Sample Category Title

Euro and Sterling Fall Despite Markets Flipping Toward ECB and BoE Hikes

Market sentiment showed tentative signs of stabilization after the sharp panic seen at the open of the day. Oil prices eased from their initial spike following reports that G7 finance ministers would discuss the potential release of emergency oil reserves. Yet the relief remains fragile, with WTI crude still hovering above the psychologically important 100 level.

Meanwhile, beyond the immediate oil market impact, the energy shock is triggering a dramatic shift in the global interest rate narrative. Only weeks ago, markets were focused on disinflation and the prospect of continued policy easing across major economies. The surge in oil prices has abruptly flipped that narrative toward rising stagflation concerns. This shift is particularly significant for the Eurozone and the UK, which are heavily dependent on imported energy.

For the ECB, market expectations have changed dramatically. As recently as February, investors largely expected the central bank to hold rates steady for an extended period following its tightening cycle, with the next move uncertain between a cut or a hike. Now the outlook has shifted sharply. Interest rate swaps are pricing in two full 25 basis point hikes by the end of 2026. This represents a major reversal from just a week ago, when markets were still discussing the possibility of another rate cut.

The repricing has been even more dramatic for the BoE. Markets previously expected a rate cut in March to support the struggling economy. That narrative has now flipped, with traders assigning around a 70 percent probability that the next move will instead be a rate hike by the end of the year.

Both central banks now face a difficult dilemma. Cutting rates to support economic activity risks allowing energy-driven inflation to accelerate, echoing the inflation shock experienced in 2022. Yet raising rates could further weaken already fragile economies. After all, it seems that markets currently believe the ECB and BoE will ultimately prioritize inflation credibility.

This creates a paradox for currency markets. Normally, expectations of tighter monetary policy support a currency by raising yields and attracting capital inflows. Yet both Euro and Sterling have struggled to gain support despite the increasingly hawkish repricing of interest rates.

The reason lies in how investors interpret the nature of these potential rate hikes. In Europe and the UK, higher rates are not viewed as a sign of economic strength but rather as a defensive move to contain inflation triggered by an external energy shock. In other words, markets see these as “bad hikes.” The ECB and BoE may be forced to tighten policy not because growth is strong, but because inflation is rising again due to higher energy prices.

Such hikes risk deepening an already fragile economic environment. Investors fear that tighter monetary policy could push both economies closer to recession, which reduces the attractiveness of holding Euro- or Sterling-denominated assets.

At the same time, the surge in energy prices reinforces the structural weakness of the Eurozone and the UK as major energy importers. Higher import bills effectively transfer income out of the region, worsening trade balances and putting additional pressure on both currencies.

On the other hand, currencies linked to energy-exporting economies—such as Canadian and Australian Dollars—are benefiting from the same energy shock that is hurting Europe and the UK. For Australia and Canada, the Iran war is a "wealth transfer" from the rest of the world to them. As energy prices rise, their national income increases. Meanwhile, Dollar continues to attract safe-haven flows as investors seek stability during a period of war.

As for the day so far, Loonie is currently the strongest, followed by Kiwi, and then Dollar. Sterling is the worst, followed by Euro, and then Yen. Swiss Franc and Loonie are positioning in the middle.

In Europe, at the time of writing, FTSE is down -1.07%. DAX is down -1.34%. CAC is down -1.86%. UK 10-year yield is up 0.169 at 4.731. Germany 10-year yield is up 0.045 at 2.907. Earlier in Asia, Nikkei fell -5.20%. Hong Kong HSI fell -1.35%. China Shanghai SSE fell -0.67%. Singapore Strait Times fell -1.89%. Japan 10-year JGB yield rose 0.02 to 2.186.

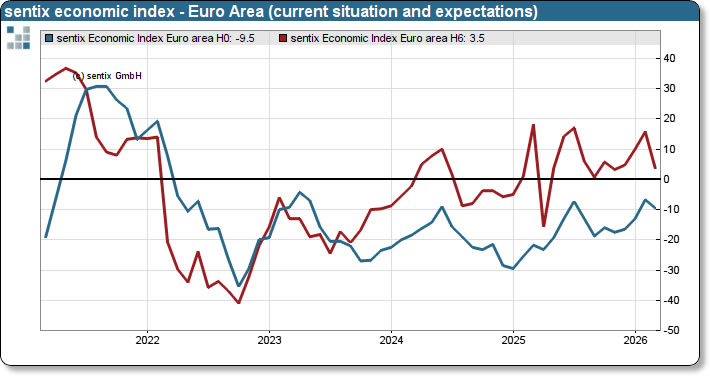

Eurozone Sentix turns negative at -3.1 amid oil surge and war

Eurozone investor sentiment deteriorated sharply in March as the escalating Middle East conflict and the surge in energy prices rattled market confidence. The Sentix Investor Confidence index fell from 4.2 to -3.1, below expectations of -1.1, marking a sudden reversal in sentiment after several months of gradual improvement.

The deterioration was visible across both current and forward-looking components. The Current Situation Index declined from -6.8 to -9.5, reflecting a weakening assessment of the present economic environment. More striking was the collapse in expectations, with the Expectations Index plunging from 15.8 to 3.5, signaling that investors have rapidly downgraded their outlook for the months ahead.

According to Sentix, the survey offers an early snapshot of the economic impact following the outbreak of the Iran war. Attacks on energy infrastructure and disruptions to shipping in the Persian Gulf have driven a sharp surge in oil prices, which in turn is weighing heavily on investor sentiment. The decline in expectations is particularly notable as it casts doubt on the Eurozone’s tentative economic recovery seen in recent months.

Rising energy costs are also reigniting inflation concerns. Sentix noted that its inflation theme barometer plunged from -7.5 to -35, indicating a sharp rise in inflation fears driven largely by turmoil in energy markets. This shift could complicate the outlook for monetary policy, as renewed inflation pressures may limit the ECB’s ability to provide further support to financial markets and the broader economy.

Japan wage momentum builds as real earnings rise first time in 13 months

Japan’s wage data delivered an encouraging signal for the BoJ at the start of the year. Real wages rose 1.4% yoy in January, rebounding from December’s -0.1% contraction and marking the first increase in 13 months. The improvement reflects a combination of stronger nominal pay and easing consumer price pressures, suggesting the prolonged squeeze on household purchasing power may finally be easing.

Nominal wage growth was robust. Total cash earnings rose 3.0% yoy, beating expectations of 2.5% and marking the fastest pace since July. Regular pay, or base salary, also climbed 3.0%, the strongest increase since October 1992. Overtime earnings rose 3.3%, the highest level in roughly three years, while special payments—largely one-off bonuses—advanced 3.8%.

The wage gains were sufficient to outpace the consumer inflation rate used by the labor ministry to calculate real wages, which slowed to 1.7% yoy in January. That was the weakest price increase since March 2022, helped by government fuel subsidies and fewer food price hikes.

Momentum in wage negotiations also remains strong. Japan’s largest labor union federation, Rengo, said last week that its member unions are seeking an average wage hike of 5.94% this year. That follows an average increase of 5.25% in 2025, the largest in 34 years, reinforcing expectations that wage growth could remain a central pillar supporting Japan’s domestic demand and the broader policy normalization narrative for the BoJ.

China CPI jumps to 1.3% as Lunar New Year spending boosts inflation

China’s consumer inflation rebounded sharply in February, offering a fresh sign of improving domestic demand. Headline CPI rose from 0.2% yoy to 1.3%, well above expectations of 0.9% and marking the strongest increase in more than three years. On a monthly basis, prices climbed 1.0% mom, also beating economists’ forecasts for a 0.5% rise.

The surge in inflation was largely driven by seasonal factors. A nine-day Lunar New Year holiday boosted domestic travel and consumer spending, pushing service prices higher and lifting the overall CPI reading. Core CPI, which excludes volatile food and fuel prices, strengthened to 1.8% yoy from 0.8% in January, indicating broader price pressures beyond the holiday effect.

Upstream price pressures also showed signs of easing deflation. PPI improved from -1.4% year-on-year to -0.9%, the smallest decline since July 2024 and stronger than expectations of -1.1%. NBS statistician Dong Lijuan said the moderation in producer deflation reflected firmer prices in advanced and emerging industries, as well as capacity management in key industrial sectors.

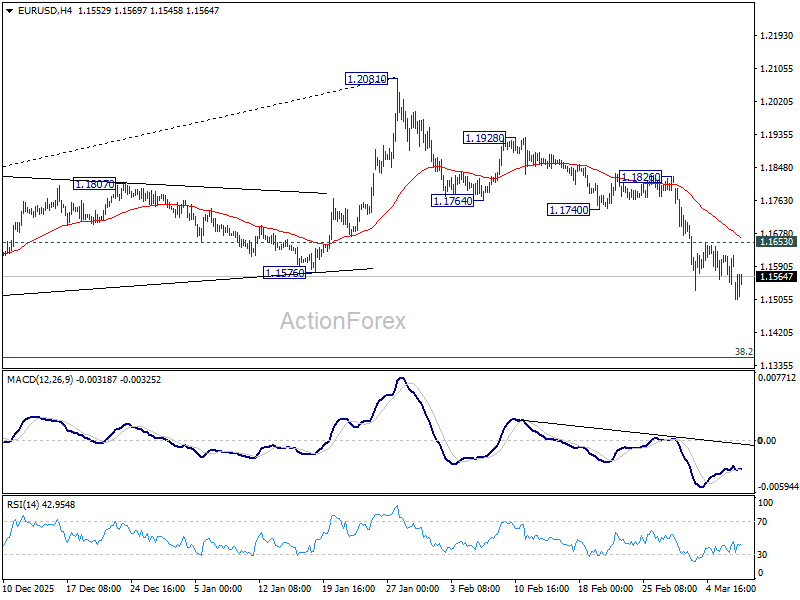

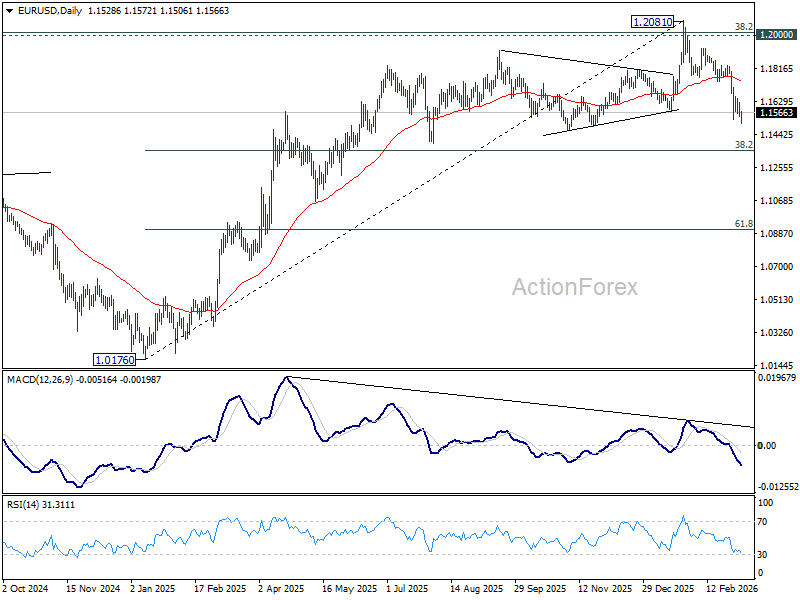

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1563; (P) 1.1594; (R1) 1.1641; More….

Intraday bias in EUR/USD remains on the downside for the moment. Current decline from 1.2081 should target 38.2% retracement of 1.0176 to 1.2081 at 1.1353 next. On the upside, above 1.1653 minor resistance will turn intraday bias neutral again first. But outlook will remain bearish as long as 1.1740 support turned resistance holds, in case of another recovery.

In the bigger picture, a medium term top should be in place at 1.2081 on bearish divergence condition in D MACD. Sustained trading below 55 W EMA (now at 1.1500) should confirm rejection by 1.2 key cluster resistance level. That would also raise the chance that whole up trend from 0.9534 (2022 low) has completed as a three wave corrective bounce too. For now, medium term outlook is neutral at best as long as 1.2081 holds, even in case of rebound.

WTI: Oil Price Spikes Near $120 as War Escalation Darkens Supply Outlook

In a widely expected scenario, WTI oil opened with big gap higher and spiked to nearly $120 per barrel (the highest since mid-2022) at the start of the week.

Growing fears of prolonged larger supply disruptions, due to closure of Hormuz strait, damaged oil installations and high risk and cost of transportation, continue to inflate oil prices and threaten of an energy crisis not seen since 1970s.

Quick break of psychological $100 barrier and rise near 2022 peak ($130) warns that oil prices may advance further and remain elevated for longer period that would cause a domino-effect and hit all sectors of world economies.

Subsequent pullback from new peak ($119.44) cracked $100 level which reverted to support, though dips would rather mark positioning for fresh push higher as escalation of the war and deepening crisis, can work only as very supportive factor for oil prices.

Supports at $100/$97.40 (psychological / Fibo 38.2% of $61.75/$119.44 upleg) should contain pullback and keep larger bulls in play for acceleration towards $130 (June 2022 high), violation of which would expose targets at $135.13 (Fibo 200% projection of the rally from $54.87) and $140 (round-figure).

Res: 105.83; 107.35; 110.00; 116.75.

Sup: 102.65; 101.00; 100.00; 97.40.

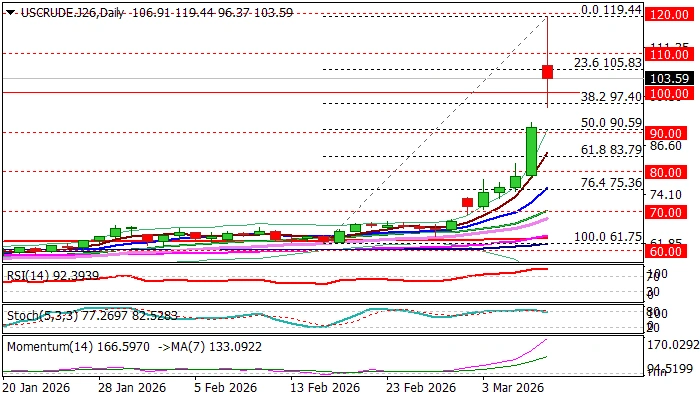

Chart Alert: WTI Crude Oil Key Short-Term Support at $102.25 for Another 20% Rally

Key takeaways

- Oil surges amid geopolitical supply fears: West Texas Intermediate crude oil jumped as much as 30% intraday to $119.54, marking its highest level since 2022, driven by concerns that the US–Iran war in 2026 could disrupt global energy flows through the Strait of Hormuz.

- Pullback after potential strategic reserve release: Prices later retraced to around $102–$103 after reports that several Group of Seven nations may coordinate a release of emergency oil reserves to ease supply pressures.

- Technical outlook remains bullish above key support: As long as WTI holds above $102.25, the short-term bullish acceleration phase may persist with potential upside targets at $124.40 and $130–$132, while a break below that level could trigger a deeper correction toward $92–$86.

West Texas (WTI) crude oil has continued its relentless bullish move in today’s Asia session, 9 March 2026, where it gapped up and staged an intraday rally of 30% to print a current high of $119.54/barrel, its highest level since June 2022.

Thereafter, WTI crude oil gains have been reduced by almost half to around 13% to trade at around $102.90/barrel after a media report highlighted that three of the G-7 countries, including the US, have expressed support for a possible joint release of their respective stockpile of oil reserves.

The recent steep rally seen in oil prices, WTI crude oil recorded a weekly gain of 35.6% for the week of March 2, 2026, its best weekly performance since the week of July 30, 1979 (+38.7%) has been attributed to a rising risk that global oil supplies may face significant shortages to the a prolong closure of the Strait of Hormuz after Iran stated that its military forces are prepared to continue an “intense war” against the US and Israel for at least six months.

Here’s the latest potential short-term trajectory (1 to 3 days) of WTI crude oil from a technical analysis perspective.

WTI Crude Oil – Minor bullish acceleration phase remains intact

Fig. 1: West Texas Oil CFD minor trend as of 9 Mar 2026 (Source: TradingView)

Watch the $102.25 tightened key short-term pivotal support on the West Texas Oil CFD (a proxy of the WTI crude oil futures). to maintain the minor bullish acceleration leg/phase from the 26 February 2026 low.

Next intermediate resistances are located at $124.40 and $130.30/132.67 (Fibonacci extension and the important major swing high of 7 March 2022, formed during the onset of Russia’s invasion of Ukraine).

However, a break and an hourly close below $102.25 negates the bullish tone to kickstart an extended minor corrective decline sequence to expose the next intermediate supports at $92.47 (lower limit of the gap support), and $86.10 (the pull-back of the former minor ascending channel resistance).

Key elements to support the bullish bias on WTI crude oil

- The current corrective pull-back from its intraday high of $119.54 has reached the 38.2% Fibonacci retracement of the recent steep rally from the 4 March 2026 low to the 9 March 2026 current intraday high.

- The hourly RSI momentum indicator has started to start a rebound from a key ascending trend line support at around the 56 level, which suggests a potential revival of short-term bullish momentum.

No One Will Help the Euro

- Europe is an unintended victim of the Middle East conflict.

- The growing likelihood of two ECB rate hikes is not enough to boost EURUSD.

The US dollar posted its strongest weekly performance in a year and may extend its rally amid intensifying geopolitical risks in the Middle East. Political developments in Iran have increased uncertainty about the conflict’s trajectory, boosting safe-haven demand for the dollar. As a result, EURUSD opened the week with a gap lower.

The rapid rise in oil prices contributed to recessions in the US economy in 1973, 1980, 1990 and 2008. And the current cooling of the American labour market, driven by the White House’s tariff and anti-immigration policies, suggests a downturn. Indeed, in February, non-farm employment fell by 92K, and the unemployment rate rose to 4.4%. However, the United States is currently a net energy exporter. Its economy will suffer less from a rally in Brent and WTI above $100 per barrel than Europe or Asia.

This is why the shock of rising oil and gas prices is reversing the ‘sell America’ flows. US stock indices have fallen less than their competitors, and the greenback has risen. Speculators have reduced their net shorts on the USD by two-thirds over the past few days.

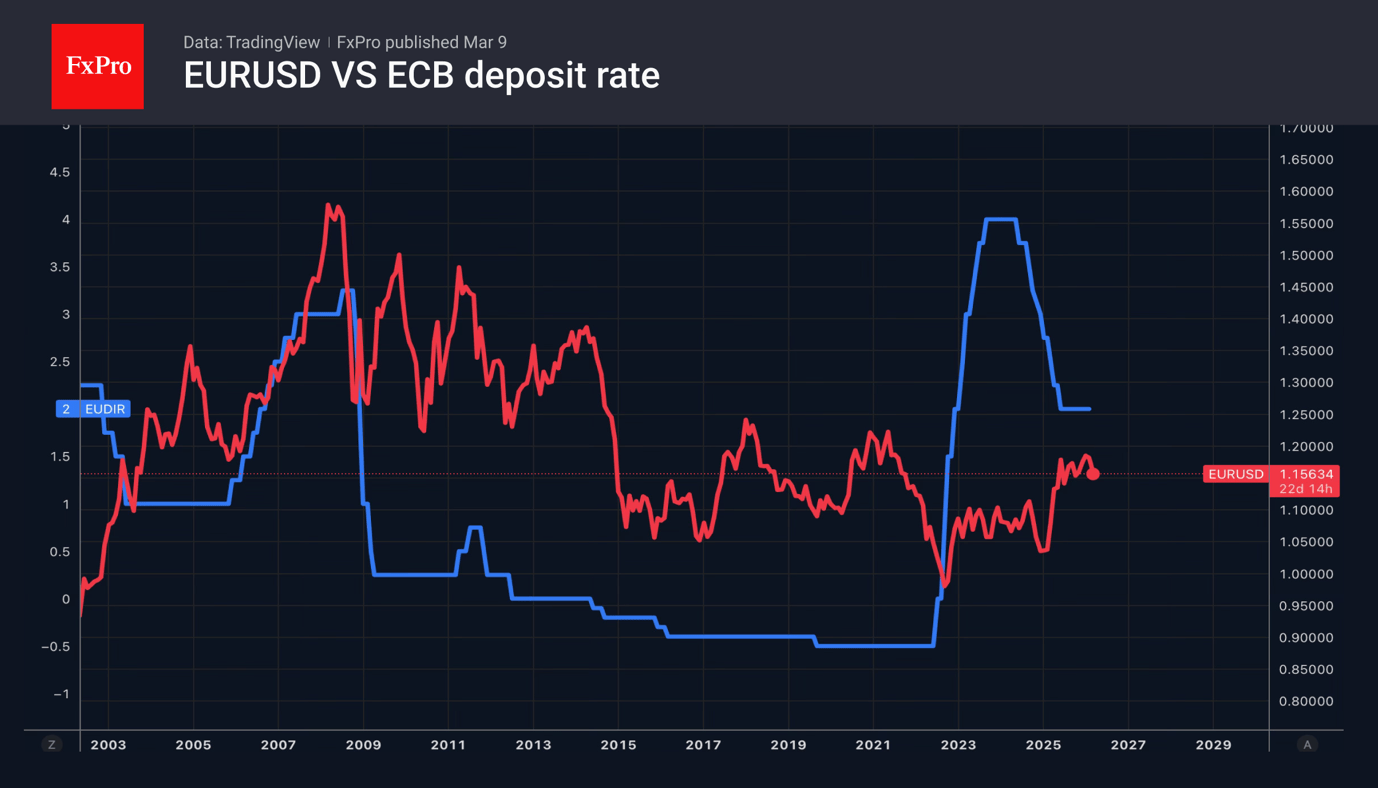

Even the increased chances of two ECB rate hikes this year to above 30% are not enough to halt the euro’s fall. Before the armed conflict in the Middle East, investors believed that the deposit rate would remain unchanged in 2026. Now they are confident it will rise from 2% to 2.25% and estimate the possibility of growth to 2.5% amid potential inflation acceleration. However, when geopolitics reigns supreme, central banks fade into the background.

The ECB is unlikely to start a cycle of monetary tightening amid serious economic pain from energy disruptions and a surge in oil and gas prices. European reserves are depleted, and the region is a net importer of energy, with the lion’s share coming from the Middle East. EURUSD rightly looks like one of the main currency pairs affected by the escalation of the conflict between the US, Israel and Iran on Forex.

Dollar Index (DXY) Hits Yearly High

Today, the dollar index rose above last week’s peak around the 99.68 level, setting a new high for 2026. This movement is supported by a tense fundamental backdrop:

- → Inflationary pressures from rising oil prices. Markets may be pricing in a “higher for longer” scenario, with elevated Fed rates persisting.

- → Safe-haven demand. Escalation in the Middle East—including strikes on Iran and the rise of hardline leader Mojtaba Khamenei in Tehran—may push market participants towards defensive strategies and the US dollar.

- → Weakness in other currencies. The Middle East conflict can weigh on the yen and euro, as European and Japanese economies remain highly sensitive to energy prices.

Technical Analysis of the DXY Chart

On the morning of 3 March, analysing the DXY chart, we:

- → drew an ascending channel (highlighted in blue);

- → anticipated that military escalation could drive the DXY index to the upper boundary of the channel.

Indeed, on the same day, the dollar index surged:

- → breaking above the channel’s upper boundary;

- → the RSI indicator entered overbought territory;

- → price slightly exceeded the January peak, signalling a possible bull trap.

As indicated by the first arrow, a long upper wick formed at the peak on 3 March, showing seller activity around the 99.60 level. Today’s brief surpassing of last week’s peak confirms this thesis, resembling a Liquidity Grab pattern.

On the other hand, buyers:

- → demonstrated strength at the market open (the bullish gap may continue to act as support);

- → can rely on support from the line dividing the upper half of the channel into two quarters (shown by the second arrow).

Traders should therefore be prepared for a scenario where DXY fluctuations show signs of stabilising near the yearly highs. Key developments around Iran are likely to have the strongest influence on the evolving balance.

Trade global index CFDs with zero commission and tight spreads (additional fees may apply). Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Eurozone Sentix turns negative at -3.1 amid oil surge and war

Eurozone investor sentiment deteriorated sharply in March as the escalating Middle East conflict and the surge in energy prices rattled market confidence. The Sentix Investor Confidence index fell from 4.2 to -3.1, below expectations of -1.1, marking a sudden reversal in sentiment after several months of gradual improvement.

The deterioration was visible across both current and forward-looking components. The Current Situation Index declined from -6.8 to -9.5, reflecting a weakening assessment of the present economic environment. More striking was the collapse in expectations, with the Expectations Index plunging from 15.8 to 3.5, signaling that investors have rapidly downgraded their outlook for the months ahead.

According to Sentix, the survey offers an early snapshot of the economic impact following the outbreak of the Iran war. Attacks on energy infrastructure and disruptions to shipping in the Persian Gulf have driven a sharp surge in oil prices, which in turn is weighing heavily on investor sentiment. The decline in expectations is particularly notable as it casts doubt on the Eurozone’s tentative economic recovery seen in recent months.

Rising energy costs are also reigniting inflation concerns. Sentix noted that its inflation theme barometer plunged from -7.5 to -35, indicating a sharp rise in inflation fears driven largely by turmoil in energy markets. This shift could complicate the outlook for monetary policy, as renewed inflation pressures may limit the ECB’s ability to provide further support to financial markets and the broader economy.

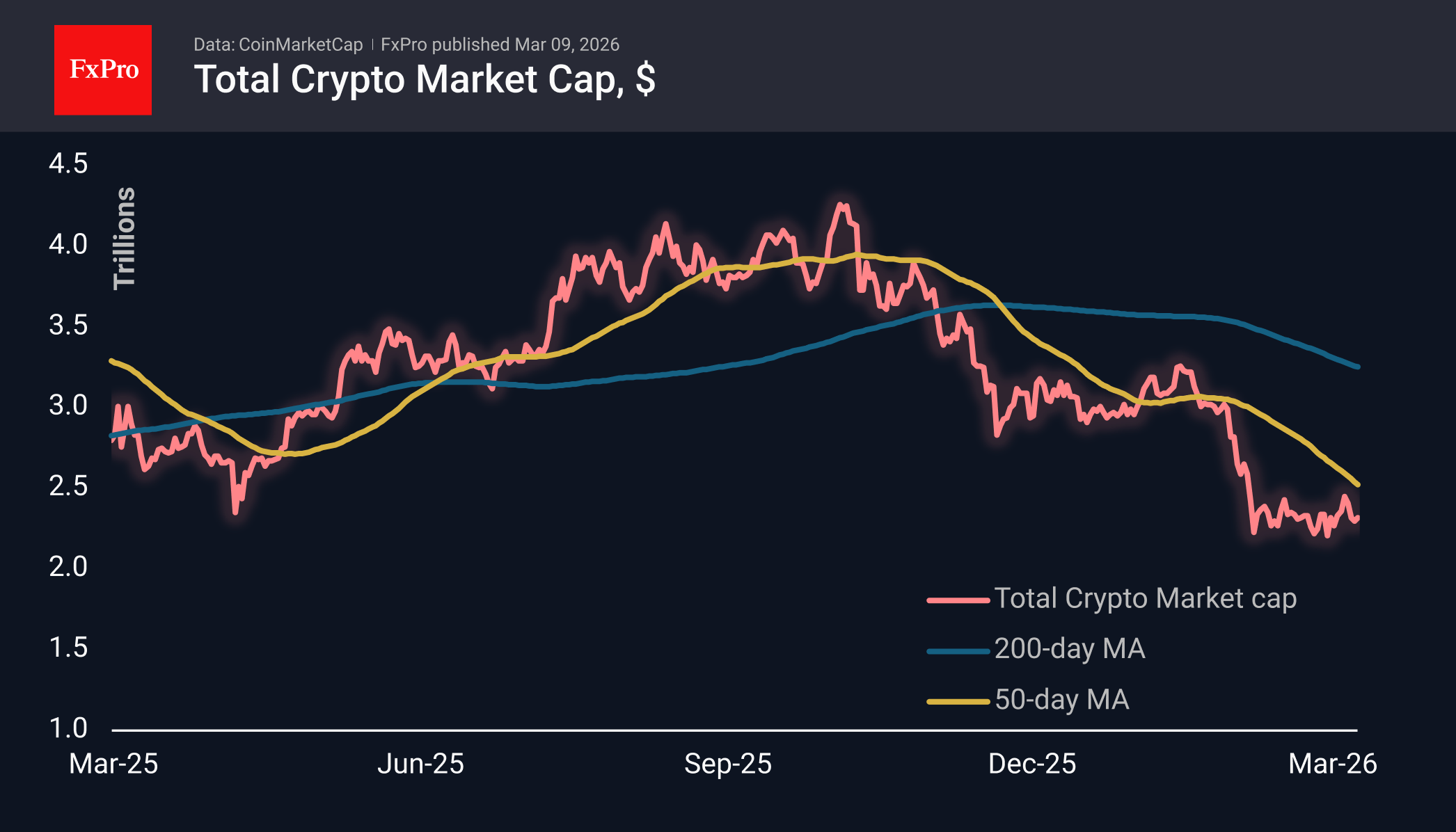

Crypto Market Has Temporarily Found Balance

Market Overview

The crypto market cap on Monday morning is $2.31 trillion, just over 1% higher than a week ago. Volatility in cryptocurrencies decreased significantly in the second half of the week, unlike in traditional financial markets. Cryptocurrencies did not emerge as a safe haven; instead, they found only a temporary balance between opposing forces. Last week, crypto failed to maintain its mid-week momentum. They are also avoiding a collapse following traditional markets, which began trading on Monday. This is too fragile a balance, and we see a greater risk of increased cryptocurrency sell-offs as institutional players are forced to reduce leverage amid the decline of key assets.

The sentiment index stood at 8 on Monday, returning to single digits after twelve days of attempts to stabilise and form a rebound. This behaviour proves once again that not all extremely low sentiment values should be considered a good entry point.

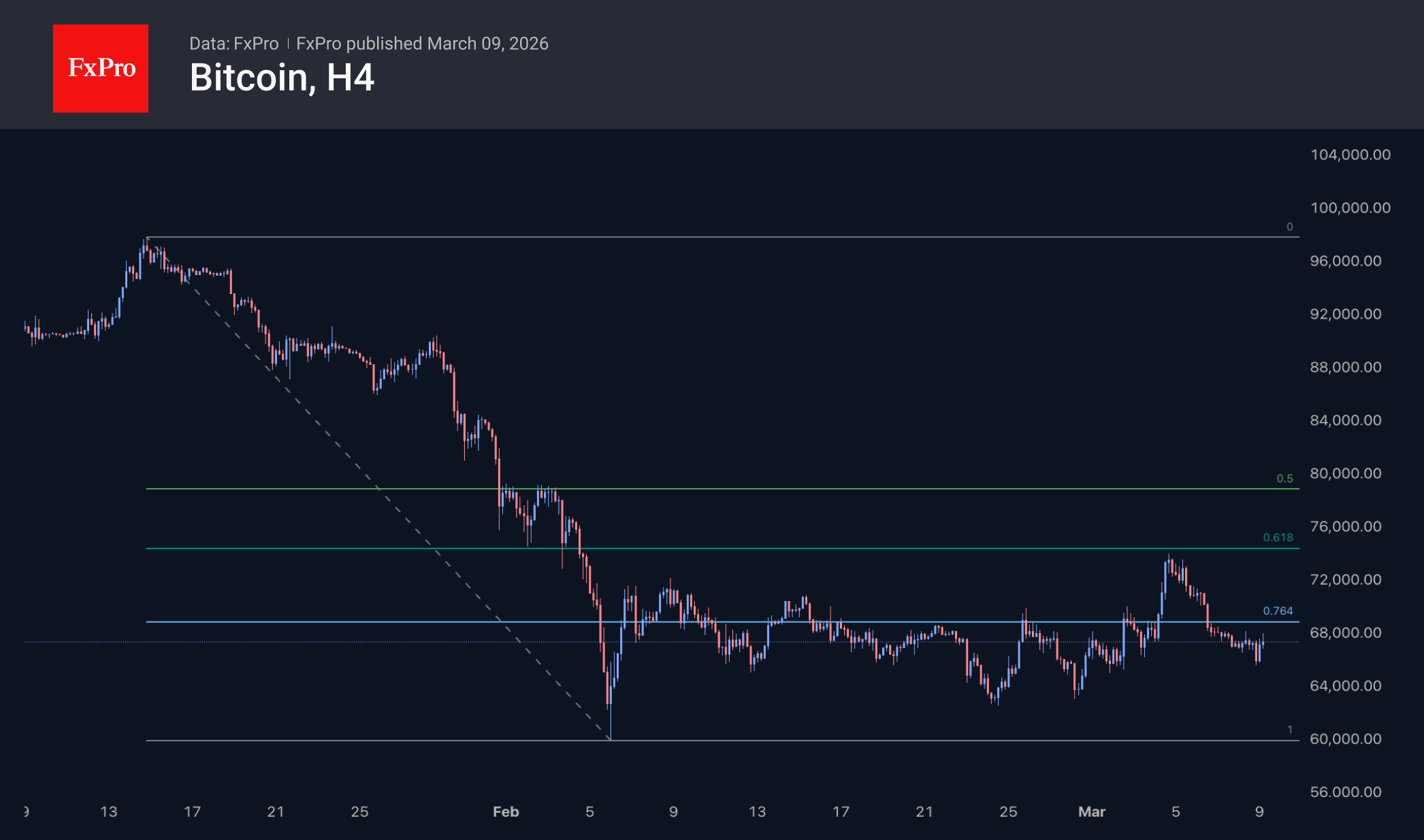

Bitcoin is trading at $67K, around which it has been for more than 4 weeks. On intraday intervals, purchases are still noticeable on dips below $66K. Still, it is difficult to rely on this support given the powerful movements in financial markets.

News Background

Bitcoin is in the deepest phase of a bear market, and the situation could worsen, according to ZX Squared Capital, which expects BTC to fall further by 30% in 2026 due to the war with Iran.

Culper Research has opened short positions on Ethereum and BitMine shares. Analysts believe that the altcoin’s economy has deteriorated following the recent Fusaka update.

For the first time in US history, the Trump administration has included cryptocurrencies and blockchain in the National Cybersecurity Strategy, which explicitly states the need to protect these technologies at the state level.

Florida has passed the first state-level stablecoin bill in the US. Governor Ron DeSantis will sign the document within the next 30 days.

The US SEC has dropped charges against Justin Sun. The founder of Tron agreed to pay a $10 million fine but did not admit guilt. In 2023, the SEC accused Sun of unregistered sales of securities in the form of Tron and BitTorrent cryptocurrencies, as well as fraudulent price manipulation.

About 38% of altcoins have approached historic lows. The situation in the sector is worse than after the collapse of the FTX crypto exchange, notes analyst Darkfost.

WTI Oil Price Rises Above $100

Another shocking Monday for the energy market. Last week’s start was remembered for a bullish gap of more than 10% (which was later followed by a pullback), but today’s market open proved even more volatile (as reflected by the ATR indicator). After a bullish gap of roughly 11%, the price continued to climb, reaching a peak of around $114 per barrel of WTI during the Asian session. This is the highest price since 2022.

The drivers of the rally are obvious – the escalation of the war in the Middle East, with more countries becoming involved. Risks have reached a critical point, with discussions emerging around the scenario of a complete blockade of shipping through the Strait of Hormuz. In such a case, oil-producing countries could invoke force majeure as grounds for halting supplies.

Technical Analysis of the XTI/USD Chart

Analysing the oil price chart a week ago, we assumed that the $70 level would act as support. Indeed, the market remained above this psychological level, while rising highs and lows reflected traders’ concerns.

Extreme volatility must be taken into account when applying classical technical patterns. Today, the oil price chart allows us to draw a broad ascending channel with a steep slope. In this context, it is worth noting (as indicated by the arrows):

- → the rapid rise in oil prices within the upper quarter of the channel;

- → the subsequent reversal and a swift decline towards the median.

This price action (essentially resembling a Bearish Engulfing pattern) points to a sharp shift in sentiment.

From the bulls’ perspective → the median of the wide channel, reinforced by the psychological $100 level, may act as support.

However, judging by the extremely wide candle, during which the XTI/USD quote dropped from $111 to $100 today, it is reasonable to assume that the initiative currently lies with the bears. And even if a rebound from the median occurs, it may fade near the $105 level (which has already acted as resistance on lower timeframes).

Start trading commodity CFDs with tight spreads (additional fees may apply). Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

AUD/USD and NZD/USD Struggle as Market Jitters Shake Risk Sentiment

AUD/USD failed to stay in a positive zone and declined below 0.7000. NZD/USD is also moving lower and might extend losses below 0.5850.

Important Takeaways for AUD/USD and NZD/USD Analysis Today

- The Aussie Dollar started a fresh decline from well above 0.7100 against the US Dollar.

- There is a bearish trend line forming with resistance at 0.7020 on the hourly chart of AUD/USD at FXOpen.

- NZD/USD declined steadily from 0.6000 and traded below 0.5900.

- There is a key bearish trend line forming with resistance at 0.5900 on the hourly chart of NZD/USD at FXOpen.

AUD/USD Technical Analysis

On the hourly chart of AUD/USD at FXOpen, the pair struggled to clear 0.7150. The Aussie Dollar started a fresh decline below 0.7050 against the US Dollar.

The pair even settled below 0.7000 and the 50-hour simple moving average. There was a clear move below 0.6980. A low was formed at 0.6956, and the pair is now consolidating losses. There was a minor recovery wave above the 23.6% Fib retracement level of the downward move from the 0.7089 swing high to the 0.6956 low.

On the upside, immediate hurdle is near the 50-hour simple moving average and the 50% Fib retracement at 0.7020. There is also a bearish trend line forming with resistance at 0.7020.

The next major level for the bears could be 7060. The main selling point could be 0.7090, above which the price could rise toward 0.7140. Any more gains might send the pair toward 0.7200. A close above 0.7200 could start another steady increase in the near term. In the stated case, the next key resistance on the AUD/USD chart could be 0.7280.

On the downside, initial support is near 0.6975. The next area of interest might be 0.6955. If there is a downside break below 0.6955, the pair could extend its decline. The next target for the bears might be 0.6920. Any more losses might send the pair toward 0.6900.

NZD/USD Technical Analysis

On the hourly chart of NZD/USD on FXOpen, the pair also followed a similar pattern and declined from the 0.6000 zone. The New Zealand Dollar gained bearish momentum and traded below 0.5950 against the US Dollar.

The pair settled below 0.5900 and the 50-hour simple moving average. Finally, it tested 0.5850 and is currently consolidating losses. There was a minor increase above the 23.6% Fib retracement level of the downward move from the 0.5948 swing high to the 0.5848 low.

If the pair recovers, it could face hurdles near 0.5900 and a key bearish trend line. The next major barrier is at 0.5910 since it coincides with the 61.8% Fib retracement.

If there is a move above 0.5910, the pair could rise toward 0.5950. Any more gains might open the doors for a move toward 0.6010 in the coming days. On the downside, immediate support on the NZD/USD chart is 0.5850.

The next major stop for the bears might be 0.5835. If there is a downside break below 0.5835, the pair could extend its decline toward 0.5800. The main target for the bears could be 0.5740.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

WTI Crude Oil Soars Over 30% Before Settling Below 120.00

- WTI crude oil posts a bullish gap, reaching its highest levels since July 2022.

- Iran-related tensions fuel upward pressure, but rally could be short-lived.

- Momentum indicators mirror the surge, extending into overbought territory.

WTI crude oil surged more than 30% on Monday, reaching its highest levels since mid‑2022, as the deepening conflict in the Middle East intensified supply‑disruption fears, further amplified by the appointment of Iran’s new supreme leader. The rally pushed prices just shy of the 120.00 level before easing lower toward the 102.00 area.

If the pullback extends, as the price action currently continues to retreat from the intraday spike, a sustained break below the 200% Fibonacci level at 103.97 and a stabilization near the 102.00 area would expose the next support at 94.63, followed by 92.80, which marks an over two‑and‑a‑half‑year high. Below that, additional support is located in the 88.87-85.30 region.

That said, the technical indicators reinforce the strong bullish momentum, with the RSI pushing deep into overbought territory, and the MACD continuing to overextend above zero and its red signal line.

Thus, if the accelerated buying persists above the 261.8% Fibonacci retracement level of the June-December 2025 downleg at 119.58, the price could retest resistance at the June 2023 highs near 123.70, followed by the March peaks in the 127.00-130.00 zone.

Overall, WTI crude oil has extended a six‑day rally to climb toward nearly four‑year highs. However, with price action now paring gains and volatility triggering aggressive swings between 98.00 and 120.00, the advance may pause, potentially allowing for a retracement toward the 90.00 region before the broader uptrend resumes.