61.8% projection of 1.3141 to 1.2618 from 1.2799 at 1.2476. Firm break there could prompt downside acceleration to 100% projection at 1.2276.

In the bigger picture, for now, fall from 1.3141 medium term top is seen as a correction to up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3141 at 1.2075. Strong support would be seen there to bring rebound on first attempt. But outlook will be neutral at best as long as 1.3141 resistance holds, and consolidation from there is set to extend, until further development.

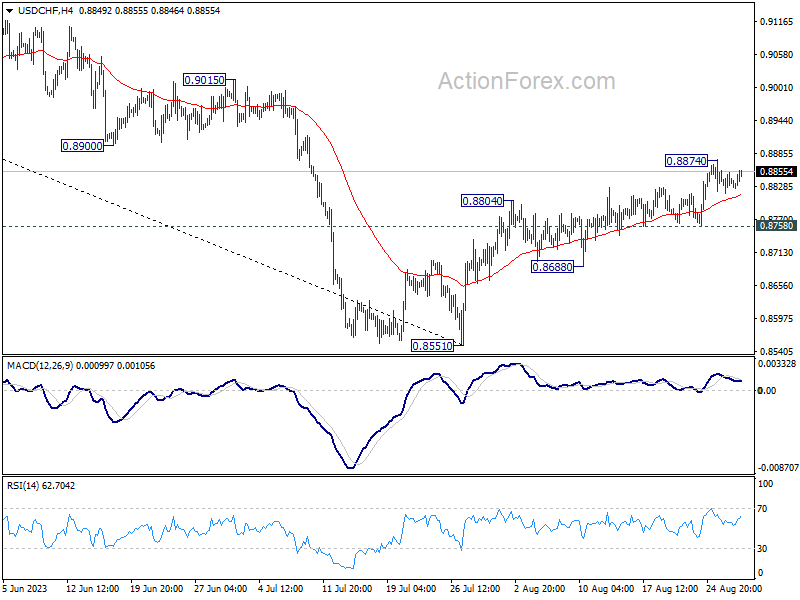

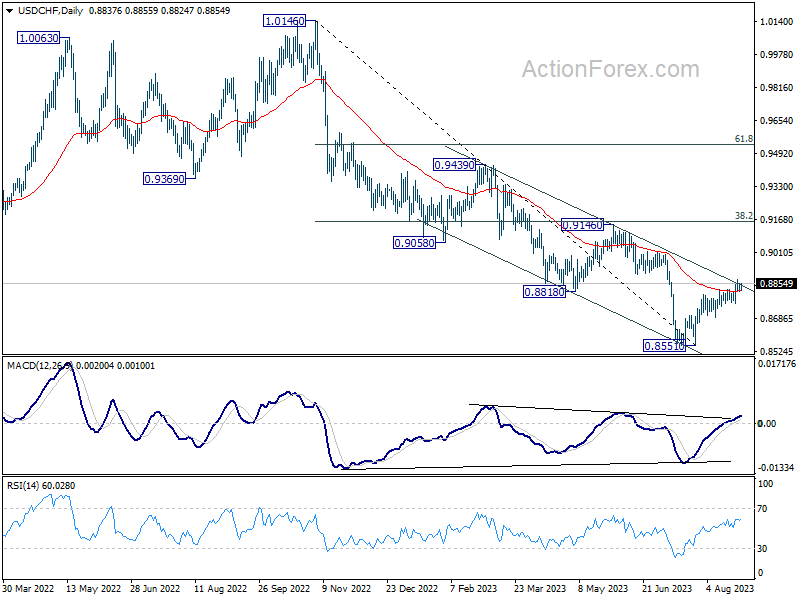

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8779; (P) 0.8819; (R1) 0.8839; More....

USD/CHF is still extending the consolidation pattern below 0.8874 and intraday bias stays neutral at this point. Further rally is expected as long as 0.8758 support holds. On the upside, break of 0.8874 will resume the rise from 0.8551 to 0.9146 cluster resistance next.

In the bigger picture, rebound from 0.8551 medium term bottom is currently seen as a correction to the downtrend from 1.0146 (2022 high). Further rally would be seen to 0.9146 cluster resistance (38.2% retracement of 1.0146 to 0.8551 at 0.9160). Strong resistance could be seen there to limit upside, at least on first attempt. Nevertheless, medium term outlook is neutral at best as long as 0.8551 holds, until further developments.

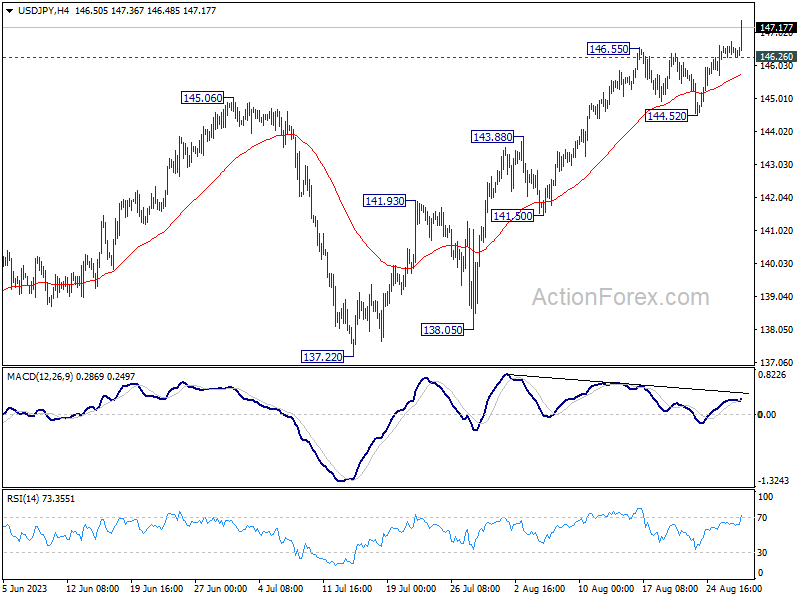

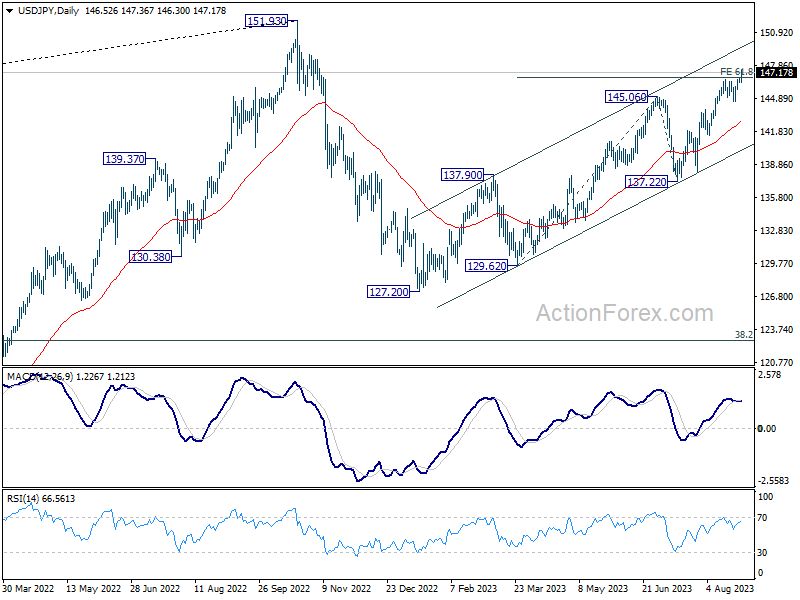

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 145.83; (P) 146.30; (R1) 146.52; More...

USD/JPY's rally accelerates to as high as 147.63 today so far. The strong break of 61.8% projection of 129.62 to 145.06 from 137.22 at 146.76 indicates solid underlying momentum. Intraday bias stays on the upside, and the rise from 127.20 should target a test on 151.93 high. On the downside, below 146.26 minor support will turn intraday bias neutral first. But near term outlook will remain mildly bullish as long as 144.52 support holds.

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Rise from 127.20 is seen as the second leg of the pattern and could still be in progress. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.

USD/JPY Hits Year-High in Subdued Markets

In a relatively uneventful trading day, the notable standout is the rally in the USD/JPY currency pair, which has now reached its highest level this year. The bullish momentum for Dollar against Yen raises questions about whether traders are positioning themselves ahead of crucial employment and inflation data set to be released from the US this week. An upside surprise in either of these indicators could add fuel to expectations for another Fed rate hike this year, even if not as soon as September. Meanwhile, Japanese Yen is facing some headwinds following a higher-than-expected unemployment rate in Japan, which has undoubtedly put some pressure on the currency.

On the flip side, despite hawkish comments from incoming RBA Governor Michele Bullock, Australian Dollar is showing signs of weakness. Its near-term recovery appears to be stalling, raising prospects for further downside. Market participants will closely watch the upcoming monthly CPI data from Australia to gauge the currency's direction. New Zealand Dollar trails as the third weakest for the day, while Swiss Franc and Canadian Dollar claim spots as the second and third strongest currencies, respectively. Both Euro and Sterling are delivering a mixed performance.

On the technical front, focus will shift to whether the U.S. Dollar's rally can gain broader momentum. Key levels to keep an eye on include a temporary low of 1.076 in EUR/USD, 1.2546 in GBP/USD, and a temporary top of 0.8874 in USD/CHF. Simultaneous break of these levels could firmly set the Dollar's tone leading into the highly anticipated non-farm payroll report due on Friday.

In Europe, at the time of writing, FTSE is up 1.44%. DAX is up 0.20%. CAC is up 0.27%. Germany 10-year yield is down -0.0114 at 2.571. Earlier in Asia, Nikkei rose 0.18%. Hong Kong HSI rose 1.95%. China Shanghai SSE rose 1.20%. Singapore Strait Times rose 0.29%. Japan 10-year JGB yield dropped -0.0210 to 0.647.

RBA Bullock sets eyes on inflation, signals possibility of further rate hikes

Incoming RBA Governor Michele Bullock made clear her primary focus would be tackling the country's persistently high inflation. As Bullock prepares to take the helm of RBA on September 18, replacing her current role as deputy governor, her comments carry considerable weight for markets and policymakers alike.

"My first priority is to keep very focused on inflation. Inflation is still too high in Australia. It is coming down and we're forecasting it to continue to come down, but it's still too high," said Bullock.

While she stopped short of providing a timeline for how long interest rates may remain elevated, Bullock did hint at the possibility of additional hikes in the future.

"I'm reluctant to give any sort of predictions on how long interest rates might have to stay high. In Australia's case, all I can say is that we might have to raise interest rates again, but we're watching the data very carefully," she said.

Additionally, Bullock clarified that rate-setting decisions would, for the time being, be made on a "month-by-month" basis until at least next year.

German consumer sentiment slides to -25.5, dashing hopes for a late-year recovery

Consumer sentiment in Germany continues to languish as the GfK Consumer Sentiment Index for September slipped to -25.5, missing market expectations of -24.3 and marking a decline from last month's -24.6.

"The consumer sentiment is currently not showing a clear trend, neither downward nor upward – and that at a very low level overall," stated Rolf Bürkl, consumer expert at GfK.

Adding to the gloom, Bürkl warned, "The chances that consumer sentiment can sustainably recover before the end of this year are dwindling more and more."

He cited "persistently high inflation rates, especially for food and energy supplies," as the main obstacles hindering any meaningful advance in consumer sentiment.

The sub-components of the index painted an equally disheartening picture. Economic expectations in August plummeted from 3.7 to a worrying -6.2, marking the lowest level since last December's -10.3. Meanwhile, income expectations saw a significant drop from -5.1 to -11.5. The propensity to buy, another crucial sub-index, also declined, falling from -14.3 to -17.0.

Japan's unemployment rate up to 2.7%, first rise in four months

Japan's job market showed unexpected signs of weakening in July, as the unemployment rate rose to 2.7%, defying expectations of remaining steady at June's 2.5% level. This marks the first uptick in unemployment in four months. The data reveals that the number of employed workers decreased by -100k during the month, while the ranks of those without jobs swelled by 110k.

Adding to the concern, jobs-to-applicants ratio—a leading indicator of labor market health—dipped to 1.29 in July from 1.30. This is the third consecutive monthly decline, counter to median economist forecasts that predicted the ratio would remain flat. These figures indicate that there were only 129 job openings for every 100 applicants, a metric that is closely watched for signs of labor market tightness or slack.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 145.83; (P) 146.30; (R1) 146.52; More...

USD/JPY's rally accelerates to as high as 147.63 today so far. The strong break of 61.8% projection of 129.62 to 145.06 from 137.22 at 146.76 indicates solid underlying momentum. Intraday bias stays on the upside, and the rise from 127.20 should target a test on 151.93 high. On the downside, below 146.26 minor support will turn intraday bias neutral first. But near term outlook will remain mildly bullish as long as 144.52 support holds.

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Rise from 127.20 is seen as the second leg of the pattern and could still be in progress. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Unemployment Rate Jul | 2.70% | 2.50% | 2.50% | |

| 06:00 | EUR | Germany Gfk Consumer Sentiment Sep | -25.5 | -24.3 | -24.4 | -24.6 |

| 13:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y Jun | -1.50% | -1.70% | ||

| 13:00 | USD | Housing Price Index M/M Jun | 0.20% | 0.70% | ||

| 14:00 | USD | Consumer Confidence Aug | 116.5 | 117 |

Australian Dollar Edges Up Ahead of Inflation Report

- US releases consumer confidence and job openings later on Tuesday

- Australia releases CPI on Wednesday

The Australian dollar is in positive territory on Tuesday. In the European session, AUD/USD is trading at 0.6437, up 0.12% on the day.

China’s woes raising concerns in Australia

China’s economic slowdown is bad news for the Australian economy, which counts China as its biggest export market. China’s imports have been falling and as a result, commodity prices have dropped, hurting Australia’s exports of iron ore and gold to China.

China continues to record weak economic numbers and this will likely be reflected in lower GDP releases, although economic growth is above 5%. The Australian dollar is sensitive to China’s economic strength and has declined by around 3% in the third quarter.

The Reserve Bank of Australia meets on September 5th and is widely expected to hold rates at 4.10% for a second straight month. There are clear signs of the economy cooling, including inflation and wage growth easing and a slight rise in unemployment. The RBA would like to extend the pause in rate hikes, with an eye on lowering rates sometime in 2024.

All eyes will be on Australia’s July inflation report which will be released on Wednesday. Inflation has been falling, albeit slowly. In June, inflation fell from 5.5% to 5.4% and the consensus estimate for July is 5.2%. If inflation drops to 5.2% or lower, it should cement a RBA pause in September. A higher rate than 5.2% won’t necessarily mean a rate hike, but it would likely lower the odds of a pause, which are currently around 90%.

In the US, it is a busy Tuesday with consumer confidence and employment releases. The Conference Board Consumer Confidence index has been on the rise and soared to 117.0 in July, up from 110.1 in June. The estimate for August is 116.0 points. JOLTS Job Openings is projected to decelerate for a second straight month in July, from 9.58 million to 9.46 million.

AUD/USD Technical

- AUD/USD tested support at 0.6424 earlier. Below, there is support at 0.6360

- There is resistance at 0.6470 and 0.6531

Bitcoin Trading Volumes Fell to a Minimum of 4 Years

CNBC, citing CryptoQuant agency, reports that:

→ the total volume of bitcoins held on all cryptocurrency exchanges is at its lowest level since 2019;

→ as of August 26, the volume of bitcoin trading on all exchanges was about 130k BTC;

→ a maximum of 3.5 million BTC were traded in 1 day.

Perhaps the decrease in trading volumes is due to a drop in interest due to the uncertainty with the regulation of cryptocurrencies, or the fading of the bullish trend that began from the early days of 2023.

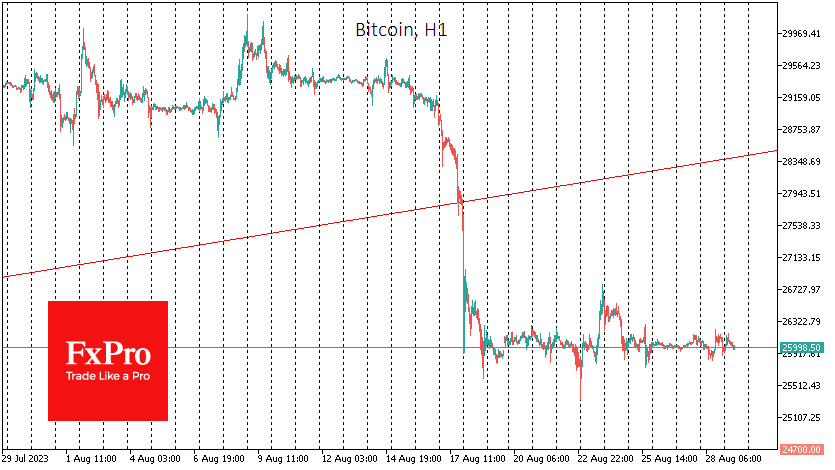

According to JP Morgan analysts, a decrease in open interest may indicate that the price of bitcoin is near a significant low, but the BTC/USD chart suggests that the bearish trend may continue. This is indicated by the descending channel, the outlines of which are becoming clearer.

The analysis shows that:

→ today, the price is near the median line of the descending channel. There are high chances that supply and demand will balance each other. And the price will be in a flat — then the trading volumes may decrease even more;

→ the level 25,500 continues to work as support;

→ an attempt to rise from this level on August 23 (shown by the arrow) failed, indicating the dominance of the bears;

→ the fact that the price of bitcoin is below 50% of the decline in A→B is bearish.

The bullish catalyst could be the approval of the SEC's applications for the creation of ETFs based on bitcoin. But if there are no drivers for growth, the bears can push through the level of 25,500 — then it is possible that it will become resistance.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

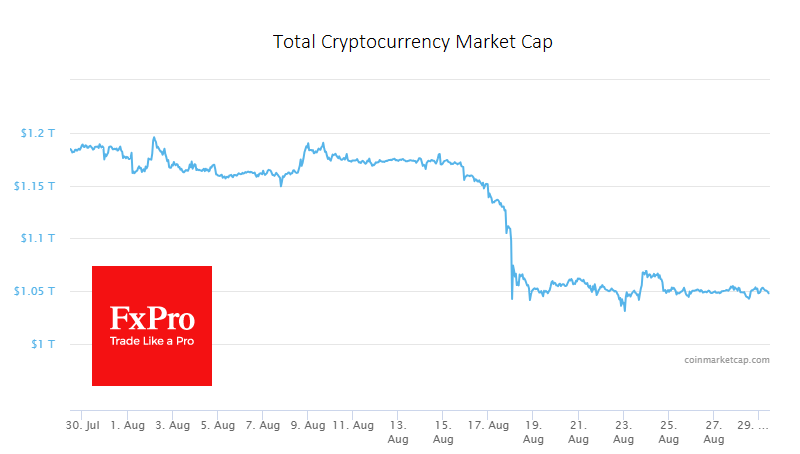

Constricted Bitcoin Corridor Signals a Volatility Boom

Market picture

The crypto market continues to trade in a 0.3% range around the $1.05 trillion capitalisation level. Despite some improvement in risk sentiment, sellers got the upper hand on the approach of the 1.06 trillion level.

The narrow range has also become a hallmark of Bitcoin, which has been walking on a short leash of around $26K for the past eleven days. Such a lull usually ends with a boom in volatility, which is what we should expect this week.

Bitcoin’s tera hash profit margin has reached historic lows as the price has fallen, and the network’s hash rate has risen as more efficient ASICs went to work. Without a rise in the BTC exchange rate, miners’ operations will soon become unprofitable.

News background

Arkham Intelligence says the Robinhood platform holds over $3 billion worth of BTC, making it the third largest Bitcoin holder after Binance (6.4B) and Bitfinex (4.3B).

Due to extreme heat and drought, Laos has imposed temporary restrictions on cryptocurrency mining. These factors have led to an increase in demand for electricity.

Approximately 16 trillion PEPE meme tokens (~$15 million) were illegally withdrawn and sold on various cryptocurrency exchanges. Pepe’s remaining developer revealed that three former project team members were behind the theft.

Shibarium, the second-tier solution from meme token creators Shiba Inu (SHIB), resumed withdrawals via the Ethereum Bridge after a prolonged malfunction during the launch.

Dollar Braces for Data-Heavy Week

Chinese stocks paved the way higher for Asian shares on Tuesday as optimism from China’s measures to cut stamp duty boosted risk appetite. European futures are pointing to a positive open with the UK returning from a day’s holiday ahead of a data-heavy week for markets. In the commodity space, gold is modestly higher this morning with bulls drawing strength from a softer dollar and falling Treasury yields. Oil markets are flat, waiting for the next fundamental spark as supply concerns counter worries over demand.

US PCE inflation and NFP in focus

The US dollar was choppy on Tuesday as investors watched on the sidelines ahead of a slew of key US economic releases over the next few days.

Due to the Federal Reserve's current data dependent stance, every release of US economic data could play a critical role in determining whether the Fed raises rates again in 2023. As a result, close attention will be paid to upcoming releases such as August consumer confidence, Q2 GDP (2nd estimate), and weekly initial jobless claims.

However, the potential market shakers could be Thursday’s PCE inflation data and the NFP report on Friday. The Fed’s preferred inflation gauge, the Core Personal Consumption Expenditure will be closely scrutinised by investors for more signs of inflationary pressures cooling. Regarding the August NFP report, markets expect the US economy to have added 170,000 jobs in August with the unemployment rate unchanged at 3.5%. Ultimately, a strong set of economic releases may strengthen the argument around the Fed raising rates one more time this year, especially after Powell’s hawkish remarks last Friday.

Regarding the dollar, it has appreciated against every G10 currency this month with the USD Index trading around 104.00 as of writing. Although the trend is bullish on the daily charts, there are early signs of exhaustion with a break under 103.30 encouraging bears to jump back into the scene. Should 104.00 prove to be reliable support, prices could push back above 104.50, rising towards levels not seen since March around 105.00.

RBA Bullock sets eyes on inflation, signals possibility of further rate hikes

Incoming RBA Governor Michele Bullock made clear her primary focus would be tackling the country's persistently high inflation. As Bullock prepares to take the helm of RBA on September 18, replacing her current role as deputy governor, her comments carry considerable weight for markets and policymakers alike.

"My first priority is to keep very focused on inflation. Inflation is still too high in Australia. It is coming down and we're forecasting it to continue to come down, but it's still too high," said Bullock.

While she stopped short of providing a timeline for how long interest rates may remain elevated, Bullock did hint at the possibility of additional hikes in the future.

"I'm reluctant to give any sort of predictions on how long interest rates might have to stay high. In Australia's case, all I can say is that we might have to raise interest rates again, but we're watching the data very carefully," she said.

Additionally, Bullock clarified that rate-setting decisions would, for the time being, be made on a "month-by-month"" basis until at least next year.