Sample Category Title

June CPI: More Convincing Progress Underway

Summary

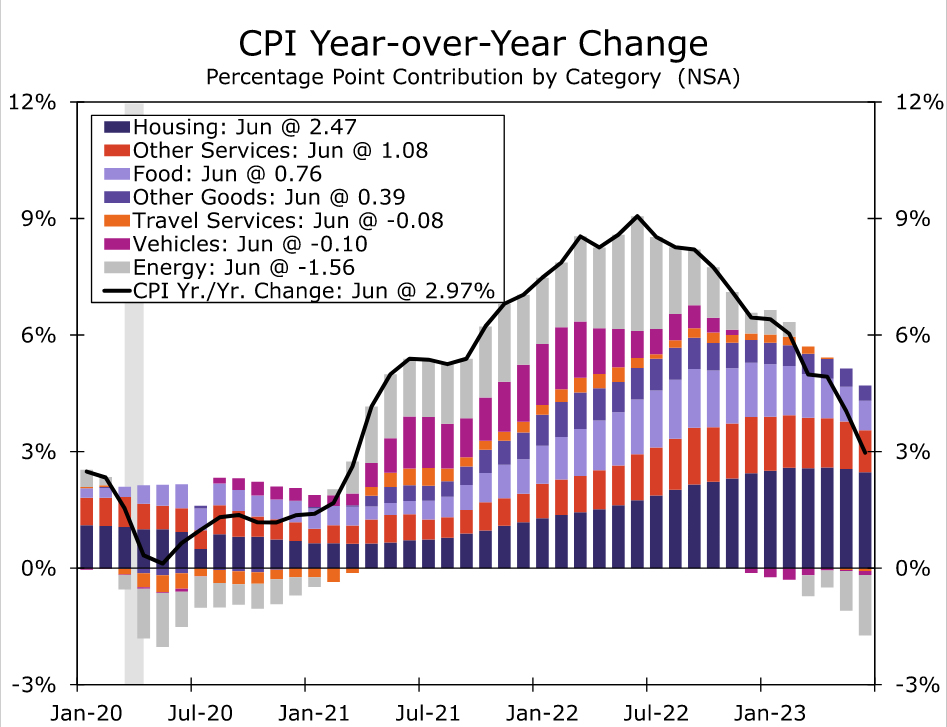

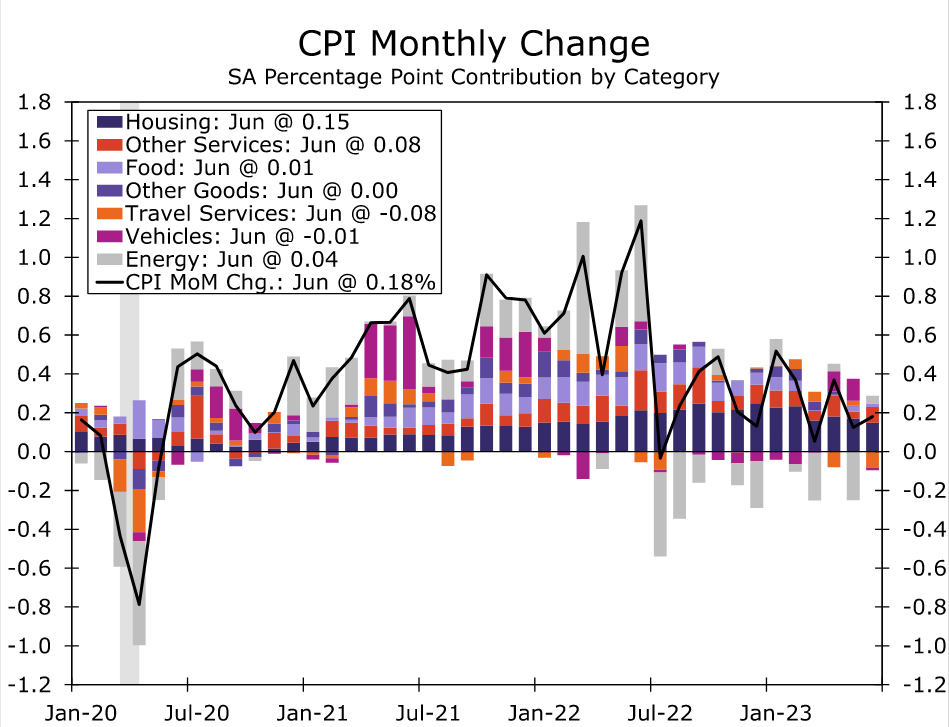

Today's report on the Consumer Price Index for June brought good news. Headline consumer price inflation increased 0.2% over the month and 3.0% over the past year. For the latter, this was the lowest reading since March 2021. Excluding food and energy prices, the core CPI increased 0.2% (rounded up from 0.16%) over the month, the smallest monthly increase in core inflation since February 2021. A big decline in prices for travel services such as airfares and lodging-away-from-home contributed to the deceleration in core prices, as did the ongoing slowdown in primary shelter inflation. Used vehicle prices declined 0.5%, new vehicle prices rounded flat, and goods prices excluding vehicles fell 0.1%.

In the near term, we expect the more moderate pace of price growth signaled by the June CPI to continue. While the sharp drop in travel prices will be hard to repeat, the decline in vehicle prices has more room to run, and the ongoing disinflation in primary shelter should continue into the second half of this year. More broadly, the expanding supply side of the economy and slowing demand growth are helping to slow inflation from the blistering rates seen in 2021 and 2022. That said, core CPI inflation is still up 4.8% over the past year and 4.1% annualized over the past three months. The FOMC will need to see several more inflation prints like today's before it declares its mission accomplished.

We expect core inflation in the second half of the year to run about 3% on an annualized basis. This expected improvement relative to the 4.6% pace of core inflation in the first half of this year will likely be enough to where the FOMC believes it can sit and wait for the effects of prior tightening to work through the economy after one additional 25 bps hike at its next meeting on July 26. However, with the underlying trend in inflation likely to be stuck closer to 3% than 2%, rate cuts remain a long way off, in our view.

CPI Inflation Drops to Lowest Reading since March 2021

The Consumer Price Index (CPI) rose 0.2% in June, a tenth slower than the consensus expectation among forecasters. Consumer price inflation over the past year fell to 3.0%, the lowest reading since March 2021 and well below the peak of 9.1% in June 2022. Some of the inflation slowdown over the past year has been driven by base effects, particularly for energy prices. One year ago, prices for oil and natural gas were much higher due in large part to a surge in prices that followed Russia's invasion of Ukraine. But even setting this aside, there are clear signs that inflation continues to slow steadily.

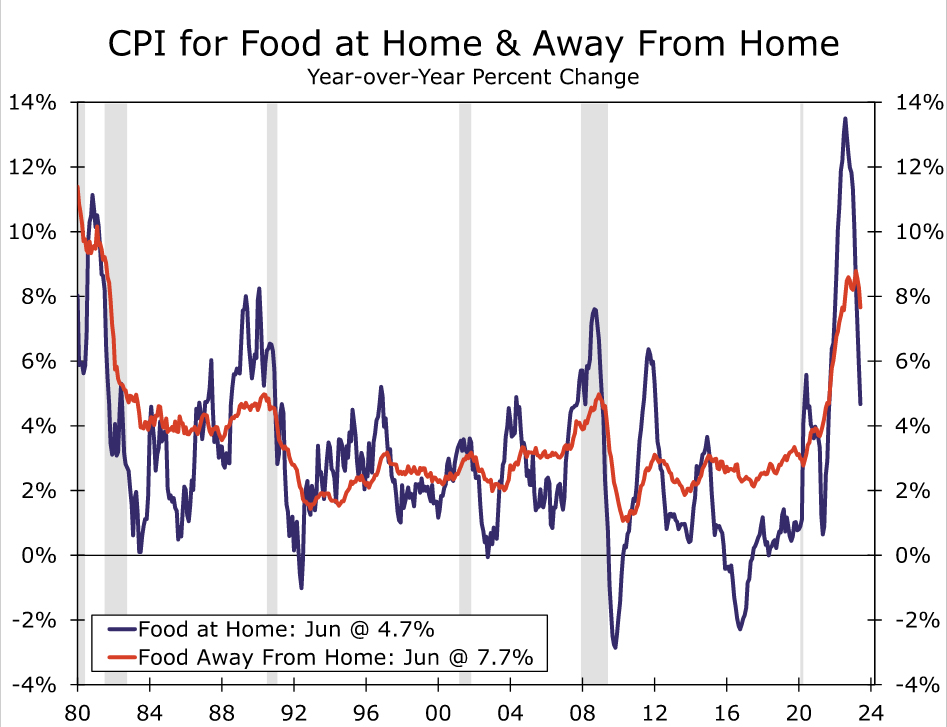

Compared to one month ago, energy prices increased 0.6%, led by gasoline (+1.0%) and electricity (+0.9%). Prices for natural gas utilities continued to come back down to Earth, falling 1.7% in June and 19% over the past year. Food prices increased a modest 0.1% in June compared to May. Grocery store inflation, which rose more sharply last year compared to prices for food consumed away from home, has also dropped off more quickly on the way down. Food at home prices are up "only" 4.7% over the past year. While still high, this is the slowest pace of food inflation in nearly two years.

Excluding food and energy, price growth also came in a touch softer than expected. The core CPI rose 0.2% in June, the smallest monthly increase since February 2021. The more benign print was helped along by goods prices resuming their retreat, dropping 0.1%. After back-to-back gains of over 4%, used vehicle prices fell 0.5%, with further declines expected to be on June's heels as auction prices have tumbled. New vehicle prices edged down ever so slightly (-0.03%), while recreational and household goods also declined in a sign pandemic spending patterns are slowly reverting and supply snarls continue to abate.

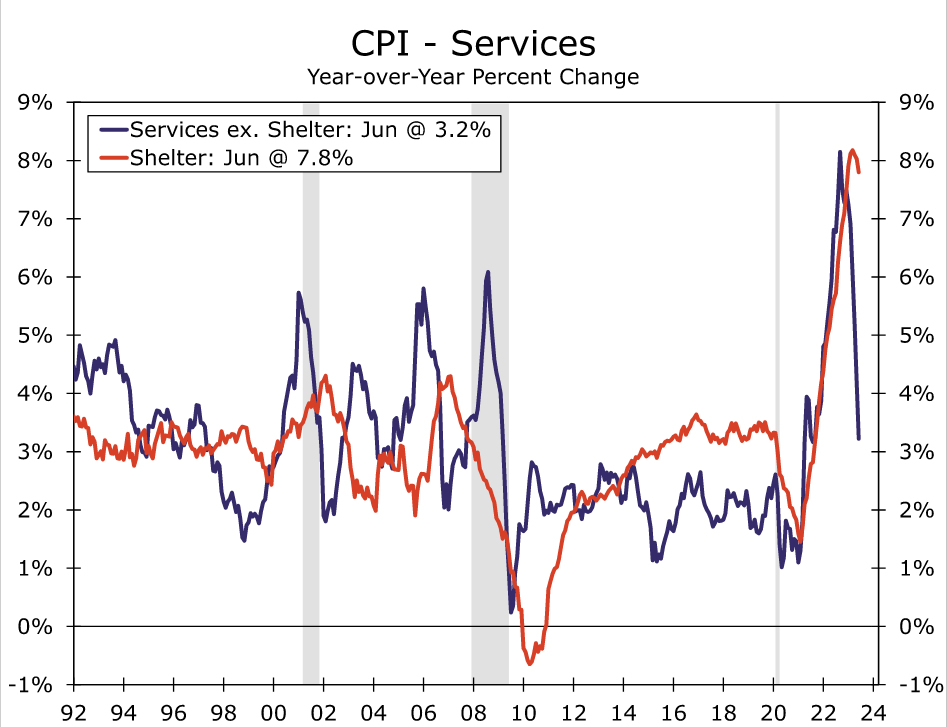

Core services inflation also pointed to activity normalizing after a wild few years. Prices for travel-related services tumbled 3.8% with notable declines in both airfare (-8.1%) and hotel prices (-2.0%). Gains in primary rent and owners' equivalent rent also decelerated amid a cooler housing market this past year. Yet, prices for remaining "other" services, which include medical care, insurance, recreation and personal care among other things, continue to advance at a solid rate, up 0.3% in June and 3.8% annualized over the past three months.

One More Hike in July, Then Done

Today's softer-than-expected print with signs of pandemic-era distortions fading provides additional evidence that disinflation is occurring in real-time. Looking ahead, we expect the more moderate pace of price growth signaled by the June CPI to continue. The decline in vehicle prices has more room to run, and the ongoing disinflation in primary shelter should continue in the second half of this year. Goods inflation beyond vehicles also has scope to slow, with supply chain pressures unwinding and the cost of input goods down over the past year. More generally, the increasing financial squeeze on consumers as pandemic savings run dry and borrowing costs rise is making consumers more discerning and less willing price-takers when compared to the past two years.

However, a timely and sustained return to the FOMC's 2% inflation target remains far from assured. Wages may no longer be accelerating, but the tight jobs market is keeping labor costs growing in excess of the range that is consistent with 2% inflation over time. Prices for food and energy commodities have been largely stable since the start of the year, and the deflationary impulse from these categories should fade in the months ahead. While headline inflation has tumbled from its 42-year high a year ago, we expect the next leg of disinflation to be slower going. Even within the core CPI where the disinflation forces in housing and vehicles will be more pronounced, we expect core inflation in the second half of the year to run a bit north of 3% on an annualized basis. The improvement relative to the 4.6% pace of core inflation in the first half of this year will likely be enough to where the FOMC believes it can sit and wait for the effects of prior tightening to work through the economy after one additional 25 bps hike at its next meeting on July 26. However, with the underlying trend in inflation likely to be stuck closer to 3% than 2%, rate cuts remain a long way off in our view.

As Good a US Inflation Report as We Could Have Realistically Hoped for

Financial markets are buzzing at the US open on Wednesday, with investors buoyed by a very promising inflation report from the US.

The report not only beat at the headline level but core actually slipped even further, dropping to 4.8% for the first time since October 2021. The monthly data was also extremely encouraging, with headline and core falling to 0.2% which was lower than the consensus forecast in both cases. It really is just what the doctor ordered.

Of course, there's been plenty of setbacks over the last couple of years so we don't want to get too carried away with one inflation report but it really is about as good as we could have realistically hoped for.

That said, it's unlikely to change the outcome of the debate that takes place in two weeks. The Fed is still extremely likely to hike by 25 basis points, rightly or wrongly, as the labor market data on Friday simply wasn't good enough. In fact, the wages component was quite the opposite and will likely convince the FOMC that one more hike is warranted, which is what markets are still heavily pricing in.

But that may well now be the last and if we can see any further signs of progress over the summer then that will likely end the debate altogether, shifting the conversation from how many more hikes to the timing of the first cut.

Brent Crude trying to break $80 after US inflation report

Oil prices have been understandably lifted by the release which makes sense. Anything that could enable a soft landing in the US is good for oil prices. Brent was already trending higher though and is now at its highest point since April, having already broken out of the range it traded within for the last couple of months.

The next level for Brent to overcome is $80, which would be a big psychological leap. That may also see WTI break above its June high following the spike on the 5th. The move higher also suggests the latest efforts of Saudi Arabia and Russia are working in tightening the markets and boosting prices after multiple failed efforts.

Gold gets a welcome boost but can it be sustained?

The US inflation data gave gold just the boost it needed to break back above $1,940 after failing to pierce that level in recent days. The yellow metal has been range-bound in recent weeks between $1,900 and $1,940 and today's report did what the jobs data failed to do; it provided the catalyst for a breakout.

There remains plenty of resistance ahead for gold and today's move doesn't necessarily suggest the correction we've seen since May is over but it's a massive step in the right direction. If the inflation data continues to improve then that could be bullish for gold. The next tests for gold are $1,940, $1,960 and $2,000, which roughly represent the 38.2%, 50% and 61.8% Fibonacci retracement levels from the May high to the June lows.

Is lower inflation good for crypto?

There's been a lot of volatility in bitcoin in the aftermath of the US inflation release but in terms of sustained direction, not much appears to have changed. At the time of writing, it's basically trading back where it started, although the price remains extremely choppy so that may not be the case an hour from now, let alone by the end of the day. Traders, as it stands, seemingly can't make up their mind if it's good or bad for crypto.

Sunset Market Commentary

Markets

Today was one stretched countdown to the US inflation numbers without a lot of market fireworks in the run-up to it. Prices at the other side of the Atlantic generally came in slightly below expectations. Both headline and core inflation rose 0.2% m/m, missing a 0.3% analyst estimate. Yearly price pressures eased from 4% to 3% in the headline gauge and from 5.3% to 4.8% in the core. The bar was set at 3.1% and 5% respectively. It’s the slowest pace in about two years. Base effects had their maximum downward impact as CPI in June last year hit its four-decade high on a 1.2% m/m surge. Core inflation back then also shot up an unusual 0.6% m/m but only hit its peak in September 2022, also on a 0.6% m/m pace. This means we still might see some strong statistical downward pressure in the core number later this year. Specifically this month, though, used cars (-0.5% m/m) and airline fares (-8.1%) weighed the figure down. Shelter prices rose a solid 0.4%, explaining about 70% of the monthly June increase. Energy prices picked up again (0.6%) after declining in May, led by gasoline and electricity. Goods inflation fell 0.1% m/m but service inflation still rose 0.3%. For Richmond Fed president Barkin today’s inflation is still too high. He warned for backing off too soon and added that he is comfortable to do more if inflation doesn’t get to the 2% goal. Barkin, however, does not vote on monetary policy this year.

US rates and the dollar since the payrolls last Friday corrected lower, even as economic data earlier last week surprised to the upside. It tells you something about the market’s mindset going into today’s CPI release. The reaction as such was textbook. Core bonds jumped with US Treasuries outperforming vs Bunds. Yields at the 2-5 year bucket drop 10.7-11.6 bps. The 2 year yield eases further south of the symbolic 5% barrier. Longer maturities including 10 and 30 year slip 5.9 and 0.3 bps respectively with the former testing support at the 3.90-3.92% zone. German yields follow US peers by shedding 1-5.9 bps with the front end outperforming. First important support zones are not (yet?) being tested though (3.17% for the 2 y yield, 2.57% for the 10 y yield). Equities cheered at the data, presuming it relieves the Fed somewhat. The EuroStoxx50 extends gains to 1.4%, Wall Street opens with gains between 0.7-1.2%. Oil turns positive for the day with a barrel of Brent touching $80 for the first time since May. The dollar slid. EUR/USD jumped to the highest level since early May. At 1.1084 the pair is ever closer towards the YtD high of 1.1095. It even came to a test. DXY (100.95) in a mirror move dropped towards the YtD lows of 100.78. The yen takes advantage and pushes through to USD/JPY 139.24.

News & Views

The Bank of England published its bi-annual Financial Stability Review. The UK economy has so far been resilient to interest rate risk, though it will take time for the full impact of higher interest rates to come through. More households are being affected by higher interest rates as fixed-rate mortgage deals expire. The proportion of households with high debt service ratios, after accounting for the higher cost of living, has increased and is expected to continue to do so through 2023. The corporate sector is expected to remain broadly resilient to higher interest rates and weak growth. The UK banking system is well capitalized and maintains large liquidity buffers. Asset quality overall remains relatively strong, with higher interest rates having had a limited impact on credit risk so far.

Reserve Bank of Australia governor Lowe this morning announced that the rate-setting board will move to 8 meetings a year from 11 now beginning in 2024. The former is the pace followed by most major central banks: “The less frequent and longer meetings will provide more time for the board to examine issues in detail and to have deeper discussions on monetary policy strategy, alternative policy options and risks, as well as on communication.” The RBA meets next on August 1 and conduct a full review of its central forecasts and risks. Lowe, who’s term ends mid-September but could still be reappointed, said that consumption growth is weak largely because of what is going on with monetary policy. The RBA is confident that they’re doing is working. The question is how much more they need to do and the RBA has a completely open mind on that. Australian money markets discount a policy rate peak around 4.5% from 4.1% currently. The Aussie dollar gains today against an overall weak US dollar with AUD/USD (0.6735), taking out short term resistance around 0.67.

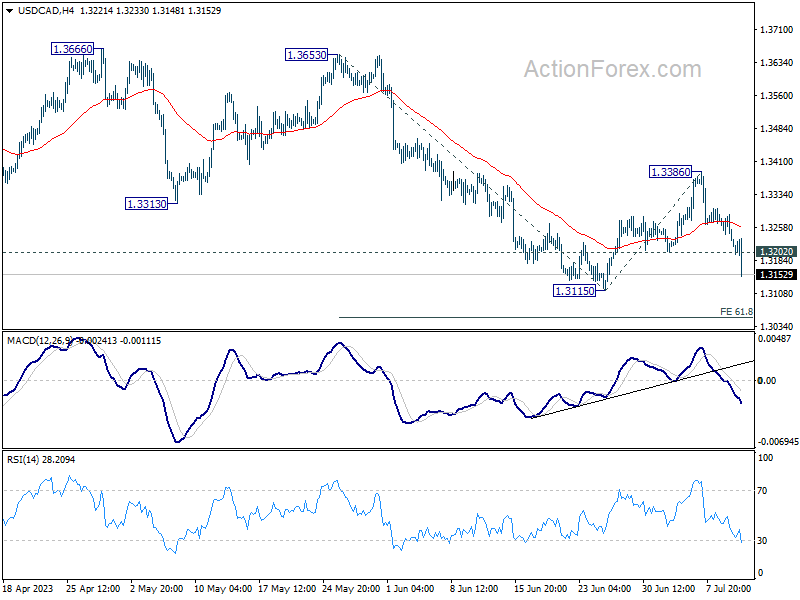

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3209; (P) 1.3253; (R1) 1.3274; More....

USD/CAD's strong break of 1.3202 support confirms completion of rebound from 1.3115 at 1.3385. Rejection by 55 D EMA also maintains near term bearishness. Intraday bias is back on the downside for retesting 1.3115 first. Break there will resume larger down trend to 61.8% projection of 1.3653 to 1.3115 from 1.3386 at 1.3054, and then 100% projection at 1.2848. For now, outlook will remain bearish as long as 1.3386 resistance holds, in case of recovery.

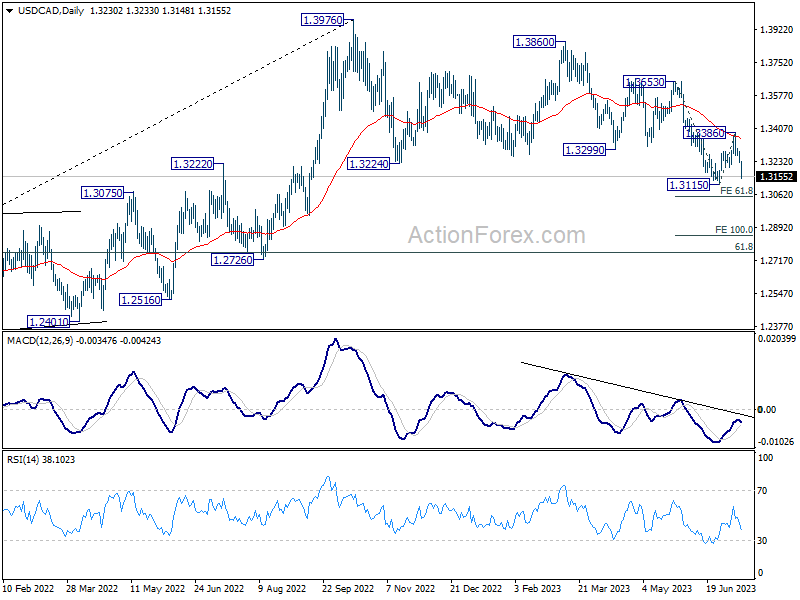

In the bigger picture, price actions from 1.3976 are viewed as a correction to up trend from 1.2005 (2021 low) only. Hence, the up trend is in favor to resume through 1.3976 at a later stage. Nevertheless, another fall below 1.3115 will extending the decline from 1.3976 to 61.8% retracement of 1.2005 to 1.3976 at 1.2758, and raise the chance of bearish trend reversal.

BoC hikes 25bps, raises 2023 GDP and CPI forecasts

BoC raises overnight rate by 25bps to 5.00% as widely expected. Correspondingly, the Bank Rate and deposit rate are increased to 5.25% and 5.00% respectively. In the new economic projections, both GDP and CPI forecasts for 2023 are upgraded.

Nevertheless, the central bank didn't explicitly state a tightening bias in the statement. But the Governing Council will "continue to assess the dynamics of core inflation and the outlook for CPI inflation", and " remains resolute in its commitment to restoring price stability".

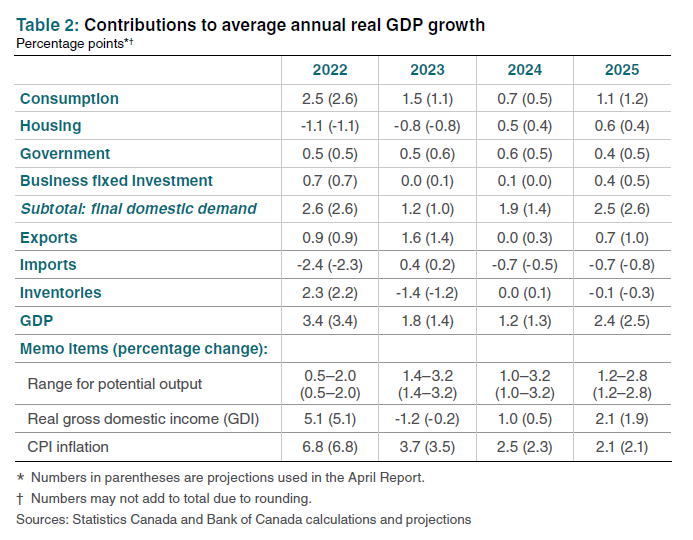

BoC said that "Canada's economy has been stronger than expected, with more momentum in demand". In the new economic projections, GDP is forecast to grow 1.8% in 2023 (raised from 1.4%), 1.2% in 2024 (lowered form 1.3%0, and then 2.4% in 2025 (lowered from 2.5%).

CPI is projected to have a "slower return to target than was forecast in the January and April projections". CPI is projected to slow to 3.7% in 2023 (raised from 3.5%), then 2.5% in 2024 (raised from 2.3%), and then 2.1% in 2025 (unchanged).

(BOC) Bank of Canada raises policy rate 25 basis points, continues quantitative tightening

The Bank of Canada today increased its target for the overnight rate to 5%, with the Bank Rate at 5¼% and the deposit rate at 5%. The Bank is also continuing its policy of quantitative tightening.

Global inflation is easing, with lower energy prices and a decline in goods price inflation. However, robust demand and tight labour markets are causing persistent inflationary pressures in services. Economic growth has been stronger than expected, especially in the United States, where consumer and business spending has been surprisingly resilient. After a surge in early 2023, China's economic growth is softening, with slowing exports and ongoing weakness in its property sector. Growth in the euro area is effectively stalled: while the service sector continues to grow, manufacturing is contracting. Global financial conditions have tightened, with bond yields up in North America and Europe as major central banks signal further interest rate increases may be needed to combat inflation.

The Bank's July Monetary Policy Report (MPR) projects the global economy will grow by around 2.8% this year and 2.4% in 2024, followed by 2.7% growth in 2025.

Canada's economy has been stronger than expected, with more momentum in demand. Consumption growth has been surprisingly strong at 5.8% in the first quarter. While the Bank expects consumer spending to slow in response to the cumulative increase in interest rates, recent retail trade and other data suggest more persistent excess demand in the economy. In addition, the housing market has seen some pickup. New construction and real estate listings are lagging demand, which is adding pressure to prices. In the labour market, there are signs of more availability of workers, but conditions remain tight, and wage growth has been around 4-5%. Strong population growth from immigration is adding both demand and supply to the economy: newcomers are helping to ease the shortage of workers while also boosting consumer spending and adding to demand for housing.

As higher interest rates continue to work their way through the economy, the Bank expects economic growth to slow, averaging around 1% through the second half of this year and the first half of next year. This implies real GDP growth of 1.8% in 2023 and 1.2% in 2024. The economy will move into modest excess supply early next year before growth picks up to 2.4% in 2025.

Inflation in Canada eased to 3.4% in May, a substantial and welcome drop from its peak of 8.1% last summer. While CPI inflation has come down largely as expected so far this year, the downward momentum has come more from lower energy prices, and less from easing underlying inflation. With the large price increases of last year out of the annual data, there will be less near-term downward momentum in CPI inflation. Moreover, with three-month rates of core inflation running around 3½-4% since last September, underlying price pressures appear to be more persistent than anticipated. This is reinforced by the Bank's business surveys, which find businesses are still increasing their prices more frequently than normal.

In the July MPR projection, CPI inflation is forecast to hover around 3% for the next year before gradually declining to 2% in the middle of 2025. This is a slower return to target than was forecast in the January and April projections. Governing Council remains concerned that progress towards the 2% target could stall, jeopardizing the return to price stability.

In light of the accumulation of evidence that excess demand and elevated core inflation are both proving more persistent, and taking into account its revised outlook for economic activity and inflation, Governing Council decided to increase the policy interest rate to 5%. Quantitative tightening is complementing the restrictive stance of monetary policy and normalizing the Bank's balance sheet. Governing Council will continue to assess the dynamics of core inflation and the outlook for CPI inflation. In particular, we will be evaluating whether the evolution of excess demand, inflation expectations, wage growth and corporate pricing behaviour are consistent with achieving the 2% inflation target. The Bank remains resolute in its commitment to restoring price stability for Canadians.

Information note

The next scheduled date for announcing the overnight rate target is September 6, 2023. The Bank will publish its next full outlook for the economy and inflation, including risks to the projection, in the Monetary Policy Report on October 25, 2023.

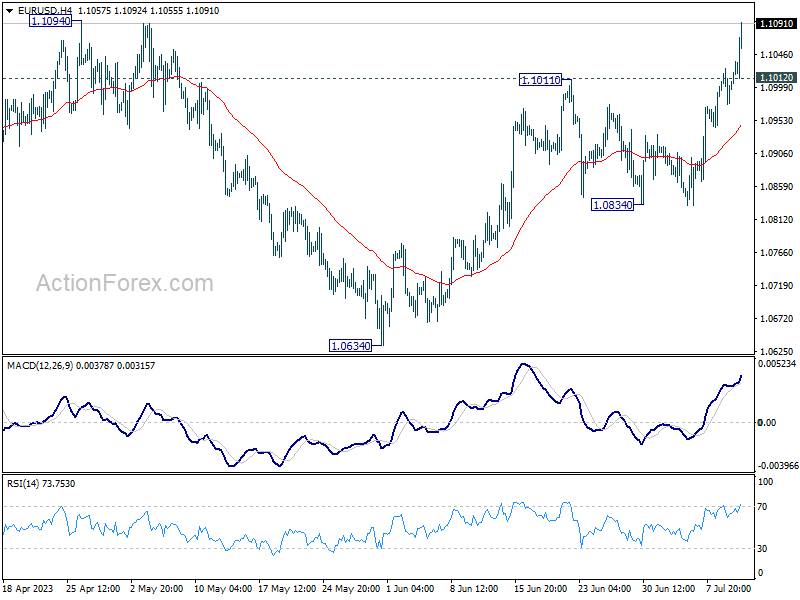

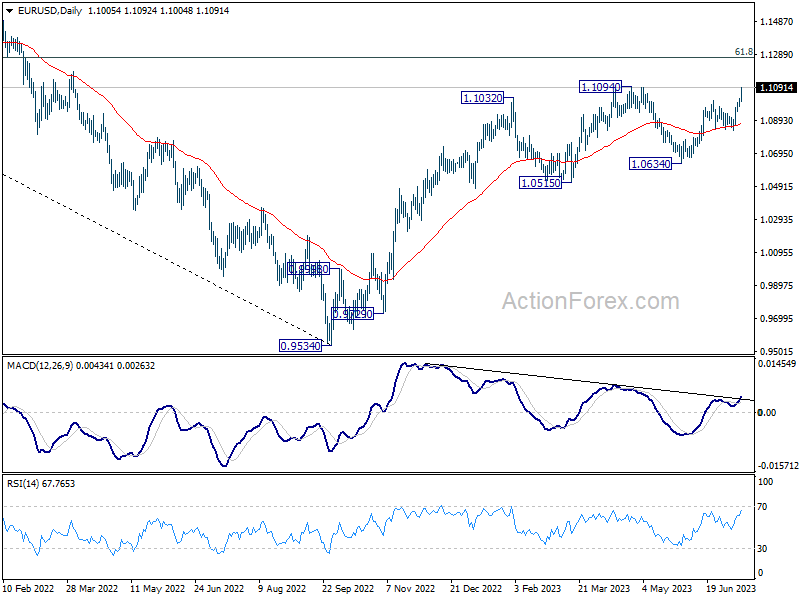

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0981; (P) 1.1004; (R1) 1.1031; More...

EUR/USD's rally is still in progress and intraday bias remains on the upside. Decisive break of 1.1094 will resume larger up trend from 0.9534 to 1.1273 fibonacci level. On the downside, below 1.1012 minor support will turn intraday bias neutral first. But further rally will remain in favor as long as 1.0834 support holds.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

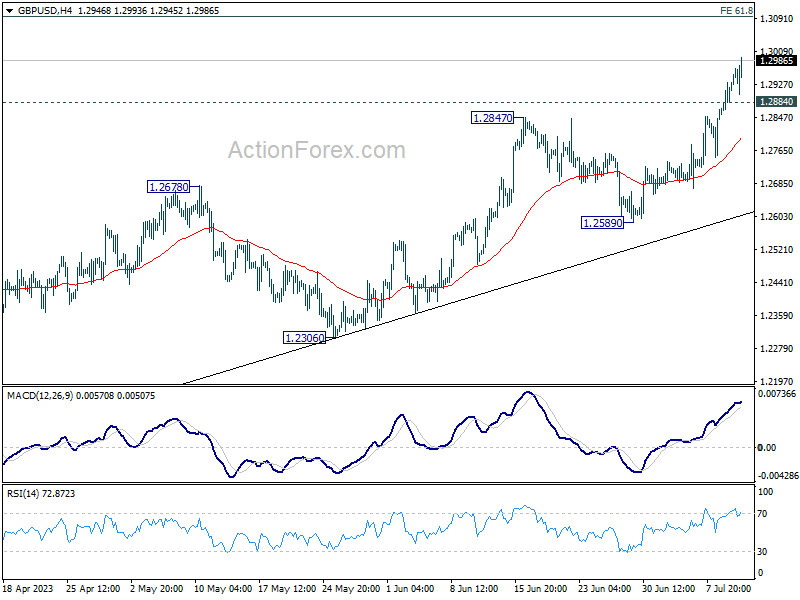

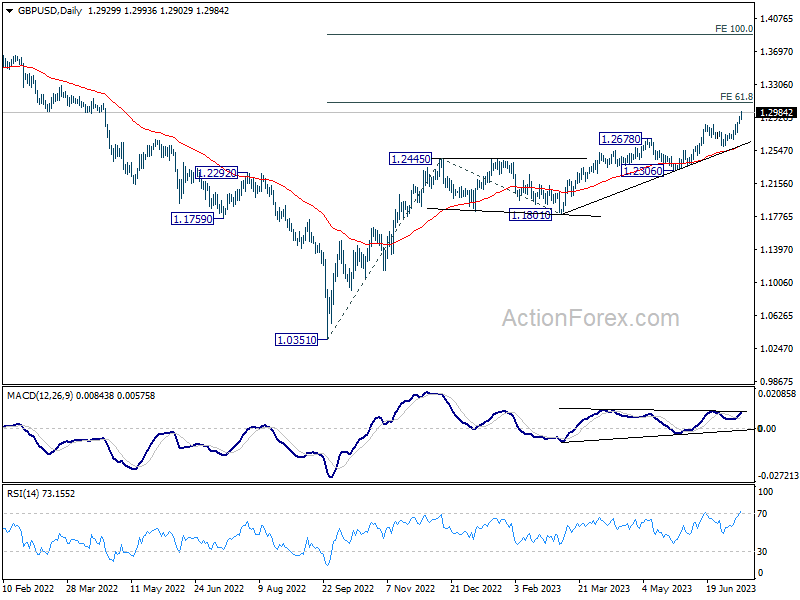

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2880; (P) 1.2907; (R1) 1.2960; More...

Intraday bias in GBP/USD stays on the upside for the moment. Current rally should target 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095. On the downside, below 1.2884 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, the strong support from 55 W EMA (now at 1.2341) is a medium term bullish sign. Outlook will stay bullish as long as 1.2306 support holds. Rise from 1.0351 medium term bottom (2022 low) is expected to extend further to retest 1.4248 key resistance (2021 high).

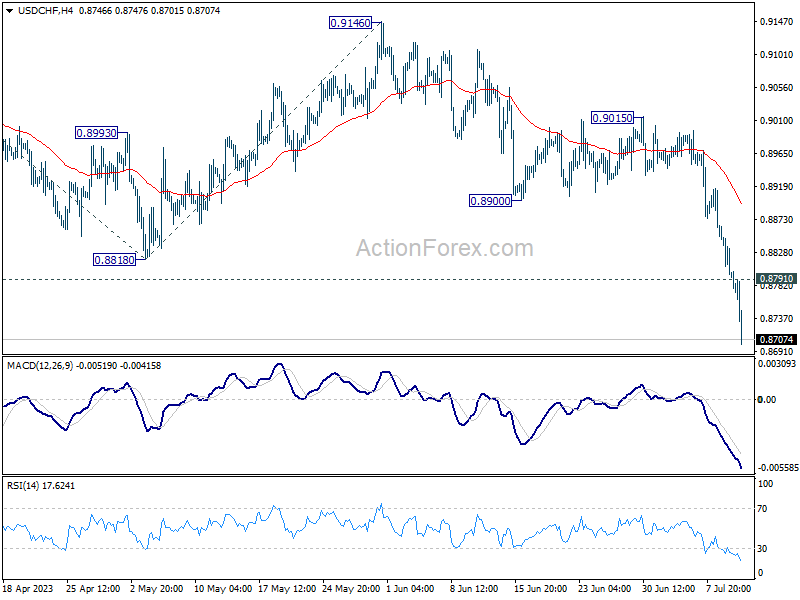

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8766; (P) 0.8822; (R1) 0.8851; More...

USD/CHF's decline accelerates today and breaks through 0.8756 key long term support decisively. There is no sign of bottoming and intraday bias on the downside. Next target is 100% projection of 0.9439 to 0.8818 from 0.9146 at 0.8525. On the upside, above 0.8791 minor resistance will turn intraday bias neutral first. But outlook will remain bearish as long as 0.8900 support turned resistance holds.

In the bigger picture, the break of 0.8756 (2021 low) indicates break out from the long term range pattern. For now, medium term outlook will stay bearish as long as 0.9146 resistance holds. Further fall would be seen back towards 0.7065 (2011 low).

US: Inflation Continues to Ease in June, But Remains Too Hot for FOMC

The Consumer Price Index (CPI) rose 0.2% month-on-month (m/m) in June, a tick below expectations. On a 12-month basis, CPI slipped to 3.0% – its slowest pace since March 2021 – and well off its peak of nearly 9% last June.

- The monthly uptick in headline inflation was driven by higher energy costs (+0.6% m/m), including an uptick in gasoline (+0.8% m/m) and energy services (+0.4% m/m). Food prices rose a modest 0.1% m/m and have slowed to 5.7% on a year-over-year (y/y) basis.

Excluding the direct effects of food and energy, core inflation rose 0.2% m/m – also coming in a hair below expectations. The 12-month change on core edged lower by 0.5%-pts on the month, falling to 4.8%, while the three-month annualized change slipped to 4.1%.

Price growth across services rose 0.3% m/m – a deceleration from the 0.4% m/m gains seen over the three-months prior. Core services are up 6.2% relative to June 2022.

- A major contributor to the price growth in services remains rent, with both owners' equivalent rent (OER) and rent of primary residence (RPR) notching sizeable gains of 0.5% m/m. That said, the much-anticipated slowing in shelter costs now appears firmly intact. Over the last three months, OER and RPR have averaged gains of 0.5% m/m, down from the 0.7% m/m increase seen over the 12 months ending in March.

- Price growth across non-housing services declined by 0.1% m/m, with the weakness concentrated in lodging away from home (-2.0% m/m) and education & communication services (-0.3% m/m). Recreational services (+0.5% m/m) was the only sub-category to report an acceleration last month.

Core goods prices (-0.1% m/m) also declined in June, snapping what had been three consecutive months of gains. Prices across household furnishings (-0.3% m/m), transportation (-0.2% m/m) recreational goods (-0.4% m/m) and education & communication goods (-0.1% m/m) were all lower last month.

Key Implications

Headline inflation has fallen sharply over the past year, with prices up just 3% (or roughly a third of the price growth) relative to June 2022. The core index has been much slower to come down, though encouraging signs are starting to emerge. Shelter costs – a key contributor to price growth through this cycle – have definitively rolled over, while goods have (again) become a source of deflation. We are even starting to see some easing in price pressures across the stickier and more labor-intensive service component of inflation, with the 12-month annualized change on non-housing services falling to 3.9% – the slowest pace of growth since December 2021.

Inflation is moving in the right direction, but progress should not be confused with mission accomplished. Core inflation is still running at a multiple of the Fed's 2% inflation target, while last week's employment data showed that the labor market continues to exude a surprising degree of resilience. Another 25 basis-point rate hike at FOMC's upcoming July 25-26th meeting seems inevitable, with policymakers likely to maintain a tightening bias over the near-term as they continue to monitor incoming data to determine the future path of the policy rate.