Sample Category Title

Expect Markets to Still be Pushed Back and Forth by Headlines on Conflict in the Middle East

Markets

Yesterday’s price moves on almost all markets were again highly correlated to the intraday swings in oil prices. Brent oil in Asian trading almost touched the $120 p/b level as the there was no indication after the weekend that the conflict in the Middle East would end anytime soon. Iran approving Mojtaba Khamenei as new leader at least suggested that the country didn’t intend to prepare for the regime change the US was hoping for. The sharp rise in oil prices in a first reaction intensified a broad stagflation trade/risk-off trade. Short-term yields jumped sharply higher. EMU 2-y swap at some point early in the session jumped about 20 bps higher. The UK 2-y gilt yield even jumped close to 30 bps intraday. A sharp reappraisal also occurred on smaller markets with currencies being highly sensitive to global risk sentiment (Hungary). European equities initially tumbled sharply (Europe -2%+). The dollar remained the primus inter pares. Throughout session, oil price gradually eased and this also removed some pressure from the above-mentioned risk-off stagflation trade. Markets maybe took some comfort from the G7 pondering options to use strategic oil reserves to try to manage the jump in oil prices. Sentiment improved further in US dealings. US president Trump later suggested that the war might end soon but wasn’t concrete on an exact timing. He also suggested waivers on oil sanctions and US action/escorts to keep passage at the Strait of Hormuz. Even as the President’s guidance was far from specific, markets drew some further comfort, reversing part of the early session ‘panic trade’. Oil closed below $100 p/b and this morning even is seen near $94. US yields at the end of the day even eased 2-3 bps across the curve. German yields, despite wild intraday swings closed with day changes of less than 1 bp. US equity indices even finished in green (S&P 500 +0.83%). The intraday setback of the oil price also eased the bid for the dollar. DXY closed off the intraday highs (99.17). EUR/USD again avoided a close below 1.16.

Asian markets this morning also show relief in the wake of President Trump’s comments overnight. The Nikkei gains 2.9% with almost all other regional markets in green. The dollar mostly holds the overnight setback (DXY 98.75, EUR/USD 1.163). Later today, one can expect markets to still be pushed back and forth by headlines on the conflict in the Middle East. We look out whether some stabilization can kick in at the short end of the yield curves in the likes of EMU and the UK. EMU money markets are pondering the need for the ECB to address inflationary risks and discount about 50%-75% chance of a rate hike by summer. UK money markets fully priced out any further BoE easing. Interesting to hear the assessments of Powell, Lagarde and Bailey as they all hold policy meetings next week. On FX, we stay cautious to row against the USD-friendly stream also as visibility on the conflict in the Middle East remains as low as it is. EUR/USD 1.1507/1.1492 remains next reference on the technical charts.

News & Views

Inflation expectations ticked down at the short-term horizon, the NY Fed February survey showed yesterday. The one-year ahead gauge eased by 0.1 ppt to 3% while three- and five-year-ahead horizons held steady at 3%. Labor market expectations declined slightly overall with the one-year-ahead earnings growth expectations decreasing to 2.5%, just below the trailing twelve-month average. The expected quit rate (leaving a job voluntarily), in the next twelve months decreased to 15.9%, a new series low while the perceived probability of finding a job in the next three months if one’s current job was lost decreased to 44%. This contrasted with expectations of a higher unemployment rate one year from now falling by 2 ppts to 39.9% The perceived probability of missing a minimum debt payment over the next three months fell to the lowest level since February 2024, decreasing by 2.1 ppts to 11.6%.

The British Retail Consortium (BRC) reported a slowdown in the UK's retail sales growth with the y/y printing at 1.1% in the four weeks ending February, down from 2.7% in January and below the 12-month average growth of 2.3%. Food sales rose 2.9% from 3.8% in January while non-food sales dropped compared to February of last year. The -0.4% y/y contrasted with a 1.7% bump the month before. Same store sales grew by 0.7%, the slowest pace since May of last year. Food sales rose by 2.3% while the non-food sector reported a 0.6% annual drop. "February's grey, wet weather hit retail sales hard," BRC Chief Executive Helen Dickinson said, adding that "Spending was weak across most categories, online and in-store, as households pulled back after Christmas and January's rebound.” Retailers looking to spring and better weather to revive sales see that case undermined by the conflict in the Middle East.

Chart Alert: Hang Seng Index Recovered at 24,765, Bulls Need to Break Above 26,350

Key takeaway:

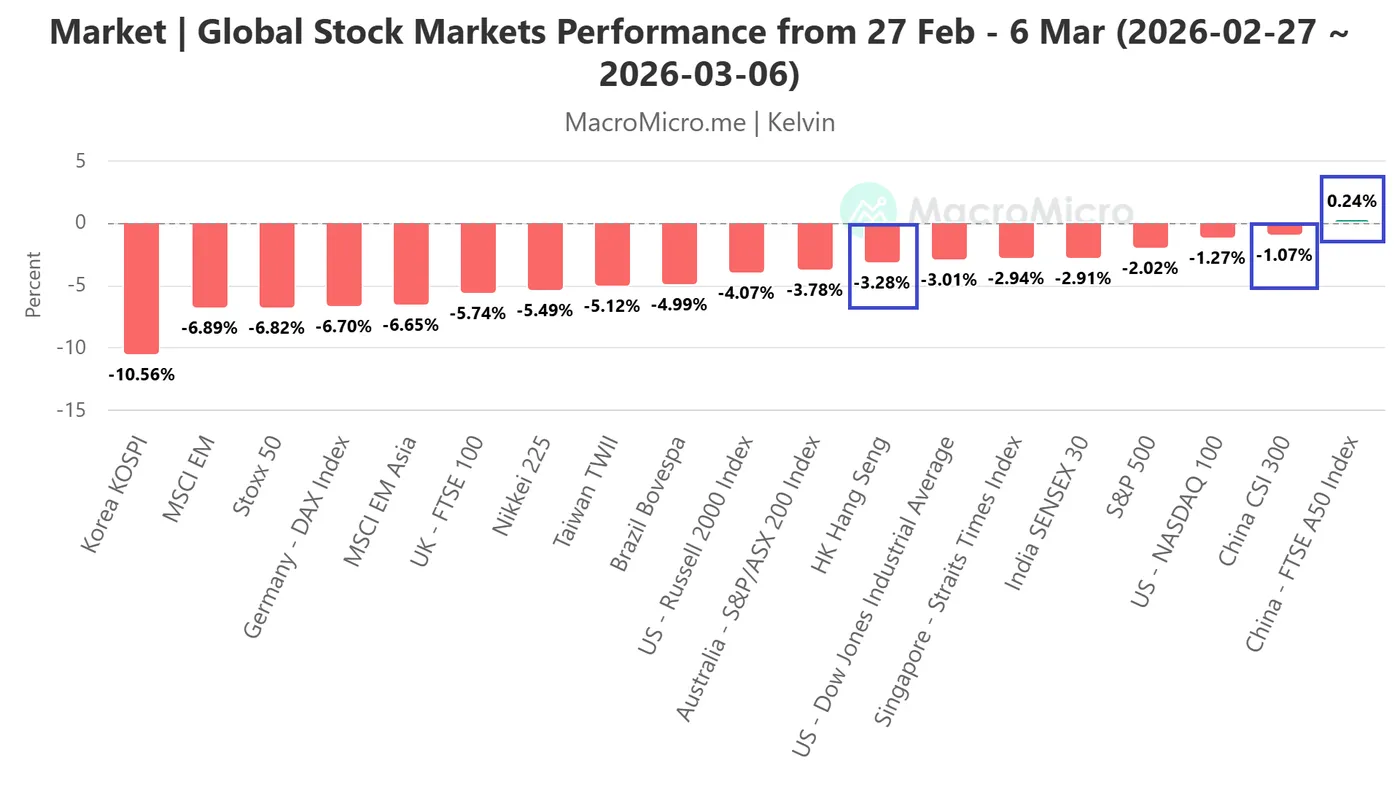

- Relative resilience in Asia: The Hang Seng Index and CSI 300 outperformed most Asian peers during the US–Iran war 2026, declining only -3.3% and -1.1% respectively from 27 Feb to 6 Mar, while markets like the KOSPI and Nikkei 225 suffered deeper losses amid rising oil-driven stagflation fears.

- Policy supports cushioning markets: Investor sentiment in China and Hong Kong improved after signals from the National People's Congress, where Li Qiang outlined a 4.5%–5% growth target and a stronger focus on boosting domestic consumption and reversing deflation risks.

- Key technical levels to watch: The Hang Seng Index rebounded from 24,765 long-term support and reclaimed its 200-day moving average. Bulls need a break above 26,350 to confirm a stronger recovery, while a drop below 25,385 risks a retest of the 24,765 support zone.

The China and Hong Kong benchmark stock indices have outperformed their major Asian Pacific peers among global stock indices in the ongoing 10-day US-Iran war.

Based on a reference period from 27 February 2026 to last Friday, 6 March 2026, where the start of the reference period is one day before the US-Iran war kick-started on 28 February, Hong Kong’s Hang Seng Index and China’s CSI 300 shed -3.3% and -1.1% respectively, while the narrower China A50 was almost unchanged (+0.2%) (see Fig. 1).

Fig. 1: Performances of global benchmark stock indices from 27 Feb 2026 to 6 Mar 2026 (Source: MacroMicro)

In contrast, South Korea’s KOSPI plummeted 11% (the worst hit), and Japan’s Nikkei 225 declined by 5.5% due to stagflation fears from higher oil prices.

China, Japan, and South Korea are significant net oil importers. The reason why China and Hong Kong stock markets have managed to take a lesser “bearish hit” from the recent upward spiral in oil prices (WTI crude oil staged a weekly gain of 35.6% for the week of 2 March 2026) was due to guidance on China’s next 5-year economic strategy during last week’s key National People’s Congress meeting.

China’s leadership has set a lower economic growth rate target of 4.5%-5% for 2026, the least ambitious to rebalance China’s economy from exports, its current growth driver. In addition, Premier Li Qiang’s speech has made a subtle acknowledgment of deflationary risk towards the economy, and pledged to bring prices back into positive territories, and called for a modest rebound in the inflation trend (versus last year’s vaguer speech to get prices to a reasonable range).

Hence, such statements and new growth targets from China’s leadership suggest that top policymakers are making domestic consumption have a more significant influence in driving China’s economic growth in the next five years.

Let’s now look at the short-term trajectory (1 to 3 days) of the Hang Seng Index from a technical analysis perspective

Hang Seng Index – Rebounded back above the key 200-day moving average

Fig. 2: Hong Kong 33 CFD index minor trend as of 10 Mar 2026 (Source: TradingView)

Fig. 3: Hong Kong 33 CFD index major & long-term secular trends as of 10 Mar 2026 (Source: TradingView)

The recent -11% decline seen from the Hong Kong 33 CFD index (a proxy of the Hang Seng Index futures from its 26 January 2026 high to Monday’s 19 March 2026 low of 24,882 has stalled right at the 24,765 long-term pivotal support depicted on its weekly chart (see Fig. 3).

Today, it has staged an intraday rebound of 1.6% and traded back above the 200-day moving average at the time of writing, reinforced by US President Trump’s remarks that signaled a possible end to the current US-Iran war.

Watch the 25,385 key short-pivotal support on the Hong Kong 33 CFD index for a potential minor recovery in the first step to test the 26,350 key intermediate resistance.

A clearance above 26,350 (also the descending channel resistance in place from 29 January 2026 high, and close to the 20-day/50-day moving averages) suggests a bullish exit and a possible start of a new bullish impulsive up move sequence for the next intermediate resistances to come in at 26,690 and 27,100 in the first step (see Fig. 2).

On the other hand, failure to hold and an hourly close below 25,385 invalidates the recovery scenario for a push down to retest the 24,765 key long-term pivotal support.

Key elements to support the bullish bias on the Hang Seng Index

- Today’s positive price reaction has occurred right above the 24,756 key long-term pivotal support and the reintegration back above the 200-day moving average (see Fig. 3).

- The hourly RSI momentum indicator has flashed out a prior bullish divergence condition at its oversold region before it stages the bullish breakout above its descending trendline resistance today (see Fig. 2).

Wild Fluctuations

Rare are days in the markets when you get this much volatility. Asian indices were deeply sold, while US and European futures were down by 2–3% as US crude prices had spiked to $120pb on escalating conflict in the Middle East. But crude spent the day retracing gains and ended Monday’s session more than 7% lower – near the $85pb level.

The catalyst was the announcement that the G7 countries could release their strategic reserves. The latter really helped pour cold water on the crude rally. European indices recovered early losses and US indices ended the day in the positive on mounting speculation that the Iran war would end ‘soon’. How soon? No one knows. But not ‘this week’ according to Trump. But the Nasdaq gained up to 1.38%. Bulls are impatient to trigger a fresh rally – without a dip this time. Why bother waiting?

The problem is that the strategic reserves the G7 said they could release amount to about 300–400 million barrels reportedly. Global oil demand is about 100 million barrels per day. So we’re talking about roughly 3–4 days of global demand. That’s not much.

Plus, Middle East producers are now cutting oil production as storage facilities fill up… and Saudi Arabia is reportedly selling more oil for immediate delivery whereas they normally prefer long-term contracts – meaning they’re trying to feed the market as fast as they can.

Other – more noteworthy – news is that Saudi Arabia is rerouting its crude toward Yanbu in the Red Sea, from where it could export up to 5mbpd (Saudi produces around 10mbpd and exports roughly 7mbpd of it). The latter wouldn’t be a perfect solution but could help. If things go really badly, Russian oil could re-enter the circuit.

But the latter measures may not pull oil prices back to pre-war levels: US crude was trading below $68pb before the Iran operation. It could stay above $80pb until there is a clear resolution.

Of course, market pricing changes by the minute, but yesterday’s spike in oil prices shook European Central Bank (ECB) and Bank of England (BoE) expectations quite dramatically, as rising oil prices combined with a stronger US dollar would immediately push inflation higher in Europe.

As such, swaps were pointing to two full 25bp rate hikes from the ECB this year, compared to just one rate hike last Friday. Meanwhile, BoE expectations swung from rate cuts to a potential rate hike as inflation in the UK – which is very sensitive to energy prices – could end up more than double the BoE’s pre-war expectations, according to ING forecasts. They see inflation nearing 5% in Q3, versus earlier expectations that inflation would ease toward the BoE’s 2% target by that time.

The funny thing is that BoE hike expectations were valid only a part of the session. By the time the session ended, the rate hike chances had fallen back to neglectable levels, leaving behind crazy volatility and deep uncertainty about what’s to come.

Pricing in FX reflects the volatile expectations – of course. The EURUSD tested and rebounded from the 1.15 mark yesterday, but the move was mostly about the US dollar gaining and then giving back gains as the session moved from fear to greed. Same with Cable: the pair dipped below 1.33 at the open and ended the session above 1.34. The USDJPY approached the 159 level – here we’re very close to levels that spook officials and could trigger at least a verbal intervention to slow the yen depreciation. But at the end of the day, it all comes down to the US dollar – and the war headlines and energy prices.

So this uncertainty will continue. The fact that investors overreact to every piece of news without questioning feasibility adds another layer of difficulty when navigating markets. Part of yesterday’s optimism came after Trump said the war would end ‘soon’ and that the US was ahead of schedule. Concretely, however, the conflict in the Middle East continues at full speed, political developments are not pointing to a near-term resolution, and there is little clarity about the US plans in this war – even officials’ statements sometimes contradict each other.

As a result, crude is rebounding this morning – it was up around 5% when I first came to my desk this morning and is now up by less than 3% at the time I write this sentence. The price action will depend on geopolitical developments. The best thing to do is hold on and avoid reacting in panic if you have the possibility to do so.

Speaking of inflation, the world is facing energy-led inflation. Fertilizer prices are rising – as we discussed in detail yesterday – threatening to push global food inflation higher as well. Then there is memory chip inflation, which will push the prices of PCs, cars and gaming consoles higher. How high? It depends on companies’ ability to pass these costs onto customers. Bloomberg reports that in some cases DRAM prices – the most common working memory in computers – have surged by around 700%. So we’ll see.

In a rare piece of good news in yesterday’s session, HPE gave a better-than-expected revenue outlook when it released earnings, and its stock jumped more than 3%, while Oracle – a barometer of AI infrastructure spending risks – is due to announce earnings today after the bell.

Investors will focus less on the headline numbers and more on whether Oracle can confirm that AI-driven cloud demand remains as strong as markets believe. The key metrics will be growth in Oracle Cloud Infrastructure (OCI), the size of its AI-related backlog and capex guidance for new data centers. Strong OCI growth and rising backlog would signal that companies are still aggressively spending on AI computing power—reinforcing demand for chips from Nvidia and supporting the broader AI infrastructure trade. But if cloud growth slows or capex rises without clear demand visibility, investors may question whether the AI investment boom is running ahead of real revenue and revive worries that the industry is taking on too much leverage.

Oil Takes Centre Stage as Markets Rebound Globally

In focus today

Markets will be looking closely for any additional comments from the Trump administration confirming or rejecting the narrative that the war in the Middle East is getting close to an end.

From the US, the NFIB's small business optimism index is due for release for February. Business sentiment has recovered gradually over winter.

After surprisingly high Norwegian inflation in January, the February figures released today will be extremely important in terms of the interest rate outlook going forward. We suspect that part of the price increase in January was one-off effects that will not be reversed in February, while some of it is probably an expression of underlying price pressure in parts of the economy. We expect that core inflation rose 0.7% m/m in February, which is roughly in line with the historical pattern. Due to base effects, this will pull the annual growth rate down to 3.0%, because both food prices and non-rent service prices will rise somewhat less than last year.

In Denmark, February inflation data is released today. This inflation print includes about 70% of the yearly rent increases. Considering the 21% weight of rents in the consumer basket, this is key for the inflation level throughout the coming year. It will also be interesting to see whether the declining trend in food inflation continues. We expect inflation at 0.9%, up from 0.8% in January on particularly higher electricity prices.

In Sweden, focus will be on the January activity data released today. While the GDP indicator tends to be volatile, it can offer an early signal for actual growth trends. The consumption indicator, typically more stable, will provide valuable insight into the situation for households.

Economic and market news

What happened overnight

Global markets rebounded overnight, following sharp declines on Monday, as US President Donald Trump suggested the war in Iran could end soon, easing fears of prolonged inflationary pressures. The oil market has been on a rollercoaster ride, with Brent crude trading as high as 119 USD/barrel early Monday before plunging to as low as 88 USD/barrel last night. At the time of writing, it trades around 94 USD/barrel, as the market weighs Trump's comments, the possible easing of oil-related sanctions on Russia, and a potential release of strategic reserves. The key focus remains whether oil shipments through the Strait of Hormuz will resume.

Asian markets staged a strong recovery, with Japan's Nikkei up 2.4% and South Korea's Kospi up 4.6% at the time of writing, while European futures pointed higher. In the US, the S&P 500 rebounded after Monday's decline, where the Dow Jones and S&P 500 closed at +0.8% and +0.5%, respectively. Bond yields retreated, with the US 10-year Treasury yield down to 4.12%, as inflation concerns eased slightly.

In China, exports surged 21.8% y/y in January-February, significantly exceeding expectations (7.1%). The growth was driven by strong electronics demand and surprising strength in clothing, textiles and bags. The trade surplus reached USD 213.6bn, highlighting China's export resilience despite US tariff policies. The robust export momentum is broadly expected to continue, supported by demand for electric vehicles, batteries and solar cells.

What happened yesterday

Iran's Revolutionary Guards declared they would block all oil exports from the Middle East if US and Israeli attacks continue, effectively shutting the Strait of Hormuz, which handles one-fifth of global oil supply. In response, US President Donald Trump warned that any attempt to block oil shipments would result in far harsher strikes, stating the US would hit Iran "twenty times harder" than before. The development underscores the likelihood of prolonged tensions in the region but apparently eased market expectations.

In the US, Anthropic filed lawsuits against the government to challenge its designation as a supply-chain risk and blacklisting of its AI technology, Claude, for military use. The Pentagon's decision stems from Anthropic's refusal to remove restrictions on using its AI for autonomous weapons and domestic surveillance, citing ethical concerns. President Trump ordered all federal agencies to cease using Claude, escalating tensions between Anthropic and the government.

In pharmaceuticals, Novo Nordisk struck a deal with US telehealth company Hims & Hers to sell its blockbuster Wegovy and Ozempic drugs directly through Hims' platform. The deal resolves a legal dispute from February and focuses on offering FDA-approved treatments at competitive prices (USD 149-299/month). Shares of Hims rose 36% while Novo Nordisk rose 2.7% following the announcement, as the deal reflects growing demand for accessible obesity treatments and strengthens Novo's position amid rising competition in the US market.

In the euro area, the Sentix investor confidence indicator declined to -3.1 from 4.2, in line with consensus expectations. The drop was largely attributed to the war in Iran, which has unsettled investors and financial markets.

Equities: Equities followed the oil price yesterday. S&P 500 that was scheduled to decline at least 2% according to morning futures eventually closed 0.9% higher amid the oil price plunge. Stoxx 600 that was down more than -2% at open, closed down a meagre -0.6%. European futures indicate an opening just below 1% today. US futures have dipped into negative, however, as the oil price has rebounded somewhat since close.

It is not the level of the oil price but the longevity of it that matters for equities. Our capital goods analysts have estimated that a 10% rise in the oil price hits operating earnings in their companies between 1-3%, all things held constant. A 120-dollar oil price would thereby strip off anything between 7-20% - sizable indeed, if it would last. Perhaps this has served as a timely reminder to investors on why software multiples have had a premium to HALO-sectors in the past, as software is immune to raw material spikes or tariffs, for that matter. Tech stocks rebounded last week and continued to fare well yesterday, with the US tech sector up 2% in the US session, thereby outperforming the worst performing sector, financials, by 2.5pp.

FI and FX: Energy markets were the big mover yesterday as risk-off sentiment continued, USD strengthened and equities declined. Brent crude declined from an overnight high of almost USD 120/bbl to just below USD 100/bbl. Fixed income sold off heavily in the morning session but recovered throughout the day and yields ended the day at an almost unchanged level. The market is weighing US President Trump's hint that the war could end soon, possible easing of oil related sanctions on Russia and release of strategic reserves. Overnight, EUR/USD rose back above 1.16, UST yields declined and equities rebounded.

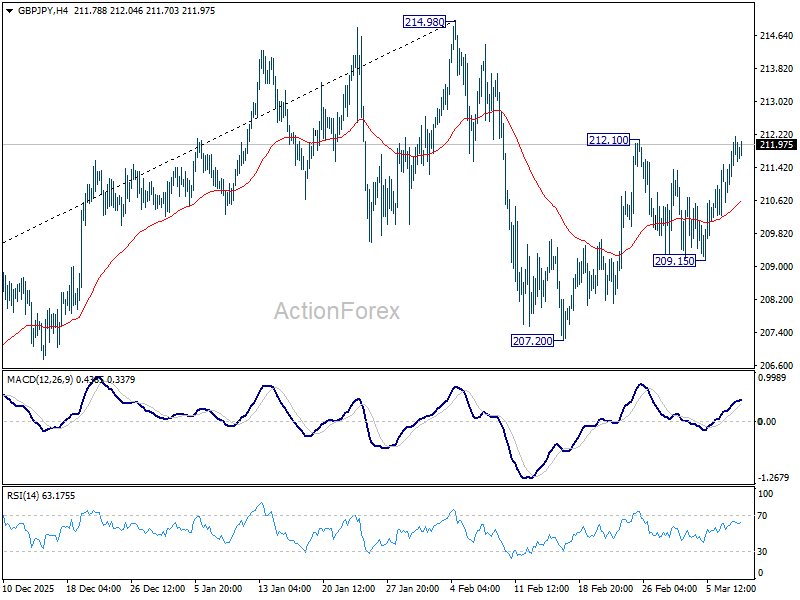

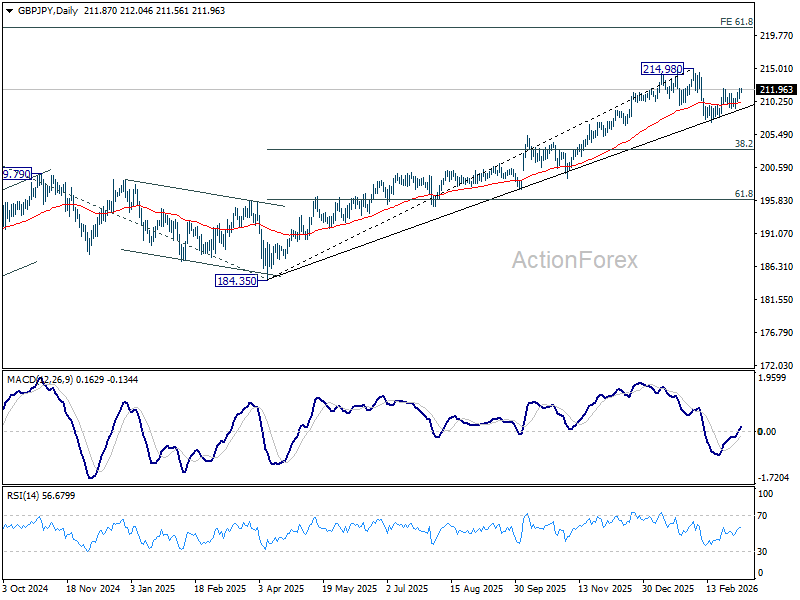

GBP/JPY Daily Outlook

Daily Pivots: (S1) 210.95; (P) 211.57; (R1) 212.52; More...

Intraday bias in GBP/JPY remains neutral first. On the upside, break of 212.10 will resume the rebound from 207.20 to retest 214.98 high. On the downside, below 209.15 will bring deeper fall to 207.20 support. Overall, as long as 207.20 support holds, price actions from 214.98 are seen as a near term consolidation pattern only. Larger up trend should resume sooner rather than later.

In the bigger picture, up trend from 123.94 (2020 low) is still in progress. Firm break of 214.98 will target 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. This will remain the favored case as long as 55 W EMA (now at 202.80) holds, even in case of another deep pullback.

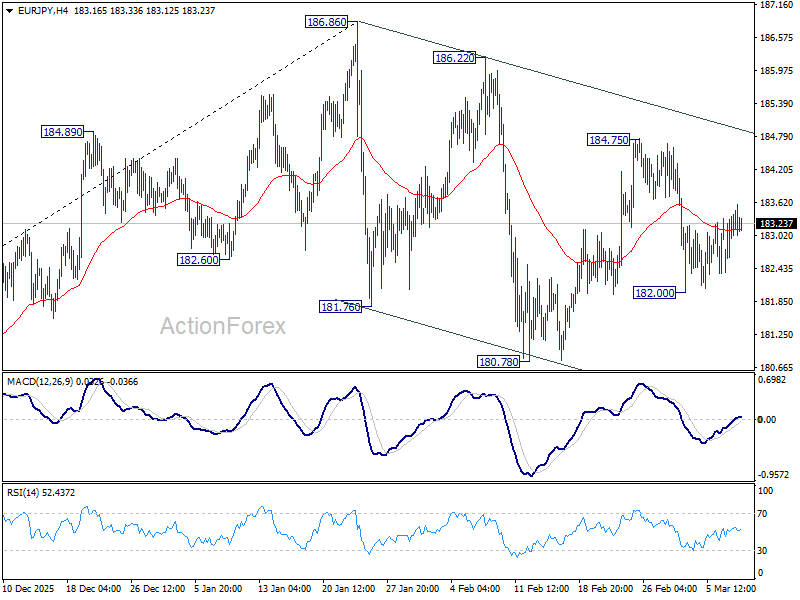

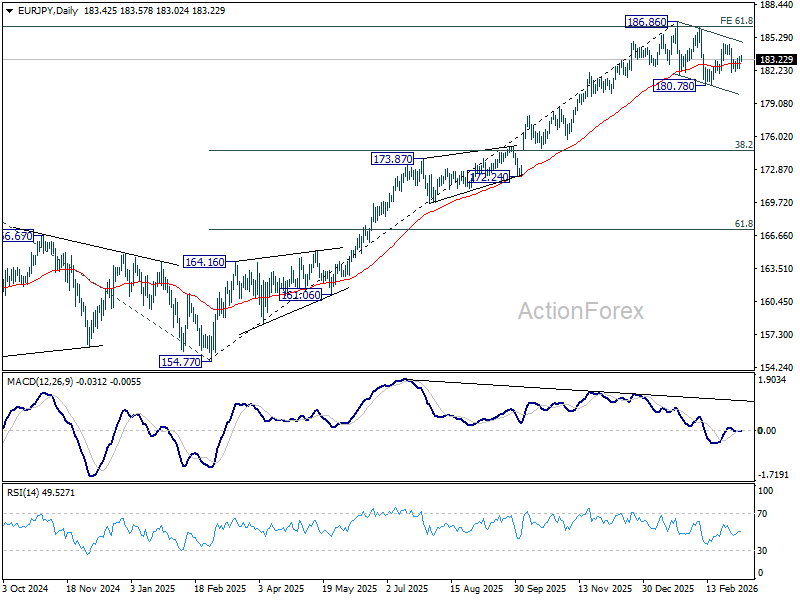

EUR/JPY Daily Outlook

Daily Pivots: (S1) 182.73; (P) 183.12; (R1) 183.83; More...

Intraday bias in EUR/JPY stays neutral for the moment. On the downside, below 182.00 will target 180.78. Firm break there will indicate that fall from 186.86 is already correcting whole up rise from 154.77. Deeper fall should then be seen to 38.2% retracement of 154.77 to 186.86 at 174.60. For now, near term outlook is neutral at best as long as 186.86 holds, or until there is sign of upward acceleration.

In the bigger picture, a medium term top should be in place at 186.86 and some more consolidations could be seen. Nevertheless, the larger up trend from 114.42 (2020 low) remains intact. Firm break of 186.86 will pave the way to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88 next.

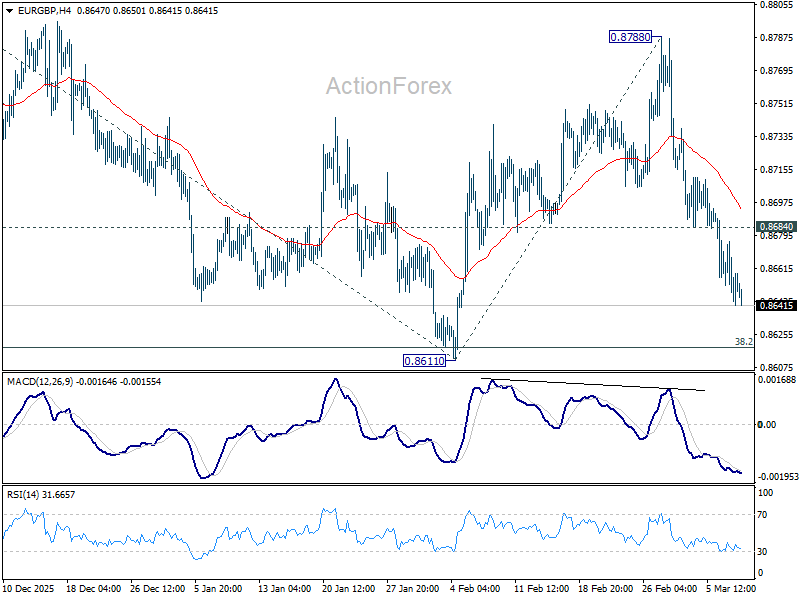

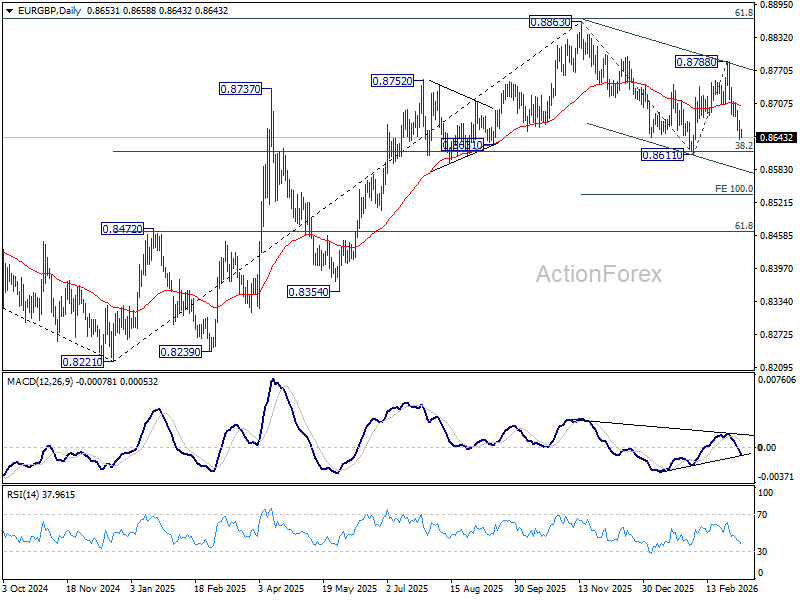

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8641; (P) 0.8661; (R1) 0.8677; More…

Intraday bias in EUR/GBP stays on the downside for the moment, as fall from 0.8788 is in progress for 0.8611 support. Firm break there will target 100% projection of 0.8863 to 0.8611 from 0.8788 at 0.8536. On the upside, above 0.8684 minor resistance will turn intraday bias neutral again first.

In the bigger picture, current development revived the case that whole rise from 0.8221 (2024 low) has completed at 0.8863, after rejection by 61.8% retracement of 0.9267 (2022 high) to 0.8221 at 0.8867. Sustained trading below 38.2% retracement of 0.8821 to 0.8863 at 0.8618 will confirm this case, and bring deeper fall to 61.8% retracement at 0.8466 at least. For now, medium term outlook is neutral at best as long as 0.8863 resistance holds.

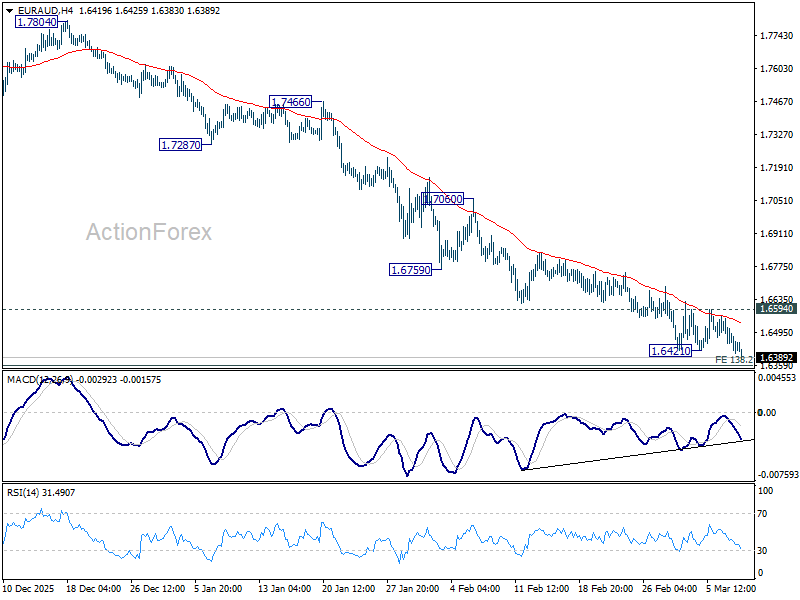

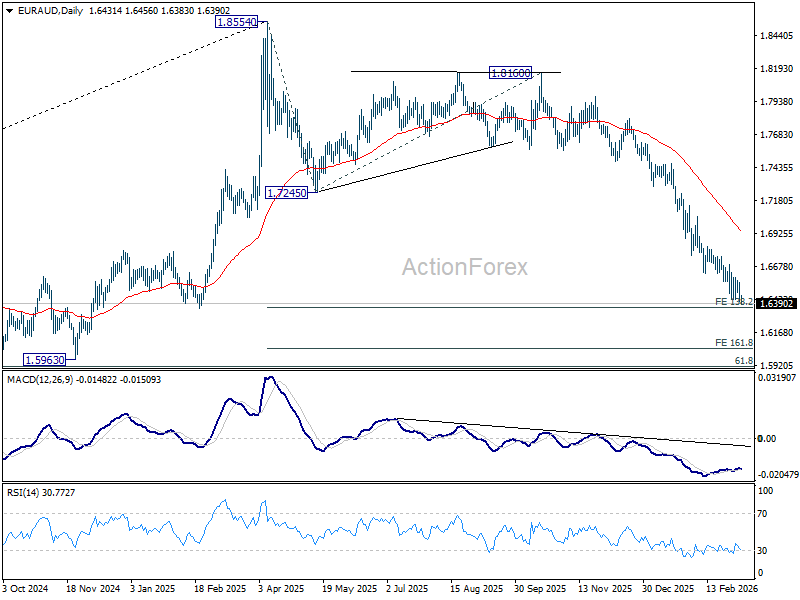

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6387; (P) 1.6471; (R1) 1.6531; More...

Intraday bias in EUR/AUD is back on the downside with break of 1.6421 temporary low. Sustained break of 138.2% projection of 1.8554 to 1.7245 from 1.8160 at 1.6351 will extend larger down trend to 161.8% projection at 1.6042 next. However, considering bullish convergence condition in 4H MACD, firm break of 1.6594 resistance will indicate short term bottoming. Intraday bias will be back on the upside for stronger rebound towards 55 D EMA (now at 1.6940).

In the bigger picture, fall from 1.8554 medium term top is seen as reversing the whole up trend from 1.4281 (2022 low). Deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. For now, risk will stay on the downside as long as 1.7245 support turned resistance holds, even in case of strong rebound.

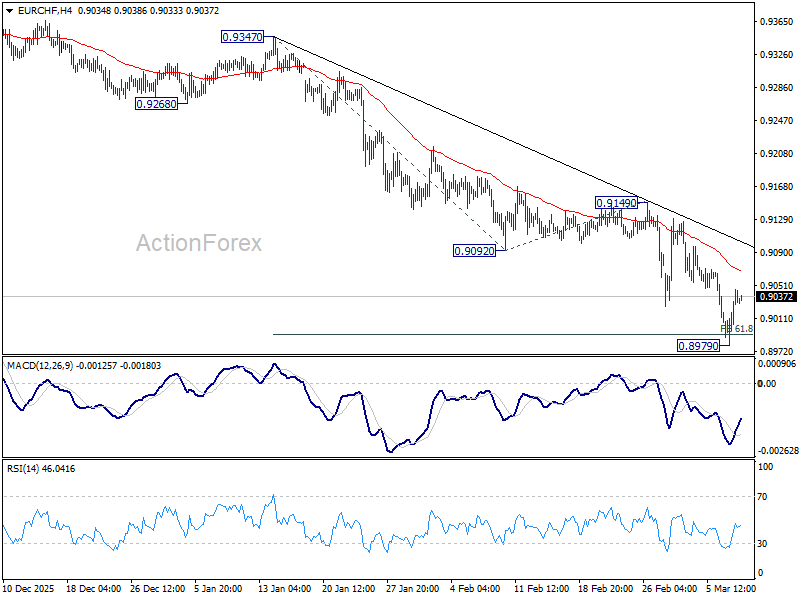

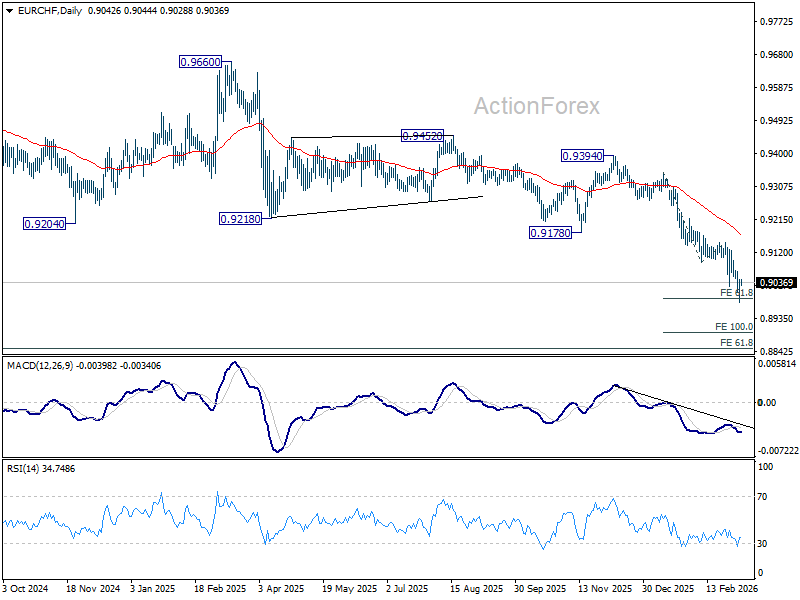

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9000; (P) 0.9025; (R1) 0.9070; More....

Intraday bias in EUR/CHF is turned neutral with current recovery and some consolidations could be seen. Outlook will stay bearish as long as 0.9149 resistance holds. On the downside, below 0.8979 will extend the larger down trend to 100% projection of 0.9347 to 0.9092 from 0.9149 at 0.8894.

In the bigger picture, down trend from 0.9928 (2024 high) is still in progress. Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Outlook will stay bearish as long as 0.9394 resistance holds, in case of rebound.

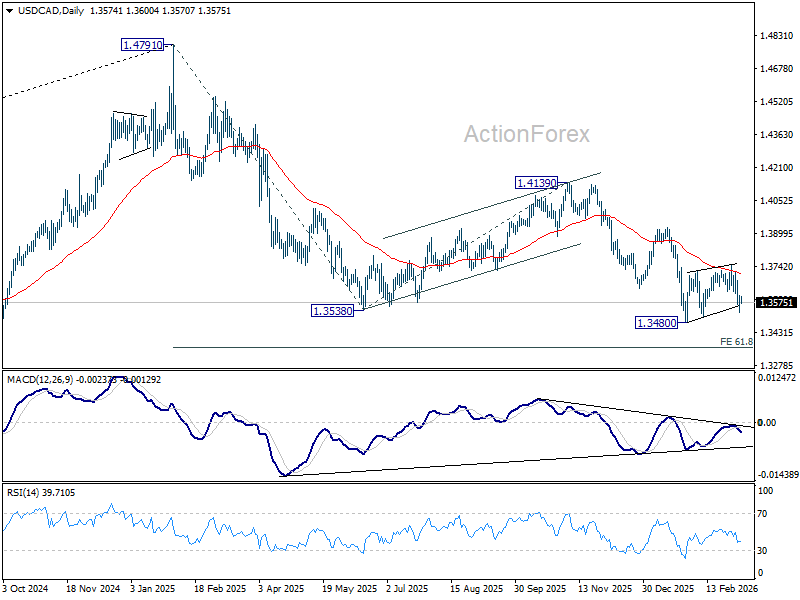

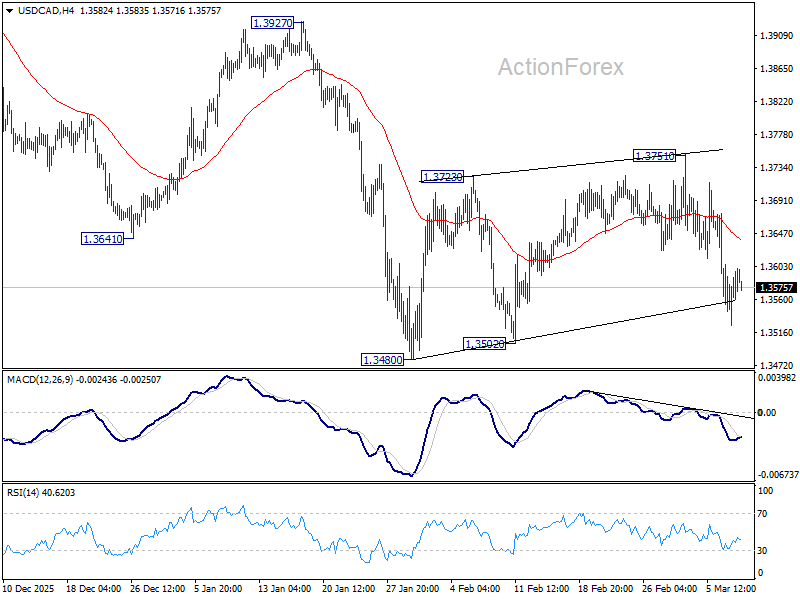

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3540; (P) 1.3573; (R1) 1.3621; More...

Intraday bias in USD/CAD remains mildly on the downside for the moment. Consolidation pattern from 1.3480 could have completed at 1.3751, after hitting 55 D EMA (now at 1.3708). Firm break of 1.3480 low will confirm resumption of whole fall from 1.4791, and target 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365. For now, near term outlook will remain bearish as long as 1.3751 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. For now, medium term outlook will be neutral at best, until there are signs that the correction has completed, or that a bearish trend reversal is confirmed.