Sample Category Title

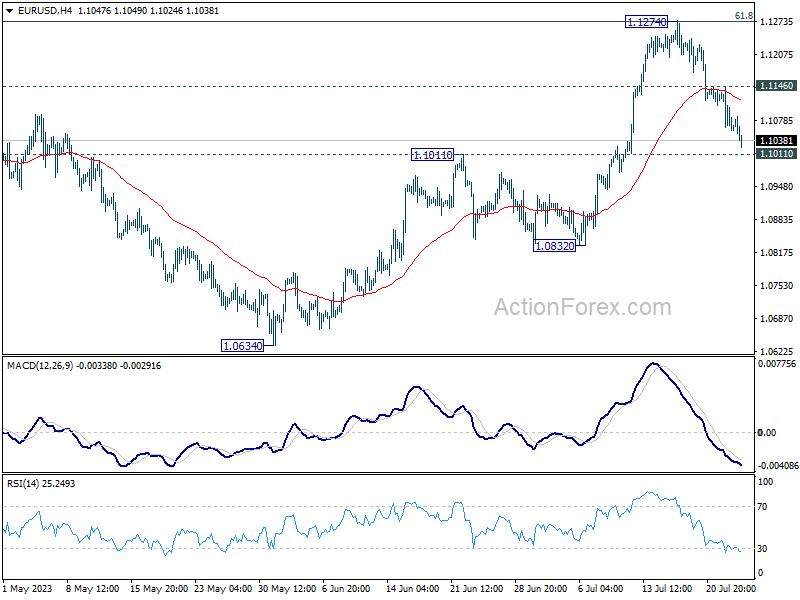

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1034; (P) 1.1091; (R1) 1.1121; More...

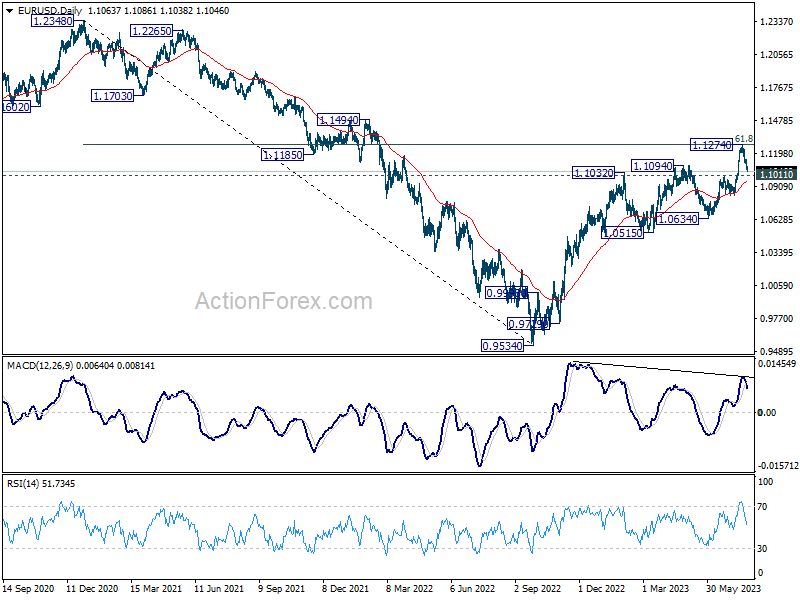

EUR/USD's fall from 1.1274 continues today and intraday bias stays on the downside. Still, outlook will remain bullish as long as 1.1011 resistance turned support holds. Above 1.1146 minor resistance will turn bias back to the upside for retesting 1.1274 high first. However, firm break of 1.1011 will argue that larger correction is underway.

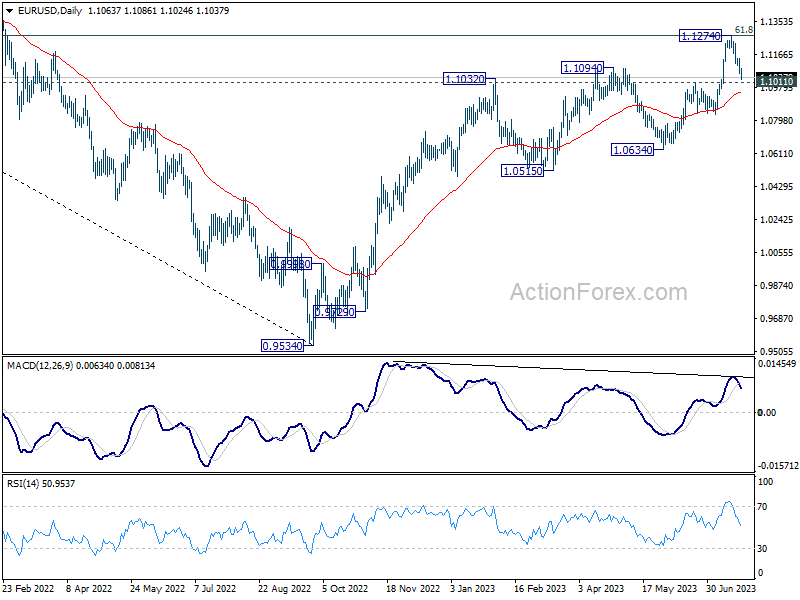

In the bigger picture, rise from 0.9534 is still expected to continue as long as 1.1011 resistance turned support holds. Decisive break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next. However, firm break of 1.1011 will bring deeper fall back to 1.0634 support next.

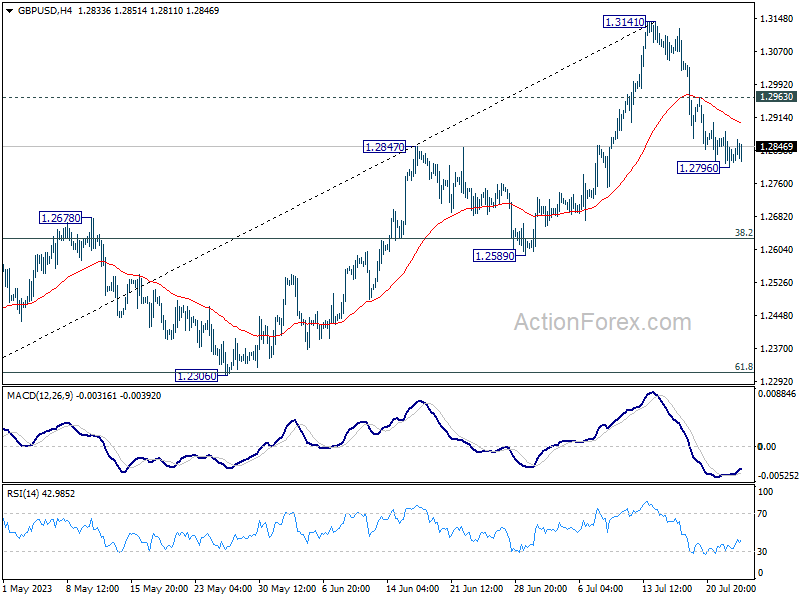

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2787; (P) 1.2835; (R1) 1.2873; More...

Intraday bias in GBP/USD remains neutral for the moment. On the downside, below 1.2796 will resume the fall from 1.3141 to 55 D EMA (now at 1.2703) next. On the upside, break of 1.2963 minor resistance will turn bias back to the upside retest 1.3141 high instead.

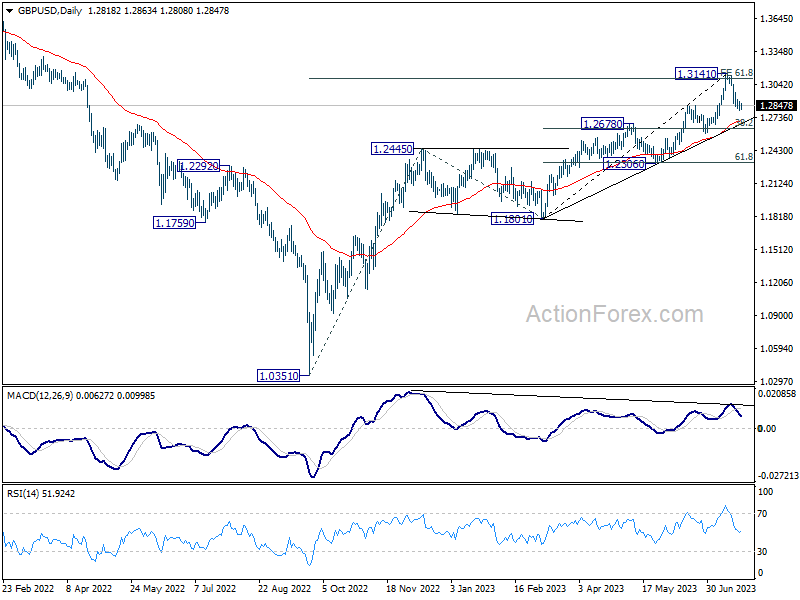

In the bigger picture, as long as 1.2678 resistance turned support holds, rise form 1.0351 (2022 low) is expected to continue. Next target is 100% projection of 1.0351 to 1.2445 from 1.1801 at 1.3895. However, sustained break of 1.2678 will argue that it's at least correcting this rally, with risk of bearish reversal.

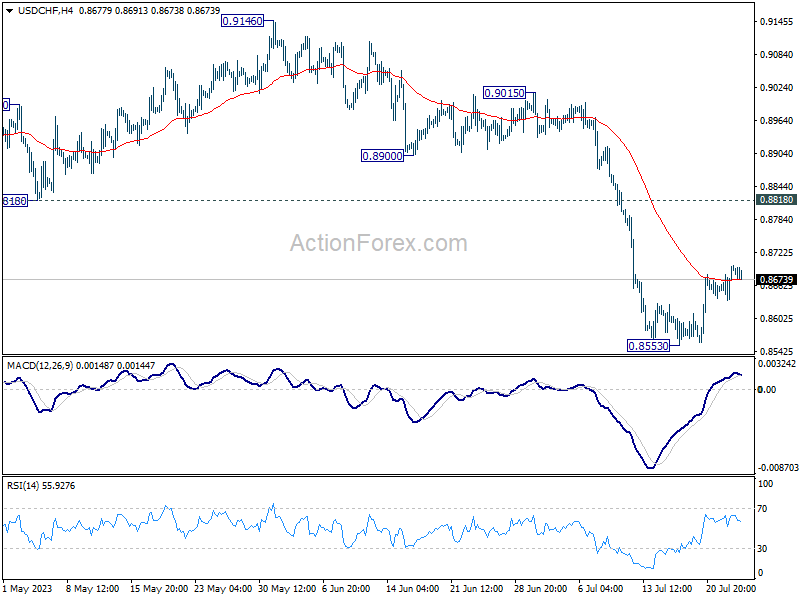

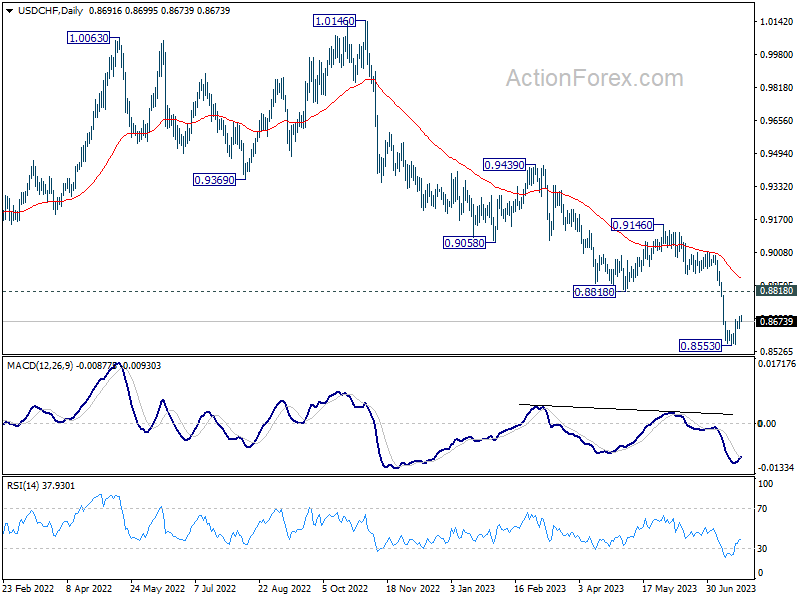

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8656; (P) 0.8678; (R1) 0.8719; More...

USD/CHF's rebound from 0.8553 is still in progress and intraday bias stays mildly on the upside. Further rally would be seen towards 0.8818 support turned resistance. Rejection by 0.8818 will retain near term bearishness for another decline through 0.8553. Meanwhile for now, risk will stay mildly on the upside as long as 0.8553 holds, in case of retreat.

In the bigger picture, the break of 0.8756 (2021 low) indicates break out from the long term range pattern. For now, medium term outlook will stay bearish as long as 0.9146 resistance holds. Further fall would be seen to 61.8% retracement of 0.7065 (2011 low) to 1.0342 (2016 high) at 0.8317 next.

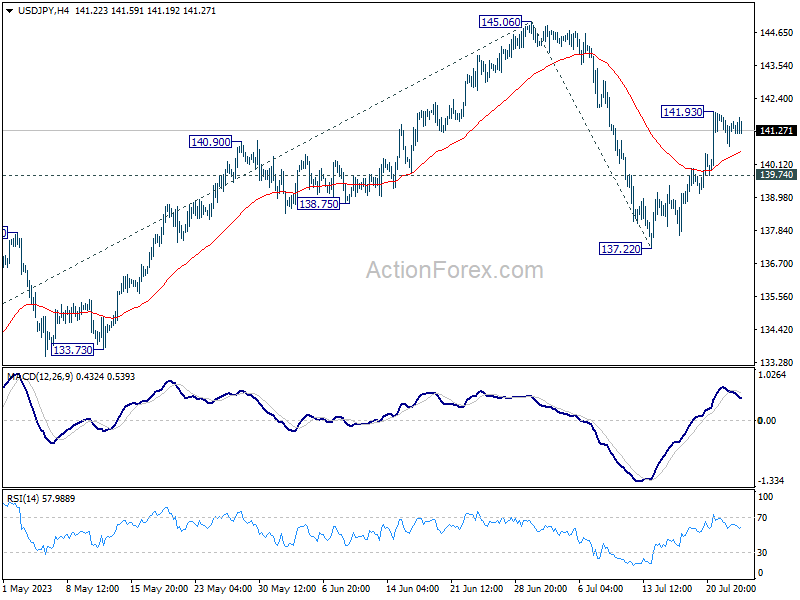

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 140.88; (P) 141.35 (R1) 141.94; More...

USD/JPY is staying in consolidation below 141.93 temporary top and intraday bias remains neutral. But further rally is mildly in favor. On the upside, above 141.93 will resume the rebound from 137.22 to 145.06 first. Firm break there will target 61.8% projection of 129.62 to 127.22 from 145.06 at 146.76 next. On the downside, below 139.74 minor support will bring retest of 137.22 instead.

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Current development suggests that the second leg (the rise from 127.20) might not be over yet. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.

Sunset Market Commentary

Markets

The ECB’s Bank Lending Survey was in the spotlights today. The quarterly questionnaire involving 158 banks showed credit standards for loans or credit to enterprises (commercial real estate and energy-intensive manufacturing in particular) and households – both for house purchases and other purposes – have tightened further in 2023Q2. “Higher risk perceptions related to the economic outlook and borrower-specific situation, lower risk tolerance as well as banks’ higher cost of funds contributed to the tightening”, the ECB explained. The financial sector for the current quarter expects a further, albeit more moderate net tightening of credit standards on enterprise loans while those for loans to households for house purchases are expected to be unchanged. Loan demand from firms dropped to an all-time low since the start of the survey in 2003. The net decrease was substantially stronger than banks expected in Q1 and driven by rising interest rates and lower financing needs for fixed investments. The respondents also pointed out a strong net decrease in household demand for housing loans. The demand decline is seen continuing in Q3 too, but at a much smaller pace. Today’s published survey is another sign that the ECB’s rapid tightening cycle is filtering through the economy as intended. Published simultaneously was the German July Ifo indicator. The headline figure missed the bar, coming in at 87.3 vs 88 expected and down from 88.6 in June. Things got particularly worse in the assessment of the current situation (93.7 to 91.3) by manufacturing, services and construction. The outlook was little changed, from 83.8 to 83.5 but with sectoral differences (worse in manufacturing, trade and construction but less pessimistic in services). German Bunds very briefly jumped higher in a Pavlov-reaction but soon pared those gains. Daily net changes vary between +1.4 to 2.3 bps across the curve. US yields slightly underperform, adding 2.1-3.2 bps with sharper than expected house price rises helping the move higher. FX markets trade muted ahead of key events including the Fed and ECB later this week. An (unconvincing) attempt by EUR/USD to recoup some of yesterday’s losses failed. The pair instead turned further south to test 1.1033 support zone. DXY ekes out a small gain to 101.58. EUR/GBP is testing 0.86 support after stronger-than-expected UK data (see below). The yuan is profiting from the measures announced by China to stimulate the economy/property sector. Australia and its Aussie dollar as a main trading partner got caught in the slipstream. A strong Asian equity performance barely filtered through in western dealings. The EuroStoxx50 trades flat, Wall Street adds no more than 0.3% (Nasdaq).

News & Views

Data published today by the Confederation of British industry painted a more benign/mixed picture compared to yesterday’s UK July PMI release. According to the quarterly trends survey, business optimism in July improved further from -2 in April to 6 reaching the highest level in two years. At the same time CBI warned on worrying signs that a margin squeeze and higher financing costs are hurting investment plans. The quarterly subseries on plant investment over the next twelve months declined from 14 to -1. In the monthly survey, orders also improved from -15 to -9, the best reading this year and above the long run average of -13. Both volume of output over the past 3 months (3 from -6) and expected output over the next three months (9 from 4) also improved. Expectations on average selling prices over the next three months eased slightly further from 19 to 18, but remain elevated.

According to the monthly business survey of the National Bank of Belgium, business sentiment in July deteriorated for the fourth consecutive month. The overall synthetic curve declined from -12.1 in June to -14.8 in July. The building sector was the only sector escaping the deterioration, more or less stabilizing at -5.8 (from -6.0). In business-related services, general market demand expectations have been sharply revised downwards for the second month in a row. Business leaders, turned extremely pessimistic on activity expectations last month and did not revise their assessment this month. They remain very wary, expressing an even more unfavourable view of their current activity levels. In the trade sector, the decline in the indicator is attributable to a marked downward revision of demand expectations and, to a lesser extent, employment expectations. In the manufacturing industry, all underlying components of the indicator are down, with the exception of the assessment of stock levels. The loss of confidence has particularly impacted employment expectations and demand expectations. The industry capacity utilization declined to 75.3 in July, compared to 77.7 in April.

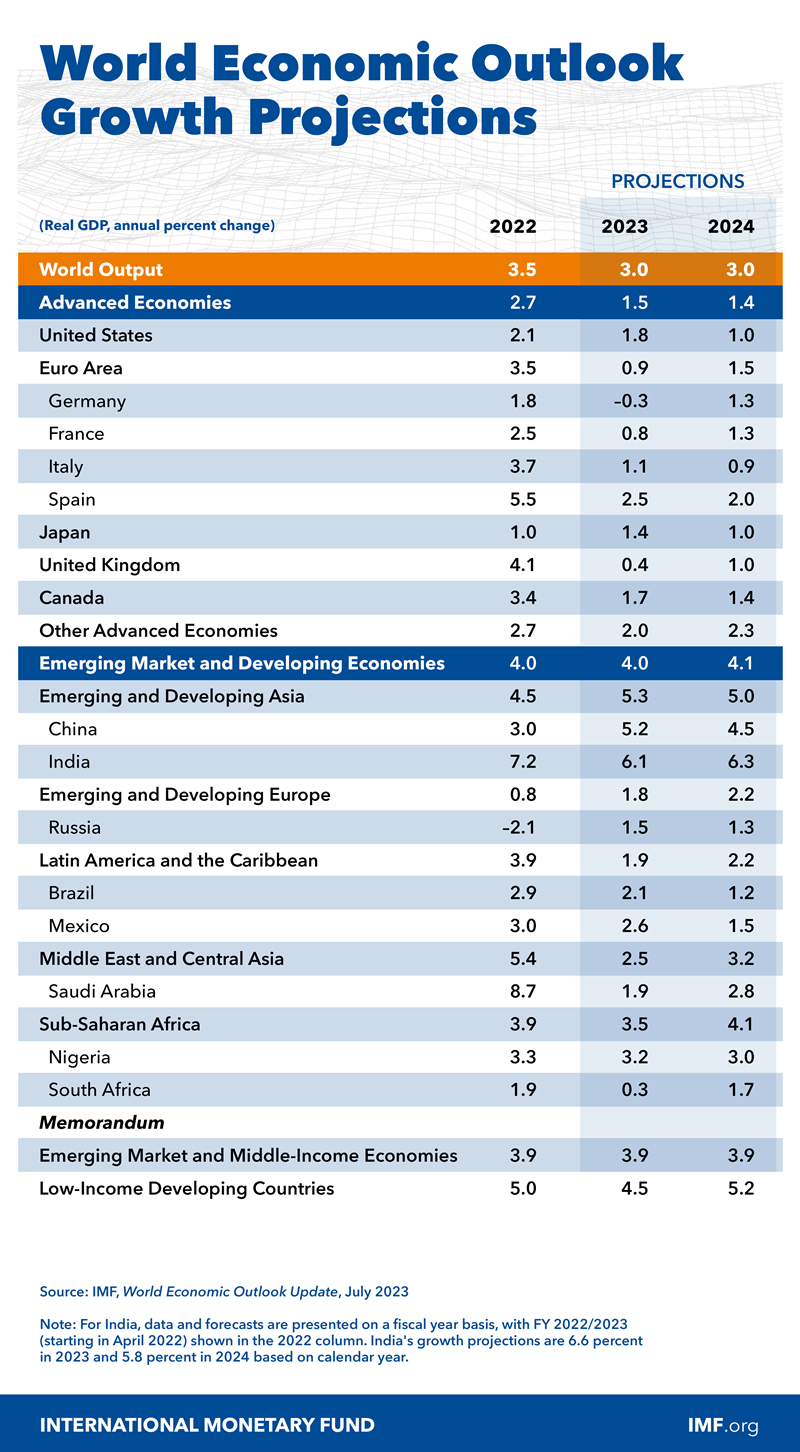

IMF raises global growth forecast for 2023, cautions on central bank rates

In the World Economic Outlook Update, IMF raised its forecast for global GDP growth in 2023 by 0.2% to 3.0%, while leaving the 2024 projection steady at 3.0%.

The IMF increased 2023 growth estimate for the United States by 0.2% to 1.8%, but pared back 2024 forecast by -0.1% to 1.0%. Eurozone growth forecasts received a slight boost of 0.1% for both 2023 and 2024, bringing them to 0.9% and 1.5% respectively.

On the inflation front, global headline inflation is expected to decline from 8.7% in 2022 to 6.8% in 2023, and further to 5.2% in 2024.

The IMF statement noted that although the 2023 forecast is marginally higher than what was predicted in the April 2023 World Economic Outlook. it still remains "weak by historical standards."

Furthermore, the IMF drew attention to the impact of rising central bank policy rates used to combat inflation, stating, "The rise in central bank policy rates to fight inflation continues to weigh on economic activity."

It also emphasized that most economies should prioritize achieving sustained disinflation while ensuring financial stability. Therefore, the IMF urged central banks to "remain focused on restoring price stability and strengthen financial supervision and risk monitoring."

Markets Steady Ahead of Fed and ECB, China Stimulus Promise, Unilever Rallies after Results

It's been another relatively flat session for equity markets, with investors seemingly having one eye on the Fed and ECB later in the week despite a strong showing in Chinese stocks earlier in the day.

They were lifted by the promise of Chinese stimulus following the Politburo meeting this week and some potential relief for the property market. It's been a tougher re-emergence from zero-Covid than many anticipated, with consumers still seemingly holding back and the property sector still reeling from the previous crackdown.

The enthusiasm hasn't filtered through to Europe and the US though, perhaps due to the lack of detail currently on the stimulus measures, but also the distraction of the central bank meetings over the next 48 hours. Progress on inflation could mean both the Fed and ECB are about to announce their final rate hikes of the tightening cycle; the question is will they acknowledge that or maintain a hawkish position over the rest of the summer?

Unilever rallies amid hints at price pressures easing

Unilever is among the top performers on the FTSE 100 today, buoyed by a surge in profits in the last quarter. It comes at a challenging time when high inflation is pushing up costs and there is a growing spotlight on producers and supermarkets amid claims of profiteering.

What's more, the cost-of-living crisis is pushing consumers toward cheaper own-brand products which partly contributed to a decline in sales volumes. The company did reassure investors that pressures are easing though which should be good news for households and the share price is also reaping the rewards, up around 5%.

Chinese stimulus hints do little to boost Oil prices further

Oil prices barely changed on Tuesday, after appearing to have been little impacted by the promise of new Chinese stimulus. This further supports the view that the lack of detail is stalling any reaction in the markets and that only once we get that can we determine how effective it will be in stimulating demand.

We've already seen some powerful gains over the last four weeks, with Brent up almost 15% from its late June lows. That was driven by cuts from Saudi Arabia and Russia and then better economic readings elsewhere that supported the case for a soft landing following a very aggressive monetary tightening cycle.

Gold pares gains as traders await Fed position on further rate hikes

Gold is hovering around $1,960 ahead of the Fed decision, having pared recent gains over the last four sessions. It came close to $2,000 but traders appear to have opted to hold off considering how influential the central bank could be in the next big move in the yellow metal.

Another 25 basis point rate hike is basically fully priced in at this stage, it's now a question of whether they will signal more to come or adopt a less hawkish position. The dot plot last month indicated two more rate hikes were likely, with one policymaker favouring four, but recent data may have changed that. They won't close the door entirely on tightening further but they could hint at being done for now.

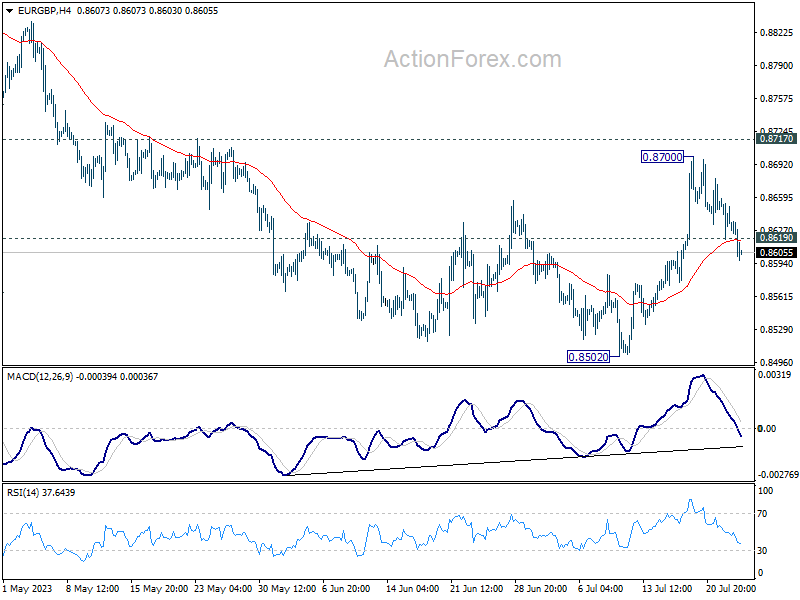

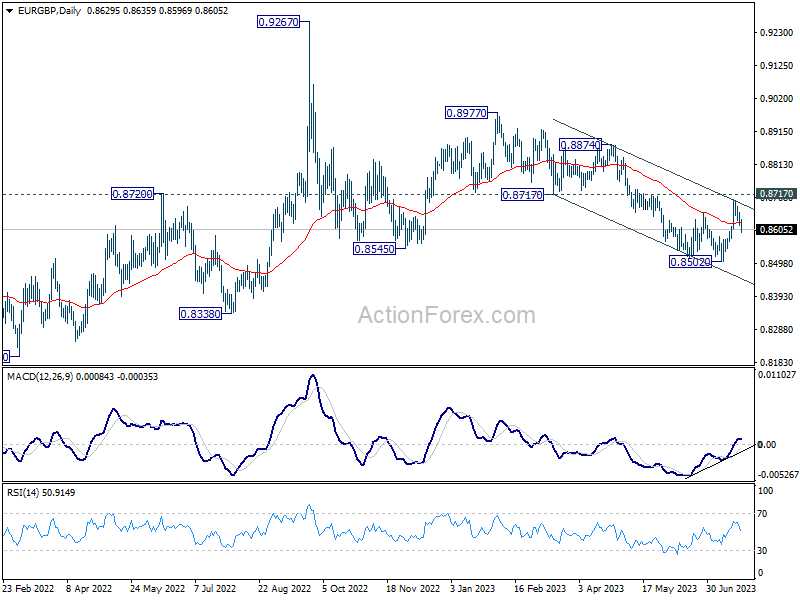

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8612; (P) 0.8636; (R1) 0.8653; More...

EUR/GBP's break of 0.8619 minor support argues that rebound from 0.8502 has completed at 0.8700, ahead of 0.8717 support turned resistance. Intraday bias is back on the downside for retesting 0.8502 low. Firm break there will resume larger decline form 0.8977. Nevertheless, break of 0.8700 will revive near term bullishness for another take on 0.8717.

In the bigger picture, the down trend from 0.9267 (2022 high) is seen as part of the long term range pattern from 0.9499 (2020 high). Firm break of 0.8717 support turned resistance will argue that it has completed with three waves down to 0.8502. Further break of 0.8977 will bring retest of 0.9267 high. Nevertheless, rejection by 0.8717, followed by break of 0.8502 will resume the decline towards 0.8201 (2022 low).

Euro Trades Lower on Disappointing German Ifo Data

Euro falls broadly today following release of weaker than expected German Ifo business climate data, although losses remain somewhat contained for the moment. It appears traders are holding their bets in anticipation of the upcoming FOMC and ECB rate decisions. Further, with July drawing to a close and the markets in a characteristic summer lull, significant movements are somewhat restrained.

Australian Dollar holds onto its position as the strongest performer of the day, bolstered by earlier gains and closely trailed by New Zealand dollar. Swiss Franc claims the third spot, given a boost by the weakening Euro. On the other end of the spectrum, Canadian dollar follows the common currency as the next weakest, while Dollar trails behind. Japanese Yen presents a mixed picture, with traders also keenly awaiting BoJ's decision due on Friday.

All eyes in the forex market will be on EUR/USD in the coming days. From a technical perspective, the pair could have peaked at 1.1274, after reaching the 61.8% retracement of 1.2348 (2021 high) to 0.9534 (2022 low) at 1.1273. However, decisive break through 1.1011 resistance-turned-support level would be needed for confirmation. Should this occur, deeper decline could be seen to 1.0634 support level before a rebound sets up the medium-term range.

In Europe, at the time of writing, FTSE is up 0.16%. DAX is up 0.05%. CAC is up 0.07%. Germany 10-year yield is up 0.0177 at 2.444. Earlier in Asia, Nikkei dropped -0.06%. Hong Kong HSI rose 4.10%. China Shanghai SSE rose 2.13%. Singapore Strait Times rose 0.64%. Japan 10-year JGB yield rose 0.0159 to 0.467.

Germany's Ifo business climate fell to 87.3, economy turning bleaker

Germany's Ifo Business Climate Index has fallen for the third consecutive month in July, from 88.6 to 87.3, slightly missing expectation of of 88.0. Both the Current Assessment Index and Expectations Index noted a drop, signaling a potential slowdown in Europe's largest economy.

Current Assessment Index, which measures the present business conditions, dropped from 93.7 to 91.3, falling short of the expected 93.0. Meanwhile, Expectations Index, which gauges future business prospects, slipped from 83.8 to 83.5, although it managed to outperform the expectation of 83.0.

Ifo, the institute that conducts the survey, delivered a grim prognosis for the German economy. "The situation in the German economy is turning bleaker," they said in their statement.

A breakdown by sectors shows a similar trend, with all reporting lower figures. Manufacturing took a hit, dropping from -9.7 to -14.2. Services sector also posted a decline, falling from 2.7 to 0.9. Trade sector suffered a fall from -20.2 to -23.7, and construction, too, saw a downturn, from -20.5 to -24.0.

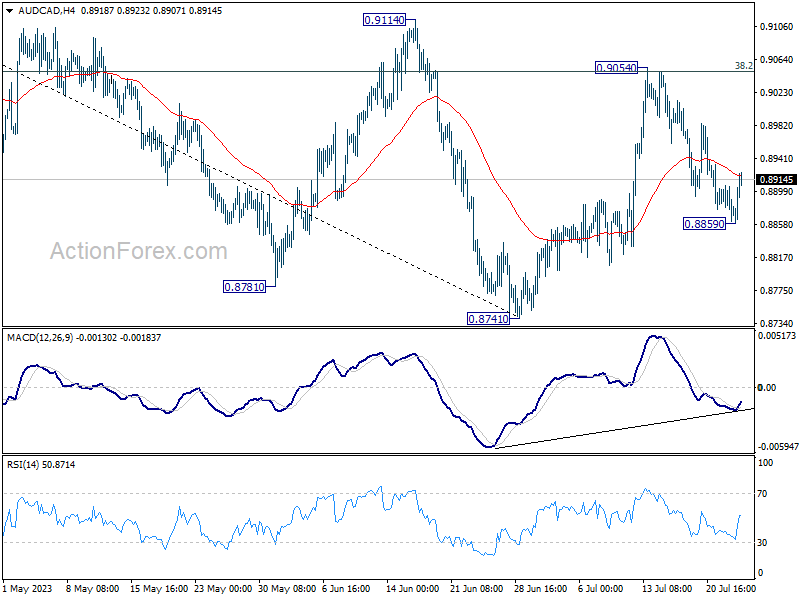

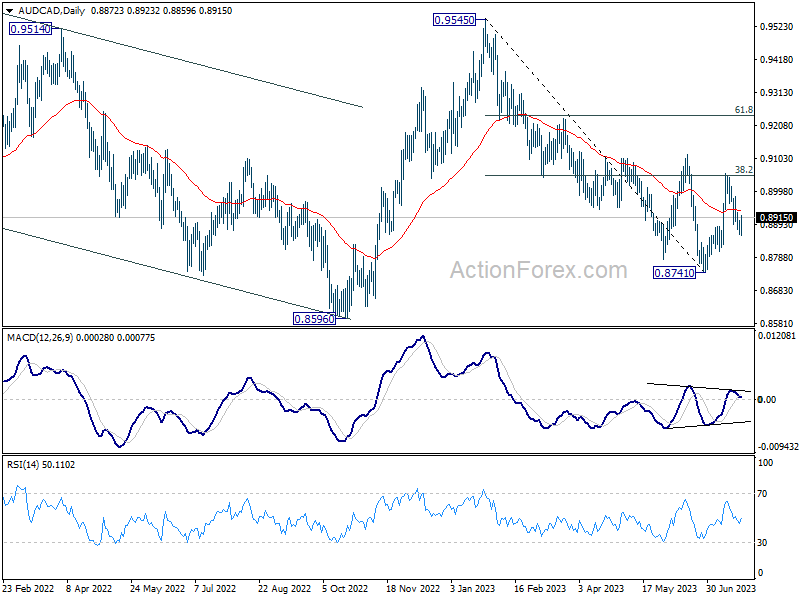

AUD/CAD recovering, head and shoulder in the making?

AUD/CAD is one of the top movers today, riding on Aussie's broad based recovery. Immediate focus is on 55 4H EMA (now at 0.8191). Sustained trading above there will indicate that the pull back from 0.9054 has completed at 0.8859, and bring stronger rise back to 0.9054 resistance.

While it's still a bit early, it's worth to point out that AUD/CAD could be forming a head and shoulder bottom pattern (ls: 0.8781; h: 0.8741; rs: 0.8859). Decisive break of 0.9054 cluster resistance (38.2% retracement of 0.9545 to 0.8741 at 0.9048) will be a strong signal of bullish reversal. That would set the stage for further rise to 61.8% retracement at 0.9238 next.

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8612; (P) 0.8636; (R1) 0.8653; More...

EUR/GBP's break of 0.8619 minor support argues that rebound from 0.8502 has completed at 0.8700, ahead of 0.8717 support turned resistance. Intraday bias is back on the downside for retesting 0.8502 low. Firm break there will resume larger decline form 0.8977. Nevertheless, break of 0.8700 will revive near term bullishness for another take on 0.8717.

In the bigger picture, the down trend from 0.9267 (2022 high) is seen as part of the long term range pattern from 0.9499 (2020 high). Firm break of 0.8717 support turned resistance will argue that it has completed with three waves down to 0.8502. Further break of 0.8977 will bring retest of 0.9267 high. Nevertheless, rejection by 0.8717, followed by break of 0.8502 will resume the decline towards 0.8201 (2022 low).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 08:00 | EUR | Germany IFO Business Climate Jul | 87.3 | 88 | 88.5 | 88.6 |

| 08:00 | EUR | Germany IFO Current Assessment Jul | 91.3 | 93 | 93.7 | |

| 08:00 | EUR | Germany IFO Expectations Jul | 83.5 | 83 | 83.6 | 83.8 |

| 13:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y May | -1.70% | -1.40% | -1.70% | |

| 13:00 | USD | Housing Price Index M/M May | 0.70% | 0.60% | 0.70% | |

| 14:00 | USD | Consumer Confidence Jul | 112.1 | 109.7 | ||

| 14:00 | USD | Richmond Fed Manufacturing Index Jul | -10 | -7 |

AUD/CAD recovering, head and shoulder in the making?

AUD/CAD is one of the top movers today, riding on Aussie's broad based recovery. Immediate focus is on 55 4H EMA (now at 0.8191). Sustained trading above there will indicate that the pull back from 0.9054 has completed at 0.8859, and bring stronger rise back to 0.9054 resistance.

While it's still a bit early, it's worth to point out that AUD/CAD could be forming a head and shoulder bottom pattern (ls: 0.8781; h: 0.8741; rs: 0.8859). Decisive break of 0.9054 cluster resistance (38.2% retracement of 0.9545 to 0.8741 at 0.9048) will be a strong signal of bullish reversal. That would set the stage for further rise to 61.8% retracement at 0.9238 next.