Sample Category Title

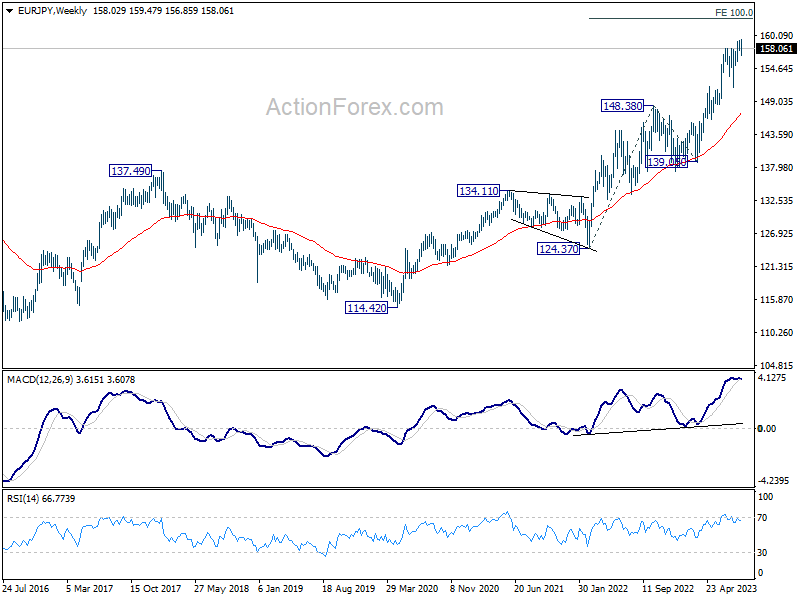

EUR/JPY Weekly Outlook

EUR/JPY edged higher again last week to 159.47 but retreated to 156.85. With subsequent recovery, initial bias is neutral this week first. Risk will stay mildly on the downside as long as 159.47 short term top holds. Break of 156.85 will resume the corrective fall to 55 D EMA (now at 155.72) and possibly below.

In the bigger picture, rise from 114.42 (2020 low) is in progress. Next target is 100% projection of 124.37 to 148.38 from 139.05 at 163.06. Sustained break there will pave the way to retest long term resistance at 169.96. This will remain the favored case as long as 151.39 support holds, even in case of deep pull back.

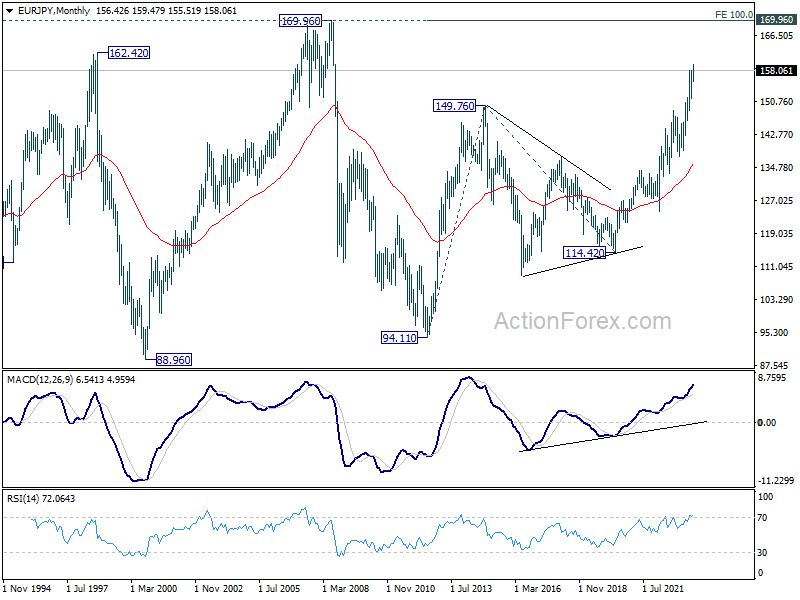

In the long term picture, rise from 109.03 (2016 low) is seen as the third leg of the whole up trend from 94.11 (2012 low). Next target is 100% projection of 94.11 to 149.76 from 114.42 at 170.07 which is close to 169.96 (2008 high).

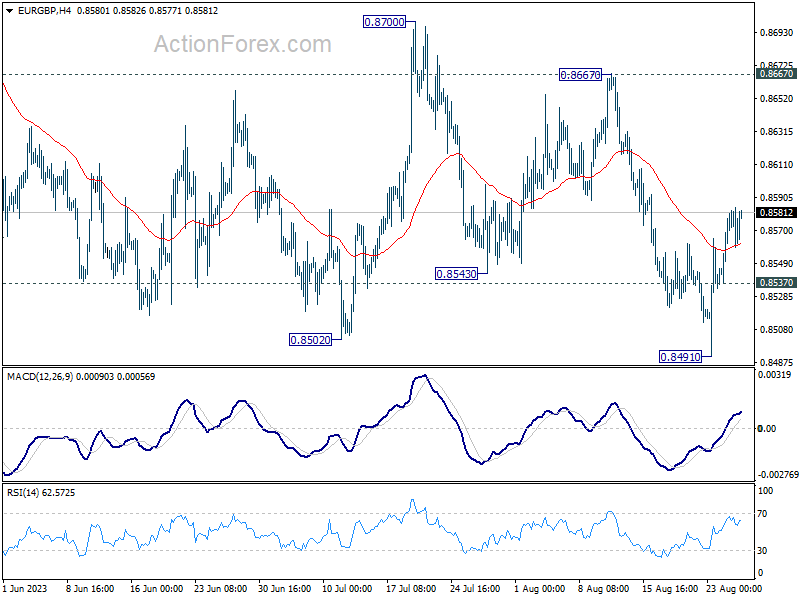

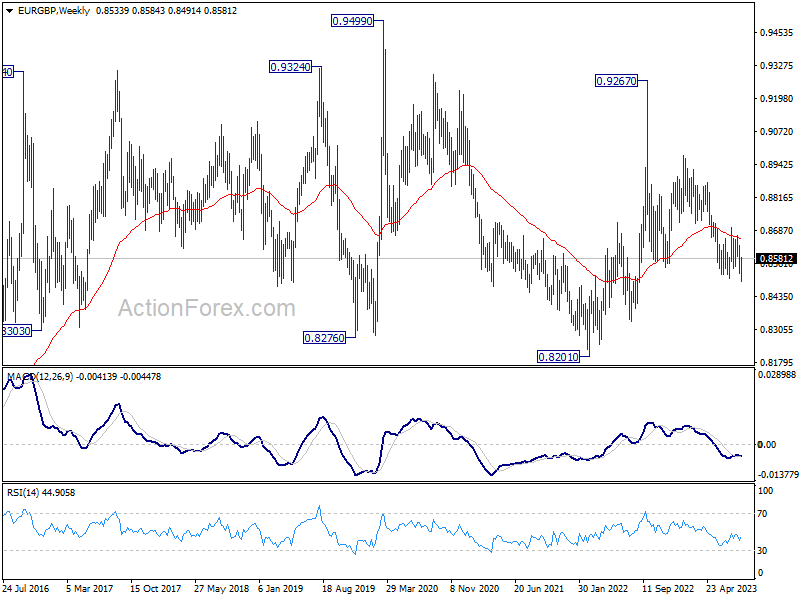

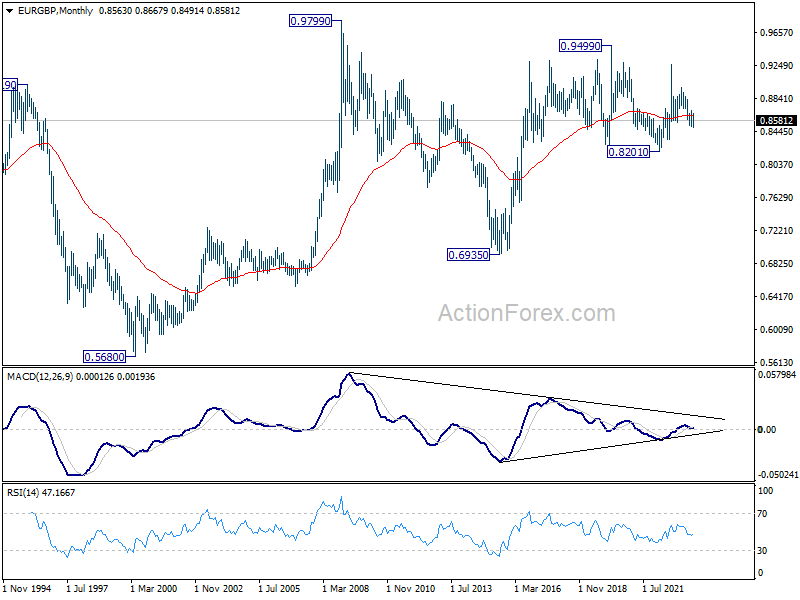

EUR/GBP Weekly Outlook

EUR/GBP dipped to 0.8491 last week but rebounded strongly since then. Initial bias is mildly on the upside for stronger rebound. But overall outlook will stay bearish as long as 0.8667 resistance holds. That is, larger down trend from 0.8977 is in favor to continue. Below 0.8537 minor support will bring retest of 0.8491 low first.

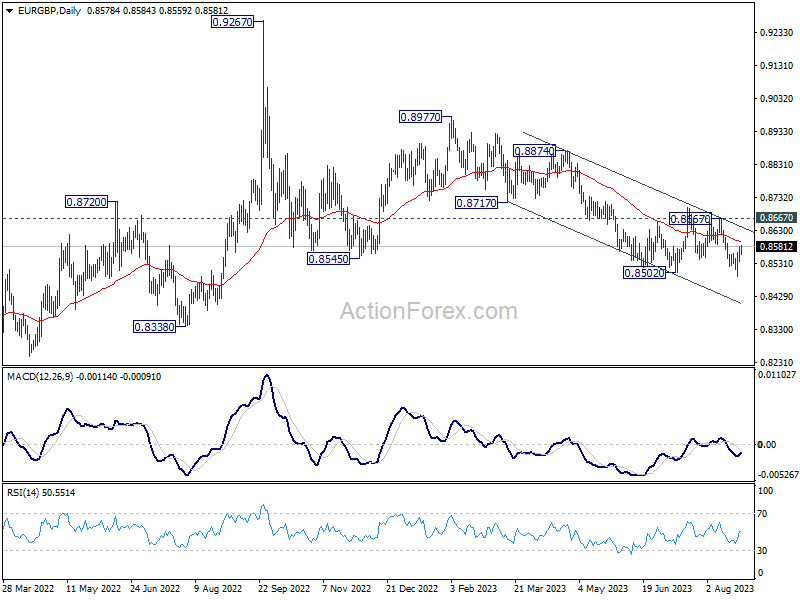

In the bigger picture, the down trend from 0.9267 (2022 high) is seen as part of the long term range pattern from 0.9499 (2020 high). Further decline is in favor as long as 0.8667 resistance holds. Break of 0.8502 will resume the fall towards 0.8201 (2022 low).

In the long term picture, long term range pattern is extending. But rise from 0.6935 (2015 low) is expected to resume at a later stage, to 0.9799 (2009 high).

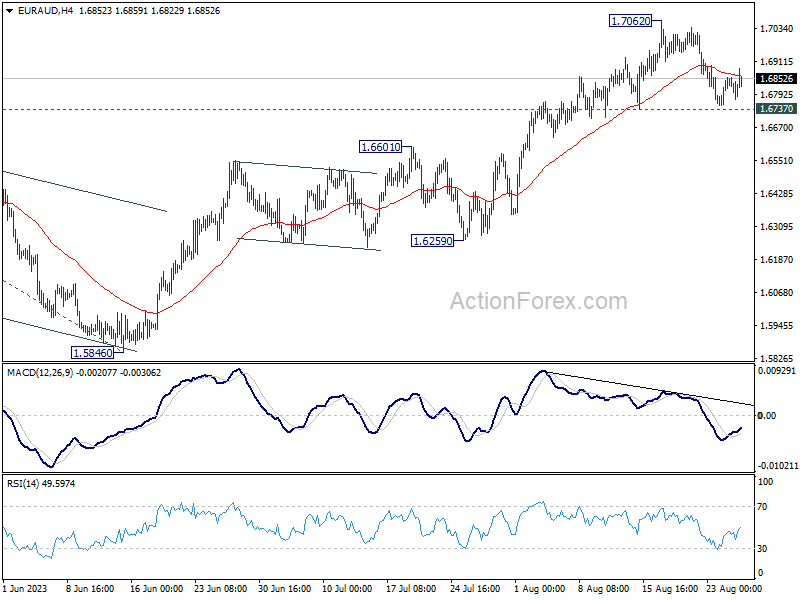

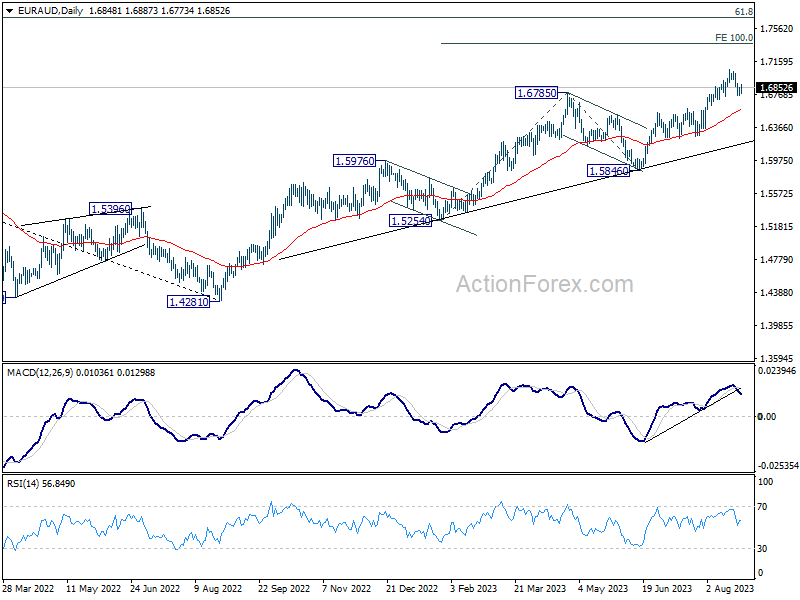

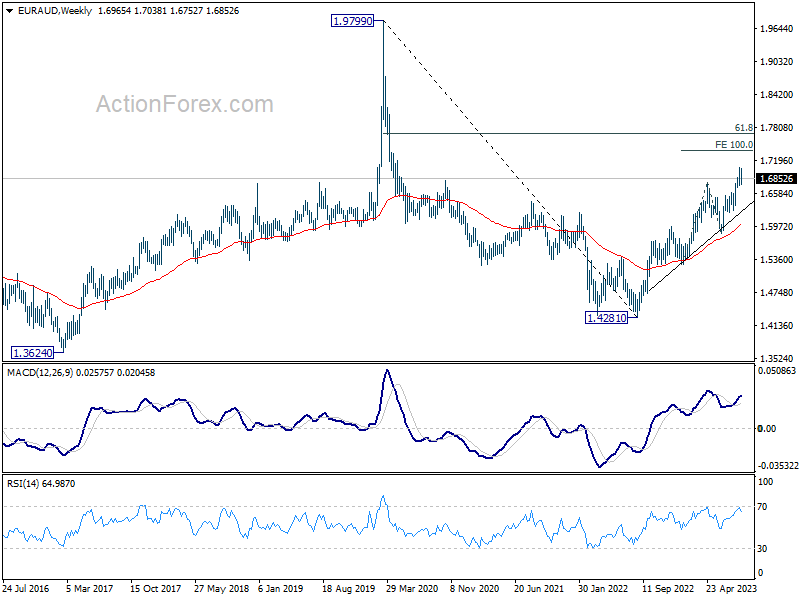

EUR/AUD Weekly Outlook

EUR/AUD's pull back from 1.7062 extended lower last week, but stayed above 1.6737 support. Initial bias stays neutral this week first and further rally is in favor. On the upside, firm break of 1.7062 resistance will resume larger up trend to 1.7377 projection level next. However, firm break of 1.6737 will bring deeper pull back to 1.6601 resistance turned support instead.

In the bigger picture, the rise from 1.4281 (2022 low) is in progress. Next target is 100% projection of 1.5254 to 1.6785 from 1.5846 at 1.7377. For now, outlook will stay bullish as long as 1.5846 support holds, even in case of another pull back.

In the longer term picture, it's still early to decide if rise from 1.4281 is resuming whole up trend from 1.1602 (2012 low). But in either case, further rally is in favor as long as 1.5846 support holds. Next target is 61.8% retracement of 1.9799 to 1.4281 at 1.7691.

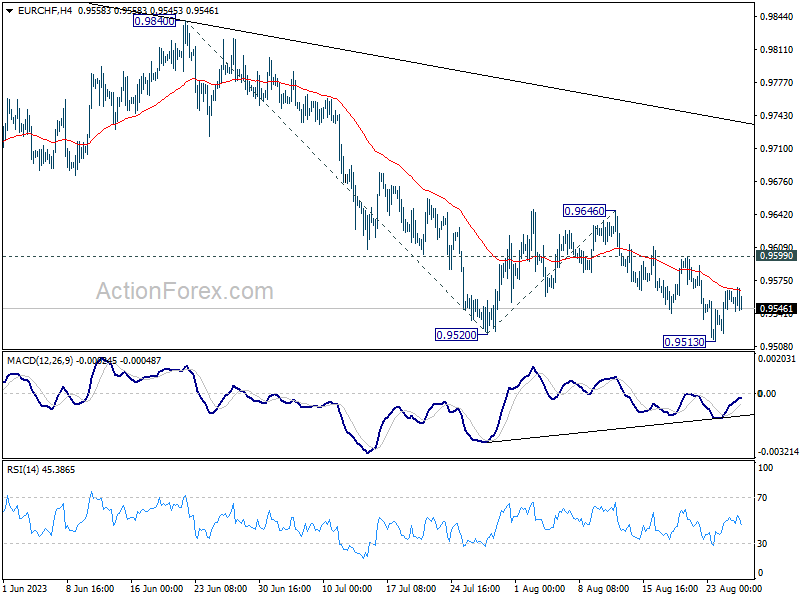

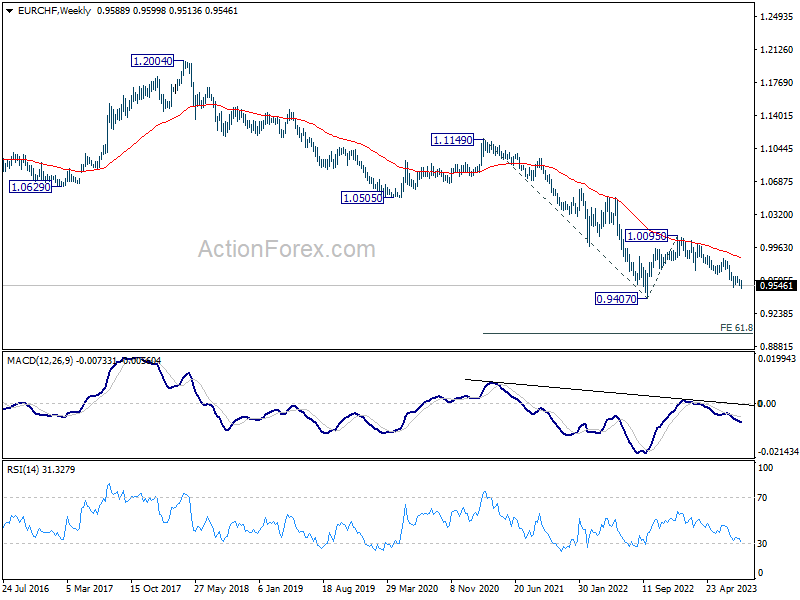

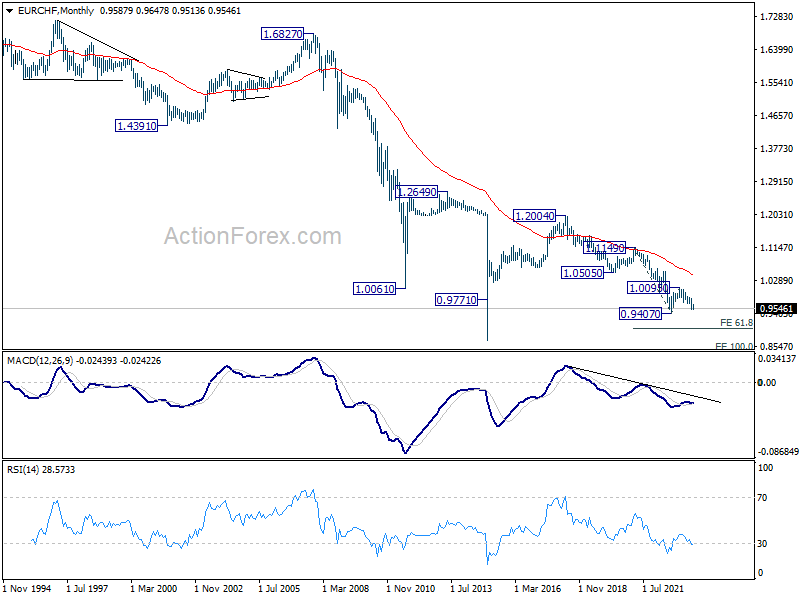

EUR/CHF Weekly Outlook

EUR/CHF's breach of 0.9520 support argues that fall from 1.0095 is resuming. But as it recovered after hitting 0.9513, initial bias is neutral this week first. Further decline is expected as long as 0.9599 resistance holds. Break of 0.9513 will target 61.8% projection of 0.9840 to 0.9520 from 0.9646 at 0.9448.

In the bigger picture, medium term outlook is staying bearish as the pair is capped well below falling 55 W EMA (now at 0.9839). Down trend from 1.2004 (2018 high) is in favor to continue. Sustained break of 0.9407 will target 61.8% projection of 1.1149 to 0.9407 from 1.0095 at 0.9018. For now, this will remain the favored case as long as 0.9670 support turned resistance holds, in case of strong rebound.

In the long term picture, outlook remains bearish as it's staying well below 55 M EMA (now at 1.0421). Break of 1.00095 resistance is needed to be the first sign of bottoming, or the multi-decade down trend is expected to continue.

Powell at Jackson Hole: Fed Committed to 2% Inflation But Agility Required

Summary

- Fed Chair Jerome Powell reiterated the FOMC's commitment to bring inflation down to 2% during his speech in Jackson Hole, WY today. He stated that "two percent is and will remain our inflation target."

- In order to bring inflation back to target, Powell said that a period of below-trend economic growth will be required. Consequently, the stance of monetary policy will need to remain restrictive for the foreseeable future. The Fed Chair also indicated that the FOMC "is prepared to raise rates further if appropriate."

- But the FOMC is facing a number of uncertainties at this juncture. Consequently, Fed policymakers will need to be "agile." In other words, the FOMC is in data dependency mode for the foreseeable future.

- We believe there is a high bar for the FOMC to raise rates at its September 20 meeting. We forecast the Committee will remain on hold at subsequent meetings, but we acknowledge the risk of further tightening if economic growth does not slow to a below-trend rate and/or inflation remains unacceptably high.

Fed Committed to 2% Inflation Target

As has become customary for the Chair of the Federal Reserve, Jerome Powell kicked off the Kansas City Fed's annual Jackson Hole Economic Policy Symposium today with a speech entitled "Inflation: Progress and the Path Ahead." The speech that Powell delivered last year at Jackson Hole, which we discussed in our Weekly Economic and Financial Commentary on August 26, 2022, was short and to the point. In the five-page speech that he delivered last year, Powell essentially said that the FOMC would do everything needed to ensure that inflation would return to the Committee's 2% target. The FOMC had already raised rates by 225 bps when Powell delivered his speech last year. It would go on to hike by another 300 bps in the subsequent 12 months.

The mission at Jackson Hole last year was simple. Powell needed to convince market participants that the FOMC was committed to bringing down inflation, and his concise and direct remarks largely succeeded in that regard. Because inflation remains above target today, the Fed Chair apparently wanted to send a message that the FOMC remains committed to bringing inflation down. He reiterated last year's mantra at the very beginning of his remarks today by saying "it is the Fed's job to bring inflation down to our two percent goal, and we will do so." In case the point was missed, he closed by saying "restoring price stability is essential," and "we will keep at it until the job is done." Powell also threw cold water on any expectations that the FOMC might tweak its inflation target higher by stating "two percent is and will remain our inflation target."

Although Powell welcomed the decline in the rate of inflation that has occurred since last year's speech—the year-over-year rate of core PCE inflation has receded gradually from its peak of 5.4% in February 2022 to 4.1% currently—he indicated that "it remains too high." In order to bring inflation back to the Committee's 2% target, the Fed Chair said that the labor market must become less tight. Powell went on to state that "a period of below-trend economic growth" will be needed to bring inflation sustainably back to target. Consequently, the stance of monetary policy, which Powell characterized as "restrictive" at present, will need to remain so for the foreseeable future. In short, the Fed likely will not be cutting rates anytime soon. Indeed, Powell indicated that the FOMC "is prepared to raise rates further if appropriate."

Uncertainties Cloud the Outlook for Monetary Policy

But Powell also highlighted in this year's speech the uncertainties the FOMC faces in achieving its goal. He noted that "it is challenging to know in real time" when a sufficiently restrictive stance of policy has been achieved, and he said "that assessment is further complicated by uncertainty about the duration of the lags with which monetary tightening affects economic activity and especially inflation." Because there is a risk of doing too much (i.e., tanking the economy) as well as a risk of doing too little (i.e., allowing high inflation to become entrenched), Powell said that policymaking will need to be "agile" going forward. In short, the FOMC is in data dependency mode at present. Incoming economic data will determine whether the Committee tightens policy further or whether it decides to remain on hold. But given the current state of play—the real economy appears to be holding up rather well and inflation remains well above target—don't expect monetary easing anytime soon.

Our assessment is that there is a high bar for the FOMC to raise rates at its next policy meeting on September 20. Patrick Harker, the president of the Federal Reserve Bank of Philadelphia and a voting member of the FOMC this year, said yesterday that the Committee has "probably done enough" in terms of monetary tightening. It appears that there are a number of other Committee members who also think that further tightening is not warranted. If the macro U.S. economy evolves largely in line with our forecast in coming months, then we think the FOMC will remain on hold at its November 1 meeting as well. That said, we acknowledge the risk that the Committee could tighten further at future meetings if economic growth does not slow to a below-trend rate and/or inflation remains unacceptably high.

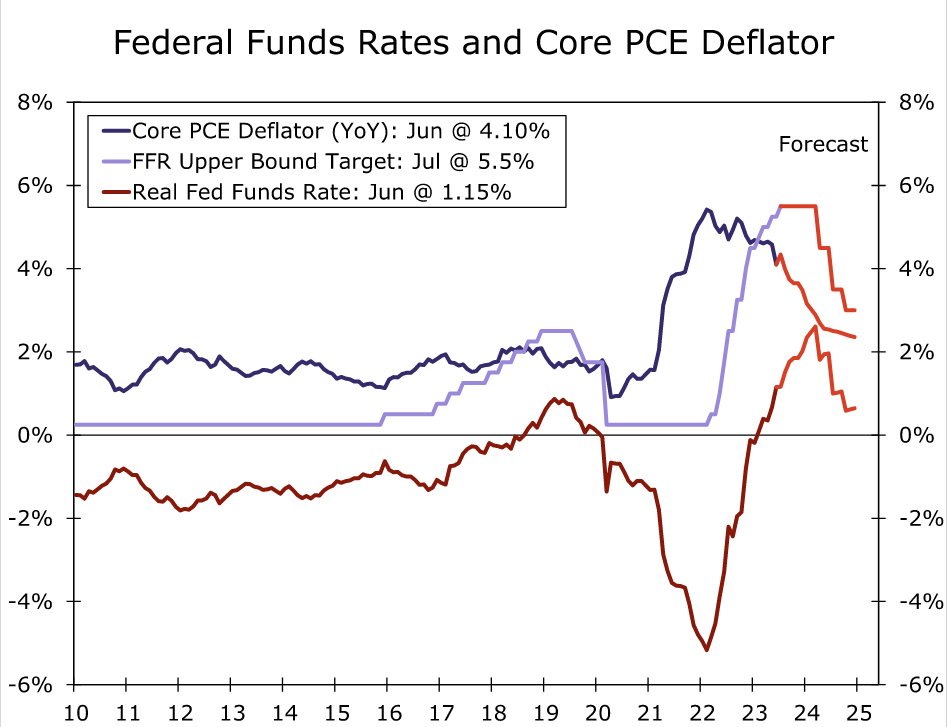

Even if the FOMC remains on hold, the stance of monetary policy is likely to tighten passively in coming months. Real interest rates matter more for real economic growth than nominal interest rates. If, as we forecast, the FOMC remains on hold as inflation recedes gradually further in coming months, then the real fed funds rate will creep higher (Figure 1). Although the probability of a "soft landing" has increased, the economy is by no means "out of the woods" in terms of a potential recession. Indeed, we continue to forecast that real GDP will contract modestly in the first half of 2024 and that the unemployment rate will rise by roughly one percentage point or so from its current level of 3.5%. For details, see our most recent U.S. Economic Outlook.

Fed Chair Powell on “Navigating by the Stars Under Cloudy Skies”

At the Federal Reserve Bank of Kansas City's Jackson Hole Symposium, Federal Reserve Chair Jay Powell gave a much-anticipated speech titled, Inflation: Progress and the Path Ahead.

Chair Powell kicked off his remarks re-iterating the Fed's 2% target, and its commitment to attaining that goal. Powell outlined the decline in inflation so far, and acknowledged the welcome cooler inflation readings in past two months. However, he then emphasized that there is "substantial further ground to cover to get back to price stability."

On the inflation outlook, he discussed the three key parts of inflation in more detail, but stuck to his past messaging that "getting inflation sustainably back down to 2 percent is expected to require a period of below-trend economic growth as well as some softening in labor market conditions." In terms of inflation details:

- He noted that sustained progress on core goods prices is needed.

- On the services side, that housing services inflation has recently begun to fall, and the process is expected to continue given the well known lags (see report), but they will be watching market rent data closely.

- Finally, inflation in non-housing services , aka "supercore", has finally started to decline on a three and six-month basis, and "further progress will be essential to restoring price stability". But that "over time restrictive monetary policy… reducing inflationary pressures in this key sector."

On the economic outlook, he pointed out that there is evidence that higher real long-term yields (up about 150 basis points since last year), and tighter financial conditions are contributing to slower growth in the economy. But that more recently, growth has remained above trend, and consumer spending has been picking up. Powell also noted that the labor market is rebalancing but the process remains incomplete. On both scores the speech emphasized that if progress is no longer being made, it would also call for a "monetary policy response" – aka further rate hike(s).

Before concluding he acknowledged that the uniqueness of the current cycle causes additional uncertainty for policymakers. For example, job openings have declined substantially without a rise in the unemployment rate. Therefore, the fed will need to remain "agile" in setting policy.

As to where that policy is headed, given that they are "navigating by the stars under cloudy skies" he kept his options open. The Fed will "proceed carefully" on whether to tighten further or hold steady.

Key Implications

The Chair's speech at Jackson Hole is always a marquee economic event, but with the Fed at a pivot point in its tightening cycle, this year's speech was particularly important. Markets are trying to gauge whether the fed is in wait-and-see mode, and feels it can be patient and wait for past rate hikes to cool the economy and bring down inflation, or whether more rate hikes are required. Looking at the market's reaction immediately following the speech, the odds on future fed hikes didn't shift a great deal. The slim odds of a hike in September got slimmer, and the roughly 50% odds of a hike in November are every so slightly higher. Market odds on the first rate cut next year remain unchanged at June.

In recent weeks market pricing had likely moved in a direction the Fed liked, so Powell likely didn't want to rock the boat too much. The Fed is in wait and see mode, but has its finger hovering over the hike button if progress on cooler growth stalls. As discussed in our recent Q&A, the FOMC will likely to continue to talk tough, to prevent an undesirable give back in bond yields, as it watches the incoming data closely.

Weekly Economic & Financial Commentary: Cracks Starting to Emerge?

Summary

United States: Cracks Starting to Emerge?

- After a strong run last week, this week’s barrage of economic data brought expectations back down to Earth. Durable goods orders seem to be stagnating as high mortgage rates keep the housing market under pressure. Meanwhile, preliminary benchmark revisions from BLS reveal that the labor market is not as scorching as previously thought.

- Next week: Personal Income & Spending (Thu.), Employment (Fri.), ISM Manufacturing (Fri.)

International: European Economic Prospects Getting Dimmer

- This week's PMI surveys from Europe pointed to the growth challenges facing Europe's key economies and highlighted the risk of a renewed stumble across the Eurozone. Of particular note, the August service sector PMIs returned to contractionary territory as the Eurozone services PMI fell to 48.3, and the U.K. services PMI fell to 48.7.

- Next week: China PMIs (Thu.), Eurozone CPI (Thu.), Canada GDP (Fri.)

Topic of the Week: What Would a "Hard Landing" in China Portend for Other Major Economies?

- Some observers worry that the debt build-up in China's property sector may lead to an economic "hard landing" in the world's second-largest economy. We analyze what effects a significant economic slowdown/downturn in China may have on the U.S., Eurozone and Japanese economies.

The Weekly Bottom Line: Fed Chair Powell Sticks to Tough Talk

U.S. Highlights

- Speaking at the Jackson Hole Economic Symposium on Friday, Chair Powell noted that some progress had been made on the inflation front, but that inflation was still “too high”. He noted that the Fed would proceed carefully in either tightening the policy rate further or holding it constant as it watches the data.

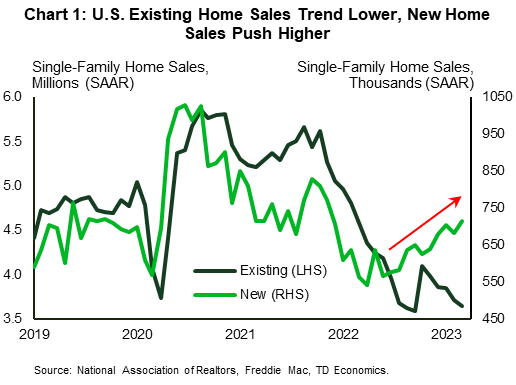

- Existing home sales were one piece of data reacting strongly to higher rates, falling further in July. Inventories remained lean, at 42% below pre-pandemic levels.

- Lack of supply in the existing market continues to push buyers to the new market, with sales there up strongly in July.

Canadian Highlights

- Consumer activity was soft in June, with retail sales posting a very mild gain. Actual Q2 consumer spending is released with GDP data next week, and the retail data is pointing to a subdued 1% annualized gain in overall spending.

- July’s flash estimate flagged stronger retail spending growth last month, in line with our internal debit and credit card data. However, temporary government income supports were likely behind these healthy prints, and spending growth is set to fade.

- In a bid to help housing affordability, the federal government may be looking at capping international students. This restricting of population inflows would weigh on consumption.

U.S. – Fed Chair Powell Sticks to Tough Talk

In a relatively quiet economic data week, markets took their cue from Chair Powell’s Jackson Hole Economic Symposium speech. The annual speech is always a highly anticipated event, but this year’s was particularly important with the Fed being at a monetary policy pivot point. The speech struck a balance between acknowledging that some progress had been made on inflation, but that it remained “too high” with substantial ground to cover to get back to price stability. Equity and bond markets didn’t like this reminder and were down on Friday (at time of writing).

The Chair noted the FOMC was prepared to “raise rates further if appropriate”, and that it intended to hold policy at a restrictive level until confident that inflation was moving sustainably down toward its objective. However, given that they are navigating in a cloudy environment, they would proceed “carefully”. What appeared to be off the table was any indication of potentially lowering rates, thus giving the speech a more hawkish tilt in our view. We believe that the continuation of this tough talk is necessary to prevent an undesirable give back in bond yields and, ultimately, to help keep inflationary expectations in check as it continues to monitor the data closely.

Powell provided a little more detail into the factors that will go into policymaking by breaking down inflation into three key categories. This included core goods inflation, along with housing and non-housing services. He noted progress on all three. On non-housing services – a category also known as “supercore”, which accounts for over half of the core PCE index – annual inflation has moved mostly sideways, but encouragingly it has started to decline on a three and six-month basis. Meanwhile, housing services inflation is expected to continue to ease given well-known lags, but they will be watching market rent data closely.

Speaking of housing, existing home sales continued to head lower in July. With mortgage rates some 40 basis points higher than in the two months prior it is no wonder that activity pulled back. The elevated rate environment also poses a hurdle on the supply side, as existing homeowners with much lower mortgage rates are reluctant to move and take on a higher rate. This theme is evident in inventories, which were 42% lower than pre-pandemic July levels (July 2019).

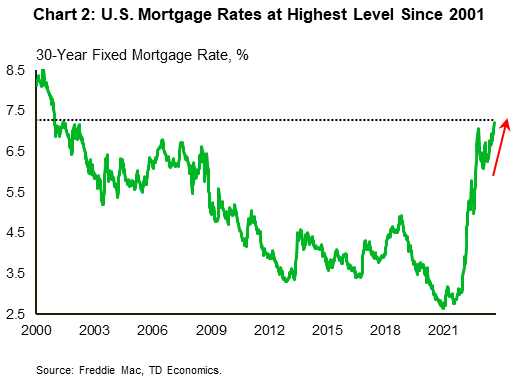

The tightness in resale market has kept a floor on home prices, while also pushing more would-be buyers to the “new” home market. New single-family home sales continue to buck the broader negative trend, making additional gains in July (Chart 1). This has been much to the delight of homebuilders, who have looked to boost supply in the single-family sector. While this trend may have some more room to run, mortgage rates have pushed even higher recently and are now hovering in the 7.2-7.5% range (Chart 2). This could test the strength of the positive single-family homebuilding trend sooner than anticipated, as evidenced by the recent pullback in homebuilder confidence and some flattening in single-family housing permits. Ultimately, it all ties back to interest rates, which, given the Fed’s continued tough talk, appear set to remain higher for longer.

Canada – Cooler Spending On Tap

It was a choppy week for bonds, with Canadian yields diving lower on Wednesday amid weak global PMI data before recovering some lost ground to end the week. As of writing, the benchmark Canadian 10-year yield was on track to end the week modestly lower than where it began. Oil prices are seemingly headed for their second weekly decline on Chinese growth concerns, reports of healthy supply coming out of Iran and the possibility that U.S. sanctions might be lifted on the Venezuelan oil sector.

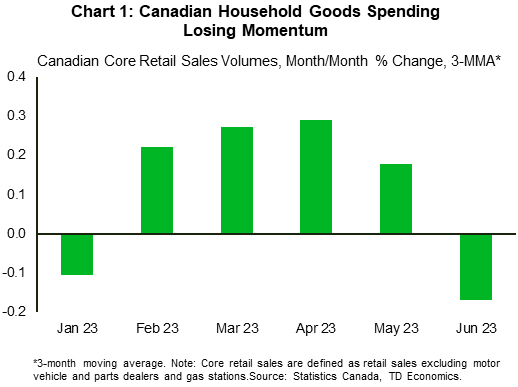

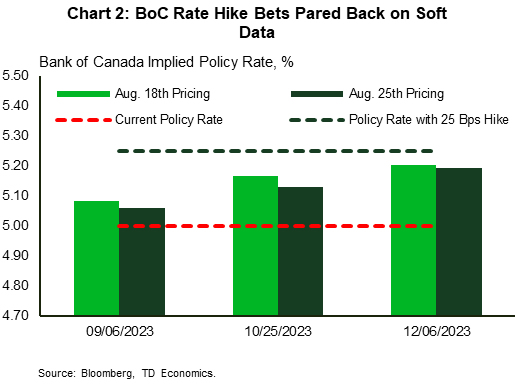

This soft tone extended to the June retail sales data, which inched only marginally higher by 0.1% month-on-month (m/m). On the one hand, it slightly beat Statistics Canada's advance estimate. On the other, core sales (which strip out autos and gas stations), plunged nearly 1% m/m (Chart 1), and volumes were slightly lower. This cooler consumer momentum contributed to traders paring back their expectations for BoC hikes (Chart 2).

One silver lining from the retail report was that nominal spending may have increased 0.4% m/m in July according to Statcan's preliminary estimate. Taken together with healthy flash estimates for manufacturing and wholesale activity in July and growth in hours worked reported in the Labour Force Survey, it appears that overall economic growth was positive last month.

The retail report also squares with our internal data showing a solid monthly gain in debit and credit card spending in July. But there are good reasons to fade this positive news. Recall that last month, the federal government paid out the $2.5 billion Grocery Rebate and one payment of the enhanced Canada Workers Benefit. Assuming no additional step-up in government supports, this temporary boost to household incomes will dissipate and with it, momentum in consumer spending. Accordingly, after a hefty third quarter, we expect a slowdown in household spending thereafter.

The federal government may soon be doing their part to soften consumer spending by limiting population flows. Cabinet ministers met this week to discuss Canada's housing affordability crisis and one of the solutions floated was a cap on international students. Capping international student inflows is likely an easier lever to pull to address rental affordability than ramping up new home construction quickly. However, the idea was met with some resistance. At least one province – Quebec – has been unreceptive, vowing to reject the federal government's idea. Provinces would likely be on the hook for some of the tuition shortfall for post-secondary schools.

Summary 8/28 – 9/1

Monday, Aug 28, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Retail Sales M/M Jul | 0.30% | -0.80% |

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Jul | 0.00% | 0.60% |

| 23:30 | JPY | Unemployment Rate Jul | 2.50% | 2.50% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Retail Sales M/M Jul | |

| Forecast: 0.30% | Previous: -0.80% | ||

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Jul | |

| Forecast: 0.00% | Previous: 0.60% | ||

| 23:30 | JPY | Unemployment Rate Jul | |

| Forecast: 2.50% | Previous: 2.50% | ||

Tuesday, Aug 29, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 06:00 | EUR | Germany Gfk Consumer Sentiment Sep | -24.3 | -24.4 |

| 13:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y Jun | -1.50% | -1.70% |

| 13:00 | USD | Housing Price Index M/M Jun | 0.20% | 0.70% |

| 14:00 | USD | Consumer Confidence Aug | 116.5 | 117 |

| 22:45 | NZD | Building Permits M/M Jul | 3.50% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 06:00 | EUR | Germany Gfk Consumer Sentiment Sep | |

| Forecast: -24.3 | Previous: -24.4 | ||

| 13:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y Jun | |

| Forecast: -1.50% | Previous: -1.70% | ||

| 13:00 | USD | Housing Price Index M/M Jun | |

| Forecast: 0.20% | Previous: 0.70% | ||

| 14:00 | USD | Consumer Confidence Aug | |

| Forecast: 116.5 | Previous: 117 | ||

| 22:45 | NZD | Building Permits M/M Jul | |

| Forecast: | Previous: 3.50% | ||

Wednesday, Aug 30, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Monthly CPI Y/Y Jul | 5.20% | 5.40% |

| 01:30 | AUD | Building Permits M/M Jul | -0.50% | -7.70% |

| 05:00 | JPY | Consumer Confidence Index Aug | 37.5 | 37.1 |

| 06:00 | EUR | Germany Import Price Index M/M Jul | -0.20% | -1.60% |

| 07:00 | CHF | KOF Economic Barometer Aug | 91.3 | 92.2 |

| 08:00 | CHF | Credit Suisse Economic Expectations Aug | -32.6 | |

| 08:30 | GBP | Mortgage Approvals Jul | 52K | 55K |

| 08:30 | GBP | M4 Money Supply M/M Jul | 0.10% | -0.10% |

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Aug | 93.9 | 94.5 |

| 09:00 | EUR | Eurozone Services Sentiment Aug | 4.2 | 5.7 |

| 09:00 | EUR | Eurozone Industrial Confidence Aug | -9.8 | -9.4 |

| 09:00 | EUR | Eurozone Consumer Confidence Aug F | -16 | -16 |

| 12:00 | EUR | Germany CPI M/M Aug P | 0.30% | 0.30% |

| 12:00 | EUR | Germany CPI Y/Y Aug P | 6.00% | 6.20% |

| 12:15 | USD | ADP Employment Change Aug | 205K | 324K |

| 12:30 | USD | GDP Annualized Q2 P | 2.40% | 2.40% |

| 12:30 | USD | GDP Price Index Q2 P | 2.20% | 2.20% |

| 12:30 | USD | Goods Trade Balance (USD) Jul P | -90.0B | -87.8B |

| 12:30 | USD | Wholesale Inventories Jul P | 0.20% | -0.50% |

| 14:00 | USD | Pending Home Sales M/M Jul | -0.40% | 0.30% |

| 14:30 | USD | Crude Oil Inventories | -6.1M | |

| 23:50 | JPY | Industrial Production M/M Jul P | -1.40% | 2.40% |

| 23:50 | JPY | Retail Trade Y/Y Jul | 5.40% | 5.90% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Monthly CPI Y/Y Jul | |

| Forecast: 5.20% | Previous: 5.40% | ||

| 01:30 | AUD | Building Permits M/M Jul | |

| Forecast: -0.50% | Previous: -7.70% | ||

| 05:00 | JPY | Consumer Confidence Index Aug | |

| Forecast: 37.5 | Previous: 37.1 | ||

| 06:00 | EUR | Germany Import Price Index M/M Jul | |

| Forecast: -0.20% | Previous: -1.60% | ||

| 07:00 | CHF | KOF Economic Barometer Aug | |

| Forecast: 91.3 | Previous: 92.2 | ||

| 08:00 | CHF | Credit Suisse Economic Expectations Aug | |

| Forecast: | Previous: -32.6 | ||

| 08:30 | GBP | Mortgage Approvals Jul | |

| Forecast: 52K | Previous: 55K | ||

| 08:30 | GBP | M4 Money Supply M/M Jul | |

| Forecast: 0.10% | Previous: -0.10% | ||

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Aug | |

| Forecast: 93.9 | Previous: 94.5 | ||

| 09:00 | EUR | Eurozone Services Sentiment Aug | |

| Forecast: 4.2 | Previous: 5.7 | ||

| 09:00 | EUR | Eurozone Industrial Confidence Aug | |

| Forecast: -9.8 | Previous: -9.4 | ||

| 09:00 | EUR | Eurozone Consumer Confidence Aug F | |

| Forecast: -16 | Previous: -16 | ||

| 12:00 | EUR | Germany CPI M/M Aug P | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 12:00 | EUR | Germany CPI Y/Y Aug P | |

| Forecast: 6.00% | Previous: 6.20% | ||

| 12:15 | USD | ADP Employment Change Aug | |

| Forecast: 205K | Previous: 324K | ||

| 12:30 | USD | GDP Annualized Q2 P | |

| Forecast: 2.40% | Previous: 2.40% | ||

| 12:30 | USD | GDP Price Index Q2 P | |

| Forecast: 2.20% | Previous: 2.20% | ||

| 12:30 | USD | Goods Trade Balance (USD) Jul P | |

| Forecast: -90.0B | Previous: -87.8B | ||

| 12:30 | USD | Wholesale Inventories Jul P | |

| Forecast: 0.20% | Previous: -0.50% | ||

| 14:00 | USD | Pending Home Sales M/M Jul | |

| Forecast: -0.40% | Previous: 0.30% | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -6.1M | ||

| 23:50 | JPY | Industrial Production M/M Jul P | |

| Forecast: -1.40% | Previous: 2.40% | ||

| 23:50 | JPY | Retail Trade Y/Y Jul | |

| Forecast: 5.40% | Previous: 5.90% | ||

Thursday, Aug 31, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:00 | CNY | NBS Manufacturing PMI Aug | 49.5 | 49.3 |

| 01:00 | CNY | Non-Manufacturing PMI Aug | 51.1 | 51.5 |

| 01:00 | NZD | ANZ Business Confidence Aug | -13.1 | |

| 01:30 | AUD | Private Capital Expenditure Q2 | 1.10% | 2.40% |

| 05:00 | JPY | Housing Starts Y/Y Jul | -0.80% | -4.80% |

| 05:00 | JPY | Construction Orders Y/Y Jul | -1.30% | 8.60% |

| 06:00 | EUR | Germany Retail Sales M/M Jul | 0.30% | -0.80% |

| 06:45 | EUR | France Consumer Spending M/M Jul | 0.30% | 0.90% |

| 06:45 | EUR | France GDP Q/Q Q2 | 0.50% | 0.50% |

| 07:55 | EUR | Germany Unemployment Change Jul | 10K | -4K |

| 07:55 | EUR | Germany Unemployment Rate Jul | 5.60% | 5.60% |

| 08:00 | EUR | Italy Unemployment Jul | 7.40% | 7.40% |

| 09:00 | EUR | Eurozone Unemployment Rate Jul | 6.40% | 6.40% |

| 09:00 | EUR | Eurozone CPI Y/Y Aug P | 5.10% | 5.30% |

| 09:00 | EUR | Eurozone CPI Core Y/Y Aug P | 5.30% | 5.50% |

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | ||

| 12:30 | CAD | Current Account (CAD) Q2 | -6.2B | |

| 12:30 | USD | Initial Jobless Claims (Aug 25) | 227K | 230K |

| 12:30 | USD | Personal Income M/M Jul | 0.30% | 0.30% |

| 12:30 | USD | Personal Spending Jul | 0.70% | 0.50% |

| 12:30 | USD | PCE Price Index M/M Jul | 0.20% | 0.20% |

| 12:30 | USD | PCE Price Index Y/Y Jul | 3.30% | 3.00% |

| 12:30 | USD | Core PCE Price Index M/M Jul | 0.20% | 0.20% |

| 12:30 | USD | Core PCE Price Index Y/Y Jul | 4.20% | 4.10% |

| 13:45 | USD | Chicago PMI Aug | 44.1 | 42.8 |

| 14:30 | USD | Natural Gas Storage | 18B | |

| 23:50 | JPY | Capital Spending Q2 | 7.90% | 11.00% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:00 | CNY | NBS Manufacturing PMI Aug | |

| Forecast: 49.5 | Previous: 49.3 | ||

| 01:00 | CNY | Non-Manufacturing PMI Aug | |

| Forecast: 51.1 | Previous: 51.5 | ||

| 01:00 | NZD | ANZ Business Confidence Aug | |

| Forecast: | Previous: -13.1 | ||

| 01:30 | AUD | Private Capital Expenditure Q2 | |

| Forecast: 1.10% | Previous: 2.40% | ||

| 05:00 | JPY | Housing Starts Y/Y Jul | |

| Forecast: -0.80% | Previous: -4.80% | ||

| 05:00 | JPY | Construction Orders Y/Y Jul | |

| Forecast: -1.30% | Previous: 8.60% | ||

| 06:00 | EUR | Germany Retail Sales M/M Jul | |

| Forecast: 0.30% | Previous: -0.80% | ||

| 06:45 | EUR | France Consumer Spending M/M Jul | |

| Forecast: 0.30% | Previous: 0.90% | ||

| 06:45 | EUR | France GDP Q/Q Q2 | |

| Forecast: 0.50% | Previous: 0.50% | ||

| 07:55 | EUR | Germany Unemployment Change Jul | |

| Forecast: 10K | Previous: -4K | ||

| 07:55 | EUR | Germany Unemployment Rate Jul | |

| Forecast: 5.60% | Previous: 5.60% | ||

| 08:00 | EUR | Italy Unemployment Jul | |

| Forecast: 7.40% | Previous: 7.40% | ||

| 09:00 | EUR | Eurozone Unemployment Rate Jul | |

| Forecast: 6.40% | Previous: 6.40% | ||

| 09:00 | EUR | Eurozone CPI Y/Y Aug P | |

| Forecast: 5.10% | Previous: 5.30% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Aug P | |

| Forecast: 5.30% | Previous: 5.50% | ||

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | |

| Forecast: | Previous: | ||

| 12:30 | CAD | Current Account (CAD) Q2 | |

| Forecast: | Previous: -6.2B | ||

| 12:30 | USD | Initial Jobless Claims (Aug 25) | |

| Forecast: 227K | Previous: 230K | ||

| 12:30 | USD | Personal Income M/M Jul | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 12:30 | USD | Personal Spending Jul | |

| Forecast: 0.70% | Previous: 0.50% | ||

| 12:30 | USD | PCE Price Index M/M Jul | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 12:30 | USD | PCE Price Index Y/Y Jul | |

| Forecast: 3.30% | Previous: 3.00% | ||

| 12:30 | USD | Core PCE Price Index M/M Jul | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 12:30 | USD | Core PCE Price Index Y/Y Jul | |

| Forecast: 4.20% | Previous: 4.10% | ||

| 13:45 | USD | Chicago PMI Aug | |

| Forecast: 44.1 | Previous: 42.8 | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 18B | ||

| 23:50 | JPY | Capital Spending Q2 | |

| Forecast: 7.90% | Previous: 11.00% | ||

Friday, Sep 1, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Aug F | 49.7 | 49.7 |

| 01:45 | CNY | Caixin Manufacturing PMI Aug | 49.4 | 49.2 |

| 06:30 | CHF | CPI M/M Aug | -0.10% | |

| 06:30 | CHF | CPI Y/Y Aug | 1.60% | |

| 07:30 | CHF | PMI Manufacturing Aug | 41.5 | 38.5 |

| 07:45 | EUR | Italy Manufacturing PMI Aug | 45.9 | 44.5 |

| 07:50 | EUR | France Manufacturing PMI Aug F | 46.4 | 46.4 |

| 07:55 | EUR | Germany Manufacturing PMI Aug F | 39.1 | 39.1 |

| 08:00 | EUR | Eurozone Manufacturing PMI Aug F | 43.7 | 43.7 |

| 08:30 | GBP | Manufacturing PMI Aug F | 42.5 | 42.5 |

| 12:30 | CAD | GDP M/M Jun | 0.20% | 0.30% |

| 12:30 | USD | Nonfarm Payrolls Aug | 170K | 187K |

| 12:30 | USD | Unemployment Rate Aug | 3.50% | 3.50% |

| 12:30 | USD | Average Hourly Earnings M/M Aug | 0.30% | 0.40% |

| 13:30 | CAD | Manufacturing PMI Aug | 49.6 | |

| 13:45 | USD | Manufacturing PMI Aug F | 47.00 | 47.00 |

| 14:00 | USD | ISM Manufacturing PMI Aug | 46.6 | 46.4 |

| 14:00 | USD | ISM Manufacturing Prices Paid Aug | 42.9 | 42.6 |

| 14:00 | USD | ISM Manufacturing Employment Index Aug | 44.4 | |

| 14:00 | USD | Construction Spending M/M Jul | 0.50% | 0.50% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Aug F | |

| Forecast: 49.7 | Previous: 49.7 | ||

| 01:45 | CNY | Caixin Manufacturing PMI Aug | |

| Forecast: 49.4 | Previous: 49.2 | ||

| 06:30 | CHF | CPI M/M Aug | |

| Forecast: | Previous: -0.10% | ||

| 06:30 | CHF | CPI Y/Y Aug | |

| Forecast: | Previous: 1.60% | ||

| 07:30 | CHF | PMI Manufacturing Aug | |

| Forecast: 41.5 | Previous: 38.5 | ||

| 07:45 | EUR | Italy Manufacturing PMI Aug | |

| Forecast: 45.9 | Previous: 44.5 | ||

| 07:50 | EUR | France Manufacturing PMI Aug F | |

| Forecast: 46.4 | Previous: 46.4 | ||

| 07:55 | EUR | Germany Manufacturing PMI Aug F | |

| Forecast: 39.1 | Previous: 39.1 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Aug F | |

| Forecast: 43.7 | Previous: 43.7 | ||

| 08:30 | GBP | Manufacturing PMI Aug F | |

| Forecast: 42.5 | Previous: 42.5 | ||

| 12:30 | CAD | GDP M/M Jun | |

| Forecast: 0.20% | Previous: 0.30% | ||

| 12:30 | USD | Nonfarm Payrolls Aug | |

| Forecast: 170K | Previous: 187K | ||

| 12:30 | USD | Unemployment Rate Aug | |

| Forecast: 3.50% | Previous: 3.50% | ||

| 12:30 | USD | Average Hourly Earnings M/M Aug | |

| Forecast: 0.30% | Previous: 0.40% | ||

| 13:30 | CAD | Manufacturing PMI Aug | |

| Forecast: | Previous: 49.6 | ||

| 13:45 | USD | Manufacturing PMI Aug F | |

| Forecast: 47.00 | Previous: 47.00 | ||

| 14:00 | USD | ISM Manufacturing PMI Aug | |

| Forecast: 46.6 | Previous: 46.4 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Aug | |

| Forecast: 42.9 | Previous: 42.6 | ||

| 14:00 | USD | ISM Manufacturing Employment Index Aug | |

| Forecast: | Previous: 44.4 | ||

| 14:00 | USD | Construction Spending M/M Jul | |

| Forecast: 0.50% | Previous: 0.50% | ||

Week Ahead – Focus Shifts Back to Data after Jackson Hole, NFP the Highlight

US

Now that we heard from Fed Chair Powell at the Kansas City Fed’s Jackson Hole Symposium, the focus shifts back to the data. This week is filled with data that will outline how quickly the economy is weakening. Consumer data will show personal income growth is not keeping up with spending, while confidence holds steady. The Fed’s favorite inflation reading is also expected to show subdued growth is holding steady on a monthly basis. Friday’s NFP report will show private sector hiring is cooling.

Over the weekend, the spotlight will be on US-China relations. US Commerce Secretary Gina Raimondo will meet with Chinese officials, striving to lower tensions between the world’s two largest economies.

The week will also be filled with Fed speak. On Monday and Tuesday, Barr speaks about banking services. On Thursday, we hear from both Bostic and Collins, while Friday contains appearances by Bostic, a couple of hours before the NFP report, and Mester on inflation later in the morning.

Eurozone

Next week is data-heavy but there are a few releases that stand out. The most notable is the HICP flash estimate for the eurozone on Thursday which is expected to drop slightly at the headline and core levels. There will be individual country releases in the days running up to this which may signal whether Thursday’s data will likely beat or fall short of expectations. ECB accounts are also released on Thursday which will be of interest considering markets now view the rate decision at the next meeting as a coin toss between 25 basis points and no change.

UK

The week starts with a bank holiday and it doesn’t get much more exciting from there. There are a few tier-three data releases and Huw Pill from the Bank of England will make appearances on Thursday and Friday.

Russia

A selection of economic data is on offer next week including unemployment on Wednesday, GDP on Thursday, and the manufacturing PMI on Friday.

South Africa

No major events next week with PPI on Thursday the only notable release. It follows CPI data this past week which fell to 4.8%, well within the SARB 3-6% target range, following a much lower 0.9% monthly reading in July.

Turkey

The CBRT surprised markets last week by hiking rates far more aggressively than expected, taking the repo rate to 25%, up from 17.5%. The move may cost people at the central bank their jobs if history is anything to go by, with President Erdogan openly no fan of higher rates. That said, he did employ these people shortly after his election victory so perhaps with that behind him, he may be more open to it while remaining vocally against. This week offers very little, with GDP on Thursday the only release of note.

Switzerland

Inflation data on Friday is expected to show prices rising 1.5% on an annual basis, slightly lower than in July and well below the SNB 2% target. The central bank hasn’t appeared satisfied though and markets are fully pricing in a hike in September, with 32% chance of it being 50 basis points. The manufacturing PMI will also be released on Friday, with retail sales on Thursday, and the KoF economic barometer and economic expectations on Wednesday.

China

Only three key economic releases to monitor for the coming week. First up, the NBS manufacturing and services PMIs for August will be out on Thursday. Another contractionary print of 49.5 is expected for the manufacturing sector, almost unchanged from July’s reading of 49.5. If it turns out as expected, it will be the fifth consecutive month of negative growth for manufacturing activities as China grapples with a weak external environment and domestic financial contagion risk that has been triggered by debt-laden property developers.

Secondly, the NBS services PMI for August is forecasted to remain surprisingly resilient at 51, almost unchanged from 51.5 in July. The services sector is still in an expansionary mode albeit at a slower pace that is likely being supported by domestic tourism.

Thirdly, the private sector-focused Caixin manufacturing PMI for August which consists of small and medium enterprises will be released on Friday, 1 September. Consensus is still expecting a contractionary reading of 49.5, almost unchanged from July’s print of 49.2. If it turns out as expected, it will be the second consecutive month of negative growth.

A slew of key earnings releases to take note of starting this Saturday, 26 August will be China Merchants Bank, and Bank of Communications followed by; BYD (Monday, 28 August), Ping An Insurance, NIO, Country Garden (Tuesday, 29 August), Agricultural Bank of China (Wednesday, 30 August), ICBC, Bank of China, China Minsheng Bank (Thursday, 31 August).

Also, market participants will be on the lookout for fiscal stimulus measures to defuse the $23 trillion debt bomb owed by local governments, financial affiliates, and property developers. On Friday, 25 August, China policymakers unveiled a further easing of its home mortgage policies that scrap a rule that disqualifies first-time homebuyers who had a mortgage that is fully repaid from being considered a first-time buyer in major cities in an attempt to boost up residential property transactions.

India

Two key data to focus on. Q2 GDP on Thursday where the consensus is expecting a further economic growth expansion to 7% y/y in Q2, a further acceleration from 6.1% y/y recorded in Q1.

Lastly, the manufacturing PMI for August will be released on Friday where it is being forecasted to come in at 57, almost unchanged from the July reading of 57.7 which will indicate a 26th straight month of growth expansion for manufacturing activities.

Australia

Retail sales for July will be out on Monday, with a recovery to 0.3% m/m from -0.8% m/m in June.

On Wednesday, the important monthly CPI indicator for July will be out and the consensus forecast is another month of cooling to 5.2% from 5.4% in June. If it turns out as expected, RBA may have more reasons to justify its current pause at 4.1% for two consecutive meetings. Its next monetary policy meeting will be on 5 September, and as of 24 August, the ASX 30-day interbank cash rate futures have priced in a 12% chance of a rate cut to 3.85% (25 bps cut).

New Zealand

A quiet week with the only focus on the ANZ business confidence indicator for August on Thursday followed by ANZ consumer confidence for August on Friday.

Japan

The action comes mid-week. Consumer confidence for August is released on Wednesday and is expected to be almost the same at 37.2 versus July’s 37.1.

On Thursday, we will have retail sales and industrial production for July. Growth in retail sales is expected to slip slightly to 5.4% y/y from 5.9% in June. Meanwhile, industrial production is expected to contract to -1.4% m/m from 2.4% m/m in June, and -0.7% y/y is forecasted from 0% y/y recorded in June.

Singapore

The sole key data to monitor will be the producer prices index for July out on Tuesday with another month of negative growth forecasted at -9% y/y, a slower pace of contraction from -14.3% recorded in June. It would be the 7th consecutive month of decline.

Economic Calendar

Saturday, Aug. 26

- Kansas City Fed’s annual symposium concludes with speeches from BOE’s Broadbent

Sunday, Aug. 27

Economic Data/Events

- China industrial profits

- US Commerce Secretary Raimondo meets with Chinese officials

Monday, Aug. 28

Economic Data/Events

- Australia retail sales

- Mexico trade

- ECB’s Nagel, de Cos, and Holzmann, as well as Danish central bank governor Signe Krogstrup, speak at the Alpbach forum in the Austrian Tyrol

- UK financial markets closed for the Summer Bank Holiday.

Tuesday, Aug. 29

Economic Data/Events

- US Conference Board consumer confidence

- Czech Republic GDP

- Japan unemployment

- Mexico international reserves, GDP

- Sweden GDP

- UK Foreign Secretary Cleverly to visit China and discuss war in Ukraine

- Bank of Finland news conference on monetary policy

- US bank regulators expected to propose requirements for smaller banks

- Informal meeting of EU defense ministers in Spain

Wednesday, Aug. 30

Economic Data/Events

- US Q2 GDP(Prelim), wholesale inventories, pending home sales

- Australia CPI, building approvals

- Eurozone economic confidence, new car registrations, consumer confidence

- Germany CPI

- New Zealand building permits

- Russia unemployment

- Spain CPI

- Bank of China earnings

Thursday, Aug. 31

Economic Data/Events

- US personal spending and income, initial jobless claims

- China manufacturing PMI, non-manufacturing PMI

- Eurozone CPI, unemployment

- Finland GDP

- France CPI, GDP

- Germany unemployment

- Hong Kong retail sales

- India GDP

- Italy unemployment, CPI

- Japan industrial production, retail sales

- Mexico unemployment

- Poland CPI

- South Africa trade balance

- Thailand trade

- Turkey GDP

- ECB releases account of July monetary policy meeting

- EU foreign affairs ministers meet in Toldeo, Spain

- ECB’s Schnabel speaks at inflation conference organized by ECB and the Cleveland Fed

- ECB Executive Board member Luis de Guindos speaks at seminar organized by Universidad Internacional Menéndez Pelayo in Santander, Spain

- BOE chief economist Huw Pill and Fed’s Bostic speak at South African Reserve Bank biennial conference

Friday, Sept. 1

Economic Data/Events

- US unemployment, nonfarm payrolls, light vehicle sales, ISM manufacturing, construction spending.

- Canada GDP

- China Caixin manufacturing PMI

- European Final manufacturing PMI readings: Eurozone, Germany, France, and the UK

- Hungary GDP

- India manufacturing PMI

- Italy GDP

- Japan capital spending

- Singapore to hold presidential vote

- South African Reserve Bank governor Kganyago, Fed’s Bostic, and the BOE’s Huw Pill speak at the South African Reserve Bank conference

- Fed’s Collins speaks on the role of community colleges at a virtual event

- Ambrosetti Forum in Italy

Sovereign Rating Updates:

- Belgium (Fitch)

- Hungary (Moody’s)