Sample Category Title

GBP/USD Daily Outlook

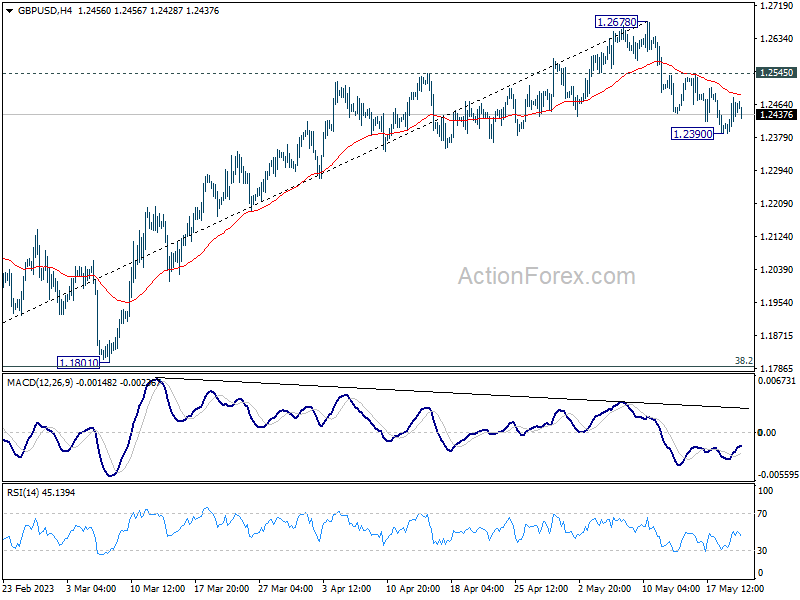

Daily Pivots: (S1) 1.2396; (P) 1.2440; (R1) 1.2488; More...

Intraday bias in GBP/USD remains neutral at this point. Decline from 1.2678 short term top is expected to continue as long as 1.2545 resistance holds. On the downside, sustained trading below 55 D EMA (now at 1.2394) should confirm that it's already in correction to whole up trend form 1.0351. Deeper fall should then be seen to 1.1801 cluster support (38.2% retracement of 1.0351 to 1.2678 at 1.1789). On the upside, however, break of 1.2545 will bring stronger rebound back to retest 1.2678 high.

In the bigger picture, as long as 1.1801 support holds, rise from 1.0351 medium term bottom (2022 low) is expected to extend further. Sustained break of 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759 will add to the case of long term bullish trend reversal. However, firm break of 1.1801 will indicate rejection by 1.2759, and bring deeper decline, even as a correction.

USD/CHF Daily Outlook

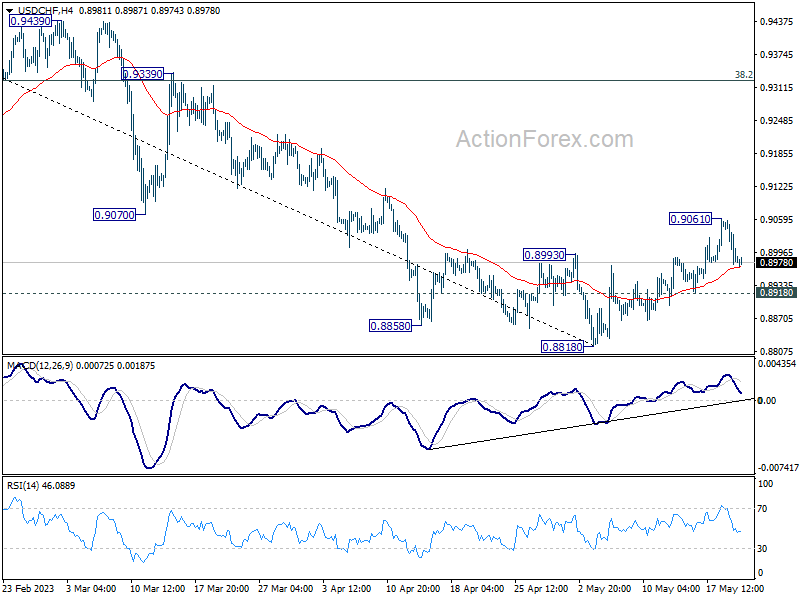

Daily Pivots: (S1) 0.8960; (P) 0.9010; (R1) 0.9044; More...

Intraday bias in USD/CHF remains neutral for the moment. Rebound from 0.8818 short term bottom is expected to continue as long as 0.8918 minor support holds. On the upside, sustained trading above 55 D EMA (now at 0.9039) should confirm that current rally is at least correcting whole down trend from 1.0146. Further rise should then be seen to 38.2% retracement of 1.0146 to 0.8818 at 0.9325. On the downside, though, break of 0.8918 will bring retest of 0.8818 low instead.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high). So, downside should be contained by 0.8756 to bring reversal. Sustained break of 0.9058 support turned resistance will be the first sign of medium term bottoming. However, decisive break of 0.8756 will carry larger bearish implications.

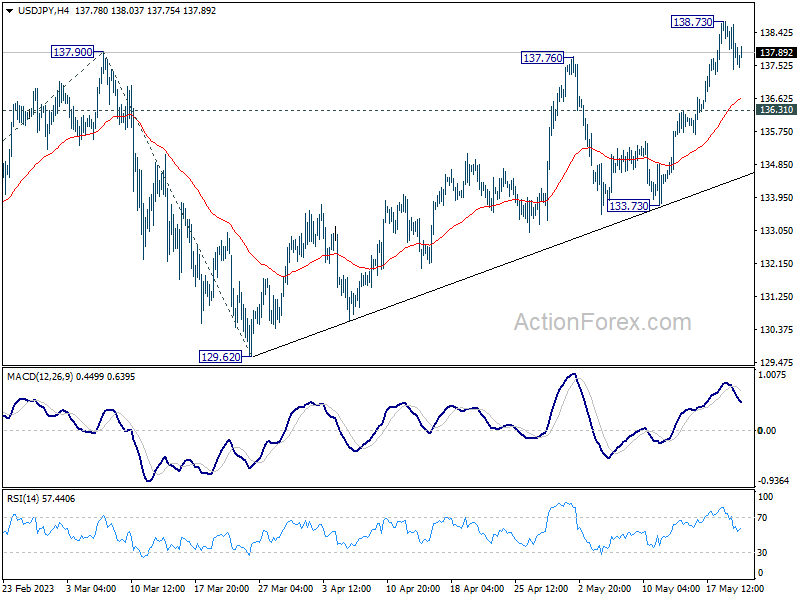

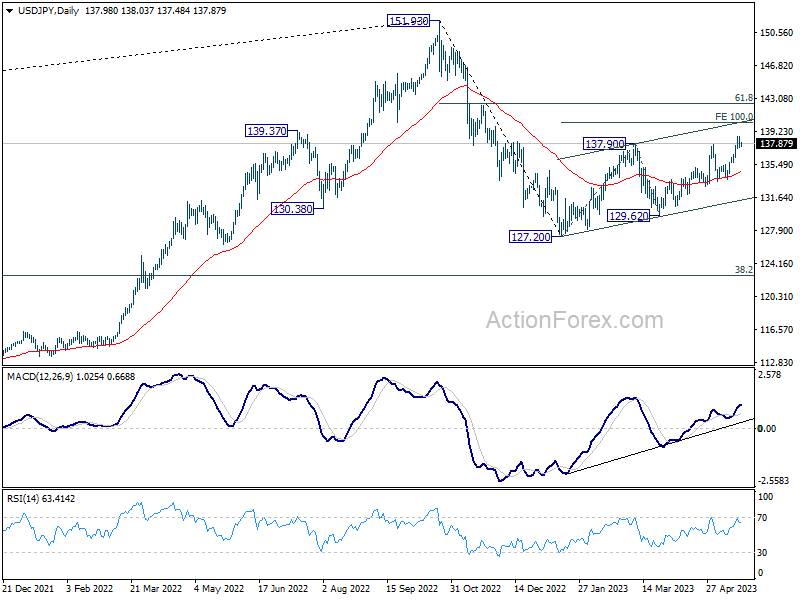

USD/JPY Daily Outlook

Daily Pivots: (S1) 137.34; (P) 138.04; (R1) 138.65; More...

Intraday bias in USD/JPY remains neutral for consolidation below 138.73 temporary top. Downside of retreat should be contained by 136.31 support to bring another rally. Break of 138.73 will turn bias back to the upside for 100% projection of 127.20 to 137.90 from 129.62 at 140.32. Break there will target 142.48 fibonacci level.

In the bigger picture, rise from 127.20 is seen as the second leg of the corrective pattern from 151.93 high. Stronger rally would be seen to 61.8% retracement of 151.93 to 127.20 at 136.34. Sustained break there will pave the way back to retest 151.93. On the downside, however, break of 133.73 support will argue that the pattern could have started the third leg through 127.20 low.

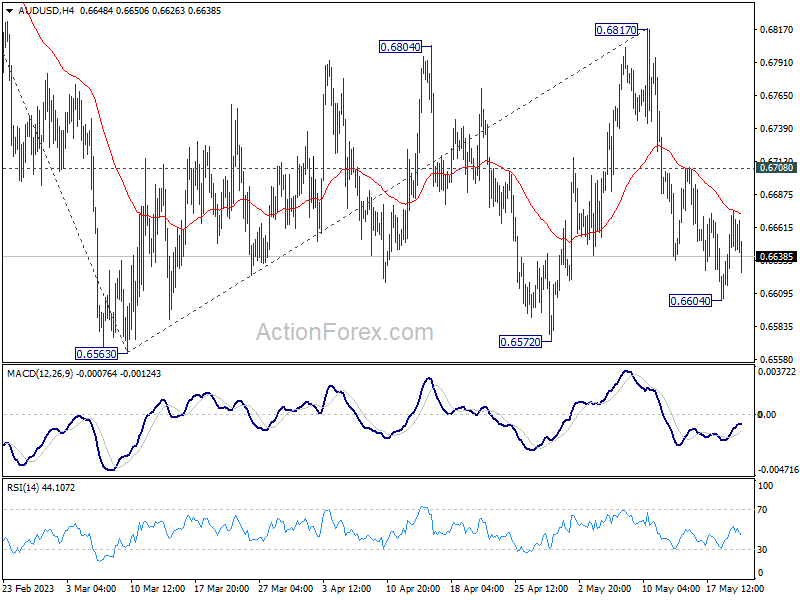

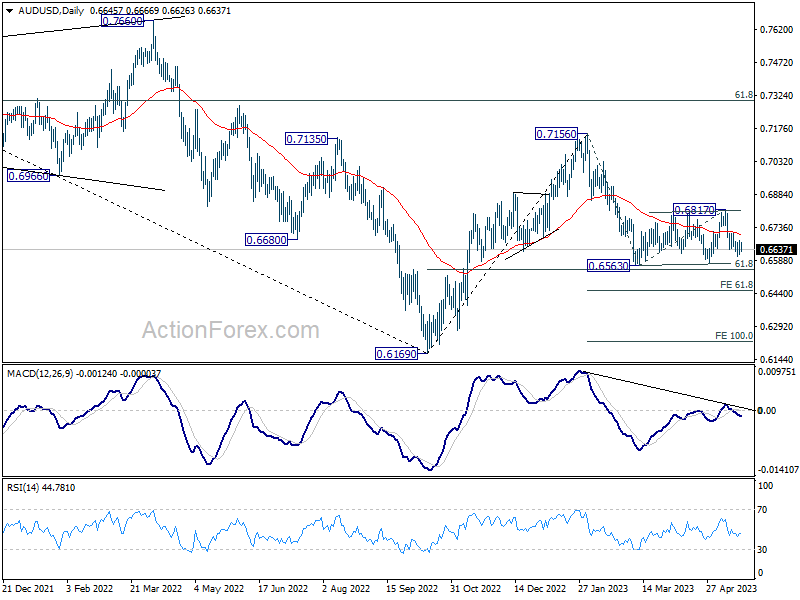

AUD/USD Daily Report

Daily Pivots: (S1) 0.6619; (P) 0.6647; (R1) 0.6678; More...

Intraday bias in AUD/USD remains neutral and outlook is unchanged. Further decline is in favor as long as 0.6708 resistance holds. Below 0.6604 will bring retest of 0.6563 low first. Decisive break there will resume larger decline from 0.7156 to 61.8% projection of 0.7156 to 0.6563 from 0.6817 at 0.6451. On the upside, above 0.6708 minor resistance will delay the bearish case, and extend the corrective pattern from 0.6563 with another rising leg.

In the bigger picture, the failure to break through 55 W EMA (now at 0.6822) keeps medium term outlook bearish. Firm break of 61.8% retracement of 0.6169 to 0.7156 at 0.6546 will raise the chance of long term down trend resumption through 0.6169 low. This will now be the favored case as long as 0.6817 resistance holds.

EUR/USD Trying to Extend Bottoming Out

Markets

US Treasuries and German Bunds parted ways on Friday after a joint 10 bps surge the day before. Yields in the US still rose between 1.3-4.8 bps with the belly underperforming. They easily overcame a setback in the first hours of the American trading session, when Fed chair Powell said credit stress may limit the need for new rate hikes. It put the spotlight on a growing FOMC division. Several other Fed governors last week were much less convinced of the idea of such a pause. It also contrasts with the ECB chair on Sunday calling for further hikes: “We are not done yet, we are not pausing based on the information I have today.” German rates headed into the weekend 0.5-2.9 bps lower. The technical charts posed too much of a challenge for the likes of the 10-y (2.5% resistance). This was also true for equities. The S&P500 tested but failed to clear the February high – before the collapse of SVB. European stocks still finished in the green with the EuroStoxx50 taking a shot at high-profile resistance around 4415. This is the post-pandemic recovery and multiyear high of November 2021. The dollar took a breather after its earlier strengthening. EUR/USD rebounded from a 1.076 low to 1.0805. DXY (trade-weighted dollar) eased from the highest level since mid-March (103.58) to 103.2. Sterling consolidated near the strongest levels since December last year. EUR/GBP settled in the high 0.86 area.

Asian stocks trade mostly in the green this morning with some minor outperformance in China. News flow is limited and that’s unlikely to change later today. Except from the European Commission’s consumer confidence, the eco calendar is empty. There are, however, a series of ECB and Fed speeches scheduled. They serve as a wildcard for trading. The same goes for the debt ceiling story. There were conflicting messages last week. There was hope talks could land this weekend but so far there’s no breakthrough. President Biden said talks with McCarthy went well and he will continue them today. Core bonds trade a tad stronger this morning. We expect some consolidation near the recent highs ahead of tomorrow’s May PMIs. EUR/USD is trying to extend its bottoming out. The pair is moving a little higher north of 1.08. Sterling keenly awaits those same PMIs as well as Wednesday’s CPI data. The Bank of England is awaiting evidence of more stubborn (services) inflation before hiking further. That leaves the pound vulnerable to a downside surprise in the data.

News Headlines

S&P rating agency on Friday affirmed the credit rating of Slovakia at A+. At the same time it raised the outlook from negative to stable. According to S&P, the country has successfully reduced its exposure to Russian hydrocarbon imports and the economy has proved resilient to the effects of the war between Russia and Ukraine. Inflation has remained high and the budget deficit will decline only gradually over the next few years from 5.5% this year. Government measures to support households and businesses increased this year’s government deficit. According to S&P, the political turbulence causes greater uncertainty. However, the rating agency expects that anchors for fiscal and economic policies remain intact. S&P expects 1.2% growth this year and 2.0% growth next year. It expects to government deficit to narrow to 3.6% of GDP by 2026. The net general government debt is expected hovering below 50% of GDP through 2025.

The ruling conservative New Democracy came out as victor in the parliamentary elections in Greece this weekend. With about 95% of the votes counted, the party gained about 41% of the votes. The left Syriza party of former prime minister Alex Tsipras secured about 20 % of the votes. However, according to projections of Interior Ministry, New Democracy might obtain 145 sets out of 300 in Parliament, just short of an absolute majority. Prime minister Mitsotakis of the New Democracy Party already indicated that he wants a one-party government. If none of the major party leaders succeeds forming a government, a second election is likely this summer in which the New Democracy Party will seek a majority in Parliament.

Debt Ceiling Talks Off and On, But Carry On

The European stocks were up and the S&P500 hit a fresh high since summer, until Garret Graves, who was negotiating for the Republicans abruptly walked out, calling the White House ‘unreasonable’ and declaring that the discussions are on a pause.

Equities sold off and yields rose.

Happily, US President Joe Biden and House Speaker Kevin McCarthy had a ‘productive’ call Sunday and agreed to resume talks today, to avoid what could be a very damaging US default.

The market mood is sweeter this Monday on news that the US politicians will at least resume talks after Friday’s crisis. They will likely strike a last-minute deal to avoid a catastrophic outcome.

But Treasury Secretary Janet Yellen reminds that the US will receive taxes by mid-June, but that she is not sure there will be enough money in the coffers to carry on until that date.

The US Treasury General Account, that US government now taps in to pay the bills, has no more than $116 bn.

The US 2-year spiked past 4.30% on Friday, even though Federal Reserve (Fed) Chair Jerome Powell said on Friday that rates may not have to rise as much as expected to curb inflation, as the bank stress is playing a nice role restricting credit conditions. Beyond Powell, the Fed members look undecided on whether to keep raising the rates or to pause. But none see the US rates being cut this year.

The US dollar is down for the second day after a more than 2.50% rebound since the beginning of May. The safe haven demand due to the debt ceiling saga is one of the reasons why the US dollar saw inflows over the past couple of weeks, and an eventually lower liquidity once the crisis is over could be supportive of the greenback. But the divergence between the Fed, which has certainly come to the end of its tightening cycle, and the European Central Bank (ECB), that still has a couple of rate hikes left on the pipeline, hint that the recent weakness in the EURUSD could see a bottom. From a technical standpoint, 1.0730, the minor 23.6% retracement on September to May rally, should give support to the actual bullish trend for a renewed rally above 1.10 and to 1.12.

In Japan, the selling pressure on the yen continues. Yet, the latest data from Japan revealed that the national CPI rose to 4.5% in April, up from 3.2% printed earlier, and defying analyst expectations of a fall to 2.5%. Core inflation rose from 3.1% to 3.4% as expected.

Cheap yen, the Bank of Japan’s (BoJ) ultra-supportive policy, Japanese corporate reforms, and some help from Warren Buffett who has recently invested in Japanese stocks, helped the Nikkei to hit a 3-decade high this month. The inflows could continue as according to the latest BoFA survey, portfolio allocations to Japanese stocks fell to net 11% underweight.

The question is, what will happen when the BoJ will finally reverse its ultra-easy monetary policy to adopt to rising inflation and the hawkish global winds? The yen will certainly gain, and the equities will certainly give back gains. But no one knows how long the BoJ plans to remain absurdly dovish!

What we know however is that tensions between China and the West get worse by the day. The G7 meetings over the weekend revealed that the UK is willing to follow US in curbing business investments in China. China on the other hand hit back saying that Micron chips failed to pass a cybersecurity review and the government warned Chinese operators against buying the company’s chips.

Nasdaq’s Golden Dragon China index has clearly underperformed Nasdaq since the start of this year and there is no apparent improvement in appetite for Chinese stocks despite a supportive monetary policy and return to growth following the end of the Covid measures. Investors are scared that Xi Jinping’s national security obsession could scrap investor friendly measures and leave investors on the back foot.

Debt Ceiling Negotiations Set to Resume Today

Market movers today

We start the week off with a slow day on the data front. We get consumer confidence figures from the euro area.

We also have several Fed speakers on the wire.

Overnight, Japanese May PMIs are released. The economy has been picking up in 2023, recently reflected in surprisingly strong Q1 GDP figures. Further strength increases pressures on the Bank of Japan to loosen its grip on the yield curve.

Looking at the rest of the week, PMIs in the other big economies released Tuesday will catch markets' focus. Besides, we will look out for the German IFO survey, FOMC minutes and US PCE inflation.

The 60 second overview

Debt ceiling: The negotiations between Biden and McCarthy to lift the US debt ceiling are set to resume today. Risk sentiment weakened on Friday when the republican negotiators said the talks had stalled. The treasury cash balance has fallen to just USD57.3 billion, and yesterday Yellen reaffirmed that June 1 'is a hard deadline' for lifting the ceiling in order to ensure avoiding a default. The next round of tax receipts is due to be paid on June 15, which would buy Congress more time for negotiations until July, but whether or not the remaining cash balances are large enough to reach mid-June remains uncertain. We still expect Congress to eventually reach a deal, but the discussions will once again likely go down to the wire.

China: The People's Bank of China maintained the 1 and 5-year Loan Prime Rates unchanged overnight in line with consensus expectations. The weaker-than-expected economic data in April sparked some speculation on potential rate cuts, and we think that further signs of stalling recovery combined with the still low inflation could eventually push the central bank towards introducing new stimulus measures.

Fed speak: Yields turned lower on Friday afternoon after the Fed's Powell commented that the 'policy rate may not have to rise as far as otherwise due to tightened credit conditions'. Yesterday, Kashkari appeared relatively more hawkish, noting that he could support a pause but was also open to hiking rates further at the June meeting. Market prices in around 15% probability of another hike, down from 35-40% before the Powell's comments. We still think the Fed is now done hiking rates as underlying inflation and inflation expectations appear to be gradually cooling, but we also think the recent upbeat macro data underscores that there is no room for cutting rates this year.

FI: 10Y US Treasury yield rose some 3-4bp on Friday. We are seeing a very slow disinversion of the US curve 10Y-30Y and 2Y-10Y, which is the typical move when we are close to the peak or done tightening monetary policy. Comments during the weekend from both ECB's Lagarde and Federal Reserve's Kashkari supports this view as Lagarde stated that ECB was going to raise rates in June, but bulk part of the tightening was done and Kashkari said that he supported a pause in June in order to assess the effects of tightening.

FX: After a strong week for the USD, EUR/USD is trading slightly above 1.08 and USD/JPY just below 138. Scandies had a rough last week, at the end of it exacerbated by thin liquidity which pushed EUR/SEK close to 11.40 and EUR/NOK beyond 11.75.

Credit: iTraxx Main traded slightly tighter on Friday and closed 4.1bp tighter than the week before at 82.6bp, while Xover tightened 17.8bp during the week to close at 434.3bp. The shortened week was characterized by high activity in the primary market, sentiment remains constructive in credit and investor appetite for new deals continues to look solid.

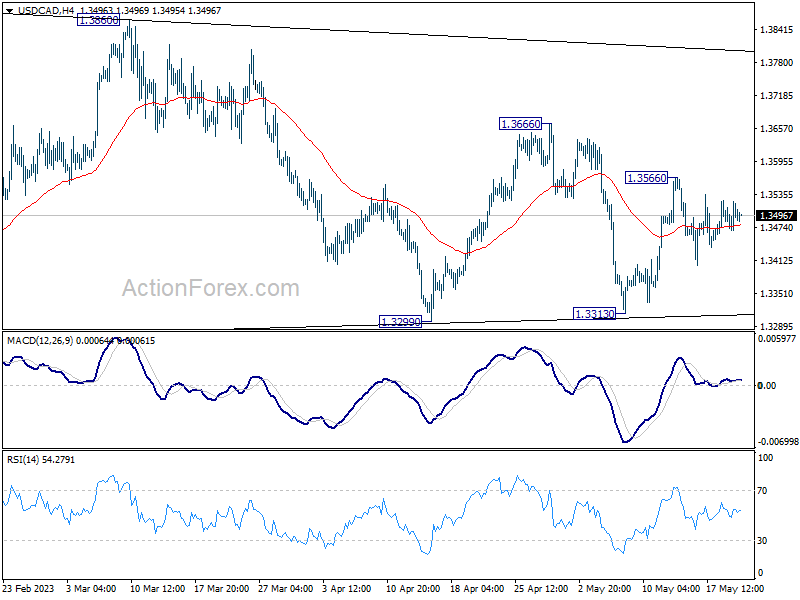

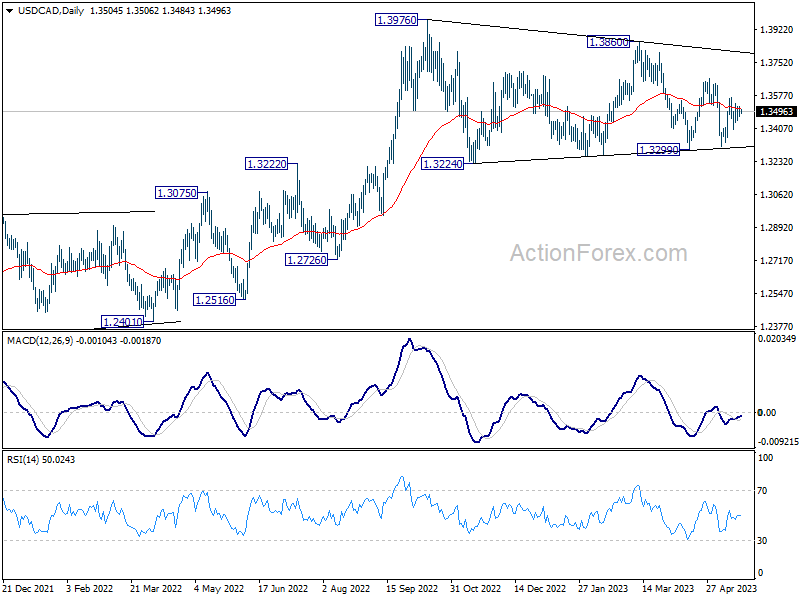

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3470; (P) 1.3496; (R1) 1.3524; More....

Intraday bias in USD/CAD remains neutral as range trading continues. Overall, the pair is seen as extending the triangle consolidation pattern from 1.3976. Above 1.3566 will resume the rebound from 1.3313 towards 1.3666 resistance and then 1.3860. However, firm break of 1.3313 support will invalidate this view and indicate that deeper correction is underway.

In the bigger picture, as long as 55 W EMA (now at 1.3333) holds, up trend from 1.2005 (2021 low) is still in favor to resume through 1.3976 at a later stage. However, sustained trading below the EMA and 38.2% retracement of 1.2005 to 1.3976 at 1.3233 will raise the chance of bearish reversal. Deeper should then be seen to 61.8% retracement at 1.2758 next.

Markets in Mildly Positive Mood as Another Debt Ceiling Talk Awaited

Mood is generally positive in Asian session today, with Hong Kong HSI leading other major indexes higher. While the G7 communique released after the meeting in Hiroshima drew furious response from both China and Russia, there was little reactions among investors. Dollar is trading mildly lower, followed by Canadian and Aussie. Kiwi is currently the stronger one as markets await this week's RBNZ rate hike. Yen is also recovering, followed by Euro and Swiss Franc. But overall, almost all major pairs and crosses are bounded inside Friday's range.

Investors are likely to focus on a scheduled meeting between US President Joe Biden and Republican House Speaker Kevin McCarthy concerning the contentious issue of raising the debt ceiling. Reiterating her cautionary stance, Treasury Secretary Janet Yellen warned on Sunday that the "hard deadline" of June 1 remains in place for augmenting the debt limit. Yellen expressed concern about the looming deadline, stating, "my assessment is that the odds of reaching June 15 while being able to pay all of our bills is quite low." Any updates regarding this matter are expected to significantly sway the market.

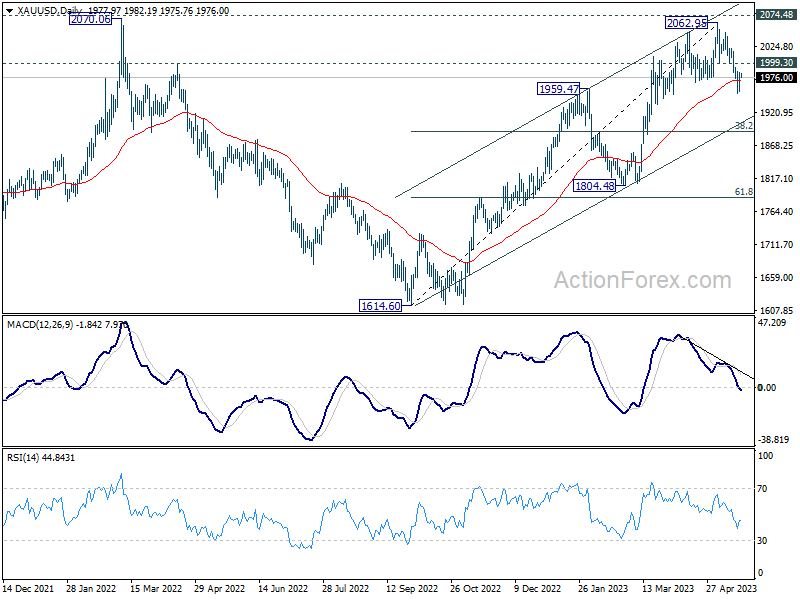

On a technical front, Gold's recent drop from 2062.95 stalled after hitting a low of 1951.77 last week. Nonetheless, outlook remains the same – the precious metal is seen to be in the process of correcting the rally from its 2022 low at 1614.50. Deeper fall is expected, with a break below 1951.77 targeting 38.2% retracement of 1614.60 to 2062.95 at 1891.68. Yet, breaking minor resistance of 1999.30 would dampen this bearish view, potentially sparking a robust rebound back to 2062.95, or even challenging the record high of 2074.48. The next move in Gold will be used to gauge, or at least confirm, that of Dollar's as usual.

In Asia, at the time of writing, Nikkei is up 0.39%. Hong Kong HSI is up 1.30%. China Shanghai SSE is up 0.11%. Singapore Strait Times is up 0.08%. Japan 10-year JGB yield is down -0.0185 at 0.389.

ECB's Lagarde:We are not done yet, we are not pausing

In am interview on the Buitenhof TV show, ECB President Christine Lagarde discussed the bank's progress in tackling inflation, but refrained from giving forward guidance on the monetary policy.

Lagarde noted significant strides have been made in controlling inflation and bringing it in line with ECB's target. However, she cautioned that the journey isn't over yet. "I think we covered a large chunk of the journey toward taming inflation and bringing it back to our target," she said.

Despite this progress, she made it clear "We are not done yet, we are not pausing based on the information I have today." And, "inflation outlook is too high and for too long."

When asked about providing forward guidance, Lagarde expressed caution, citing the potential for various unforeseen factors that could disrupt the economic outlook. "So many things can go wrong that we cannot give what we call forward guidance," she said. "I don't have a predetermined number in my mind."

Lagarde also addressed the ongoing US debt ceiling standoff, emphasizing its potential consequences for both the US and the global economy. "If the United States was to default on its debt it would be a catastrophic development for its economy and for the global economy because of the size of the US economy, because of the depth of its financial sector and because of the totally unpredictable situation that they are facing," she explained.

Despite these risks, Lagarde expressed optimism that common sense would prevail among US leaders, thus avoiding a severely negative economic development. "I have trust in the common sense and the civic sense of the leaders to reach an agreement — which otherwise would take us into a very, very negative development," she said.

Fed's Kashkari: Skipping a meeting is different from "we're done"

Minneapolis Fed President Neel Kashkari, in an interview with Wall Street Journal, suggested that Fed could afford to adopt a slower pace in its current policy trajectory, while emphasizing that this should not be construed as the end of their monetary tightening efforts.

Expressing his openness to a slower approach, Kashkari stated, "I'm open to the idea that we can move a little bit more slowly from here,". However, he strongly disagreed with any sentiment that suggested the Fed's task was complete. "I would object to any kind of declaration that we're done," he clarified.

Kashkari went on to argue that skipping a meeting to gather more data could be a sensible decision. "If the committee chooses to skip a meeting because we want to get more information, I could make the argument why that makes sense," he explained.

He further distinguished this action from an implied cessation of the Fed's work, saying, "A skip to get more information is very different in my mind than [saying], 'Hey, we think we're done.'"

RBNZ shadow board divided on rate hike this week

NZIER disclosed that its RBNZ Shadow Board is in disagreement over whether RBNZ should raise OCR the Official Cash Rate (OCR) this week. A "large number" of the Shadow Board members viewed a 25bps to 5.50% as "warranted". But "the rest" recommended to hold at 5.25%.

This discord was extended to future projections, as NZIER noted a divergence of opinion regarding where OCR should stand in twelve months.

The Shadow Board acknowledged several recent economic developments that indicated a slowing pace in New Zealand economy, including weaker government tax revenue, decreased consumer spending, and ongoing declines in business profitability.

However, members also recognized potential inflation risks from rising net migration inflows and any new fiscal stimulus in the new Budget.

RBNZ rate hike and FOMC minutes: The week ahead

As we look forward to the forthcoming week, RBNZ is widely anticipated to raise the Official Cash Rate by 25bps to 5.50%, which matches the peak indicate in the February Monetary Policy Statement. The case for a pause following this increment is bolstered by recent economic indicators. Notably, annual inflation in the first quarter receded more than RBNZ projected, dropping to 6.7%. Meanwhile, inflation expectation also fell sharply two-year-ahead inflation expectation also fell to 2.79%, back inside RBNZ's target band for the first time since December 2021.

However, other developments could prompt RBNZ to prolong the tightening cycle. The newly proposed government budget, perceived by many as inflationary, projects a 2% fiscal impulse of GDP over the 2023/24 period. The repercussions of the recovery from Cyclone Gabrielle and the uptick in net migration also warrant re-evaluation. Therefore, the risks of a 50bps hike - mirroring RBNZ's action in April - or hints of further tightening, remain plausible.

Turning our gaze to the US, Fed is set to release the minutes from the May FOMC meeting. There are several key questions among market participants. Firstly, is Fed pivoting towards a pause mode? If not, how much further could tightening extend? Finally, when might Fed initiate interest rate cuts? Though these minutes will be under intense scrutiny for answers, they are unlikely to unearth fresh insights unknown to market observers. More significant information may only come to light with new economic projections in June, at the earliest.

In terms of economic data, inflation figures and Purchasing Managers' Indexes will take centre stage this week. Notable releases include UK CPI and US PCE inflation data. PMIs will be reported by Australia, Japan, Eurozone, UK, and US. Additionally, New Zealand retail sales, Germany's Ifo business climate index, and US durable goods orders are among the key data points to watch.

Here are some highlights for the week:

- Monday: Japan machine orders; Eurozone consumer confidence.

- Tuesday: Australia PMIs; Japan PMI manufacturing; UK public sector net borrowing, PMIs; Eurozone PMIs; Swiss trade balance; Canada IPPI, RMPI; US PMIs, new home sales.

- Wednesday: New Zealand retail sales; RBNZ rate decision; UK CPI, PPI; Germany Ifo business climate; FOMC minutes.

- Thursday: Germany GDP final, Gfk consumer climate; US GDP revision, jobless claims, pending home sales.

- Friday: Japan Tokyo CPI, corporate services price index; Australia retail sales; UK retail sales; US durable goods orders, personal income and spending with PCE inflation, goods trade balance.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3470; (P) 1.3496; (R1) 1.3524; More....

Intraday bias in USD/CAD remains neutral as range trading continues. Overall, the pair is seen as extending the triangle consolidation pattern from 1.3976. Above 1.3566 will resume the rebound from 1.3313 towards 1.3666 resistance and then 1.3860. However, firm break of 1.3313 support will invalidate this view and indicate that deeper correction is underway.

In the bigger picture, as long as 55 W EMA (now at 1.3333) holds, up trend from 1.2005 (2021 low) is still in favor to resume through 1.3976 at a later stage. However, sustained trading below the EMA and 38.2% retracement of 1.2005 to 1.3976 at 1.3233 will raise the chance of bearish reversal. Deeper should then be seen to 61.8% retracement at 1.2758 next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Machinery Orders M/M Mar | -3.90% | 0.70% | -4.50% | |

| 10:00 | EUR | German Buba Monthly Report | ||||

| 14:00 | EUR | Eurozone Consumer Confidence May P | -17 | -18 |

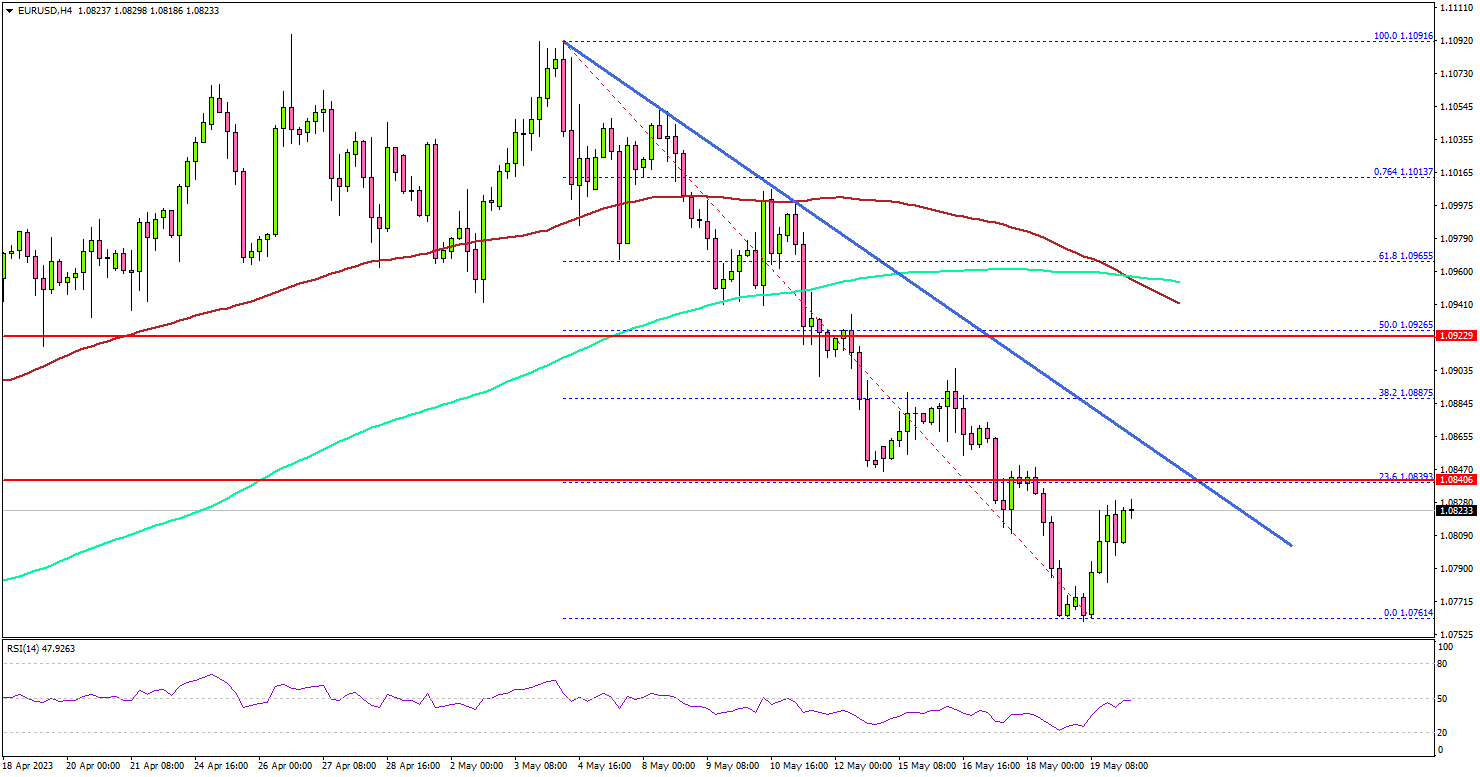

EUR/USD Could Struggle To Recover Above 1.0900

Key Highlights

- EUR/USD started a fresh decline from well above 1.1050.

- A key bearish trend line is forming with resistance near 1.0840 on the 4-hour chart.

- GBP/USD is consolidating losses below the 1.2500 resistance.

- USD/JPY is showing positive signs above the 137.00 level.

EUR/USD Technical Analysis

The Euro started a major decline from well above 1.1050 against the US Dollar. EUR/USD traded below the 1.0920 support to move into a bearish zone.

Looking at the 4-hour chart, the pair settled below the 1.0900 level, the 100 simple moving average (red, 4 hours), and the 200 simple moving average (green, 4 hours).

It even traded below the 1.0840 support level. A low is formed near 1.0761 and the pair is now attempting a recovery wave. Immediate resistance is near the 1.0840 level. There is also a key bearish trend line forming with resistance near 1.0840 on the same chart.

The next major resistance is near 1.0885, above which the pair could rise toward the 1.0900 level. The main resistance is now near 1.0940 and the 100 simple moving average (red, 4 hours).

On the downside, the pair might find bids near 1.0780. The next major support is near the 1.0760 level. If there is a downside break below the 1.0760 level, the pair could test the 1.0720 support level. The next major support sits near the 1.0650 level.

Looking at GBP/USD, the pair could start a fresh increase if the bulls are able to clear the 1.2500 resistance zone.

Economic Releases

- Euro Zone Consumer Confidence for May 2023 (Preliminary) – Forecast -17.0, versus -17.5 previous.