Sample Category Title

Week Ahead – Volatility to Continue as US Jobs and Inflation Data on the Way

Markets have been taunted by shifting Fed expectations over the past week and there’s likely to be more anguish for investors in the next few days as crucial payrolls and inflation numbers are coming up. The August jobs report and PCE inflation readings will be closely watched amid signs the US economy is starting to lose steam fast. The Eurozone economy is going through an even rougher patch, putting the spotlight on flash CPI figures. China has been another source of concern and its PMI prints for August will be important too.

NFP report and PCE inflation to raise the stakes

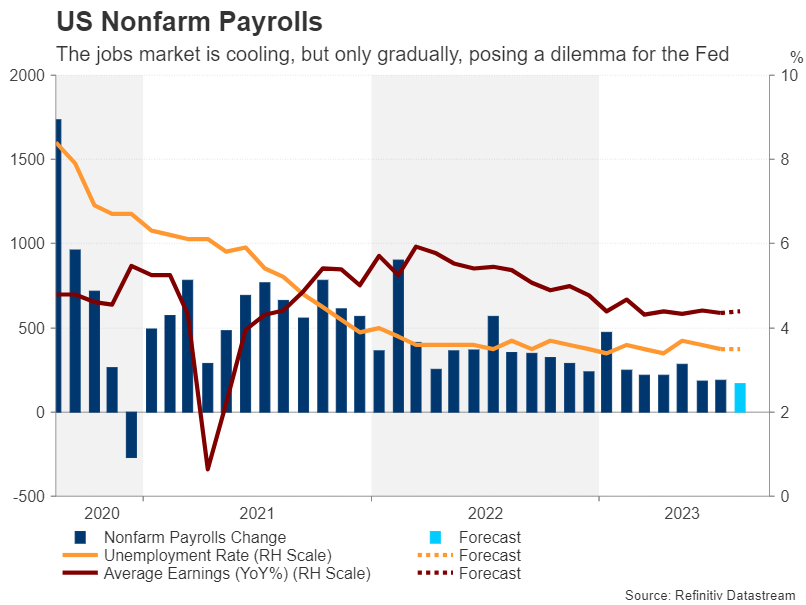

It's payrolls week in the United States and the August numbers will be eagerly awaited on Friday as, apart from some signs already that jobs growth is slowing, the latest S&P Global PMI survey raised a few alarm bells about hiring conditions. Nonfarm payrolls are projected to have increased by 170k in August, moderating from the 187k jobs added in July.

The unemployment rate is expected to hold steady at 3.5%, while average hourly earnings growth is also forecast to remain unchanged at 4.4% y/y in August.

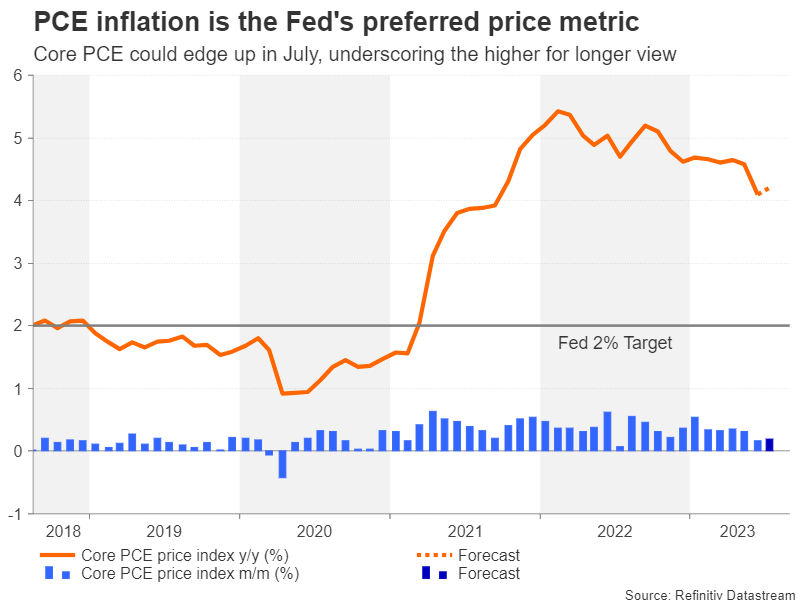

Also attracting a lot of attention is Thursday’s personal income and outlays report, which contains the all-important core PCE price index. With both personal income and personal consumption holding up surprisingly well against the backdrop of rising borrowing costs, another solid reading for August would ease worries about a slowing economy. What has been more of concern, however, is the stickiness of the Fed’s favourite inflation gauge.

Although core PCE did finally take a dive in July to fall to 4.1% y/y, that’s still double the Fed’s target of 2%. Furthermore, core PCE could edge up to 4.2% in July, so those investors hoping for further declines in this particular metric are likely to be disappointed.

Yet, with the economic risks tilted somewhat more towards a recession than a soft landing after the PMI releases, if the above indicators are broadly better than expected, it’s unlikely that rate hike odds would rise very significantly. On the other hand, an overall soft or even poor set of data could lead investors to further up their rate cut bets for next year, punishing the US dollar but probably boosting Wall Street.

Ahead of those big reports, the Conference Board’s consumer confidence index will be watched on Tuesday along with the JOLTS job openings for July. On Wednesday, the second estimate for Q2 GDP growth and ADP employment report will keep the top-tier data flowing. Pending home sales are due on Wednesday too and the Chicago PMI will follow on Thursday.

Wrapping up the US agenda on Friday will be the ISM manufacturing PMI, which will get to have the final say on how markets close for the week. It’s expected to come in at 46.6 for August, a very modest improvement over the prior month.

Will Eurozone inflation keep falling?

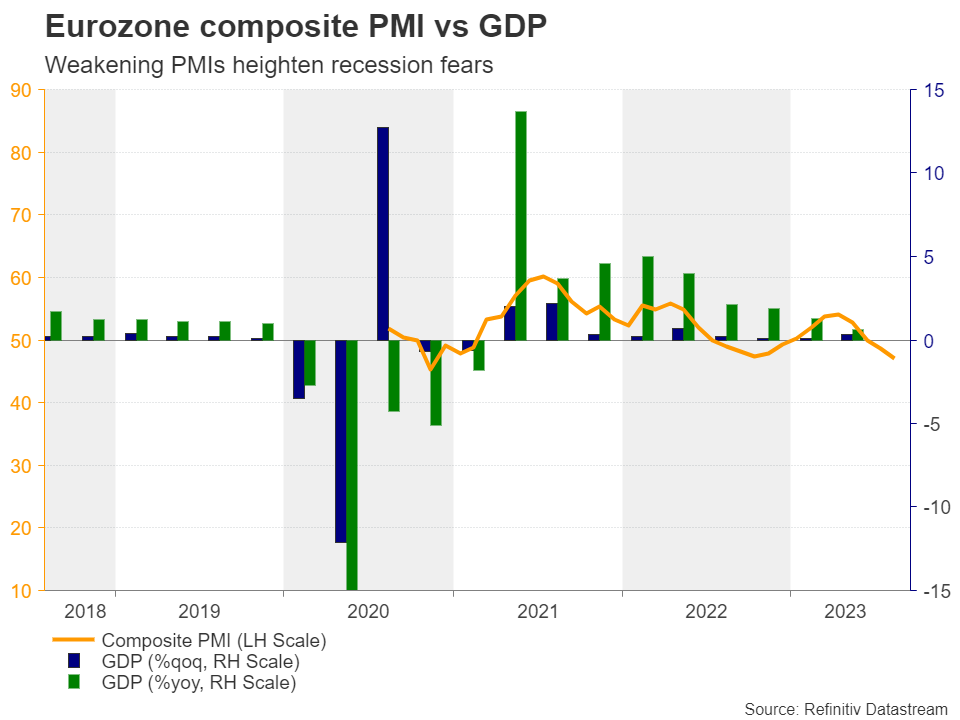

Across the pond, recession fears are heightened even more so, as there appears to be no relief for European businesses lately. Manufacturing activity did improve slightly in August, but services output slumped deeper into contraction territory. With interest rates at a record high since the euro’s inception, energy prices rising again and demand weakening in key export markets such as the US and China, one of the few things Europeans can celebrate about is that inflation is on the way down.

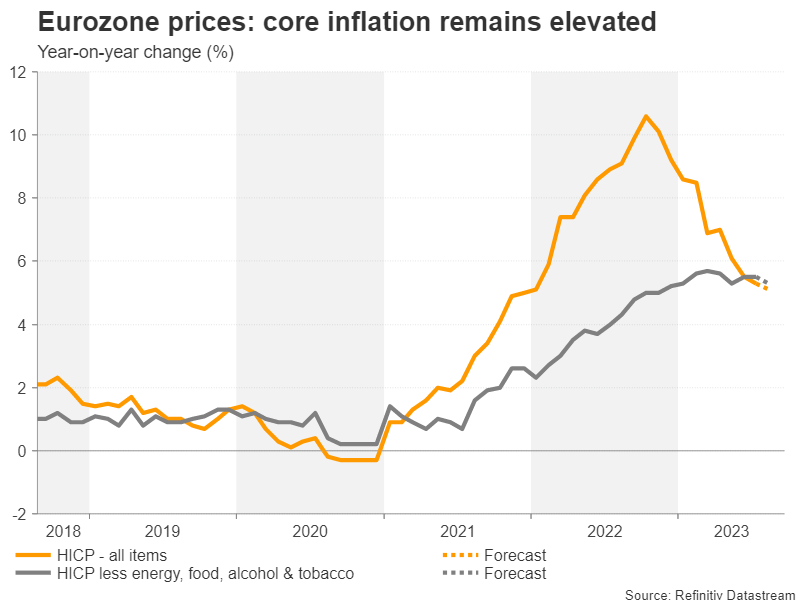

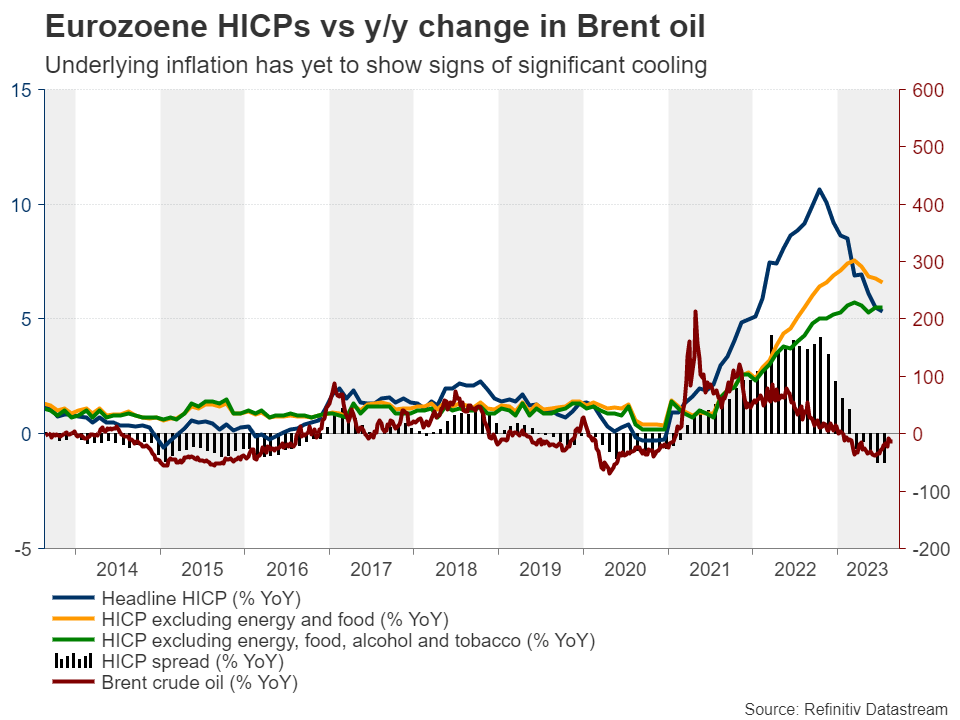

The flash estimates for August are due on Thursday and should show further declines. The headline rate of CPI is expected to dip from 5.3% to 5.1% y/y, while core CPI that strips out food, energy, alcohol and tobacco prices is forecast to ease from 5.5% to 5.3% y/y.

The European Central Bank has repeatedly stressed that getting core CPI down to 2% is its main priority and will likely relay that message in the minutes of the July meeting that will be published on Thursday. However, a less hawkish-than-anticipated tone is possible as the recent deceleration in growth is raising doubts about the need for further rate increases.

The euro could halt its slide and firm somewhat should rate hike bets for September, which at the moment is a coin toss, be ratcheted up from any upside surprises. But even then, the gains would be limited as the risk of a more severe downturn would also rise.

Battered aussie eyes Chinese PMIs and local CPIs

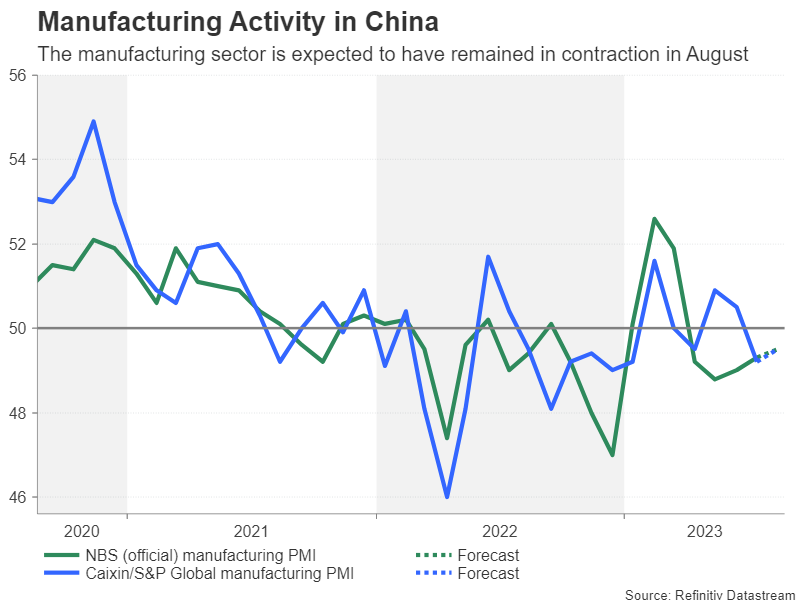

Amid frustration about China’s drip-feed stimulus, announcements on new support measures have become almost a daily occurrence. Yet, for the markets, a one-off bazooka is seen as having a bigger impact. In the absence of one, all investors can do is to look for signs that the incremental policy tweaks are starting to generate some momentum in the economy.

There could be some clues of this on Thursday when China reports its manufacturing and non-manufacturing PMIs for August. The Caixin manufacturing PMI will follow on Friday.

The Australian dollar, which is viewed as a liquid proxy for China-related risks, has taken quite a beating lately following a series of downbeat Chinese data. China’s slowdown is already being felt across the Australian economy as pointed by the recent dismal PMIs.

Next week, the focus will be on domestic barometers, comprising July retail sales (Monday), monthly CPI prints (Wednesday) and Q2 capital expenditure (Thursday).

In recent meetings, the Reserve Bank of Australia had become more concerned about growth than inflation. If the annual CPI rate maintains a downward course in July, the RBA would have little incentive to hike rates again, and unless there is a turnaround in risk sentiment, the aussie looks poised to remain under pressure.

In other data, second quarter GDP growth figures are due out of Canada on Friday, while in Japan, there’s a slew of releases, including preliminary industrial output for July on Thursday and the Ministry of Finance’s estimate of Q2 capital expenditure on Friday. The latter will provide an indication on whether or not the preliminary GDP reading of 6.0% annualized growth is likely to be revised up or down.

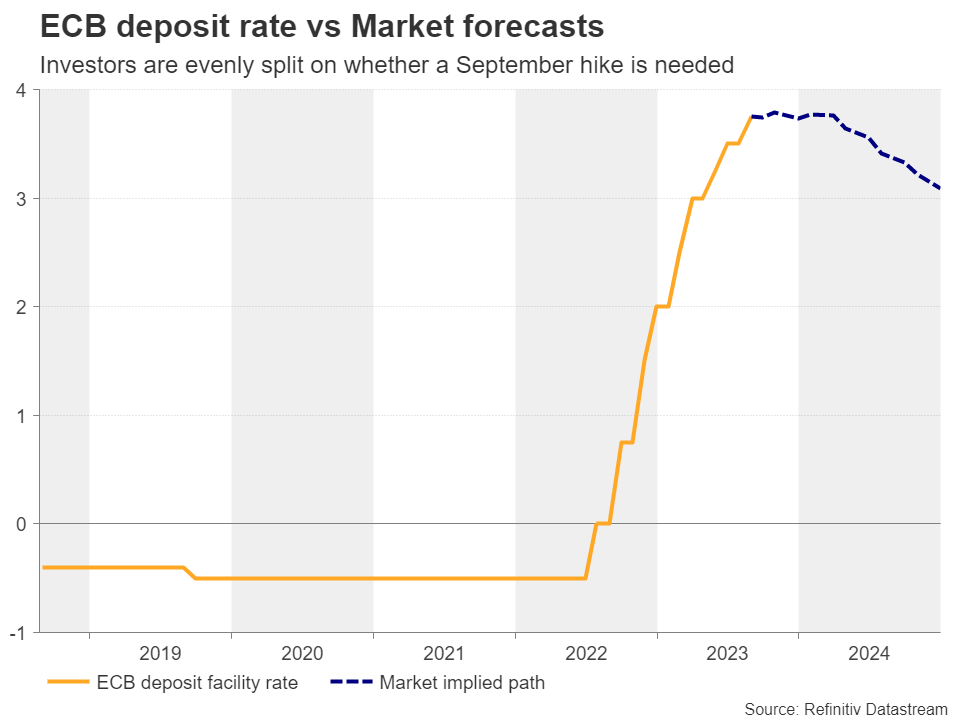

As ECB Hike Dilemma Sharpens, Traders Seek Clarity in Inflation Numbers

With Lagarde taking off her ultra-hawk armor at the latest ECB gathering and last week’s business surveys pointing to deepening wounds for the Euro area economy, investors have become skeptical as to whether the ECB should press the hike button again in September. Will the Eurozone preliminary inflation numbers, due out on Thursday at 09:00 GMT, clear the fog? And could traders become willing to buy the euro again?

To hike or not to hike?

At the July ECB gathering, policymakers decided to raise interest rates by 25bps to a historic high as it was widely anticipated, but they abstained from committing to further moves. At the press conference following the decision, President Lagarde appeared way less hawkish than she did at previous gatherings, acknowledging that the economic outlook has deteriorated and replying with a “decisive maybe” when asked whether they are planning to hike again in September.

Since then, the CPI data for July revealed that headline inflation dropped to 5.3% year-on-year from 5.5%, but the core metric that excludes energy, food, alcohol and tobacco, held steady at 5.5% yoy. Combined with a rise in services inflation to a new record of 5.6% yoy, this is far from suggesting that the ECB’s job is done.

Nevertheless, the ECB’s soft rhetoric and a streak of data pointing to continued economic weakness in the region have made investors skeptical as to whether officials should raise rates again at the September 14 gathering, and the decision now boils down to a coin toss according to money markets. Preliminary business surveys for August have rung the recession bells, with the service-sector PMI falling into contractionary territory for the first time since December, joining the manufacturing index and dragging the composite down to 47.0 from 48.6. Will the ECB take the sidelines in order to protect the overall economy, or will they stay committed to bringing inflation to heel at any cost?

Further inflation cooling to bolster the pause case

With the ECB trapped between a rock and a hard place, Thursday’s flash CPI numbers could attract special attention as they could tilt the scale either towards a September hike or a pause. The headline CPI rate is expected to have declined further to 5.1% from 5.3%, and the ultra-core that excludes energy, food, alcohol and tobacco, is forecast to have slipped to 5.3% yoy from 5.5%.

Further slowdown in inflation amid a bleeding economy could convince market participants that Lagarde and her colleagues could wait for a while before deciding whether and when further hikes are appropriate. In other words, a pause in September could turn out to be the base case scenario in the eyes of investors.

Euro/dollar may continue drifting south

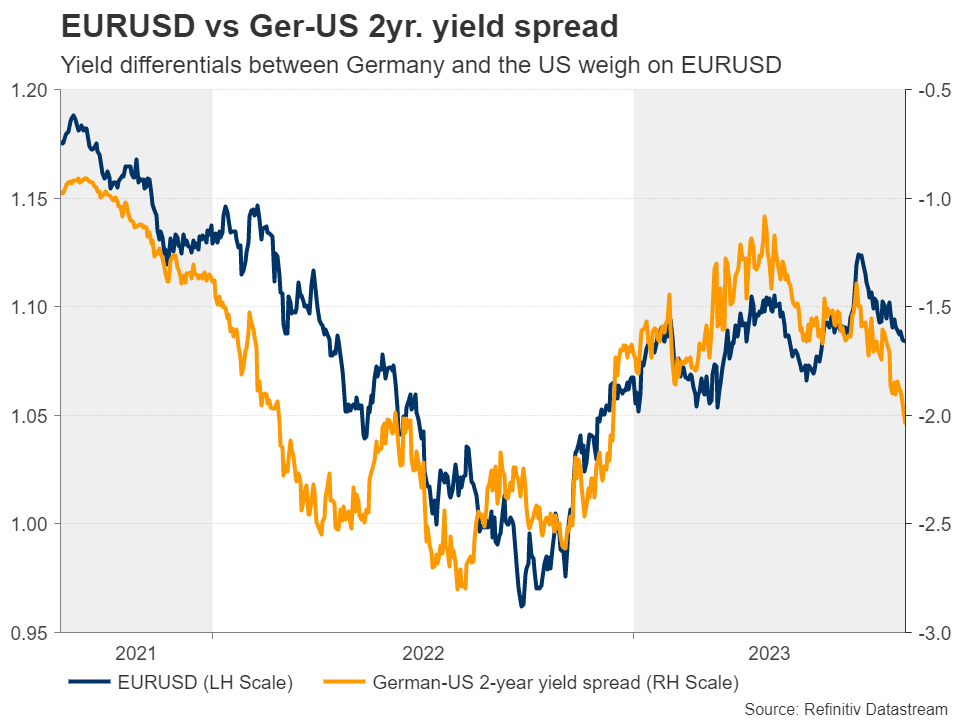

Something like that could result in further selling in the euro, especially against its US counterpart which has been enjoying inflows, not only because traders are re-examining the case of interest rates in the US staying higher for longer than previously thought, but also as a safe haven. Concerns surrounding the performance of the Chinese economy have intensified as the latest stimulus measures by Chinese authorities and the People’s Bank of China (PBOC) failed to revive market sentiment.

Euro/dollar fell below the support (now turned into resistance) zone of 1.0830 on Thursday and broke below the 200-day exponential moving average (EMA) on Friday. Combined with the fact that the pair is trading well below the prior uptrend line drawn from the low of September 26, these technical signs increase the likelihood for further declines, at least until the critical area of 1.0665, the break of which may be the confirmation signal for a full-scale bearish reversal.

But let’s not ignore some upside risks

Having said all that though, besides painting an ugly economic picture, the PMIs revealed that inflationary pressures have picked up in August, both in terms of average selling prices and input costs, although both measures are still pointing to far weaker inflation rates than the ones seen during the two years prior to this summer.

This means that there may be some upside risks surrounding Thursday’s CPI figures. Ergo, in the case that inflation reaccelerates somewhat instead of slowing further, the euro may rebound on renewed speculation about a September ECB hike. Nonetheless, a lot more is needed for euro/dollar to re-enter an uptrend orbit. Eurozone data may have to start showing signs of stabilization and from a technical perspective, the pair may need to rebound and return above the key resistance of 1.1070.

Weekly Focus – Slowing Down

Financial stress in China and weak US and euro PMIs set the scene for global markets this week. It started out with continued focus on China where the housing crisis and financial risks from shadow banking has resurfaced. Chinese financial stress eased somewhat during the week, though, as there was no new bad news to fuel a further sell-off. It does not mean the problems are no longer there, however. We see increasing downside risks to Chinese growth and have revised down the annual growth estimate to 4.8% from 5.2%, see Resarch China: downside risks on the rise - scenarios for Chinese growth, 21 August. We expect Chinese policy makers to step up stimulus to stave off a crisis but there is a risk they continue to be two steps behind and growth slows even more.

PMIs out of the US and the euro area added to the picture of a slowing global economy. In the US Composite PMI dropped to 50.4 in August from 52.0 in July with declines in both manufacturing and services. The European PMI figures also came out much weaker than expected with services showing renewed signs of slowing. The German Services PMI numbers stood out with a massive 5 index points decline, which has only happened three times before with the latest being in March 2020 during the Covid-19 lockdown. The service sector has been the engine that kept activity running at a decent level while the manufacturing sector has been in recession for a while. However, it now seems the service sector is finally losing some steam as well. It will be interesting to see if this finally translates into more weakness in labour markets, which have stayed surprisingly resilient over the past year despite weaker growth.

The BRICS countries this week expanded the cooperation with six new members being Argentina, Ethiopia, Egypt, Saudi Arabia, United Arab Emirates and Iran. BRICS' stated goal is to be a champion for the Global South working for a multipolar world and with the increase in members they now represent 37% of global GDP (PPP terms) and 46% of global population. We could very well see a further expansion of the group in the years to come.

Bond yields started the week higher but the soft PMI data led markets to rethink the need for further central banks hikes and yields turned lower again. That was until markets started to fret about Jackson Hole and coming speeches by Governors of both the Fed and ECB, Jerome Powell and Christine Lagarde. Then yields came back up. Equities rallied on the softer central bank outlook despite the economic weakness but fell back again when jitters rose going into Jackson Hole.

Looking ahead, it's time for US labour market data again, with main focus naturally on the August non-farm payrolls, where the gradual cooling in employment growth has likely continued. We're looking for +160k. The Fed pays close attention to the development in average hourly earnings and another print at 0.4% m/m or above would likely be a hawkish signal for the markets. JOLTS data for July is also up for release on Tuesday where job openings have been a good leading indicator for wage growth as well. US ISM Manufacturing and July PCE data is also due for release. In China, PMI for August will be in focus while Flash CPI inflation in the euro area will be a key input for the coming ECB meeting in September.

Is the Price of Natural Gas Forming a New Trend?

The US Energy Information Administration said on Thursday that natural gas inventories in US storage rose by 18 billion cubic feet in the week ended Aug. 18. That was below the 29 billion cubic feet increase forecast by analysts polled by S&P Global Commodity Insights.

It is possible that market participants thought that insufficient filling of storage facilities will lead to a rise in gas prices in the coming winter. According to the forecast of the International Energy Agency (IEA), the price of gas will peak at USD 3.44/MMBtu in December 2023 (approximately +36% from current levels).

The natural gas price chart shows that:

→ in July-August, a series of rising supports was formed;

→ the peak of August is higher than the peak of June, which in turn is higher than the peak of May.

A sequence of higher extremes could indicate that the market is in an uptrend that could bring the price closer to the IEA's price targets. The nearest resistance on this way is the level of 2.78, which in July-August repeatedly influenced the price dynamics.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Sunset Market Commentary

Markets:

“We will keep at it until the job is done”. Fed chair Powell’s long-awaited speech at the Jackson Hole Symposium by the Kansas City Fed finally arrived. His message is the same as last year when he scared markets in an eight-minute address that the Fed will stick to a restrictive monetary policy. This time around markets were more prepared for the communication though. “Although inflation has moved down from its peak—a welcome development—it remains too high. We are prepared to raise rates further if appropriate, and intend to hold policy at a restrictive level until we are confident that inflation is moving sustainably down toward our objective.” “The lower monthly readings for core inflation in June and July were welcome, but two months of good data are only the beginning of what it will take to build confidence that inflation is moving down sustainably toward our goal. We can’t yet know the extent to which these lower readings will continue or where underlying inflation will settle over coming quarters. Twelve-month core inflation is still elevated, and there is substantial further ground to cover to get back to price stability.” Overall, Fed Chair’s Powell didn’t really alter his message from previous press conferences. He continues to err on the hawkish side of expectations. US Treasuries spiked lower in a first reaction as Powell kept the possibility of a (September) rate hike firmly alive. Money markets only discount a one in five probability for that to happen. US yield changes currently range between flat (2-yr) and -2.8 bps (30-yr). The move didn’t last though. The dollar couldn’t build on recent gains, currently losing some ticks. EUR/USD changes hands around 1.0830. US stock markets rise between 0.5% and 1%. Interestingly, topics like the possibility of higher neutral rate or raising the inflation target weren’t touched upon during his speech.

News & Views:

The monthly business survey published by the National Bank of Belgium, which started to fall in April, levelled off in August (-14.9 from -14.8 in July). However, stabilization compared to the previous month masks disparate developments at sector level. Business climate improved in trade as respondents expect higher demand and increased their orders with suppliers. Still employment expectations in the sector were more muted. In the building industry (-7.2 from -5.8) confidence is suffering from much gloomier demand expectations and a less favourable assessment of order books. Confidence in manufacturing stabilized (-16.1 from -16.0), influenced by a fall in all underlying components, with the exception of demand expectations, which rose strongly. After two months of sharp decline, general market demand expectations also recovered in the business-related services, due to an improved assessment of current activity. Still, business leaders expressed a much more reserved opinion when it came to expectations of their own activity. All in all, services confidence remained fairly stable (-8.8 from -9.0).

Statistics Sweden today reported several data series including lending data and data on real estate prices. The Real Estate Price index (for one to two-dwelling buildings) in the second quarter declined another 1% compared to the previous quarter and was 12% lower compared to the same quarter last year. Other data series showed that the annual growth rate of lending to households slowed to just 0.9% Y/Y (from 1.1% Y/Y in June). Mortgages accounted for 83% of total lending to households. The amount of mortgages rose 1.3% Y/Y in July. The annual growth rate of loans for consumption eased to 0.6% Y/Y (accounting for 6% of household lending). Lending to non-financial corporates still was 7% Y/Y in July. Labour market data showed an unexpected decline in the unemployment rate (SA) from 7.9% to 7%. The number of people in the labour force and the number of employed people were about 120k higher compared to last year. Both the labour force participation rate (75.7%) and employment rate rose (73.1% up 1.3% Y/Y).At EUR/SEK 11.89 the Swedish krone continues to trade within reach of the all-time low level against the euro (EUR/SEK 11.96) touched earlier this week. The Riksbank raised its policy rate to 3.75% at the end of June meeting and is expected to hike the policy rate at least one more time, starting with a step to 4% at the September 21 meeting. July CPIF inflation was unchanged at 6.4% Y/Y. Core inflation stays high at.8% Y/Y.

Powell signals Fed’s readiness to tighten further amid inflation concerns

Fed Jerome Powell made clear the Central Bank's stance on the current inflation environment in his opening remarks at the Jackson Hole Symposium. Noting a decline from peak inflation rates, Powell emphasized, "Although inflation has moved down from its peak—a welcome development—it remains too high."

Demonstrating Fed's commitment to fight inflation, he added, "We are prepared to raise rates further if appropriate, and intend to hold policy at a restrictive level until we are confident that inflation is moving sustainably down toward our objective."

Acknowledging the recent decline in core inflation during June and July, Powell cautioned against reading too much into short-term data. "The lower monthly readings for core inflation in June and July were welcome, but two months of good data are only the beginning of what it will take to build confidence that inflation is moving down sustainably toward our goal," he remarked.

Drawing a metaphor to describe the present economic landscape, Powell stated, "As is often the case, we are navigating by the stars under cloudy skies." Under such conditions, he emphasized the importance of a strategic and risk-aware approach.

Elaborating on the Fed's forward plan, Powell said, "At upcoming meetings, we will assess our progress based on the totality of the data and the evolving outlook and risks. Based on this assessment, we will proceed carefully as we decide whether to tighten further or, instead, to hold the policy rate constant and await further data."

This clear yet cautious messaging from Powell reiterates the Fed's commitment to ensuring price stability and managing the inflationary pressures faced by the economy, while also emphasizing a data-driven and measured approach to monetary policy adjustments.

Market Treads Cautiously Ahead of Powell and Lagarde’s Speeches

As the financial world gears up for the much-anticipated remarks from Fed Chair Jerome Powell and ECB President Christine Lagarde, market participants are treading with caution. Dollar has started to retreat, shedding some of its recent impressive gains. Simultaneously, Euro grapples to find solid ground elsewhere amidst a mixed backdrop.

Both leading central bank figures hold the potential to introduce unexpected elements in their addresses, and market stakeholders are all too aware of the volatility this could trigger. The spotlight on Powell will shine particularly on his interpretation of the juxtaposed trends of softening headline inflation and the persistence of service sector prices. Additionally, the consequences of robust consumer spending will be keenly observed.

In the European context, the grapevine is abuzz with speculation. Following the recently revealed PMI data, which fell well short of market expectations, rumors are rife that Lagarde might hint at a monetary policy pause in September. Such a move, if communicated or even hinted at, could instigate significant market shifts as the week concludes.

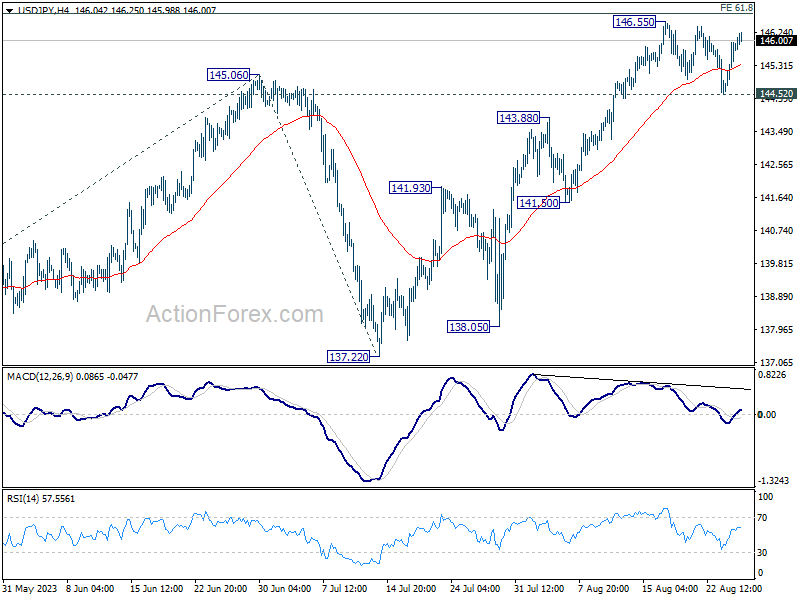

Technically, to indicate a near term bearish reversal in Dollar, 1.0929 resistance in EUR/USD, 1.2799 resistance in GBP/USD, 0.8758 support in USD/CHF will need to be taken out decisively Meanwhile, for Dollar to confirm underlying bullish momentum, UUSD/JPY and USD/CD should break through 146.55 and 1.3602 resistance respectively with ease. The market awaits these developments with bated breath.

In Europe, at the time of writing, FTSE is up 0.66%. DAX is up 0.65%. CAC is up 0.88%. Germany 10-year yield is up 0.0368 at 2.553. Earlier in Asia, Nikkei dropped -2.05%. Hong Kong HSI dropped -1.40%. China Shanghai SSE dropped -0.56%. Singapore Strait Times rose 0.29%. Japan 10-year JGB yield rose 0.0110 to 0.660.

German Ifo business climate sinks for fourth month, economy faces uphill battle

Germany's economic outlook has dimmed yet again, as indicated by the Ifo Business Climate Index which registered its fourth consecutive monthly drop. In August, the index tumbled from 87.4 to 85.7. The downward trajectory was visible across both Current Situation Index, which slid from 91.4 to 89.0, and Expectations Index, which descended from 83.6 to 82.6.

A sectoral breakdown of the data highlighted broad-based concerns. Manufacturing saw a decline from -13.9 to -16.6. Meanwhile, Services sector took a more significant hit, plummeting from a modest 1.0 to a concerning -4.2. Trade and Construction sectors also continued their downward spiral, recording readings of -25.5 and -29.3 respectively, from their previous standings of -23.7 and -24.6.

Ifo's commentary on the data was stark. They noted, "Assessments of the current situation fell to their lowest level since August 2020." The institution also flagged a growing pessimism among companies regarding the forthcoming months, adding, "The German economy is not out of the woods yet."

Chinese stocks falter despite efforts to boost confidence

In a bid to shake off the lethargy that has seen Chinese stocks on a decline for three consecutive weeks, authorities have taken notable measures. Yet, the efforts seem to have fallen short. Reports suggest that the Chinese government is contemplating a reduction in stamp duty on stock trading by up to 50%. This is seen as a move to rejuvenate waning investor confidence.

The China Securities and Regulatory Commission also made an endeavor to put concerns at bay. The regulatory body convened a virtual meeting with multiple global financial institutions, emphasizing the resilience and potential of China's economic landscape. But these overtures seem to have done little in swaying investor sentiment, at least for now.

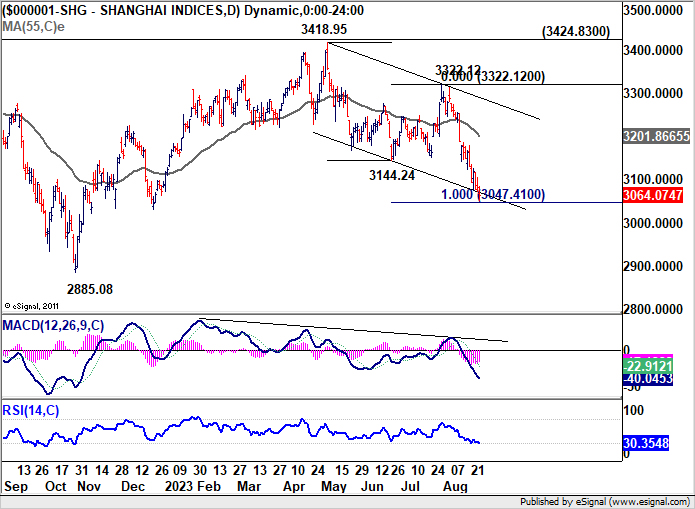

The Shanghai SSE extended the whole down trend from 3418.95 to close at 3064.07. It's now in proximity to 100% projection 3418.95 to 3144.24 from 3322.12. Strong rebound from current level, followed by firm break of 3144.24 support turned resistance, will argue that the decline has completed already. The three wave structure would also affirm that it's merely a corrective move.

However, sustained break of 3047.41 could prompt further downside acceleration towards 2885.08 (2022 low), and open up more medium term bearish bias. The situation could probably unfolded next week and that would be an important risk factor in Asia, in addition to the aftermath of Jackson Hole in the US.

USD/JPY Daily Outlook

Daily Pivots: (S1) 144.98; (P) 145.47; (R1) 146.34; More...

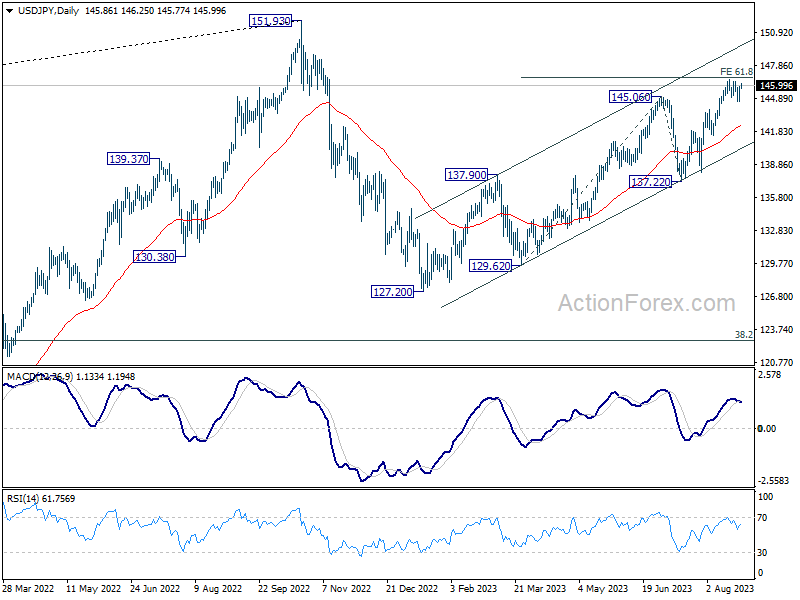

Intraday bias in USD/JPY stays neutral as it's still bounded in range. On the upside, sustained break of 61.8% projection of 129.62 to 145.06 from 137.22 at 146.76 will pave the way to retest 151.93 high. However, considering bearish divergence condition in 4H MACD, firm break of 144.52 support will be a sign of reversal, and turn bias back to the downside for 55 D EMA (now at 142.45).

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Rise from 127.20 is seen as the second leg of the pattern and could still be in progress. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Y/Y Aug | 2.90% | 3.00% | 3.20% | |

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Aug | 2.80% | 2.90% | 3.00% | |

| 23:30 | JPY | Tokyo CPI ex Food Energy Y/Y Aug | 4.00% | 4.00% | ||

| 23:50 | JPY | Corporate Service Price Index Y/Y Jul | 1.70% | 1.20% | 1.20% | 1.40% |

| 06:00 | EUR | Germany GDP Q/Q Q2 F | 0.00% | 0.00% | 0.00% | |

| 08:00 | EUR | Germany IFO Business Climate Aug | 85.7 | 86.6 | 87.3 | 87.4 |

| 08:00 | EUR | Germany IFO Current Assessment Aug | 89.0 | 89.8 | 91.3 | 91.4 |

| 08:00 | EUR | Germany IFO Expectations Aug | 82.6 | 83.8 | 83.5 | 83.6 |

| 14:00 | USD | Michigan Consumer Sentiment Index Aug F | 71.2 | 71.2 |

Chinese stocks falter despite efforts to boost confidence

In a bid to shake off the lethargy that has seen Chinese stocks on a decline for three consecutive weeks, authorities have taken notable measures. Yet, the efforts seem to have fallen short. Reports suggest that the Chinese government is contemplating a reduction in stamp duty on stock trading by up to 50%. This is seen as a move to rejuvenate waning investor confidence.

The China Securities and Regulatory Commission also made an endeavor to put concerns at bay. The regulatory body convened a virtual meeting with multiple global financial institutions, emphasizing the resilience and potential of China's economic landscape. But these overtures seem to have done little in swaying investor sentiment, at least for now.

The Shanghai SSE extended the whole down trend from 3418.95 to close at 3064.07. It's now in proximity to 100% projection 3418.95 to 3144.24 from 3322.12. Strong rebound from current level, followed by firm break of 3144.24 support turned resistance, will argue that the decline has completed already. The three wave structure would also affirm that it's merely a corrective move. However, sustained break of 3047.41 could prompt further downside acceleration towards 2885.08 (2022 low), and open up more medium term bearish bias.

Investors will likely be keeping an eagle eye on developments next week. The unfolding situation in China's stock market stands as a significant risk factor in Asia, especially when juxtaposed with the aftermath of the Jackson Hole symposium in the US.

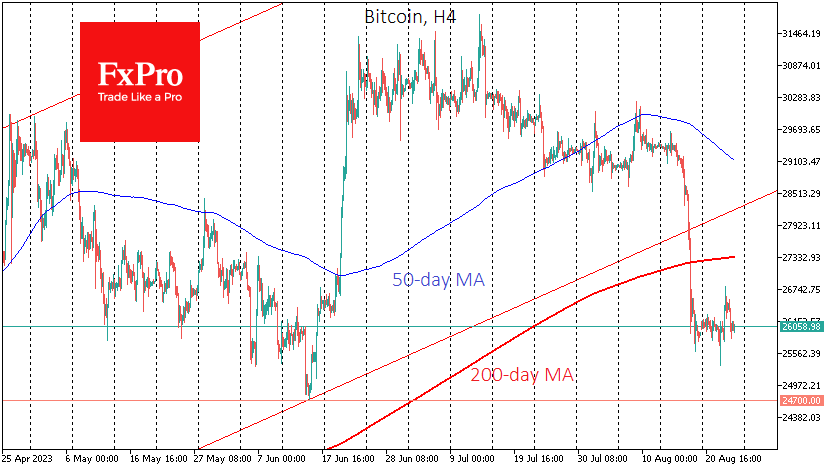

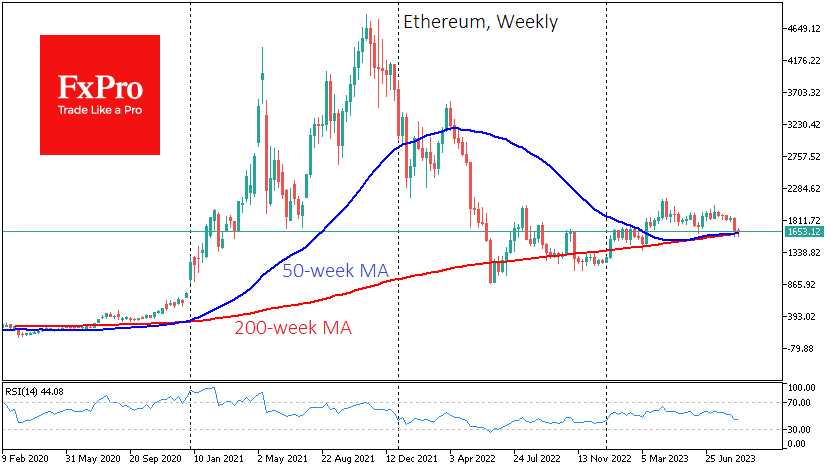

Crypto Market Tamed on the Lower Ladder

Market picture

Thursday’s sell-off in the US stock market forced cryptocurrencies to bounce back from the previous day. As a result, the crypto market capitalisation is back at $1.05 trillion (-1.8% in 24 hours). Solana (-5.2%) and XRP (-3.3%) led the decline among the top altcoins, while Ethereum held up relatively well, losing 1.3%.

The Cryptocurrency Fear and Greed Index is in “Fear” territory for the latest week, with a current reading of 39. By this measure, the market is far from oversold and not yet attractive to bargain hunters.

Bitcoin has entered another long horizontal consolidation and is going down another ladder. The previous two ladders were from late June to mid-July (around $30.5K) and from late July to mid-August (around $29.3K).

Ethereum is consolidating around $1650, a significant pivot level of the last 12 months. A failure below this level could start a capitulation that could take the price to $1200 within a week or two. The ability to hold here would indicate buyer support, potentially kick-starting a rally.

However, we still see a higher probability of a continued downturn in the crypto market in the coming months.

News background

Social media-famous crypto analyst Justin Bennett warned that Bitcoin could fall as low as $14,000. According to him, BTC has fallen out of the bullish channel it has been in for about a decade. A likely global economic recession and falling stock markets compound the risks.

Bitcoin will halve to $35,000 by April next year and rise to a new record high of $148,000 by July 2025, Pantera Capital predicts, based on historical data from past growth cycles.

Donald Trump’s NFTs surged in value following his interview with US TV host Tucker Carlson. The trading volume of the politician’s NFT collection increased by nearly 1,000% overnight.

Binance stopped supporting cryptocurrency cards in Latin America and the Middle East. Binance launched the first bank cards with cryptocurrency support in 2020.

The decentralised payment protocol Solana Pay has integrated its plugin with the e-commerce platform Shopify. In the first phase, only USDC stablecoin is available for payment.

USD/JPY Breaks Above 146, Tokyo Core CPI Dips to 2.8%

- Tokyo Core CPI gains 2.8%, less than expected

- Powell and Ueda to speak at Jackson Hole symposium

USD/JPY has posted small gains on Friday, enough to push above the symbolic 146 line. On the data calendar, Tokyo Core CPI dipped lower and Fed Chair Powell addresses the Jackson Hole Symposium later today.

Tokyo Core CPI eases to 2.8%

Japan released the Tokyo Core CPI earlier today. This is the first inflation release of the month, making it a key event. In August, Tokyo Core CPI rose 2.8% y/y, down from 3.0% in July and just under the consensus estimate of 2.9%. Despite the drop in inflation, the indicator has remained above the Bank of Japan’s 2% target for some fifteen months. Earlier in the month, the so-called “core-core index”, which excludes fresh food and energy, remained at 4.0%. This points to broad inflationary pressure and raises questions about the BoJ’s insistence that inflation is transient.

The BoJ has said it will not exit its ultra-loose monetary policy until wage growth rises enough to keep inflation sustainable around 2%. Still, the markets have been burned before by the BoJ making unexpected moves and are on guard for the BoJ tightening policy, especially with the yen at very low levels.

The markets are keeping a close eye on the Jackson Hole symposium, with Fed Chair Powell and BoJ Governor Ueda both attending. Powell delivers a key speech on Friday and Ueda will participate in a panel discussion on Saturday. If either one provides insights into future rate policy, it could mean some volatility from USD/JPY on Monday.

What does the Fed have planned? That depends on which Fed member is addressing the media. Philadelphia Fed President Patrick Harker said on Thursday that he didn’t see a need to raise rates further, absent any unexpectedly poor data, but added that the Fed wouldn’t be lowering rates anytime soon. However, Boston Fed President Susan Collins said that rate increases might still be necessary. The Fed is likely to pause at the September meeting, but what happens after that is unclear..

USD/JPY Technical

- USD/JPY is facing resistance at 146.41, followed by 147.44

- There is support at 145.54 and 144.51