Sample Category Title

Has Oil Run its Upswing Potential?

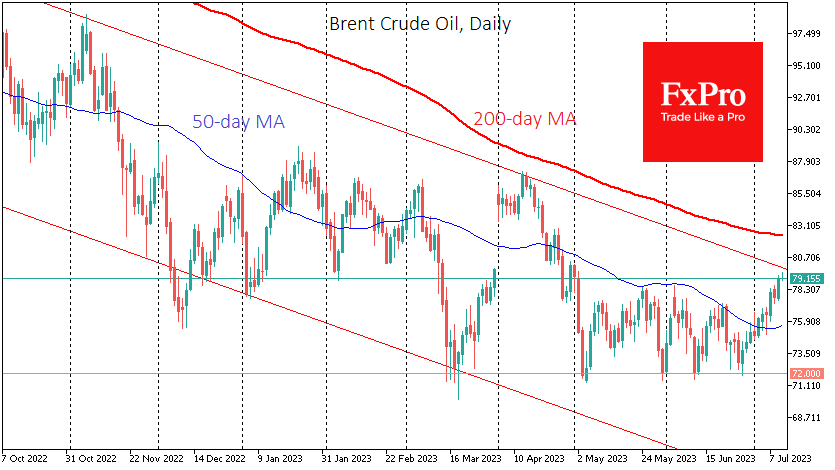

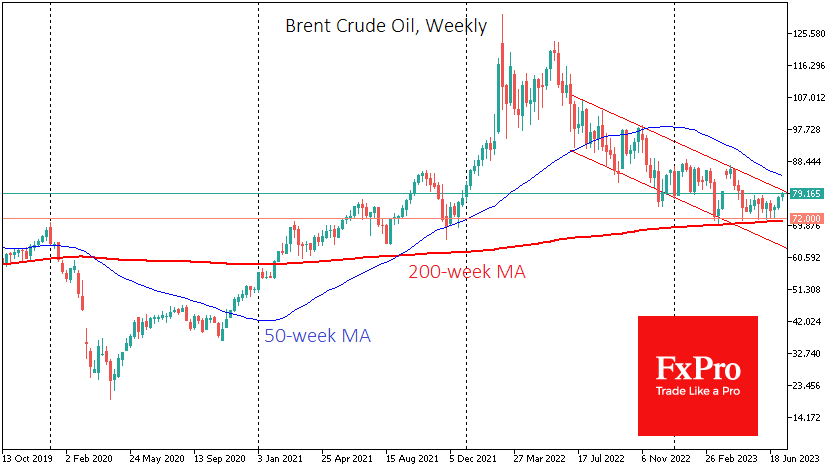

Crude oil has rallied more than 10% from the lows two weeks ago. The price of a barrel of Brent rose above $79.50 on Wednesday, its highest level since early May. But the easy part of the journey for the bulls may be over, and a severe battle to stay within the year-long downtrend is now beginning.

The actions of the OPEC+ members since March have drawn a clear horizontal line of support for the price, as supply reduction interventions have almost always followed the price closer to $72.

Thanks to a relatively strong labour market and a weaker dollar since the beginning of the month, oil has climbed to levels it was reluctant to breach in May and June.

However, this rise is all within the downtrend that has been in place since last July, and the latest spike has taken the price to the upper boundary of this downtrend.

On the technical side, the most exciting part is now beginning, as we are about to witness a battle for the trend, which promises a surge in volatility.

A further rally and the ability to consolidate above $80 will be the first signal to break the downtrend. If the bears retreat quickly here, we could see a rapid rise to $82.50, close to the 200-day moving average. The final break of the year-long downtrend would only be a move above the previous highs at $87.

However, the more likely scenario is a pullback within the range and at least a retest of critical support. The maximum would be a break of this line and a move lower. On the side of this scenario are fundamental factors in the form of China’s slowdown, which has proved unresponsive to the announced stimulus measures, and growing signs of contraction in the major developed economies under interest rate pressure.

From a technical point of view, the downtrend remains in place until a reversal is confirmed. In this case, be prepared for Brent crude to return to $72 this month and for an attempt to storm this key OPEC+ support line next month. This is also where the 200-week moving average is, and a sharp break below it could have the effect of a dam bursting, as it did in 2020 or 2014.

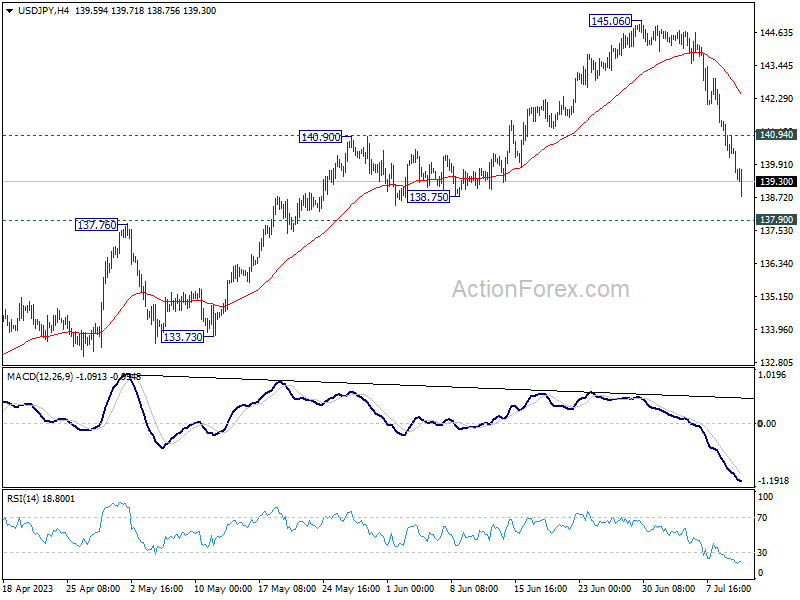

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 139.86; (P) 140.66; (R1) 141.16; More...

USD/JPY reaches as low as 138.75 so far today as fall from 145.06 continues today. Next target is 137.90 resistance turned support. Decisive break there will confirm the larger bearish case. On the upside, above 142.06 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another fall.

In the bigger picture, current downside acceleration, as seen in daily MACD, argues that fall from 145.06 is already the third leg of the corrective pattern from 151.93 (2022 high). Sustained break of 137.90 resistance turned support should confirm this case and target 127.20 (2023 low) and below. For now, this will remain the favored case as long as 145.06 resistance holds.

Dollar’s Plunge Deepens After Underwhelming Consumer Inflation Figures

Dollar's decline accelerates again following US inflation data that reflected a more substantial than anticipated slowing in both core and headline CPI for June. Although the underwhelming data might not deter Fed from delivering another rate hike later this month, it may alleviate pressure for subsequent increases.

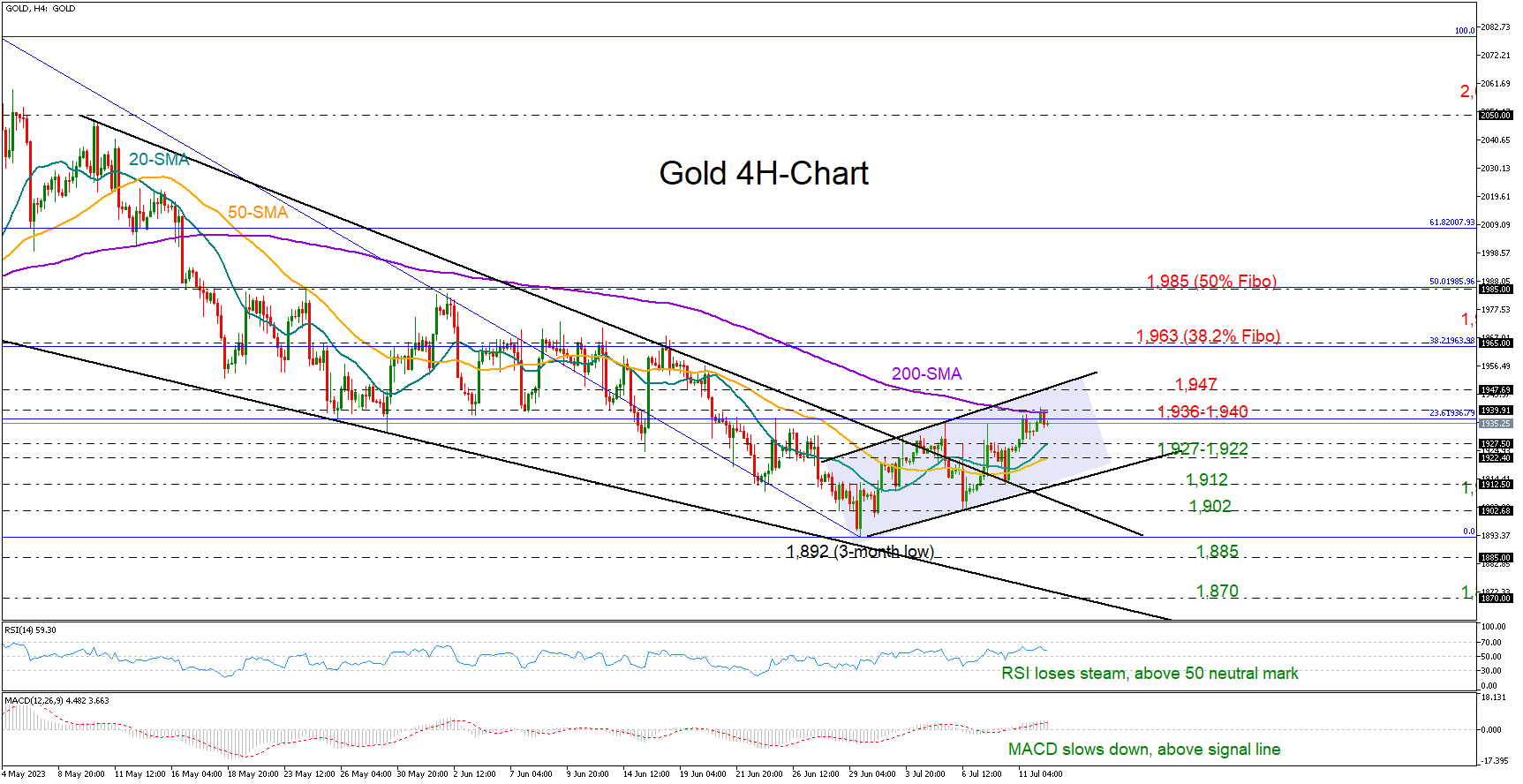

In response to the data, US stock futures appear to be on an upward trajectory, while 10-year yield is continuing its near term pull back. Correspondingly, gold is seeing a solid rally, propelled by greenback's weakness.

For now, Yen appears to be the biggest beneficiary, maintaining its position as the strongest currency. Hot on its heels is Euro, but Sterling is currently floundering, ranking as the second weakest next to Dollar. Australian and New Zealand Dollars have also gained strength following Euro, although Canadian Dollar remains steady as traders adopt a cautious approach in anticipation of BoC's imminent interest rate decision.

Technically, Gold's rebound is also accelerating as seen in 4H MACD. Next focus is 38.2% retracement of 2062.95 to 1892.76 at 1957.77. Firm break there will pave the way to 61.8% retracement at 1997.93, with prospect of at least a test on 2000 psychological level.

In Europe, at the time of writing, FTSE is up 1.62%. DAX is up 1.20%. CAC is up 1.08%. Germany 10-year yield is down -0.0459 at 2.607. Earlier in Asia, Nikkei dropped -0.81%. Hong Kong HSI rose 1.08%. China Shanghai SSE dropped -0.78%. Singapore Strait Times rose 0.36%. Japan 10-year JGB yield rose 0.0239 to 0.480.

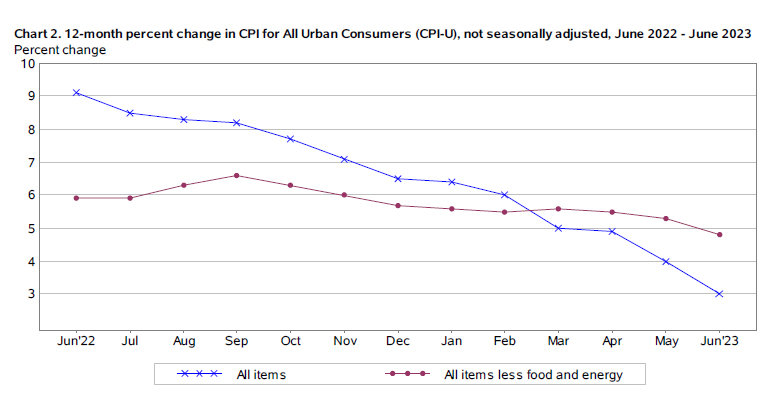

US CPI slowed to 3% yoy in Jun, core CPI down to 4.8% yoy, both below exp

US CPI rose 0.2% mom in June, below expectation of 0.3% mom. CPI core (all items less food and energy) rose 0.2% mom, below expectation of 0.3% mom, the smallest 1-month increase since August 2021. Food index rose 0.1% mom while energy index rose 0.6% mom.

Over the last 12 months, CPI slowed from 4.0% yoy to 3.0% yoy, below expectation of 3.1% yoy. That's the lowest reading since March 2021. Core CPI slowed from 5.3% yoy to 4.8% yoy, below expectation of 5.0% yoy. Energy index was down -16.7% yoy while food index was up 5.7% yoy.

RBNZ holds OCR steady at 5.5%, expresses confidence in returning inflation to target range

In line with broad expectations, RBNZ keeps OCR unchanged at 5.5%, as tightening cycle has finally entered in to a pause phase.

RBNZ expressed its confidence in the current restrictive interest rate level, stating, "consumer price inflation will return to within its target range of 1 to 3% per annum, while supporting maximum sustainable employment."

When discussing their Remit objectives, the Committee noted that it still expects inflation to fall within the target band by the second half of 2024. Risks surrounding the inflation projection as being "broadly balanced". While employment remains above its maximum sustainable level, recent indicators suggest that "labour market conditions are easing."

RBNZ also acknowledged the slight contraction in economic activity in Q1. It added that "growth is likely to remain weak in the near term."

RBA Lowe: Further tightening possible, look into new forecasts in Aug

RBA Governor Philip Lowe noted the current economic outlook is a "complex picture" with significant uncertainties". He said in a speech today, "the Board decided that, having already increased rates substantially, it was appropriate to hold interest rates steady this month and re-examine the situation next month."

Looking ahead, Lowe noted, "It is possible that some further tightening will be required to return inflation to target within a reasonable timeframe," adding that requirement for further action will largely depend on evolution of the economy and inflation.

He highlighted that the Board will be provided with an updated set of economic forecasts, a revised risk assessment, and fresh data on inflation, the global economy, labour market, and household spending at the next meeting in August to inform its decision-making process.

He pointed to recent forecasts in May which saw inflation returning to top of target band in "mid-2025:. But he acknowledge, Data received since then had suggested that the inflation risks had shifted somewhat to the upside."

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 139.86; (P) 140.66; (R1) 141.16; More...

USD/JPY reaches as low as 138.75 so far today as fall from 145.06 continues today. Next target is 137.90 resistance turned support. Decisive break there will confirm the larger bearish case. On the upside, above 142.06 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another fall.

In the bigger picture, current downside acceleration, as seen in daily MACD, argues that fall from 145.06 is already the third leg of the corrective pattern from 151.93 (2022 high). Sustained break of 137.90 resistance turned support should confirm this case and target 127.20 (2023 low) and below. For now, this will remain the favored case as long as 145.06 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | PPI Y/Y Jun | 4.10% | 4.50% | 5.10% | 5.20% |

| 23:50 | JPY | Machinery Orders M/M May | -7.60% | 1.20% | 5.50% | |

| 02:00 | NZD | RBNZ Interest Rate Decision | 5.50% | 5.50% | 5.50% | |

| 12:30 | USD | CPI M/M Jun | 0.20% | 0.30% | 0.10% | |

| 12:30 | USD | CPI Y/Y Jun | 3.00% | 3.10% | 4.00% | |

| 12:30 | USD | CPI Core M/M Jun | 0.20% | 0.30% | 0.40% | |

| 12:30 | USD | CPI Core Y/Y Jun | 4.80% | 5.00% | 5.30% | |

| 14:00 | CAD | BoC Interest Rate Decision | 5.00% | 4.75% | ||

| 14:30 | USD | Crude Oil Inventories | -1.1M | -1.5M | ||

| 15:00 | CAD | BoC Press Conference | ||||

| 18:00 | USD | Fed's Beige Book |

US CPI slowed to 3% yoy in Jun, core CPI down to 4.8% yoy, both below exp

US CPI rose 0.2% mom in June, below expectation of 0.3% mom. CPI core (all items less food and energy) rose 0.2% mom, below expectation of 0.3% mom, the smallest 1-month increase since August 2021. Food index rose 0.1% mom while energy index rose 0.6% mom.

Over the last 12 months, CPI slowed from 4.0% yoy to 3.0% yoy, below expectation of 3.1% yoy. That's the lowest reading since March 2021. Core CPI slowed from 5.3% yoy to 4.8% yoy, below expectation of 5.0% yoy. Energy index was down -16.7% yoy while food index was up 5.7% yoy.

Gold Tries to Recover

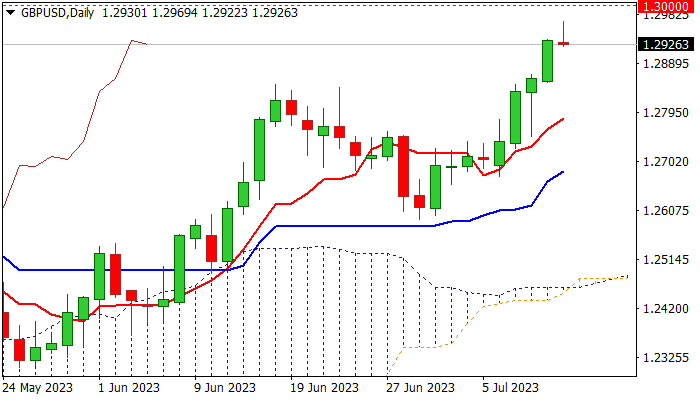

GBP/USD breaks higher

The pound advanced after resilient UK wage growth put pressure on the Bank of England to tighten policy. A new high above 1.2850 suggests a bullish continuation after a near four-week long consolidation. Such an upbeat confirmation in market sentiment would attract more trend followers. The supply zone formed by the psychological level of 1.3000 and a 15-month high of 1.3050 is next where resistance could be felt. As the RSI ventures into the overbought area again, 1.2880 is the closest support in case of a pullback.

XAU/USD bounces back

Gold bounced as Fed officials hinted at the near end of the tightening cycle. The price seems to have found a solid foundation over the psychological level of 1900 from where the bulls hope the precious metal is bottoming out. A decisive break above the recent swing high of 1935 has prompted more bears to cover in fear of a short-squeeze, which could pave the way for an extended recovery towards June’s peak of 1982 with 1955 as an intermediate hurdle. 1924 is a fresh support to keep the rebound momentum intact.

US Oil breaks key resistance

WTI crude rallied after the IEA commented that the market may tighten in the second half of the year. A close above the previous swing high of 72.50 then the 6-week high of 74.50 may open the door to a broader recovery in the medium-term by forcing the shorts to cut their losses. A bullish MA cross on the daily chart compounds the reversal pressure with 76.80 as the next target. The RSI’s double top in the overbought area may cause a limited fallback and the base of the momentum at 73.00 is the level to assess follow-up bids.

GBP/USD: Bulls Lose Traction on Approach to 1.30 Barrier, US CPI in Focus for Fresh Signals

Cable eases from new 15-month high (1.2969), posted in late Asian trading on Wednesday, as bulls faced headwinds on approach to psychological 1.30 barrier, due to overbought daily studies.

Wednesday’s action was so far shaped in a shooting star candlestick, which usually signals reversal when on top of an uptrend, generating initial signal of potential reversal, which will need a verification on completion of the pattern.

The signal is negative, but it collides with overall bullish structure and expectations for upbeat US inflation report, which may offer fresh support to sterling on weaker than expected June figures and lift pound through 1.30 barrier for the first time since Apr 2022.

Former top (1.2848) turned to solid support, with deeper pullback expected to find firm ground above rising daily Tenkan-sen (1.2784) to keep near-term bias with bulls.

Res: 1.2969; 1.3000; 1.3045; 1.3105.

Sup: 1.2900; 1.2848; 1.2800; 1.2784.

Gold Trends Higher; Resistance Within 1,940 Area

Gold has been swinging higher in the four-hour chart since hitting a three-month low of 1,892 at the end of June, rising as high as 1,940 today.

The precious metal is hovering around a familiar constraining zone and near the 200-period simple moving average, which caused a soft decline over the past few hours. The 23.6% Fibonacci retracement of the previous downleg is cementing that wall as well. Hence, traders might wait for a clear close above the 1,936-1,940 boundary before they target the upper band of the short-term bullish channel at 1,947. A successful move higher could last till the 38.2% Fibonacci mark of 1,963, while a steeper rally could approach the 50% Fibonacci of 1,985.

From a technical perspective, the short-term bias is still positive, as the RSI and the MACD are comfortably above their neutral levels. However, some caution might be needed as the indicators seem to have lost some momentum.

A pullback below 1,936 could pause somewhere between the 20- and 50-period SMAs at 1,927 and 1,922 respectively. If sellers persist, the price may slide towards the channel’s lower band at 1,912. Even lower, the bears might pressure the 1,900-1,896 floor with scope to mark new lower lows, likely around the 1,870 handle if the 1,885 low from March 15 gives way.

Summing up, the short upward trend in gold may keep buying interest intact in the coming sessions. A continuation above 1,947 could boost market sentiment, whilst a slide below 1,912 could add more pressure on the market.

FTSE 100 – Tentatively Higher With an Eye on US Inflation Data

- Attention remains on US inflation data today

- Only a much lower core CPI reading could tempt the Fed to reconsider hiking in two weeks

- UK100 rebounds but caution may remain unless key level is overcome

European stock markets are tentatively higher on Wednesday, with the FTSE 100 leading the way up more than 1%, as traders adopt a cautious position ahead of the US inflation report.

Any hopes of another pause from the Fed this month have dwindled in recent weeks as the data simply hasn't delivered what it needed to in order to convince the FOMC to do so for a second consecutive meeting. A second pause would be taken as a sign that the tightening cycle is over so it's not a decision that would be taken lightly.

The jobs report on Friday was nowhere near good enough to convince the Fed that it has achieved its objectives. There will no doubt have been relief that the NFP number didn't replicate that of the ADP but together with the wage component, it still pointed to a labor market that is very tight.

It would take something remarkable from the inflation report today to convince policymakers that they can afford to pause again. The headline CPI falling to 3.1% doesn't fall into that category when the core number is expected to remain high at 5%. It would take a real shock on the core side to really stimulate the debate in two weeks.

A failure to break back above 7,400 could be viewed as confirmation of the initial break

It hasn't been a great few months for the UK index, having fallen almost 9% from its April peak before rebounding a little this week. It did run into some support around 7,200 where it has reacted to on numerous occasions in the past, including in March, the last time it fell back to these levels.

UK100

Source – OANDA on Trading View

Having recovered a little in the last couple of days, it now faces a test around 7,400, another level it has previously been responsive to, most recently a couple of weeks ago when it saw strong support here.

A rebound off that level this time could be viewed as confirmation of the break below there on Thursday and therefore a bearish signal. That would draw attention back to 7,200 which may, as a result, look a little more vulnerable.

NZD/USD – RBNZ May Be Done With Its Tightening Cycle After Pause

- RBNZ leaves rates unchanged after near-two year hiking cycle

- Inflation is seen returning to target next year

- NZD performing better but potentially running on fumes

The RBNZ opted to pause its tightening cycle earlier today after a very aggressive tightening cycle over the last couple of years.

After increasing the cash rate to 5.5%, there are signs that the economy is slowing which will bring inflation down. While inflation has only fallen to 6.7% so far, data next week is expected to show it falling further and the central bank is confident it will return to its 1-3% target range next year.

New Zealand faced many challenges in the aftermath of the pandemic which contributed to surging inflation but much higher rates and levels of immigration appear to be easing those pressures.

Is the New Zealand dollar running on fumes?

The kiwi has been gradually trending lower in the first half of the year but there have been some small signs that this may be about to change. The question is, if the RBNZ is done, has the bullish case softened somewhat? Or could a stronger economy draw investors back in?

NZDUSD Daily

Source – OANDA on Trading View

Over the last month, it's run into support around 0.60 against the US dollar which falls around the 50% Fibonacci retracement level – October 2022 lows to February 2023 highs.

Then in late June, it rebounded slightly ahead of that previous low which could be viewed as a bullish signal but many will still be unconvinced.

A break above the descending channel could be another stronger signal that the trend has turned for the pair, although so far, it appears to be running low on momentum just when it needs it most.

NZDUSD 4-Hour

CPI Release Will Decide the Next FOMC Step

Today's focus is on the US CPI data, which experts believe will be better than expected. The forecasted US CPI m/m is 0.3%, and y/y is 3.1%, a positive sign for the market as the Fed's inflation target is 2%. Even a strong inflation reading may lead to one more interest rate hike, keeping traders somewhat worried. The reaction of the 2-year Treasury yield and the dollar index will indicate the Fed's next move. With inflation slowing down, the path of least resistance for the US equity market is skewed to the upside.

US DOLLAR - D1 Timeframe

The US Dollar on the daily timeframe has reached a significant mark. As the chart highlights, the demand zone presents a reliable point of interest for a likely reversal in the price action toward the resistance trendline. If the CPI figures are higher-than-expected, this is likely the course of movement on the Dollar.

Analyst’s Expectations:

- Direction: Bullish

- Target: 102.779

- Invalidation: 100.938

GBPUSD - D1 Timeframe

The upward movement of GBPUSD has been a steady climb in a channel pattern which seems to now be approaching a key area of resistance. As shown in the attached chart, the supply zone has further confluence from the resistance trendline and could be a turning point for the bullish price action - should the CPI favor the Dollar, as I mentioned earlier.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1.28280

- Invalidation: 1.30393

EURUSD - D1 Timeframe

EURUSD is another likely candidate for a brilliant reversal stunt. We currently see price trading within the supply zone right next to a major pivot level from the Weekly timeframe. Based on this and the likelihood of a positive CPI outcome for the Dollar, I would look for opportunities to short the market, possibly to the support trendline.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1.08948

- Invalidation: 1.10985

CONCLUSION

The trading of CFDs comes at a risk. Thus, to succeed, you have to manage risks properly. To avoid costly mistakes while you look to trade these opportunities, be sure to do your due diligence and manage your risk appropriately.