Sample Category Title

AUD/USD Daily Report

Daily Pivots: (S1) 0.7058; (P) 0.7115; (R1) 0.7177; More...

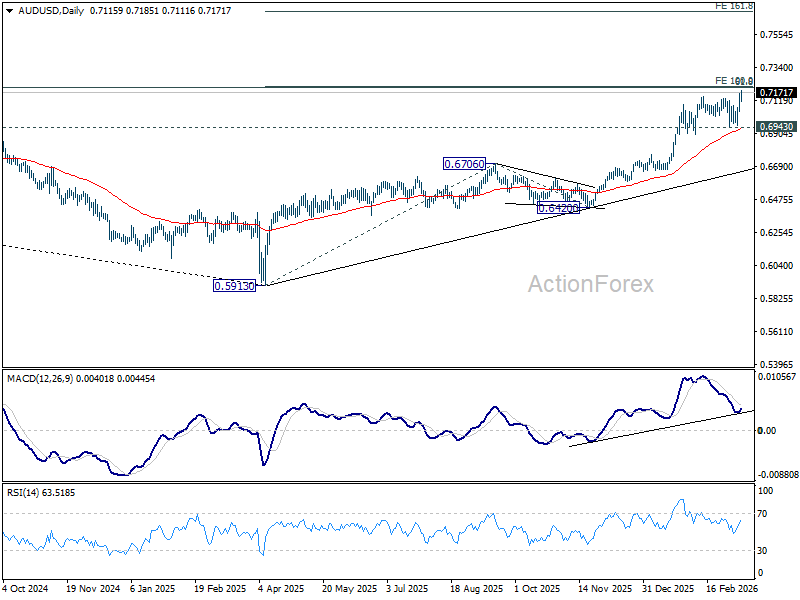

AUD/USD's rally resumed by breaking through 0.7146 resistance today. Intraday bias is back on the upside for 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213. Decisive break there could prompt upside acceleration to 161.8% projection at 0.7703. For now, outlook will remain bullish as long as 0.6943 support holds, in case of retreat.

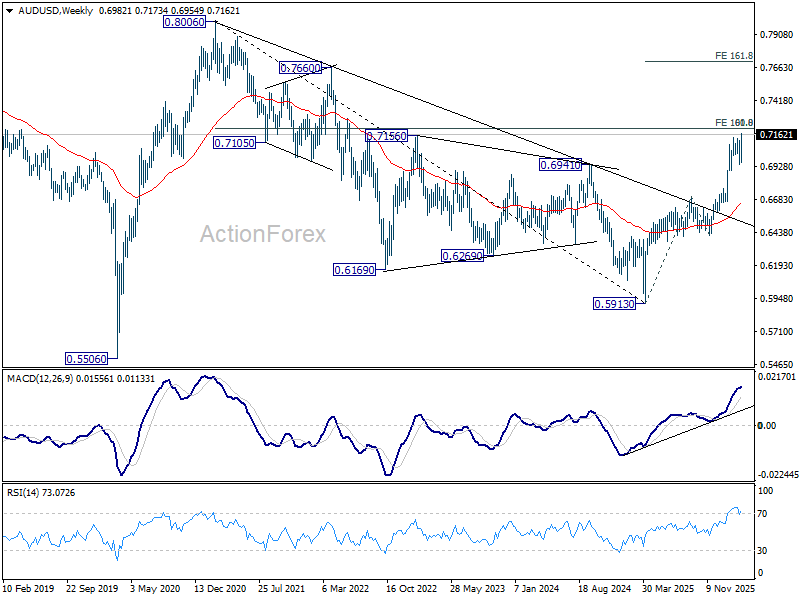

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will pave the way back to 0.8006. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3547; (P) 1.3575; (R1) 1.3609; More...

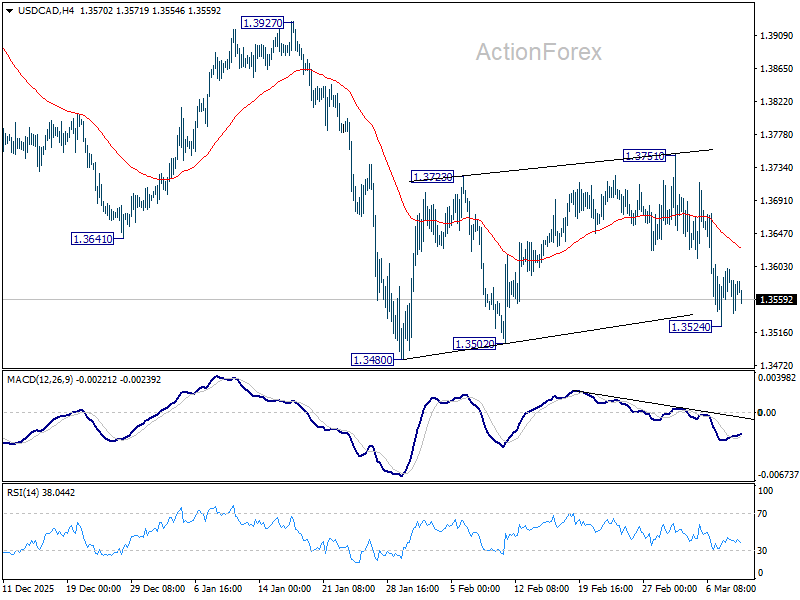

Intraday bias in USD/CAD is turned neutral first with a temporary low formed at 1.3524. Nevertheless, outlook is unchanged that consolidation pattern from 1.3480 could have completed at 1.3751, after hitting 55 D EMA (now at 1.3704). Risk will stay on the downside as long as 1.3751 resistance holds. On the downside, below 1.3524 will bring retest of 1.3480 low. Firm break there will confirm resumption of whole fall from 1.4791, and target 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. For now, medium term outlook will be neutral at best, until there are signs that the correction has completed, or that a bearish trend reversal is confirmed.

Dollar Weakens Ahead of February CPI, Last Clean Inflation Read Before Iran War

The "safe haven" trade continues to unwind today, as seen in the weakness in Dollar. This softening is mirrored across the traditional safe-haven trio, with Yen and Swiss Franc also underperforming. The primary catalyst for this shift in sentiment is the "Trump de-escalation" narrative regarding the Iran conflict, which has successfully pulled a significant portion of the geopolitical risk premium out of the currency markets.

Meanwhile, the greenback is not simply drifting; it is bracing for a critical fundamental test in the form of the February US CPI data. The timing of this February report is particularly vital. Because the massive "war premium" that spiked gasoline and energy prices occurred late in the month and into March, today’s data offers a final "clean" look at underlying US inflation. It represents the baseline of price pressures that existed before the latest global shock, allowing the market to see if the disinflationary trend continued to stall, or even reversed.

Expectations for the Fed’s policy path have undergone a drastic recalibration since the onset of the Iran conflict. While the market was once hopeful for a series of aggressive cuts in early 2026, those dreams have largely evaporated. However, it is important to note that expectations have not yet flipped to a regime of further rate hikes; instead, the market has just moved into a defensive "higher for longer" stance.

Traders are now treating a March "hold" as a certainty, with the focus shifting to the mid-year outlook. Fed Fund futures currently indicate only a 40% chance of a cut in June, making September the more realistic candidate for any policy easing. This reflects a broader consensus that we are looking at a maximum of two cuts this year, a far cry from the aggressive easing cycles predicted just months ago.

Today’s core inflation readings will be an important arbiter of this outlook. Should Core CPI print higher than 0.3% mom, or exceed 2.5% on an annual basis, the narrative could shift significantly. Such a "hot" reading would likely force traders to move beyond the "hold" scenario and seriously entertain the possibility of an interest rate hike to combat a secondary wave of inflation.

Conversely, a downside surprise in the core readings would be a major relief for the markets. If a cooling CPI is coupled with the current pullback in oil prices—specifically if Brent and WTI slide below 80 mark—hopes for a rate cut in the first half of the year could be revived. This would likely accelerate the Dollar’s slide as the "yield advantage" narrative weakens.

For the week so far, Aussie is leading the pack as the week’s top performer. Markets are aggressively betting on a hawkish divergence, where the RBA pulls ahead a rate hike from May to this month. Following the Aussie’s lead are the Kiwi and Sterling, both of which are capitalizing on the "risk-on" mood. These currencies are effectively absorbing the liquidity that is currently exiting the safe-haven trio of Dollar, Yen, and Franc, which sit at the bottom.

In Asia, at the time of writing, Nikkei is up 1.94%. Hong Kong HSI is down -0.20%. China Shanghai SSE is down -0.04%. Singapore Strait Times is down -0.11%. Japan 10-year JGB yield is down -0.012 at 2.174. Overnight, DOW fell -0.07%. S&P 500 fell -0.21%. NASDAQ rose 0.01%. 10-year yield closed flat at 4.136.

AUD/USD Breakout as RBA Faces Urgency to Hike, 0.80 After Clearing 0.72?

Aussie has staged a remarkable breakout today, surging broadly higher to clip a near four-year peak against Dollar. AUD/USD is now knocking on the door of a critical resistance zone at 0.72. Firm break above this level wouldn't just be a win for the bulls—it would signal strong underlying momentum that could pave the way for a climb toward 0.77 or even a return to 0.80 handle.

This aggressive rally isn't happening in a vacuum. It is being fueled by a violent repricing of interest rate expectations. Global markets have suddenly realized that the RBA is pivoting toward a much more aggressive tightening cycle than anyone predicted just a month ago. The "patience" stance is being replaced by a sense of tactical urgency.

Previously, the "consensus" roadmap was clear and cautious. Following the 25bp hike to 3.85% in February, the RBA was expected to hold steady on March 17. The plan was to wait for the comprehensive quarterly CPI data in late April before considering a follow-up move in May. It was a "wait-and-see" approach designed to protect the economy.

However, the outbreak of the Iran war has shredded that calculus. The geopolitical shock sent oil prices into a frenzied spike to $120 earlier this week. While prices have pulled back, they remain stubbornly elevated above $80—carrying a "war premium" of roughly $20 compared to pre-conflict levels. For a central bank fighting inflation, this is an external shock that cannot be ignored.

The RBA could now view waiting until May as a luxury it simply cannot afford. There is a growing fear within the Board that if inflation expectations become "unanchored" due to this energy shock, the genie will be impossible to put back in the bottle. To prevent inflation from running further away, the RBA could feel compelled to act as an "inflation hawk" right now.

The data justifies this anxiety. Headline CPI sat at 3.8% in January, but the real concern lies in the Trimmed Mean, which rose to 3.4%. Both figures are well above the RBA’s 2–3% target range. More importantly, the rise in the Trimmed Mean—which strips out volatile items like petrol—proves that inflation is not just a "fuel story." It is becoming "sticky" and embedded across the broader service economy.

The messaging from Martin Place has been unusually blunt. Deputy Governor Andrew Hauser has led the charge this week, using his platform to describe high inflation as "toxic." He cautioned that the Middle East conflict could push domestic prices even higher, emphasizing that the March 17 meeting will involve a “very genuine debate” about hiking. In central-bank-speak, a "genuine debate" is a clear warning that a hike is on the table.

The banking sector has heard the message loud and clear. NAB and Westpac official teared up their old playbooks. Both banks now forecast back-to-back 25-basis-point hikes in both March and May.

Technically, AUD/USD's up trend from 0.5913 (2025 low) resumed today and it will soon be testing a key cluster resistance zone at around 0.72. That zone includes 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213, and 61.8% retracement of 0.8006 (2021 high) to 0.5913 at 0.7206. Decisive break there would pave the way to 161.8% projection at 0.7703 or even further to 0.8006 high.

Japan import costs surge on weak Yen, fastest since July 2024

Japan’s producer inflation moderated in February, offering some relief on the domestic cost front even as import prices surged. Producer Price Index rose 2.0% yoy, slowing from January’s 2.3% pace and coming in slightly below market expectations of 2.1%.

The softer PPI reading suggests upstream price pressures in Japan’s domestic production sector may be easing slightly. However, the picture is less benign when looking at import costs, which are heavily influenced by Yen’s weakness.

Japan’s yen-based import price index jumped 2.8% yoy, accelerating sharply from a revised 0.7% increase in January and marking the fastest rise since July 2024. The data highlights how the weak Yen continues to push up import costs, a dynamic that could keep underlying inflation pressures elevated despite the moderation in producer prices.

ECB’s Lagarde says too much uncertainty to predict March rate decision

ECB President Christine Lagarde signaled that policymakers will remain vigilant against inflation risks stemming from the Iran war while avoiding hasty decisions in the face of heightened uncertainty. In an interview with France2, Lagarde said the ECB will ensure the conflict does not trigger the kind of inflation shock the Eurozone experienced after Russia’s invasion of Ukraine.

“We are in an economic situation that’s different,” Lagarde said, adding that the Eurozone now has a "greater capacity" to manage disruptions. She emphasized that the ECB will take the necessary steps to keep inflation under control and avoid a repeat of the sharp price increases seen in 2022 and 2023 following the energy crisis triggered by the Ukraine war.

At the same time, Lagarde acknowledged that the current geopolitical environment makes policymaking particularly challenging. With the Iran conflict adding new uncertainty to global energy markets, she said it was impossible to predict the outcome of the ECB’s March 18–19 policy meeting. “There is so much uncertainty that I’d be incapable to say precisely what we will decide,” she said.

Lagarde added that the degree of volatility currently facing policymakers is unusually high, even compared with the turbulence seen during the 2022 energy shock. Nevertheless, she rejected the suggestion that Europe is heading toward stagflation, insisting that the ECB remains committed to maintaining price stability while navigating the heightened uncertainty.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3547; (P) 1.3575; (R1) 1.3609; More...

Intraday bias in USD/CAD is turned neutral first with a temporary low formed at 1.3524. Nevertheless, outlook is unchanged that consolidation pattern from 1.3480 could have completed at 1.3751, after hitting 55 D EMA (now at 1.3704). Risk will stay on the downside as long as 1.3751 resistance holds. On the downside, below 1.3524 will bring retest of 1.3480 low. Firm break there will confirm resumption of whole fall from 1.4791, and target 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. For now, medium term outlook will be neutral at best, until there are signs that the correction has completed, or that a bearish trend reversal is confirmed.

Elliott Wave Perspective: Assessing Oil’s (CL) Upside Amid War-Driven Volatility

The short-term Elliott Wave outlook in Crude Oil (CL) indicates that the cycle from the December 16, 2025 low has advanced as a five-wave impulse. From that low, wave (1) concluded at $66.48, followed by a corrective pullback in wave (2) which ended at $61.12. The commodity then resumed its upward trajectory in wave (3), reaching $77.98, before another retracement in wave (4) that settled at $71.65. The final leg, wave (5), extended sharply and terminated at $119.40, thereby completing wave ((1)) at a higher degree. With this structure in place, the market has now entered a corrective phase in wave ((2)), designed to retrace the cycle that began in December 2025.

The internal subdivision of this correction is unfolding as a zigzag pattern. From the $119.40 peak, wave (A) declined impulsively and ended at $76.73. Subsequently, wave (B) has begun to rally, working to correct the cycle from the March 9, 2026 high. This rally is expected to be temporary, setting the stage for another downward move in wave (C).

Near term, as long as the pivot at $119.40 holds, the rally is projected to fail in either three or seven swings. Such a failure would confirm the continuation of the larger degree correction against the December 16, 2025 low. Traders should therefore remain cautious, recognizing that the prevailing structure favors another leg lower before a sustainable recovery can emerge.

Oil (CL) 60-Minute Elliott Wave Chart

CL Elliott Wave Video:

https://www.youtube.com/watch?v=1MUzJnJme6Y

AUD/USD breakout as RBA faces urgency to hike, 0.80 after clearing 0.72?

Aussie has staged a remarkable breakout today, surging broadly higher to clip a near four-year peak against Dollar. AUD/USD is now knocking on the door of a critical resistance zone at 0.72. Firm break above this level wouldn't just be a win for the bulls—it would signal strong underlying momentum that could pave the way for a climb toward 0.77 or even a return to 0.80 handle.

This aggressive rally isn't happening in a vacuum. It is being fueled by a violent repricing of interest rate expectations. Global markets have suddenly realized that the RBA is pivoting toward a much more aggressive tightening cycle than anyone predicted just a month ago. The "patience" stance is being replaced by a sense of tactical urgency.

Previously, the "consensus" roadmap was clear and cautious. Following the 25bp hike to 3.85% in February, the RBA was expected to hold steady on March 17. The plan was to wait for the comprehensive quarterly CPI data in late April before considering a follow-up move in May. It was a "wait-and-see" approach designed to protect the economy.

However, the outbreak of the Iran war has shredded that calculus. The geopolitical shock sent oil prices into a frenzied spike to $120 earlier this week. While prices have pulled back, they remain stubbornly elevated above $80—carrying a "war premium" of roughly $20 compared to pre-conflict levels. For a central bank fighting inflation, this is an external shock that cannot be ignored.

The RBA could now view waiting until May as a luxury it simply cannot afford. There is a growing fear within the Board that if inflation expectations become "unanchored" due to this energy shock, the genie will be impossible to put back in the bottle. To prevent inflation from running further away, the RBA could feel compelled to act as an "inflation hawk" right now.

The data justifies this anxiety. Headline CPI sat at 3.8% in January, but the real concern lies in the Trimmed Mean, which rose to 3.4%. Both figures are well above the RBA’s 2–3% target range. More importantly, the rise in the Trimmed Mean—which strips out volatile items like petrol—proves that inflation is not just a "fuel story." It is becoming "sticky" and embedded across the broader service economy.

The messaging from Martin Place has been unusually blunt. Deputy Governor Andrew Hauser has led the charge this week, using his platform to describe high inflation as "toxic." He cautioned that the Middle East conflict could push domestic prices even higher, emphasizing that the March 17 meeting will involve a “very genuine debate” about hiking. In central-bank-speak, a "genuine debate" is a clear warning that a hike is on the table.

The banking sector has heard the message loud and clear. NAB and Westpac official teared up their old playbooks. Both banks now forecast back-to-back 25-basis-point hikes in both March and May.

Technically, AUD/USD's up trend from 0.5913 (2025 low) resumed today and it will soon be testing a key cluster resistance zone at around 0.72. That zone includes 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213, and 61.8% retracement of 0.8006 (2021 high) to 0.5913 at 0.7206. Decisive break there would pave the way to 161.8% projection at 0.7703 or even further to 0.8006 high.

RBA to Hike 0.25% in March, Follow-Up in May Also Expected

We revise our view of RBA policy: 25bp hikes in both March and May expected. Single hike still possible but not our base case.

The RBA is now expected to hike rates 25bp in both March and May; this is a change from our previous view of a single hike in May with further hikes as a risk only. The expected peak cash rate is now 4.35%.

The effect of higher oil prices on headline inflation is large but temporary. The RBA Monetary Policy Board will nevertheless feel compelled to react, especially given the hit to confidence and financial markets has so far not been severe.

Key information shifting our view is RBA communication revealing it has not changed its pessimistic view of growth in supply capacity following the national accounts, even though data revisions, consumption and unit labour costs paint a more benign picture. In addition, it has signalled a willingness to respond to the spike in headline inflation to head off a sustained rise in inflation expectations. This is despite expectations having remain anchored in recent years in the face of more lasting shocks.

This new information since the national accounts is in addition to the steer from the February minutes that the RBA believes that all the exchange rate appreciation this year reflects the changed domestic rates outlook. It has not allowed for any additional disinflation from the USD selloff separate from domestic rate moves. We think this puts downside risk into imported inflation relative to the RBA’s expectations, but not until at least late this year.

There are good arguments for staying on hold until May given the temporary nature of the shock and the possibility of more extreme market instability. A split vote at next week’s meeting is possible. Market participants should allow for the possibility that the RBA opts to wait until May, but it is no longer our base case. Similarly, a swift and clear resolution of the war (and fall in oil prices) or a clear and sudden loss of momentum in domestic activity would mean that the expected March hike would not be followed up in May. Again, this is not our base case, but we will keep the possibility under review.

By the end of next year, underlying inflation will be close to the 2½% target midpoint and unemployment noticeably higher. It will also be clearer that supply capacity growth is above 2% and that labour market slack is building outside the formal labour force. We therefore also shift our expectations of the necessary reversal of tight policy, to Nov and Dec 2027 and Feb 2028 (was Nov 2027 and Feb 2028).

These more frequent shifts in policy are partly a consequence of the refinement to the RBA’s mandate in the latest Statement on the Conduct of Monetary Policy. In addition, we assess that the recent changes in the composition of the Monetary Policy Board have made it more comfortable with policy activism and attempts to fine-tune policy to hit the target midpoint by a fixed horizon.

Ethereum Coils in Key Zone, Traders Brace for Break

Key Highlights

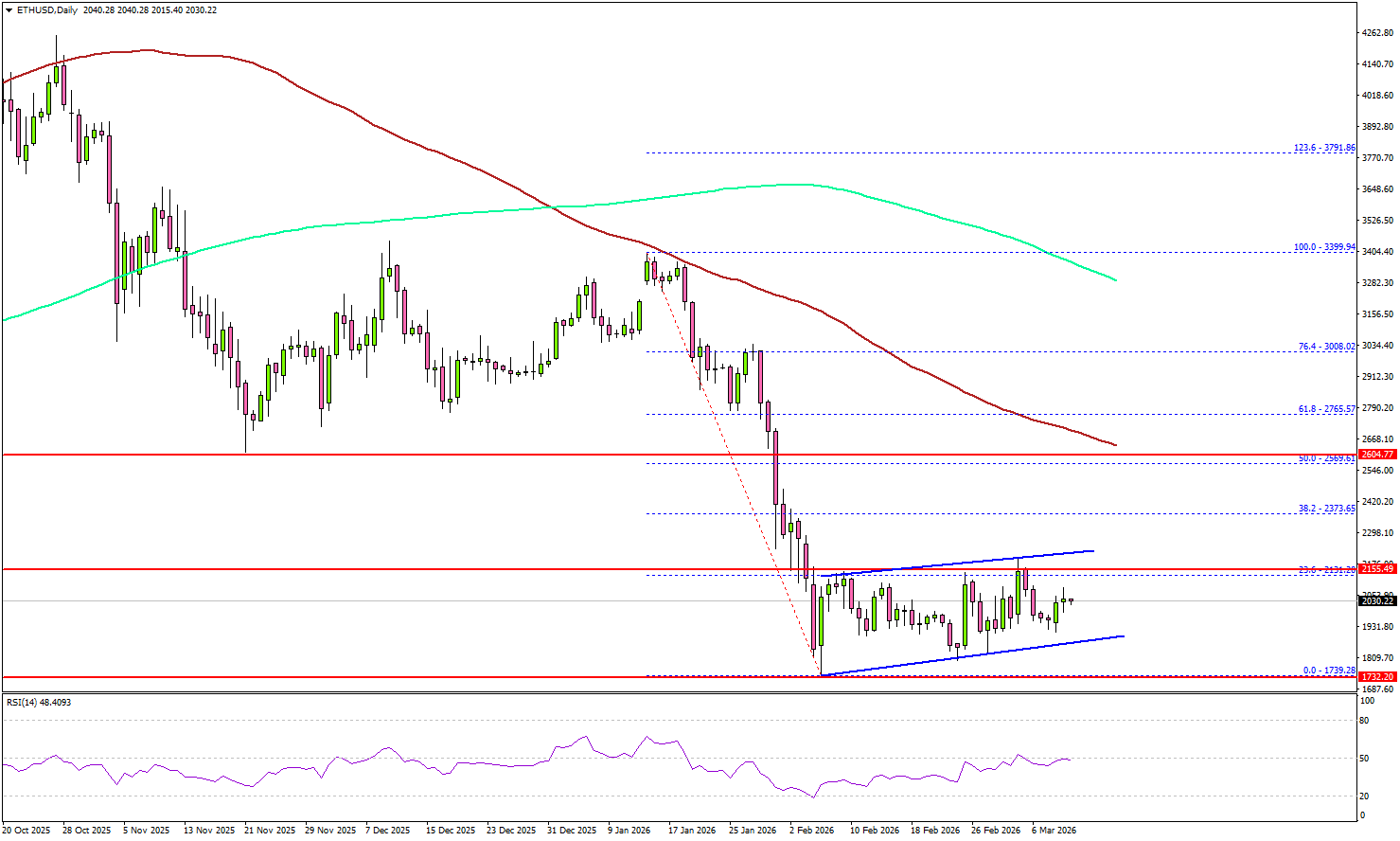

- Ethereum remained in a range above the $1,850 support.

- A rising channel is forming with support at $1,865 on the daily chart of ETH/USD.

- Bitcoin price started a fresh recovery wave above $68,000 and $68,500.

- XRP is consolidating above the key support at $1.3350.

Ethereum Technical Analysis

Ethereum failed to surpass $2,200 and trimmed gains. ETH declined below $2,050 but remained in a range above the $1,850 support.

Looking at the daily chart, the price again failed to clear the 23.6% Fib retracement level of the downward move from the $3,400 swing high to the $1,740 low. There is also a rising channel forming with support at $1,865.

On the upside, the bears might remain active near $2,120. The first key resistance could be near the $2,155 level. The main hurdle for bulls sits near $2,200.

A close above the $2,200 level could open doors for a larger upward movement. In the stated case, ETH could rise toward the 50% Fib retracement level of the downward move from the $3,400 swing high to the $1,740 low at $2,570 and the 100-day simple moving average (red).

On the downside, the bulls might be active near $1,950 and $1,920. The main support is now forming near $1,865, below which the price could slide toward $1,750. Any more losses might call for a move toward $1,650.

Looking at Bitcoin, there was another recovery wave, but the bears remained active below the $72,000 resistance zone.

Economic Releases

- US Consumer Price Index for Feb 2026 (MoM) – Forecast +0.3%, versus +0.2% previous.

- US Consumer Price Index for Feb 2026 (YoY) – Forecast +2.4%, versus +2.4% previous.

- US Consumer Price Index Ex Food & Energy for Feb 2026 (YoY) – Forecast +2.5%, versus +2.5% previous.

Japan import costs surge on weak Yen, fastest since July 2024

Japan’s producer inflation moderated in February, offering some relief on the domestic cost front even as import prices surged. Producer Price Index rose 2.0% yoy, slowing from January’s 2.3% pace and coming in slightly below market expectations of 2.1%.

The softer PPI reading suggests upstream price pressures in Japan’s domestic production sector may be easing slightly. However, the picture is less benign when looking at import costs, which are heavily influenced by Yen’s weakness.

Japan’s yen-based import price index jumped 2.8% yoy, accelerating sharply from a revised 0.7% increase in January and marking the fastest rise since July 2024. The data highlights how the weak Yen continues to push up import costs, a dynamic that could keep underlying inflation pressures elevated despite the moderation in producer prices.

ECB’s Lagarde says too much uncertainty to predict March rate decision

ECB President Christine Lagarde signaled that policymakers will remain vigilant against inflation risks stemming from the Iran war while avoiding hasty decisions in the face of heightened uncertainty. In an interview with France2, Lagarde said the ECB will ensure the conflict does not trigger the kind of inflation shock the Eurozone experienced after Russia’s invasion of Ukraine.

“We are in an economic situation that’s different,” Lagarde said, adding that the Eurozone now has a "greater capacity" to manage disruptions. She emphasized that the ECB will take the necessary steps to keep inflation under control and avoid a repeat of the sharp price increases seen in 2022 and 2023 following the energy crisis triggered by the Ukraine war.

At the same time, Lagarde acknowledged that the current geopolitical environment makes policymaking particularly challenging. With the Iran conflict adding new uncertainty to global energy markets, she said it was impossible to predict the outcome of the ECB’s March 18–19 policy meeting. “There is so much uncertainty that I’d be incapable to say precisely what we will decide,” she said.

Lagarde added that the degree of volatility currently facing policymakers is unusually high, even compared with the turbulence seen during the 2022 energy shock. Nevertheless, she rejected the suggestion that Europe is heading toward stagflation, insisting that the ECB remains committed to maintaining price stability while navigating the heightened uncertainty.

Metals Reject Their Daily Bounce After New Iran Threats – Gold (XAU/USD) & Silver (XAG/USD) Update

It's only Tuesday and we can already talk about an insane week!

After yesterday's chaos in the Oil Market, commodities still have a few surprises in store. Today seemed to mark a new beginning in the current war-flows, with Crude crawling back to $76.50 around the mid-session, a 35% move lower!

The ongoing profit-taking got stretched by the numerous dip-buying attempts and a falling volatility, but this didn't last long.

Metals had been enjoying a strong session, helped by the smoother inflation expectations as stagflationary pressure eased – Combining higher yields and a strong US Dollar, the recent War flows hadn't helped the highly positioned metals to rise.

The fact that the conflict also failed to gather proper risk-off Market flows insisted on these trends.

Nonetheless, as Oil fell back below $90, Precious metals quickly found a renewed bid, with Gold back above $5,200, Silver tipping the $90 level, and Platinum up more than 3%, a first since early February.

Current Session in Metals (15:05 ET) – Courtesy of Finviz. March 10, 2026

The issue with current moves, is that they tend to be erratic.

US Intel revealed that Iran was moving to place water mines in the Strait of Hormuz, which could prove to be a nail in the coffin for an already non-existent traffic (despite some form of progress in recent days).

The news quickly saw Oil prices rebounding back towards $84 and the action now bouncing from there!

WTI Oil 15M Chart. March 10, 2026. Source: TradingView

This led to a daily top in Equities and Cryptos, but more particularly in the subject of today's analysis: Metals.

Let's dive into intraday chart and levels for both Silver (XAG/USD) and Gold (XAU/USD) to see if the recent news really market a session top or if a more widespread bounce was to come.

Gold 4H Chart and Intraday Levels

Gold 4H Chart. March 10, 2026. Source: TradingView

These days, Markets aren't all about technical analysis (which still helps to find decent levels for decision-making, like entry and exits). The best way to navigate Markets are by looking at correlated and inversely correlated assets.

By looking at Oil movements, one was able to catch bottoms in Equities and Metals – A catalyst detailed in our past week US Dollar analysis.

So what about now? Since the Oil has marked its daily bottom, metals haven't been able to bounce, leading to the formation of a triangle formation.

- Breaking the 4H 50-Period MA would point to a quick test of the lower trendline around $5,050

- Any major break above the session highs ($5,238) would point to continue upside.

- This could lead to a retest of the $5,400 March highs

Levels of interest for Gold trading:

Support Levels:

- $5,180 4H 50-Period MA imminent support

- $5,050 to $5,100 Major support

- $4,850 to $4,900 Support (Mid-Feb Lows)

- Pivotal Support and December record $4,400 to $4,500 (Bearish below)

- Channel lows $4,200

Resistance Levels:

- Session highs ($5,238) and $5,250 Pivot Zone (+/- $25)

- $5,400 Wartime Resistance

- Current All-time Highs Resistance – $5,500 to $5,600

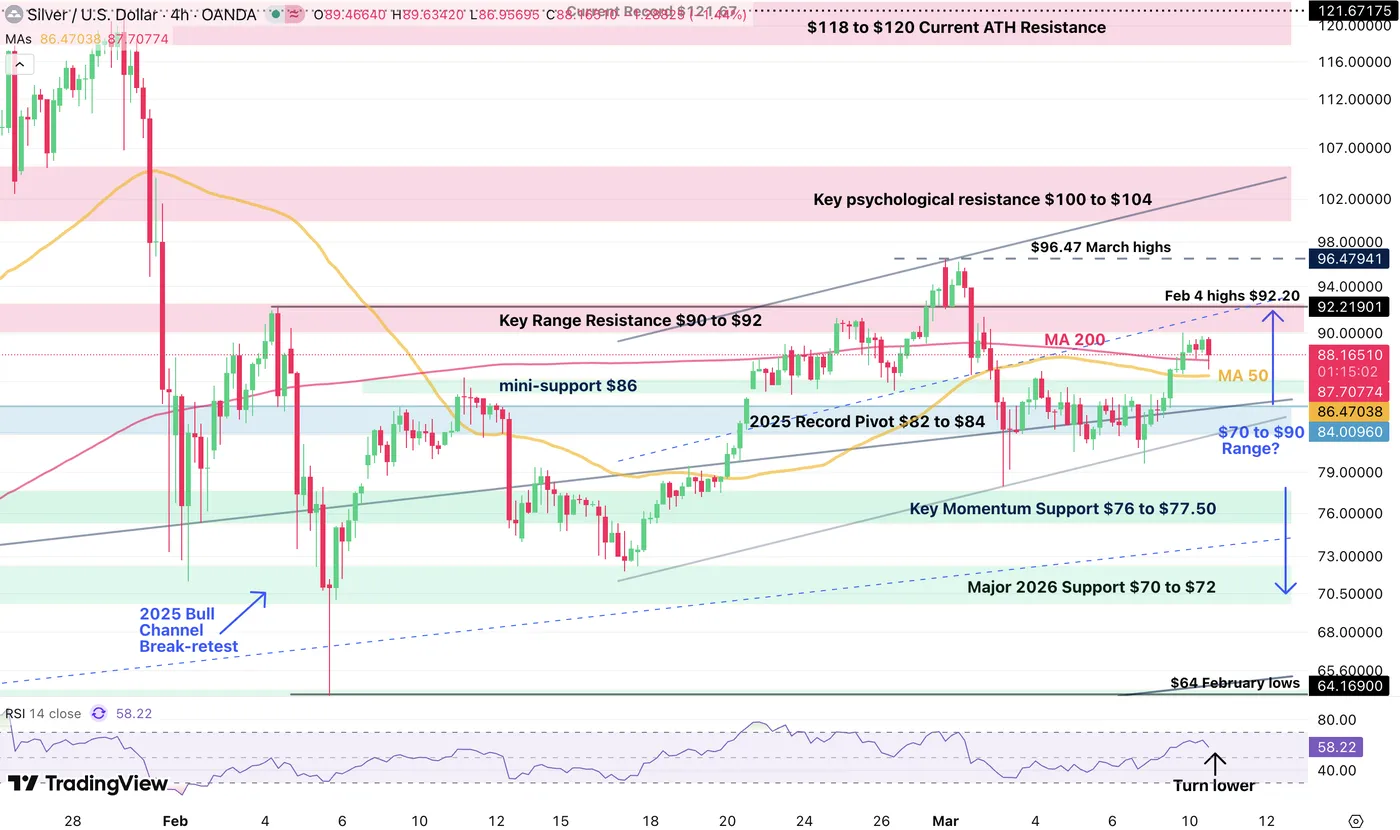

Silver (XAG/USD) 4H Chart and Intraday Levels

Silver 4H Chart. March 10, 2026. Source: TradingView

Silver also managed a decent push higher but is finding pressure as Oil maintains its rebound.

The key level to watch is $90:

- Having failed to break the level in today's action, odds are higher for a correction back towards at least $86

- Below this, $82 will be the next key Support on deck.

- For bulls, breaking above with a 1H close would point to higher chances of a breakout

Levels of interest for Silver trading:

Support Levels:

- Mini-support $86

- 2025 Record Pivot (Acting as key support) $82 to $84

- February Momentum Support $76 to $77.50

- Major 2026 Support $70 to $72

Resistance Levels:

- Key Range Resistance $90 to $92

- $96.47 March highs

- Key psychological resistance $100 to $104