Sample Category Title

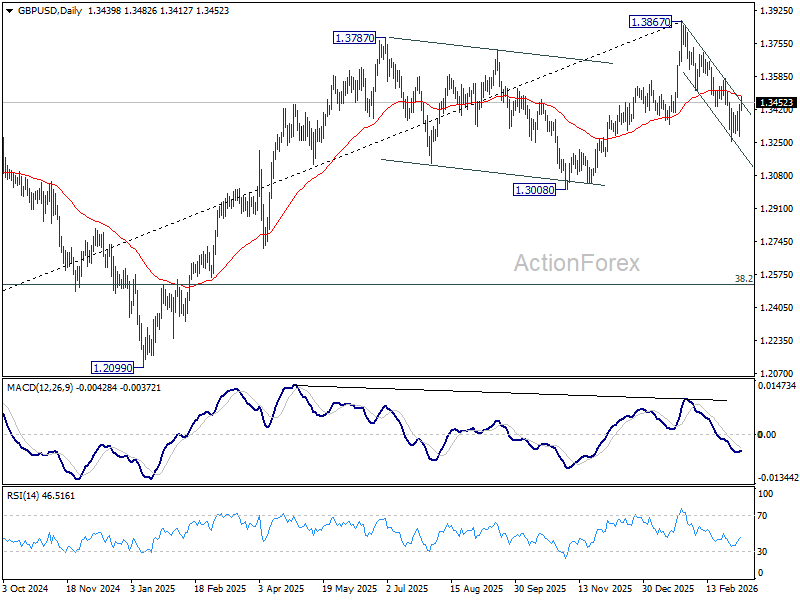

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3332; (P) 1.3389; (R1) 1.3497; More...

GBP/USD's recovery from 1.3252 extended higher today but upside is still capped well below 1.3574 resistance. Intraday bias remains neutral and further fall is in favor. On the downside, below 1.3252 will extend the decline from 1.3867 to 1.3008 structural support. Decisive break there will carry larger bearish implications.

In the bigger picture, considering bearish divergence condition in both D and W MACD, a medium term top should be in place from 1.3867. Firm break of 1.3008 support will argue that fall from 1.3867 is at least corrective the whole rise from 1.0351 (2022 low) with risk of bearish reversal. That would open up further decline to 38.2% retracement of 1.0351 to 1.3867 at 1.2524. For now, medium term outlook will be neutral at best as long as 1.3867 resistance holds, or under further development.

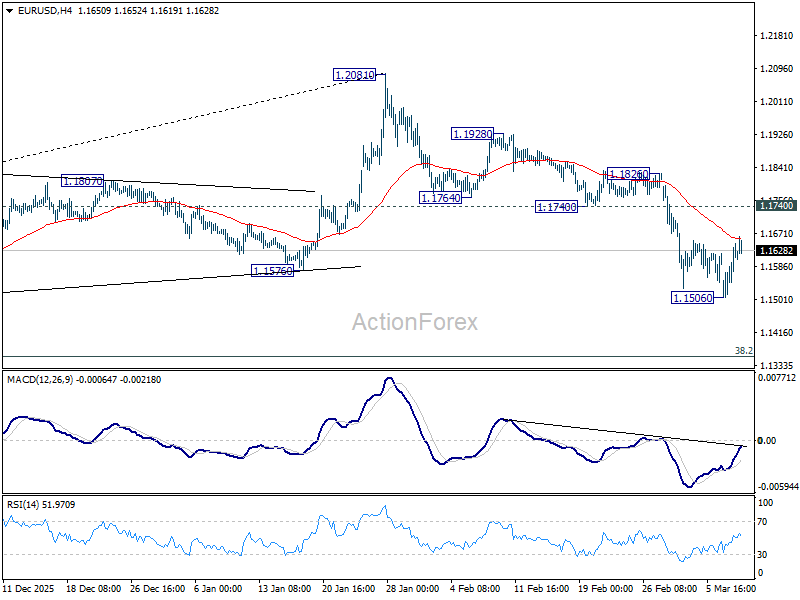

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1548; (P) 1.1594; (R1) 1.1681; More….

EUR/USD's recovery from 1.1506 continues today, but stays well below 1.1740 support turned resistance. Intraday bias remains neutral, and further decline is still expected. Break of 1.1506 will resume the fall from 1.2081 and target 38.2% retracement of 1.0176 to 1.2081 at 1.1353 next.

In the bigger picture, a medium term top should be in place at 1.2081 on bearish divergence condition in D MACD. Sustained trading below 55 W EMA (now at 1.1500) should confirm rejection by 1.2 key cluster resistance level. That would also raise the chance that whole up trend from 0.9534 (2022 low) has completed as a three wave corrective bounce too. For now, medium term outlook is neutral at best as long as 1.2081 holds, even in case of rebound.

Market Sentiment Improves Further on Saudi Oil Rerouting, Dollar Stays Soft

Global markets extended their recovery today as fears of a catastrophic disruption in global oil supply continued to ease. Asian and European equities rebounded broadly, although US futures were relatively sluggish. WTI crude also remains elevated at around 90 level.

The improvement in sentiment reflects a growing shift in how markets are pricing the conflict. Earlier fears centered on the possibility of a severe supply vacuum if the Strait of Hormuz were effectively shut down. Now, investors appear increasingly confident that global oil flows can be partially maintained through alternative routes and logistical adjustments.

A key development supporting this reassessment came from Saudi Aramco. The company announced it expects to restore roughly 70% of its normal crude shipments within days despite the ongoing disruption to shipping routes in the Gulf region.

Saudi Arabia normally exports about 6.4 million barrels per day. By rerouting supplies through alternative channels, Aramco aims to bring roughly 5 million barrels per day back to the global market almost immediately, significantly reducing the scale of the potential supply shock.

The primary workaround is the East–West Pipeline, also known as the Petroline. The 1,200-kilometer pipeline connects Saudi Arabia’s eastern oil fields with the Red Sea port of Yanbu, allowing shipments to bypass the Strait of Hormuz entirely.

This emergency activation of the pipeline has helped reassure markets that oil exports from the world’s largest crude exporter can continue flowing even while the conflict disrupts traditional shipping lanes.

Nevertheless, Saudi Aramco Chief Executive Amin Nasser warned that the global economy would still struggle to sustain a prolonged closure of the Strait. Global oil inventories are already sitting near five-year lows, leaving limited buffer if disruptions persist.

The easing of supply fears has also triggered a reversal in safe-haven flows across currency markets. Dollar has come under broad pressure as investors unwind defensive positions built during the height of the oil panic.

For the week so far, the Dollar is now among the worst-performing major currencies alongside Japanese Yen and Swiss Franc. Commodity-linked currencies have benefited the most from improving sentiment, with Australian Dollar leading gains, followed by New Zealand Dollar.

Aussie has also been supported by domestic factors after RBA Deputy Governor Andrew Hauser reiterated that the upcoming policy meeting remains “live,” signaling that policymakers will engage in a genuine debate about whether another rate hike may be needed.

In Europe, at the time of writing, FTSE is up 1.20%. DAX is up 1.69%. CAC is up 1.12%. UK 10-year yield is down -0.026 at 4.561. Germany 10-year yield is up 0.013 at 2.875. Earlier in Asia, Nikkei rose 2.88%. Hong Kong HSI rose 2.17%. China Shanghai SSE rose 0.65%. Singapore Strait Times rose 2.19%. Japan 10-year JGB yield closed flat at 2.186.

RBA’s Hauser signals “genuine debate” at March policy meeting

RBA Deputy Governor Andrew Hauser signaled that policymakers face a difficult decision at next week’s board meeting, warning that the recent surge in oil prices is adding new uncertainty to the inflation outlook. Speaking in an interview with The Conversation, Hauser said there will be “a lot for the board to discuss” when it meets later this month.

Hauser emphasized that a “very genuine debate” is likely among board members as they weigh competing risks. While inflation remains too high and rising energy prices could push it higher, policymakers must also consider broader economic conditions. “Inflation is too high. Higher prices don’t help that debate,” Hauser said, adding that arguments exist on both sides of the policy discussion.

The RBA’s current projections already point to headline inflation reaching 4.2% by June, but Hauser acknowledged that the recent oil spike linked to the Middle East conflict could push inflation above that forecast. However, he downplayed the likelihood of inflation climbing as high as 5% in the near term, noting that such projections assume oil prices remain around the USD 100 level.

Hauser stressed that the central bank has not yet updated its formal forecasts and will only revise them in May, after the upcoming policy meeting. For now, the key takeaway is that inflation risks are clearly tilted to the upside.

Australia Westpac consumer sentiment edges Up, but war fears slam late responses

Australia’s Westpac Consumer Sentiment index edged up 1.2% mom to 91.6 in March. While sentiment remains firmly in pessimistic territory, the survey indicates that consumers have responded less negatively than expected to the RBA’s 25 bps increase in February.

However, daily responses collected during the survey week point to steep deterioration in confidence as geopolitical conflicts intensified. According to Westpac, responses gathered in the final three days of the survey were consistent with a much weaker sentiment reading of around 84.

Looking ahead to the RBA’s March 16–17 policy meeting, a rate hike remains possible but is not the base case. While policymakers are likely to be concerned about how rising petrol prices could feed into domestic inflation, the rapidly evolving global situation may encourage caution. Westpac expects the central bank to hold rates steady this month, with the next rate increase more likely to come in May once the external environment becomes clearer.

Australia NAB business confidence turns negative after RBA hike

Australia’s NAB Business confidence fell sharply by five points to -1 February, slipping into negative territory for the first time in eleven months. In contrast, business conditions held steady at +7, roughly in line with the long-run average. The split suggests that firms are still experiencing stable trading conditions but are becoming increasingly cautious about the outlook.

Cost pressures also showed signs of firming again during the month. Labour costs rose to 1.5% on a quarterly equivalent basis. Retail price growth accelerated to 1.0% from just 0.3% previously. The rebound in price indicators suggests that underlying inflation pressures in the business sector may still be present.

The deterioration in sentiment has largely been attributed to the RBA’s 25 basis point rate hike in February to 3.85%, which marked the first increase in two years. NAB analysts noted that the survey only partially captured the subsequent escalation in Middle East tensions and the surge in global energy prices, meaning business confidence could face additional pressure in the months ahead.

China trade surges as exports jump 21.8% and imports beat forecasts

China’s trade activity accelerated sharply in the first two months of 2026, according to data released by the country’s Customs agency. Exports surged 21.8% yoy, far exceeding expectations of a 7.1% increase. Imports climbed 19.8% yoy, also well above the 6.3% consensus forecast.

The stronger-than-expected figures suggest both resilient global demand for Chinese goods and solid domestic consumption of imported materials. China typically combines January and February trade figures to minimize the distortions created by the shifting Lunar New Year holiday period.

Despite the overall strength, trade flows with the US continued to decline. Chinese exports to the U.S. fell about -11% yoy, while imports from the U.S. dropped nearly 27%. In response, Chinese manufacturers have increasingly redirected exports toward emerging markets, particularly Southeast Asia, Africa, and Latin America, highlighting an ongoing reorientation of China’s global trade network.

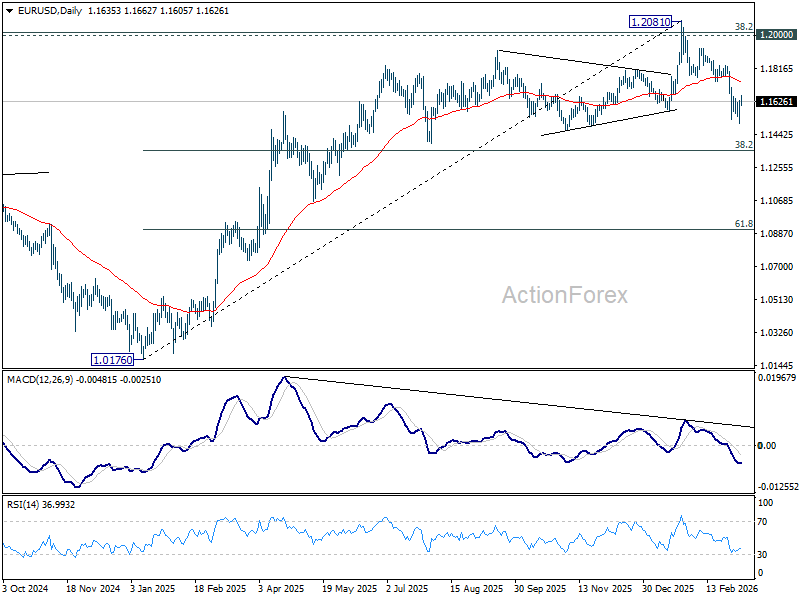

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1548; (P) 1.1594; (R1) 1.1681; More….

EUR/USD's recovery from 1.1506 continues today, but stays well below 1.1740 support turned resistance. Intraday bias remains neutral, and further decline is still expected. Break of 1.1506 will resume the fall from 1.2081 and target 38.2% retracement of 1.0176 to 1.2081 at 1.1353 next.

In the bigger picture, a medium term top should be in place at 1.2081 on bearish divergence condition in D MACD. Sustained trading below 55 W EMA (now at 1.1500) should confirm rejection by 1.2 key cluster resistance level. That would also raise the chance that whole up trend from 0.9534 (2022 low) has completed as a three wave corrective bounce too. For now, medium term outlook is neutral at best as long as 1.2081 holds, even in case of rebound.

Fed Could Do What ECB Can’t

- The Fed may keep rates high, while the ECB is unlikely to raise them.

- Japan’s economy has been hit by a double blow and needs new stimulus measures.

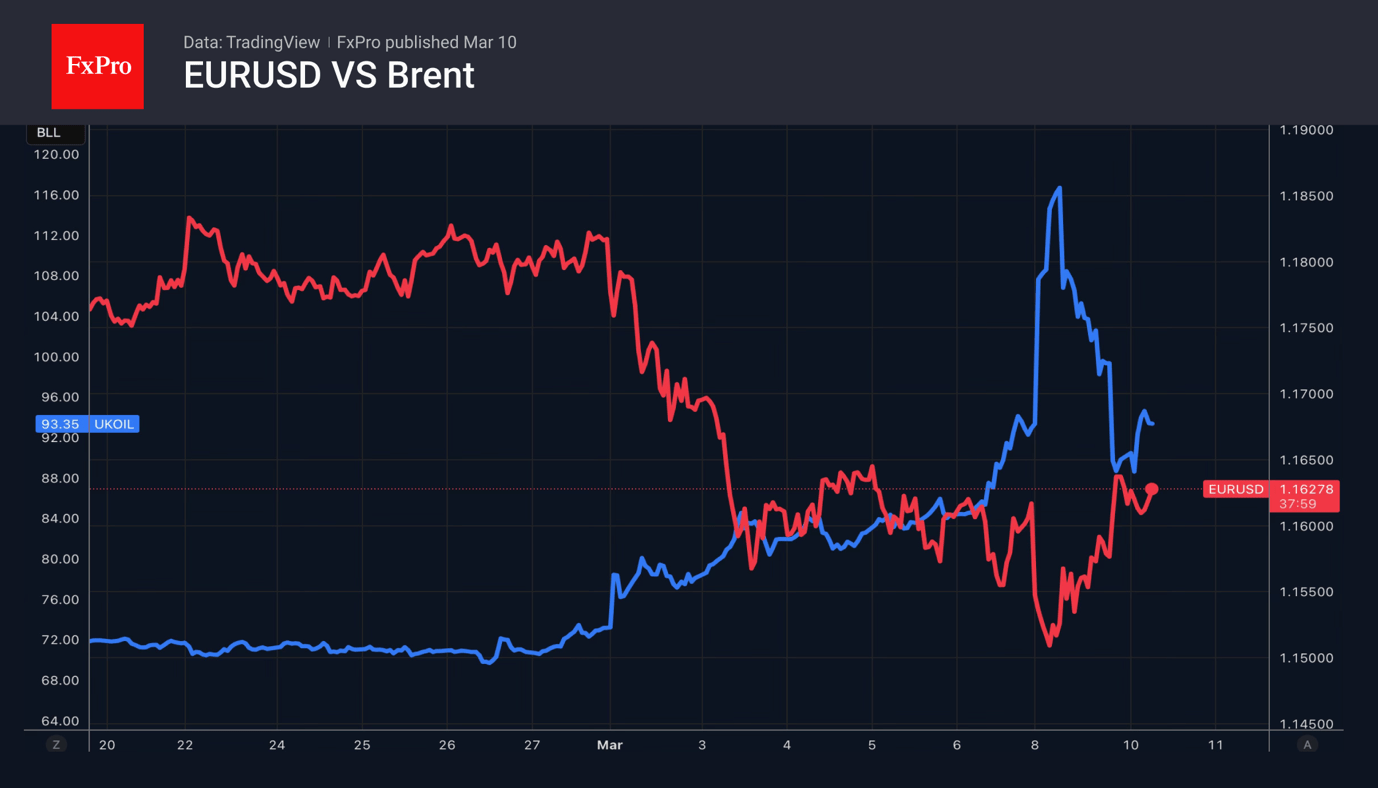

The US dollar fell sharply after Donald Trump said the Middle East conflict is nearing its end. If it had dragged on, oil prices could have soared to $150 per barrel, a serious blow to the economies of oil-importing countries. The US, with its strategic reserves of 415 million barrels and active drilling, would be able to withstand the energy shock, but Europe would not, so the latest turn was a relief for the battered EURUSD.

The resilience of the US economy could allow the Fed to keep interest rates high despite a potential acceleration in inflation. The futures market has increased the likelihood of the federal funds rate remaining unchanged until the end of 2026 to 18% from 8% before the conflict in the Middle East. Investors now anticipate one period of monetary easing rather than two as previously expected.

Derivatives in Europe indicate a rising chance of the ECB tightening monetary policy. In reality, the European Central Bank will be constrained if the eurozone enters a recession due to excessively high oil prices. Even if the conflict concludes soon, restoring oil production will be challenging. There is a market view that prices will not revert to pre-war levels until the end of 2026.

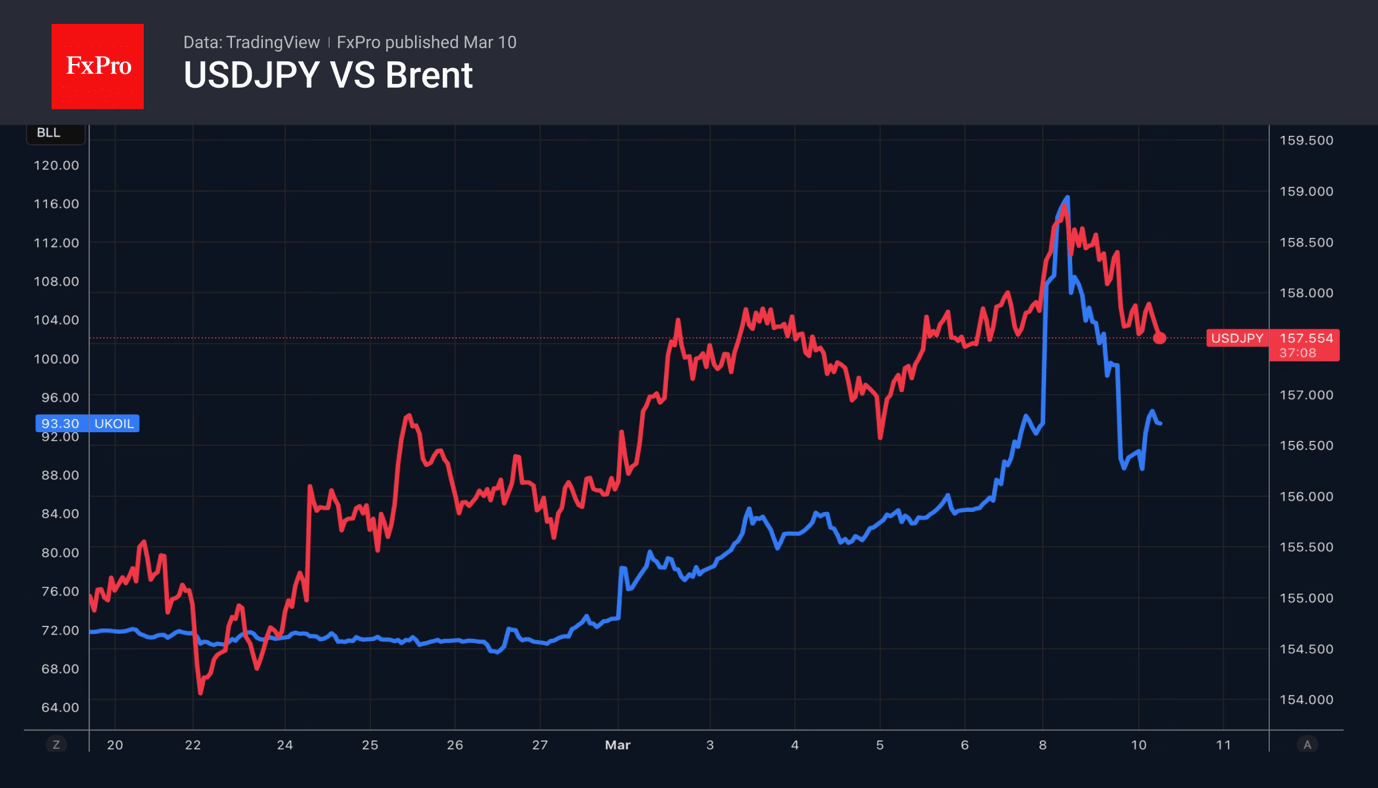

The rise in oil prices, combined with a weak yen, presents a double blow to the Japanese economy, ballooning the risk of stagflation. The USDJPY rate is climbing because, if the Middle East confrontation persists, the Japanese Prime Minister will need to prepare a new set of fiscal support measures. This will further weaken the yen.

If Donald Trump’s statement about an imminent peace deal had not caused the US dollar to fall, one might have assumed the USDJPY decline was due to currency intervention. In the past, when the pair approached 160, it triggered active measures by market authorities.

The US dollar’s retreat has helped gold recover. According to Bloomberg, gold-focused ETF holdings fell by 30 tonnes over the past week, marking the sharpest decline in two years.

EUR/USD in Turbulence: Market Questions When Conflict Over Iran Will End

EUR/USD is trading around 1.1608 on Tuesday. The US dollar attempted to recover from a sharp intraday decline the previous day, which had been driven by expectations of a faster resolution to the conflict involving Iran, temporarily reducing demand for the dollar as a safe-haven asset.

US President Donald Trump stated that the military operation in Iran is nearing completion and is progressing faster than initial estimates, which had suggested a duration of four to five weeks. He also announced plans to reduce oil sanctions and deploy US Navy ships to escort tankers through the Strait of Hormuz in an effort to contain rising oil prices.

Previously, the dollar had strengthened significantly due to safe-haven demand. The escalation of the Middle East conflict and rising energy prices had intensified fears of prolonged economic disruption and a fresh wave of inflation.

Investor attention is now shifting to macroeconomic statistics from the United States. The February consumer price index (CPI) is scheduled for release on Wednesday, followed by the January PCE index on Friday. Market participants believe these data points will not yet fully capture the conflict's impact on inflation expectations.

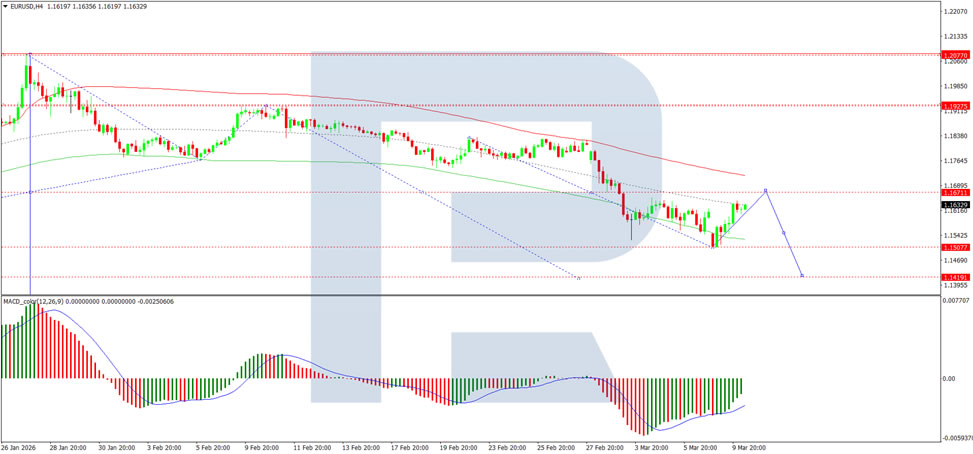

Technical Analysis

On the H4 chart of EUR/USD, the market is forming a consolidation range around the 1.1588 level. An upward wave is expected, with a continuation towards the 1.1668 level. Thereafter, the beginning of a new downward wave within the broader trend is anticipated, targeting 1.1419 as a local objective. Technically, this scenario is confirmed by the MACD indicator, whose signal line remains below zero and is pointing strictly downwards, reflecting sustained bearish momentum with potential for further downside.

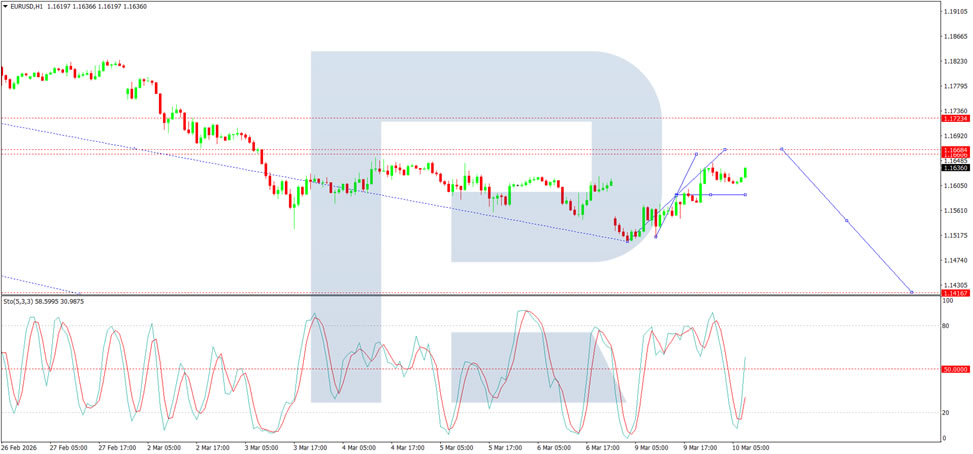

On the H1 chart, the market is forming the structure of the next growth wave towards the 1.1668 level. After reaching this level, a decline to 1.1419 is expected, followed by the initiation of a new growth wave to 1.1650. Technically, this scenario is supported by the Stochastic oscillator, with its signal line below 50 and pointing strictly upwards towards the 80 level.

Conclusion

EUR/USD remains highly sensitive to geopolitical developments, with signals of a potential de-escalation in the Iran conflict temporarily weighing on the dollar's safe-haven appeal. However, the broader technical picture suggests any upside may be limited, with bearish momentum likely to reassert itself once the current corrective wave completes. Upcoming US inflation data will provide crucial clues about whether recent energy price increases are beginning to filter through to consumer prices, potentially influencing Fed policy expectations.

Gold Price Holds Near Key Support

As the XAU/USD chart shows, the gold price has been holding within the $5,060–$5,200 range over the past several sessions.

Bullish view: the key support is the lower boundary of the long-term channel that has been in place since the beginning of 2026.

Bearish view: pressure on the price comes from statements by President Trump suggesting that the conflict in the Middle East could end soon. Yesterday, the US president described the operation in Iran as a “small incursion” and a “short-term” measure, which helped ease geopolitical risks and reduce demand for gold as a safe-haven asset.

Technical Analysis of the XAU/USD Chart

On the morning of 2 March, while analysing gold price movements following the attack on Iran, we confirmed the validity of the long-term ascending channel and also:

- → drew a local purple channel;

- → noted that the price was trading in close proximity to resistance lines;

- → suggested that emotions would settle and that the gold price might pull back, with support likely emerging in the $5,250–$5,300 area.

Indeed, later that evening the indicated zone acted as local support (shown by the blue arrow), but by 3 March the pullback had extended to the lower boundary of the blue channel.

It is worth noting that yesterday’s attempt by the bears (marked by the red arrow) failed to gain continuation — a sign that selling pressure may be weakening. Therefore, it would be reasonable to expect bulls to attempt to regain the initiative. A closer look at the XAU/USD chart also reveals that yesterday’s rising local lows form a cup-and-handle pattern.

At the same time, in the near term an important test of bullish intent may come at the breakout level of the purple channel around the $5,250 mark.

Start trading commodity CFDs with tight spreads (additional fees may apply). Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

EUR/USD Chart Analysis: Pair Rebounds from the Year’s Low

Analysing the EUR/USD chart five days ago, we:

- → constructed a downward channel, noting signs that the bears remained in control;

- → outlined a scenario in which the rate would decline to a new yearly low (and test the lower boundary of the channel).

Yesterday’s price action confirmed these assumptions – the low at H is below the low of 3 February (F), refining the lower boundary of the channel. At the same time, the sharp upward reversal (shown by the arrow) indicates increasing demand, driven by a shift in sentiment due to several factors, including:

- → Trump’s speech, in which the president stated that the war in Iran is progressing successfully and that he has contingency plans for any scenario. This cooled demand for the USD as a safe-haven asset.

- → Expectations of US inflation data scheduled for release tomorrow.

Technical Analysis of the EUR/USD Chart

Recent developments mean that the previously formed sequence of lower extremes A–B–C–D–E–F has been extended with new turning points G and H. However, the EUR/USD chart suggests that this sequence has already been disrupted.

Note that:

- → the price has confidently recovered after yesterday’s bearish gap at the market open;

- → the drop below the F low near the 1.1530 level was extremely brief (a sign of a bullish Liquidity Grab pattern);

- → the market may be sensing the proximity of the psychological 1.1500 level.

Moreover, demand-side forces are today attempting to push the price into the upper half of the channel. Therefore, forex traders should not rule out the possibility of a further recovery in EUR/USD from the fresh yearly low. In this case, former support levels at 1.1680 and 1.1750 may act as resistance to further gains.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

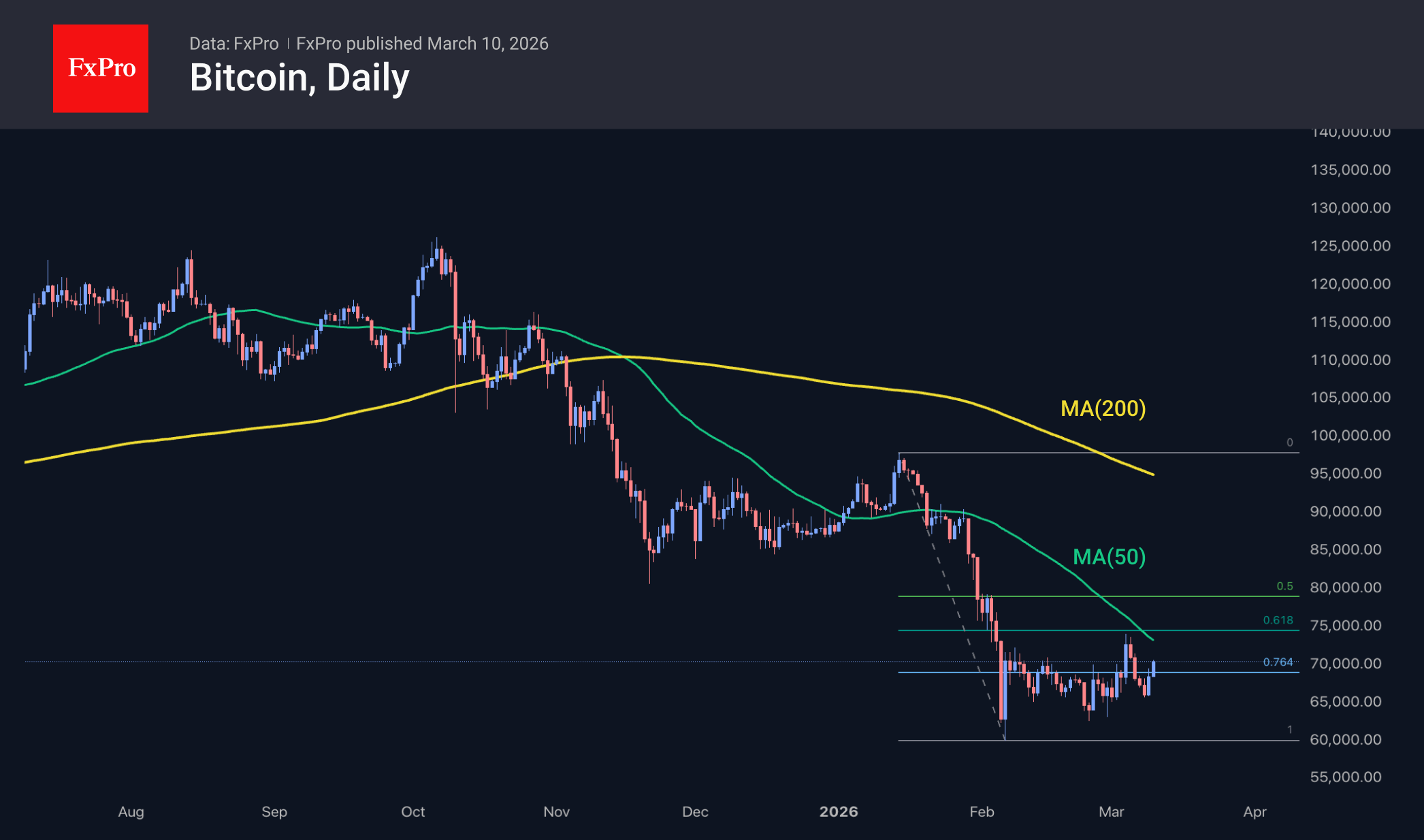

Green Shoots in Crypto Market

Market Overview

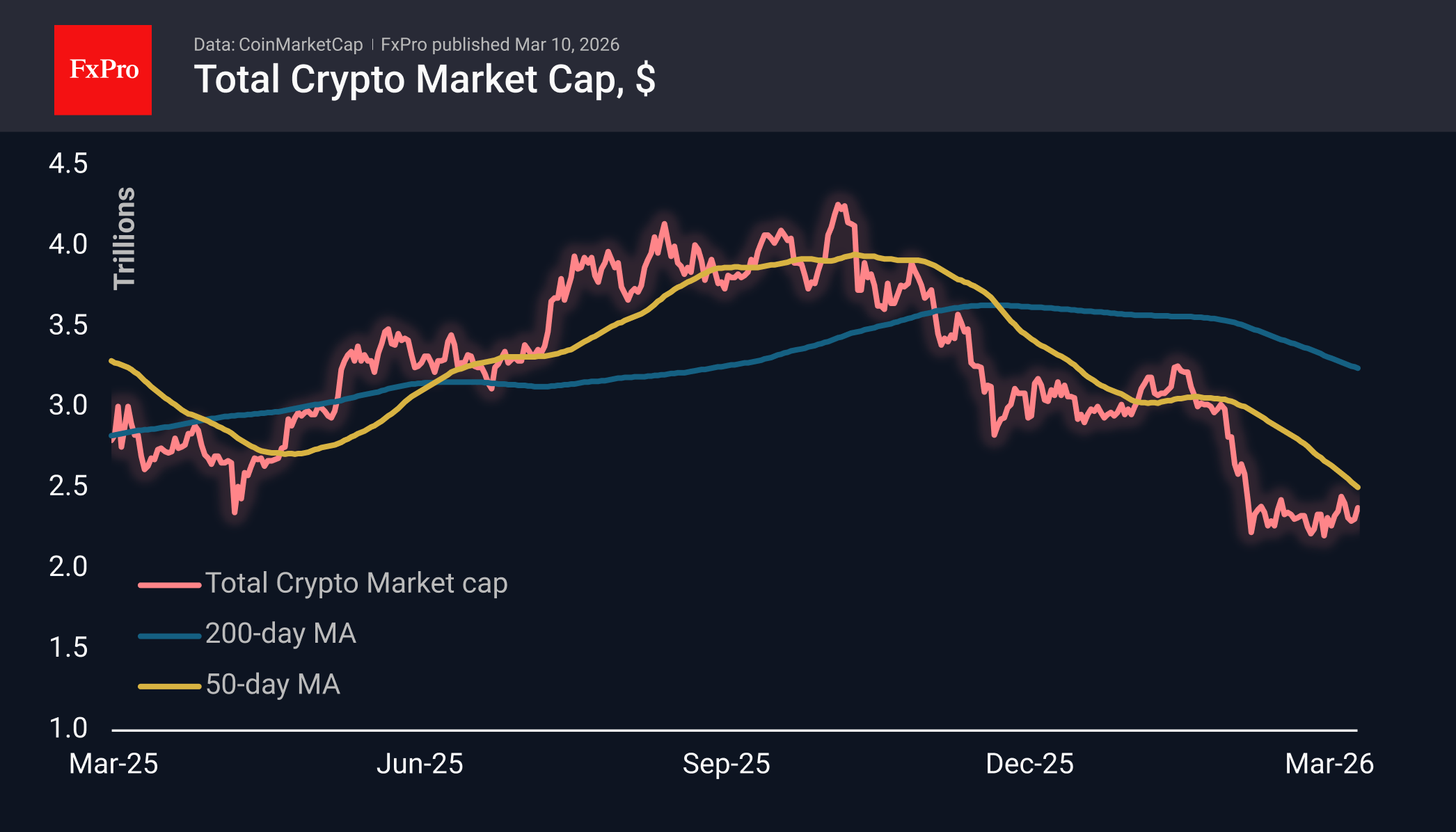

The crypto market cap increased by 3% over 24 hours to $2.38 trillion, supported by the impressive stock market rebound. Officially, the market is moving within a relatively narrow range after the collapse in the second half of January. Often in such situations, a new downward trend is expected around the corner, which remains the baseline scenario for now. However, it would be unwise to overlook the early signs of the crypto market’s growing interest in good news from outside, which was not the case a few months ago.

Bitcoin is testing the $70K level, gaining over 7% from the lows at the start of Monday. Buyers are becoming more confident, creating a series of higher local lows since the end of last month. The first cryptocurrency reached an important local resistance level in February. Still, bulls will need to sustain the price above the last peak at $73K, where the 50-day moving average also resides, to confirm the development of a medium-term uptrend.

News Background

According to CoinShares, global investment in crypto funds increased by $619 million last week, marking the second consecutive week of growth after five weeks of outflows. Investments in Bitcoin rose by $521 million, in Ethereum by $89 million, in Solana by $15 million, and in Chainlink by $1 million. Investments in XRP decreased by $30 million.

Strategy purchased 17,994 BTC ($1.28 billion) last week at an average price of $70,946 per coin. Strategy now holds 738,731 BTC, acquired for $56.04 billion at an average price of $75,862 per Bitcoin.

BitMine acquired an additional 60,000 ETH over the past week. The company’s reserves now total 4.53 million ETH, representing 3.76% of Ethereum’s total supply. BitMine aims to accumulate 5% of all Ether supply.

Overall data on inflows into global crypto ETFs indicate generally positive sentiment towards this asset class amid a period of geopolitical tension stemming from events surrounding Iran, CoinShares notes. The surge in oil prices is an unfavourable factor for Bitcoin, according to CryptoQuant.

An energy shock could push inflation higher and complicate the Fed’s task of lowering interest rates. Additionally, it increases miners’ costs, reducing the business’s attractiveness and potentially creating an overhang of sales for already-mined coins.

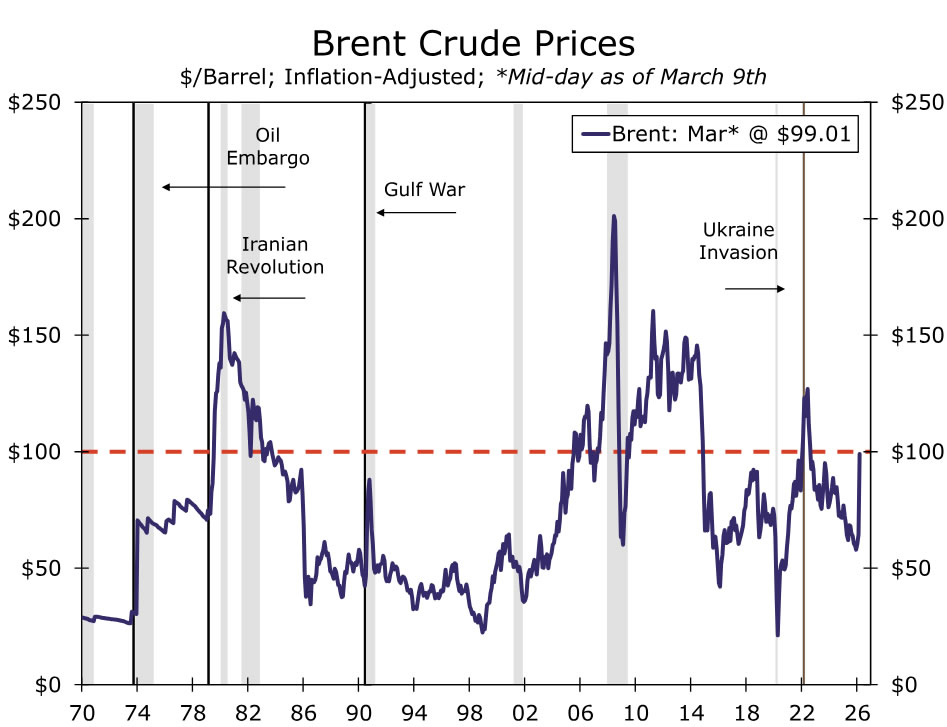

What Would It Take to Tip the Economy into Recession? Oil Prices & Recession Risk Roadmap

- Recession is not our base case, but we believe the risk distribution has shifted decisively to the downside, as oil briefly broke above $110/barrel and remains volatile. The U.S. economy does not enter the current oil price shock from a position of robust strength. With headline inflation on its way back above 3% as soon as this month, higher oil prices add a new headwind at a moment when the U.S. economy's margin for error is narrow.

- Recessions ultimately reflect broad and persistent declines in activity. An oil price shock becomes recessionary when it turns a slowing expansion into a self-reinforcing downshift: real income falls, consumption growth slows, investment contracts, hiring weakens, and income declines further.

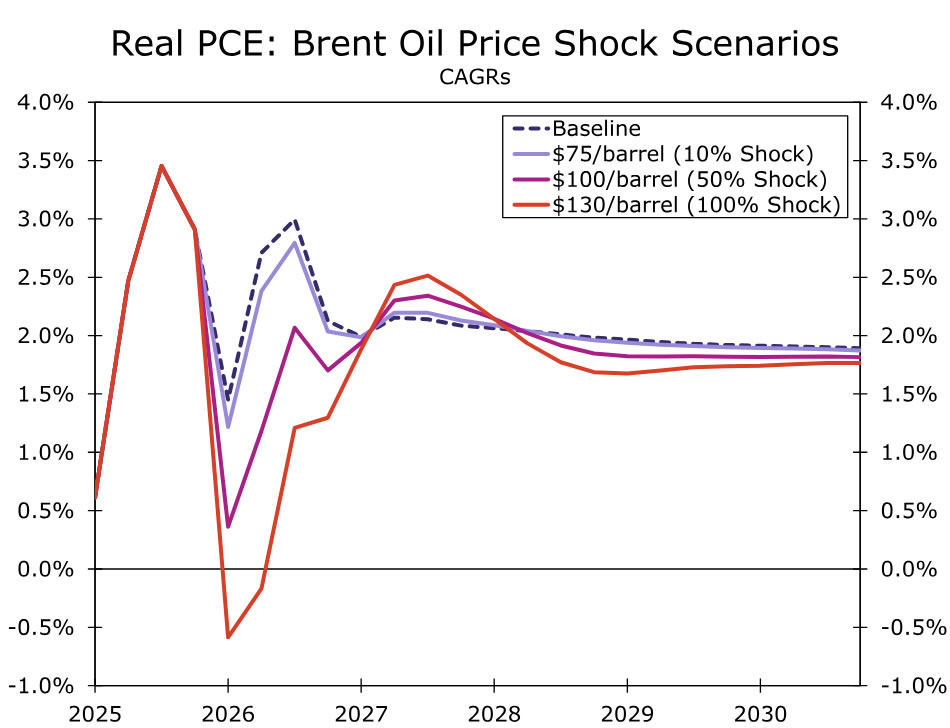

- Our model simulations suggest that a 50% sustained increase in oil prices would reduce annual average growth of real personal consumption expenditures (PCE) by a full percentage point—more than offsetting the expected boost to consumer spending from the One Big Beautiful Bill's household tax cut provisions.

- In an additional modeling exercise, sustained oil prices at $130/barrel, which is a ~100% increase from the pre-conflict baseline, would lead to back-to-back contractions in quarterly PCE in the middle part of this year.

- Higher oil prices tend to provide a boost to business fixed investment, primarily through increased energy-sector spending. This energy investment impulse is layered on top of a structural capex boom tied to the generative AI build-out, which has been relatively insensitive to energy costs and broader macro volatility.

- Moderate increases in oil prices tend to reallocate growth, rather than eliminate it: consumer spending slows, but investment accelerates, helping to stabilize aggregate demand. However, this offset is neither full, nor immediate.

- As a net energy exporter, the U.S. economy can better weather higher oil prices than many other countries, but sustained prices north of $130/barrel would materially raise the risk of recession.

The Economy Is Vulnerable to an Oil Shock Right Now

With intraday oil prices nearly hitting $120/barrel over the past day (and then receding almost as fast), we know some folks are wondering about potential downside economic risks. So let's talk about it. To be clear, it seems very premature to notably alter recession odds at this juncture (given the volatility of oil prices mentioned a moment ago, that seems practical). But that shouldn’t stop us from talking about risks associated with big upswings in oil (Figure 1) and providing a roadmap of sorts.

The reality is the U.S. economy does not enter the current oil shock from a position of robust strength. Payroll growth remains soft at best, the unemployment rate is modestly above most estimates of full employment, and real income growth was already under pressure before energy prices moved higher. With headline inflation on its way back above 3% as soon as this month, higher oil prices add a new headwind at a moment when the margin for error is narrow.

As we flagged in our FAQ last week, the longer prices stay elevated, the greater the downside economic hit becomes. Stated differently, the left tail grows fatter the longer prices rise and stay elevated. So from our lens, the relevant question for markets is no longer whether higher oil prices are “bad for U.S. growth,” but what conditions would be required for an oil shock to push a fragile expansion into outright recession?

Recessions ultimately reflect broad and persistent declines in activity. An oil shock becomes recessionary when it turns a slowing expansion into a self-reinforcing downshift: real income falls, consumption growth slows, investment contracts, hiring weakens, and income declines further.

The Three Conditions that Typically Turn an Oil Spike into a Recession

1) The jump in oil prices is high enough to force real income to contract

- A sustained rise in energy prices mechanically weakens real income growth, especially when wage growth is already slowing and hiring is soft, as it happens to be right now.

2) The shock persists long enough to spread beyond energy

- One-off spikes hit sentiment and headline inflation, but recessions usually require months of pressure that force households to change behavior and businesses to revise staffing and capex plans. Put differently: the economy can “absorb” a spike; it struggles with a new, sustained higher plateau.

3) Spillovers tighten broader financial conditions

- The most dangerous pathway is not just the direct energy price spike—it’s the second-order effect: higher inflation expectations, weaker sentiment, and tighter financial conditions that make investment harder and ding household consumption, particularly for the higher income cohorts currently driving spending growth. Market concerns about growth have the potential to become self-fulfilling by choking off the confidence/wealth channel and turn what has already felt like a recessionary environment for many Americans into an actual recession.

Modeling the Consumer Impact: Some Wiggle Room, but Not Limitless

Most households devote a relatively small share (less than 3%) of their budgets directly to gasoline and other energy goods, but these are expenditures that are difficult to curtail when prices rise. As seen in Figure 2, our model simulations suggest that a 50% sustained increase in oil prices would reduce the annual average pace of real personal consumption expenditures (PCE) by a full percentage point—more than offsetting the expected boost to consumer spending from the One Big Beautiful Bill's household tax cut provisions.

Even so, a larger oil price shock would need to be sustained to generate a contraction in aggregate consumer spending that is typically associated with recession. While real retail and wholesale sales are near stall speed, broader consumption has remained more resilient in recent months, supported by the growing dominance of services spending, demographic dynamics (e.g., more spending on healthcare), and income concentration among higher income households. In an additional modeling exercise, sustained oil prices at $130/barrel, which is a ~100% increase from the pre-conflict baseline, would lead to back-to-back contractions in quarterly PCE in the middle part of this year.

Modeling the Investment Impact: A Partial Offsetting Boost

Higher oil prices tend to provide a boost to business fixed investment, primarily through increased energy-sector spending. Rising prices improve project economics, lift cash flow for producers and incentivize new drilling, infrastructure, and related capital outlays.

In the current cycle, this investment impulse is layered on top of a structural capex boom tied to the generative AI build-out, which has been relatively insensitive to energy costs and broader volatility. As a result, moderate increases in oil prices tend to reallocate economic growth, rather than eliminate it: consumer spending slows, but investment accelerates, helping to stabilize aggregate demand.

However, this offset is neither full, nor immediate. The hit to household purchasing power occurs quickly, while investment responds with a lag. More importantly, the investment response does not scale one‑for‑one with oil prices, meaning we would not expect the pick-up in energy-related investment spending to offset fully the loss in household purchasing power.

Bottom Line: Recession Risks Elevated

Oil shocks do not automatically produce recessions. They become recessionary when they persist, compress real incomes, and trigger spillovers that feed back into employment and financial conditions. The key takeaway for markets is the non-linearity of the risk: moderate oil price increases slow growth; sufficiently high and sustained prices can overwhelm the offsets and tip the economy into recession. The question is not whether oil matters—but how high, and for how long. As a net energy exporter, the U.S. economy can better weather higher oil prices than many countries. But, sustained prices north of $130/barrel would materially raise the risk of recession.

A Practical "Recession Checklist":

- Oil stays elevated long enough to push up headline inflation and produce outright declines in real incomes.

- Consumption rolls over in back-to-back quarterly declines, which our model suggests can occur around $130/barrel.

- Financial conditions tighten in a way that hits investment spending and higher income consumption, turning the current bifurcated consumption pattern into a broader downshift.

- Prices climb to a level where the boost to energy-related capex no longer offsets the broad hit to household spending.

When all four are checked—especially #2 plus #3—the probability of recession rises materially.

RBA’s Hauser signals “genuine debate” at March policy meeting

RBA Deputy Governor Andrew Hauser signaled that policymakers face a difficult decision at next week’s board meeting, warning that the recent surge in oil prices is adding new uncertainty to the inflation outlook. Speaking in an interview with The Conversation, Hauser said there will be “a lot for the board to discuss” when it meets later this month.

Hauser emphasized that a “very genuine debate” is likely among board members as they weigh competing risks. While inflation remains too high and rising energy prices could push it higher, policymakers must also consider broader economic conditions. “Inflation is too high. Higher prices don’t help that debate,” Hauser said, adding that arguments exist on both sides of the policy discussion.

The RBA’s current projections already point to headline inflation reaching 4.2% by June, but Hauser acknowledged that the recent oil spike linked to the Middle East conflict could push inflation above that forecast. However, he downplayed the likelihood of inflation climbing as high as 5% in the near term, noting that such projections assume oil prices remain around the USD 100 level.

Hauser stressed that the central bank has not yet updated its formal forecasts and will only revise them in May, after the upcoming policy meeting. For now, the key takeaway is that inflation risks are clearly tilted to the upside.