Sample Category Title

AUD/USD Weekly Report

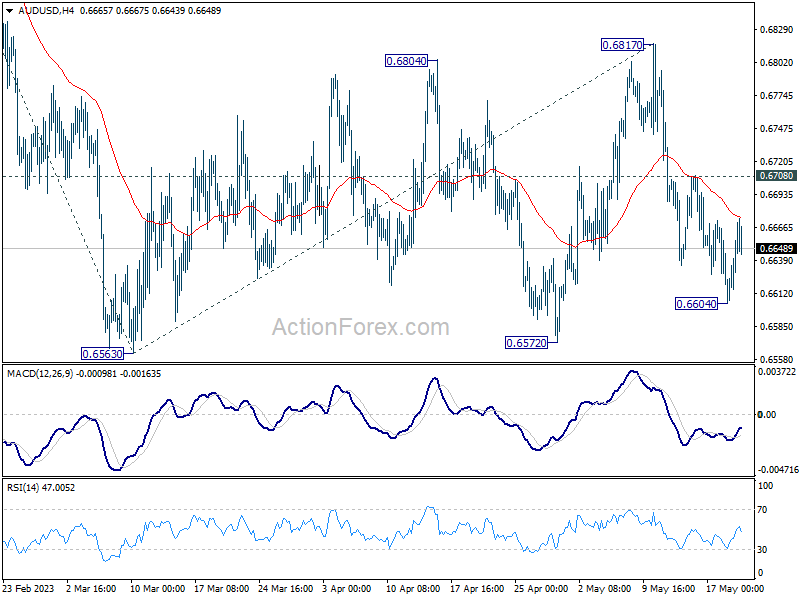

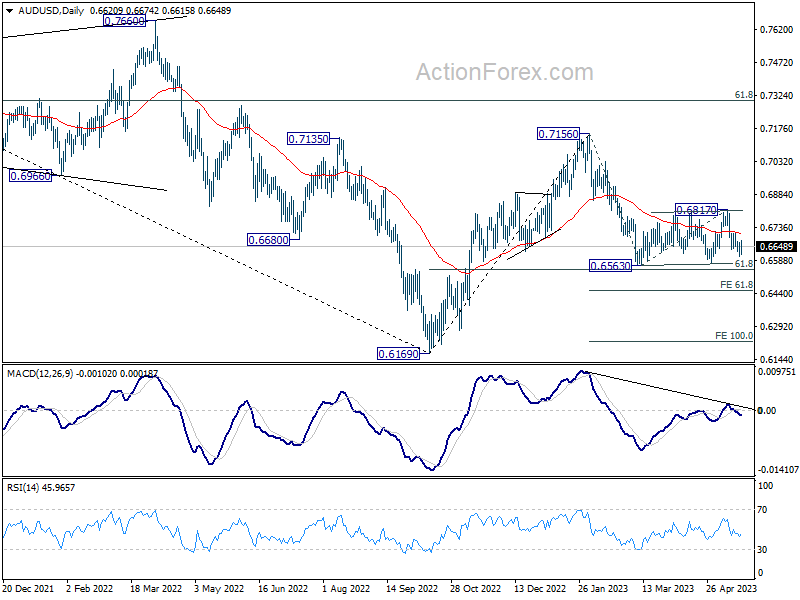

AUD/USD recovered after hitting 0.6604 last week. Intraday bias is turned neutral this week first. Further decline is in favor as long as 0.6708 resistance holds. Below 0.6604 will bring retest of 0.6563 low first. Decisive break there will resume larger decline from 0.7156 to 61.8% projection of 0.7156 to 0.6563 from 0.6817 at 0.6451. . On the upside, above 0.6708 minor resistance will delay the bearish case, and extend the corrective pattern from 0.6563 with another rising leg.

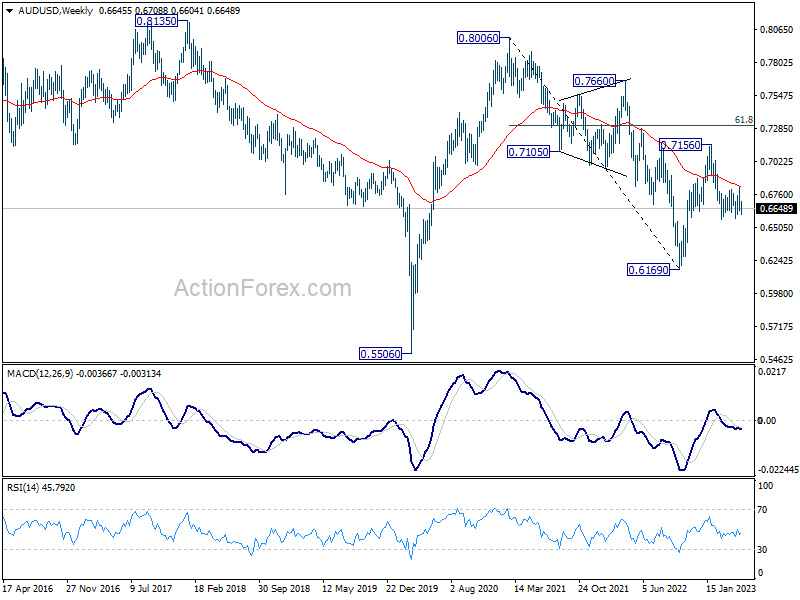

In the bigger picture, the failure to break through 55 W EMA (now at 0.6822) keeps medium term outlook bearish. Firm break of 61.8% retracement of 0.6169 to 0.7156 at 0.6546 will raise the chance of long term down trend resumption through 0.6169 low. This will now be the favored case as long as 0.6817 resistance holds.

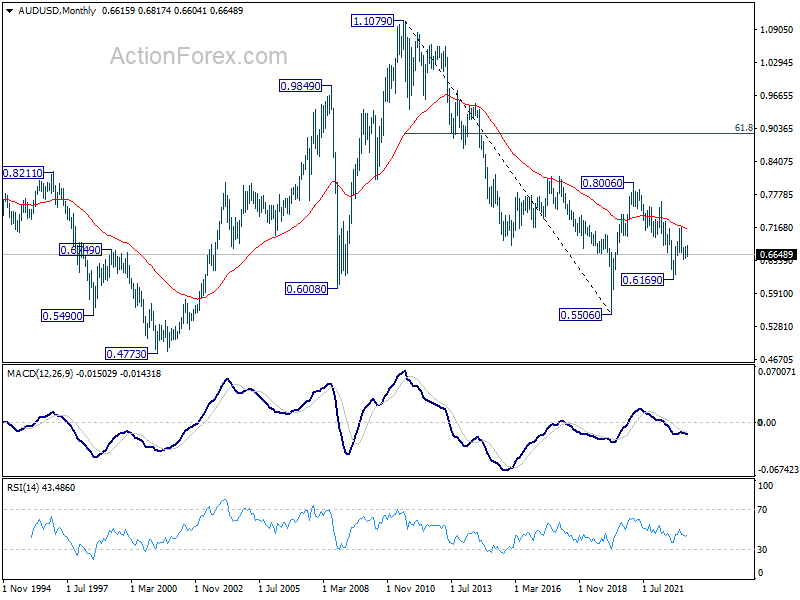

In the long term picture, initial rejection by 55 M EMA (now at 0.7128) retains long term bearishness. That is, down trend from 1.1079 (2011 high) could still resume through 0.5506 (2020 low) on resumption.

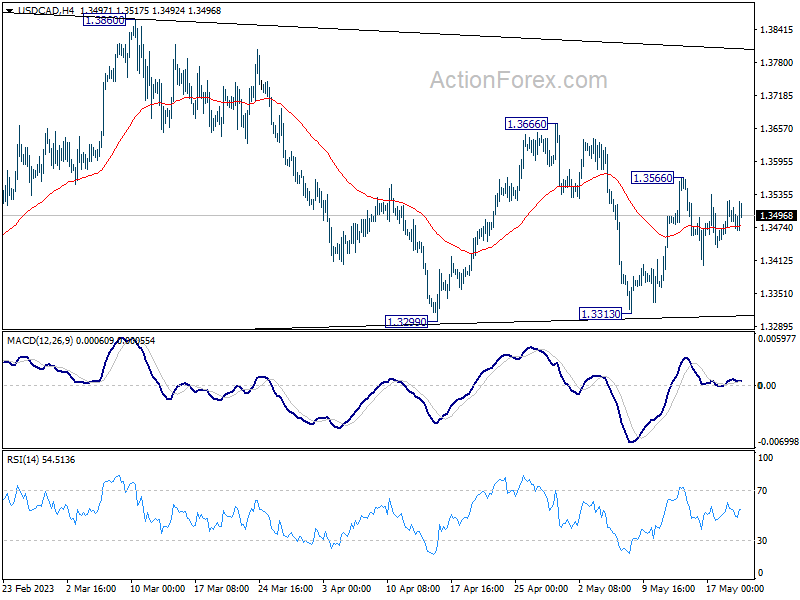

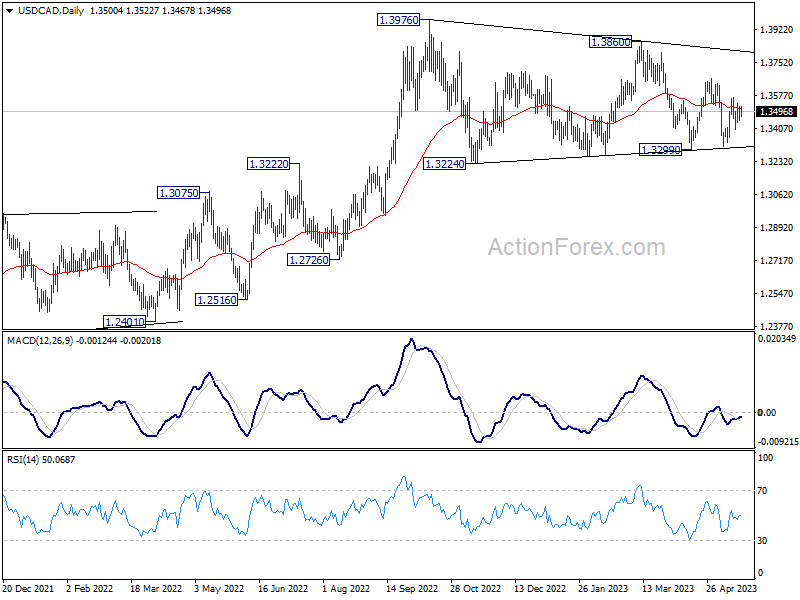

USD/CAD Weekly Outlook

USD/CAD's stayed in range between 1.3313/3566 last week and outlook is unchanged. Overall, the pair is seen as extending the triangle consolidation pattern from 1.3976. Above 1.3566 will resume the rebound from 1.3313 towards 1.3666 resistance and then 1.3860. However, firm break of 1.3313 support will invalidate this view and indicate that deeper correction is underway.

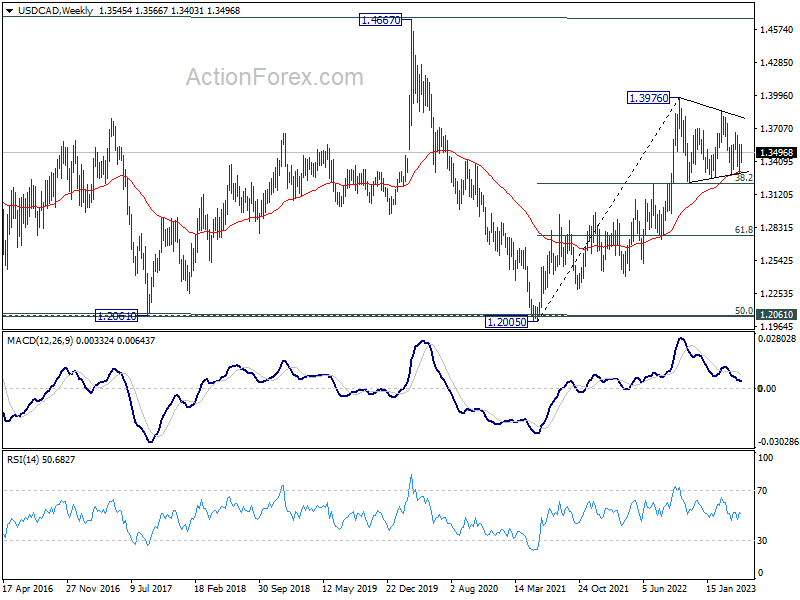

In the bigger picture, as long as 55 W EMA (now at 1.3327) holds, up trend from 1.2005 (2021 low) is still in favor to resume through 1.3976 at a later stage. However, sustained trading below the EMA and 38.2% retracement of 1.2005 to 1.3976 at 1.3233 will raise the chance of bearish reversal. Deeper should then be seen to 61.8% retracement at 1.2758 next.

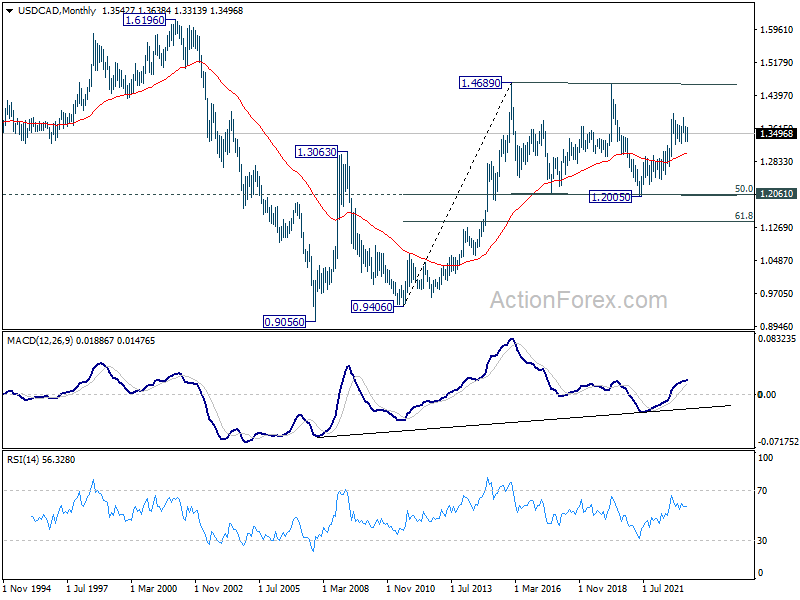

In the longer term picture, price actions from 1.4689 (2016 high) are seen as a consolidation pattern only, which might have completed at 1.2005. That is, up trend from 0.9506 (2007 low) is expected to resume at a later stage. This will remain the favored case as 55 M EMA (now at 1.3031) holds.

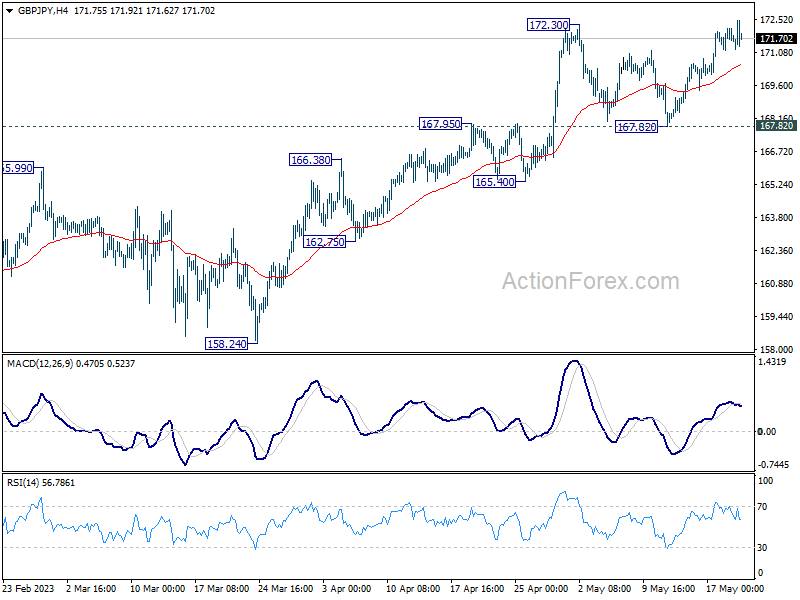

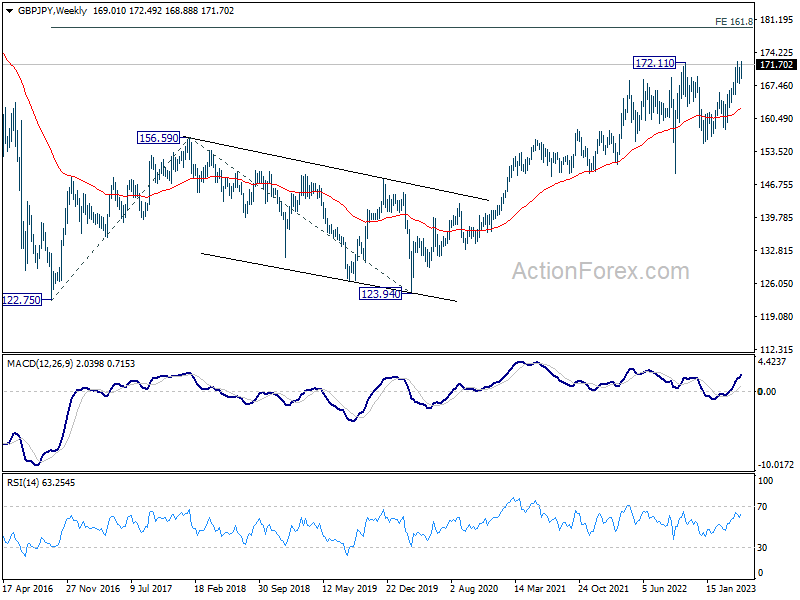

GBP/JPY Weekly Outlook

GBP/JPY's breach of 172.30 resistance last week argues that larger up trend is resuming. Initial bias is mildly on the upside this week. Next target is 100% projection of 148.93 to 172.11 from 155.33 at 178.51. For now, outlook will stay bullish as long as 167.82 support holds, in case of retreat.

In the bigger picture, focus stays on 172.11 resistance (2022 high). Decisive break there will resume whole up trend from 123.94 (2020 low). Next target will be 161.8% projection of 122.75 (2016 low) to 156.59 (2018 high) from 123.94 at 178.69. Nevertheless, firm break of 167.82 support will indicate rejection by 172.11 and extend the corrective pattern from there with another falling leg.

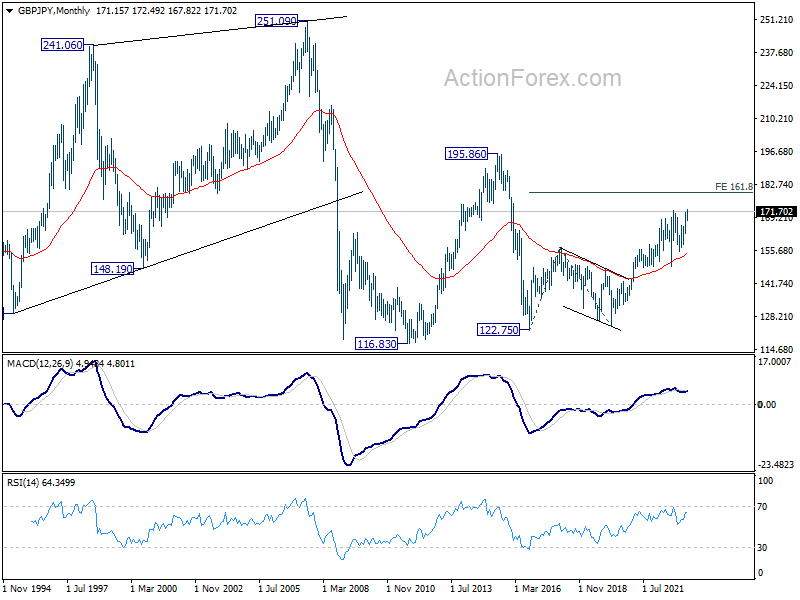

In the longer term picture, as long as 55 M EMA (now at 154.46) holds, rise from 122.75 (2016 low) could still extend higher at a later stage to 195.86 (2015 high).

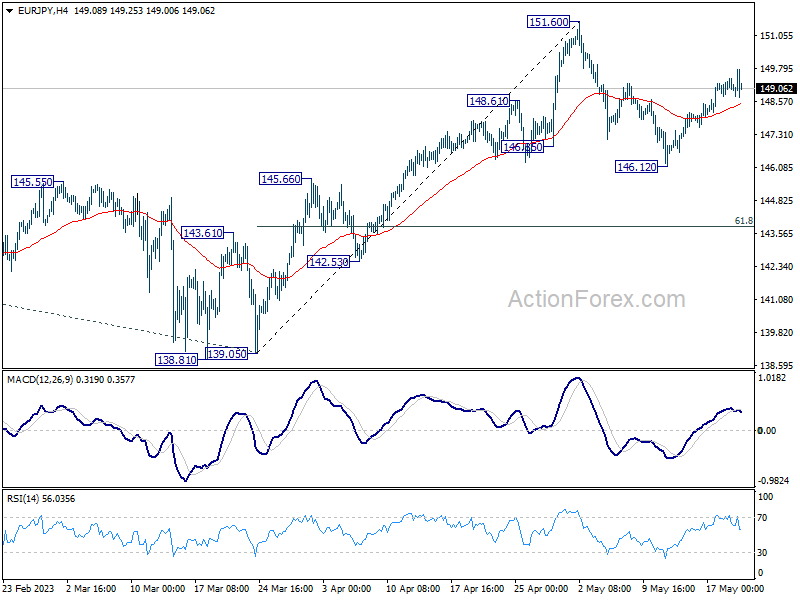

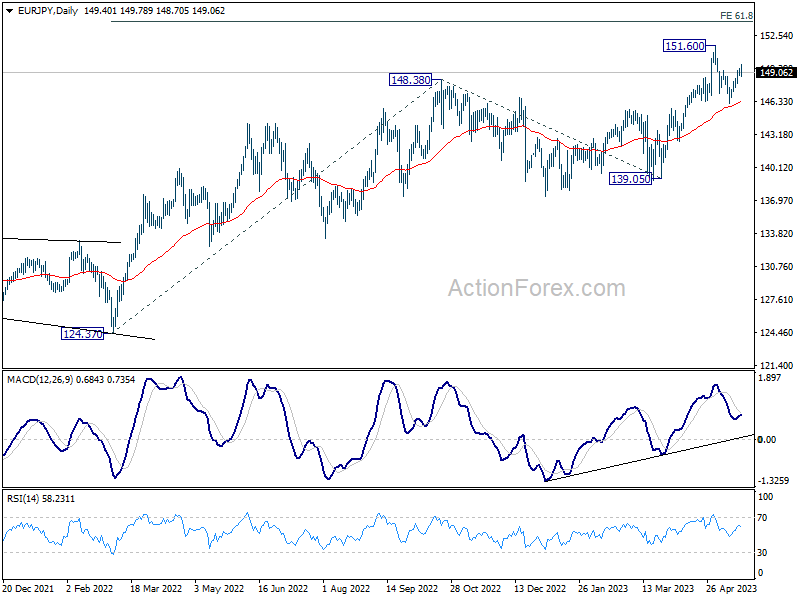

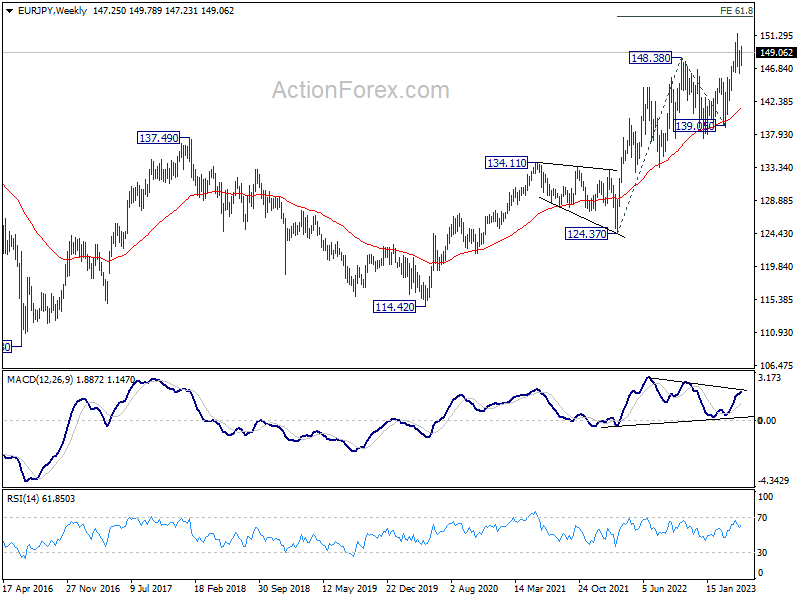

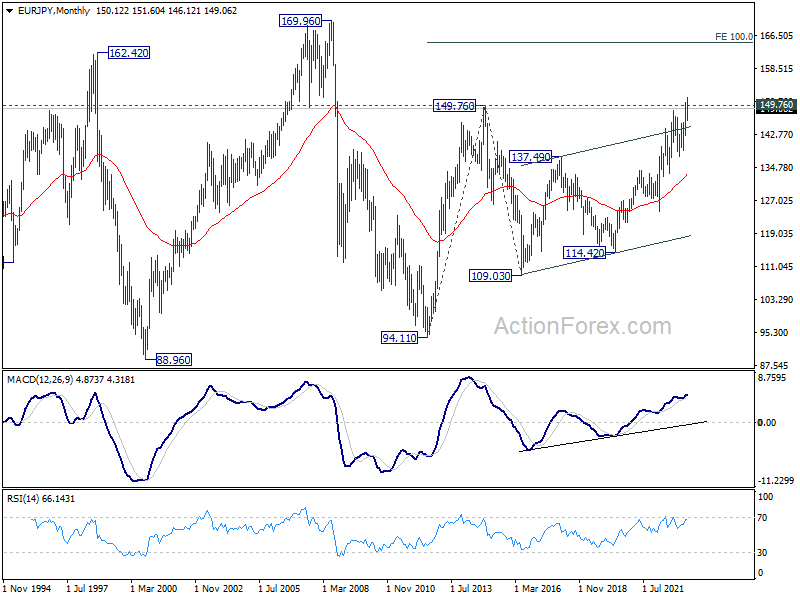

EUR/JPY Weekly Outlook

EUR/JPY's rebound from 146.12 extended higher last week and the development argues that pull back from 151.60 has completed. Initial bias is mildly on the upside this week for retesting 151.60. Decisive break there will resume larger up trend. On the downside, however, break of 146.12 will resume the fall to 61.8% retracement of 139.05 to 151.60 at 143.84.

In the bigger picture, rise from 114.42 (2020 low) is in progress. Next target is 61.8% projection of 124.37 to 148.38 from 138.81 at 153.64. Sustained break there will pave the way to 100% projection at 162.82. For now, medium term outlook will remain bullish as long as 139.05 support holds, even in case of deep pull back.

In the long term picture, break of 149.76 (2014 high) argues that whole up trend form 94.11 (2012 low) is resuming. Sustained trading above 149.76 will pave the way to 100% projection of 94.11 to 149.76 from 109.03 at 164.68, which is close to 169.96 (2008 high).

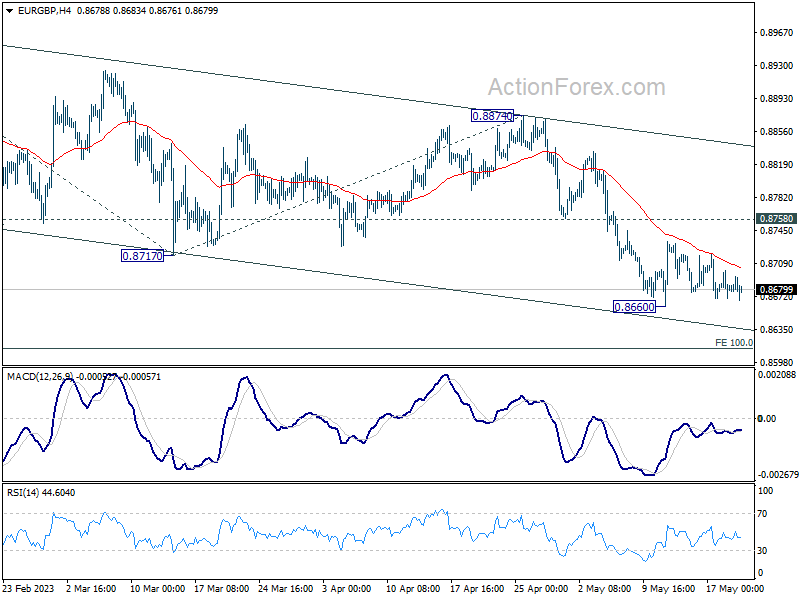

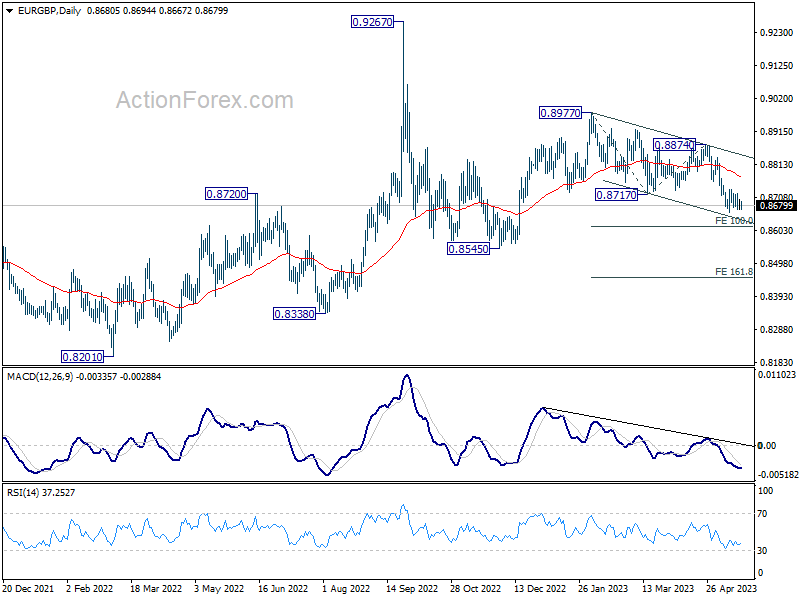

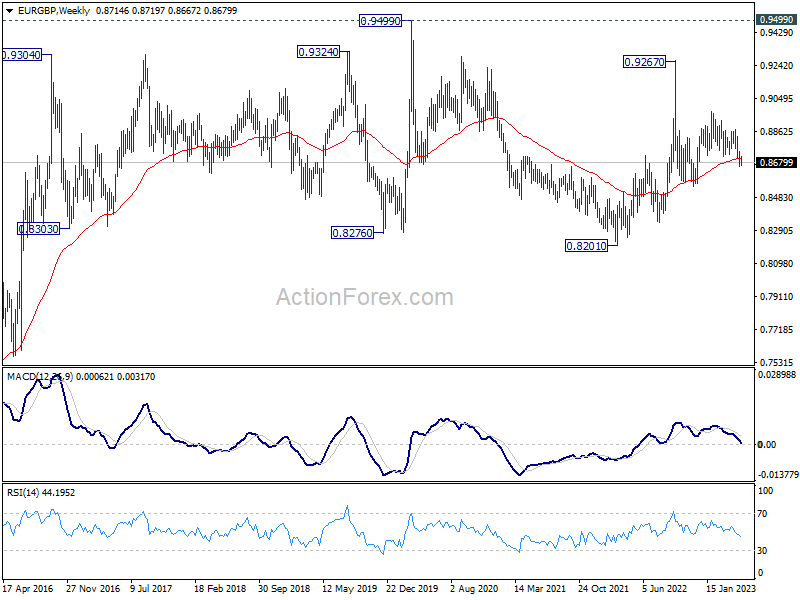

EUR/GBP Weekly Outlook

EUR/GBP stayed in consolidation above 0.8660 last week and outlook is unchanged. Initial bias remains neutral this week first. Further decline is expected as long as 0.8758 resistance holds. On the downside, break of 0.8660 will resume recent decline from 0.8977 to 100% projection of 0.8977 to 0.8717 from 0.8874 at 0.8614. Nevertheless, break of 0.8758 minor resistance will turn bias back to the upside for stronger rebound.

In the bigger picture, current development argues that whole decline from 0.9267 (2022 high) is still in progress. This is part of the long term range pattern from 0.9499 (2020 high). Deeper fall would be seen through 0.8545 support. This will now remain the favored case as long as 0.8874 resistance holds.

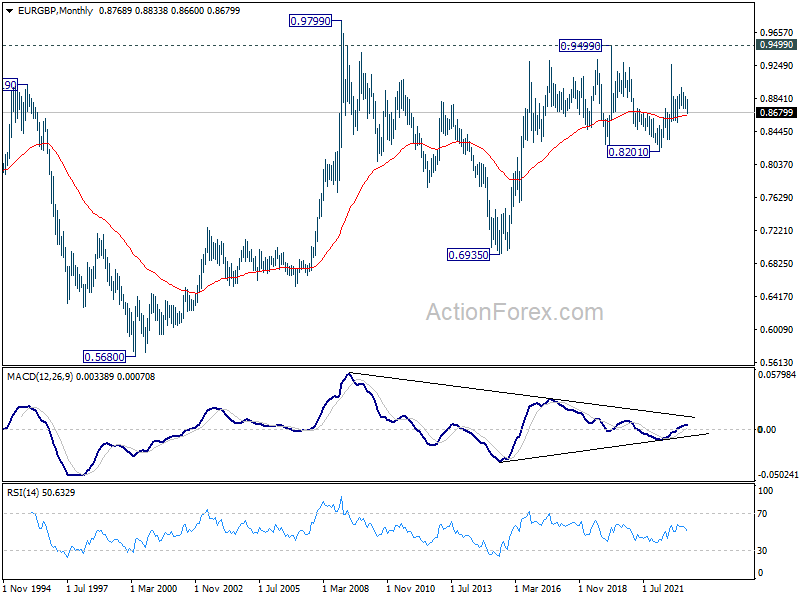

In the long term picture, long term range pattern is extending. But rise from 0.6935 (2015 low) is expected to extend at a later stage, to 0.9799 (2009 high).

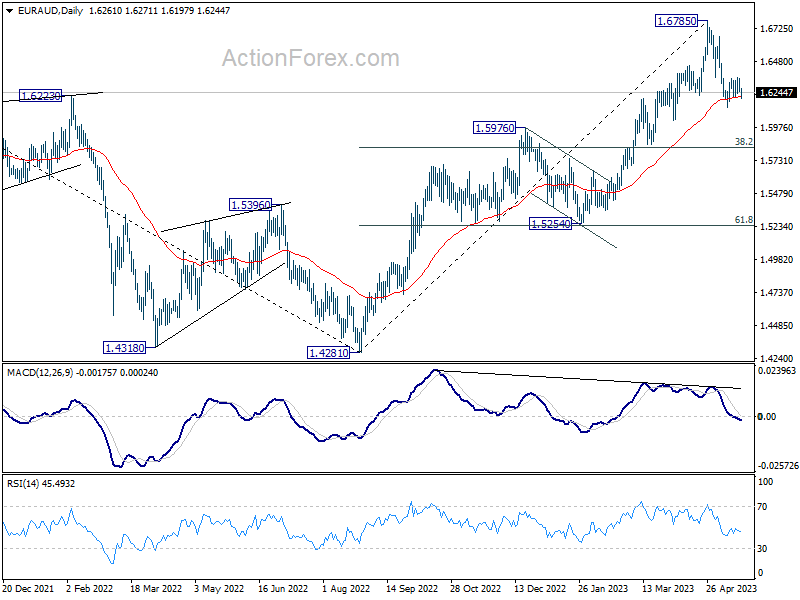

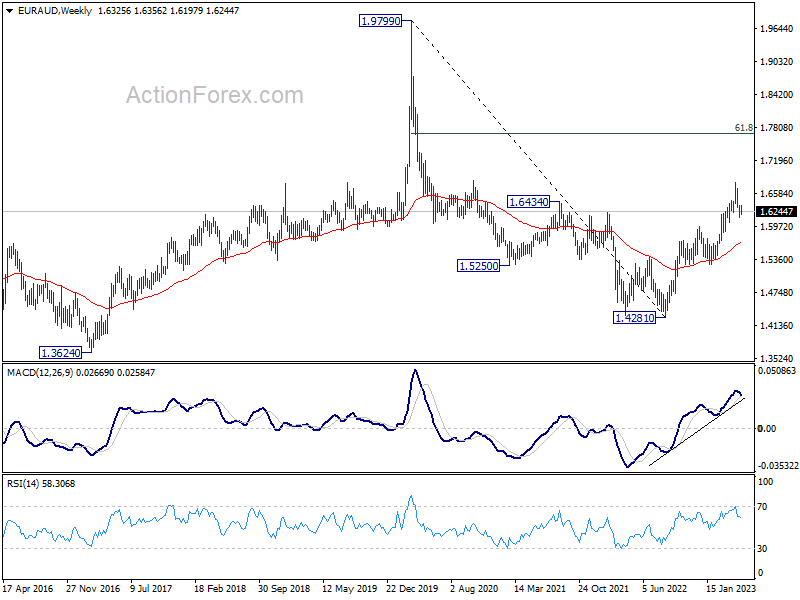

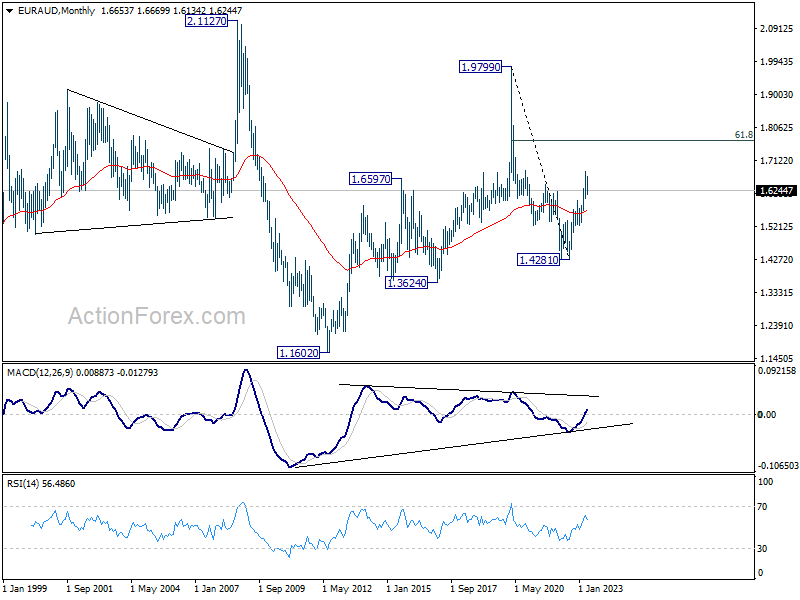

EUR/AUD Weekly Outlook

EUR/AUD stayed in consolidation above 1.6134 last week and outlook is unchanged. Initial bias stays neutral this week first. Fall from 1.6785 might be a correction to whole up trend from 1.4281. Break of 1.6134 will target 38.2 retracement of 1.4281 to 1.6785 at 1.5828, which is inside 1.5254/5976 support zone. Nevertheless, sustained break of 1.6354 minor resistance will turn bias back to the upside for retesting 1.6785 high instead.

In the bigger picture, whole down trend from 1.9799 (2020 high) should have completed at 1.4281 (2022 low). Further rise should be seen to 61.8% retracement of 1.9799 to 1.4281 at 1.7691 next. For now, outlook will stay bullish as long as 1.5976 resistance turned support holds, even in case of deep pull back.

In the longer term picture, it's still early to decide if rise from 1.4281 is resuming whole up trend from 1.1602 (2012 low). Attention will be paid on the structure on the current rally to make an assessment later.

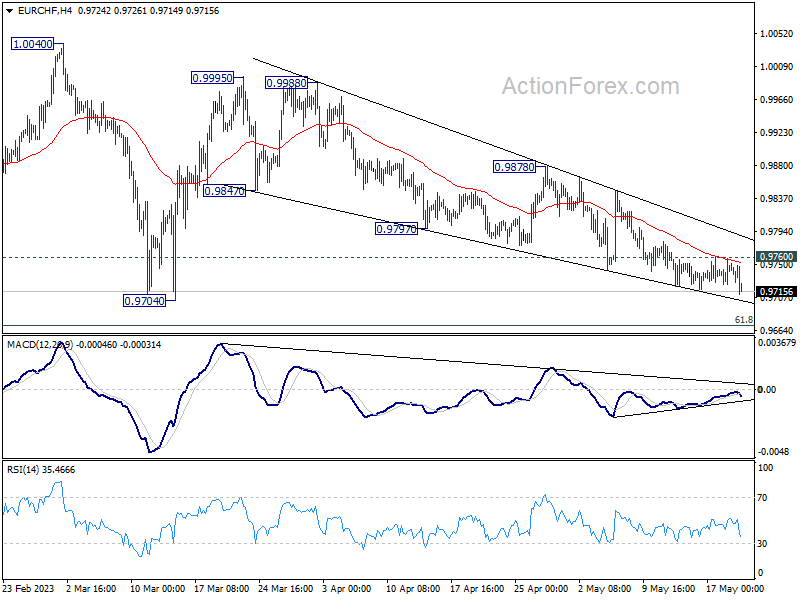

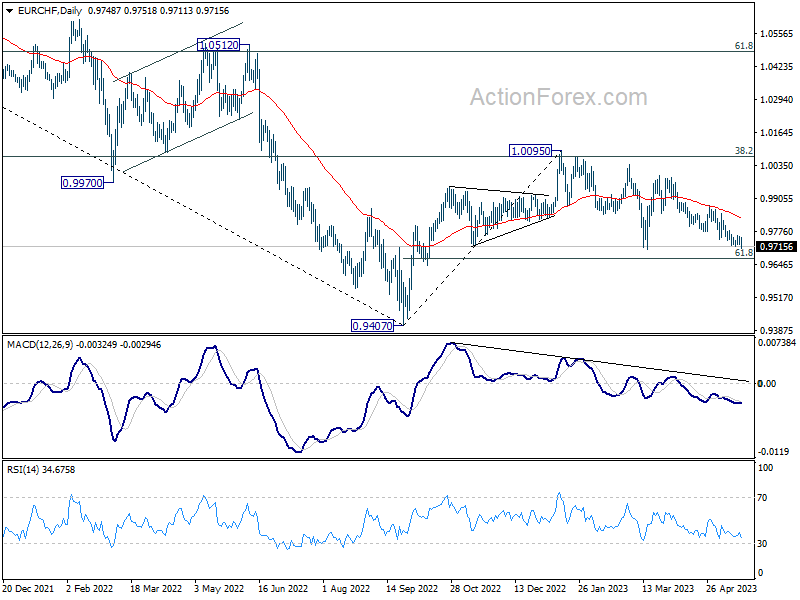

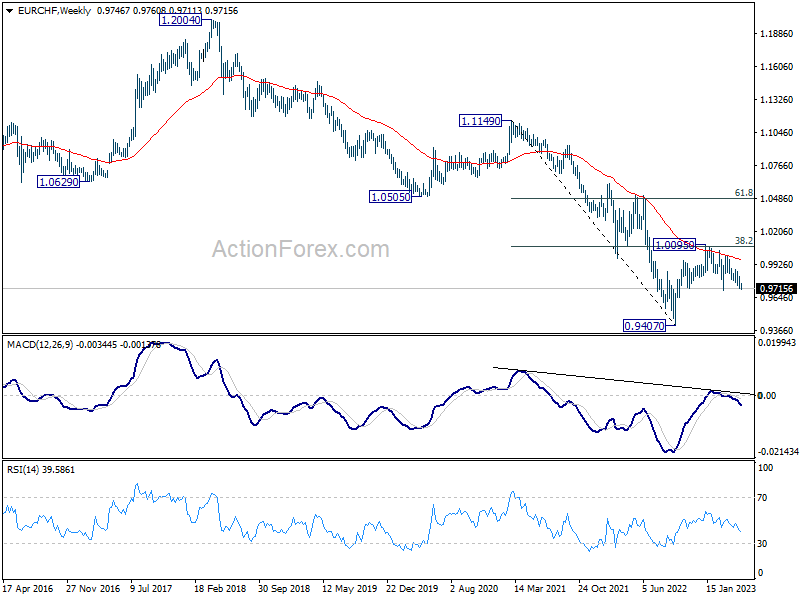

EUR/CHF Weekly Outlook

EUR/CHF's decline from 0.9995 extended lower last week without clear sign of bottoming. This decline now looks more likely part of the whole corrective pattern from 1.0095. But even so, considering bullish convergence condition in 4H MACD, downside should be contained by 61.8% retracement of 0.9407 to 1.0095 at 0.9670. On the upside, break of 0.9760 resistance should confirm short term bottoming and turn bias back to the upside for stronger rebound.

In the bigger picture, prior rejection by 38.2% retracement of 1.1149 to 0.9407 at 1.0072 suggests that medium term outlook is staying bearish. The pair is also capped below 55 W EMA (now at 0.9963). Down trend from 1.2004 is not completed yet and is in favor to resume through 0.9407 at a later stage. However, decisive break of 1.0095 resistance will raise the chance of bullish trend reversal. Rise from 0.9407 should then target 1.0505 cluster resistance (2020 low at 1.0505, 61.8% retracement of 1.1149 to 0.9407 at 1.1484).

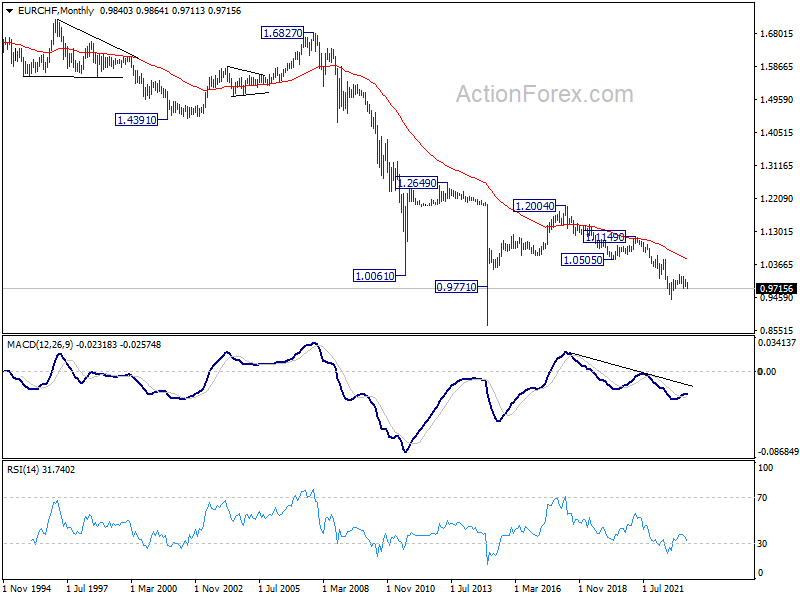

In the long term picture, it's still way too early too call for bullish trend reversal with upside capped well below 55 M EMA (now at 1.0515) and 1.0505 support turned resistance (2020 low). The multi-decade down trend could still continue.

Summary 5/22 – 5/26

Monday, May 22, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:50 | JPY | Machinery Orders M/M Mar | 0.70% | -4.50% |

| 10:00 | EUR | German Buba Monthly Report | ||

| 14:00 | EUR | Eurozone Consumer Confidence May P | -17 | -18 |

| 23:00 | AUD | Manufacturing PMI May P | 48 | |

| 23:00 | AUD | Services PMI May P | 53.7 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:50 | JPY | Machinery Orders M/M Mar | |

| Forecast: 0.70% | Previous: -4.50% | ||

| 10:00 | EUR | German Buba Monthly Report | |

| Forecast: | Previous: | ||

| 14:00 | EUR | Eurozone Consumer Confidence May P | |

| Forecast: -17 | Previous: -18 | ||

| 23:00 | AUD | Manufacturing PMI May P | |

| Forecast: | Previous: 48 | ||

| 23:00 | AUD | Services PMI May P | |

| Forecast: | Previous: 53.7 | ||

Tuesday, May 23, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI May P | 49.5 | |

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Apr | 17.5B | 20.7B |

| 07:15 | EUR | France Manufacturing PMI May P | 46.1 | 45.6 |

| 07:15 | EUR | France Services PMI May P | 54.3 | 54.6 |

| 07:30 | EUR | Germany Manufacturing PMI May P | 45.2 | 44.5 |

| 07:30 | EUR | Germany Services PMI May P | 55.5 | 56 |

| 08:00 | EUR | Eurozone Manufacturing PMI May P | 46.2 | 45.8 |

| 08:00 | EUR | Eurozone Services PMI May P | 55.6 | 56.2 |

| 08:00 | EUR | Current Account (EUR) Mar | 20.2B | 24.3B |

| 08:30 | GBP | Manufacturing PMI May P | 48.2 | 47.8 |

| 08:30 | GBP | Services PMI May P | 55.5 | 55.9 |

| 12:30 | CAD | Industrial Product Price M/M Apr | 0.20% | 0.10% |

| 12:30 | CAD | Raw Material Price Index Apr | 0.70% | -1.70% |

| 13:45 | USD | Manufacturing PMI May P | 50.0 | 50.2 |

| 13:45 | USD | Services PMI May P | 53.6 | 53.6 |

| 13:45 | USD | Composite PMI May P | 50 | 53.4 |

| 14:00 | USD | New Home Sales Apr | 665K | 683K |

| 22:45 | NZD | Retail Sales Q/Q Q1 | -0.60% | |

| 22:45 | NZD | Retail Sales ex Autos Q/Q Q1 | -1.30% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI May P | |

| Forecast: | Previous: 49.5 | ||

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Apr | |

| Forecast: 17.5B | Previous: 20.7B | ||

| 07:15 | EUR | France Manufacturing PMI May P | |

| Forecast: 46.1 | Previous: 45.6 | ||

| 07:15 | EUR | France Services PMI May P | |

| Forecast: 54.3 | Previous: 54.6 | ||

| 07:30 | EUR | Germany Manufacturing PMI May P | |

| Forecast: 45.2 | Previous: 44.5 | ||

| 07:30 | EUR | Germany Services PMI May P | |

| Forecast: 55.5 | Previous: 56 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI May P | |

| Forecast: 46.2 | Previous: 45.8 | ||

| 08:00 | EUR | Eurozone Services PMI May P | |

| Forecast: 55.6 | Previous: 56.2 | ||

| 08:00 | EUR | Current Account (EUR) Mar | |

| Forecast: 20.2B | Previous: 24.3B | ||

| 08:30 | GBP | Manufacturing PMI May P | |

| Forecast: 48.2 | Previous: 47.8 | ||

| 08:30 | GBP | Services PMI May P | |

| Forecast: 55.5 | Previous: 55.9 | ||

| 12:30 | CAD | Industrial Product Price M/M Apr | |

| Forecast: 0.20% | Previous: 0.10% | ||

| 12:30 | CAD | Raw Material Price Index Apr | |

| Forecast: 0.70% | Previous: -1.70% | ||

| 13:45 | USD | Manufacturing PMI May P | |

| Forecast: 50.0 | Previous: 50.2 | ||

| 13:45 | USD | Services PMI May P | |

| Forecast: 53.6 | Previous: 53.6 | ||

| 13:45 | USD | Composite PMI May P | |

| Forecast: 50 | Previous: 53.4 | ||

| 14:00 | USD | New Home Sales Apr | |

| Forecast: 665K | Previous: 683K | ||

| 22:45 | NZD | Retail Sales Q/Q Q1 | |

| Forecast: | Previous: -0.60% | ||

| 22:45 | NZD | Retail Sales ex Autos Q/Q Q1 | |

| Forecast: | Previous: -1.30% | ||

Wednesday, May 24, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Westpac Leading Index M/M Apr | 0.00% | |

| 02:00 | NZD | RBNZ Rate Decision | 5.50% | 5.25% |

| 03:00 | NZD | RBNZ Press Conference | ||

| 06:00 | GBP | CPI M/M Apr | 1.70% | 0.80% |

| 06:00 | GBP | CPI Y/Y Apr | 8.20% | 10.10% |

| 06:00 | GBP | Core CPI Y/Y Apr | 6.20% | 6.20% |

| 06:00 | GBP | RPI M/M Apr | 1.70% | 0.70% |

| 06:00 | GBP | RPI Y/Y Apr | 11.20% | 13.50% |

| 06:00 | GBP | PPI Input M/M Apr | -0.50% | 0.20% |

| 06:00 | GBP | PPI Input Y/Y Apr | 3.80% | 7.60% |

| 06:00 | GBP | PPI Output M/M Apr | -0.10% | 0.10% |

| 06:00 | GBP | PPI Output Y/Y Apr | 7.40% | 8.70% |

| 06:00 | GBP | PPI Core Output M/M Apr | 0.10% | 0.30% |

| 06:00 | GBP | PPI Core Output Y/Y Apr | 7.30% | 8.50% |

| 08:00 | EUR | Germany IFO Business Climate May | 93.4 | 93.6 |

| 08:00 | EUR | Germany IFO Current Assessment May | 95.2 | 95 |

| 08:00 | EUR | Germany IFO Expectations May | 91.7 | 92.2 |

| 14:30 | USD | Crude Oil Inventories | 5.0M | |

| 18:00 | USD | FOMC Minutes |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Westpac Leading Index M/M Apr | |

| Forecast: | Previous: 0.00% | ||

| 02:00 | NZD | RBNZ Rate Decision | |

| Forecast: 5.50% | Previous: 5.25% | ||

| 03:00 | NZD | RBNZ Press Conference | |

| Forecast: | Previous: | ||

| 06:00 | GBP | CPI M/M Apr | |

| Forecast: 1.70% | Previous: 0.80% | ||

| 06:00 | GBP | CPI Y/Y Apr | |

| Forecast: 8.20% | Previous: 10.10% | ||

| 06:00 | GBP | Core CPI Y/Y Apr | |

| Forecast: 6.20% | Previous: 6.20% | ||

| 06:00 | GBP | RPI M/M Apr | |

| Forecast: 1.70% | Previous: 0.70% | ||

| 06:00 | GBP | RPI Y/Y Apr | |

| Forecast: 11.20% | Previous: 13.50% | ||

| 06:00 | GBP | PPI Input M/M Apr | |

| Forecast: -0.50% | Previous: 0.20% | ||

| 06:00 | GBP | PPI Input Y/Y Apr | |

| Forecast: 3.80% | Previous: 7.60% | ||

| 06:00 | GBP | PPI Output M/M Apr | |

| Forecast: -0.10% | Previous: 0.10% | ||

| 06:00 | GBP | PPI Output Y/Y Apr | |

| Forecast: 7.40% | Previous: 8.70% | ||

| 06:00 | GBP | PPI Core Output M/M Apr | |

| Forecast: 0.10% | Previous: 0.30% | ||

| 06:00 | GBP | PPI Core Output Y/Y Apr | |

| Forecast: 7.30% | Previous: 8.50% | ||

| 08:00 | EUR | Germany IFO Business Climate May | |

| Forecast: 93.4 | Previous: 93.6 | ||

| 08:00 | EUR | Germany IFO Current Assessment May | |

| Forecast: 95.2 | Previous: 95 | ||

| 08:00 | EUR | Germany IFO Expectations May | |

| Forecast: 91.7 | Previous: 92.2 | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 5.0M | ||

| 18:00 | USD | FOMC Minutes | |

| Forecast: | Previous: | ||

Thursday, May 25, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 06:00 | EUR | Germany Gfk Consumer Confidence Jun | -24.5 | -25.7 |

| 06:00 | EUR | Germany GDP Q/Q Q1 F | 0% | 0% |

| 12:30 | USD | Initial Jobless Claims (May 19) | 253K | 242K |

| 12:30 | USD | Initial Jobless Claims 4-week average (May 19) | 244.25K | |

| 12:30 | USD | Continuing Jobless Claims (May 12) | 1.806M | 1.799M |

| 12:30 | USD | GDP Price Index Q1 P | 4% | 4% |

| 12:30 | USD | GDP Annualized Q1 P | 1.10% | 1.10% |

| 14:00 | USD | Pending Home Sales M/M Apr | 1.20% | -5.20% |

| 14:30 | USD | Natural Gas Storage | 99B | |

| 23:30 | JPY | Tokyo CPI Core Y/Y May | 3.40% | 3.50% |

| 23:50 | JPY | Corporate Service Price Index Y/Y Apr | 1.40% | 1.60% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 06:00 | EUR | Germany Gfk Consumer Confidence Jun | |

| Forecast: -24.5 | Previous: -25.7 | ||

| 06:00 | EUR | Germany GDP Q/Q Q1 F | |

| Forecast: 0% | Previous: 0% | ||

| 12:30 | USD | Initial Jobless Claims (May 19) | |

| Forecast: 253K | Previous: 242K | ||

| 12:30 | USD | Initial Jobless Claims 4-week average (May 19) | |

| Forecast: | Previous: 244.25K | ||

| 12:30 | USD | Continuing Jobless Claims (May 12) | |

| Forecast: 1.806M | Previous: 1.799M | ||

| 12:30 | USD | GDP Price Index Q1 P | |

| Forecast: 4% | Previous: 4% | ||

| 12:30 | USD | GDP Annualized Q1 P | |

| Forecast: 1.10% | Previous: 1.10% | ||

| 14:00 | USD | Pending Home Sales M/M Apr | |

| Forecast: 1.20% | Previous: -5.20% | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 99B | ||

| 23:30 | JPY | Tokyo CPI Core Y/Y May | |

| Forecast: 3.40% | Previous: 3.50% | ||

| 23:50 | JPY | Corporate Service Price Index Y/Y Apr | |

| Forecast: 1.40% | Previous: 1.60% | ||

Friday, May 26, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Retail Sales M/M Apr | 0.30% | 0.40% |

| 06:00 | GBP | Retail Sales M/M Apr | 0.00% | -0.90% |

| 12:30 | USD | Durable Goods Orders Apr | -0.90% | 3.20% |

| 12:30 | USD | Durable Goods Orders ex Transportation Apr | 0.00% | 0.20% |

| 12:30 | USD | Personal Income M/M Apr | 0.40% | 0.30% |

| 12:30 | USD | Personal Spending M/M Apr | 0.40% | 0.00% |

| 12:30 | USD | PCE Price Index M/M Apr | 0.40% | 0.10% |

| 12:30 | USD | PCE Price Index Y/Y Apr | 3.90% | 4.20% |

| 12:30 | USD | Core PCE Price Index M/M Apr | 0.40% | 0.30% |

| 12:30 | USD | Core PCE Price Index Y/Y Apr | 5.00% | 4.60% |

| 12:30 | USD | Goods Trade Balance (USD) Apr P | -85.6B | -84.6B |

| 12:30 | USD | Wholesale Inventories Apr P | 0.10% | 0.00% |

| 14:00 | USD | Michigan Consumer Sentiment Index May F | 58.2 | 57.7 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Retail Sales M/M Apr | |

| Forecast: 0.30% | Previous: 0.40% | ||

| 06:00 | GBP | Retail Sales M/M Apr | |

| Forecast: 0.00% | Previous: -0.90% | ||

| 12:30 | USD | Durable Goods Orders Apr | |

| Forecast: -0.90% | Previous: 3.20% | ||

| 12:30 | USD | Durable Goods Orders ex Transportation Apr | |

| Forecast: 0.00% | Previous: 0.20% | ||

| 12:30 | USD | Personal Income M/M Apr | |

| Forecast: 0.40% | Previous: 0.30% | ||

| 12:30 | USD | Personal Spending M/M Apr | |

| Forecast: 0.40% | Previous: 0.00% | ||

| 12:30 | USD | PCE Price Index M/M Apr | |

| Forecast: 0.40% | Previous: 0.10% | ||

| 12:30 | USD | PCE Price Index Y/Y Apr | |

| Forecast: 3.90% | Previous: 4.20% | ||

| 12:30 | USD | Core PCE Price Index M/M Apr | |

| Forecast: 0.40% | Previous: 0.30% | ||

| 12:30 | USD | Core PCE Price Index Y/Y Apr | |

| Forecast: 5.00% | Previous: 4.60% | ||

| 12:30 | USD | Goods Trade Balance (USD) Apr P | |

| Forecast: -85.6B | Previous: -84.6B | ||

| 12:30 | USD | Wholesale Inventories Apr P | |

| Forecast: 0.10% | Previous: 0.00% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index May F | |

| Forecast: 58.2 | Previous: 57.7 | ||

Weekly Economic & Financial Commentary: Fractures on FOMC Emerge

Summary

United States: Recession Is Taking Its Time

- Economic data continue to suggest the U.S. economy is only gradually losing momentum. Consumers continue to spend, and industrial and housing activity are seeing some stabilization. We still view a recession is more likely than not by year-end, but there is no denying the underlying resiliency evident in the data.

- Next week: New Home Sales (Tue), Personal Income & Spending (Fri), Durable Goods (Fri)

International: Mixed Trends for Key Asian Economies

- China's retail sales and industrial output firmed markedly in April, boosted by favorable base effects. However, those activity readings still came in below the consensus forecast and hint at a possible waning in momentum of China's recovery. In Japan, Q1 GDP rose by 1.6% quarter-over-quarter annualized, more than expected. Consumer spending and business capital spending both rose as well, while Japan's April CPI also quickened.

- Next week: Eurozone PMIs (Tue), RBNZ Policy Rate (Wed), U.K. CPI (Wed)

Credit Market Insights: Picking Up the Pieces of the Pandemic Refi Boom

- The Federal Reserve Bank of New York's Quarterly Report on Household Debt and Credit found U.S. aggregate household debt balances rose by $148 billion in Q1-2023. Mortgage debt advanced by just $121 billion in Q1. Mortgage originations for both purchases and refinancing also fell sharply in Q1 to $324 billion, the lowest level since Q2-2014. The historic pandemic-era refinancing boom has tapered off, but its effects will be felt for some time.

Topic of the Week: Fractures on FOMC Emerge

- A majority of Federal Open Market Committee (FOMC) voters made public appearances this week. Policymaker comments are particularly important in assessing the Fed's path after the May meeting language signaled a data-dependent, month-to-month Fed from now on. The consensus around the Fed's next steps appears to be fractured.

Week Ahead – Debt Ceiling Drama, Turkish Rate Decision Pre-Presidential Run-off

US

Wall Street will remain focused on debt ceiling drama, a plethora of Fed speak, flash PMIs, and bank stress. It will be a busy week filled with economic releases, with most of the attention falling on the first look at the May PMI readings, a second look at Q1 GDP/Core PCE, New Home Sales, and the FOMC meeting minutes.

Debt ceiling talks are getting close to finalizing a deal, but posturing for the best deal could drag talks out longer.

This week contains five Fed appearances, with Bullard, Bostic, and Barkin speaking on Monday. Logan gives welcoming remarks at a conference on Tuesday. Wednesday is the main event as the Minutes could provide some hints that some policymakers are ready to pause tightening. Any signs that the Fed is likely done with its aggressive tightening campaign may put an end to those wagers that are saying the June meeting is a live one.

Eurozone

In the absence of hard-hitting data, attention will be on the various ECB policymakers making appearances throughout the week including President Lagarde on Wednesday. There’s still a big element of uncertainty over the remainder of the tightening cycle in the eurozone with markets pricing in only one or two more hikes, which given how little progress we’ve seen on core inflation seems optimistic.

On the data front, we have eurozone, German, and French manufacturing and services PMIs on Tuesday followed by German business and consumer surveys on Wednesday and Thursday, respectively.

UK

Next week is big for the UK as we get a selection of data that will give us our first real insight into how much progress is actually being made on inflation. BoE Governor Andrew Bailey has been very confident that this April CPI release will show the first big fall in price pressures, coming one year on from the Ukraine invasion and surge in energy prices. A disappointingly high read could quickly see the expected terminal rate jump back above 5% in the markets. Core inflation is expected to remain stubbornly high.

Also on the agenda is PMI surveys on Tuesday, retail sales on Friday, and appearances from BoE policymakers including Governor Bailey again on Wednesday, providing an immediate opportunity to respond to the inflation data earlier in the day.

Russia

Very little on the calendar next week with CBR officials due to speak at a banking conference on Thursday and PPI inflation being released on Wednesday. Perhaps we’ll get more insight on the next policy move from the central bank with Governor Elvira Nabiullina previously hinting that further cuts are not guaranteed.

South Africa

The SARB is expected to hike the repo rate by another 25 or 50 basis points next week in what may be one of if not the final increase in the tightening cycle. That will obviously depend on whether inflation is continuing to make progress in returning to target with the core CPI already comfortably back in the 3-6% range but the headline is still above. It is expected to slip a little closer though in April, with CPI data on Wednesday seen falling to 7%. PPI data on Thursday could also offer insight into whether further progress is expected over the months ahead.

Turkey

Erdogan outperformed expectations in the Presidential election but fell just short of the 50% required to prevent a run-off on 28 May. Markets didn’t react too favorably to the result as it likely means more years of unconventional policy action from the CBRT, high inflation, currency controls, and economic uncertainty.

The CBRT is not expected to cut the repo rate again when it meets on Thursday but would anyone really be surprised if we do see another cut just before the run-off? One final policy push to serve as a reminder to voters that Erdogan is a leader that delivers low-interest rates, whatever the cost.

Switzerland

A very quiet week with employment data on Friday the only release of note.

China

A rather quiet week in terms of economic data releases; we will have the PBoC decision on Monday on its key 1-year and 5-year loan prime rates that are used to benchmark corporate, consumer loans, and home mortgages respectively. The baseline expectation is no change for both the 1-year at 3.65% and the 5-year at 4.3% for the 9th consecutive month as it has left the 1-year medium-term lending facility (MLF) rate unchanged last week at 2.75%; the last cut on the 1-year MLF rate was implemented in August 2022.

India

No key data

Australia

A couple of key data to watch; the first up will be flash manufacturing and services PMIs for May out on Tuesday. Forecasts are expecting a slight dip in manufacturing activities to 47.6 from 48 in April. If the forecast turns out as expected, it will be the 3rd consecutive month of contraction amid a slowdown in global demand especially from China, one of Australia’s largest trading partners. In contrast, the services PMI is forecasted to remain resilient in May with a reading of 54.1 after it expanded the most in 12 months in April at 53.7.

Secondly, to round up the week, we will have flash retail sales data for April out on Friday where the forecast is expecting a decline of 0.6% month-on-month after a rise of 0.4% recorded in March.

This set of key data will be paramount to determining the health of Australia’s economy and the direction of interest rates after the RBA decided to resume its tightening cycle on 2 May following a pause on its previous April meeting.

Based on the data obtained from the ASX 30-day interbank cash rate futures as of 19 May, the implied expectation is no change in the RBA cash policy rate at 3.85% for the next meeting on 6 June due to recent downbeat employment data.

New Zealand

The key event to watch will be the RBNZ monetary policy decision on Wednesday where the consensus is expecting another 25 basis points point hike on its official cash rate to 5.50%, its 12th consecutive hike if it turns out as expected. The focus will be on the magnitude of the hike as RBNZ defied market expectations of a 25-bps hike and choose to increase by a larger 50-bps in April due to sticky elevated inflationary pressure.

Japan

Several key data to monitor. On Tuesday, both the flash manufacturing and services PMIs are expected to show improvement in May; manufacturing is forecasted to expand to 50.2 from 49.2 printed in April and the services sector is forecasted to show growth for the 9th consecutive month to 55.9 from 55.4 in April.

On Friday, consensus for the leading Tokyo core inflation data (excluding fresh food) for May is expected to slip slightly to 3.3% year-on-year from 3.5% in April. Meanwhile, the core-core inflation for Tokyo is forecasted at 2.3% year-on-year in May, its highest level since July 1992.

If the Tokyo inflation data for May continues to be elevated coupled with upbeat PMIs, it may give the impetus for the BoJ to bring forward the long overdue normalization of its decade-plus of ultra-easy accommodating monetary policy early in the second half of 2023.

Singapore

The key focus will be on inflation data for April out on Tuesday where the consensus is expecting a slight dip in core inflation to 4.7% year-on-year from 5% in March. If it turns out as expected, it will be the second consecutive month of an inflationary growth slowdown. As for the headline inflation rate, where the expectation is a dip to 5.3% year-on-year in April from 5.5% in March.

Industrial production will be up next on Friday where the consensus is expecting a slight improvement in contraction to -3.9% year-on-year in April from -4.2% in March. If it turns out as expected, it will be the 7th consecutive month of contraction due to sluggish external demand.

Economic Calendar

Sunday, May 21

Economic Events

- National Elections in Greece

- US President Biden returns from G-7 summit in Japan.

Monday, May 22

Economic Data/Events

- China loan prime rates

- Eurozone consumer confidence

- Hong Kong CPI

- Japan machinery orders

- Singapore GDP

- Canada observes Victoria Day

- ECB’s Holzmann speaks at the Austrian Central Bank conference in Vienna

- ECB’s Villeroy de Galhau speaks at conference in Paris

- ECB’s Vujcic participates in panel in Zagreb on Safeguarding Financial Stability in the Euro Area, organized by Croatian Finance Ministry and European Stability Mechanism

- Fed’s Bullard speaks in fireside chat at American Gas Association’s Financial Forum

- Fedi’s Bostic and Richmond Fed President Thomas Barkin discuss technology-enabled disruption during a conference on the subject hosted by the Richmond Fed

Tuesday, May 23

Economic Data/Events

- US flash PMI, new home sales

- European Flash PMIs: Eurozone, Germany, France, and the UK

- Mexico international reserves

- Singapore CPI

- The Qatar Economic Forum

- Russian PM Mishustin will lead government delegation to China to attend business forum along with sanctioned tycoons

- ECB’s de Guindos gives keynote address at AFME/OMFIF’s 3rd Annual European Financial Integration Conference in Frankfurt

- ECB’s Muller Muller speaks at Bank of Estonia/IMF news conference in Tallinn

- ECB’s Villeroy de Galhau speaks at AFME/OMFIF’s 3rd Annual European Financial Integration Conference in Frankfurt

- Bundesbank President Nagel participates in panel discussion in Berlin

- Fed’s Logan makes welcoming remarks on day two of a conference on technology-enabled disruption hosted by the Richmond Fed

- Riksbank Governor Thedeen speaks on monetary policy and financial stability

- BOE’s Haskel speaks as a panelist at the Federal Reserve Bank of Richmond technology-enabled disruption conference on the “Uncertainty and prospects for disruptive investments “Market uncertainties and technology investment: The role of intangibles”

Wednesday, May 24

Economic Data/Events

- US FOMC Minutes

- Germany IFO business climate

- South Africa CPI

- UK CPI

- RBNZ interest rate decision: Expected to raise the cash rate by 25 basis points to 5.5%

- RBA’s Jacobs, head of domestic markets, speaks at the Australian Government Fixed Income Forum in Tokyo

- ECB non-policy meeting in Frankfurt

- BOE Gov Bailey delivers a keynote speech at Mansion House Net Zero Delivery Summit

- BOE Gov Bailey speaks at a Wall Street Journal event

Thursday, May 25

Economic Data/Events

- US initial jobless claims, GDP

- Germany GDP

- Mexico trade

- Turkey’s central bank (CBRT) rate decision: Expected to keep the one-week repo rate unchanged at 8.50%

- South Africa’s central bank (SARB) rate decision: Expected to raise rates by 50bps to 8.25%

- Bundesbank President Nagel speaks on the future of Europe in Obbürgen, Switzerland

- ECB’s Villeroy de Galhau speaks at the ICMA conference in Paris

- BOE’s Haskel delivers a speech at Peterson Institute for International Economics in Washington

Friday, May 26

Economic Data/Events

- US consumer income, wholesale inventories, durable goods, University of Michigan consumer sentiment

- Australia retail sales

- Japan Tokyo CPI

- Malaysia CPI

- Mexico GDP

- Singapore industrial production

- ECB’s Vujcic Speaks at 29th Dubrovnik Economic Conference in Croatia. Through May 27

Sovereign Rating Updates

- Spain (Fitch)

- Czech Republic (Moody’s)

- Poland (DBRS)