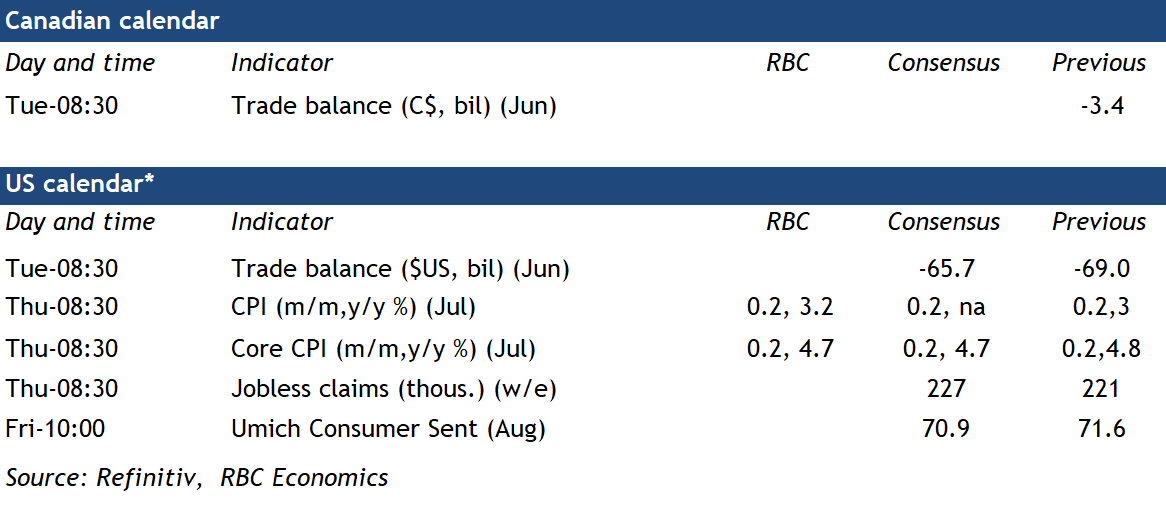

Sample Category Title

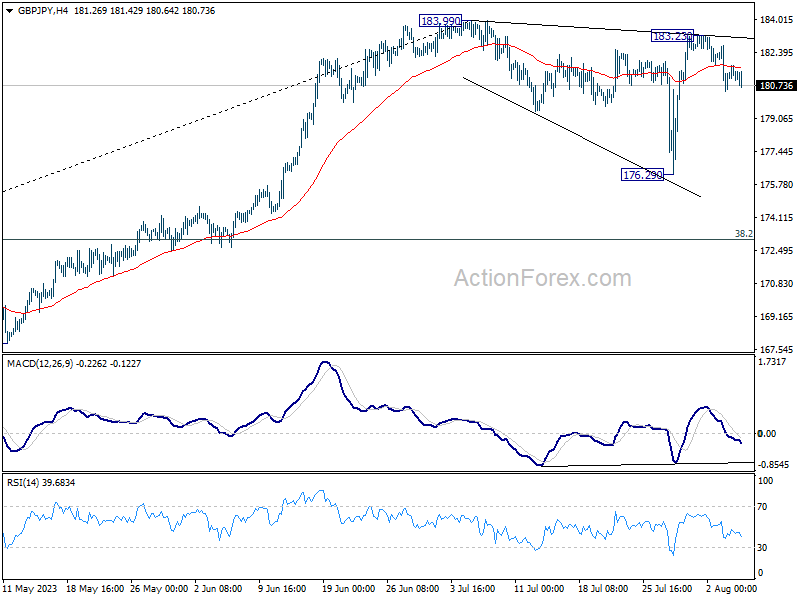

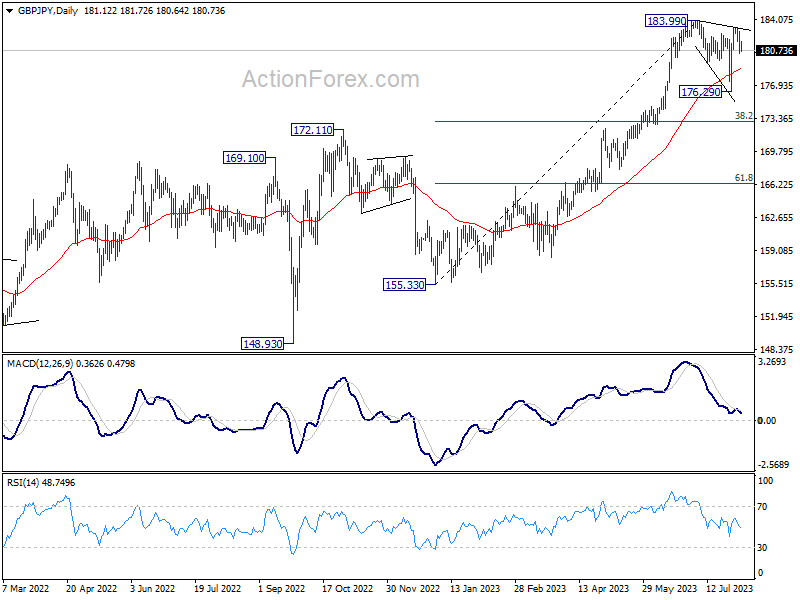

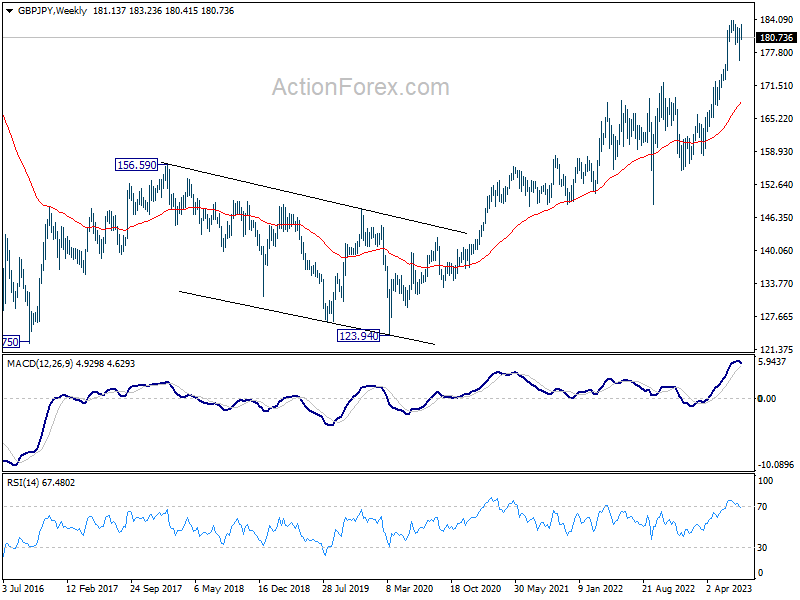

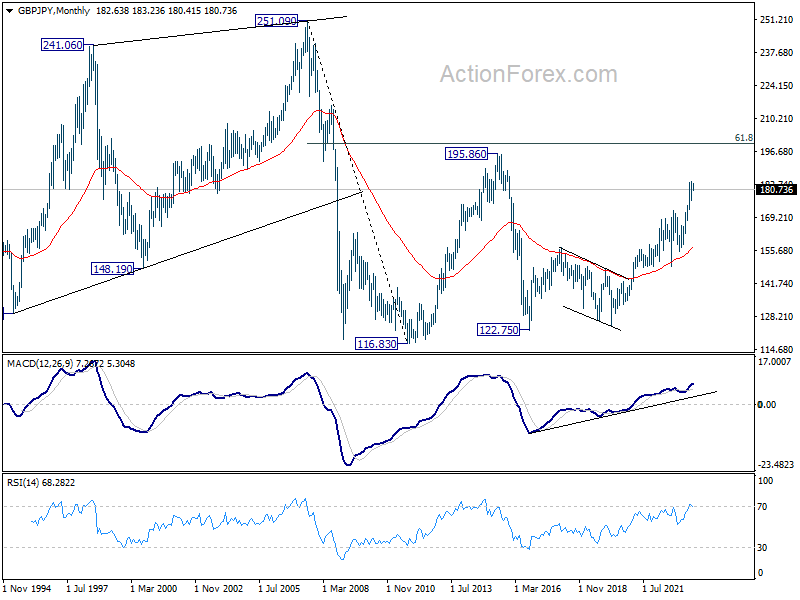

GBP/JPY Weekly Outlook

GBP/JPY failed to break through 183.99 resistance last week and reversed after hitting 183.23. Initial bias is mildly on the downside this week, to extend the corrective pattern from 183.99, back towards 176.29 support. On the upside, decisive break of 183.99 will resume larger up trend.

In the bigger picture, as long as 172.11 resistance turned support holds, up trend from 123.94 (2020 low) is expected to continue through 183.99 at a later stage, towards 195.86 (2015 high). Nevertheless, firm break of 172.11 will argue that larger correction is already underway.

In the longer term picture, rise from 122.75 (2016 low) in still in progress to retest 195.86 (2015 high). Based on current momentum, break of 195.86 is in favor. But strong resistance could still be seen from 61.8% retracement of 251.09 (2007 high) to 116.83 (2011 low) at 199.80 to limit upside on first attempt.

EUR/JPY Weekly Outlook

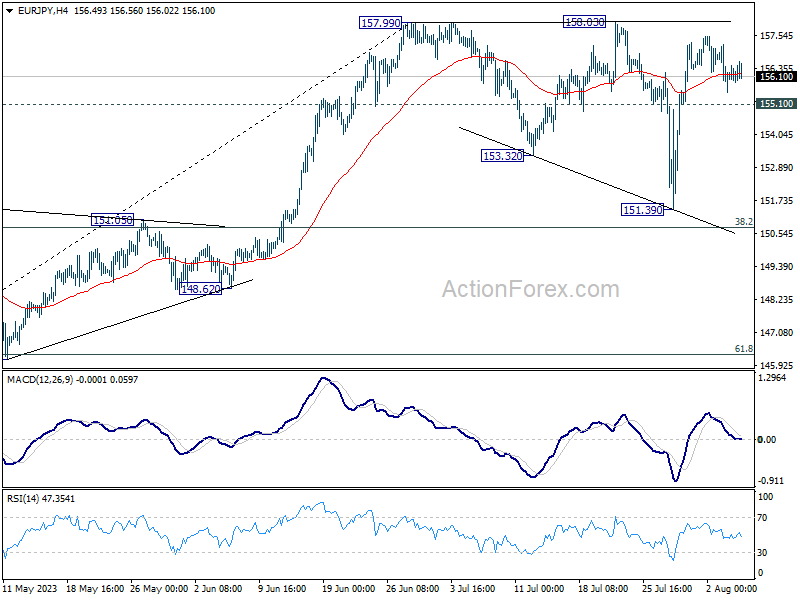

EUR/JPY's rally was capped below 158.03 resistance last week and turned sideway. Initial bias stays neutral this week first. On the upside, decisive break of 157.99/158.03 will resume larger up trend to 162.82 projection level next. However, break of 155.10 will extend the corrective pattern from 157.99 with another falling leg instead.

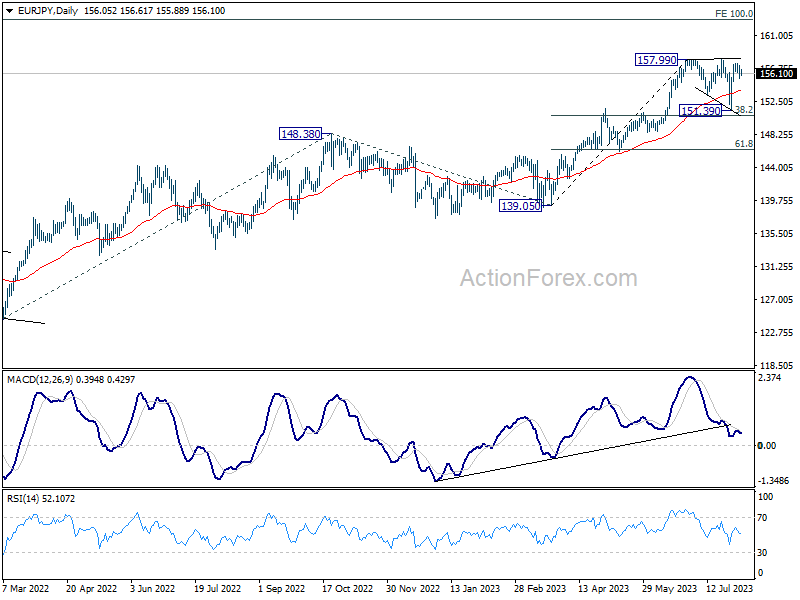

In the bigger picture, as long as 151.60 resistance turned support holds, rise from 114.42 (2020 low) is in progress. On resumption, next target is 100% projection of 124.37 to 148.38 from 138.81 at 162.82. Nevertheless, sustained break of 151.60 will argue that larger correction is already underway. Deeper decline would be seen to 55 W EMA (now at 145.94).

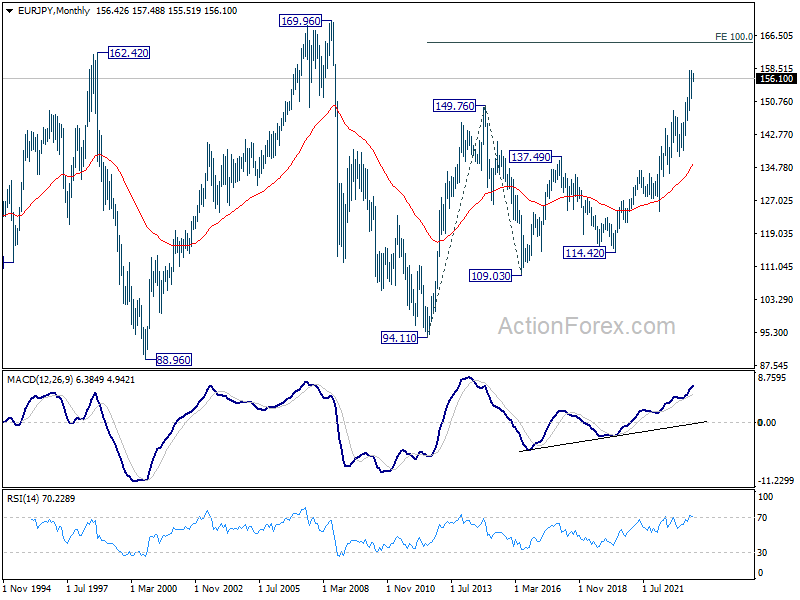

In the long term picture, rise from 109.03 (2016 low) is seen as the third leg of the whole up trend from 94.11 (2012 low). Next target is 100% projection of 94.11 to 149.76 from 109.03 at 164.68, and possibly further to 169.96 (2008 high).

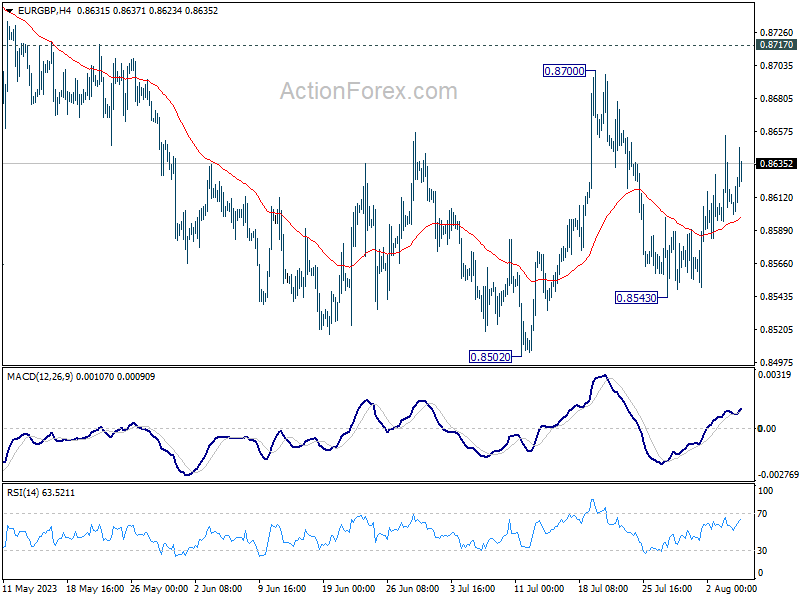

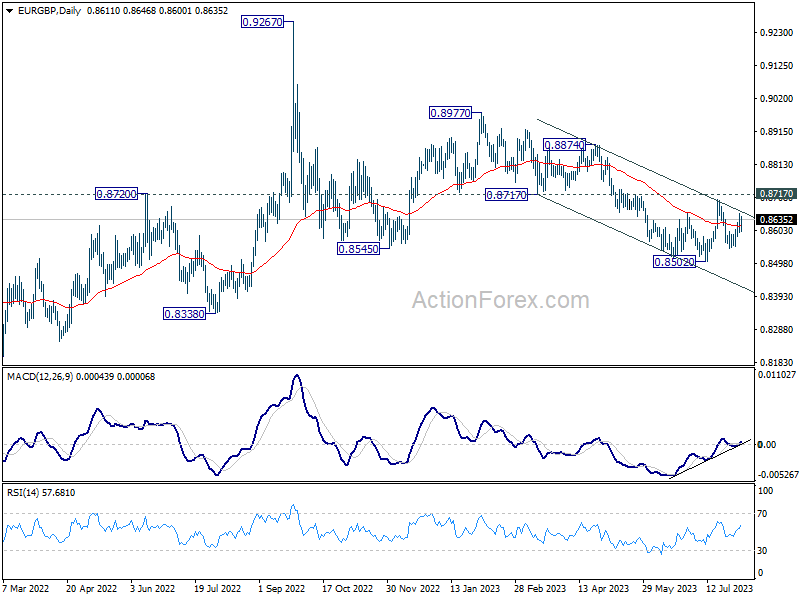

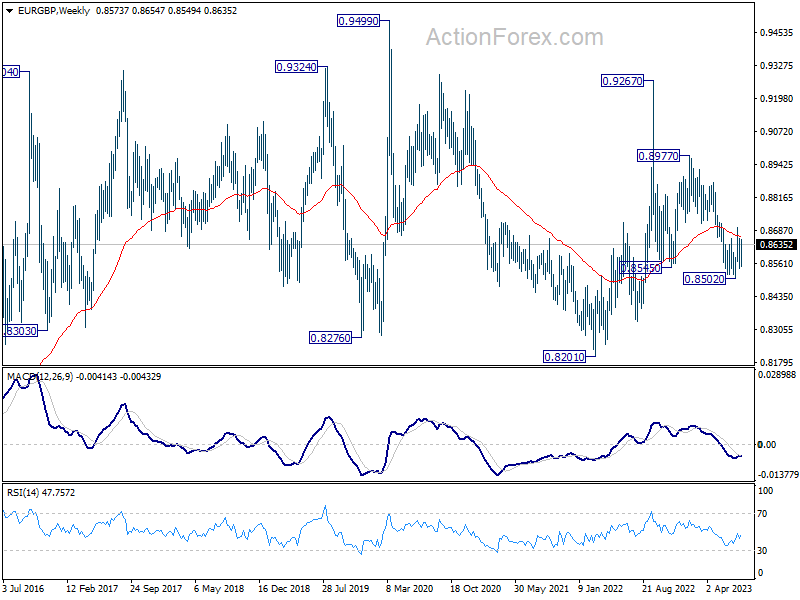

EUR/GBP Weekly Outlook

EUR/GBP was bounded in range trading last week but upside was capped comfortably below 0.8717 support turned resistance for now. Initial bias stays neutral this week first. On the downside, below 0.8543 will target a test on 0.8502 low. Decisive break there will resume larger decline from 0.8977. On the upside firm break of 0.8717 resistance will suggest larger reversal and target 0.8874 resistance next.

In the bigger picture, the down trend from 0.9267 (2022 high) is seen as part of the long term range pattern from 0.9499 (2020 high). Firm break of 0.8717 support turned resistance will argue that it has completed with three waves down to 0.8502. Further break of 0.8977 will bring retest of 0.9267 high. Nevertheless, rejection by 0.8717, followed by break of 0.8502 will resume the decline towards 0.8201 (2022 low).

In the long term picture, long term range pattern is extending. But rise from 0.6935 (2015 low) is expected to resume at a later stage, to 0.9799 (2009 high).

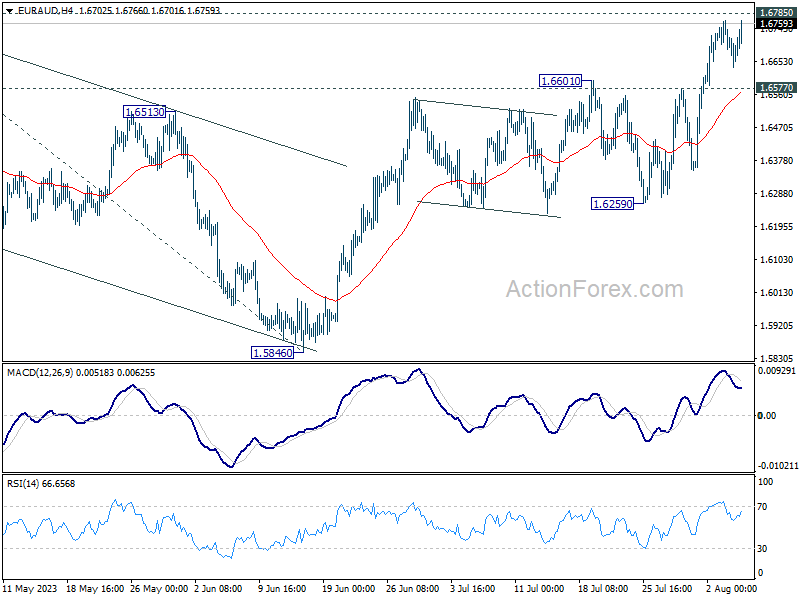

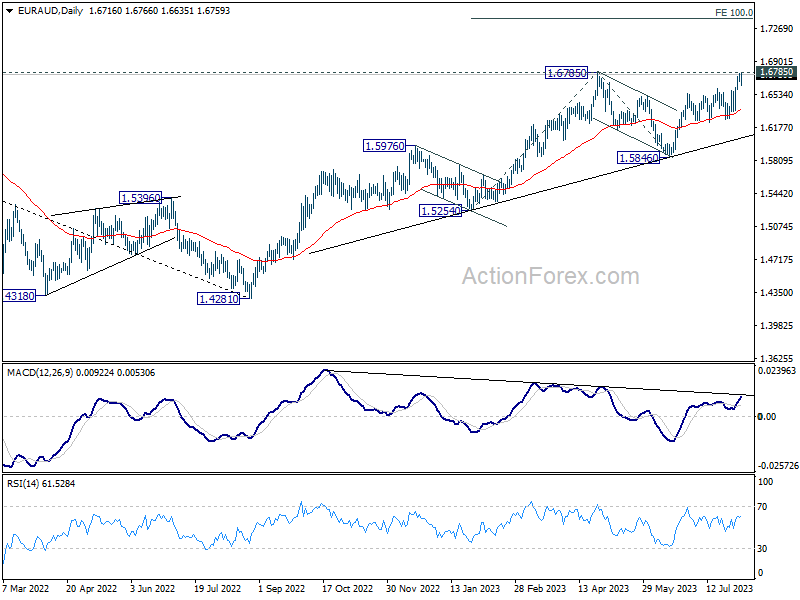

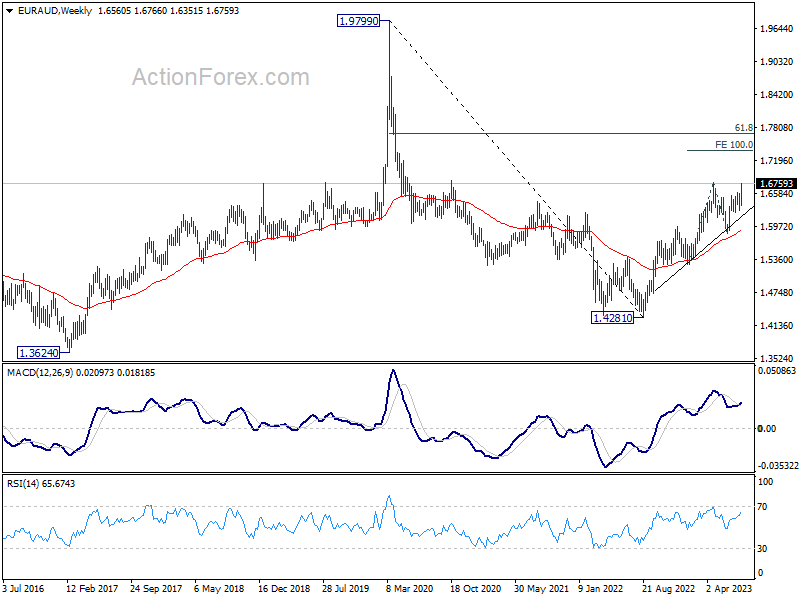

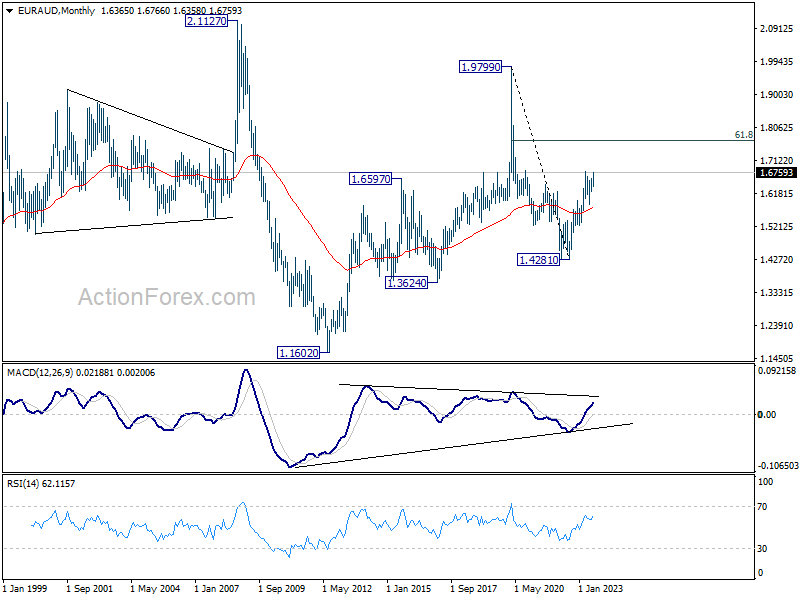

EUR/AUD Weekly Outlook

EUR/AUD's rise from 1.5846 resumed last week and hit as high as 1.6766. Immediate focus is now on 1.6785 resistance this week. Decisive break there will confirm resumption of larger up trend, and target 1.7377 projection level next. On the downside, break of 1.6577 resistance turned support will turn bias back to the downside for 1.6259 support, to extend the corrective pattern from 1.6785.

In the bigger picture, the rise from 1.4281 (2022 low) is in progress. Firm break of 1.6785 will confirm resumption for 100% projection of 1.5254 to 1.6785 from 1.5846 at 1.7377. For now, outlook will stay bullish as long as 1.5846 support holds, even in case of another pull back.

In the longer term picture, it's still early to decide if rise from 1.4281 is resuming whole up trend from 1.1602 (2012 low). But in either case, further rally is in favor as long as 1.5846 support holds. Next target is 61.8% retracement of 1.9799 to 1.4281 at 1.7691.

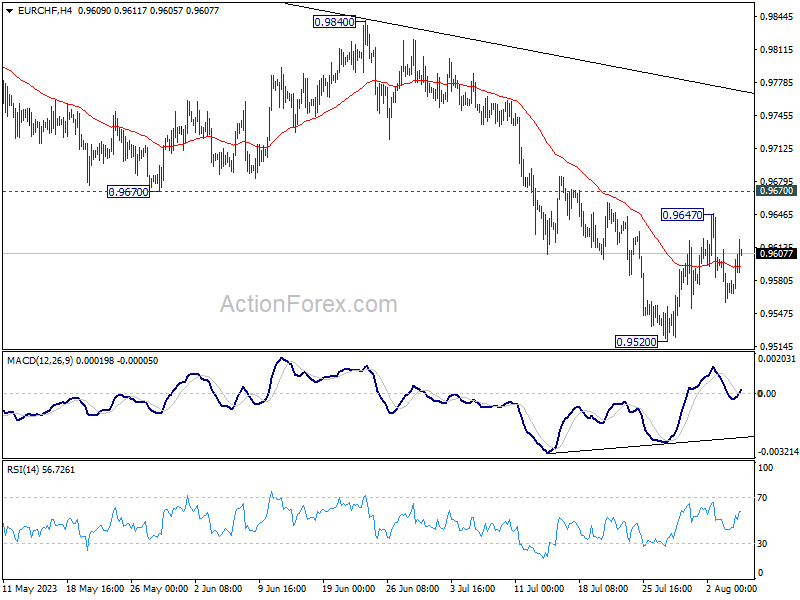

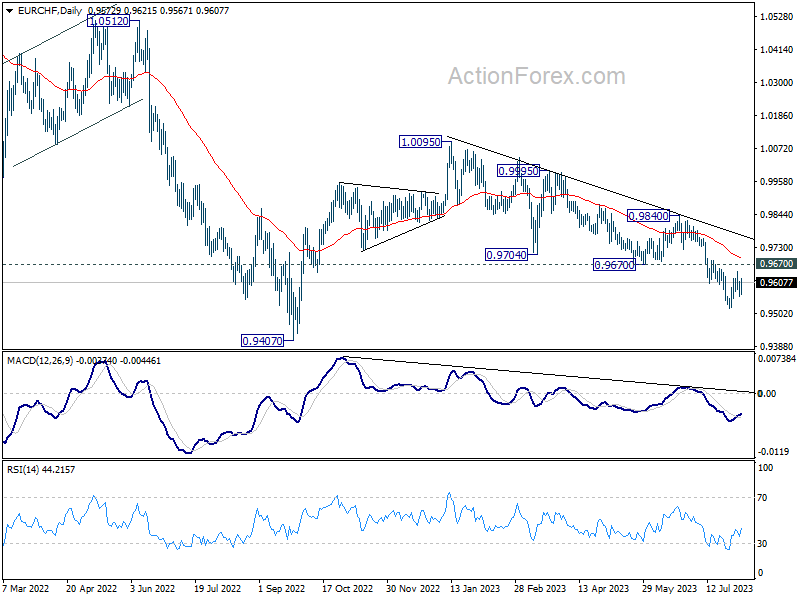

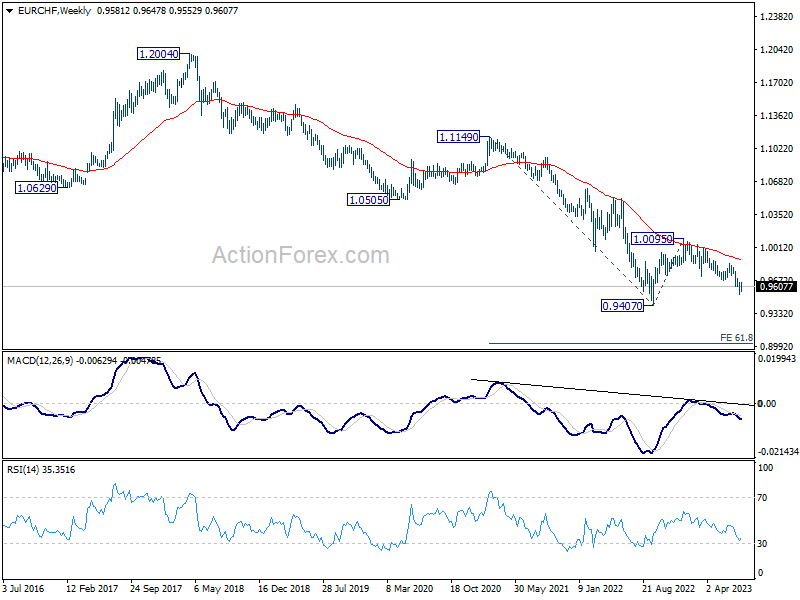

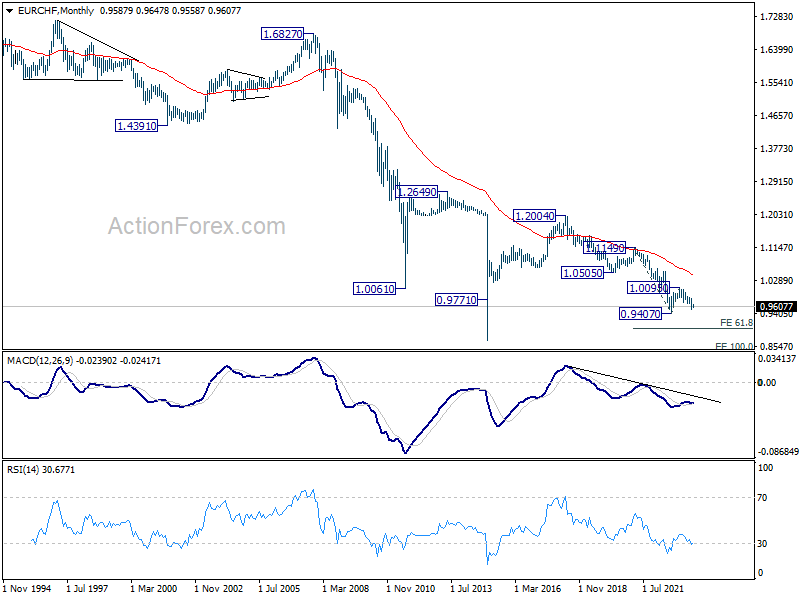

EUR/CHF Weekly Outlook

EUR/CHF's rebound from 0.9520 was capped at 0.9647 last week, below 0.9670 support turned resistance and retreated. Initial bias remains neutral this week first. Further decline is in favor as long as 0.9670 holds. On the downside, break of 0.9520 will resume the whole fall from 1.0095 towards 0.9407 low. Nevertheless, sustained break of 0.9670 will be the first sign of bullish reversal and target 0.9840 resistance for confirmation.

In the bigger picture, medium term outlook is staying bearish as the pair is capped well below falling 55 W EMA (now at 0.9869). Down trend from 1.2004 (2018 high) is in favor to continue. Sustained break of 0.9407 will target 61.8% projection of 1.1149 to 0.9407 from 1.0095 at 0.9018. For now, this will remain the favored case as long as 0.9840 resistance holds, in case of strong rebound.

In the long term picture, outlook remains bearish as it's staying well below 55 M EMA (now at 1.0423). Break of 1.00095 resistance is needed to be the first sign of bottoming, or the multi-decade down trend is expected to continue.

Weekly Economic & Financial Commentary: First Glimpse Points to July Activity Remaining Firm

Summary

United States: First Glimpse Points to July Activity Remaining Firm

- Following last week's data, which brought some encouraging updates showing ongoing strong growth and easing inflation, this week continued with the first look at key July indicators, including more evidence that the labor market continues to gradually cool.

- Next week: Consumer Credit (Mon.), NFIB Small Business Optimism (Tues.), CPI (Thu.)

International: Central Bank Bonanza

- This week, multiple central banks met to assess monetary policy. Policymakers across the G10 and emerging markets gathered to discuss economic conditions as well as set interest rates. Results varied as select institutions opted for additional tightening, some held monetary policy settings steady, while others opted for interest rate cuts.

- Next week: China Activity Data (Mon.-Fri.), Reserve Bank of India (Thu.), Central Bank of Mexico (Thu.)

Credit Market Insights: A Sweltering Summer for Credit Markets

- Credit markets are feeling the heat. The quarterly SLOOS report released on Monday detailed tightened lending standards and gradually weakening loan demand during the second quarter. The report shows that as credit has gotten expensive, consumers have pulled back on borrowing and lenders' risk appetites have dimmed. In addition, the Small Business Administration implemented a lending policy overhaul this week that aims to widen small business' access to credit.

Topic of the Week: Down but Not Out

- Fitch Ratings downgraded the United States’ long-standing credit rating from the top rating of “AAA” to “AA+.” This is only the second time in U.S. history that a credit rating agency has downgraded the country’s sovereign credit rating. Such a move raises concerns over an increase of the federal government’s borrowing costs.

The Weekly Bottom Line: Tighter Credit Weighs on Resilience

U.S. Highlights

- Fitch became the second major credit rating agency to downgrade the U.S. from the top AAA rating, citing the growing fiscal debt burden and an erosion in governance.

- The U.S. economy added 187k new jobs in July, representing the slowest pace of hiring in over two years.

- The Federal Reserve’s Senior Loan Officer Opinion Survey showed credit standards tightened across the board in the second quarter, weighing on loan demand.

Canadian Highlights

- The Canadian economy shed employment in July, pointing to looser labour market conditions. Wage growth accelerated on the month but is expected to normalize in the coming months.

- Our internal data suggests that Canadian families tightened their purses in June. All in, it looks like personal consumption expenditures are poised to decelerate notably in the second quarter.

- With employment and consumption shifting into a lower gear, the Bank of Canada will feel less pressure to hike again.

U.S. – Tighter Credit Weighs on Resilience

Nearly twelve years to the day of the first U.S. credit rating downgrade in 2011, Fitch became the second major rating agency to lower its evaluation of the government’s creditworthiness. Fitch’s rationale was related to growing fiscal deficits in the near-term, medium-term fiscal challenges stemming from aging demographics, and a multi-decade erosion of governance. Since the decision was announced on Tuesday, Treasury yields rose and equities fell, with the ten-year Treasury up 11 basis-points (bps) and the S&P 500 down 1.8% as of the time of writing. Broader implications are expected to be muted as the U.S. economy continues to have strong fundamentals, however it comes at a time when credit standards are already tight.

Monday’s Federal Reserve’s Senior Loan Officer Opinion Survey (SLOOS) showed that a significant share of banks had tightened business and consumer lending standards in the second quarter. Unsurprisingly, demand for most loan types fell over the period, with the only exception being credit card loans, which saw no change in demand. The economy is clearing feeling the effects of the rapid rise in interest rates over the past 17 months.

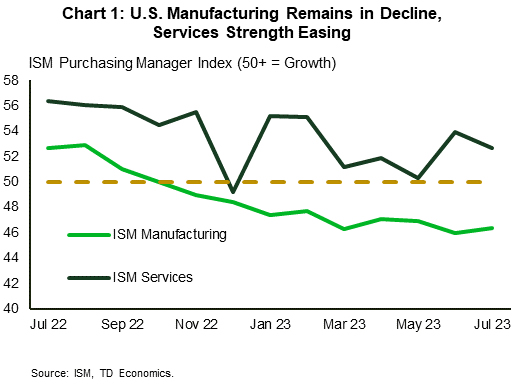

Despite tightening credit conditions, pockets of resilience remain. The ISM PMI data this week continued to show a notable divergence between the manufacturing and service sectors, with the former contracting for a ninth consecutive month and the latter expanding for a seventh straight month in July (Chart 1). Employment growth in both sectors slowed last month, but the services sector is still creating jobs as demand remains robust, whereas the manufacturing employment subindex hit its lowest level in three years.

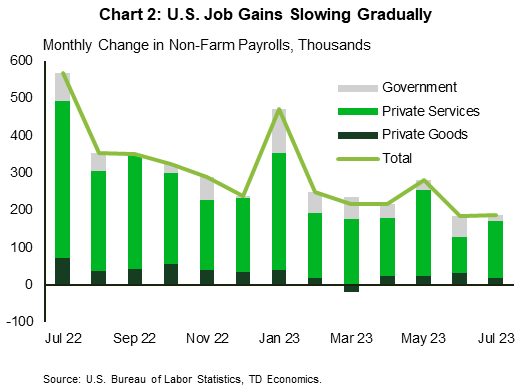

Looking more closely at the most recent labor market update, 187k jobs were created in July, which along with the revised reading for June, represent the slowest pace of job creation in over two years (Chart 2). While this puts job growth on a more sustainable footing, the labor market remains tight, as evidenced by the 4.4% year-on-year(y/y) growth in average weekly earnings in July. The moderation in hiring will be seen as a positive development by the Federal Reserve, but it is unlikely that they will take the prospect of further policy tightening off table until the sustainability of the trend is determined.

The Fed will get another important indicator next week in the form of the CPI inflation reading for July. June’s print showed core CPI fell below 5% y/y for the first time since December 2021 and the Federal Reserve will be looking to see further progress. With preliminary evidence that the cumulative effects of past rate hikes are working to cool inflationary pressures, we expect that the FOMC will leave the policy rate unchanged when they meet in September. However, they are likely to continue to emphasize the importance of incoming data on determining the future path of interest rates as the ultimate form of ‘landing’ for the economy becomes clearer.

Canada – Shifting Into Lower Gear

The weather cooled this week and so did the economy. A negative employment surprise helped prop the S&P TSX Index, which had suffered a steep selloff throughout the week, finishing 1.5% lower (at the time of writing). The 5-year Government of Canada Bond yield move lower, as financial markets recalibrated the expected probability of another Bank of Canada rate hike in September from 30% to 25%.

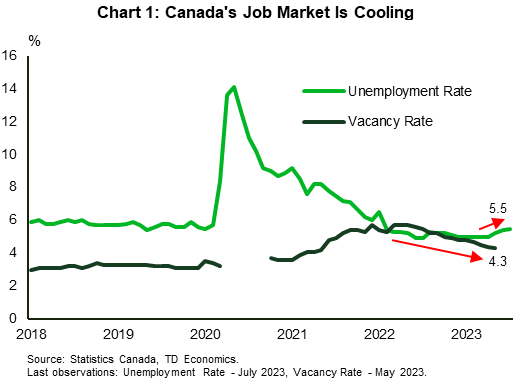

Canada's economy shed 6k jobs in July, missing consensus forecast for 25k growth. Smoothing out the employment numbers over the peaks and valleys of the last three months, provides good evidence of cooling in the labour market: the three-month average change in employment moved decisively below the pre-pandemic average. Likewise, the unemployment rate ticked up to 5.5%, marking a third consecutive month of increases. The speed of the increase in the unemployment rate (half a percent in three months) suggests that a cooling trend is starting to take hold in the job market, even as the level of unemployment rate remains below the 2019 average. The vacancy rate (the share of unfilled positions relative to total number of vacancies) has also been on the downward trend since May 2022, shedding 1.4 percentage points over the course of the last year (Chart 1).

However, wage growth moved in the wrong direction. Average hourly earnings growth accelerated relative to the previous month, increasing by 5.0% over the past year. This is good news for consumer purchasing power, but bad news for inflation dynamics. Typically, looser labour conditions should be followed by slower wage growth with a bit of a lag. We expect wage growth will step back on the downward trend as the labour market cools further in the months ahead, helping to turn the heat down on inflation.

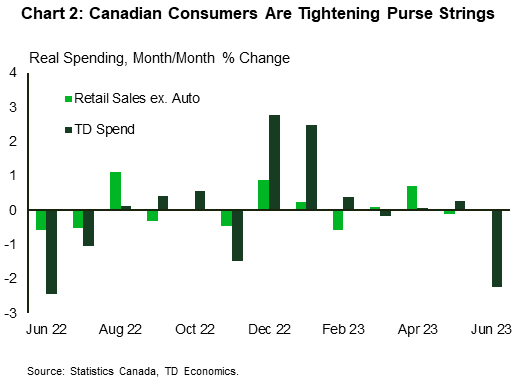

Another sign that the economy is shifting into lower gear is consumer spending. According to our internal card spending data, Canadian families tightened their purse strings in June, spending 2% less than a month prior, with sales up 1.6% versus a year ago, down from a 1.8% pace in May (Chart 2). The series are understandably volatile and affected by TD's geographic concentration, but they usually offer a good directional guide for retail spending and personal consumption expenditures. A closer look at this data shows that the higher cost of living and rising interest rates are starting to catch up with consumers, as discretionary items, such as travel and entertainment were low on consumers' shopping list in June.

With recent data incorporated, real consumption is expected to slow to below 1% in Q2 from an impressive 5.7% growth in Q1 2023. This is good news for the Bank of Canada, as it lowers the pressure for it to hike again at the time when cumulative hikes are starting to play a more prominent role in stemming consumer demand. We expect that the Bank will remain on pause for the rest of the year.

Week Ahead – Will US Core CPI Stay at the Lowest Levels Since 2021?

US

Everyone will be watching the US inflation report as a cool report could help support soft landing hopes and seal the deal for some that the Fed is done raising rates. Expectations for the July inflation report is for headline inflation to rise towards the mid-3% range, while core inflation remains steady and holding onto the lowest levels since 2021 on both a monthly basis at 0.2% and at 4.8% from a year ago. Any hot surprises might bolster the case that the Fed may need to raise rates at the November meeting.

Wall Street will pay close attention to Tuesday’s NFIB Small Business Optimism report and trade data. Thursday is all about the inflation report and the initial jobless claims. Friday contains the release of the PPI report and the preliminary University of Michigan Sentiment report/inflation expectations.

Fed speak will also include appearances by Bostic and Bowman on Monday. Harker speaks on Tuesday and Bostic provides remarks on employment on Thursday.

Earnings for the week include Alibaba Group Holding, Allianz, Bayer, Berkshire Hathaway, China Mobile, China Telecom, Eli Lilly, Honda Motor, Novo Nordisk, Palantir Technologies, Rivian Automotive, RWE, Saudi Arabian Oil, Siemens, SoftBank Group, United Parcel Service, and Walt Disney

Eurozone

Next week starts quickly on Monday with both Eurozone Investor Sentiment and German Industrial Production. The August Sentix Eurozone sentiment reading should show confidence remains low in August, declining further from -22.5 to -25.0. The June German industrial production data should show the manufacturing isn’t ready to rebound as expectations on a monthly basis are for a -0.5% drop, worse than the -0.2% prior reading. Weakening data points should support the view that inflation will slow significantly later this year.

UK

This week is all about growth and that is disappearing in the UK. Friday’s preliminary look at Q2 GDP is expected to show the economy is stagnating. The consensus estimate for Q2 GDP is for a flat reading (consensus range of 0.0% to 0.1%), down from 0.1% in Q1. The BOE is still likely to deliver more rate hikes, which should mean the UK economy is recession bound.

Russia

The CBR will have further pressure to keep on raising rates after a hot July inflation report. Headline inflation in July is expected to jump from 3.25% to 4.25%, well above the 4% target. At the end of the week, the release of the advance Q2 GDP reading is expected to show the economy rebounded from -1.8% to +3.3%.

South Africa

Next week mainly offers tier two and three economic data with both mining data and Manufacturing production results that are expected to show a modest rebound.

Turkey

A few economic indicators will be released this week, with the focus mainly on June Industrial Production, which should show activity turned negative.

Switzerland

Unemployment data on Monday is expected to show the labor market remains tight as the unemployment rate holds steady at 2.0%. The focus remains on inflation for Switzerland and a strong labor market could keep wages strong and that should support the SNB case for a September hike.

China

Three key data to watch. On Tuesday, the Balance of Trade for July, another horrendous print is being forecasted for exports growth to plunge further to -14% year-on-year from -12.4% recorded in June If it turns out as expected, it will be the third consecutive month of contraction. Imports growth is forecasted to improve slightly to -5.2% year-on-year from -6.8% in June but still a potential fifth consecutive month of contraction. Overall, such forecasts are pointing to a continuation of weak internal and external demand that market participants are getting fatigued from China’s top policymakers’ ongoing stimulus rhetoric that is too vague and too minor in the past two months in order to boost domestic consumption and the languish property sector.

Consumer inflation and producer prices data will be out on Wednesday. Higher odds of deflationary risk as the forecast is calling a negative reading on inflation at -0.3% year-on-year from 0% printed in June. Producer prices are forecasted to contract again to -5% year-on-year from -5.4% in June, a potential ten consecutive months of negative growth.

On Friday, we will have outstanding loan growth and M2 money supply data for July.

On the earnings front, Alibaba, one of China’s Big Tech will report its June quarter 2023 earnings results on Thursday, 10 August. Noteworthy to scrutinise Alibaba’s earnings and forward guidance as China policymakers have loosened their grip on the business operations of China’s Big Tech firms.

India

The key highlight will be RBI’s interest rate decision on Thursday where the consensus is expecting RBI to stand pat at 6.5%, a potential third consecutive of no change on the policy rate due to easing inflationary pressures.

On Friday, industrial production for June will be out, and a drop in growth is being forecasted at 4.1% year-on-year from 5.7% in May, still a potential eight consecutive month of expansion.

Australia

A light data week ahead, Westpac consumer confidence for August out on Tuesday where a dip of -0.7% month-on-month is being forecasted from 2.7% printed in July.

Lastly, consumer inflation expectations for August will be released on Thursday.

New Zealand

Two data to take note of: electronic retail card spending for July out on Wednesday, and manufacturing PMI for July on Friday.

Japan

The Bank of Japan (BoJ) Summary of Opinions will be out on Monday and market participants will be scrutinising any hints on the next step in monetary policy normalisation in terms of timing and form as BoJ has indirectly revised upward on the upper limit of its Yield Curve Control (YCC) on the 10-year JGB yield to 1% during its last meeting in July.

On Tuesday, we will have household spending for June where the consensus is expecting a slight contraction to -4.1% year-on-year from 4% in May but on a month-month basis, a recovery is expected at 0.3% in June from -1.1% printed in May. Bank lending data for July will be released as well on the same day.

Singapore

The only key data will be the Q2 GDP finalised reading out on Friday where the prior flash figures brushed away a recession scare as Q2 q/q and y/y came in positive at 0.3% and 0.7% respectively.

Markets

Energy

Oil prices have remained supported by OPEC+, as they appear committed to keeping this market tight. The upcoming week should have some of the focus shift back to demand. On Monday, Saudi Aramco will post their earnings results. Tuesday has two events, with the release of some key Chinese trade data, which includes oil imports and the US EIA Short-term Energy Outlook (STEO). On Thursday, OPEC publishes their monthly report, while the EIA releases their monthly publication on Friday.

Natural gas prices have also steadied in the US over cooler weather, while Europe continues to deal with a tight market over Norwegian outages.

Gold

After the Treasury’s quarterly refunding announcement, concerns grew over the US widening deficit. Gold pared weekly losses as the bond market selloff saw some relief after the NFP report showed the labor market is softening. The focus next week will be all about US inflation and some major data out of China. Soft landing hopes remain, but that could get rattled if the disinflation process stalls.

Crypto

Bitcoin continues to consolidate below $29,000 as volatility struggles to return. Bitcoin was little changed after both the Treasury quarterly refunding announcement and NFP report. Regulatory decisions and ETF rulings still remain the likely catalysts to trigger a meaningful crypto move.

Saturday, Aug. 5

Economic Events:

- Berkshire Hathaway earnings.

- Saudi Arabia is expected to host talks about Ukraine’s Peace Plans

Sunday, Aug. 6

No major events expected

Monday, Aug. 7

Economic Data/Events:

- China forex reserves

- Germany industrial production

- Thailand CPI

- Saudi Aramco earnings.

- Fed’s Bostic speaks at the bank’s virtual Fed Listens event.

- Fed’s Bowman speaks at a Fed Listens virtual event hosted by the Atlanta Fed.

- Bank of Japan issues Summary of Opinions for July monetary policy meeting.

- BOE Chief Economist Pill participates in an online event.

Tuesday, Aug. 8

Economic Data/Events:

- US wholesale inventories, trade

- Australia Westpac consumer confidence, NAB business confidence

- China trade

- France trade

- Germany CPI

- Japan household spending

- Mexico international reserves

- ECB releases consumer expectations survey.

- US Treasury quarterly refunding auctions commence

- Fed’s Harker speaks on the economic outlook at an event hosted by the Philadelphia Business Journal.

Wednesday, Aug. 9

Economic Data/Events:

- China CPI, PPI, money supply, new yuan loans and aggregate financing

- Japan money stock, machine tool orders

- Mexico CPI

- Russia CPI

Thursday, Aug. 10

Economic Data/Events:

- US initial jobless claims, July CPI m/m: 0.2%e v 0.2% prior; y/y: 3.3%e vs 3.0% prior

- India rate decision: Expected to keep rates unchanged at 6.50%

- Italy CPI

- Japan PPI

- Mexico rate decision: Expected to keep rates unchanged at 11.25%

- New Zealand home sales

- Philippines GDP

- South Africa manufacturing production

- Turkey industrial production

- German Chancellor Scholz visits Waltershausen and Erfurt.

- Fed’s Bostic pre-recorded remarks for employment webinar.

Friday, Aug. 11

Economic Data/Events:

- US University of Michigan consumer sentiment, PPI

- France CPI, unemployment

- India industrial production

- Italy trade

- Mexico industrial production

- New Zealand food prices, Manufacturing PMI

- Russia GDP

- Spain CPI

- Turkey current account

- UK industrial production, GDP

- German Chancellor Olaf Scholz speaks in FFH radio interview.

Sovereign Rating Updates:

- Finland (Fitch)

- Denmark (S&P),

- Switzerland (S&P)

- Germany (Moody’s)

Summary 8/7 – 8/11

Monday, Aug 7, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:50 | JPY | BoJ Summary of Opinions | ||

| 05:00 | JPY | Leading Economic Index Jun P | 108.9 | 109.2 |

| 06:00 | EUR | Germany Industrial Production M/M Jun | -0.40% | -0.20% |

| 07:00 | CHF | Foreign Currency Reserves (CHF) Jul | 725B | |

| 08:30 | EUR | Eurozone Sentix Investor Confidence Aug | -25 | -22.5 |

| 23:01 | GBP | BRC Like-For-Like Retail Sales Y/Y Jul | 3.00% | 4.20% |

| 23:30 | JPY | Labor Cash Earnings Y/Y Jun | 3.00% | 2.50% |

| 23:30 | JPY | Overall Household Spending Y/Y Jun | -3.50% | -4.00% |

| 23:50 | JPY | Bank Lending Y/Y Jul | 3.10% | 3.20% |

| 23:50 | JPY | Current Account (JPY) Jun | 2.24T | 1.70T |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:50 | JPY | BoJ Summary of Opinions | |

| Forecast: | Previous: | ||

| 05:00 | JPY | Leading Economic Index Jun P | |

| Forecast: 108.9 | Previous: 109.2 | ||

| 06:00 | EUR | Germany Industrial Production M/M Jun | |

| Forecast: -0.40% | Previous: -0.20% | ||

| 07:00 | CHF | Foreign Currency Reserves (CHF) Jul | |

| Forecast: | Previous: 725B | ||

| 08:30 | EUR | Eurozone Sentix Investor Confidence Aug | |

| Forecast: -25 | Previous: -22.5 | ||

| 23:01 | GBP | BRC Like-For-Like Retail Sales Y/Y Jul | |

| Forecast: 3.00% | Previous: 4.20% | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y Jun | |

| Forecast: 3.00% | Previous: 2.50% | ||

| 23:30 | JPY | Overall Household Spending Y/Y Jun | |

| Forecast: -3.50% | Previous: -4.00% | ||

| 23:50 | JPY | Bank Lending Y/Y Jul | |

| Forecast: 3.10% | Previous: 3.20% | ||

| 23:50 | JPY | Current Account (JPY) Jun | |

| Forecast: 2.24T | Previous: 1.70T | ||

Tuesday, Aug 8, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Westpac Consumer Confidence Aug | 2.70% | |

| 01:30 | AUD | NAB Business Conditions Jul | 9 | |

| 01:30 | AUD | NAB Business Confidence Jul | 0 | |

| 03:00 | CNY | Trade Balance (USD) Jul | 67.8B | 70.6B |

| 03:00 | CNY | Trade Balance (CNY) Jul | 470B | 491B |

| 05:00 | JPY | Eco Watchers Survey: Outlook Jul | 54.5 | 53.6 |

| 06:00 | EUR | Germany CPI M/M Jul F | 0.30% | 0.30% |

| 06:00 | EUR | Germany CPI Y/Y Jul F | 6.20% | 6.20% |

| 06:45 | EUR | France Trade Balance (EUR) Jun | -8.0B | -8.4B |

| 10:00 | USD | NFIB Business Optimism Index Jul | 90.6 | 91.0 |

| 12:30 | USD | Trade Balance (USD) Jun | -65.2B | -69.0B |

| 12:30 | CAD | Trade Balance (CAD) Jun | -1.7B | -3.4B |

| 14:00 | USD | Wholesale Inventories Jun F | -0.30% | -0.30% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Westpac Consumer Confidence Aug | |

| Forecast: | Previous: 2.70% | ||

| 01:30 | AUD | NAB Business Conditions Jul | |

| Forecast: | Previous: 9 | ||

| 01:30 | AUD | NAB Business Confidence Jul | |

| Forecast: | Previous: 0 | ||

| 03:00 | CNY | Trade Balance (USD) Jul | |

| Forecast: 67.8B | Previous: 70.6B | ||

| 03:00 | CNY | Trade Balance (CNY) Jul | |

| Forecast: 470B | Previous: 491B | ||

| 05:00 | JPY | Eco Watchers Survey: Outlook Jul | |

| Forecast: 54.5 | Previous: 53.6 | ||

| 06:00 | EUR | Germany CPI M/M Jul F | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 06:00 | EUR | Germany CPI Y/Y Jul F | |

| Forecast: 6.20% | Previous: 6.20% | ||

| 06:45 | EUR | France Trade Balance (EUR) Jun | |

| Forecast: -8.0B | Previous: -8.4B | ||

| 10:00 | USD | NFIB Business Optimism Index Jul | |

| Forecast: 90.6 | Previous: 91.0 | ||

| 12:30 | USD | Trade Balance (USD) Jun | |

| Forecast: -65.2B | Previous: -69.0B | ||

| 12:30 | CAD | Trade Balance (CAD) Jun | |

| Forecast: -1.7B | Previous: -3.4B | ||

| 14:00 | USD | Wholesale Inventories Jun F | |

| Forecast: -0.30% | Previous: -0.30% | ||

Wednesday, Aug 9, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | CNY | CPI Y/Y Jul | -0.40% | 0.00% |

| 01:30 | CNY | PPI Y/Y Jul | -3.80% | -5.40% |

| 03:00 | NZD | RBNZ Inflation Expectations Q/Q Q3 | 2.79% | |

| 06:00 | JPY | Machine Tool Orders Y/Y Jul P | -21.70% | |

| 12:30 | CAD | Building Permits M/M Jun | 2.30% | 10.50% |

| 14:30 | USD | Crude Oil Inventories | -17.0M | |

| 23:01 | GBP | RICS Housing Price Balance Jul | -51% | -46% |

| 23:50 | JPY | PPI Y/Y Jul | 3.50% | 4.10% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | CNY | CPI Y/Y Jul | |

| Forecast: -0.40% | Previous: 0.00% | ||

| 01:30 | CNY | PPI Y/Y Jul | |

| Forecast: -3.80% | Previous: -5.40% | ||

| 03:00 | NZD | RBNZ Inflation Expectations Q/Q Q3 | |

| Forecast: | Previous: 2.79% | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Jul P | |

| Forecast: | Previous: -21.70% | ||

| 12:30 | CAD | Building Permits M/M Jun | |

| Forecast: 2.30% | Previous: 10.50% | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -17.0M | ||

| 23:01 | GBP | RICS Housing Price Balance Jul | |

| Forecast: -51% | Previous: -46% | ||

| 23:50 | JPY | PPI Y/Y Jul | |

| Forecast: 3.50% | Previous: 4.10% | ||

Thursday, Aug 10, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:00 | AUD | Consumer Inflation Expectations Aug | 5.20% | |

| 08:00 | EUR | ECB Economic Bulletin | ||

| 12:30 | USD | Initial Jobless Claims (Aug 4) | 230K | 227K |

| 12:30 | USD | CPI M/M Jul | 0.20% | 0.20% |

| 12:30 | USD | CPI Y/Y Jul | 3.00% | |

| 12:30 | USD | CPI Core M/M Jul | 0.20% | 0.20% |

| 12:30 | USD | CPI Core Y/Y Jul | 4.70% | 4.80% |

| 14:30 | USD | Natural Gas Storage | 14B | |

| 22:30 | NZD | Business NZ PMI Jul | 47.5 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:00 | AUD | Consumer Inflation Expectations Aug | |

| Forecast: | Previous: 5.20% | ||

| 08:00 | EUR | ECB Economic Bulletin | |

| Forecast: | Previous: | ||

| 12:30 | USD | Initial Jobless Claims (Aug 4) | |

| Forecast: 230K | Previous: 227K | ||

| 12:30 | USD | CPI M/M Jul | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 12:30 | USD | CPI Y/Y Jul | |

| Forecast: | Previous: 3.00% | ||

| 12:30 | USD | CPI Core M/M Jul | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 12:30 | USD | CPI Core Y/Y Jul | |

| Forecast: 4.70% | Previous: 4.80% | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 14B | ||

| 22:30 | NZD | Business NZ PMI Jul | |

| Forecast: | Previous: 47.5 | ||

Friday, Aug 11, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 06:00 | GBP | GDP Q/Q Q2 P | 0.00% | 0.10% |

| 06:00 | GBP | GDP M/M Jun | 0.20% | -0.10% |

| 06:00 | GBP | Industrial Production M/M Jun | -0.10% | -0.60% |

| 06:00 | GBP | Industrial Production Y/Y Jun | -2.10% | -2.30% |

| 06:00 | GBP | Manufacturing Production M/M Jun | 0.10% | -0.20% |

| 06:00 | GBP | Manufacturing Production Y/Y Jun | -1.00% | -1.20% |

| 06:00 | GBP | Goods Trade Balance (GBP) Jun | -16.2B | -18.7B |

| 08:00 | EUR | Italy Trade Balance (EUR) Jun | 4.23B | 4.71B |

| 11:00 | GBP | NIESR GDP Estimate (3M) Jul | 0.00% | |

| 12:30 | USD | PPI M/M Jul | 0.10% | 0.10% |

| 12:30 | USD | PPI Y/Y Jul | 0.10% | |

| 12:30 | USD | PPI Core M/M Jul | 0.20% | 0.10% |

| 12:30 | USD | PPI Core Y/Y Jul | 2.40% | |

| 14:00 | USD | Michigan Consumer Sentiment Index Aug P | 70.9 | 71.6 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 06:00 | GBP | GDP Q/Q Q2 P | |

| Forecast: 0.00% | Previous: 0.10% | ||

| 06:00 | GBP | GDP M/M Jun | |

| Forecast: 0.20% | Previous: -0.10% | ||

| 06:00 | GBP | Industrial Production M/M Jun | |

| Forecast: -0.10% | Previous: -0.60% | ||

| 06:00 | GBP | Industrial Production Y/Y Jun | |

| Forecast: -2.10% | Previous: -2.30% | ||

| 06:00 | GBP | Manufacturing Production M/M Jun | |

| Forecast: 0.10% | Previous: -0.20% | ||

| 06:00 | GBP | Manufacturing Production Y/Y Jun | |

| Forecast: -1.00% | Previous: -1.20% | ||

| 06:00 | GBP | Goods Trade Balance (GBP) Jun | |

| Forecast: -16.2B | Previous: -18.7B | ||

| 08:00 | EUR | Italy Trade Balance (EUR) Jun | |

| Forecast: 4.23B | Previous: 4.71B | ||

| 11:00 | GBP | NIESR GDP Estimate (3M) Jul | |

| Forecast: | Previous: 0.00% | ||

| 12:30 | USD | PPI M/M Jul | |

| Forecast: 0.10% | Previous: 0.10% | ||

| 12:30 | USD | PPI Y/Y Jul | |

| Forecast: | Previous: 0.10% | ||

| 12:30 | USD | PPI Core M/M Jul | |

| Forecast: 0.20% | Previous: 0.10% | ||

| 12:30 | USD | PPI Core Y/Y Jul | |

| Forecast: | Previous: 2.40% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Aug P | |

| Forecast: 70.9 | Previous: 71.6 | ||

Forward Guidance: Core US Inflation to Tick Lower Again in July

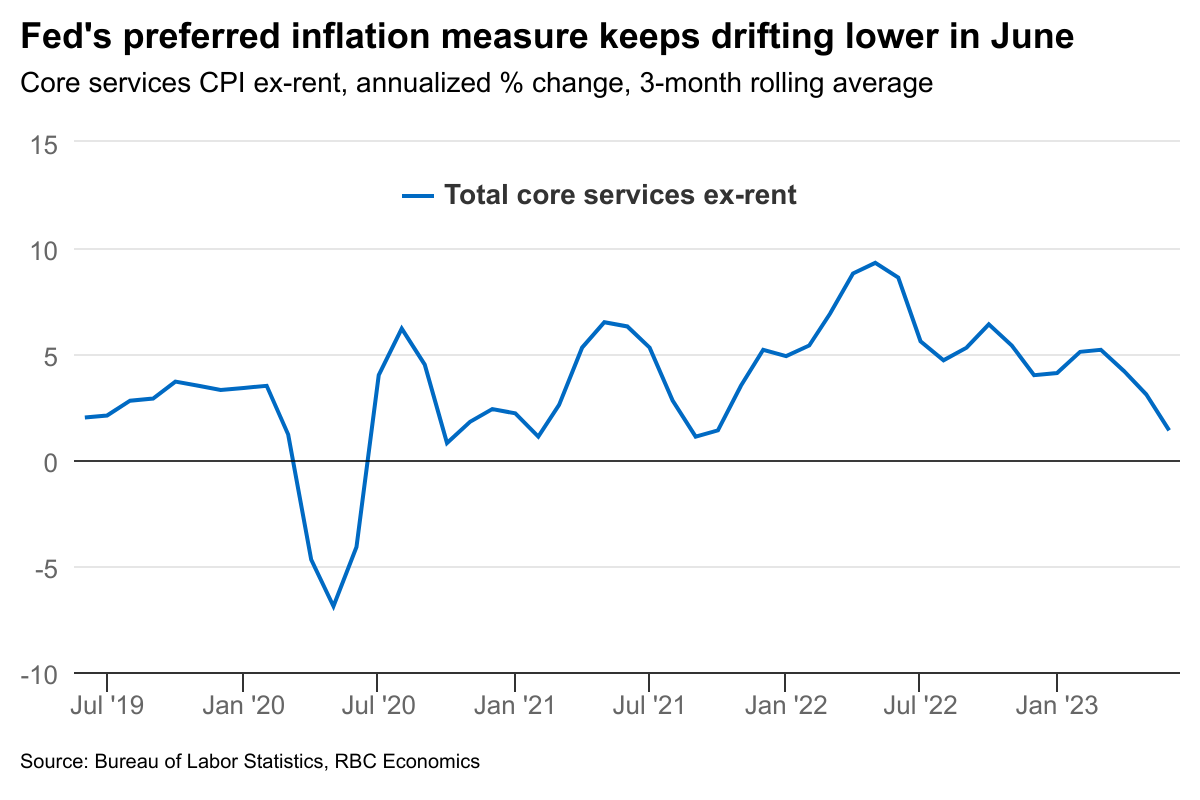

Year-over-year growth in U.S. consumer prices likely ticked slightly higher for the first time in a year in July - gasoline prices didn’t move much this July but a larger 8% drop in July a year ago will fall out of the 12-month growth rate. Year-over-year growth in core (ex-food & energy) prices will still be high (we expect +4.7%) in July, but we expect a moderate 0.2% month-over-month increase to match the June gain. Slower growth in core CPI has come alongside a pullback in home rent inflation as earlier slowing in market asking rent growth feed through to lower rent CPI with a lag as contracts get renewed.

Stripping out shelter, energy, food and other goods, the Fed’s “supercore” CPI will be watched closely for signs that easing domestic inflation pressures are being sustained. The measure is designed to get a better gauge of broader inflation trends driven by domestic rather than global inflation pressures. It has slowed sharply in recent months – month-over-month increases averaged a 1.4% annualized rate in the three months to June (below the Federal Reserve’s 2% inflation objective) thanks to a month over month decline that was also the first one in two years.

Recent moderation in U.S. inflation has led to some speculation that slower consumer spending and weaker labour markets might not be needed to get inflation back under control – increasing the odds of a ’soft landing’ for the economy. Still, we continue to think that aggressive interest rates over the last year and a half will have economic consequences, even if the economy has been more resilient than expected to-date. Household liquid real assets, including cash, checking and time deposits have been dropping lower since early 2022. The share of consumer credit card and auto loans that are moving into 30-day delinquency status have also risen over recent quarters. With indicators on household finances suggesting rising number of challenges, it will be a matter of time for consumer demand to slow more significantly, bringing down GDP growth and labour demand along the way. Fed chair Powell in the July press conference stressed that hiking all the way until inflation’s back to 2% will be a “prescription of going way past target”. Absent a reacceleration in core inflation, we expect the Fed to step to and stay on the sideline and maintain the Fed Funds at 5.25% - 5% range until 2024.

Week ahead data watch

Canadian trade deficit likely narrowed from $-3.4 billion in May to $-3.2 billion in June. Exports (-1.2%) and imports (-1.6%) both declined during that month. Our expectation echoes with StatCan’s advance estimates on manufacturing sales and wholesales trade, both pointing to sizable contractions, and foreshadowing lower trade flows.

According to the advance U.S. economic indicators, the goods deficit shrank by $4 billion from the prior month in June. Exports on goods ticked up 0.2% on a month-over-month basis, supported by capital goods and other goods. Imports fell by 1.4%, slowdowns saw in several baskets, including industrial supplies (-4.4%), capital goods (-3.3%), and other goods (-4.2%).