Sample Category Title

Sunset Market Commentary

Markets

Trading for the new week took a rather slow start today with little in the way from higher profile eco data. German Ifo business climate improved slightly more than expected from 93.2 to 93.6. Assessment of current conditions eased from 95.4 to 95 but this was compensated for by an improved in the expectations index (92.2 from 91.0). The details of the survey were slightly different from the EMU PMI’s last week. The manufacturing index rose as companies turned somewhat more optimistic on future activity. Contrary to the PMI’s, IFO indicated that the uptrend in business climate in the service sector over the recent months came to an end. The trade index also fell slightly. Business climate in construction improved on better expectations. The different nuances between the IFO and the PMI’s didn’t change market dynamics. German Bunds underperform US Treasuries. Comments from ECB’s Wunsch in the FT over the weekend (4.0% ECB depo rate not excluded) probably supported European yields compared to the US. German yields currently add between zero and 2.5 bps (2-y). At the same time, yields on US Treasuries are easing between 2.5 bps (2-y) and 4.5 bps (5-y). 10-y inter-EMU spreads versus Germany mostly were little changed even as rating agencies on Friday brought a reassessed of the rating or the outlook for the likes of Ireland, Italy and Greece. Ireland didn’t profit from the Moody’s rating upgrade from A1 to Aa3 (spread +1 bp). Greece was the exception to the rule (10-y spread narrowing 5 bps) as S&P raised the outlook on the BB+ rating from stable to positive. European equities (Eurostoxx 50 unchanged) stay in consolidation modus near recent/post corona peak levels. US indices also open little changed as markets are awaiting a heavy earnings calendar with several (tech) bellwethers later this week. Oil ($81/b) still struggles not to fall below last week’s low ($80.5 area).

On FX markets, EUR/USD returned north of 1.10 (currently 1.102). The move probably is more due to euro strength, rather than USD weakness as markets understand that the single currency will probably continue to receive ‘hard’ interest rate support at & beyond next week’s policy meeting (cf Wunsch comments), while the Fed will probably take a pause in its tightening cycle. DXY eases slightly (101.55), but USD/JPY even gains modestly (134.55 from 134.16 at the open this morning). EUR/JPY is testing the 148.4 2022 top. Euro strength is also visible in the EUR/GBP cross rate (0.8955 from 0.893 at the start of European dealings). Still cable also gained a few ticks (1.2445). S&P on Friday upwardly revised the UK rating outlook from negative to stable on a better economic and fiscal out outlook. Maybe the BoE will retain/join some of the S&P assessment when it meets on May 11. The UK 2-y yield rises 4.5 bps today, slightly more than EMU/Germany.

News & Views

The Belgian debt agency tapped OLO 85 (€1.15bn 0.8% Jun2028), OLO 97 (€1.37bn 3% Jun2033) and OLO 98 (€1bn 3.3% Jun2054). The combined amount sold was at the upper hand of the targeted €3-3.5bn. The auction bid cover was strong at 2.11 with a skew to strong demand for especially OLO 85. After today’s auction, the Kingdom of Belgium raised €20.42bn in long-term funding YTD, compared with a €45bn OLO funding target (45.38%). The bulk of the amount came from two syndicated deals in January and February (€12bn combined). In its funding plan, the debt agency suggested that a third syndicated deal was likely with the maturity being driven by investor demand and the yield environment. The 10- and 30-yr deals at the start of the year were well flagged.

Belgian business confidence deteriorated slightly in April (-7.8 from -7.6), ending a 4-month recovery. Improvements in business-related services (11.4 from 8.4) and trade (-15.9 from -21.6) were offset by a setback in the manufacturing industry (-12.1 from -10.8) and the building industry (-5.4 from -5). Both the assessment of activity levels and market demand expectations improved in the services sector. The very strong improvement in trade was mainly due to employment expectations and intentions of placing orders. Those very same factors declined in manufacturing. Belgian consumer confidence, released last week, improved from -9 to -6, the highest level in over a year. Belgian inflation and Q1 GDP data will be published respectively on Thursday and on Friday.

US Dollar is Under Pressure Due to the Fed

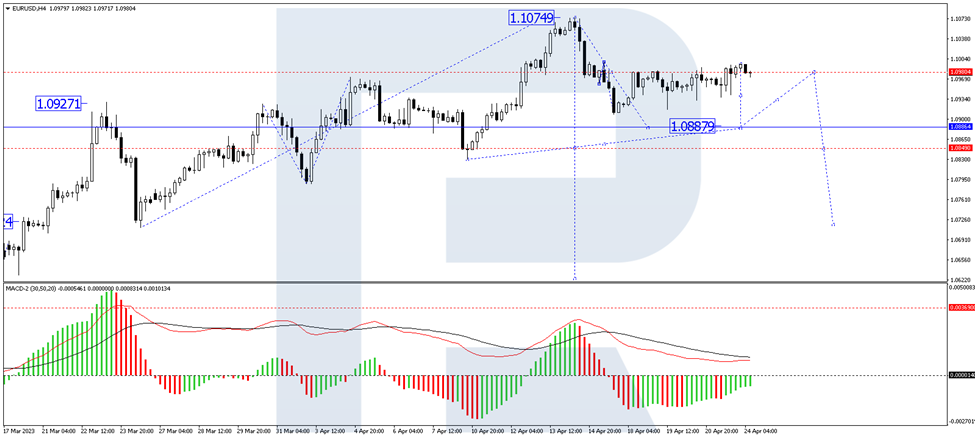

EURUSD started the final week of April with stable moves near 1.0980.

In the near term, the market's focus was on the upcoming US Federal Reserve System meeting, which will end on 3 May. Monetary policymakers are expected to further raise interest rates by 25 base points, although the focus will be on the future rate trajectory.

Investors believe the rate will remain unchanged until July and will drop by the end of the year. However, the state of the US economy might hinder this prediction. The latest statistics have shown that some sectors of the economy remain resilient, and inflation is declining.

The changes in the interest rate by the end of the year might turn out different from market expectations. At the same time, the market moods are quite vigorous.

On the H4 chart, the EURUSD pair has corrected to 1.0995. The market is now forming a consolidation range under this level. The price is expected to break the range downwards and form a descending wave structure to 1.0886. Technically, this scenario is confirmed by the MACD: its signal line is above zero, directed strictly downwards to renew the lows.

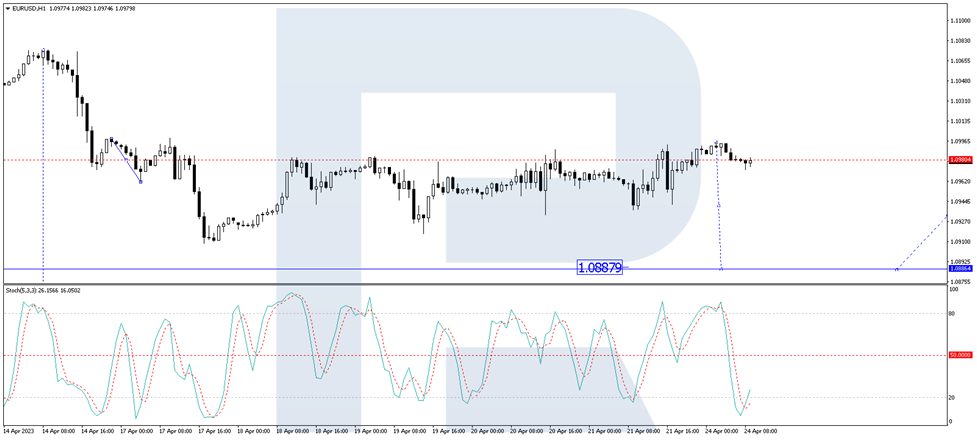

On the H1 chart, the EURUSD pair continues developing a consolidation range around the level of 1.0980. An exit from the range downwards is expected, followed by a descending wave structure to 1.0940. The target is the first one. Technically, this scenario is confirmed by the Stochastic oscillator. Its signal line is under 20, with growth to 50 expected, followed by a decline to the new lows of the indicator.

USD/JPY Extends Rally Ahead of BOJ Core CPI

- USD/JPY climbs for a third straight day

- BoJ Core CPI will be released Tuesday

- New BoJ Governor Ueda chairs his first meeting later this week

Japan inflation in focus

This week’s data calendar out of Japan will be dominated by inflation releases and the Bank of Japan’s two-day meeting at the end of the week. Traders will be keeping a close eye on BoJ Core CPI, which will be released on Tuesday. The index, which is the BoJ’s preferred inflation gauge, fell from 3.1% to 2.7% in February. Another drop would support the central bank’s view that inflation is falling back towards the 2% target.

Inflation has been running above 3% and this has raised speculation that the BoJ will respond by tightening policy, which would likely send the yen sharply higher. The BoJ has insisted that it will not tighten until it is convinced that higher inflation is sustainable and not a result of more expensive goods and raw materials. The uncertain outlook for global growth and a weak domestic economy means that the BoJ is in no rush to shift policy.

New Governor Ueda has been consistent in his message that he will maintain an ultra-loose policy, but nonetheless, speculation continues that the BoJ will tweak or even abandon its yield curve control, which has been criticised for distorting bond market pricing. I suspect that speculators hoping for a shift in policy that will send the yen higher will be disappointed after this week’s meeting, as Ueda is unlikely to rock the boat at his first meeting. The BoJ will provide updated quarterly growth and inflation forecasts, which could provide a hint as to future monetary policy.

USD/JPY Technical

- USD/JPY is testing resistance at 1.3427. Next, there is resistance at 1.3499

- 133.41 and 1.3269 are providing support

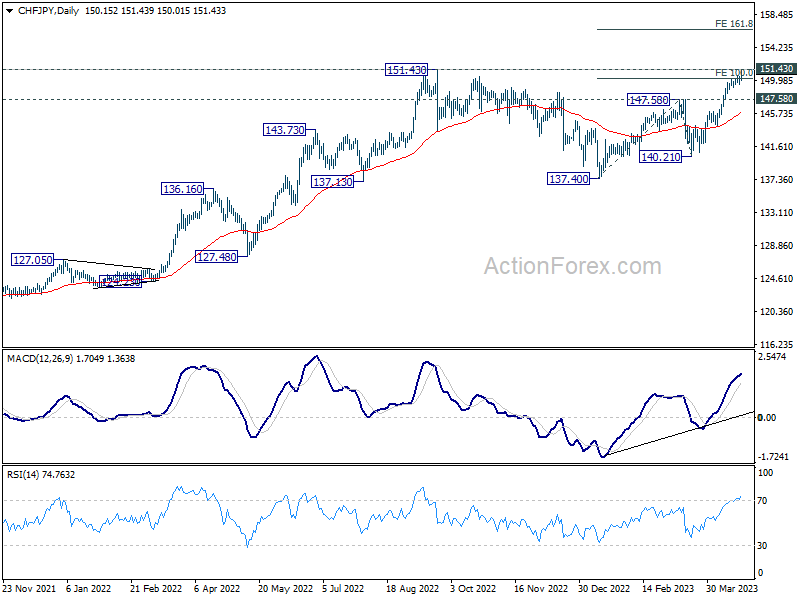

Yen Falls as BoJ Ueda Dims Hopes of Policy Shift; CHF/JPY Ready for New High

Japanese Yen suffers broad sell-off today, following comments from BoJ Governor Kazuo Ueda that seem to have quashed hopes of even a minor shift in monetary policy this week. Meanwhile, overall market sentiment remains steady, with Australian and Canadian Dollars also facing selling pressure. On the other hand, European majors are showing strength for the day, buoyed by optimism surrounding an improvement in economic momentum in the second quarter. Swiss Franc is currently outperforming Euro and Sterling, while Dollar remains mixed but vulnerable to a sell-off against European currencies.

From a technical perspective, CHF/JPY appears poised to resume its long-term uptrend through 151.43 high with strong momentum. Sustained trading above this level could pave the way to 161.8% projection of 137.40 to 147.58 from 140.21 at 156.68. A question now is when EUR/JPY will break through 148.38 resistance level to resume its long-term uptrend as well.

In Europe, at the time of writing, FTSE is down -0.13%. DAX is up 0.08%. CAC is down -0.08%. Germany 10-year yield is up 0.006 at 2.489. Earlier in Asia, Nikkei rose 0.10%. Hong Kong HSI dropped -0.58%. China Shanghai SSE dropped -0.78%. Singapore Strait Times rose 0.08%. Japan 10-year JGB yield rose 0.0099 to 0.472.

Germany Ifo rose to 93.6, worries abating, but lacks dynamism

Germany Ifo Business Climate rose slightly from 93.2 to 93.6 in April, below expectation of 94.0. Current Assessment index dropped from 95.4 to 95.0, below expectation of 96.1. Expectations index rose from 91.0 to 92.2, above expectation of 91.6.

By sector, manufacturing rose from 6.5 to 6.7. Services dropped from 8.8 to 6.8. Trade dropped from -10.1 to -10.7. Construction rose from -17.5 to -16.7.

Ifo said: "German business's worries are abating, but the economy is still lacking dynamism.

Bundesbank: Inflation to remain high overall in coming months

In its latest monthly report, Bundesbank revealed that German economy performed better than anticipated in the first quarter of 2023. Despite persistently high inflation negatively impacting private consumption, industry experienced a stronger recovery. Additionally, goods exports saw a sharp increase, and construction industry temporarily boosted production. Improved economic performance during the winter months was also reflected in the labor market. Early indicators suggest further positive developments ahead.

Inflation rate fell notably to 7.8% in March, a 1.5 percentage point decrease from February. Bundesbank attributes this decline to a base effect. However, core inflation rate, excluding energy and food, climbed by 0.5 percentage points to reach a historic high of 5.9%. In the coming months, Bundesbank expects inflation rate to continue falling somewhat, particularly due to decreasing energy prices and a potential gradual easing in prices of food, other goods, and services. However, underlying price pressure is expected to remain high overall in the coming months.

BoJ Ueda highlights importance of strong inflation projections in monetary policy decisions

BoJ Governor Kazuo Ueda emphasized today that the central bank's inflation forecasts must be "quite strong and close to 2%" within the coming year for the bank to consider adjusting its yield curve control policy.

Speaking to parliament, Ueda said that as "trend inflation is below 2%," BoJ must maintain its current monetary easing stance. However, he noted that when trend inflation is projected to reach 2% target, the central bank must normalize monetary policy.

When asked about the specifics of how BoJ might phase out YCC, Ueda opted not to provide explicit details, clarifying that such a decision would hinge on a variety of factors, encompassing the economy, inflation pace, and other elements at the time of the verdict.

"At this moment, I cannot provide a definitive answer regarding how this could be executed," he said, touching upon BoJ's exit strategy. Nonetheless, Ueda reassured that " BOJ has actively been conducting numerous evaluations on the potential impact of a monetary policy normalization on its financial situation."

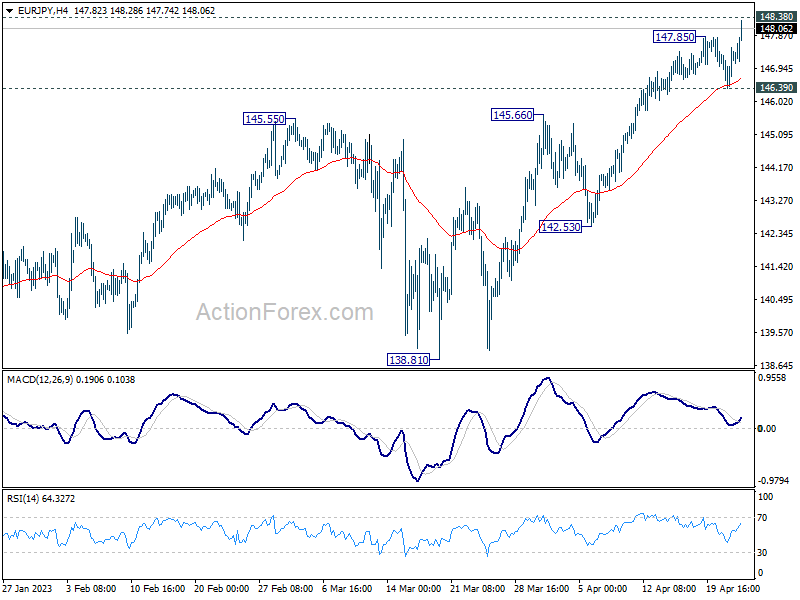

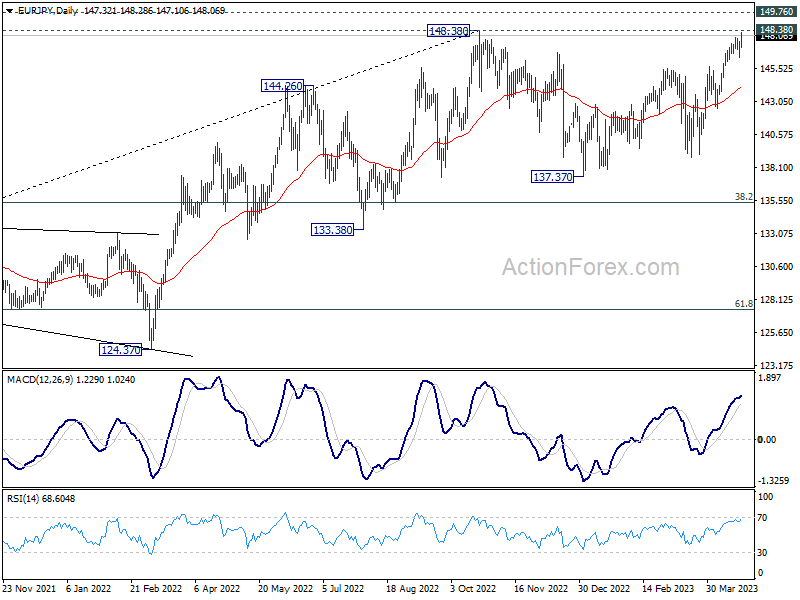

EUR/JPY Daily Outlook

Daily Pivots: (S1) 146.68; (P) 147.12; (R1) 147.84; More....

EUR/JPY's rally resumed by breaking through 147.85 and intraday bias is back on the upside. Decisive break of 148.38 will resume larger up trend to 149.75 long term resistance. For now, outlook will remain bullish as long as 146.39 support holds, in case of retreat.

In the bigger picture, as long as 55 W EMA (now at 140.44) holds, larger up trend from 114.42 (2020 low) is still in progress for 149.76 long term resistance. Decisive break there will resume long term up trend. However, sustained break of 55 W EMA will bring deeper fall to 38.2% retracement of 114.42 to 148.38 at 135.40.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 08:00 | EUR | Germany IFO Business Climate Apr | 93.6 | 94 | 93.3 | 93.2 |

| 08:00 | EUR | Germany IFO Current Assessment Apr | 95 | 96.1 | 95.4 | |

| 08:00 | EUR | Germany IFO Expectations Apr | 92.2 | 91.6 | 91.2 | 91 |

| 12:30 | CAD | New Housing Price Index M/M Mar | 0.00% | 0.10% | -0.20% |

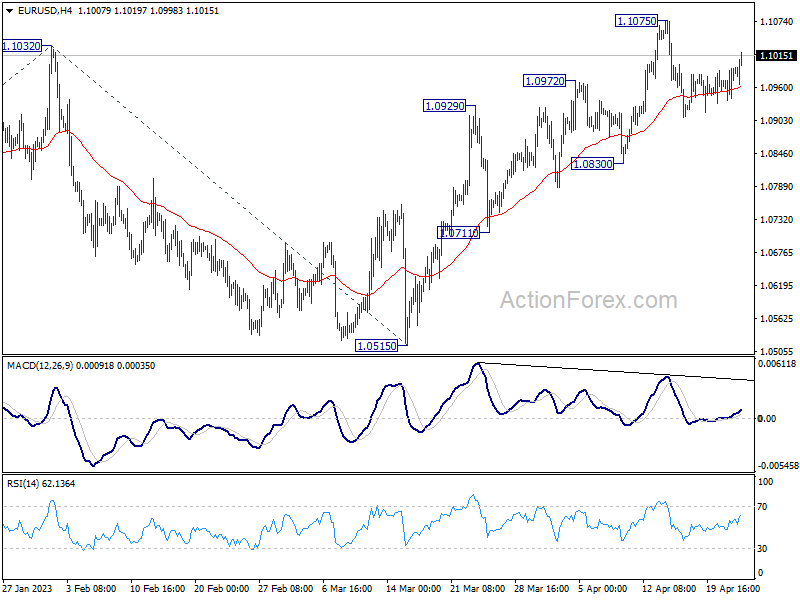

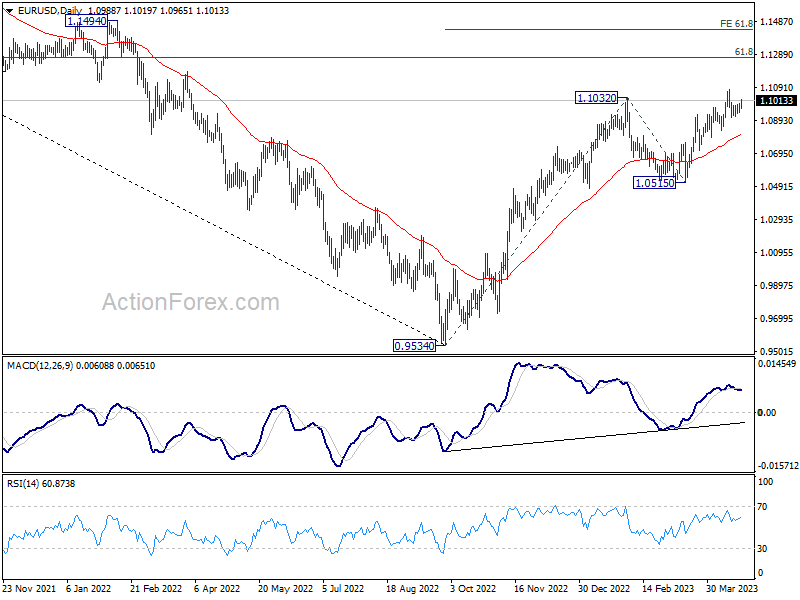

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0954; (P) 1.0974; (R1) 1.1009; More...

Intraday bias in EUR/USD stays neutral at this point. Outlook remains bullish with 1.0830 support intact. On the upside, break of 1.1075 will will resume larger up trend to 1.1273 fibonacci level. Break there will target 61.8% projection of 0.9534 to 1.1032 from 1.0515 at 1.1441. However, firm break of 1.0830 will confirm short term topping and bring deeper decline to 1.0711 support instead.

In the bigger picture, rise from 0.9534 (2022 low) is in progress for 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273. Sustained break there will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high). This will now remain the favored case as long as 1.0515 support holds, even in case of deeper pull back.

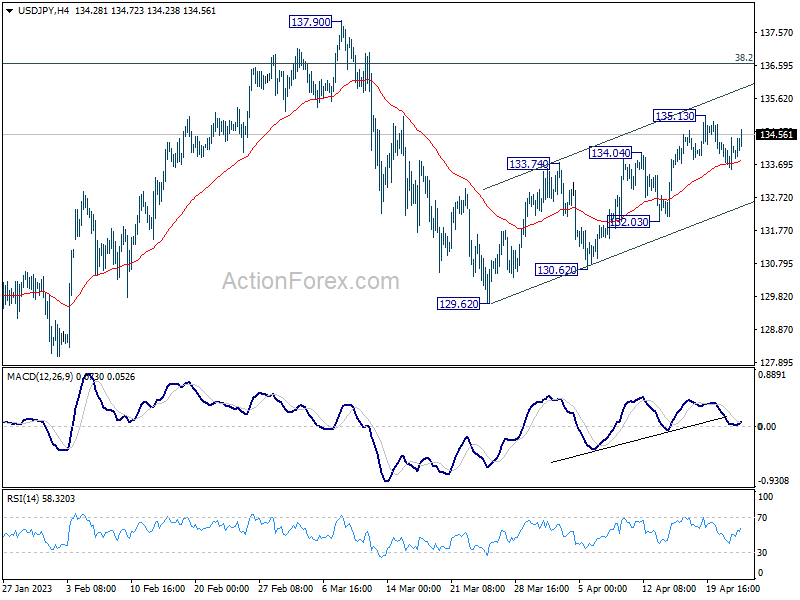

USD/JPY Daily Outlook

Daily Pivots: (S1) 133.85; (P) 134.41; (R1) 134.82; More...

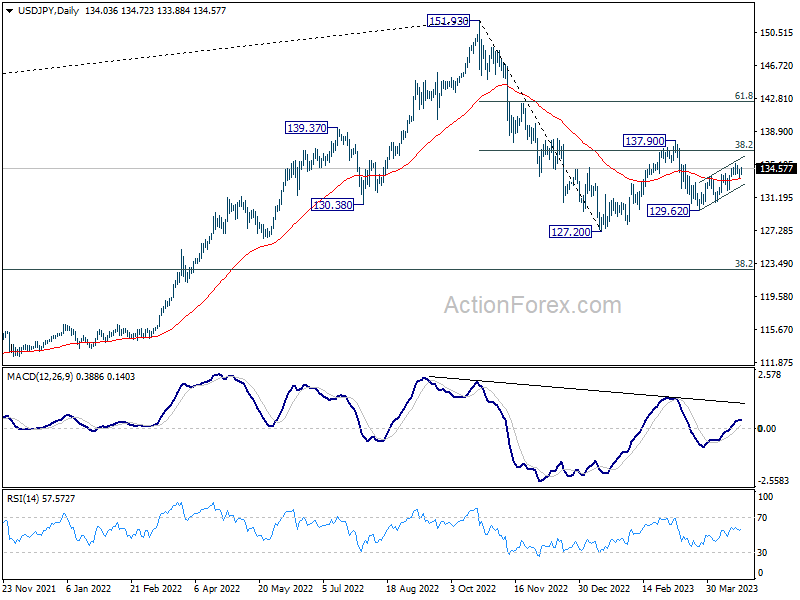

Intraday bias in USD/JPY remains neutral at this point. Further rally is expected as long as 132.03 support holds. On the upside, break of 135.13 will resume the choppy rebound from 129.62 towards 137.90 resistance next. However, break of 132.03 will argue that the rebound has completed already and turn bias back to the downside for 129.62 and below.

In the bigger picture, corrective pattern from 127.20 might be extending. But after all, down trend from 151.93 is expected to resume at a later stage. Break of 127.20 will resume this down trend and target 61.8% projection of 151.93 to 127.20 from 137.90 at 122.61. This will now be the favored case as long as 137.90 resistance holds.

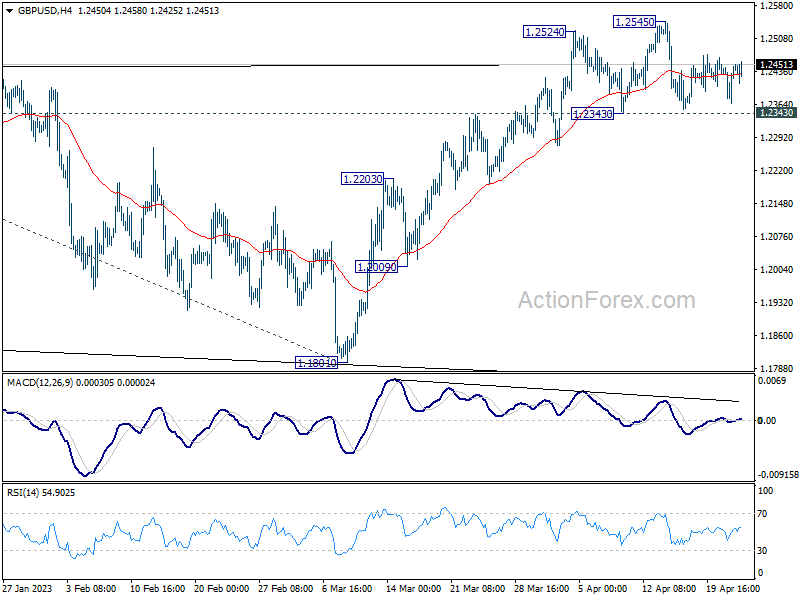

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2391; (P) 1.2419; (R1) 1.2472; More...

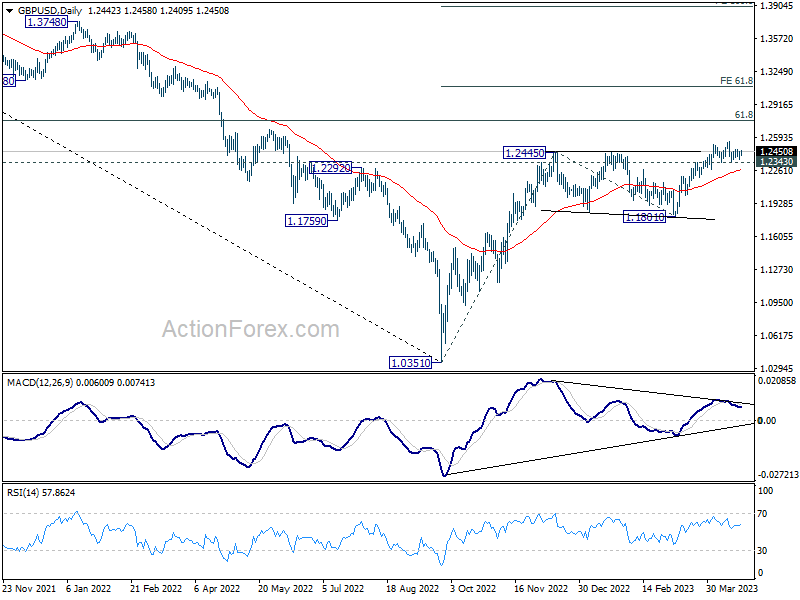

Intraday bias in GBP/USD remains neutral for the moment as consolidation from 1.2545 is still extending. Outlook remains bullish with 1.2343 support intact. On the upside, above 1.2545 will target 1.2759 fibonacci level first. Firm break there will target 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095. However, considering bearish divergence condition in 4H MACD, firm break of 1.2343 will confirm short term topping, and turn bias back to the downside for deeper pullback.

In the bigger picture, the rise from 1.0351 medium term term bottom (2022 low) is in progress for 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759. Sustained break there will add to the case of long term bullish trend reversal. Further break of 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095 could prompt upside acceleration to 100% projection at 1.3895. For now, this will remain the favored case as long as 1.1801 support holds, even in case of deep pull back.

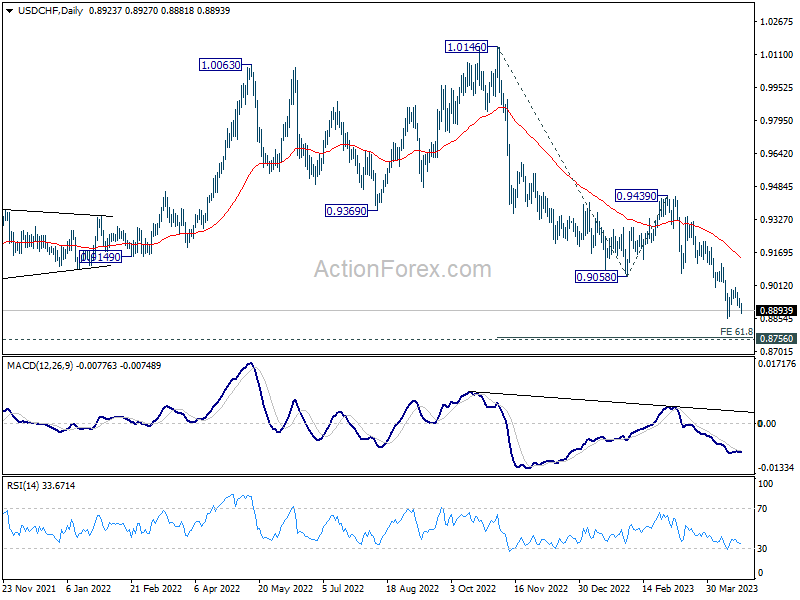

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8904; (P) 0.8929; (R1) 0.8950; More...

Intraday bias in USD/CHF remains neutral as it's still bounded in consolidation from 0.8858. Further decline is expected with 0.9070 support turned resistance intact. On the downside, below 0.8858 will resume the down trend from 1.0146 to 61.8% projection of 1.0146 to 0.9058 from 0.9439 at 0.8767, which is close to 0.8756 long term support. Strong support is expected there to bring rebound, at least on first attempt. On the upside, break of 0.9070 support turned resistance will confirm short term bottoming and turn bias back to the upside.

In the bigger picture, fall from 1.1046 (2022 high) is in progress for 0.8756 support (2021 low). But overall, this fall is still seen as a leg in the long term range pattern from 1.0342 (2016 high). So, downside should be contained by 0.8756 to bring reversal. Sustained break of 0.9058 support turned resistance will be the first sign of medium term bottoming. However, decisive break of 0.8756 will carry larger bearish implications.

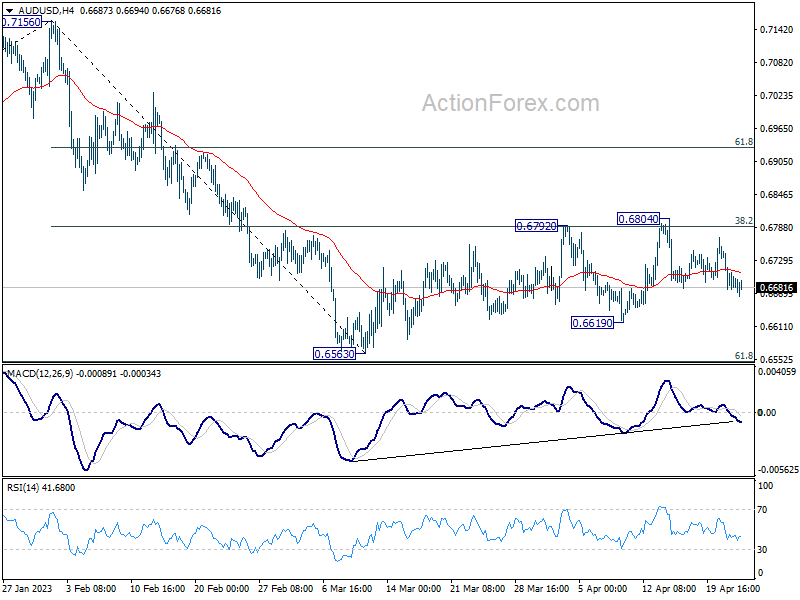

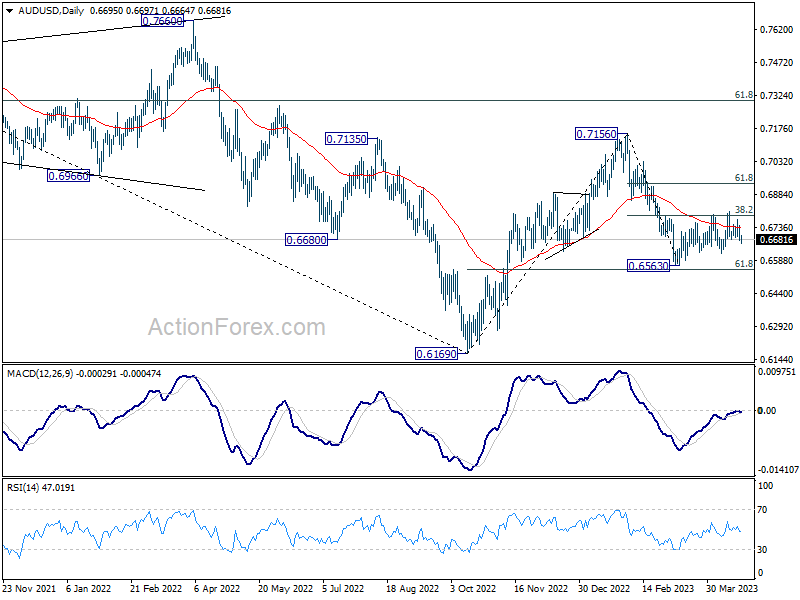

AUD/USD Daily Report

Daily Pivots: (S1) 0.6665; (P) 0.6706; (R1) 0.6734; More...

Intraday bias in AUD/USD remains neutral as consolidation pattern from 0.6563 is still extending. On the downside, break of 0.6619 will indicate that decline from 0.7156 is resuming through 0.6563 low. Nevertheless, sustained break of 0.6804 will bring stronger rally back to 61.8% retracement of 0.7156 to 0.6563 at 0.6929.

In the bigger picture, as long as 61.8% retracement of 0.6169 to 0.7156 at 0.6546 holds, the decline from 0.7156 is seen as a correction to rally from 0.6169 (2022 low) only. Another rise should still be seen through 0.7156 at a later stage. However, sustained break of 0.6546 will raise the chance of long term down trend resumption through 0.6169 low.

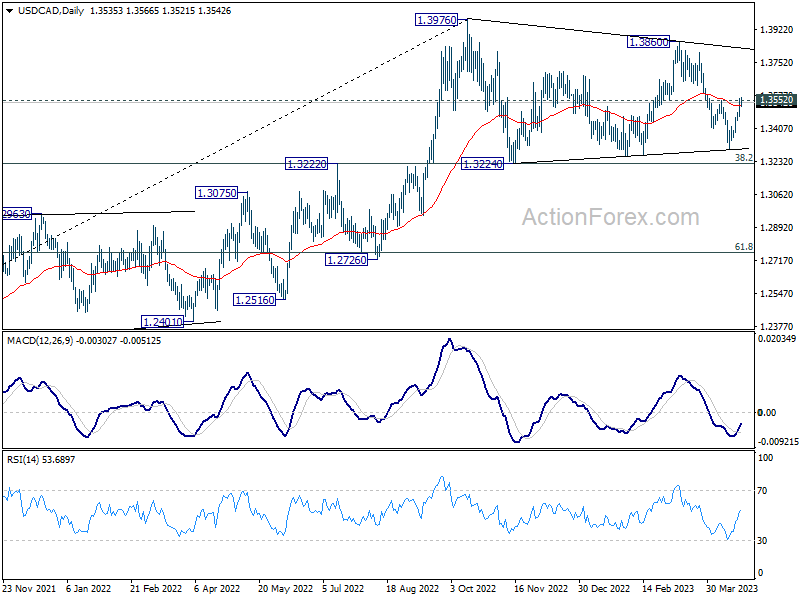

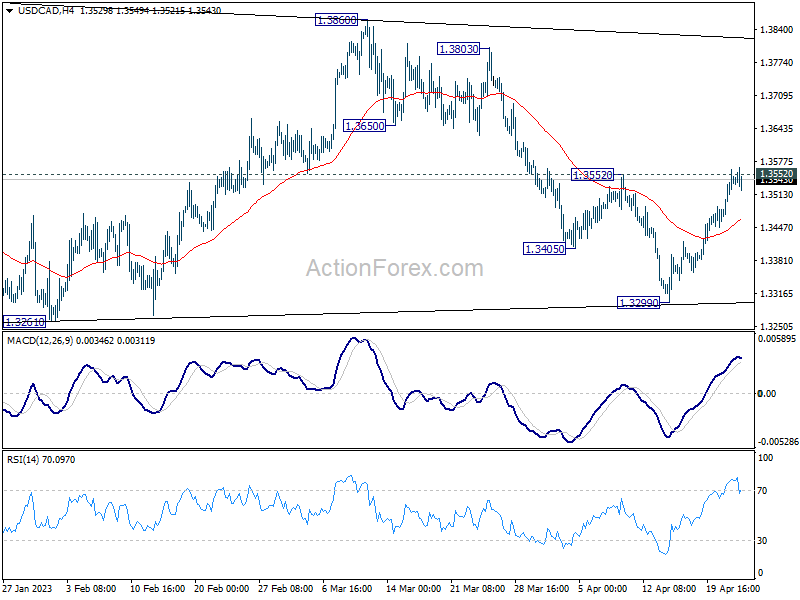

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3487; (P) 1.3525; (R1) 1.3578; More....

Immediate focus stays on 1.3552 resistance in USD/CAD. As noted before, price actions from 1.3976 are seen as a corrective pattern with fall from 1.3860 as the third leg. Decisive break of 1.3552 will argue that such corrective pattern has completed. Further rally should then be seen back to 1.3860/3976 resistance zone.

In the bigger picture, the up trend from 1.2005 (2021 low) is still in progress. Break of 1.3976 will confirm resumption and target 61.8% projection of 1.2401 to 1.3976 from 1.3261 at 1.4234. Firm break there will pave the way to long term resistance zone at 1.4667/89 (2016, 2020 highs). On the downside, sustained break of 55 W EMA (now at 1.3302) is needed to confirm medium term topping. Otherwise, outlook will remain bullish even in case of deep pull back.