Sample Category Title

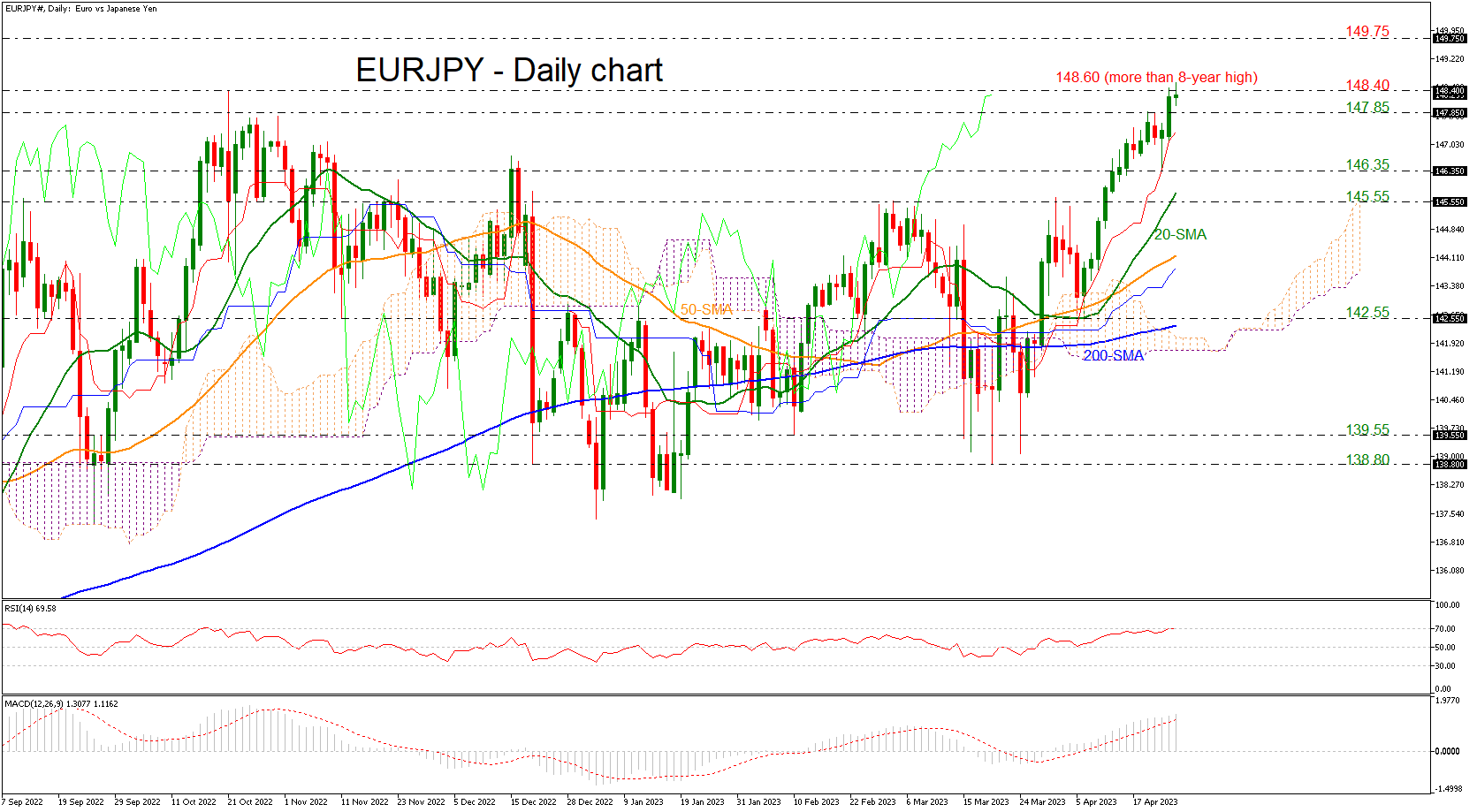

EURJPY Surges to Fresh More-than-8-Year High

EURJPY skyrocketed to a fresh more than eight-year high of 148.60 earlier today but quickly returned some of the gains. The aggressive advance above the 146.35 support added 1.6% to the pair but the technical oscillators are looking overbought at the moment. The RSI found a strong obstacle near the 70 level and is pointing slightly down, while the MACD is still extending its upside pressure above its trigger and zero lines.

Should the pair manage to strengthen its positive momentum and jump above its intraday high, the next resistance could come around 149.75, taken from the peak in December 2014. The psychological mark of 150.00 would also be a key level for traders to have in mind.

However, if prices are unable to break higher, the risk would shift to the downside for a potential bearish correction, with the 147.85 support coming first into focus. A drop lower would signal deeper declines until the 146.35 barrier and the 20-day simple moving average (SMA) at 145.80 ahead of the 145.55 line, taken from the inside swing highs on March 2.

All in all, EURJPY is strongly bullish in the short-to-medium-term timeframes and only a slip beneath the SMAs and the Ichimoku cloud may switch the outlook to neutral.

NZD/USD Eyeing New 2023 Lows, Big Support is at 0.6

NZDUSD recovered nicely from 0.6083 but it's in three waves after recent rejection down from 0.6390 resistance. We see this as a potential corrective rally that represents (B) wave, possibly already completed after lower swing high and new swing low formed in the last few trading days. Ideally, pair is headed south for five wave drop within (C) which has room even for 0.6000. However, this wave (C) is still part of a higher degree contra-trend movement, so we believe that kiwi will turn bullish this year, but from lower support levels, according to daily count. The potential ending diagonal also suggests that support will be seen at a new 2023 low.

On a higher degree chart, we see pair turning up from an important trendline of a potential triangle, so wave (E) can be finished. As such, more gains will be expected in the upcoming weeks/months.

Gold Holds Ground

EUR/GBP tests resistance

The euro advances as traders price in a 50-bps ECB hike next week. The pair’s third attempt at 0.8860 since late March shows strong buying interests especially when it is supported by a series of higher lows. A bullish breakout would send the single currency to 0.8890 at the origin of the mid-March sell-off where a breach could open the door to an extended rally above the daily double top around 0.8920. As the RSI ventures into the overbought area, 0.8830 is the first level to expect follow-up buying in case of a retracement.

XAU/USD seeks support

Gold inched higher as the US dollar fell across the board amid thin demand. The price continues to retreat from March 2022’s peak near 2050 while the daily RSI drops back to the neutral area. It would be too soon to call it a bearish reversal as there are multiple layers of support including 1975 and the daily level of 1950. The correction is likely to be driven by profit-taking as bullion approaches the all-time high and the price could be merely probing for support before another leg up. 2015 is the first resistance in case of a bounce.

Dow Jones 30 grinds support

The Dow Jones 30 steadies as investors await high-profile earnings this week. The price has met strong supply around this year’s highs of 34100-34300 and a slide below 33800 has prompted short-term buyers to trim their exposure. Still, sentiment remains upbeat from the medium-term’s perspective after a sharp recovery from the March lows (31500). The index is testing 33580 at the confluence of the former March high and the 20-day SMA. A rebound will need to lift 33950 before it could signal a bullish continuation.

Caution Prevails Ahead of Big Tech Earnings

Most Asian equities flashed red on Tuesday, pressured by losses in Chinese shares as investors evaluated China’s re-opening story in the face of negative economic and geopolitical forces. European futures are pointing to a mixed open with market players guarded ahead of another event-heavy week for financial markets. Some of the largest companies in the world including the four Big Tech titans (Microsoft, Alphabet, Meta and Amazon) will be reporting their results this week. If the corporate earnings paint an overall encouraging picture, this could boost risk sentiment and support equity bulls. However, a set of disappointing results is likely to enforce renewed pressure on stock markets with the S&P500 and Nasdaq feeling the brunt.

In the currency space, the dollar attempted to stabilise during early trade after slipping in the previous session as more signs of slowing US economic growth cooled Fed hike bets. With markets now pricing in the peak for US interest rates in June, dollar bulls could be running on fumes. Gold drew strength from falling Treasury yields while oil prices steadied after two days of gains.

Dollar bears to hijack the scene?

Repeated signs of cooling price pressures and disappointing US economic data could add more fuel to expectations around the Fed pausing rate hikes and eventually cutting down the road. On Monday, softer US manufacturing data strengthened the argument for the Fed to pause. There are more major releases from the US economy this week including April consumer confidence data, Q1 GDP figures, and most importantly the Fed’s preferred inflation gauge, the Core Personal Consumption Expenditure.

US economic growth in the first quarter is expected to moderate from the 2.6% in the previous quarter while persistent price pressures may be present in Friday’s core PCE report. Ultimately, if the data supports expectations around the Fed taking a pause from rate hikes after May, this may drag the dollar lower.

Looking at the technical picture, the Dollar Index remains under pressure on the daily charts. Weakness below 102.00 could trigger a decline towards 100.79 and 100.00, a level not seen since April 2022.

Commodity spotlight – Gold

Gold briefly punched above the psychological $2000 level during early trade this morning as falling Treasury yields and dollar weakness sweetened appetite for the precious metal. Nevertheless, it still remains trapped within a sticky range thanks to the ongoing uncertainty over the Fed’s next move beyond May. With markets now expecting US rates to peak in the summer and a rate cut by December, gold has the thumbs up to push higher in the longer term. Meanwhile, volatility could be the name of the game due to shifting expectations around future Fed policy moves.

Turning to the technicals, price action suggests that a fresh catalyst is needed to trigger a bullish or bearish breakout. A strong move above $2000 may inspire a push towards $2025 and $2048. If prices remain below $2000, gold could test $1950 and $1900.

ECB Has No Other Choice But to Continue Inflation Battle

Markets

European and US yields parted ways yesterday with Europe underperforming. A thin eco calendar failed to inspire, but comments by ECB Wunsch in an FT interview managed to do the trick. They were released ahead of the European opening bell, but resonated throughout European dealings. Wunsch added to recent hawkish comments from him and several other ECB figures, arguing that the ECB has no other choice but to continue its inflation battle as core (services) inflation and wage inflation show no sign of abating yet. He wouldn’t be surprised to see the key ECB policy rate reach 4%. We also expect him to back another 50 bps rate hike next week, our preferred scenario. German yields rose between 0.9 bps (30-yr) and 5.8 bps (2-yr) yesterday with the front end of the curve obviously underperforming. US yields eventually closed 6.5 bps (30-yr) to 10 bps (3-yr) lower! They were already on a slippery slope throughout the day, but Q1 earnings from First Republic Bank delivered the final and strongest blow at the closing bell. The US regional bank was already on death row with earnings now revealing over $100bn of deposit outflows between mid-March ($138.1bn) and mid-April. This compares with mostly single-digit deposit outflow figures at other regional banks which already reported Q1 results. The Fed and big banks provided a liquidity stopgap to secure First Republic’s short-term survival, but long-term profitability is seriously at risk. First Republic bank shares fell around 20% in after-hours trading. We won’t get dragged away too far by moves in the transition from US to Asian dealings and don’t expect this to be the start of a new period of instability as witnessed in the wake of the collapse of Silicon Valley Bank. The US/German 2y yield spread dropped below 110 bps to the lowest level since October 2021. These relative yield dynamics translate into additional gains for EUR/USD. The pair took out the 1.10 big figure and tested the 1.1076 YTD top. Real resistance stands at 1.1274 which is 62% retracement on the EUR/USD decline between early 2021 and late 2022. (Temporary?) risk aversion related to US regional banking problems last month didn’t help the greenback with EUR and JPY the preferred safe haven currencies. On balance, the single currency even outperforms the Japanese yen as new BoJ governor Ueda sticks to previous governor Kuroda’s dovish policy stance. He said in front of parliament this morning that tightening now may cause inflation (currently above target led by cost-push factors) to weaken more than currently already expected and could have serious consequences in the future. EUR/JPY is testing the 2022 top at 148.40 with next resistance (2015 top) at 149.78. Apart from general risk sentiment, we look at US eco data to guide trading (Philly Fed business outlook, Richmond Fed manufacturing index and consumer confidence). Especially disappointing numbers could be picked up.

News and views

Q1 South Korean growth printed slightly stronger than expected at 0.3% Q/Q (from -0.4% Q/Q in Q4 2022). Demand was supported by a 0.5% rise in private consumption. However, capital investment contracted by 4%. Exports and imports respectively gained 3.8% and 3.5%. The Bank of Korea expects a further economic rebound in the second half of the year but uncertainty remains high both internally and externally. Earlier this month, the BOK for a second consecutive meeting left its policy rate unchanged at 3.5% as it indicated that growth this year might be slightly below its previous 1.6% forecast. At the same time March inflation (4.2% Y/Y) remained well above the 2% inflation target. The Korean won stays in the defensive easing to USD/KRW 1336, despite an overall soft USD.

A series of economic data published in Poland yesterday printed on the softer side of expectations. PPI producer prices dropped 0.8% M/M in March easing the Y/Y figure to 10.1% Y/Y (-0.5% and 18.2% Y/Y in February). The decline in industrial output also accelerated from -1.0% Y/Y in February to -2.9% Y/Y in March as a 14.1 M/M gain was not enough to compensate for a big positive base effect last year. Construction output also missed the consensus estimate, declining 1.5% Y/Y from a positive growth of 6.6% the previous month. Last but not least, retail sales showed a similar picture as was the case for production. A 14% monthly rise was not enough to compensate for a big monthly gain last year resulting in a further decline in the Y/Y measure from -5.0% to -7.3%. For now, the National Bank of Poland is keeping a wait-and-see approach as inflation (16.1% Y/Y in March) remains too high to start the debate on possible interest rate cuts even as activity slows. Weaker eco data didn’t hurt recent positive sentiment on the zloty. EUR/PLN closed below 4.60, testing the strongest levels for the zloty since June last year.

Big German Pay Rises

Market movers today

A quiet day in terms of data releases, US Conference Board's consumer confidence index will be released for April. The University of Michigan survey released earlier pointed towards modestly improving consumer sentiment.

The National Bank of Hungary is expected to maintain rates unchanged in its meeting today.

The 60 second overview

Pay rises: German public sector wage negotiations (covering some 2.5 million workers) has reached an agreement. The deal has several elements: (1) no permanent wage increase in 2023, but a EUR 1240 one-off payment in June 2023, followed by monthly payments of EUR 220 from July 2023-February 2024; and (2) from March 2024 a permanent wage increase of EUR 200 plus 5.5%. Overall, for a 24 month agreement the union talks about wage increases between 8.2% and 16.9%, with the average wage increase around 11.5%. Overall, it marks yet another agreement with significantly higher wage growth that could further delay the return of core inflation to ECB's target. Nor will it be the last high-wage agreement: Verdi union has just started with a 15% wage demand for the retail sector negotiations covering another 2.6 million workers.

German business climate: Ifo improved for a sixth straight month in April. While business expectations continued to improve, the current situation assessment weakened a tad, especially for construction, which is feeling the heat from higher rates. Overall, Ifo continues to send a less upbeat signal for the state of the economy than PMIs. The good news is that the German economy seems to have edged further away from recession territory at the start of Q2, but on the downside Ifo suggests a strong rebound in activity is not yet in sight either.

Bank of Japan: Once again, the new governor Ueda stressed the need to keep monetary policy accommodative for now. "We see the risk of inflation undershooting forecasts as bigger than the risk of overshooting", he said, ahead of the policy meeting ending Friday. "But if wage growth and inflation accelerates faster than expected and warrants tightening monetary policy, the BOJ stands ready to respond such as by raising interest rates". See Reuters. We expect the BoJ to stay put on Friday, see Bank of Japan Preview - Risk of tightening too soon still dominates, 21 April.

Equities: Global equities marginally higher yesterday lifted by Europe and US. Tech sector underperforming ahead of the pick-up in Q1 tech reporting season the coming days. Regional banks on the weak side as well and they could come in focus today after the earnings result from First Regional (came after the bell) showed as deposit outflow of 41% in Q1. Energy the biggest outperformer followed by the group of classic defensive sectors. In US Dow +0.2%, S&P 500 +0.1%, Nasdaq -0.3% and Russell 2000 -0.2%.

Asian markets are mostly lower this morning led by tech-heavy South Korea. European and US futures 0.2%-0.3% lower.

FI: It was a mixed day in the global bond markets, where European yields rose across the curve, while US Treasury yields declined across the curve. Hence, the 10Y US-German government yield spread is testing the 100bp-level, which we have not seen since the Covid crisis in the spring 2020.

FX: The EUR continues to shine and yesterday in particular vis-à-vis USD, JPY, AUD and CAD on a day where short-term EUR rates rose to the highest level in over a month ahead of next week's ECB meeting. Scandi currencies held steady for a change and looks to be in wait-and-see mode before the Riksbank meeting and the announcement on NOK fiscal transactions later this week.

Credit: Overall a quiet session in the credit market with limited activity in secondary markets. iTraxx Main was unchanged at 83bp while iTraxx Xover was 1bp tighter at 439bp. The primary market activity was relatively high with more than 10 new deals announced - among others the Federal Republic of Germany announced a 10-year EUR benchmark Green bond offering and in the Nordics TDC NET announced intention to issue an 8-year EUR benchmark senior secured sustainability-linked bond.

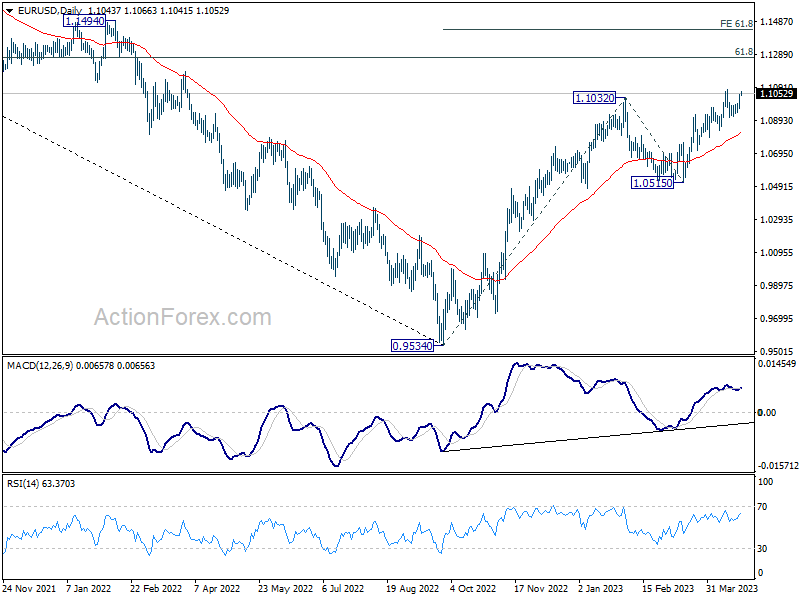

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0992; (P) 1.1021; (R1) 1.1076; More...

Immediate focus is now on 1.1075 resistance in EUR/USD as rebound extends today. Decisive break there will resume larger up trend from 0.9534 to 1.1273 fibonacci level. Break there will target 61.8% projection of 0.9534 to 1.1032 from 1.0515 at 1.1441. On the downside, break of 1.0995 minor support will now indicate that corrective pattern from 1.1075 is extending with one more falling leg before completion.

In the bigger picture, rise from 0.9534 (2022 low) is in progress for 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273. Sustained break there will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high). This will now remain the favored case as long as 1.0515 support holds, even in case of deeper pull back.

Hawkish ECB Comments Boost Euro, AUD and CAD Struggle

Euro is making broad gains in Asian session, fueled by hawkish comments from a top ECB official who suggested that the next rate hike could be a 50bps one. Euro's strength is also lifting the Swiss Franc, while Sterling remains firm but lags slightly behind. In contrast, Australian and Canadian dollars are underperforming, with the Aussie looking particularly vulnerable ahead of tomorrow's CPI report and facing additional pressure from selling in cross against New Zealand Dollar.

Yen is also weak as markets anticipate BoJ will maintain its current policy stance unchanged at this week's meeting. Mild risk aversion in Asian stocks is providing slight support for the Japanese currency, but this may be short-lived. Dollar is mixed for now, alongside US stocks and bonds, but could be vulnerable to an extended selloff against European majors if key support levels are decisively broken.

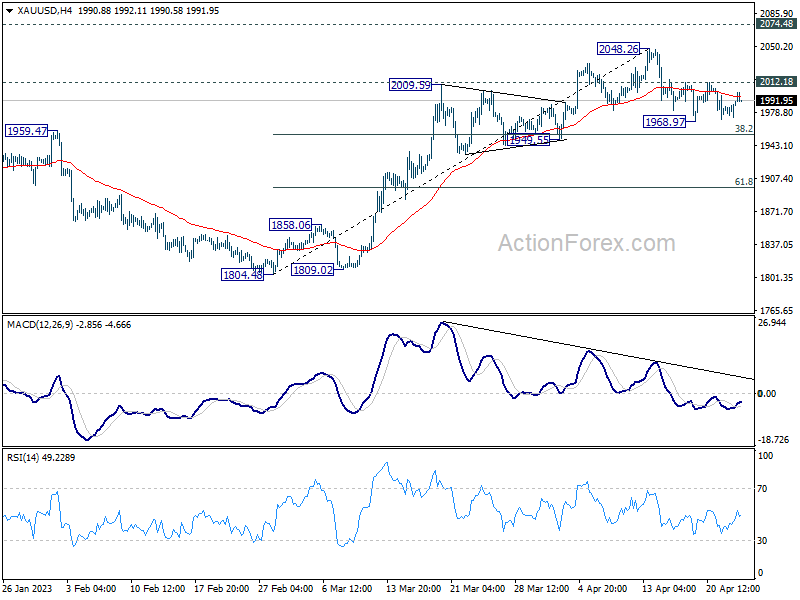

Technically, Gold appears to be attempting to find a bottom ahead of 38.2% retracement of 1804.48 to 2048.26 at 1955.13. Break of 2012.18 resistance could signal that correction from 2048.26 is complete, potentially leading to a strong rally through 2048.26 and towards record high of 2074.48. If realized, this move may coincide with break of 1.1075 in EUR/USD, regardless of which one occurs first.

In Asia, at the time of writing, Nikkei is up 0.14%. Hong Kong HSI is down -1.62%. China Shanghai SSE is down -0.35%. Singapore Strait Times is down -0.80%. Japan 10-year JGB yield is up 0.0117 at 0.484. Overnight, DOW rose 0.20%. S&P 500 rose 0.09%. NASDAQ dropped -0.29%. 10-year yield dropped -0.055 to 3.515.

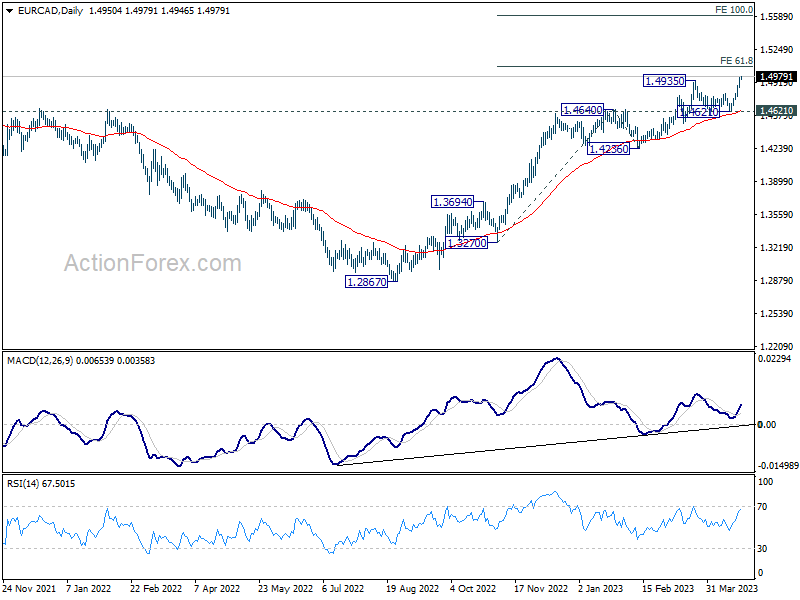

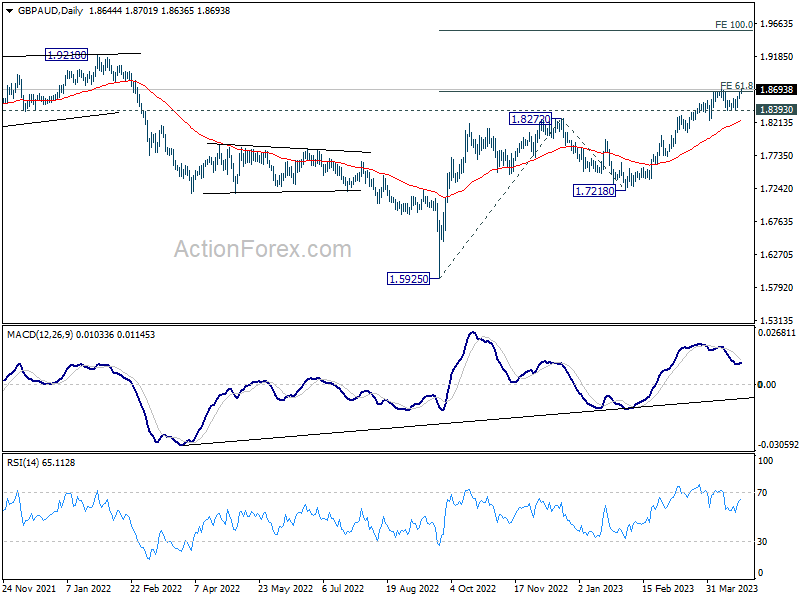

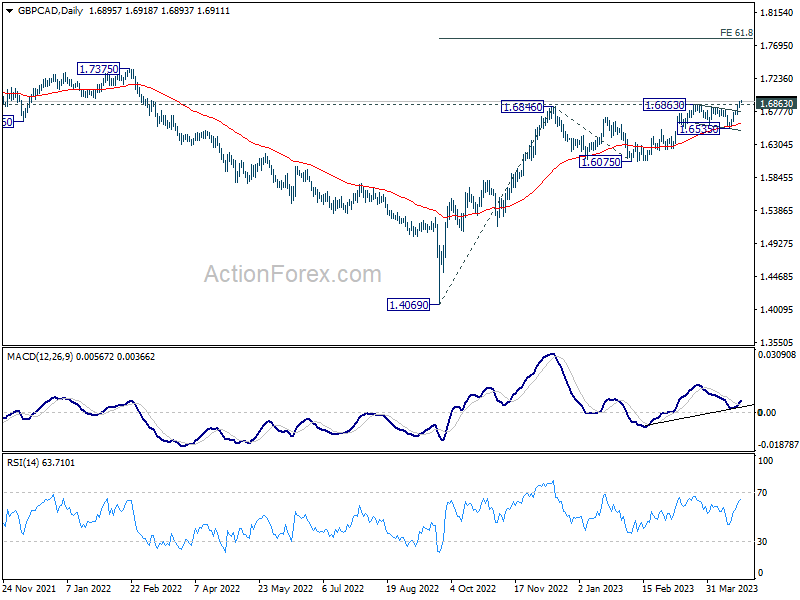

EUR/AUD, EUR/CAD, GBP/AUD, GBP/CAD uptrend resumptions

Both Euro and Sterling staged upside breakout against Australian and Canadian Dollar this week, resuming respective medium term up trend. Comments from a top ECB official overnight indicates that a 50bps is not off the table for May policy meeting. Meanwhile, recent data from the UK clearly indicates the need for extended tightening from BoE to fight the still-double-digit inflation. On the other hand, there is no data supporting BoC to move out from its pause. Aussie looks vulnerable to tomorrow's CPI release, which would be crucial to whether RBA would deliver a final hike in the currency cycle.

EUR/AUD's up trend from 1.4281 is now in progress for 100% projection of 1.4281 to 1.5976 from 1.5254 at 1.6949. Near term outlook will stay bullish as long as 1.6219 support holds, in case of retreat.

EUR/CAD's break of 1.4935 confirmed resumption of whole up trend from 1.2867. Immediate target is 61.8% projection of 1.3270 to 1.4640 from 1.4236 at 1.5083. Sustained break there could prompt upside acceleration to 100% projection at 1.5606. Meanwhile, outlook will stay bullish as long as 1.4261 support holds, in case of retreat.

GBP/AUD's breach of 1.8697 resistance argues that uptrend from 1.5925 is resuming. Outlook will stay bullish as long as 1.8393 support holds, in case of retreat. Sustained trading above 61.8% projection of 1.5925 to 1.8272 from 1.7218 at 1.8668 could prompt upside acceleration to 1.9218 resistance and then 100% projection at 1.9565.

GBP/CAD's break of 1.6846 resistance also indicates resumption of up trend from 1.4069. Near term outlook will stay bullish as long as 1.6535 support holds. Current rise should target 61.8% projection of 1.4069 to 1.6846 from 1.6075 at 1.7791 next.

ECB's Schnabel: Further rate hikes needed, 50 not off the table

ECB Executive Board member Isabel Schnabel said in a Politico interview that additional rate hikes are necessary, with the size of these hikes depending on incoming data. "The data we have so far shows that inflation is higher and the economy more resilient than projected," she added that "data dependence means that 50 basis points are not off the table" for May meeting.

She also noted that "it's far too early to declare victory on inflation." She explained that if core inflation remains high and persistent, even if it reaches a peak, the information content of that data point might be limited. "So what we really need is confidence that it's actually coming down in a sustained manner."

Schnabel acknowledged that she cannot predict the terminal interest rate, noting that rates must be set on a meeting-to-meeting basis. She also addressed concerns about a potential recession, stating, "So far, there are no particular signs of a weakening in economic developments. At this point in time, I have no reason to believe that a recession is coming."

ECB's Makhlouf: Too early to start planning for a pause

ECB Governing Council member Gabriel Makhlouf stated in a blog post that it is too early to plan for a pause in tightening of monetary policy, emphasizing the need to focus on incoming data. In a blog post, Makhlouf said, "on the evidence so far, it is too early to start planning for a pause in our tightening of policy." He further noted that based on current evidence, restrictive rate levels are necessary to balance supply and demand in the economy and reduce inflation.

In separate occasion, another Governing Council member François Villeroy de Galhau emphasized the role of climate change in affecting price stability and economic activity. He highlighted that addressing climate change is not an instance of mission creep or politicization, but rather a core duty of central banks worldwide. Villeroy stated, "It's not mission creep, it's not a politicisation of our mandate - it is our core business and core duty."

BoJ Governor Ueda stresses need for continued monetary easing

BoJ Governor Kazuo Ueda addressed parliament today, emphasizing, "In light of current economic, price and financial developments, it's appropriate to maintain monetary easing, now conducted through yield curve control."

Ueda reiterated the importance of keeping Japan's monetary policy loose to achieve the 2% inflation target in a sustainable and stable manner, along with wage hikes. He added that if wage growth and inflation accelerate faster than expected and require tightening monetary policy, BoJ is prepared to respond by raising interest rates.

Despite this, Ueda warned of the risk of inflation falling further below expectations, calling it "very worrying." He noted that "the risk of inflation undershooting forecasts is bigger than the risk of overshooting," emphasizing the need to maintain the BoJ massive stimulus for the time being.

Looking ahead

Swiss trade balance and UK public sector net borrowing will be released in European session. Later in the day, US will release house price index, consumer confidence and new home sales.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0992; (P) 1.1021; (R1) 1.1076; More...

Immediate focus is now on 1.1075 resistance in EUR/USD as rebound extends today. Decisive break there will resume larger up trend from 0.9534 to 1.1273 fibonacci level. Break there will target 61.8% projection of 0.9534 to 1.1032 from 1.0515 at 1.1441. On the downside, break of 1.0995 minor support will now indicate that corrective pattern from 1.1075 is extending with one more falling leg before completion.

In the bigger picture, rise from 0.9534 (2022 low) is in progress for 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273. Sustained break there will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high). This will now remain the favored case as long as 1.0515 support holds, even in case of deeper pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y Mar | 1.60% | 1.60% | 1.80% | 1.70% |

| 06:00 | CHF | Trade Balance (CHF) Mar | 4.20B | 3.31B | ||

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Mar | 12.2B | 15.9B | ||

| 13:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y Feb | 1.80% | 2.50% | ||

| 13:00 | USD | Housing Price Index M/M Feb | -0.20% | 0.20% | ||

| 14:00 | USD | Consumer Confidence Apr | 104.1 | 104.2 | ||

| 14:00 | USD | New Home Sales Mar | 630K | 640K | ||

| 22:45 | NZD | Trade Balance (NZD) Mar | -500M | -714M |

EUR/AUD, EUR/CAD, GBP/AUD, GBP/CAD uptrend resumptions

Both Euro and Sterling have made significant gains against Australian and Canadian Dollars this week, resuming medium-term uptrends in respective crosses. Overnight comments from a top ECB official suggest that a 50bps rate hike may be on the table for May policy meeting. Meanwhile, recent UK data underscores the necessity for BoE to extend its tightening measures in order to combat persistently high, double-digit inflation.

On the other hand, there is no data supporting a shift from BoC's current pause in rate hikes. Australian dollar appears vulnerable ahead of tomorrow's crucial CPI release, which will likely determine whether RBA will implement a final rate hike in the current cycle.

EUR/AUD's up trend from 1.4281 is now in progress for 100% projection of 1.4281 to 1.5976 from 1.5254 at 1.6949. Near term outlook will stay bullish as long as 1.6219 support holds, in case of retreat.

EUR/CAD's break of 1.4935 confirmed resumption of whole up trend from 1.2867. Immediate target is 61.8% projection of 1.3270 to 1.4640 from 1.4236 at 1.5083. Sustained break there could prompt upside acceleration to 100% projection at 1.5606. Meanwhile, outlook will stay bullish as long as 1.4261 support holds, in case of retreat.

GBP/AUD's breach of 1.8697 resistance argues that uptrend from 1.5925 is resuming. Outlook will stay bullish as long as 1.8393 support holds, in case of retreat. Sustained trading above 61.8% projection of 1.5925 to 1.8272 from 1.7218 at 1.8668 could prompt upside acceleration to 1.9218 resistance and then 100% projection at 1.9565.

GBP/CAD's break of 1.6846 resistance also indicates resumption of up trend from 1.4069. Near term outlook will stay bullish as long as 1.6535 support holds. Current rise should target 61.8% projection of 1.4069 to 1.6846 from 1.6075 at 1.7791 next.

GBP/USD Could Rally If It Clears This Resistance

Key Highlights

- GBP/USD is consolidating above the 1.2380 support.

- A major bullish trend line is forming with support near 1.2395 on the 4-hour chart.

- EUR/USD is moving higher and stable above the 1.0950 support.

- Gold price is showing a few bearish signs below the $2,000 level.

GBP/USD Technical Analysis

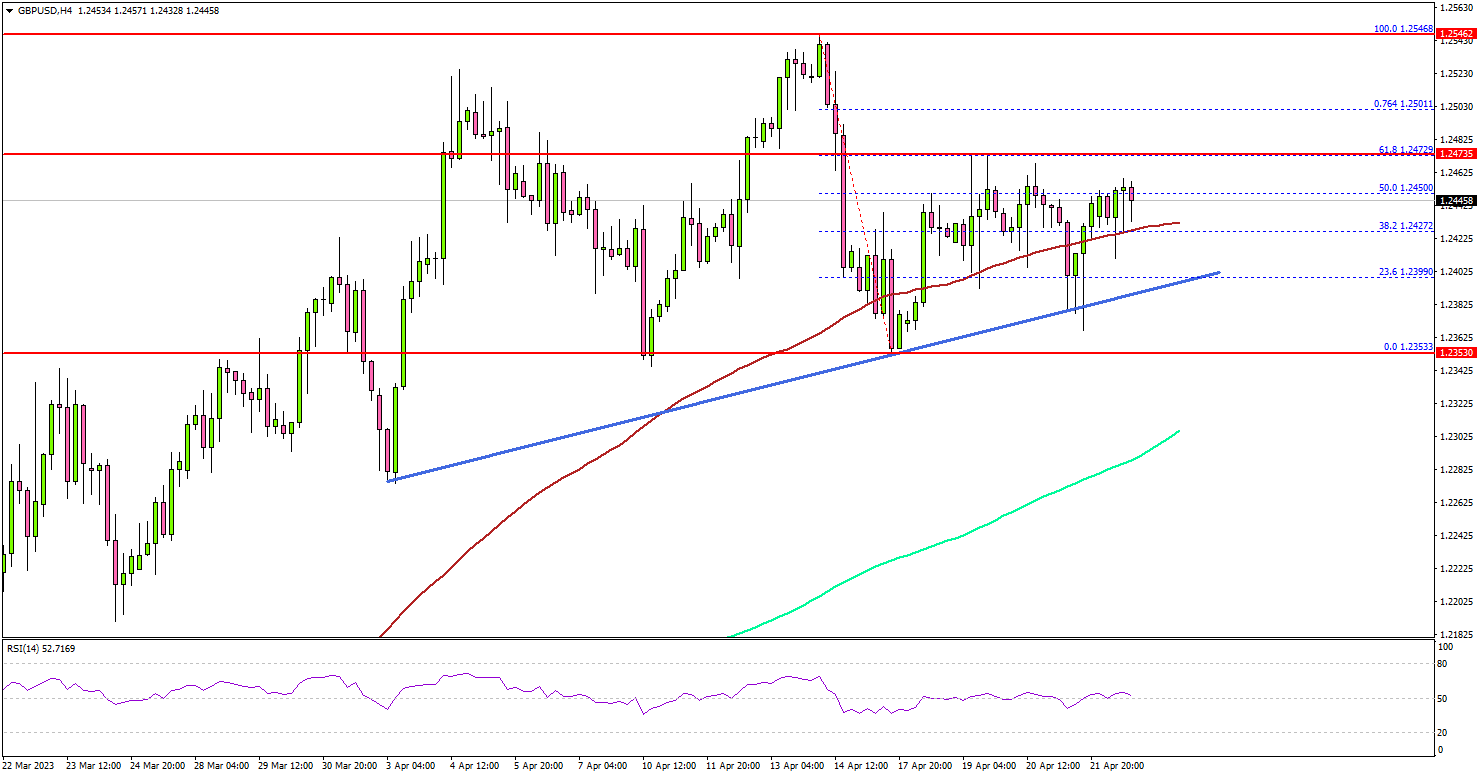

The British Pound started a downside correction from the 1.2550 zone against the US Dollar. GBP/USD declined below 1.2450 but downsides were limited.

Looking at the 4-hour chart, the pair tested the 1.2350 support zone. A low was formed near 1.2353 before the price started a fresh increase. The pair climbed above the 1.2420 level and the 100 simple moving average (red, 4 hours).

It is also trading well above the 200 simple moving average (green, 4 hours). Recently, there were a few spikes above the 50% Fib retracement level of the downward move from the 1.2546 swing high to the 1.2353 low.

The first major resistance is near the 1.2475 level. It coincides with the 61.8% Fib retracement level of the downward move from the 1.2546 swing high to the 1.2353 low.

A clear upside break and close above the 1.2745 resistance might send the pair toward 1.2520 or 1.2550. The next key resistance is near the 1.2620 zone. Any more gains might send the pair toward 1.2650.

On the downside, there is a major support forming near 1.2400. There is also a major bullish trend line forming with support near 1.2395 on the same chart. The next major support sits near the 1.2350 level, below which the pair might accelerate lower.

Looking at EUR/USD, the pair remained stable above 1.0950 and might soon attempt an upside break above the 1.1100 resistance.

Economic Releases

- US House Price Index for Feb 2023 (MoM) - Forecast -0.2%, versus +0.2% previous.

- US New Home Sales for March 2023 (MoM) – Forecast +1.1% versus +1.1% previous.