Sample Category Title

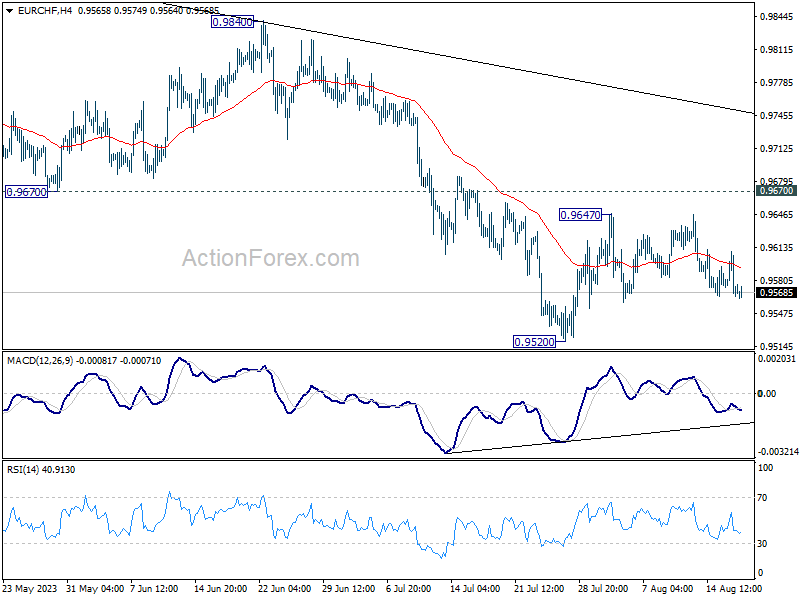

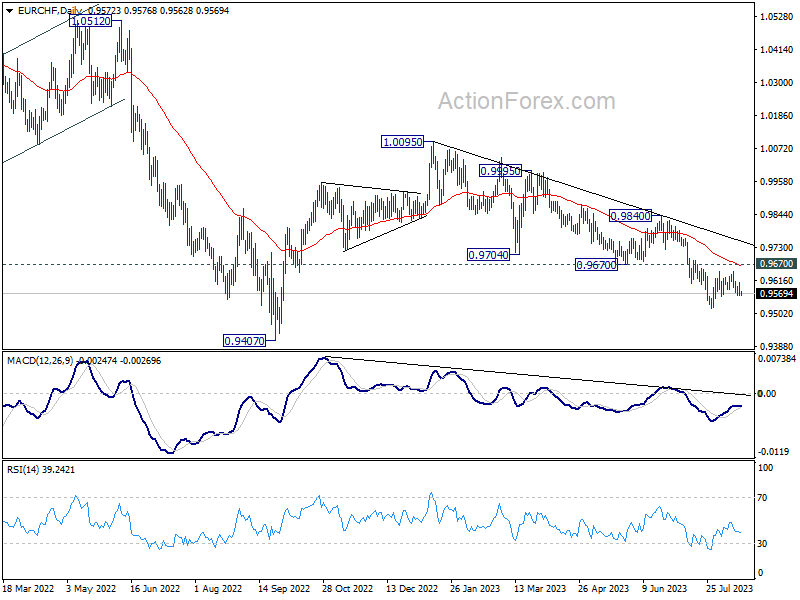

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9556; (P) 0.9584; (R1) 0.9601; More...

Intraday bias in EUR/CHF remains neutral as range trading continues. On the upside, break of 0.9647 will resume the rebound from 0.9520. Further sustained break of 0.9670 will be the first sign of bullish reversal and target 0.9840 resistance for confirmation. On the downside, break of 0.9520 will resume the whole fall from 1.0095 towards 0.9407 low.

In the bigger picture, medium term outlook is staying bearish as the pair is capped well below falling 55 W EMA (now at 0.9859). Down trend from 1.2004 (2018 high) is in favor to continue. Sustained break of 0.9407 will target 61.8% projection of 1.1149 to 0.9407 from 1.0095 at 0.9018. For now, this will remain the favored case as long as 0.9840 resistance holds, in case of strong rebound.

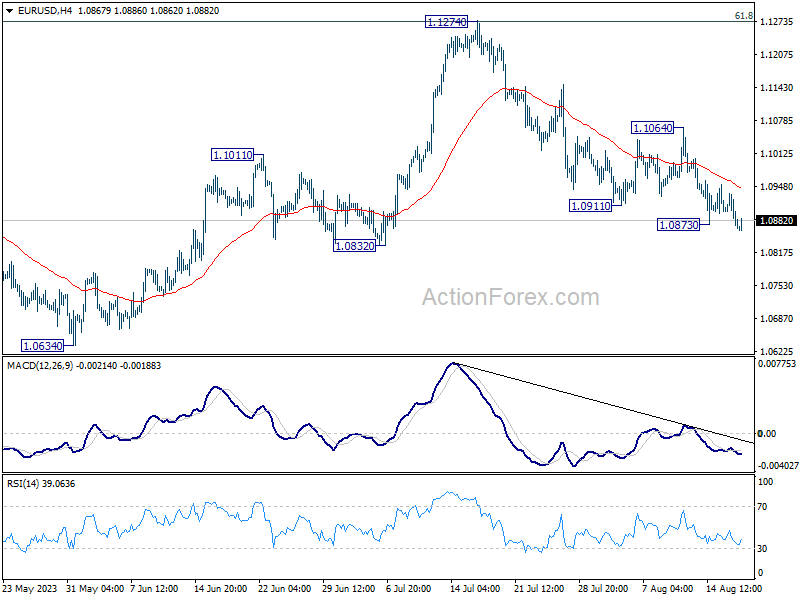

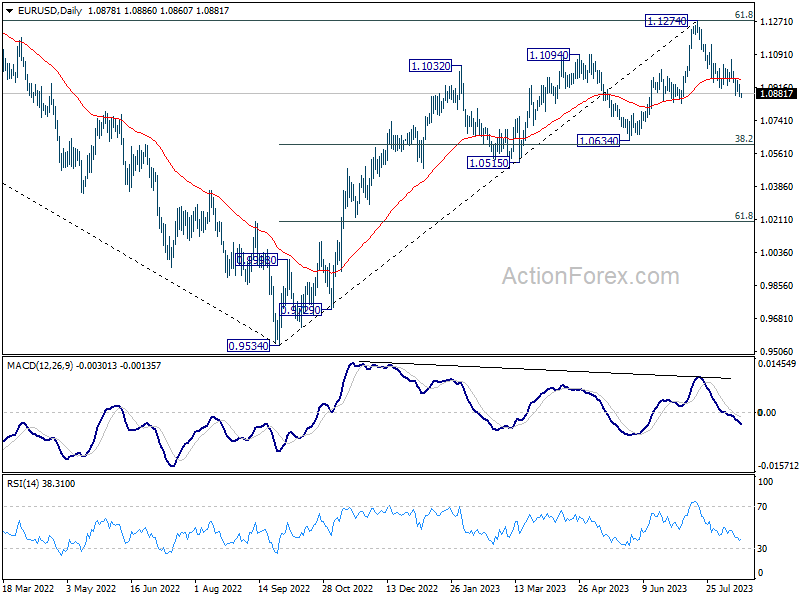

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0856; (P) 1.0895; (R1) 1.0919; More...

Intraday bias in EUR/USD is back on the downside, as fall from 1.1274 resumed by breaking 1.0873 temporary low. Deep Decisive break of 1.0832 will target 1.0609/34 cluster support. Near term outlook will stay cautiously bearish as long as 1.1064 resistance holds, in case of recovery.

In the bigger picture, a medium term top could be formed at 1.1274, after failing to break through 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 decisively, on bearish divergence condition in D MACD. Sustained trading below 55 D EMA (now at 1.0966) will bring deeper correction to 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609). Strong support could be seen there, at least on first attempt, to set the range for consolidation.

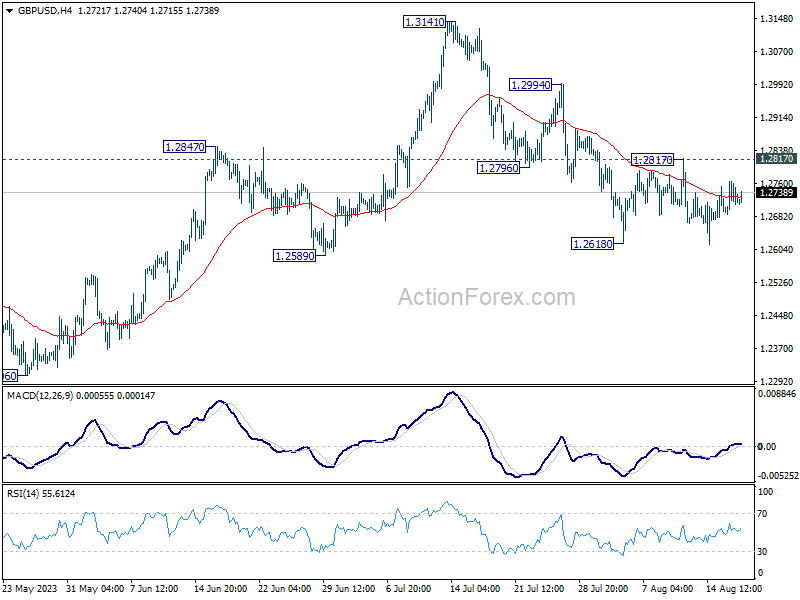

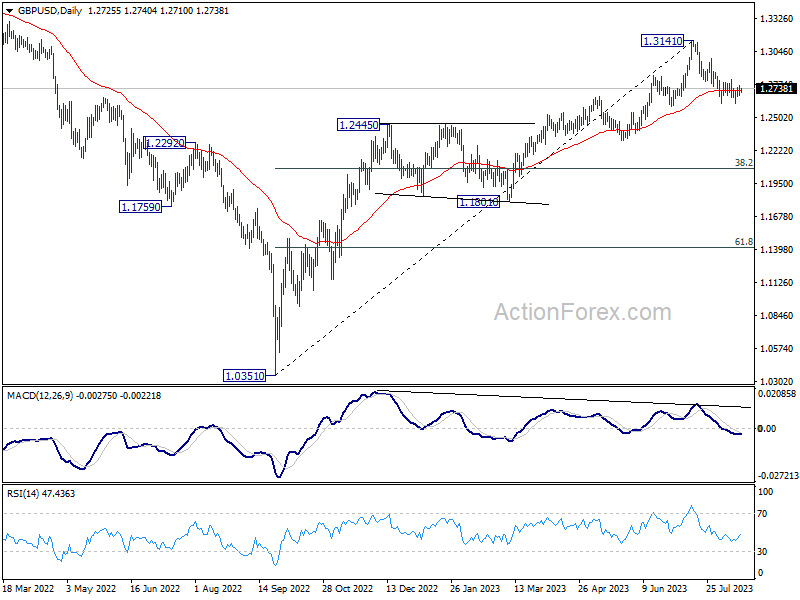

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2690; (P) 1.2729; (R1) 1.2770; More...

Intraday bias in GBP/USD remains neutral for sideway trading. On the downside, firm break of 1.2618, and sustained trading below 1.2678 resistance turned support will argue that it's already in a larger correction. Deeper decline would then be seen to 1.2306 support next. Nevertheless, break of 1.2817 minor resistance will indicate that the pull back has completed, and turn bias back to the upside for stronger rebound.

In the bigger picture, a medium term top could be in place at 1.3141 already, on bearish divergence condition in D MACD. Sustained trading below 55 D EMA (now at 1.2723) should confirm this case, and bring deeper fall to 38.2% retracement of 1.0351 to 1.3141 at 1.2075, as a correction to up trend from 1.0351 (2022 low). For now, rise will stay mildly on the downside as long as 1.3141 resistance holds, in case of strong rebound.

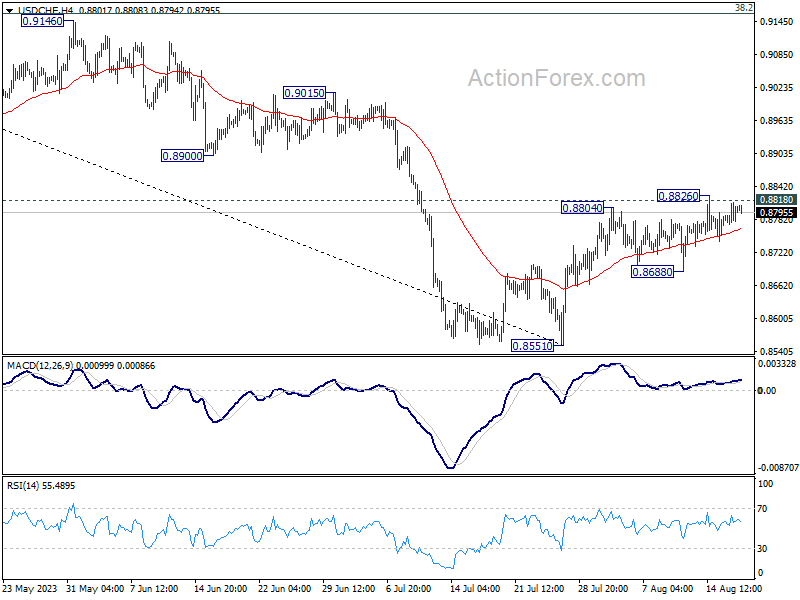

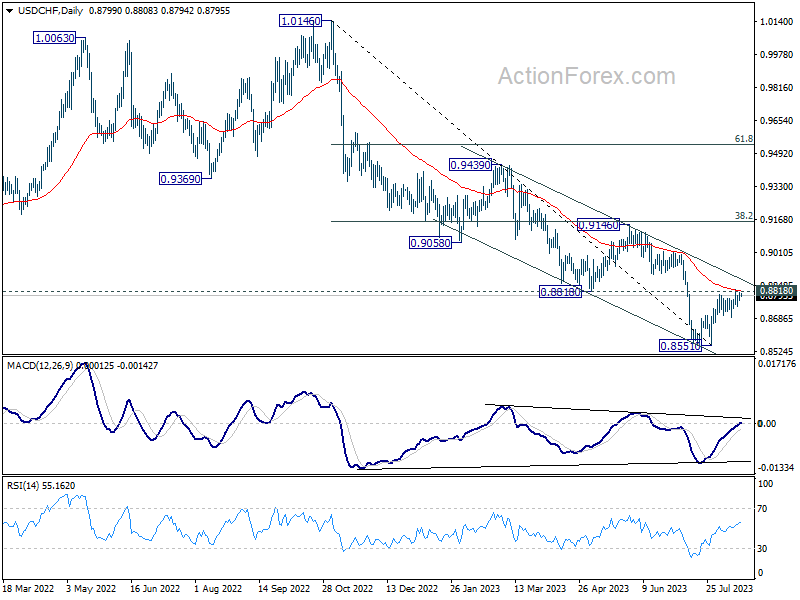

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8779; (P) 0.8796; (R1) 0.8818; More....

Intraday bias in USD/CHF stays neutral as range trading continues. On the upside, sustained trading above 0.8818 support turned resistance will carry larger bullish implication. Further rally should then be seen to 0.9146 cluster resistance next. However, break of 0.8688 support will indicate rejection by 0.8818, and turn bias back to the downside for retesting 0.8551 low.

In the bigger picture, a medium term bottom could be in place at 0.8551 already, on bullish convergence condition in D MACD. Sustained trading above 0.8818 will bring further rise to 0.9146 cluster resistance (38.2% retracement of 1.0146 to 0.8551 at 0.9160), even as a correction. Nevertheless, break of 0.8851 will resume the down trend from 1.0146 instead.

USD/JPY Daily Outlook

Daily Pivots: (S1) 145.64; (P) 146.02; (R1) 146.74; More...

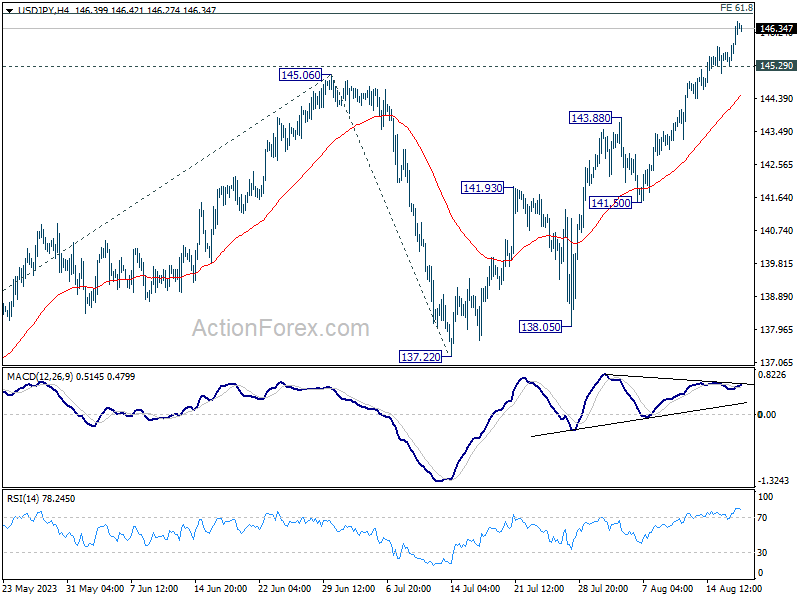

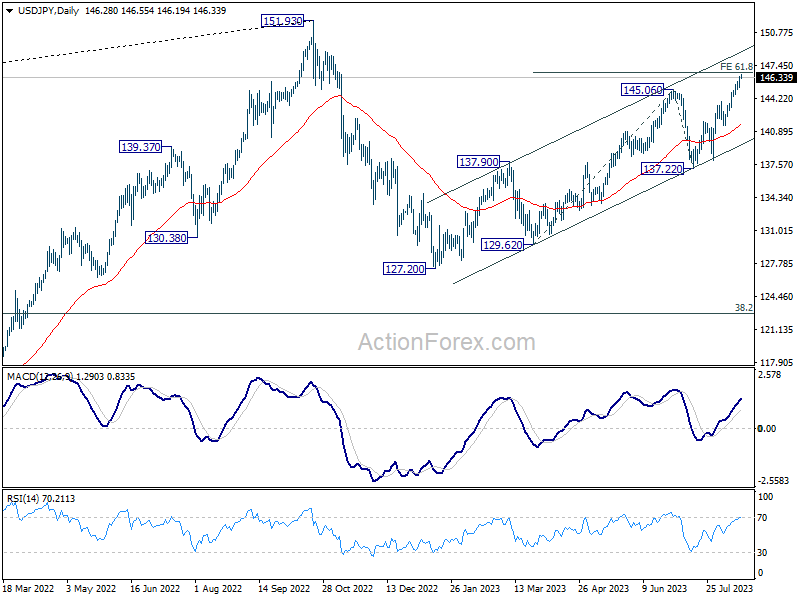

USD/JPY's rally continues today and intraday bias stays on the upside. Sustained break of 61.8% projection of 129.62 to 145.06 from 137.22 at 146.76 will pave the way to retest 151.93 high. On the downside, below 145.29 minor support will turn bias to the downside for deeper pull back.

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Rise from 127.20 is seen as the second leg of the pattern and could still be in progress. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.

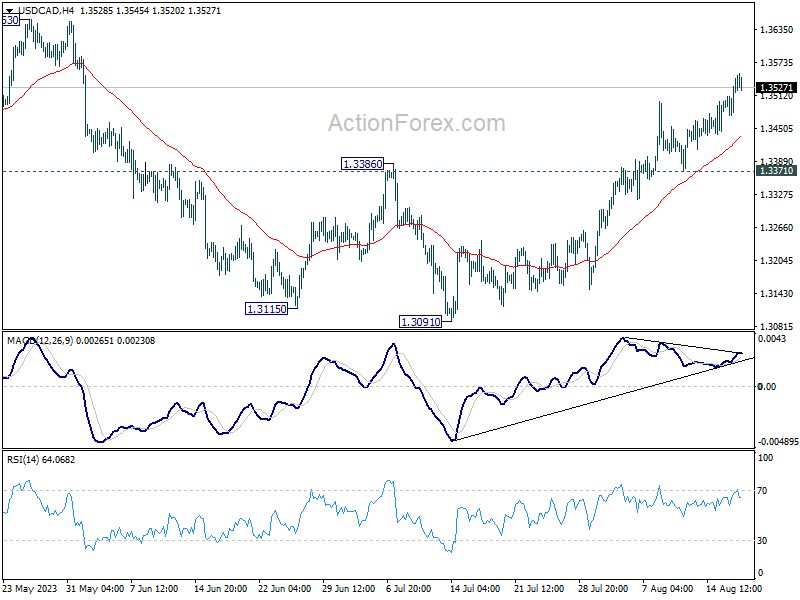

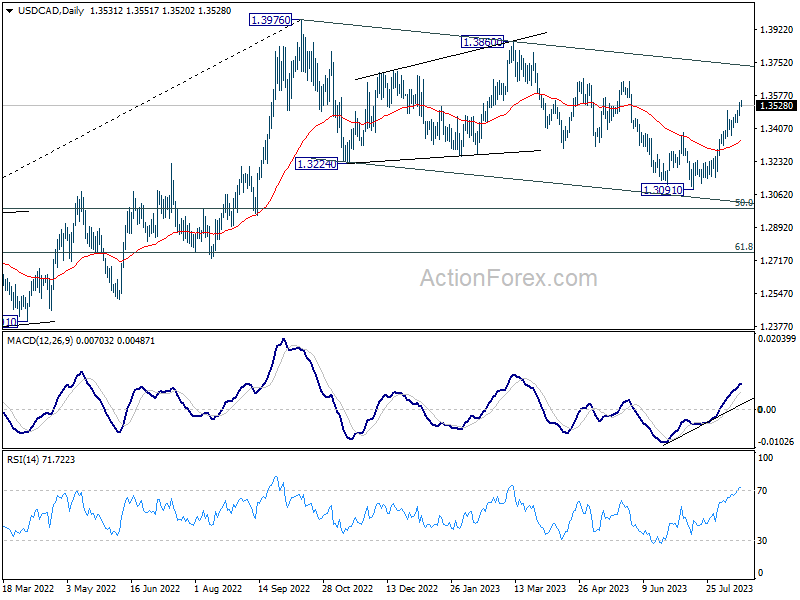

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3490; (P) 1.3518; (R1) 1.3559; More....

Intraday bias in USD/CAD stays on the upside for the moment. As noted before, corrective fall from 1.3976 should have completed with three waves down to 1.3091. Further rally would be seen to retest 1.3653 resistance next. Break there will further confirm this case and target 1.3976 high. For now, further rally is expected as long as 1.3371 support holds, in case of retreat.

In the bigger picture, price actions from 1.3976 are viewed as a corrective fall only. Upon completion, rise from 1.2005 (2021 low) would resume through 1.3976 towards 1.4667/89 long term resistance zone. In case of another fall, downside should be contained by 61.8% retracement of 1.2005 to 1.3976 at 1.2758.

USD/JPY Technical: Bullish Tone Resumes, 148.20/85 Next Resistance to Watch

- USD/JPY cleared above 145.50/146.10 resistance that confluences with BoJ’s FX intervention conducted on 22 September last year.

- Primary driver of USD/JPY rallies has been a weak Chinese yuan and rising sovereign yield premium of the 10-year US Treasury over the 10-year JGB.

- The next medium-term resistance to watch will be at 148.20/85 on the USD/JPY.

The USD/JPY has moved up relentlessly and cleared above 145.50/146.10 resistance that coincided with Bank of Japan (BoJ) FX intervention on 22 September last year to negate the JPY weakness seen in the prior major uptrend phase from the January 2021 low to Oct 2022 high, its first market intervention since 1998. It closed higher yesterday, 16 August at 146.36, near its intraday high of 146.41 printed in the US session.

So far, it has rallied by 850 pips from its 28 July 2023 low of 138.06, ex-post BoJ newly enacted flexible yield curve control programme on the 10-year Japanese Government Bond (JGB) and ignored the concerns of another round of FX intervention from BoJ.

Medium-term uptrend supported by sovereign yield premium

Fig 1: USD/JPY medium-term trend as of 17 Aug 2023 (Source: TradingView, click to enlarge chart)

The primary driver of this recent bout of USD/JPY’s sharp rallies seen in the past two weeks has been the steep sell-off inflicted on the offshore Chinese yuan (CNH) and the widening sovereign yield premium of the 10-year US Treasury note over the 10-year JGB, the yield spread has just broken above a key medium-term resistance of 3.60%.

Oscillating within a minor ascending channel since 7 August 2023 low

Fig 2: USD/JPY minor short-term trend as of 17 Aug 2023 (Source: TradingView, click to enlarge chart)

In the shorter term, watch the 145.80 key short-term pivotal support to maintain the current bullish tone to see the next resistance coming at 147.20/50 in the first step.

On the flip side, a break below 145.80 may jeopardize the bulls to expose the next supports at 144.90 and 143.70 (also close to the 20-day moving average).

Aussie Dollar Continues to Trade on Weak Side Against Strong USD

Markets

July FOMC Minutes showed that thinking within the Federal Reserve didn’t change compared to their June gathering which included updated growth/inflation forecasts and a dot plot. Two Fed officials favoured leaving rates unchanged instead of hiking by 25 bps; a preference already visible in June. “A number of participants judged that, with the stance of monetary policy in restrictive territory, risks to the achievement of the committee’s goals had become more two-sided, and it was important that the committee’s decisions balance the risk of an inadvertent overtightening of policy against the cost of an insufficient tightening”. Again, referring to June, this “number of participants” are probably the 4 governors which pencilled in a final rate hike delivered in July. “Most participants continued to see significant upside risks to inflation, which could require further tightening of monetary policy”. This is the group op 12 Fed governors which in June hinted at at least another two policy rate hikes (1 going forward). We remain flabbergasted by the fact that US money markets only attach a 1/3 probability for a final Fed rate hike by November despite this clear Fed guidance. The disinflation process runs as expected while US growth outperforms expectations, significantly reducing the 2023 recession probability. Next week’s Jackson Hole symposium offers an opportunity to dot the I’s and cross the t’s on this divergence.

US Treasuries remain in sell-off mode. Ahead of FOMC Minutes, markets digested decent eco data (housing market & industrial production). Technical elements are at play as well with the US 10-yr yield breaking the YTD high at 4.2% and pushing for a test of the 2022 high at 4.34%. Interestingly, the move is driven by higher US real yields. The US 10y real yield moved above 1.9% for the first time since 2009. We think that it’s both an indication of improved growth prospects, a return of US credit risk premia, a recognition of a higher future US neutral rate and embracing the higher for even longer scenario. Daily US yield changes yesterday varied between +1.2 bps (2-yr) and +3.9 bps (7- yr). The US 2-yr yield is pushing to move above 5% with the cycle high at 5.12% being next resistance. The US dollar holds its momentum though gains might have been bigger given the real interest rate support. EUR/USD closed at 1.0879 from an open at 1.0905. A test of the July low at 1.0834 is imminent. The Japanese yen remains on the weak side (USD/JPY > 146) following last week’s rise in core yields. Back in September, the Japanese Ministry of Finance did its first FX interventions since 1998 at the current spot rate. They later stepped it up as USD/JPY briefly passed 150 in October. We expect ruling trends – core bond weakness & dollar strength – to persist short term with today’s soft eco calendar (US weekly claims & Philly Fed index) not\interfering.Sterling yesterday outperformed the single currency on higher than expected July core CPI figures with EUR/GBP sliding to 0.8504 support.

News and views

Australian July payrolls disappointed with employment dropping by 14 600 people while consensus expected an increase by around the same amount. Details showed full time occupations falling by 24 200 with a 9 600 gain in part time employment softening the blow. The unemployment rate increased by 0.2 percentage points to 3.7% with the participation rate decreasing 0.1 ppt to 66.7%. Both indicators remain near their historically best levels, suggesting an ongoing tight labour market. The head of labour statistics at the Australian Bureau of Statistics downplayed the job losses by pointing to the average monthly employment increase of +42 000 in the first half of the year with employment also being 387 000 higher compared with last July. On top, July includes the school holidays which often shows job changes around when people take their leave and start of leave a job. Monthly hours worked increased 0.2% in July and are 5.2% higher than in July of last year suggesting that the demand for labour is partially met by people working more hours. In a separate report, the ABS said that average weekly earnings rose by 3.9% on an annual basis in May, which is the strongest annual growth since May 2013 apart from a brief spike early in the pandemic. Australian swap rates follow the global move this morning, rising by 4.1 bps (2-yr) to 8.8 bps (30- yr). The Aussie dollar continues to trade on the weak side against a strong USD with AUD/USD falling below the 0.64 big figure for the first time since November last year. The 2022 low at AUD/USD 0.6170 is key support.

Significant Upside Risks to Inflation

FOMC minutes released yesterday showed that most Federal Reserve (Fed) officials see ‘significant upside risks to inflation that may require more tightening’. Policymakers cited a range of scenarios that included the rising commodity prices that could lead to ‘more persistent elevated inflation’. Two of them favoured halting rate hikes, but the minutes showed no official dissenters. The Fed economists also expect a small rise (only) in jobless rate in the US, but they warned that commercial real estate fundamentals could worsen.

The regional banks are under a rising pressure, as a Fitch analyst warned that dozens of US bank credit ratings are at risk – just a week after the rating agency downgraded the US’ credit rating, and Moody’s downgraded 10 US small and mid-sized banks.

The US 2-year yield remained little changed at around the 5% mark, while the 10-year flirts with the 4.30% level, approaching last October’s peak, raising questions among investors on whether levels above 4% are a good entre point in the US 10-year papers, or could it go higher? Looking at the net speculative positions, the rising US treasury yields attract investors. Asset managers’ combined treasury positions hit a record in August, but that also means that these positions could be unwound and give way to a deeper selloff. The conclusion is, even though the actual levels look appetizing for US long-dated papers – especially with the Fed’s nearing the end of its tightening cycle and trouble brewing in China. risks prevail. Activity on Fed funds futures gives less than 15% chance for a September rate hike in the wake of the latest FOMC minutes. That’s slightly higher than around 10% assessed to a 25bp hike before the release of the minutes yesterday. But the pricing for a potential 25bp and even 50bp hike in November meeting are in play.

The US dollar extends gains, and the dollar index is now marching above its 200-DMA, into the overbought market territory, with little reason for investors to step back given the Fed’s decided hawkish stance on its rate policy. The S&P500 extended losses below its 50-DMA yesterday and is preparing to test the 4400 support to the downside, while Nasdaq 100 closed below the 15000 level for the first time since end of June. Tesla dropped another 3% yesterday on news that it cut its car prices in China for the second time this year, and the shares closed the session at a spitting distance from the major 38.2% Fibonacci retracement, which should distinguish between the positive trend building since the beginning of this year and a bearish reversal.

Elsewhere, Target jumped nearly 3% yesterday after beating profit expectations when it released Q2 earnings yesterday. Lower costs boosted profit margins, and gross margins jumped 27% last quarter compared to 21.5% printed a quarter earlier, net income more than quadrupled. Shiny results helped investors overcome the 11% drop in online sales – vs. 5% growth nailed by Amazon, and the slashed sales and profit outlook. Again, despite the risk that US consumers may not spend much in the next few quarters, what we see in most data is that… they continue spending – and the resilience of spending starts weighing more on Fed expectations than the risks that don’t materialize.

Slowing Europe

In Europe, the latest data released yesterday showed that growth and industrial production slowed, but slowed less than expected, while employment deteriorated less than expected – giving the European Central Bank (ECB) a good reason to continue its fight against inflation. But on a microscopic level, the Ifo said that Germany’s skilled worker pool is worsening. The Netherlands unexpectedly slipped into recession after showing two straight quarter contraction, and Eastern Europe continues feeling the pinch of Ukrainian war; the Polish economy printed a 3.7% contraction. Plus, Europe’s got a China problem. The European luxury goods have been supporting a rally in the European stocks as a result of higher Chinese purchases of the luxury products. But the souring economic conditions in China, falling home prices, rising unemployment and deteriorating sales growth weigh on valuations of companies like LVMH and Hermes. The Stoxx 600 is getting ready to test the 200-DMA, near 453, to the downside, and trend and momentum indicators hint that a deeper selloff could be on the European stocks’ menu this quarter.

On the currency front, the weak data – even though it was stronger-than-expected, combined with a broad-based surge in the US dollar, kept the EURUSD below the 100-DMA yesterday, near 1.0930. The pair fell to the lowest levels since the beginning of July and the strengthening bearish momentum calls for a deeper downside correction. The next natural target for the EURUSD bears stands at 1.0790, the 200-DMA. The ECB will likely keep its hawkish stance unchanged, but when the Fed hawks step in, the other central bank hawks just need to wait before their hawkishness is reflected in market pricing.

Norges Bank to Hike 25bp Today

Market movers today

Today's main event is the Norges Bank meeting. In June, Norges Bank signalled that the policy rate would probably be raised further at the coming week's meeting. High inflation figures for June unexpectedly opened up the possibility of the bank having to deliver another half-point hike in August, but falling core inflation in July combined with current market signals now clearly point to a quarter-point hike.

The 60 second overview

FOMC minutes: The minutes from the July FOMC meeting revealed very few new policy signals. Most Fed officials saw "significant" upside risks to inflation and believe that more tightening might be required, although with a more balanced risk outlook, which was emphasised several times. Two members backed a hold at the meeting. The FOMC minutes are obviously backward looking compared to the recent slew of data, but inflation concerns are still lingering despite the two latest benign US CPI prints. The Fed also scraps its recession call, which points to the US growth resilience as well in the face of extraordinary tightening. Market reaction was generally muted on the back of the minutes. Today is a quiet day with focus on jobless claims and Philadelphia Fed Manufacturing index.

US GDP: Atlanta Fed's GDPnow forecast for Q3 was lifted to 5.8%, up from 5.0% earlier this week.

Euro area: The strong euro area labour market was confirmed to continue in Q2 as well. While the employment growth lost some pace, it still grew by 0.2% qoq in the euro area, which is essentially the lowest since the pandemic. Indeed's hiring lab database suggested that wage growth declined further in July, albeit stayed printed at an elevated 4.2% yoy.

Equities: European and Nordic equities recovered into the session, while US closed another -1% lower and ended near session lows. It was not a risk-off session at home turf, with consumer discretionary banks and industrials all performing well. However, US saw more of a defensive and value preference. Big tech and yield sensitive sectors such as real estate sold off, as yields rose after the Fed minutes. VIX ticked another point higher to 17. Risk sentiment seems to improve this morning with Asian markets mixed and US futures a notch higher.

FI: Global bond yields moved generally sideways yesterday will no significant news to alter the pricing. The FOMC minutes released last night did not lead to a market reaction. That means that 2y UST yields are still trading just below the 5% level. Inflation swaps declined marginally yesterday coming off the recent highs of 2.65% in 5y5y inflation swap. At the same time, markets added to its rate cut expectations from the ECB yesterday to now around -65bp priced through 2024.

FX: Scandies were once again under pressure yesterday from negative risk sentiment. Both EUR/NOK and EUR/SEK rose to the highest level since early June. GBP and USD were top performers as EUR/GBP slipped to the lowest in over a month and EUR/USD hovered around the 1.09 level.

Credit: The negative tone in the credit market continued yesterday, which we largely attribute to the ongoing barrage of negative stories out of China and their potential to spill over to the rest of the global economy. This drove iTraxx Main out by 1.1bp to 74bp while Xover widened 4.4bp to 415.4bp. We note though, that the moves in cash space are less pronounced indicating that liquidity remains weak in the secondary market.

Nordic macro

Norway: Norges Bank signalled in June that the policy rate would probably be raised further in August. High inflation figures for June unexpectedly opened up the possibility of the central bank having to deliver another half-point hike in August, but core inflation fell again in July from 7.0% to 6.4%, which is only marginally above the 6.3% assumed in the June monetary policy report. Together with a slightly stronger NOK, higher FRA-OIS spreads and somewhat lower rate expectations abroad, this clearly points to a quarter-point hike as signalled at the June meeting. We expect Norges Bank to keep the tightening bias, stating that 'rates most likely will be raised again in September'. However, they will stress that this will be data dependent.

Sweden: Anna Breman will be the first Riksbank board member to comment on the economy and monetary policy after the summer break when she speaks at 14:00 today. She will get the chance to reflect on, hitherto, higher inflation than anticipated and a much weaker than expected preliminary GDP print for the second quarter. In June she expressed a lot of concern that service inflation gets stuck up here. Regarding monetary policy she stressed that if, which is in fact the case, the market prices in 'premature' rate cuts, the Riksbank may have to respond by keeping rates higher for longer. Arguably, the rationale for that would be to mitigate unwarranted easing of financial conditions. Breman is currently a hawk.