Sample Category Title

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0856; (P) 1.0895; (R1) 1.0919; More...

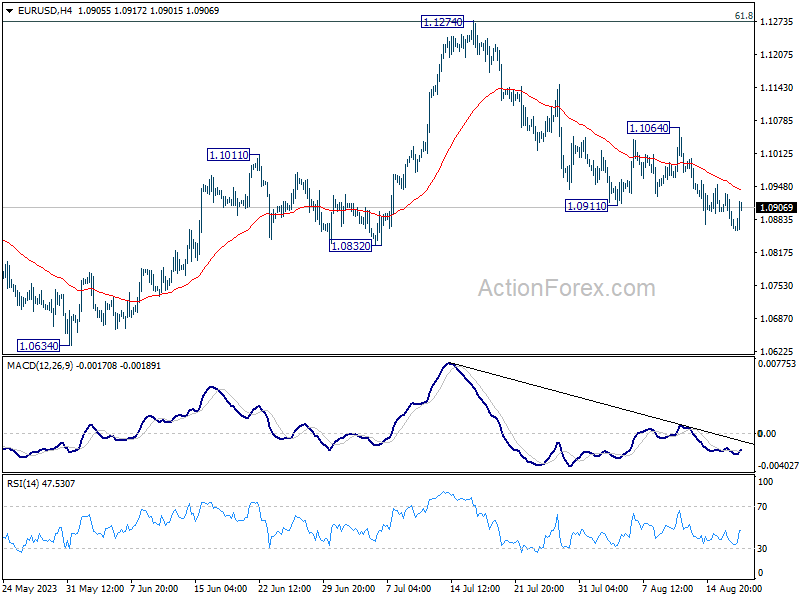

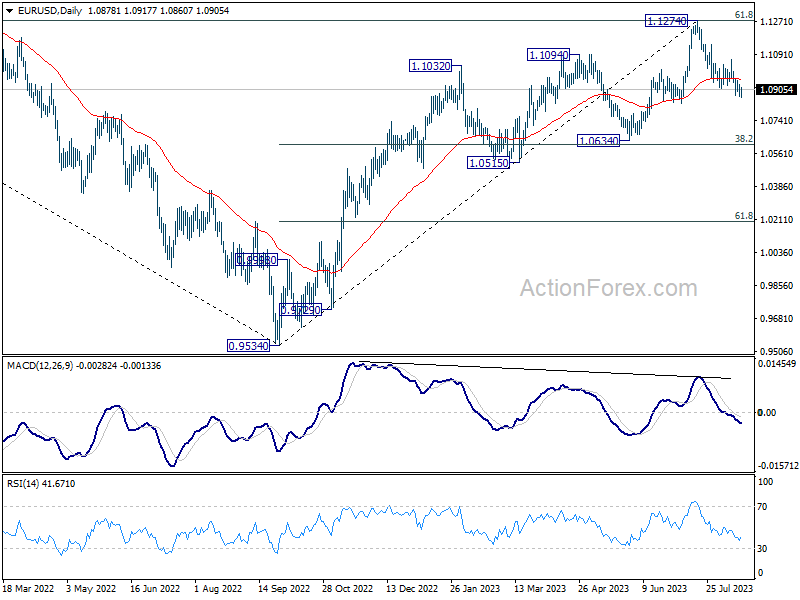

While EUR/USD continues today lose downside momentum, further decline is still expected as long as 1.1064 resistance holds. Break of 1.0832 will extend the fall from 1.1274 to 1.0609/34 cluster support. However, break of 1.1064 will argue that the fall has completed and turn bias back to the upside for stronger rebound.

In the bigger picture, a medium term top could be formed at 1.1274, after failing to break through 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 decisively, on bearish divergence condition in D MACD. Sustained trading below 55 D EMA (now at 1.0966) will bring deeper correction to 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609). Strong support could be seen there, at least on first attempt, to set the range for consolidation.

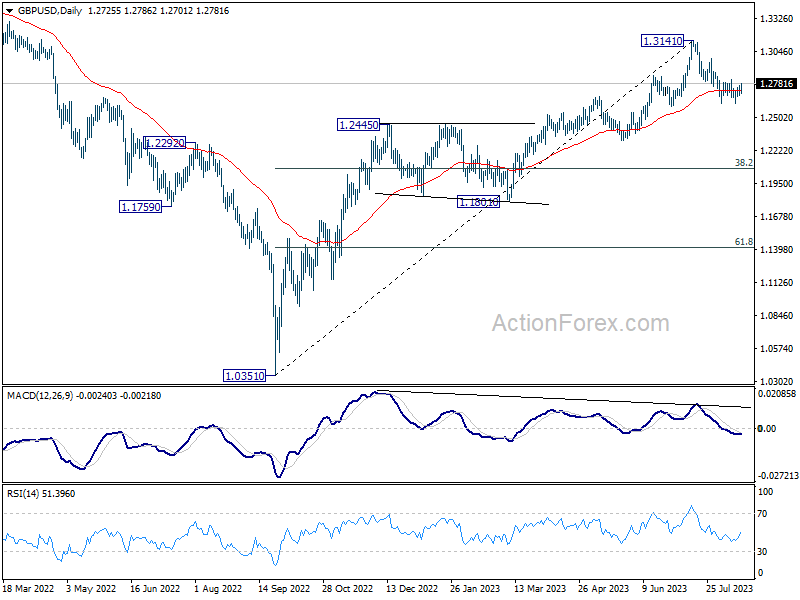

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2690; (P) 1.2729; (R1) 1.2770; More...

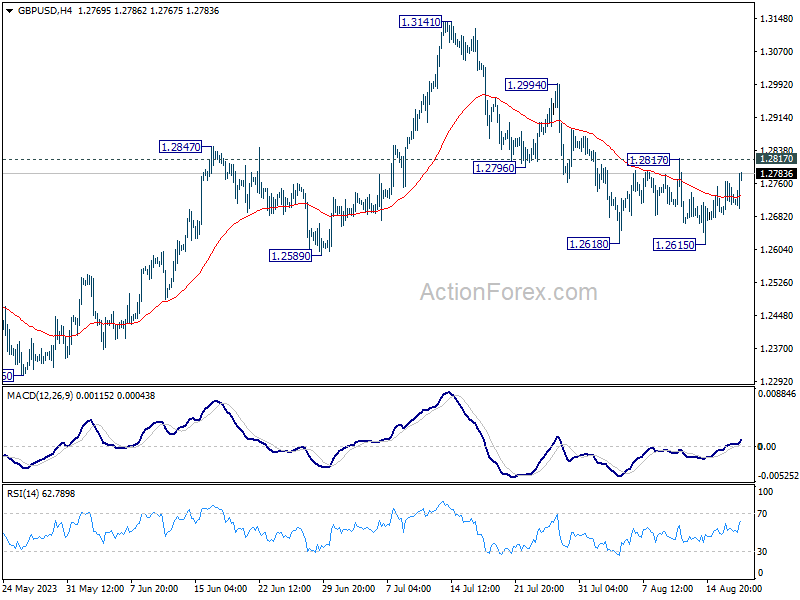

GBP/USD's recovery from 1.2615 extends higher today but stays below 1.2817 resistance. Intraday bias remains neutral for the moment. On the downside, firm break of 1.2615, and sustained trading below 1.2678 resistance turned support will argue that it's already in a larger correction. Deeper decline would then be seen to 1.2306 support next. Nevertheless, break of 1.2817 minor resistance will indicate that the pull back from 1.3141 has completed, and turn bias back to the upside for stronger rebound.

In the bigger picture, a medium term top could be in place at 1.3141 already, on bearish divergence condition in D MACD. Sustained trading below 55 D EMA (now at 1.2723) should confirm this case, and bring deeper fall to 38.2% retracement of 1.0351 to 1.3141 at 1.2075, as a correction to up trend from 1.0351 (2022 low). For now, rise will stay mildly on the downside as long as 1.3141 resistance holds, in case of strong rebound.

Dollar Retreats, Sterling Continues Dominance, Bitcoin Down

Dollar relinquished its early gains, entering US session as the day's softest currency. Even as US benchmark 10-year yields skyrocketed to touch 4.3% mark, they found themselves lagging behind their German and UK counterparts. On the flip side, Australian Dollar is mustering a recovery, buoyed in part by China's proactive measures to stabilize Yuan's exchange rate.

However, despite these fluctuations, the greenback has managed to secure its position as the second strongest currency for the week for now. Investors remain on the lookout, with possibility of a return of Dollar buyers should risk sentiments sway once more.

Sterling, marching to its own beat, continues its reign as this week's top performer, and its momentum against Euro is gaining steam. Meanwhile, Swiss Franc clinches third place. At the opposite end of the spectrum, Aussie struggles to shake off its tag as the week's laggard, trailed by Yen and Kiwi.

Technically, Bitcoin breaks through 28555 support today to resume the decline from 31815. It's uncertain whether this move is a correction to the larger up trend, or a reversal. But in either case, firm break of 61.8% projection of 31815 to 28555 from 30219 at 28204 could prompt downside acceleration to 100% projection at 26959. If materializes, this could be in tandem with deeper selloff in risk markets, in particular NASDAQ.

In Europe, at the time of writing, FTSE is down -0.32%. DAX is down -0.26%. CAC is down -0.32%. Germany 10-year yield is up 0.0396 at 2.691. Earlier in Asia, Nikkei dropped -0.44%. Hong Kong HSI dropped -0.01%. China Shanghai SSE rose 0.43%. Singapore Strait Times dropped -0.52%. Japan 10-year JGB yield is up 0.0226 at 0.655.

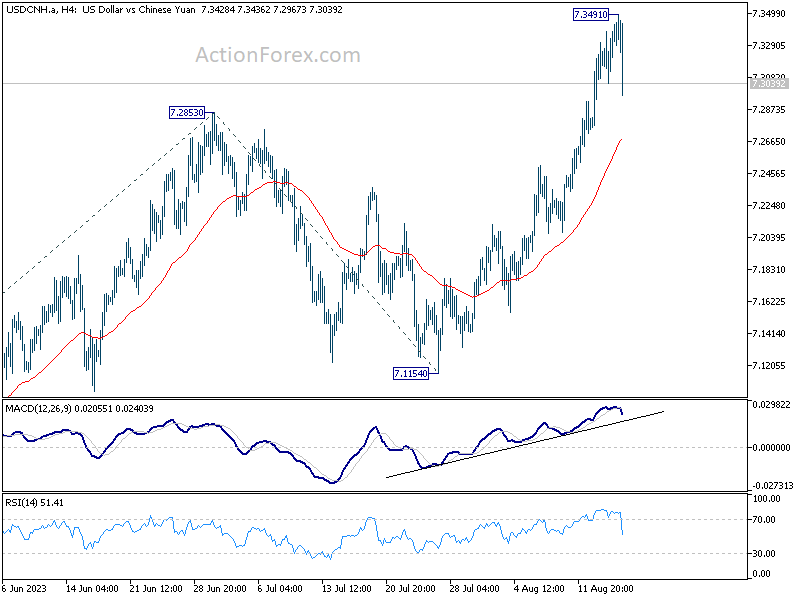

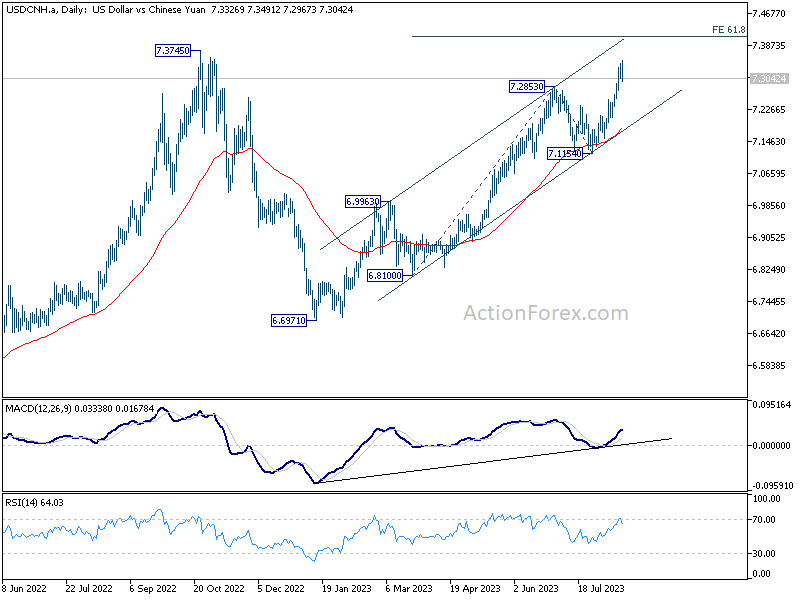

Chinese Yuan recovers as PBoC pledges to prevent over-adjustment

Chinese Yuan made a notable recovery today after PBoC made its intentions clear, vowing to staunchly prevent an "over-adjustment" in the Yuan's exchange rate and avert systemic financial pitfalls. Amplifying this verbal intervention, several of China's major state-owned banks have been observed actively selling US Dollars in favor of Yuan in both onshore and offshore markets this week.

This proactive stance by PBoC and state-owned banks arises at a time when Yuan has been on a downward trajectory, dangerously inching closer to its lowest levels since 2007.

Market observers are now grappling with a pivotal question: Is China's move aimed at establishing a firm bottom for Yuan or merely an effort to slow down its rapid decline?

Technically, a temporary top should be formed at 7.3491 in USD/CNH and some consolidation is now expected. As long as 55 4H EMA holds (now at 7.2685), further rally is still in favor. Break of 7.3491 will resume the rally from 6.6971 towards 7.3745 high, or possibly further to 61.8% projection of 6.8100 to 7.2853 from 7.1154 at 7.4889.

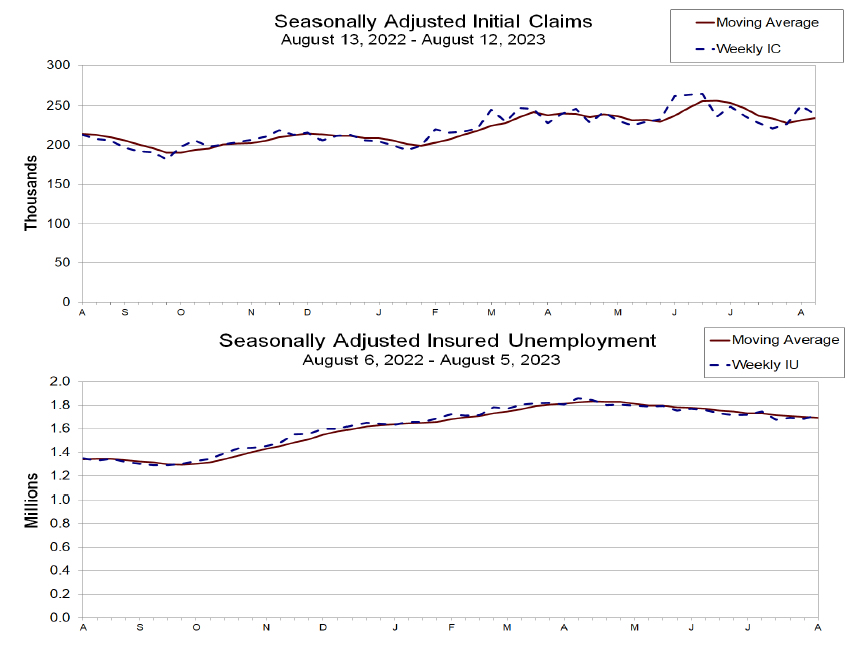

US initial claims dropped to 239k, slightly above expectation

US initial jobless claims dropped -11k to 239k in the week ending August 12, slightly below expectation of 240k. Four-week moving average of initial claims rose 3k to 234k.

Continuing claims rose 32k to 1716k in the week ending August 5. Four-week moving average of continuing claims dropped -8k to 1692k.

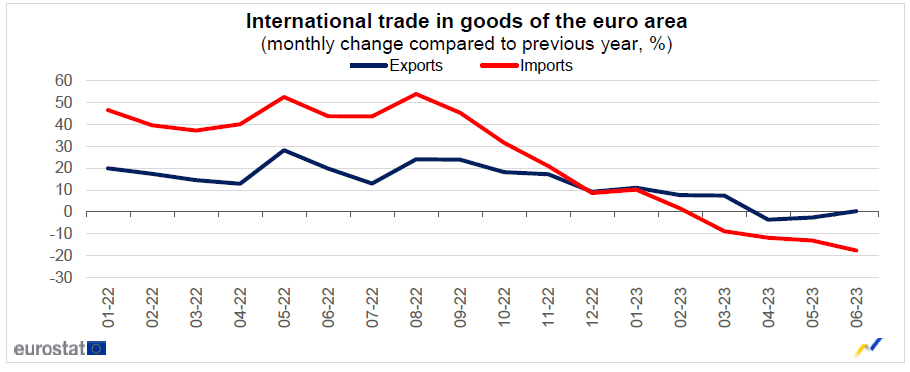

Eurozone exports rose 0.3% yoy in Jun, imports down -17.7% yoy

Eurozone exports of goods rose 0.3% yoy to EUR 252.3B in June. Imports fell -17.7% yoy to EUR 229.3B. Trade balanced recorded a EUR 23B surplus. Intra-Eurozone trade fell -4.1% yoy to EUR 231.6B.

In seasonally adjusted term, exports dropped -0.5% mom to EUR 237.2B. Imports dropped -5.6% mom to EUR 224.6B. Trade surplus widened to EUR 12.5B, larger than expectation of EUR 2.3B. Intra-Eurozone trade fell from EUR 220.8B to 217.6B during the month.

Australian employment down -14.6k, but hours worked continue to rise

Australia witnessed a contraction in employment by -14.6k in July, starkly missing expectations of a 15.2k growth. This decline was majorly attributed to a drop in full-time jobs by -24.2k, even as part-time employment saw an increase of 9.6k.

Unemployment rate rose from 3.5% to 3.7%, surpassing market anticipations which had pinned it at 3.6%. The participation rate also registered a dip, moving from 66.8% to 66.7%.

However, it wasn't all bleak. Monthly hours worked showed a marginal increase of 0.2% mom. Commenting on this aspect, Bjorn Jarvis, ABS head of labour statistics, observed, "The strength in hours worked shows that it continues to be a tight labour market."

Jarvis pointed out that hours worked have risen by an impressive 5.2% compared to July 2022, a significant outperformance relative to the 2.8% annual increase in employment.

He further noted, "The strength in hours worked over the past year, relative to employment growth, shows the demand for labour is continuing to be met, to some extent, by people working more hours."

RBNZ Orr: We don't feel a rush to be changing rates anytime soon

In a Bloomberg TV interview, RBNZ Governor Adrian Orr indicated that a forthcoming mild recession is the "bare minium" for New Zealand, as "demand has been well outstripping the pace of the supply capacity."

"We need to see subdued consumer spending, business investment and government constraints on spending, these are a critical part of the inflation process," he added.

Orr also reiterated that interest rate will need to stay high for a period of time, as "we don't feel a rush to be changing rates anytime soon."

"We believe if we stay where we are for long enough, inflation will be back inside the target band mid-next year and, and stay there," he added.

RBNZ projects OCR to peak at 5.59% in mid-2024, then retract slightly to 5.36% by early 2025. This suggests rate cuts might be off the table for about 18 months. Orr clarified that these figures are projections and "signal or constraint."

Japans' export contracts in Jul, shipments to China fell for 8th month

Japan Witnesses First Export Contraction in Over Two Years Amidst Declining Trade with China

Japan's exports experienced a dip of -0.3% yoy to JPY 8725B in July. This contraction is noteworthy as it breaks a growth streak that has lasted for over two years since February 2021.

Diving deeper into the data, while shipments to US and Europe saw a positive trajectory with respective rises of 13.5% yoy and 12.4% yoy, the trade dynamics with China narrated a different story.

Exports to China, Japan's primary trading ally, plummeted by -13.4%, marking the steepest decline since January. Notably, this reflects an ongoing trend with shipments to China diminishing for the eighth consecutive month, subsequent to a -10.9% yoy drop in June.

On the import front, Japan registered a decline of -13.5% yoy to JPY 8804B. This marks the fourth consecutive month of declining imports and is the most significant dip since September 2020. The downturn can be partly attributed to the decreasing commodities prices.

With imports exceeding exports, trade balance for the month ended in a deficit of JPY -78.7B.

When observing the figures in seasonally adjusted terms, both exports and imports displayed a 2.0% mom rise, amounting to JPY 8460B and JPY 9018B respectively. Consequently, trade deficit widened slightly, reaching JPY -557B.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2690; (P) 1.2729; (R1) 1.2770; More...

GBP/USD's recovery from 1.2615 extends higher today but stays below 1.2817 resistance. Intraday bias remains neutral for the moment. On the downside, firm break of 1.2615, and sustained trading below 1.2678 resistance turned support will argue that it's already in a larger correction. Deeper decline would then be seen to 1.2306 support next. Nevertheless, break of 1.2817 minor resistance will indicate that the pull back from 1.3141 has completed, and turn bias back to the upside for stronger rebound.

In the bigger picture, a medium term top could be in place at 1.3141 already, on bearish divergence condition in D MACD. Sustained trading below 55 D EMA (now at 1.2723) should confirm this case, and bring deeper fall to 38.2% retracement of 1.0351 to 1.3141 at 1.2075, as a correction to up trend from 1.0351 (2022 low). For now, rise will stay mildly on the downside as long as 1.3141 resistance holds, in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | PPI Input Q/Q Q2 | -0.20% | 0.40% | 0.20% | 0.00% |

| 22:45 | NZD | PPI Output Q/Q Q2 | 0.20% | 0.80% | 0.30% | 0.20% |

| 23:50 | JPY | Trade Balance (JPY) Jul | -0.56T | -0.44T | -0.55T | -0.54T |

| 23:50 | JPY | Machinery Orders M/M Jun | 2.70% | 3.60% | -7.60% | |

| 01:30 | AUD | Employment Change Jul | -14.6K | 15.2K | 32.6K | 31.6K |

| 01:30 | AUD | Unemployment Rate Jul | 3.70% | 3.60% | 3.50% | |

| 04:30 | JPY | Tertiary Industry Index M/M Jun | -0.40% | -0.10% | 1.20% | 1.00% |

| 09:00 | EUR | Eurozone Trade Balance (EUR) Jun | 12.5B | 2.3B | -0.9B | |

| 12:30 | USD | Initial Jobless Claims (Aug 11) | 239K | 240K | 248K | 250K |

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Aug | 12 | -9.5 | -13.5 | |

| 14:30 | USD | Natural Gas Storage | 35B | 29B |

US initial claims dropped to 239k, slightly above expectation

US initial jobless claims dropped -11k to 239k in the week ending August 12, slightly below expectation of 240k. Four-week moving average of initial claims rose 3k to 234k.

Continuing claims rose 32k to 1716k in the week ending August 5. Four-week moving average of continuing claims dropped -8k to 1692k.

Stocks Try to Rebound as Global Bond Yields Hit 15-year High

Now that we heard from Walmart, it is clear that the US consumer is still willing to spend. Expectations for robust consumer spending in Q3 have been confirmed and that should keep growth estimates trending higher. With COVID savings still expected to be used over the next couple of months and a lag with how student debt repayments go, confidence in continued business momentum should remain. The Atlanta Fed’s estimate of 5.8% looks like it might actually happen, which should keep the Fed standing by its hawkish stance that they might need to do more tightening to combat inflation.

US stocks are trying to hold onto gains as investors watch a bond market selloff that is taking global bond yields to a 15-year high. China remains in focus and the decision from authorities to tell state-owned banks to step up intervention efforts is providing some support to markets. It is clear that China is working on their response here and that more support is on its way.

Walmart

Walmart’s top and bottom earnings beats were accompanied with raised guidance, which made them have one of the top results from the retailers. It seems that Walmart is taking away business from Target too, with grocery and ecommerce sales leading the way. When the economy starts to cool in Q4, Walmart looks well positioned to be one of the top retailers.

FX snapshot

The Australian dollar declined after the unemployment rate rose more than expected. Labor market weakness should make the next RBA meeting easy as the economy is feeling the impacts of the RBA rate hiking cycle. The RBA will hold rates steady for a third straight time at the September policy meeting.

The Chinese yuan rallied against the dollar after the PBOC asked state banks to intervene. The yuan was depreciating too quickly and authorities needed to boost sentiment.

Some traders are not expecting BOJ intervention until we see excessive weakness that takes dollar-yen possibly beyond the 150 level. We also need to hear Japan officials state they are watching exchange rates with great interest. Japan will likely need to step into markets, but until we see further yen downside, traders might eye further dollar short-term strength.

Oil

After falling nearly six dollars, it was only a matter of time before crude prices found support. WTI crude is rebounding on expectations that Chinese officials will deliver meaningful stimulus and that the oil market will remain tight. Earnings are also providing optimism that the US consumer is still strong and willing to spend and travel at the end of the year.

The dollar rally has stalled but if the bond market selloff falls to a new level, that could prevent commodities from rebounding further. Oil looks like it will find a home around the $80 level as too many risks to the outlook still remain on the table; fears that the Fed will overtighten are back and uncertainty persists on how will the US consumer behave once all their COVID savings disappear and as student loan debt bills come due.

Gold

Gold prices are trying to recover after some hawkish Fed Minutes kickstarted a global bond market selloff. Bond yields are too high as more people become convinced inflation is not going away anytime soon. After making a 5-month low, spot gold has fallen below the $1900 level. For the spot market the $1870 level remains major support, as the $1900 level with the gold’s future contract appears to have solid support.

Bitcoin

It looks like some leveraged funds are ramping up bearish bets that Bitcoin will drift lower. The US Commodity and Futures Trading Commission's (CFTC) report on commitment of traders (COT) showed that as of August 8th, two-thirds are bearish, most likely a result of disappointment with the delays in seeing a Bitcoin US ETF approved. When you throw in what is happening in the bond market, it becomes easy for Bitcoin prices to soften. If risk aversion becomes the dominant theme on Wall Street, Bitcoin’s bearish momentum could target the $27,200 level.

Chinese Yuan recovers as PBoC pledges to prevent over-adjustment

Chinese Yuan made a notable recovery today after PBoC made its intentions clear, vowing to staunchly prevent an "over-adjustment" in the Yuan's exchange rate and avert systemic financial pitfalls. Amplifying this verbal intervention, several of China's major state-owned banks have been observed actively selling US Dollars in favor of Yuan in both onshore and offshore markets this week.

This proactive stance by PBoC and state-owned banks arises at a time when Yuan has been on a downward trajectory, dangerously inching closer to its lowest levels since 2007.

Market observers are now grappling with a pivotal question: Is China's move aimed at establishing a firm bottom for Yuan or merely an effort to slow down its rapid decline?

Technically, a temporary top should be formed at 7.3491 in USD/CNH and some consolidation is now expected. As long as 55 4H EMA holds (now at 7.2685), further rally is still in favor. Break of 7.3491 will resume the rally from 6.6971 towards 7.3745 high, or possibly further to 61.8% projection of 6.8100 to 7.2853 from 7.1154 at 7.4889.

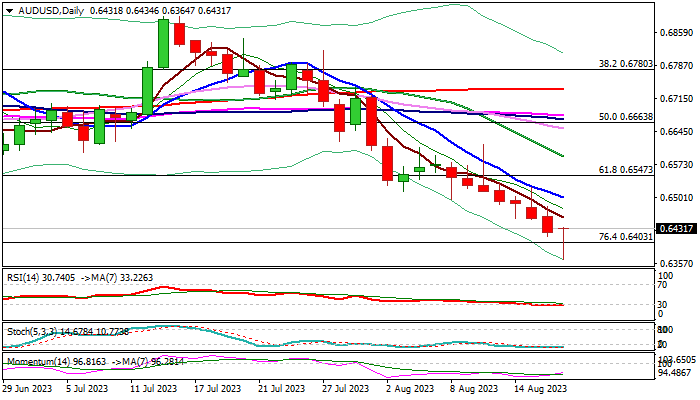

AUD/USD: Aussie Dollar Hit New Multi-Month Low, But Bears Faced Strong Headwinds

Australian dollar spiked to the lowest since early November on Wednesday, hit by downbeat Australia’s labor data (employment fell by 14.6K in July after 31.6K increase in June and well below forecast for 15K increase, while unemployment rose to 3.7% from 3.5% previous months and overshot consensus at 3.6%) adding to already weakened risk sentiment on concerns about China’s economic recovery.

Fresh bears broke through Fibo support at 0.6403 (76.4% of 0.6170/0.7157) and hit new multi-month low at 0.6364, but dip was short-lived as price quickly bounced to the session high, as daily studies are stretched.

Price adjustment is likely to precede fresh push lower and offer better selling opportunities while the price stays below falling 10DMA (0.6501).

Firm break of cracked Fibo support at 0.6403 would signal continuation of larger downtrend and risk test of 2022 low at 0.6170.

On the other hand, bears may lose traction on lift and close above 10DMA (0.6501), which would also generate initial signal of bear-trap and allow for stronger recovery.

Res: 0.6458; 0.6501; 0.6521; 0.6547.

Sup: 0.6403; 0.6364; 0.6272; 0.6170.

Dollar Can Complete a Five Wave Rise, Be Aware of a Retracement

The USD edged slightly higher, and stocks hit new lows for the week yesterday after the release of FOMC minutes. These minutes revealed that officials expressed concerns about the pace of inflation and noted the possibility of additional rate hikes unless future data suggests otherwise. So USD index retested the highs, but notice that market can be coming into the end of a fifth wave with potential wedge formation, which normally suggests that a bearish reversal is about to happen. As such, dont be surprised if the market slows down here, which on the other side can also cause some relieve rally for stocks.

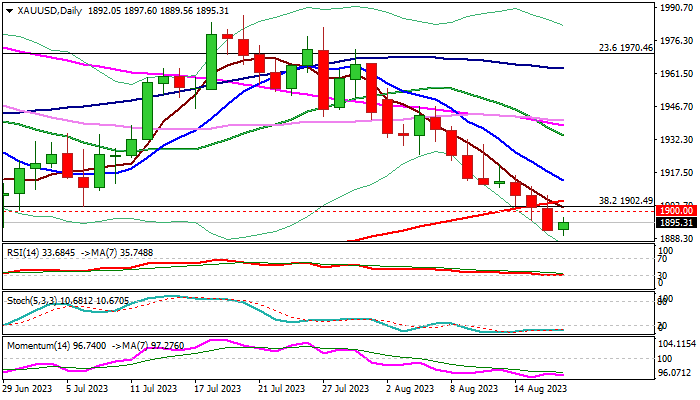

XAU/USD: Deeper Drop to be Expected on Firm Break of Key $1900 Support Zone

Gold price edged higher in European trading on Thursday, after hitting five-month low ($1889) in Asia.

Wednesday’s close below key supports at $1900 zone (200DMA - $1905; Fibo 38.2% of $1614/$2080 - 1902; psychological - $1900 and former low of June 29 - $1892) generated strong bearish signal.

Signal needs to be verified by sustained break below these supports, which will also complete a failure swing pattern on daily chart and add to bearish outlook.

Stronger dollar on overall hawkish Fed, as well as growing concerns about China’s economic growth, particularly on developing crisis in property sector, prompt traders into dollar and continue to pressure the yellow metal.

Meanwhile, bears may take a breather and consolidate, as daily studies are oversold, with the action expected to stay capped under 200DMA to keep bears intact for extension towards targets at $1858/$1847 (Mar 6 high / 50% retracement of $1614/$2080).

Caution on bounce above 200DMA which would generate initial signal of a false break lower, with acceleration above falling 10DMA ($1914) to weaken bearish structure and risk stronger rebound.

Res: 1900; 1905; 1914; 1926.

Sup: 1889; 1858; 1847; 1804.

Eurozone exports rose 0.3% yoy in Jun, imports down -17.7% yoy

Eurozone exports of goods rose 0.3% yoy to EUR 252.3B in June. Imports fell -17.7% yoy to EUR 229.3B. Trade balanced recorded a EUR 23B surplus. Intra-Eurozone trade fell -4.1% yoy to EUR 231.6B.

In seasonally adjusted term, exports dropped -0.5% mom to EUR 237.2B. Imports dropped -5.6% mom to EUR 224.6B. Trade surplus widened to EUR 12.5B, larger than expectation of EUR 2.3B. Intra-Eurozone trade fell from EUR 220.8B to 217.6B during the month.