Sample Category Title

Dollar Slightly Firmer, with USD/JPY an Outperformer

Markets

Markets had to navigate US presidents Trumps’ reaction to the Supreme Court ruling rejecting the IEEPA (reciprocal) tariffs yesterday. For now, the IEEPA tariffs are replaced by a 10% ‘temporary’ (max 150 days) global levy as the US administration develops more in depth investigations on security and trade topics that over time might result in a new tariff architecture. The US administration indicates that it is still working on an order to raise the 10% levy to 15% as President Trump announced this weekend. The new U-turn in US trade policy is causing uncertainty among trading partners on the impact on negotiated trade deals. In this respect, the EU Parliament already suspended the approval procedure for the EU-US trade deal that included a 15% tariff ceiling for most EU goods. However, as was often the case of late, this (trade) uncertainty in the first place caused some kind of market paralysis rather than an aggressive risk-off repositioning. Initial moves in core (US & EMU) yields and European equities were very modest. A weaker USD opening was also gradually reversed throughout the European session. Early in US dealings, the market focus shifted back to the lingering market theme of the potential AI disruption to other sectors as highlighted in a much-talked about new research report (Citrini Research; The 2028 global intelligence crisis). US equities finally tumbled between 1.66% (Dow) and 1.04% (S&P 500) lower. Even as the link between these potential AI-driven disruptions and monetary policy is far from clear, core bonds (and especially US Treasuries) captured a safe have bid. US yields finally declined between 6.4 bps (5-y) and 2.2 bps (30-y), the belly of the curve outperforming. The US 10-y yield (4.04%) now again nears the 4% barrier, to be compared with levels near 4.3% early February. The picture at the short end of the curve is less outspoken (2-y 3.45%) but key support (3.40% also comes within reach). German yields declined between 1.9 bps (30-y) and 3 bps (5-y). The dollar showed no unequivocal pattern. DXY closed marginally lower at 97.35. EUR/USD finished little changed near 1.1785.

Asian equities are hardly affected by the AI sell-off in the US this morning as investors focus more on chipmakers rather than companies that might by hurt by the AI-fall-out. US yields rise marginally after yesterday’s decline. The dollar is slightly firmer, with USD/JPY an outperformer (155.5). Later today, the eco calendar mostly contains second tier US data including the weekly ADP report, housing data, and consumer confidence. While interesting, they probably won’t profoundly change market expectations on Fed policy. Several Fed governors are scheduled to speak. The AI and trade themes will remain omnipresent. With respect to the latter, US president Trump’s State of the Union (Wednesday morning 03.00 CET) evidently contains the risk of some unexpected policy announcements. On US interest rate markets, we keep an eye at yields on several maturities (5-10-y) nearing YTD lows. At the same time the dollar is holding up well, with some first resistance levels still within reach (EUR/USD 1.175 area, DXY 98.1 area).

News & Views

New EU car registrations fell by 3.9% Y/Y in January. Apart from the traditional slumps in the month of August, the absolute levels of new car registrations fell below 800k for the first time in at least two years. Hybrid-electric car (HEV) registrations captured 38.6% of the market (up from 34.9%), remaining the preferred choice among consumers. Battery-electric cars (BEV) accounted for an 19.3% market share (up from 14.9% in Jan 2025). Together with plug-in EV’s, these three categories still showed Y/Y-increases. Combined market share of petrol and diesel cars fell to 30.1% (mainly petrol), from 39.5% a year ago. In Belgium petrol cars were the most popular (42.7% from 40.9%) followed by BEV’s (36.8% from 33.8%) and HEV’s (11.5%, stable). New Belgian car registrations fell 18.7% Y/Y.

Bloomberg reports that BusinessEurope, a powerful trade group that represents 42 national business federations, is drawing a report calling for reforms to the EU’s Emissions Trading System. The groupearlier warned that the risk of deindustrialization is high if the problem is not solved. He says that carbon costs are currently up to 30% of energy costs. At an industry summit in Antwerp earlier this month, German Chancellor Merz and several business CEO’s also called for ETS to be reformed. BusinessEurope calls amongst other for issuance of new allowances to be extended beyond the current implied 2039 cut-off date and more permits to be injected into the market via the Market Stability Reserve. The planned phase-out of free emissions allowances should be reconsidered, while finance raised through the ETS should be used to fund industrial decarbonization, rather than go into the EU budget.

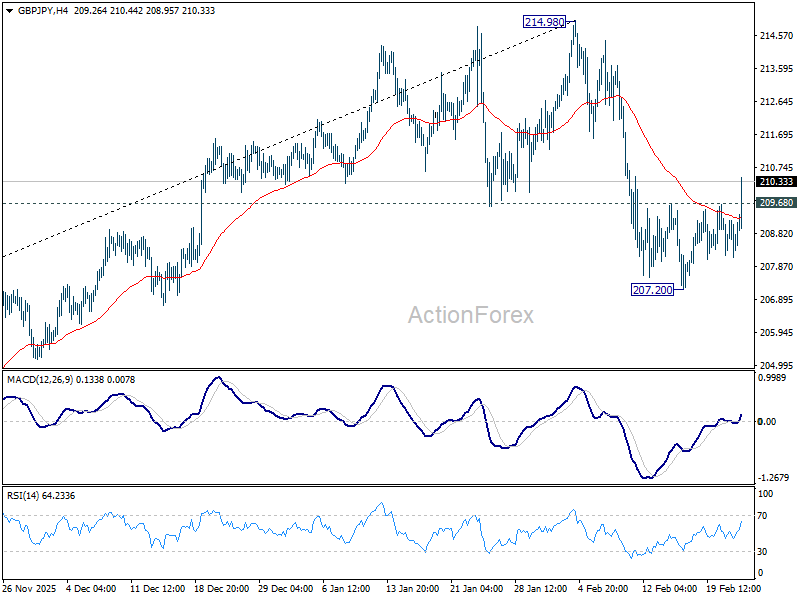

GBP/JPY Daily Outlook

Daily Pivots: (S1) 208.12; (P) 208.67; (R1) 209.21; More...

GBP/JPY's strong break of 209.68 minor resistance suggests that pullback from 214.98 has completed at 207.20 already. Intraday bias is back on the upside. Further rise should be seen to retest 214.98 first. Firm break there will resume larger up trend. For now, risk will stay on the upside as long as 207.20 holds, in case of retreat.

In the bigger picture, current development argues that price actions from 214.98 might be a near term consolidation pattern only. That is, larger up trend from 123.94 (2020 low) is still in progress. Firm break of 214.98 will target 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. On the downside, though, break of 207.20 will revive that case that it's already in a larger scale correction.

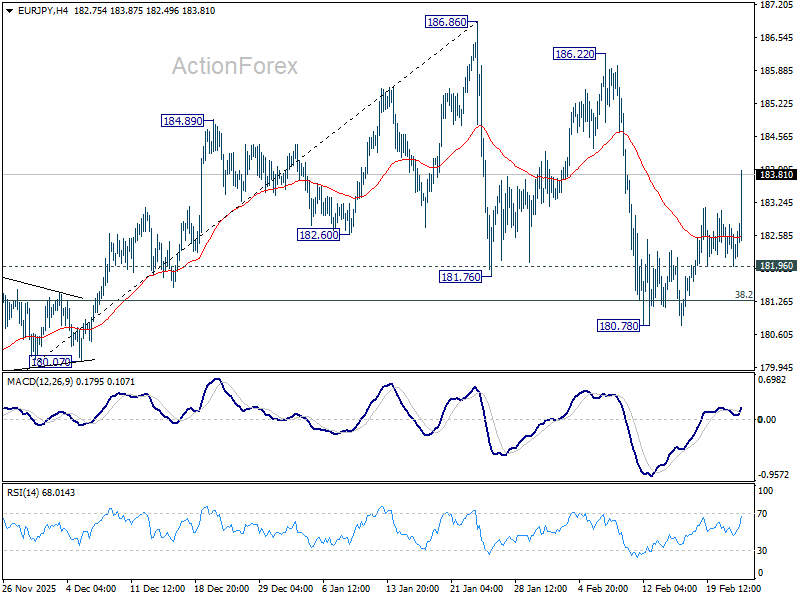

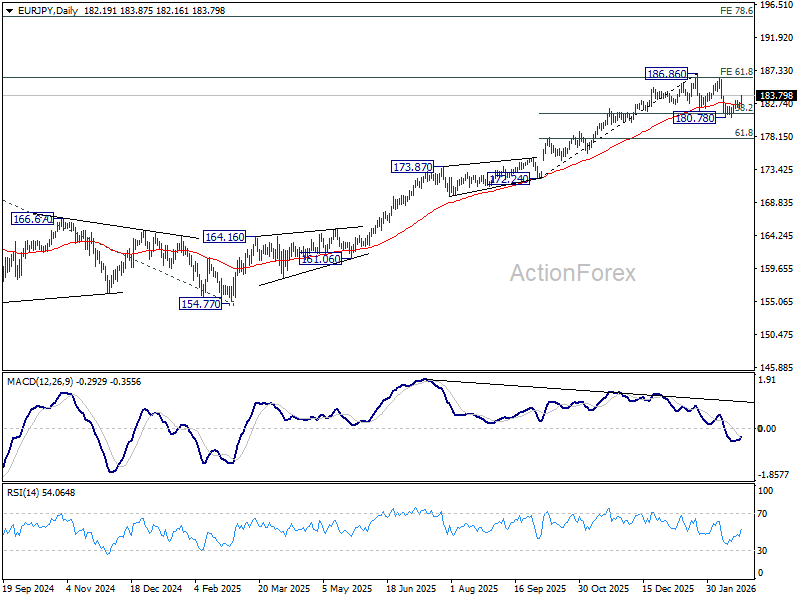

EUR/JPY Daily Outlook

Daily Pivots: (S1) 181.91; (P) 182.36; (R1) 182.73; More...

EUR/JPY's rebound from 180.78 accelerates higher today and intraday bias remains on the upside. Current development solidifies the case that fall from 187.86 has completed as a correction, after hitting 38.2% retracement of 172.24 to 186.86 at 181.27. Further rally should be seen to retest 186.22/86 resistance zone. On the downside, below 181.96 minor support will turn intraday bias neutral again.

In the bigger picture, current development suggests that price actions from 186.86 are merely a near term corrective pattern. In other words, the long term up trend is still in progress. Firm break of 186.86 will pave the way to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88 next. This will now remain the favored case as long as 180.78 support holds.

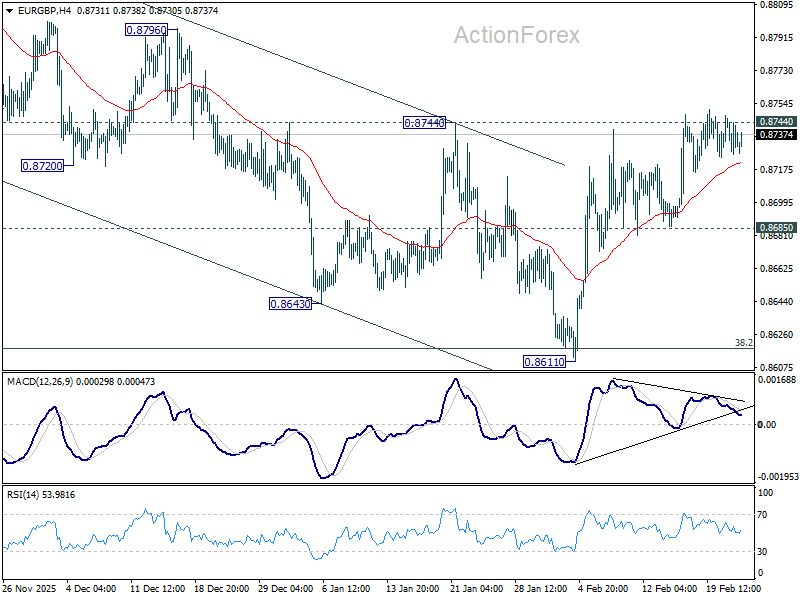

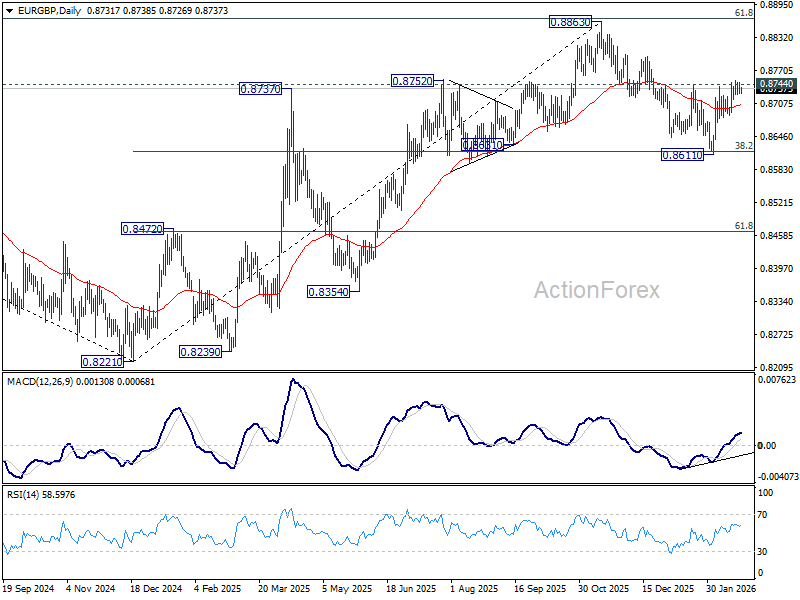

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8725; (P) 0.8738; (R1) 0.8747; More…

No change in EUR/GBP's outlook. Intraday bias stays neutral with focus on 0.8744 resistance. Decisive break there should confirm that fall from 0.8863 has completed as a correction at 0.8661. Further rise should then be seen back to retest 0.8663 high. On the downside, break of 0.8685 support will turn bias back to the downside for 0.8611. Sustained break of 38.2% retracement of 0.8221 to 0.8663 at 0.8618 will carry larger bearish implications and turn outlook bearish.

In the bigger picture, rise from 0.8221 medium term bottom (2024 low) is seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Sustained trading below 55 W EMA (now at 0.8636) should confirm that this corrective bounce has completed. In this case, deeper fall would be seen back to 0.8201/21 key support zone. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high). That should pave the way back to 0.9267.

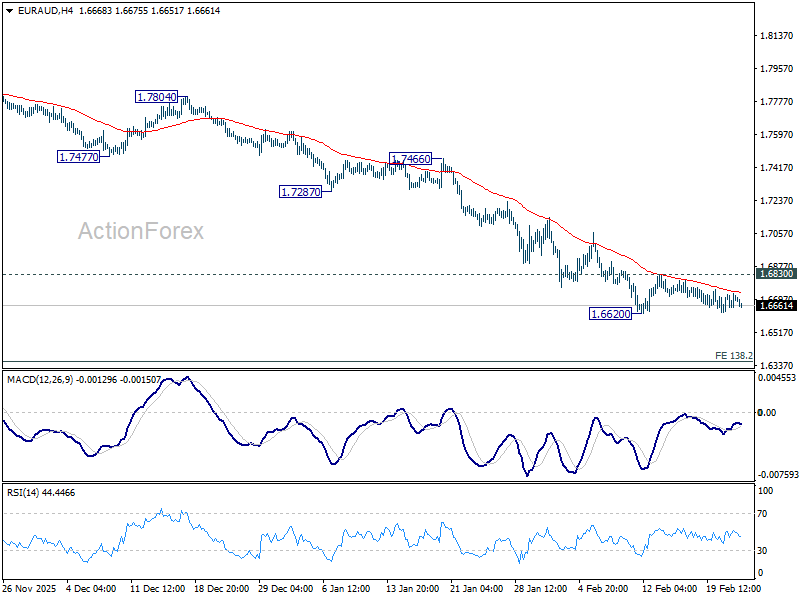

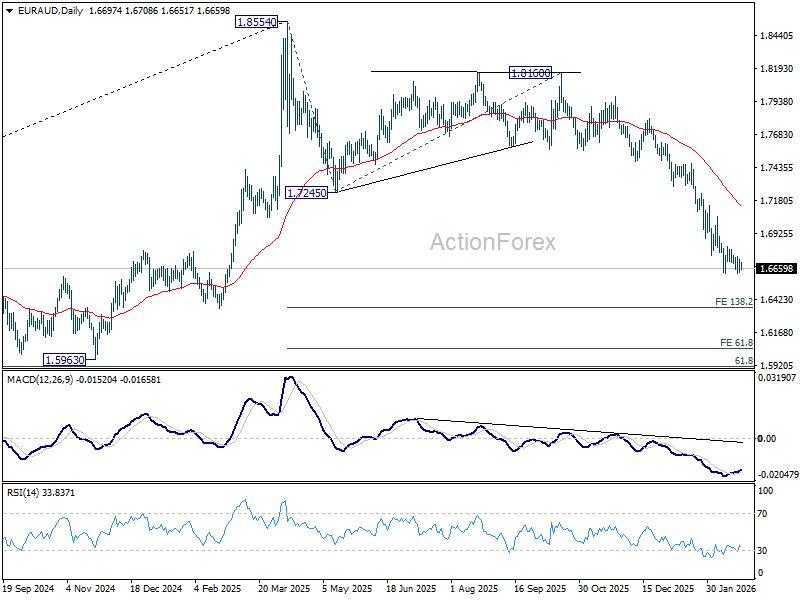

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6651; (P) 1.6691; (R1) 1.6743; More...

Intraday bias in EUR/AUD remains neutral as consolidations from 1.6620 is still in progress. Further decline is expected with 1.6830 resistance intact. On the downside, decisive break of 1.6620 will resume the larger decline from 1.8554 to 138.2% projection of 1.8554 to 1.7245 from 1.8160 at 1.6351 next. However, firm break of 1.6830 resistance will indicate short term bottoming, and bring stronger rebound.

In the bigger picture, fall from 1.8554 medium term top is seen as reversing the whole up trend from 1.4281 (2022 low). Deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. For now, risk will stay on the downside as long as 1.7245 support turned resistance holds, even in case of strong rebound.

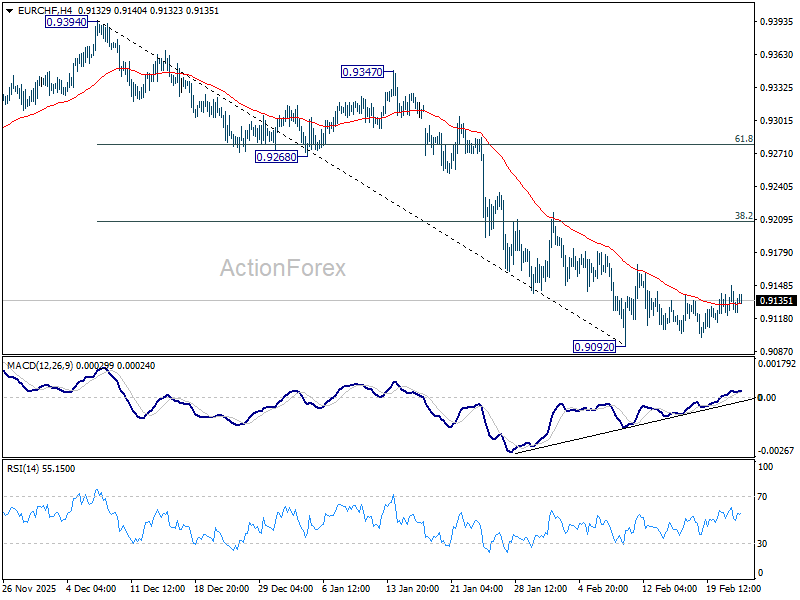

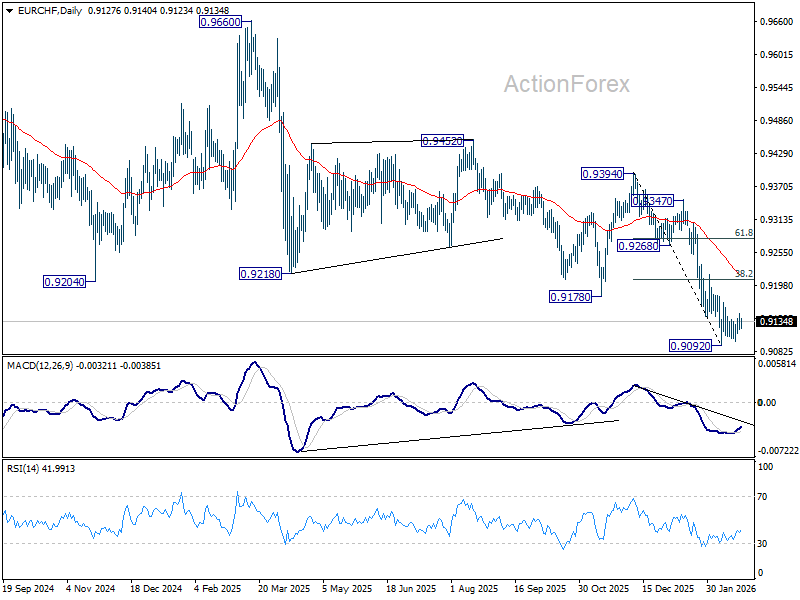

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9119; (P) 0.9134; (R1) 0.9147; More....

No change in EUR/CHF's outlook as consolidations continue above 0.9092. Stronger rebound might be seen but upside should be limited by 38.2% retracement of 0.9394 to 0.9092 at 0.9207. On the downside, firm break of 0.9092 will resume larger down trend.

In the bigger picture, down trend from 0.9928 (2024 high) is still in progress with falling 55 W EMA (now at 0.9326) intact. Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Outlook will stay bearish as long as 0.9394 resistance holds, in case of rebound.

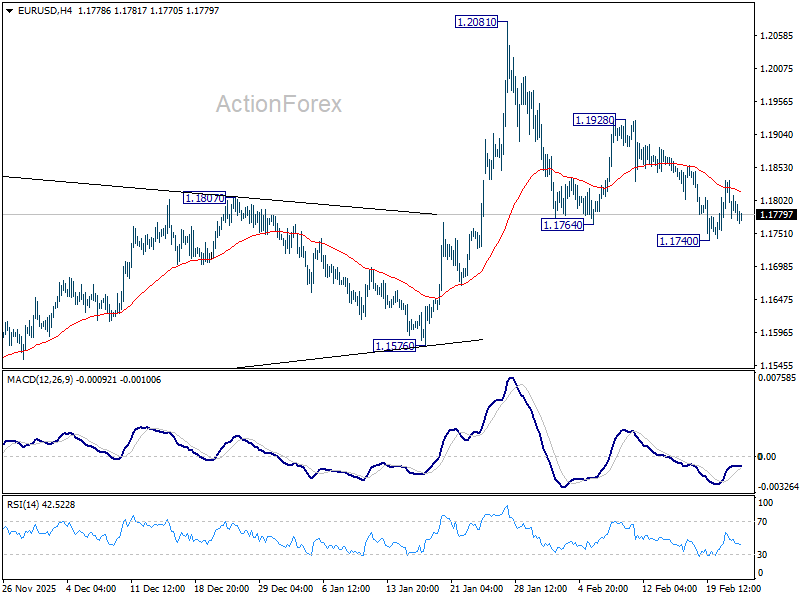

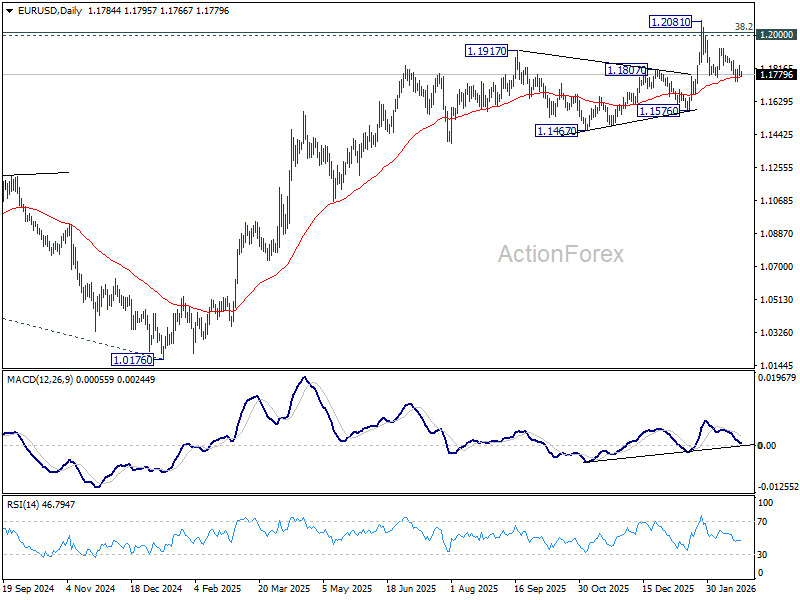

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1762; (P) 1.1798; (R1) 1.1822; More….

Intraday bias in EUR/USD remains neutral for the moment. Near term risk will remain on the downside as long as 1.1928 resistance holds. Below 1.1740 temporary low will target 1.1576 support next. Firm break there should confirm rejection by 1.2 key psychological level and turn near term outlook bearish.

In the bigger picture, as long as 55 W EMA (now at 1.1494) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.2581. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

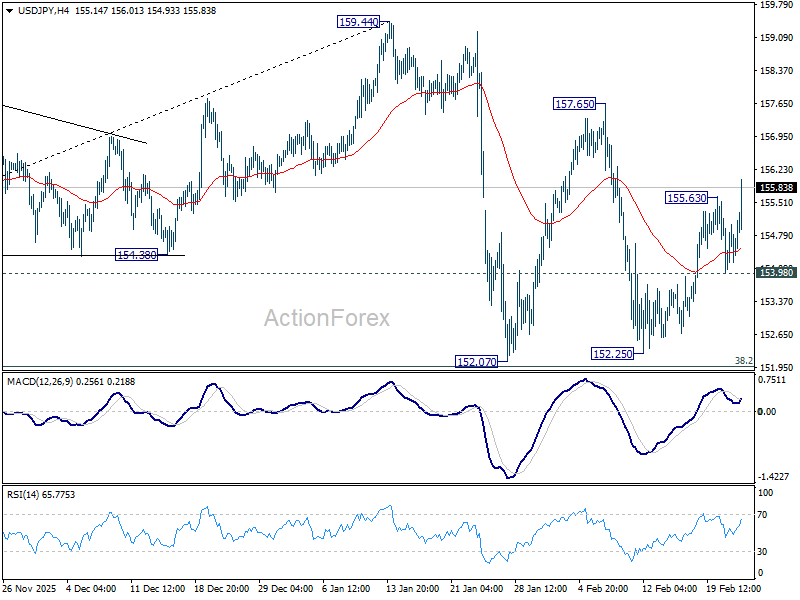

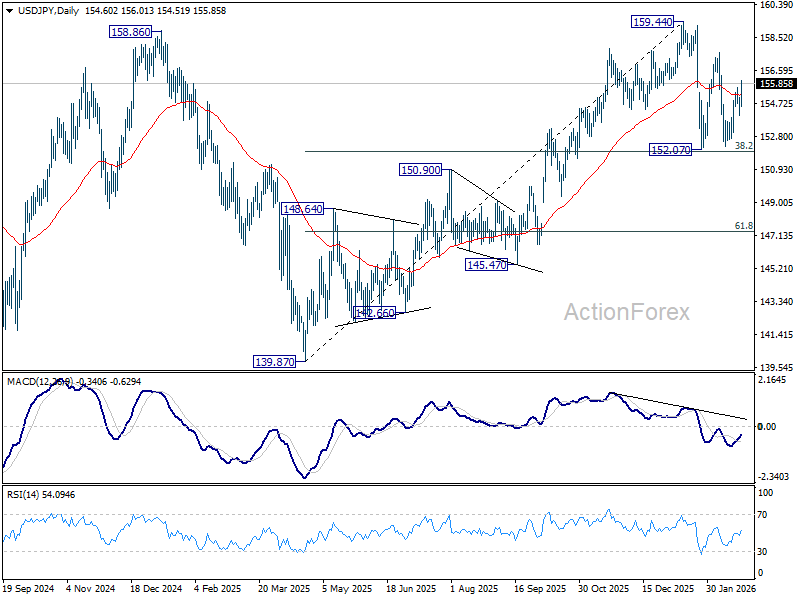

USD/JPY Daily Outlook

Daily Pivots: (S1) 154.10; (P) 154.57; (R1) 155.14; More...

USD/JPY's rise from 152.25 resumed by breaking through 155.63 and intraday bias is back on the upside for 157.65 resistance first. Firm break there will target a retest on 159.44 high. On the downside, below 153.98 minor support will turn intraday bias neutral again first. Overall, with 38.2% retracement of 139.87 to 159.44 at 151.96 intact, price actions from 159.44 are seen as a corrective pattern. Also, rise from 139.87 is expected to resume through 159.44 at a later stage.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 151.93) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

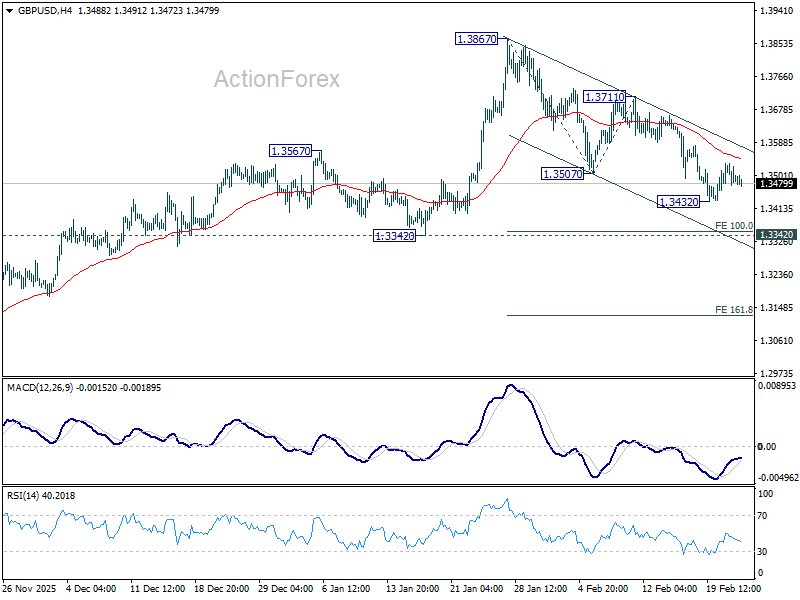

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3468; (P) 1.3501; (R1) 1.3527; More...

Intraday bias in GBP/USD stays neutral at this point. For now, fall from 1.3867 is seen as correcting the whole rise from 1.2099. Risk will stay on the downside as long as 1.3711 resistance holds. Below 1.3432 will target 1.3342 support first. Firm break there will solidify this case, and target 161.8% projection of 1.3867 to 1.3507 from 1.3711 at 1.3129.

In the bigger picture, as long as 1.3008 support holds, rise from 1.3051 (2022 low) should still be in progress for 1.4284 key resistance (2021 high). Decisive break there will add to the case of long term bullish trend reversal. However, firm break of 1.3008 will raise the chance of medium term bearish reversal and target 1.2099 support next.

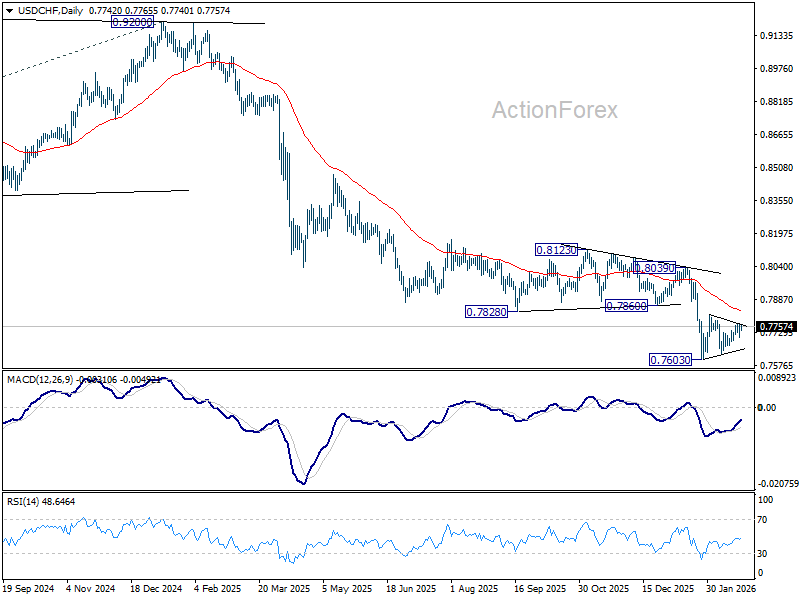

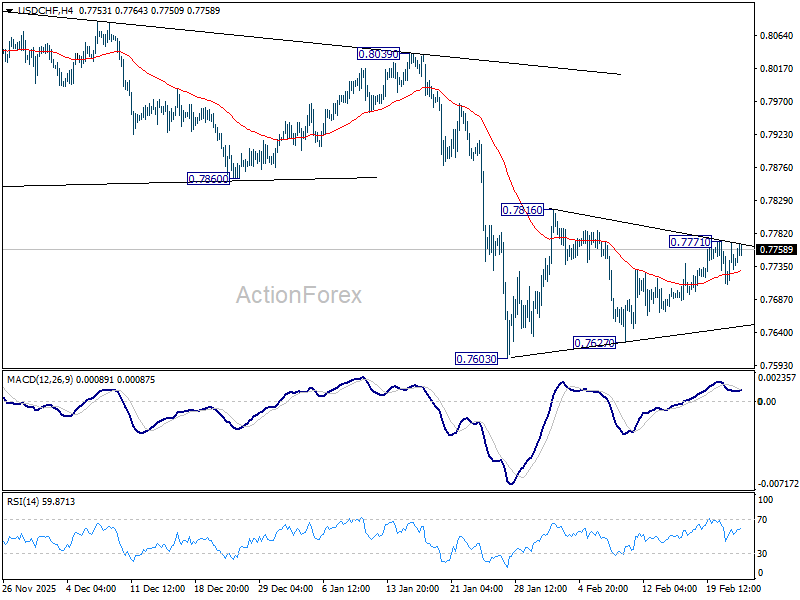

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7717; (P) 0.7742; (R1) 0.7775; More….

Intraday bias in USD/CHF stays neutral for the moment and consolidation pattern from 0.7603 is still in progress. In case of stronger rise, upside upside should be limited by 55 D EMA (now at 0.7832) to complete the pattern. On the downside, below 0.7627 will bring retest of 0.7603. Firm break there will resume larger down trend, and target 0.7382 projection level next. However, sustained break of 55 D EMA will indicate that a larger scale corrective bounce in underway and target 0.8039 resistance next.

In the bigger picture, down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8123 resistance holds.