Sample Category Title

US Dollar Index (DXY): Technical Picture as Inflation and Geopolitical Uncertainty Loom

- The US dollar and oil prices experienced intense volatility due to Middle East tensions, initially spiking after strikes on Iran but cooling after optimistic remarks from President Trump.

- The upcoming US CPI print, which is expected to show headline inflation holding steady at 2.4% may be overshadowed.

- US Dollar bulls eye acceptance above the 99.57 handle before the psychological 100.00 handle comes into play.

The US dollar found support late trade on Tuesday after it spent the majority of the day on the backfoot as hopes for a ceasefire in the Middle East grew.

The greenback retreated from its peak after a period of intense volatility sparked by joint US-Israeli strikes on Iran. While those strikes initially sent oil prices to their highest levels since 2022 and drove a surge in the greenback, the market cooled significantly following optimistic remarks from President Donald Trump.

On Monday, the President suggested that the conflict might conclude much sooner than originally anticipated, providing a much-needed reprieve for global markets.

However, this de-escalation came with a firm caveat: Trump warned that he would ramp up military action if Tehran attempted to disrupt oil flow through the Strait of Hormuz.

Despite the lingering threat, his comments were enough to soothe investor anxiety, leading to a sharp reduction in dollar buying.

By Tuesday, the shift in sentiment caused oil prices to plunge approximately 15%, reversing much of the previous session’s dramatic climb.

However, late in Tuesday's session it appears that market angst had returned as Iranian leaders struck a defiant tone. As a result, haven demand returned which provided the US dollar support while Oil prices rose around 8% for the daily lows around the $75.93/barrel mark.

The move in the US Dollar Index leaves the greenback at a crossroads heading into tomorrow's US CPI print.

US CPI data ahead

Now of course, the latest increase in oil prices will not be in tomorrow's CPI release, with first signs likely to come in the March inflation release next month.

Looking back at the inflation release last month, it was a positive one for rate cuts. YoY inflation in the US dropped to its lowest level since May 2025, 2.4%.

Source: TradingEconomics

Another drop this month though is unlikely to be met with the same optimism as the inflation release may seem somewhat out of date given the current month's developments.

Markets will be watching to see what the print is as it may still have some impact on rate cut expectations, even if that proves temporary it could lead to a spike in volatility.

Markets are currently anticipating that US headline inflation YoY will hold steady at 2.4%, with core inflation expected to remain resilient at 2.5%. Because the Federal Reserve has entered its mandatory "quiet period" leading up to the March 18th policy meeting, officials are restricted from providing public commentary on how they intend to navigate the current geopolitical crisis.

This silence leaves investors speculating on whether the Fed and its global counterparts will view the recent spike in energy costs as a transitory shock to be "looked through," or as a fundamental threat to long-term price stability that requires a more aggressive policy response.

The central question facing policymakers is whether these supply-side pressures will trigger a "second round" of price hikes across the broader economy. If central banks conclude that the conflict's impact on oil is temporary, they may maintain their current interest rate trajectories; however, if they perceive a genuine risk of inflation becoming entrenched, a shift toward higher-for-longer rates may be necessary to anchor market expectations.

The next week should be key as we have the CPI, PCE data releases ahead of the Fed meeting. The question is, will the conflict still be ongoing at that point and what will the Oil price be?

US Dollar Index - Technical picture as CPI looms

From a technical standpoint, the daily candle has tested a key support area at 98.72 before dropping further to test the 100-day MA at 98.56.

Since then, the index has seen the daily candle change course dramatically, on course to close as a hammer candle.

Now while candlestick patterns are a good analysis tool, during periods like the one we are in now where a tweet by President Trump can change the entire market sentiment I would urge caution.

Monday's daily candle close being a prime example. A massive shooting star candlestick which is looking likely to be followed by a hammer candle. This is a sign of the current indecision and impact the constantly changing narratives are having on markets.

For bulls, a clean daily candle close above the 99.57 handle remains elusive. If bulls are to challenge the 100.00 psychological level, acceptance above this handle will be key in the near-term.

Looking at the downside and support rests at the 98.56 handle where the 100-day MA rests before the 200-day MA at 98.33 comes into focus. Below that markets will begin to look at the 97.70 handle.

US Dollar Index Daily Chart, March 10, 2026

Source: Tradingview

EURAUD Wave Analysis

EURAUD: ⬇️ Sell

- EURAUD falling inside daily down channel

- Likely to fall to support level 1.6200

EURAUD currency pair has been falling in the last few trading sessions inside the sharp daily downward channel from the end of January.

The price earlier broke out of the daily down channel from last October – which accelerated the active short-term impulse wave 5 of the intermediate impulse wave (3) from October.

Given the overriding daily downtrend and the strongly bearish euro sentiment seen today, EURAUD currency pair can be expected to fall to the next support level 1.6200.

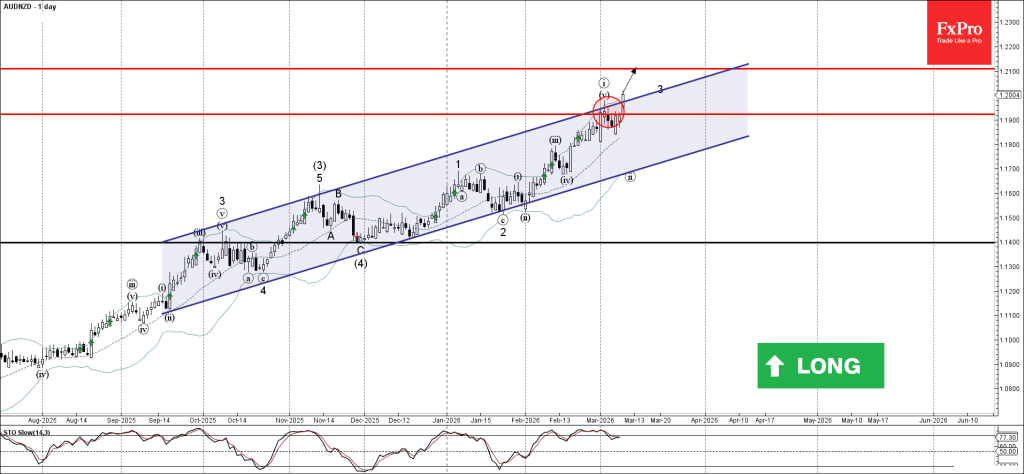

AUDNZD Wave Analysis

AUDNZD: ⬆️ Buy

- AUDNZD broke resistance zone

- Likely to rise to resistance level 1.2100

AUDNZD currency pair recently broke through the resistance zone between the resistance level 1.923 and the resistance trendline of the sharp daily up channel from September.

The breakout of this resistance zone accelerated the active short-term impulse wave 3 of the intermediate impulse wave (5) from November.

Given the strong daily uptrend, AUDNZD currency pair can be expected to rise to the next resistance level 1.2100 (target for the completion of the active impulse wave 3).

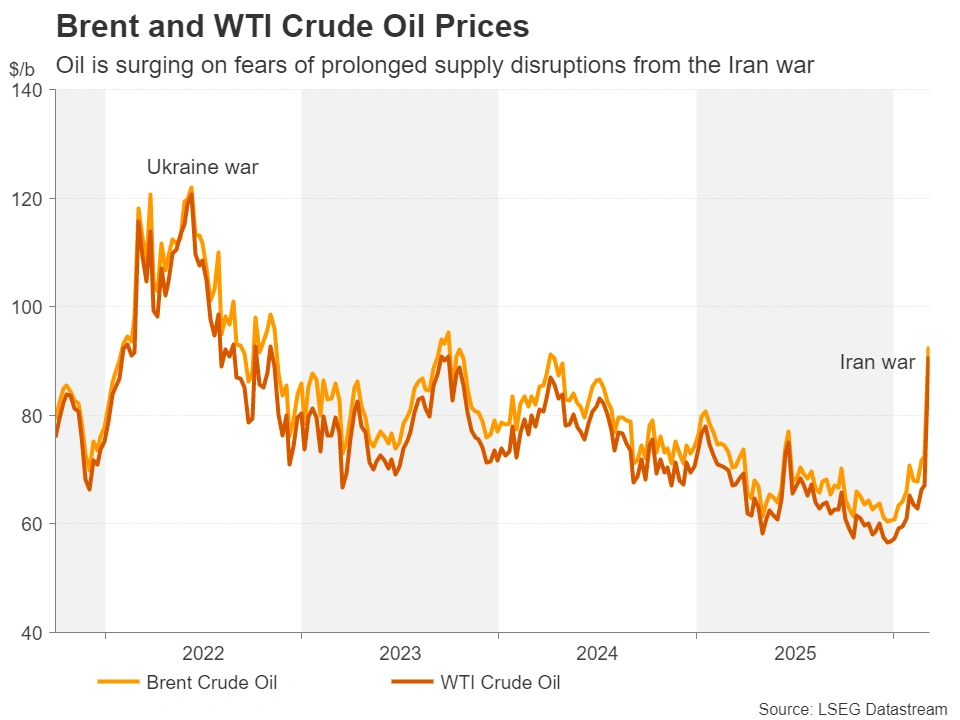

WTI Oil Eases Further on Encouraging Signals

WTI oil extends pullback from Monday’s 3 ½ year high ($119.44) on Tuesday, following unexpected and sharp change in the sentiment after President Trump said that war in the Middle East could end soon.

He also signaled that the US may lift some sanctions on sales of Russian oil, to partially compensate negative impact from expected supply shortage on closure of Hormuz strait, where about 20% of global oil supplies was flowing every day.

It looks like markets overreacted in both directions, as situation is very fragile and warning that volatility is going to remain high, although the action in past two days was driven more by speculation rather than reality.

From that point of view, President Trump’s signals (end of the war / lifting sanctions) need time to materialize, while the world hasn’t really felt stronger supply shortage so far.

However, I share a very cautious approach with many analysts, who point to ongoing war (which escalates daily) and the real consequences from oil production and supply shortage that keep the upside at risk.

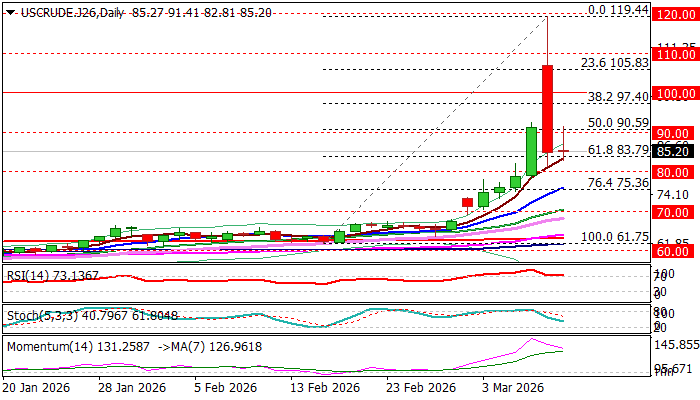

Res: 90.00; 91.41; 92.50; 95.40

Sup: 83.79; 82.81; 81.20; 80.00

Eco Data 3/11/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 23:50 | JPY | PPI Y/Y Feb | 2.00% | 2.10% | 2.30% | |

| 07:00 | EUR | Germany CPI M/M Feb F | 0.20% | 0.20% | 0.20% | |

| 07:00 | EUR | Germany CPI Y/Y Feb F | 1.90% | 1.90% | 1.90% | |

| 12:30 | USD | CPI M/M Feb | 0.30% | 0.20% | 0.20% | |

| 12:30 | USD | CPI Y/Y Feb | 2.40% | 2.40% | 2.40% | |

| 12:30 | USD | CPI Core M/M Feb | 0.20% | 0.20% | 0.30% | |

| 12:30 | USD | CPI Core Y/Y Feb | 2.50% | 2.50% | 2.50% | |

| 14:30 | USD | Crude Oil Inventories (Mar 6) | 3.8M | 2.8M | 3.5M |

| 23:50 | JPY |

| PPI Y/Y Feb | |

| Actual | 2.00% |

| Consensus | 2.10% |

| Previous | 2.30% |

| 07:00 | EUR |

| Germany CPI M/M Feb F | |

| Actual | 0.20% |

| Consensus | 0.20% |

| Previous | 0.20% |

| 07:00 | EUR |

| Germany CPI Y/Y Feb F | |

| Actual | 1.90% |

| Consensus | 1.90% |

| Previous | 1.90% |

| 12:30 | USD |

| CPI M/M Feb | |

| Actual | 0.30% |

| Consensus | 0.20% |

| Previous | 0.20% |

| 12:30 | USD |

| CPI Y/Y Feb | |

| Actual | 2.40% |

| Consensus | 2.40% |

| Previous | 2.40% |

| 12:30 | USD |

| CPI Core M/M Feb | |

| Actual | 0.20% |

| Consensus | 0.20% |

| Previous | 0.30% |

| 12:30 | USD |

| CPI Core Y/Y Feb | |

| Actual | 2.50% |

| Consensus | 2.50% |

| Previous | 2.50% |

| 14:30 | USD |

| Crude Oil Inventories (Mar 6) | |

| Actual | 3.8M |

| Consensus | 2.8M |

| Previous | 3.5M |

What’s at Stake as Trump’s Iran Gamble Sparks Energy Crisis?

- Oil and gas prices shoot up, upending rate cut bets as inflation fears return.

- Stocks tumble amid surging bond yields and stagflation risks.

- Markets increasingly price in a prolonged Iran conflict.

- Did Trump just shoot himself and the US economy in the foot?

Back to the 1970s

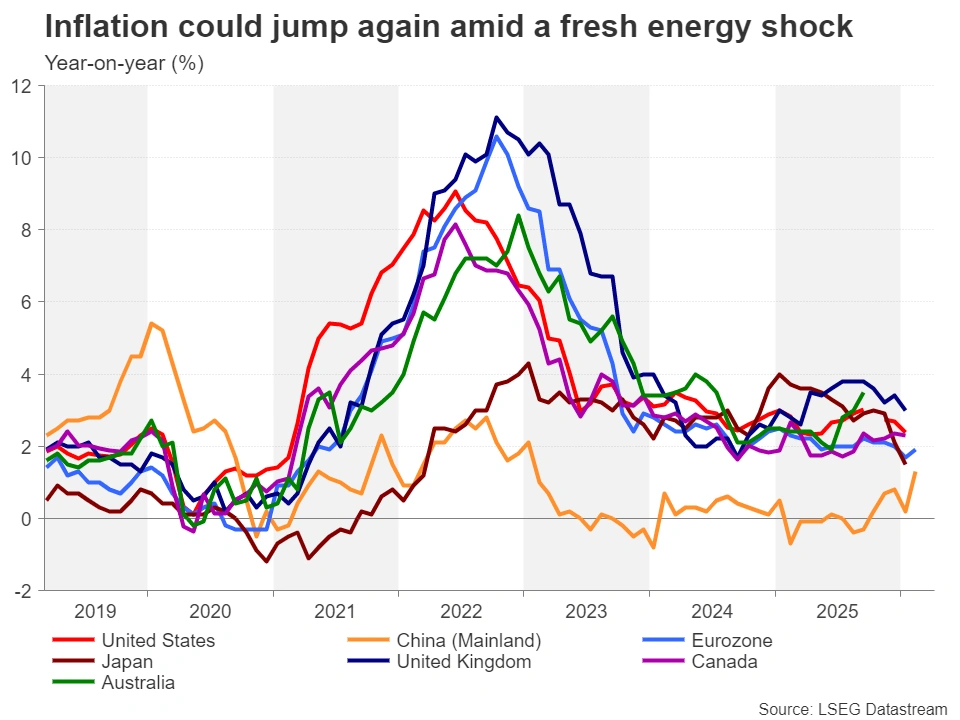

It’s only been a few years since Russia’s invasion of Ukraine triggered the worst energy crisis since the 1970s, and it’s looking increasingly likely that the world is facing yet another shock – the second one in less than a decade. All this is very reminiscent of the 1970s where inflation was rampant and economic growth was sluggish – a combination more commonly known as stagflation.

President Trump’s decision for the United States to launch joint miliary strikes with Israel on Iran may be going according to plan and “ahead of schedule”, but it’s had unintended consequences on global energy markets. America’s inability to completely stop Iranian drone and missile attacks on vessels passing through the Strait of Hormuz and guarantee their safety is not only halting shipments of oil and gas from the Middle East but is also having a crippling effect on production.

Key Oil chokepoint blocked

About 20% of global oil and gas supply is estimated to rely on the Strait of Hormuz for transit and with Arab producers such as Saudi Arabia, United Arab Emirates and Qatar unable to export, they have already reached their maximum storage capacities. What this means is that unless the Strait of Hormuz is opened for business again, which is extremely unlikely at this stage, production may soon come to a standstill.

Qatar has already ceased production of liquified natural gas (LNG) at Ras Laffan, which is the world’s largest LNG facility, while Saudi Arabia has started to reduce oil output. Oil and gas futures have subsequently soared, threatening a jump in energy costs for businesses that are still reeling from the price shock from the Ukraine war, and more recently, Trump’s tariff war.

From rate cuts to rate hikes

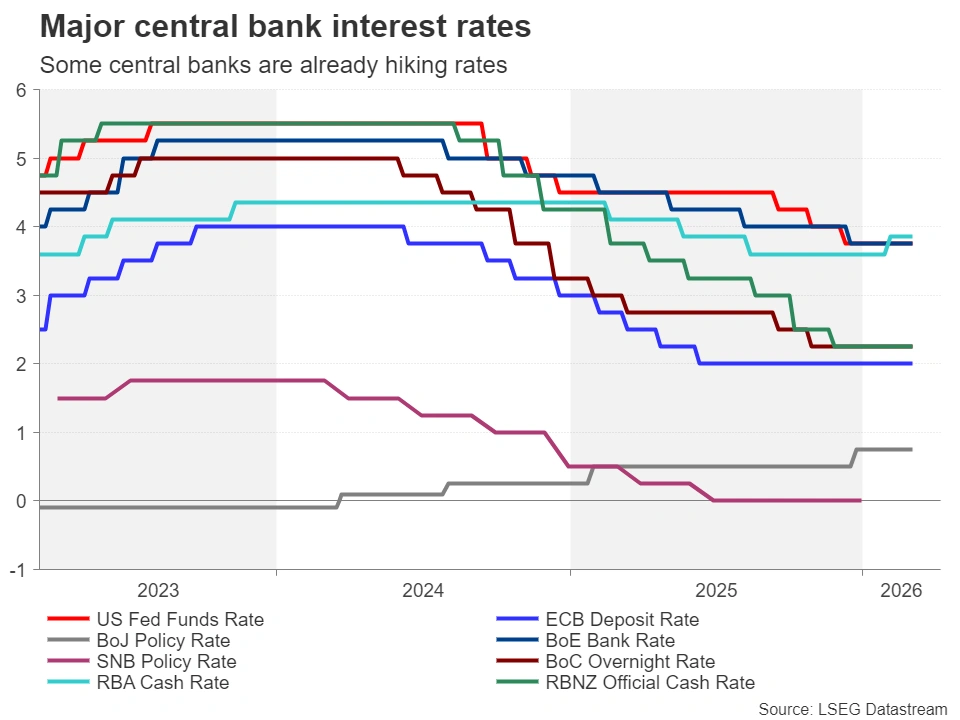

This is the last thing that central banks were hoping to revisit, as interest rates around the world have yet to return to their pre-pandemic levels. Although some central banks such as the Bank of Japan and Reserve Bank of Australia were on a tightening path well before the flare-up in Iran, others like the Federal Reserve and Bank of England looked set to cut rates by at least twice this year.

Even the European Central Bank, which has been on pause since last June, was moving towards a dovish bias before the outbreak of war amid declining price pressures in the euro area.

But hopes of additional rate cuts have now gone up in smoke, as policymakers are unlikely to signal fresh reductions in borrowing costs until oil and gas prices have peaked and they have some clarity on where inflation is headed. The most pressing issue for investors is that the White House doesn’t seem to have a clear end plan on Iran, casting doubts on Trump’s claim that the war will end “very soon”.

Iran’s neighbours can’t escape the missile barrage

Moreover, Iran has been carrying out counter strikes not just on US bases and interests in the region, but also against its neighbours, hitting their oil refineries and civilian targets such as Dubai airport. Hence, there is a high risk of further escalation, as Arab powers could decide to engage in direct military confrontation with Iran if Tehran continues to bomb them.

In the meantime, there is a growing risk of global fuel shortages from the ongoing blockage of the Strait of Hormuz. The problem is that even if there was a significant de-escalation in the war so that oil and LNG tankers started sailing again through the key shipping lane, it could take several weeks for shuttered production facilities to return to normal output. There’s also a danger that Iran and its proxies will not cease striking ships along Hormuz or other targets at every opportunity even with diminished capabilities after the US and Israel have stopped their attacks.

Fears of Energy crisis sparks market turmoil

Coordinated efforts for rich nations, such as the G7 countries, to release some of their strategic oil reserves may well end up being too little too late. It’s no surprise therefore that after a somewhat contained response to the onset of war in the Middle East, markets are now in full panic mode.

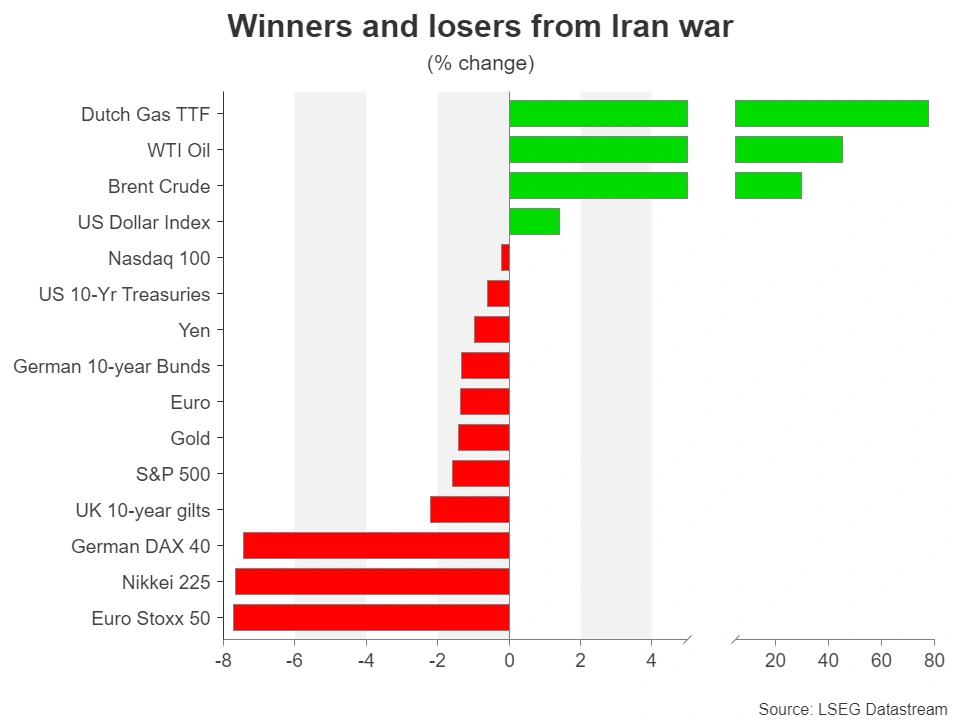

Both WTI and Brent crude futures spiked to almost $120 a barrel, while Dutch TTF futures – the benchmark for European gas prices – are up about 75% year-to-date.

Bond markets are starting to panic too, with government bond yields surging, signalling heightened fears of inflation. Global equities have slid to multi-month lows amid the renewed prospect of high inflation, high interest rates and talk of recession. Some of the hardest hit are Germany’s DAX and Japan’s Nikkei 225 indices. In both cases, the overreliance on gas and oil imports by Germany and Japan respectively, threatens to cause some serious pain for their exporters.

In addition, with debt jitters not fully subsided, some governments like in the UK are already considering the possibility of fresh financial support to households to help ease the burden of steeper energy prices.

Central banks once again face stagflation dilemma

What’s more crucial, however, is that even if a lot of these risks don’t materialize, the least that can be expected is that confidence in the major economies around the world will suffer a substantial knock, as this crisis comes hot on the heels of the unwelcome comeback of US tariff-related uncertainty.

Lower economic growth tends to strengthen the argument for rate cuts, but once again central banks find themselves in a dilemma of whether to boost growth or bring inflation under control.

Investors think inflation will take priority and have priced out rate cuts for the likes of the Fed and Bank of England, and priced in rate increases for the ECB, Bank of Canada and Reserve Bank of New Zealand. Oddly, rate hike expectations for the Bank of Japan have increased only modestly, possibly because of how an energy shock could impact the broader economy.

Will Trump keep the war short?

On the whole, it’s probably too early to predict how this latest crisis will unravel, as the US and Israel could end their military campaign within days, restoring safe passage through the Strait of Hormuz. Or, in the worst-case scenario, the war could stretch for several more weeks, dragging other countries into the conflict, with many predicting that we are on the cusp of World War III.

Most likely, however, Trump will not want to get too embroiled in the Middle East as a prolonged conflict risks pushing up energy prices permanently, which is not desirable ahead of the US midterm elections in November. The danger here is that a US pullout may not necessarily bring a resolution to the war.

WTI (Oil) Forms a Tight Range After Trump’s Comments – Oil Dynamics and Intraday Analysis

- Oil just concluded a historic session yesterday, with 30% moves up and down in a crazy rollercoaster.

- WTI is the subject of global fears, as real-economy supply shocks get priced further, but prices are stabilizing.

- Exploring an in-depth Technical Analysis of the commodity.

Yesterday's historic session in Oil

Once again, Black Gold found itself in the middle of chaotic price action, with yesterday's session breaking records across all types of volatility.

The Globex open saw an 11% gap (from $92 to $103) that quickly turned into a 30% squeeze towards $120 – That lasted from 18:00 on Sunday to 22:00.

Shortly after, G7 Leaders united to prepare for the potential release of Strategic Reserves, which aimed to calm Markets significantly and worked well, bringing commodity prices back to their weekly opening levels.

Shortly after, G7 Leaders united to prepare for the potential release of Strategic Reserves, which aimed to calm Markets significantly and worked well, bringing commodity prices back to their weekly opening levels. The Reserves will not be released just yet, but the comments helped soothe the overall panic.

President Trump added more fuel to the volatility fire by saying during a private ABC interview that the war could be resolved "very soon".

The issue with this comment is that it was quickly taken out of context and led to a $12 drop in WTI prices, but erased some of this progress overnight.

WTI Oil 5M Chart from March 9, 2026. Source: TradingView

So what's the update?

Unfortunately, despite Trump's optimistic comments in yesterday's late afternoon, the War won't conclude so easily.

The President's advisors have urged him to prepare a concrete exit plan – while military progress has been advancing well, there are still clouds over the proper way to achieve lasting peace or even the desired regime change.

The anxiety will remain if no clear plan is made, with attacks on civilian infrastructures all over the Middle East continuing. After 11 days of conflict, it may be too early to assume the counterattacks will continue indefinitely, but some clarity would be very welcome.

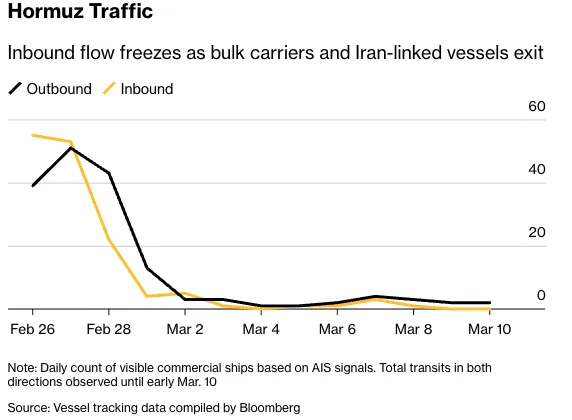

The Strait of Hormuz remains in de facto closure, with some thin traffic through, but this pales in comparison to usual flows as drone and ballistic missile threats remain elevated.

Strait of Hormuz Sea Traffic since February 27 – Source: Bloomberg

To respond to the large drops in maritime shipments, Saudi Aramco signalled that they were ramping up Oil flows in the East-West pipeline to full capacity and they are slowly getting there.

However, this would only add to 7M barrels/day which doesn't come close to the usual 20M bbl/day going through Hormuz in normal activity – The world's largest energy-commodity production firm mentioned some 180M barrels of Oil getting affected by the ongoing conflict.

Furthermore, the IRGC makes sure to not only strike civilian infrastructures but also Oil and Natural Gas production facilities.

With volatility now largely slowing down, let's explore a few key charts and scenarios for WTI (US) Oil to prepare for potential breakout levels.

US Oil Intraday Time-frame Analysis

WTI 4H Chart

WTI Oil 4H Chart – March 10, 2026. Source: TradingView

Oil is now returning within its past week's upward channel, having largely cut off its squeeze-momentum.

This implies that the largest volatility spikes are now behind us.

Even with the 4H timeframe RSI falling, there is still a decent probability that Oil will grind higher towards $100, particularly if the conflict drags on further – For now, momentum remains more neutral than anything.

Let's look at further details.

WTI 2H Chart and Technical Levels

WTI Oil 2H Chart – March 10, 2026. Source: TradingView

Due to its recent volatility, WTI has established many Support and Resistance levels and they require flexibility as they have been changing by the minute. The key levels are bolded.

To check out different trading scenarios, I invite you to check out the 30M chart just below.

WTI Technical Levels:

Resistance Levels

- $89 to $91 Channel and potential range highs

- April 2024 Top Major Momentum Pivot $86.50 to $88.00

- Resistance $93.50 to $95 (Bullish above!)

- $98 to $100 Resistance

- $106 to $108 June 2022 Resistance

- 2022 and Monday highs $116 to $120

Support Levels

- $82.80 to $84 Daily Support and channel lows (immediate test)

- 2025 Highs Key Support $78 to $80

- Past week spike $73.00 to $74.00

- $69 to $70 Main Support

- September 2025 Mid-term Support $67.50 to $68

- 2025 lows $55.00

WTI 30M Chart

WTI Oil 30M Chart – March 10, 2026. Source: TradingView

Oil is now well within its ascending channel, hence this provides essential trading levels to keep in check:

- Coming at the lows of the channel, selling exhaustion could point to a short-term rebound towards $90 – look at the 30M 50-period MA.

- A range between $82 to $90 could well be taking place, so look at whether the move remains contained.

- Breaking the daily support ($82.80) and Channel would point to a test of the $76 Support

Any break above $90 with high momentum and volume would imply a test of $95; $100 could then get reached fast depending on the news.

Safe Trades, a restful weekend, and keep track of the advancement of the conflict!

Sunset Market Commentary

Markets

A relief rally swept across financial markets today. Stock markets rally more than 2% in Europe. They open flat on Wall Street but that’s because they already banked on improved sentiment late yesterday. None other than Donald Trump was responsible. The US president suggested in CBS News the war could end soon (though not this week) and floated a possible waiver to oil-related sanctions after having called with Russian president Putin. It pressured oil prices yesterday in late US dealings and continued to do so today. Brent oil slides to $91 per barrel, down 8% from yesterday’s close. Correlated commodities such as gas prices drop significantly too (Dutch TTF -15%). No one actually knows what sanctions the Trump administration is considering to ease or how soon “soon” really is. It makes us at least cautious in terms of the sustainability of today’s rally, particularly in European (risk) assets. To that end it’s worth nothing that the euro is unable to keep its early and all in all limited gains against the likes of the US dollar. EUR/USD hit an intraday high of 1.166, the best level since March 3, before returning to around opening levels of 1.163. The common currency also continues to bite the dust against GBP. EUR/GBP slides to 0.865 despite the interest rate differentials this time working against GBP. Gilt yields tank 10 bps at the front compared to 5 bps in Europe/Germany. We also note the fact that cross currency basis swaps since the war erupted actually moved in favour of both USD and GBP (although less dramatically, but still) compared to EUR. FX markets appear specifically worried for what an energy price spike could mean for the European mainland. With the UK not at all insulated from the matter, we continue to err to the side of caution for GBP. Technicals suggest a GBP recovery could go as far as EUR/GBP 0.86. G7 energy ministers meanwhile are meeting in Paris to continue a debate on a possible release of strategic oil reserves to alleviate the oil price spike. With Brent currently stabilizing – even dropping – they do well to keep the powder dry for as long as possible. US yields today eke out a couple of basis points in a bear steepening move (up to 3.8 bps at the long end). Economic data included an average 15.5k weekly ADP job gain in the four weeks ending February 21, matching the previous reading. Existing home sales shot up 1.7% m/m to 4.09m, topping expectations. Neither print affected FX or FI markets.

News & Views

Hungarian February inflation dropped more than expected. Headline inflation rose 0.1% M/M and 1.4% Y/, down from 0.3% M/M and 2.1% in January. As such, inflation dropped below the MNB inflation target range of 3% +/- 1pt tolerance band. Market expectations were for a figure near 1.7%. In a first analysis, the national bank of Hungary (MNB) analyzed that core inflation and core inflation ex indirect taxes both declined to 2.1% Y/Y. MNB also takes notice that ’incoming inflation data was lower than the projection in the December Inflation Report, driven by more favourable changes in the price of food and market services than expected’. Disinflation of all main product groups (except for fuels) contributed to the decline in the annual index. In a monthly perspective, the MNB indicates that monthly repricing was lower than the 2017-2020 average. The inflation of tradables declined to 2.1 Y/Y. Market services prices rose 0.4% M/M but slowed to 5.2% Y/Y from 5.7%. Forint short-term yields this morning eased a bit further after the favourable inflation release. In a stable global context, today’s inflation data probably would have rubberstamped an additional MNB rate cut at the March 24 meeting. However, with the MNB still giving weight to financial stability considerations, money markets mainly expect the MNB to hold rates unchanged for the foreseeable future. The easing of market tensions today allows to forint the regain some ground (EUR/HUF 385).

CPI inflation in Norway rose 0.6% M/M and 2.7% Y/Y down from 3.4% Y/Y last month. Underlying CPI-ATE inflation (ex. tax changes and energy) rose 0.7% M/M but the Y/Y figure also eased to 3% from 3.4%. The outcome was close to expectations. However, it came after a big upward surprise in January. The latter had made markets reconsider the room for the Norges Bank to gradually ease its policy rate (currently 4%) as still guided at the time of the end January policy meeting . Even so, markets currently still see a modest risk (+/- 35% chance) for the next NB move to be a rate hike rather than a rate cut. The Norwegian krone due to its energy-/oil-related profile over the previous week continued its rise against the euro that was already in place since the turn of the year. EUR/NOK currently trades near 11.14, testing the lowest levels (strongest for the krone) since July 2023.

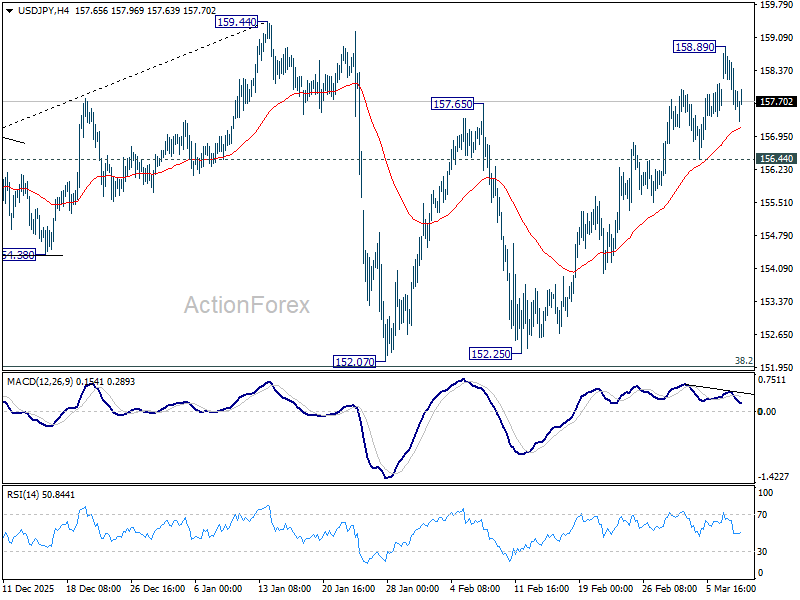

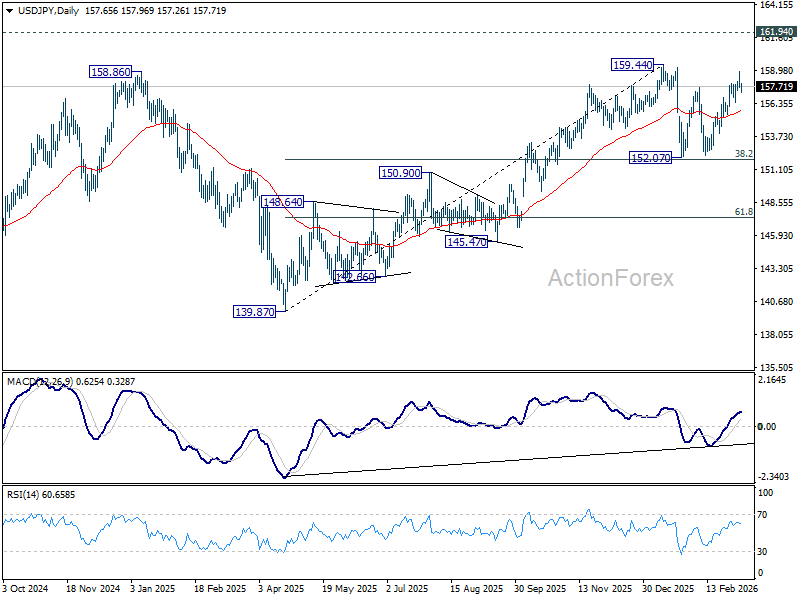

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 157.23; (P) 158.06; (R1) 158.50; More...

Intraday bias in USD/JPY remains neutral at this point. On the upside, above 158.89 will extend the rise from 152.07 to 159.44 resistance. Decisive break there will target 161.94 high next. However, considering bearish divergence condition in 4H MACD, firm break of 156.44 support will argue that the rebound has completed, and turn bias back to the downside for 152.07 support. Overall, price actions from 159.44 are viewed as a near term consolidation pattern. Outlook will remain bullish as long as 38.2% retracement of 139.87 to 159.44 at 151.96 holds.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.16) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

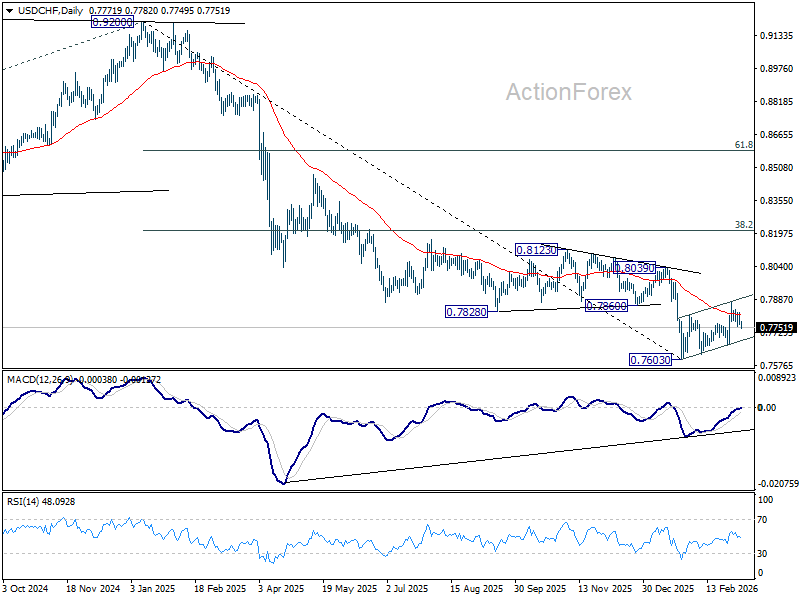

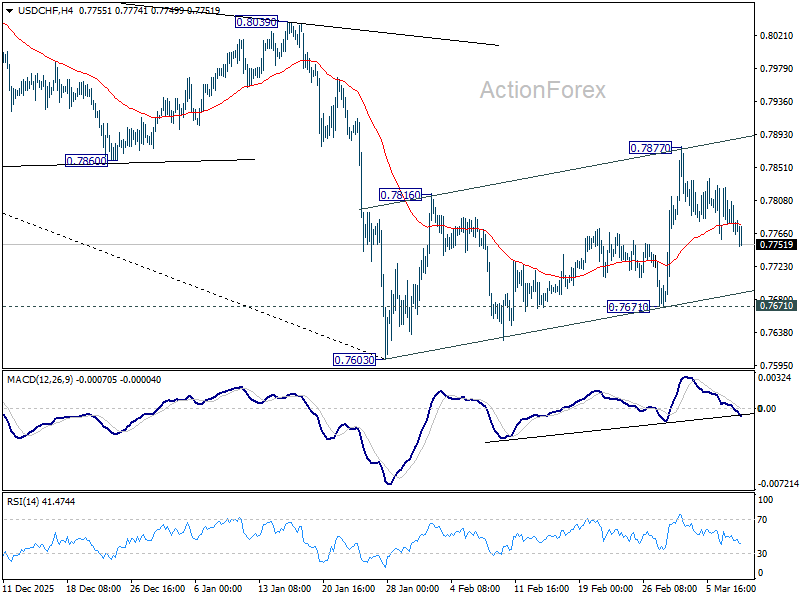

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7751; (P) 0.7792; (R1) 0.7814; More….

USD/CHF gyrates lower today but stays well above 0.7671 support. Intraday bias remains neutral first. On the downside, break of 0.7671 support will revive near term bearishness and bring retest of 0.7603 low. Decisive break there will resume larger down trend. On the upside, though, break of 0.7877 will bring stronger rally to 0.8039 resistance next.

In the bigger picture, a medium term bottom could be in place at 0.7603 on bullish convergence condition in D MACD, Firm break of 0.8039 resistance will argue that it's at least correcting the down trend from 0.9002. Stronger rebound would then be seen to 38.2% retracement of 0.9200 to 0.7603 at 0.8213. However, break of 0.7603 will resume the down trend to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.