Sample Category Title

Elliott Wave View on EURJPY Highlights 5 Swings Since Feb 13, Suggesting Upside Potential

From the January 23 high, EURJPY completed a measured three‑swing pullback that reached 180.78. This decline has been identified as wave (4) within the broader Elliott Wave structure. Following the completion of this corrective phase, the pair turned higher in wave (5). However, to fully confirm the bullish continuation and eliminate the possibility of a double correction, price must break decisively above the January 23 peak at 186.87. Until that level is surpassed, traders should remain aware of potential alternative scenarios.

From the wave (4) low, the rally has unfolded in a clear five‑swing sequence, which favors further upside. Wave ((i)) advanced to 182.27, followed by a corrective pullback in wave ((ii)) that ended at 180.8. The pair then nested higher within wave ((iii)). Inside this structure, wave (i) concluded at 183.15, while wave (ii) dipped modestly to 182. The subsequent rally carried wave (iii) to 184.18, before a minor retracement in wave (iv) ended at 183.3.

Near term, the expectation is for EURJPY to continue higher in wave (v), which will complete wave ((iii)). As long as the pivot at 180.78 remains intact, pullbacks should find support in the typical three, seven, or eleven‑swing corrective sequences. This technical condition reinforces the bullish bias and suggests that the pair retains potential for further appreciation.

EURJPY 1-Hour Elliott Wave Chart From 2.25.2026

EURJPY Elliott Wave Video:

https://www.youtube.com/watch?v=SFKEkTQ_-bg

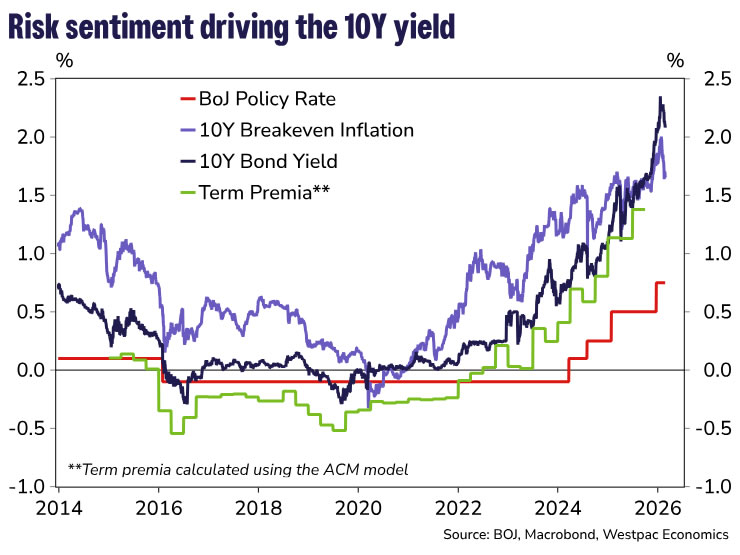

No Need to Fear the Yield in Japan

Fiscal anxiety has pushed yields far but fundamentals still point to a 2.0% yield for the 10Y bond in Japan.

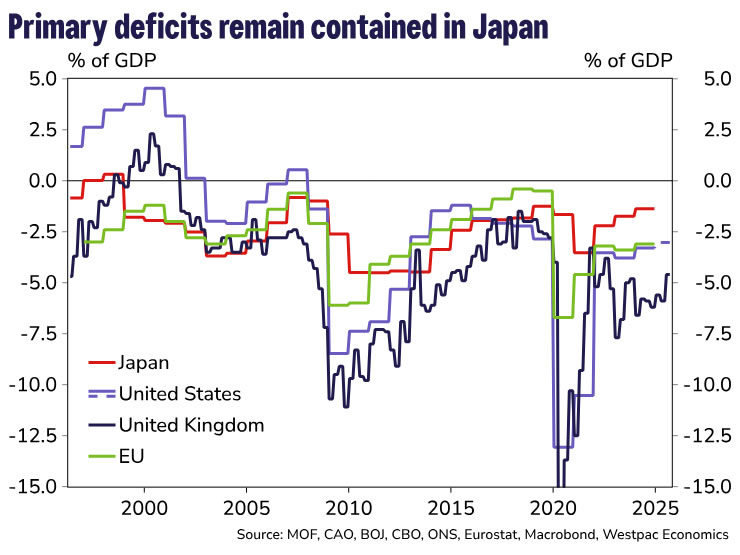

There has been a lot of concern around Japan’s bond market, centred around the impact of Prime Minister Sanae Takaichi’s fiscal package. These concerns overlook some of the fundamental shifts in the Japanese economy that will allow the government to sustain greater spending.

To start, it is worth putting the JPY17.1tril package (~10% of GDP) into context. Japan’s primary deficit as a percentage of its GDP of 1.4% is far lower than that of its peers like the US of around 3%. Japan has also made more progress reducing its debt-to-GDP ratio since the pandemic than other major economies and in contrast to the US where, despite a strongly growing economy, this ratio has increased. Compared to its peers, Japan has managed its fiscal position well. With inflation sustaining a 2.0%+ pace, nominal debt will also now be deflated for the first time in decades.

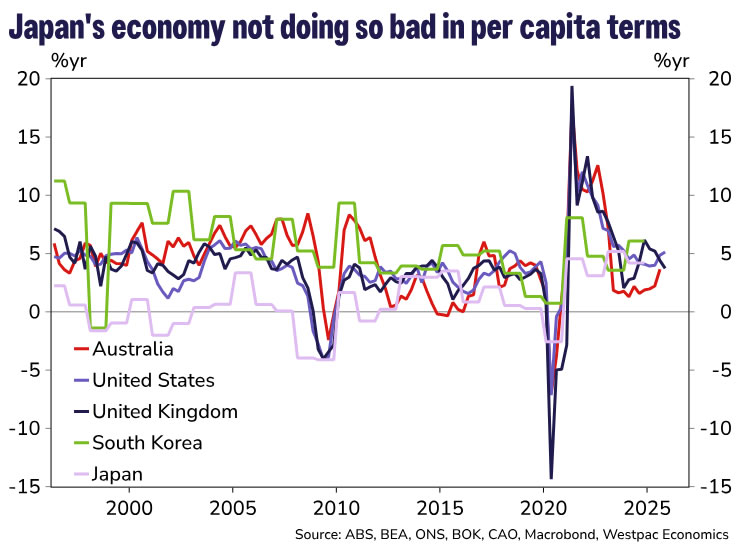

Some may point to Japan’s 1.0% real GDP growth as evidence that it cannot grow out of debt, but this overlooks the drag from a declining population. Adjusting for demographics, per‑capita GDP grew by 4.2% in 2024, broadly in line with the US, UK, South Korea and Australia. With government spending largely tied to population growth rather than headline GDP, modest aggregate growth need not imply deteriorating fiscal dynamics. While population ageing will place upward pressure on social spending, this is likely to be partly offset by arising participation.

Crucially, debt dynamics also benefit from low interest costs. Interest payments remain around 1.0% of GDP, while nominal GDP growth – what matters for debt sustainability – has averaged around 4.0% over the past two years. In this environment, debt‑to‑GDP can stabilise even with modest fiscal deficits, provided per‑capita growth remains robust.

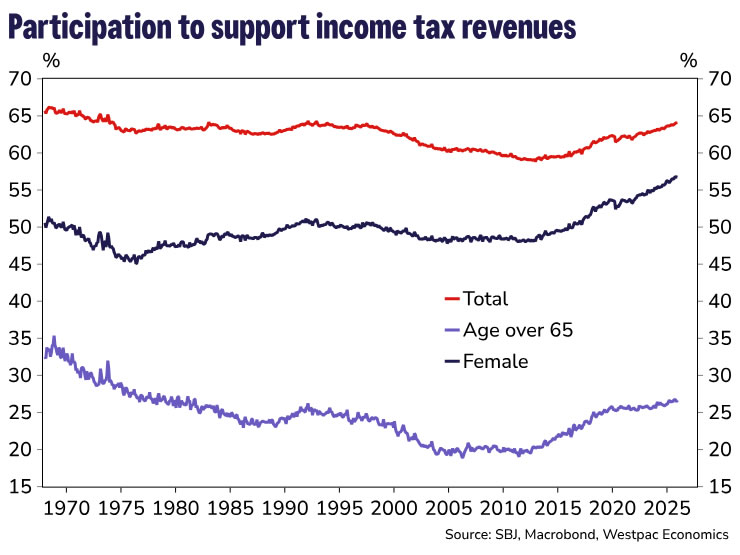

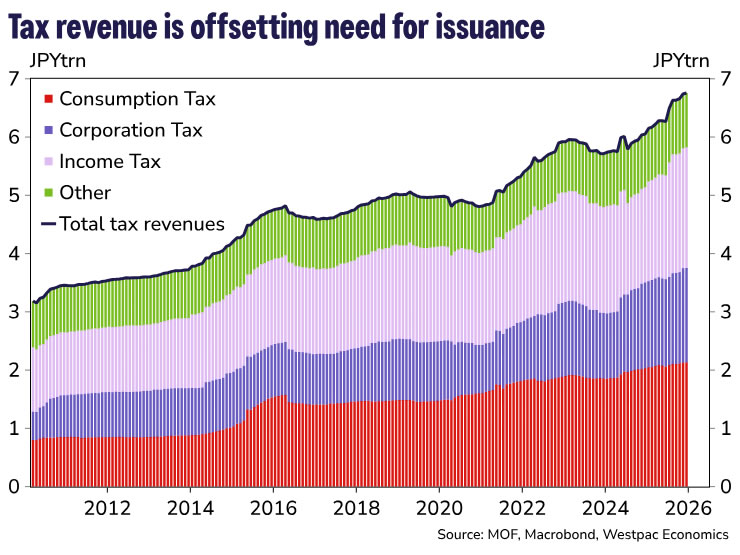

There is also upside for revenue going forward. The labour market is tight as ever, with labour force participation hitting 64.1%, the highest since December 1992, supported by an increase in participation of women and seniors—female labour force participation is at a record high of 56.7%. As we have previously discussed, this trend is unlikely dissipate with Japan’s population continuing to age and shrink. A larger labour force alongside greater nominal wage increases should help support income tax revenues.

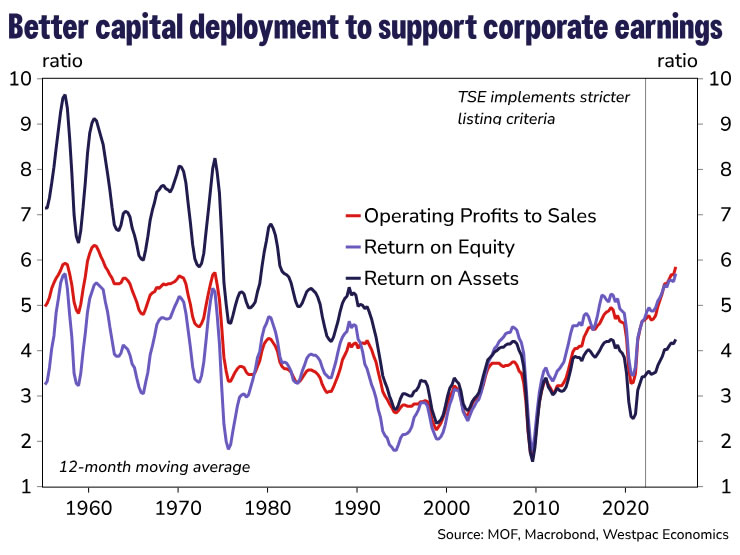

Also assisting revenue growth, will be the impact corporate governance reforms have had on profitability. Over the last three years, the Tokyo Stock Exchange requirements have forced firms to unwind their cross-shareholdings and improve capital efficiency which has seen the return on equity climb to an average of 5.5 in the year to September 2025, compared to an average of 3.4 over 1990–2019 and 4.0 over 1960–90. Combined with a shift in price-setting behaviour and strong export earnings, corporate profits have reached levels unseen since before the Lost Decades. The benefits of these corporate reforms are likely to support profitability and hence corporate tax revenue going ahead.

While external risks are significant, particularly China’s competitive position in autos and semiconductor manufacturing, these reforms will also help enhance adaptability. Firms are now allocating capital to research and development versus maintaining inefficient conglomerates.

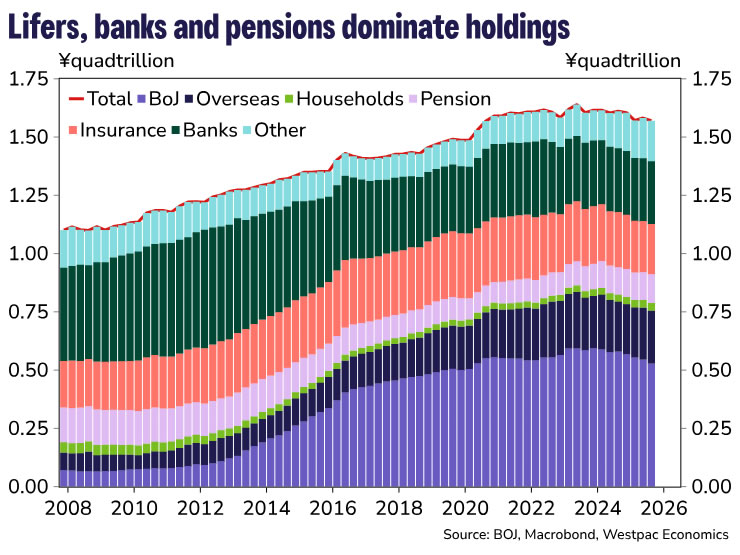

Alongside serviceability concerns, investors have expressed concerns around excess supply of Japanese Government Bonds (JGBs) as the Bank of Japan slows its purchases of bonds. However, these concerns are overstated. For one, the BoJ has been vocal about reducing its holdings in a way that “avoid[s] inducing destabilizing effects on the financial markets”. This isn’t just rhetoric. The BoJ tapered its pace of purchases in July 2025 from JPY400bn to JPY200bn and have, on numerous occasions, affirmed that “In the case of a rapid rise in long-term interest rates, it will make nimble responses by, for example, increasing the amount of JGB purchases…”. Note as well, their current purchase pace is not insignificant at around JPYs2.9tril a month (which annualises to around JPY36tril a year) against the Ministry of Finance’s (MoF) planned JPY190tril of issuance through FY2025 (ending in March 2026). The MoF also has flexibility on the duration of issuance, offering another way to contain market volatility and an unwanted tightening of financial conditions.

Interest cost concerns also miss the mark for another reason. Interest costs as a share of GDP remain low in Japan compared to peers and, given the BoJ owns around half of outstanding JGBs, almost half of the Government’s initial interest outlay flows back to the government, making them fiscally neutral. The pace of the BoJ’s balance sheet normalisation will be gradual and only as market conditions warrant, and so this interest cost offset is set to remain in place for the foreseeable future.

The portion of the bond market not held by the BoJ is mostly held by domestic investors, with foreign ownership sitting at 14%, compared to 23% in the US and 31% in the UK. This insulates against risks of foreign capital flight in times of uncertainty making comparisons between Takaichi and Truss unjust. Domestic players tend to hold JGBs to match liabilities, particularly important for Japan’s large life insurance sector, and regulatory requirements. The MoF has proven nimble in its flexibility to match issuance tenors to demand to accommodate preferences. In the near term, our Strategy team continues to expect that Japan is unlikely to export as much capital to offshore bonds and will continue to purchase JGBs. Further information on this will come in April as the investment intentions of Japan's mega life insurers are made public.

Given these factors, we anticipate the premium markets are pricing into JGBs will fade with time returning the 10-year government bond yield to 2.0%, roughly 100bps above the terminal policy rate. This is still at the high end of global cash to 10-year curve spreads, but not deleteriously so. We see this adjustment unfolding over the next year, as markets continue to focus on supply dynamics and political noise even as Japan’s underlying fiscal and macro fundamentals remain supportive.

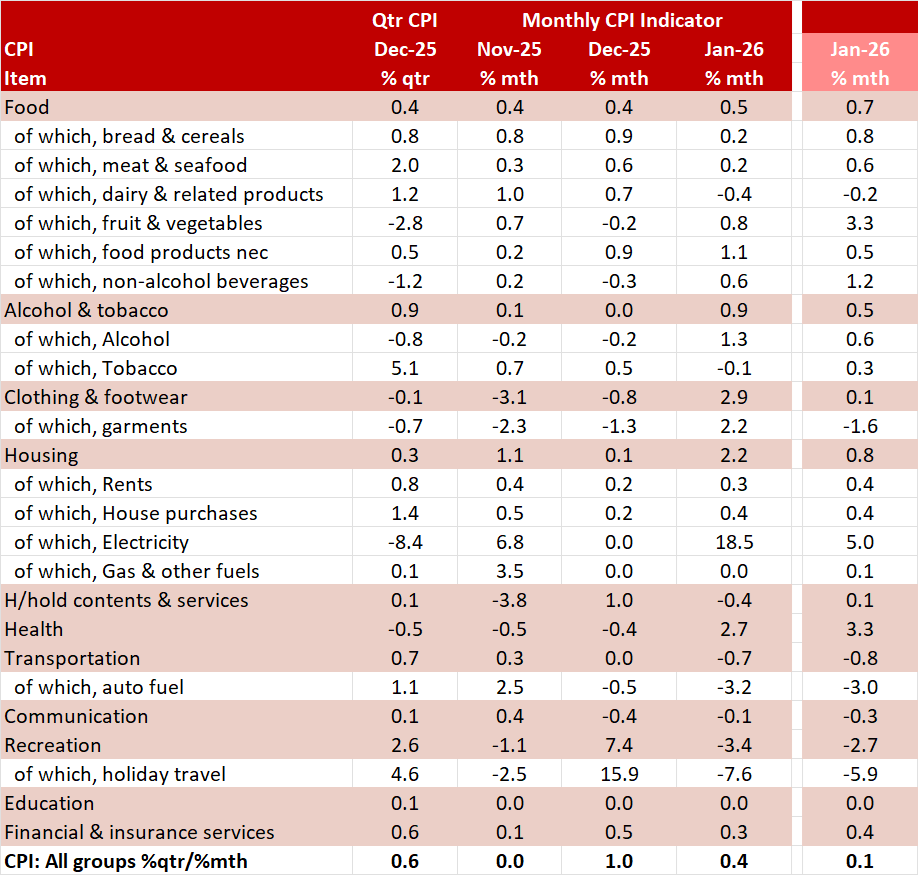

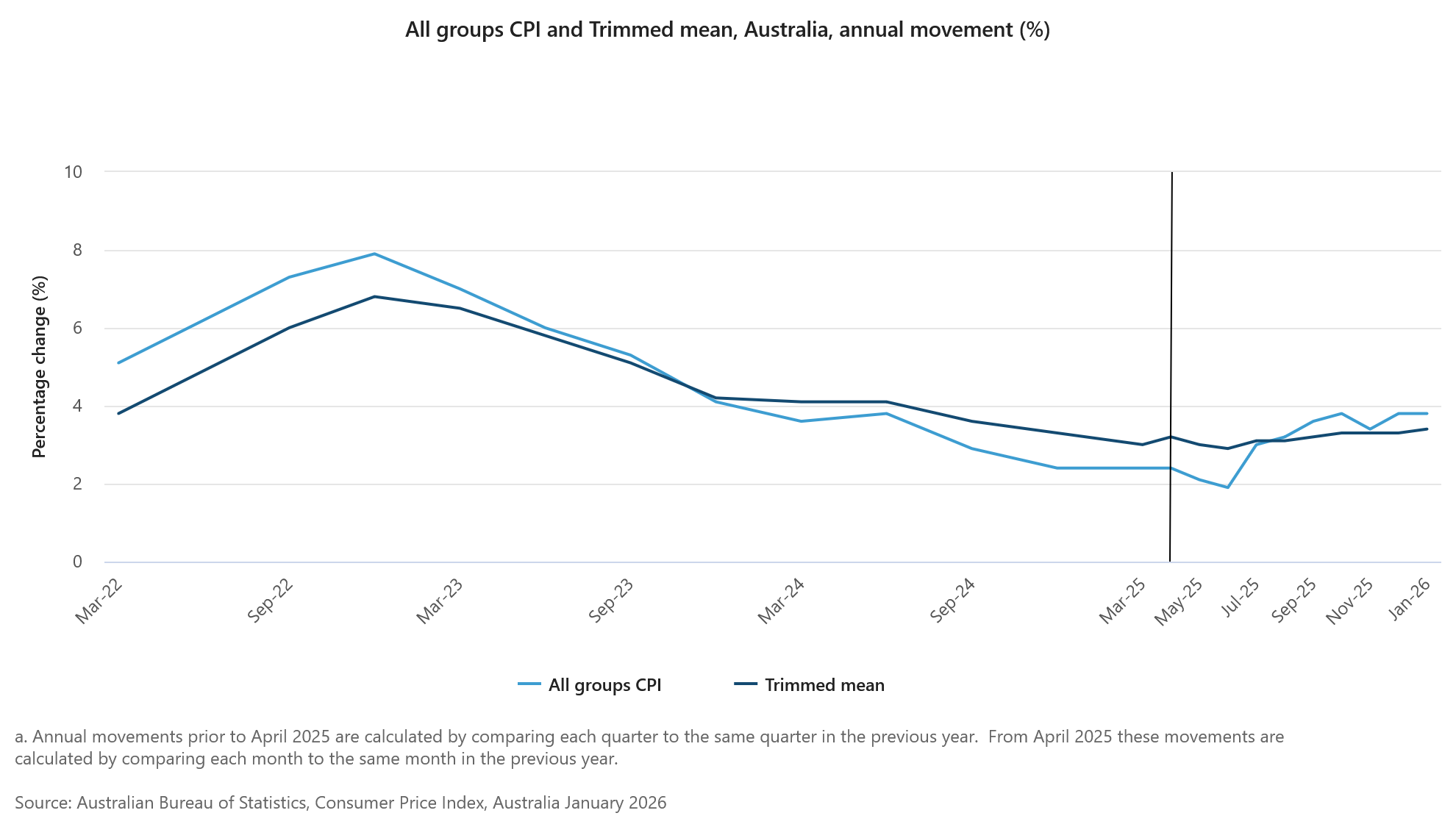

Australia: January CPI – Sparks and Sneakers Behind the Lift

A touch stronger than expected, with minimal risk to our March quarter estimates.

- Electricity and garments & footwear boosted the January CPI more than expected.

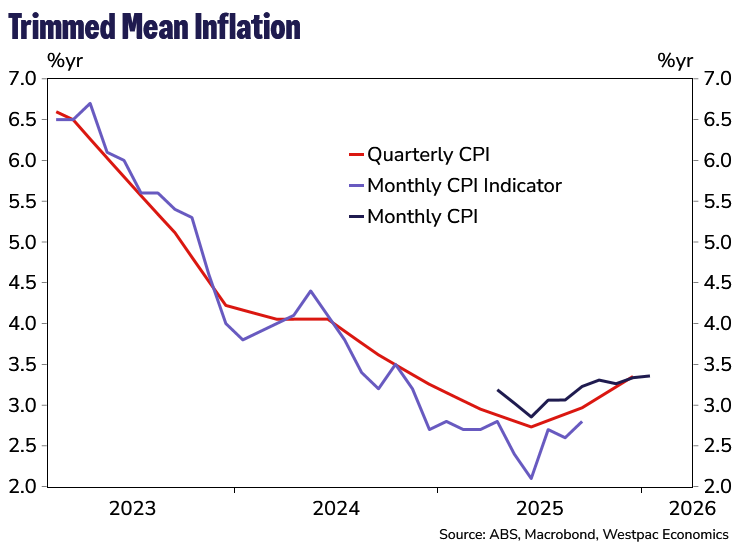

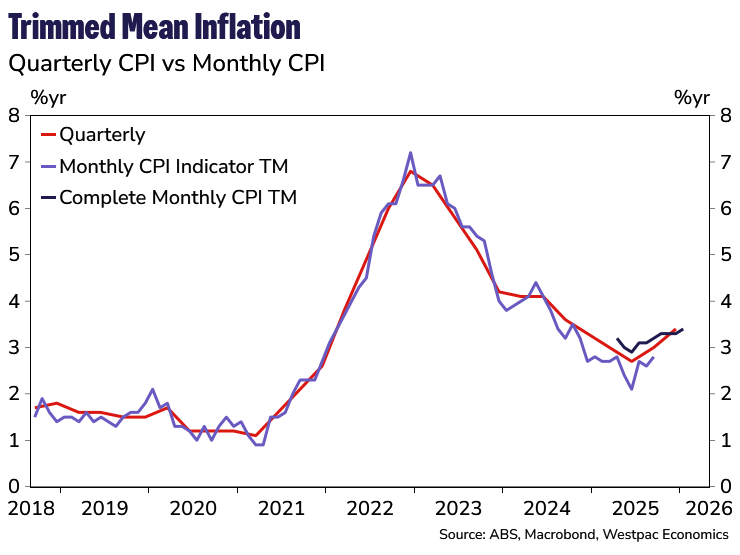

- In the month the Trimmed Mean was as expected with revision resulting in a modest uptick in the annual pace to 3.4%yr.

- Our preliminary review of the January Monthly CPI suggests little risk current inflation profile.

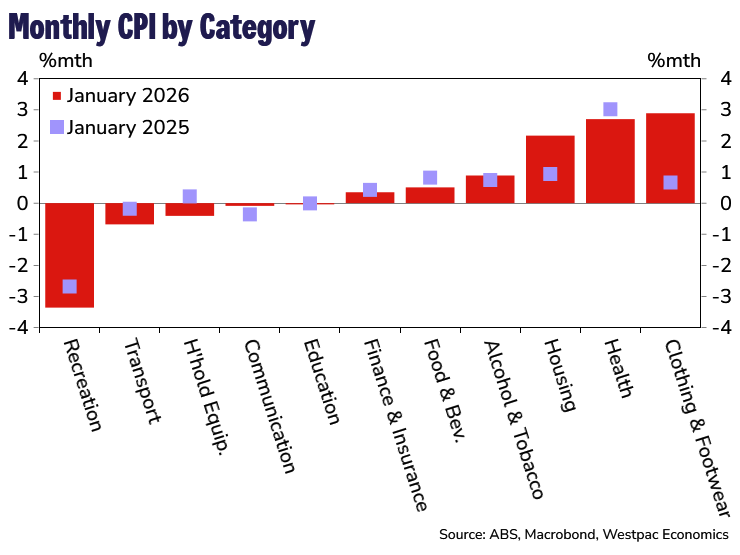

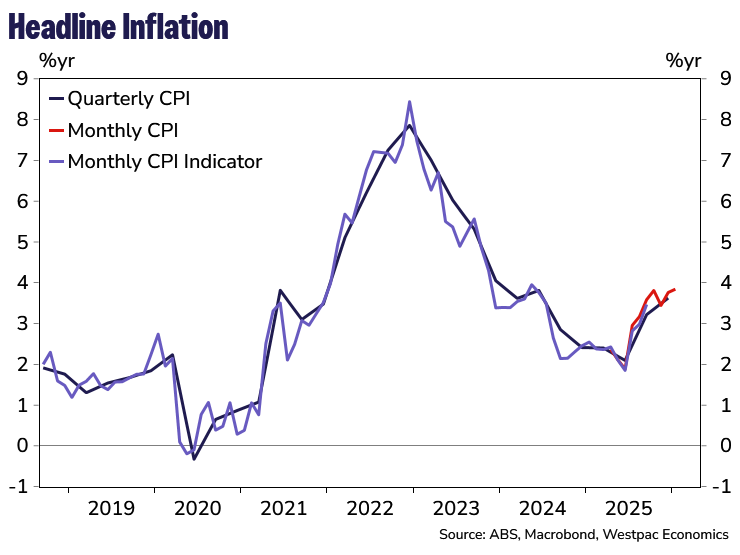

We start 2026 with a complete Monthly CPI. In January the CPI gained 3.8% in the year, a touch stronger than Westpac’s estimate of 3.6%yr and the market estimate of 3.7%yr. In the month, the CPI lifted 0.4%, stronger than Westpac’s published near-cast of 0.1% on the back of stronger than expect gains in electricity and garments & footwear offset somewhat by a larger than expected fall in holiday travel and a smaller than expected rise in health.

January is seasonally a soft month with the seasonally adjusted CPI lifting 0.5% in January. Due to the short history of the new monthly expenditure class series, we expect to see ongoing revisions to the CPI seasonal factors with the ABS fine tuning the process as they gather more data. In the December release the ABS estimated a seasonal impact of 0.3% in January, this was reported as 0.1% in the January release. Remembering that the Trimmed Mean is seasonally adjusted, this suggests we should expect to see revisions to the Trimmed Mean until the seasonal adjustment process is more mature.

The Monthly Trimmed Mean (TM) measure was up 3.4% in the year to January, Westpac and the market had estimated 3.3%yr, which is up a touch from 3.3%yr in December.

The TM lifted 0.3% in the month of January, on par with Westpac’s estimate of 0.3% with the higher than expected annual pace due to revisions. The monthly TM has printed 0.3%mth in five of the last six months. This month expenditure classes trimmed off the top included electricity, insurance, garments, child care, veterinary services and take away & fast foods. Trimmed off the lower bound in January included automotive fuel, vegetables and other non-durables.

As Michael Plumb, Head of Economic Analysis Department at the RBA noted in a speech this week, the RBA is using the expanded monthly data to evaluate and compare underlying inflation measures and is examining bias, seasonality, responsiveness and leading properties with a view of eventually moving to a monthly measure of core inflation. But it will take time to understand the properties and seasonal patterns of the data. As such the Bank will continue to focus on the quarterly CPI for forecasting and assessing underlying inflationary pressures.

Consistent with out preliminary review we see little risk to our current inflation profile. Our current estimate for the March quarter TM is 0.9%qtr, lifting the annual pace very slightly to 3.5%yr from 3.4%yr. Our March quarter CPI estimate is 1.1%qtr with the annual pace lifting from 3.6%yr to 3.8%yr as the energy rebates roll off boosting electricity prices in the CPI.

January Monthly CPI Indicator in more detail

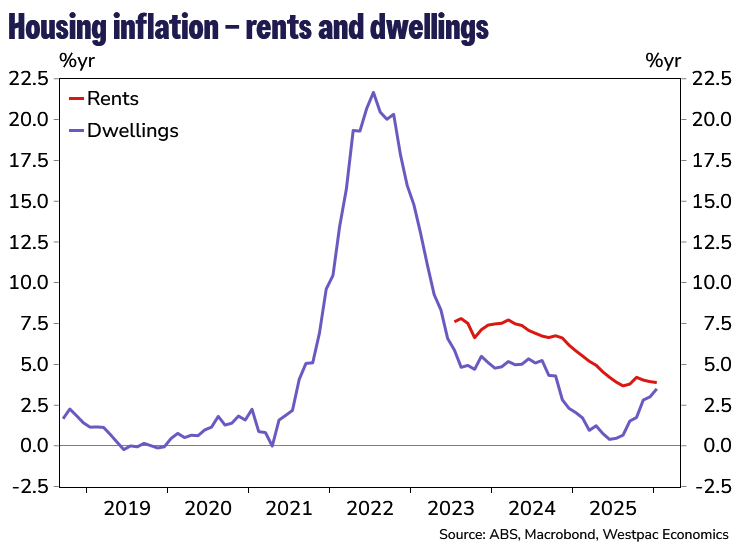

Rents were a touch softer than expected lifting 0.3% vs. Westpac’s 0.4% estimate. We are closely watching rents to see if this modest trend continues as expected. Dwellings gained 0.4% in the month, on par with our expectations as we note a strengthening trend which is likely to continue through the first quarter of 2026. The ABS notes that project home builders in some cities have raised base prices in response to increased demand and to pass through higher labour and material costs.

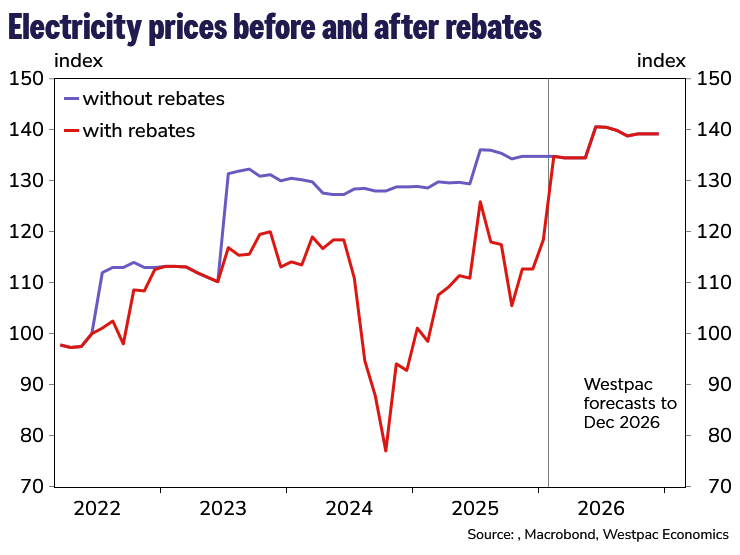

Electricity gained 18.5% in January compared to our forecast for 5.0% with the rise this month driven by households using up the extended EBRF rebates. This has seen the gap between electricity prices reported in the CPI, and the prices before rebates, almost close as it is now just 0.9%. We would expect this gap to close in February and without any new rebates, electricity prices will return to more normal pricing arrangements.

Holiday travel & accommodation fell –7.6% in January, a bit more than our estimate of –5.9% due to a –16.3% decline in international travel being only partially offset by a small 1.3% increase in domestic travel.

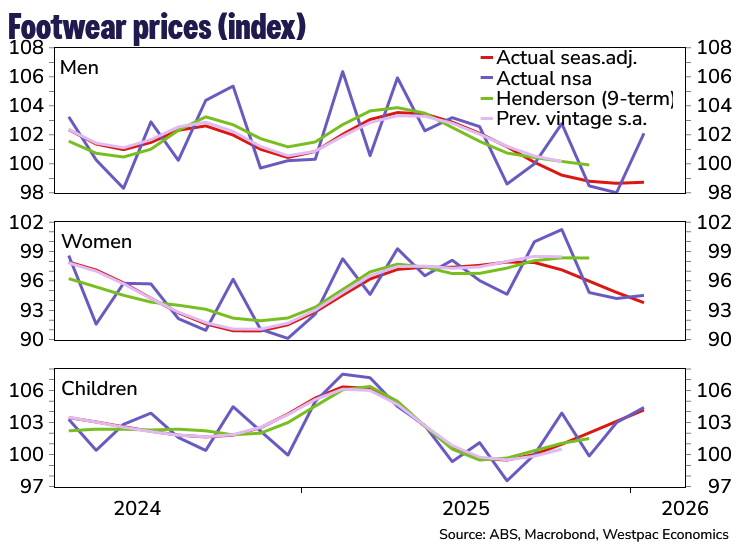

A key upside surprise was in clothing & footwear which gained 2.9% in the month compared to our estimate of 0.1%. Most of this discrepancy was due to garments which lifted 2.2% vs. Westpac’s expectation for a seasonal –1.6% decline. Also of note was a robust 4.2% increase in footwear for men and a 5.7% gain in accessories.

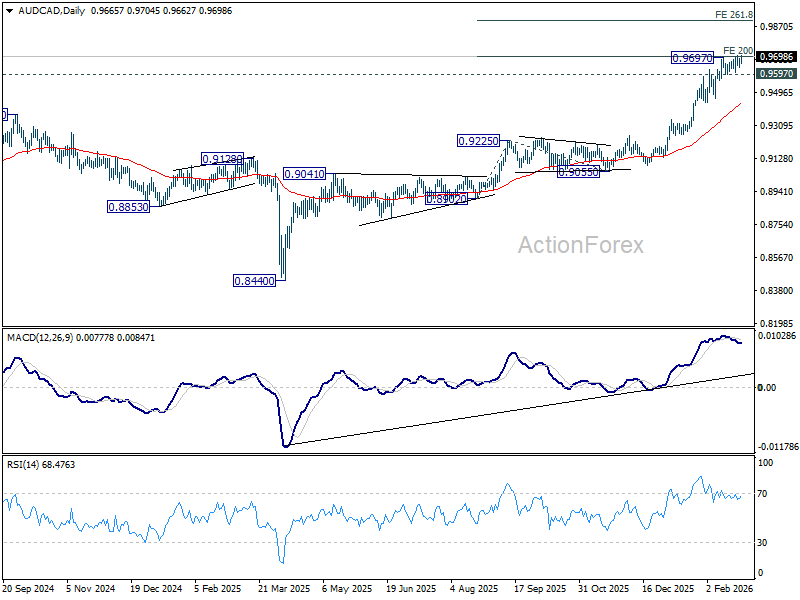

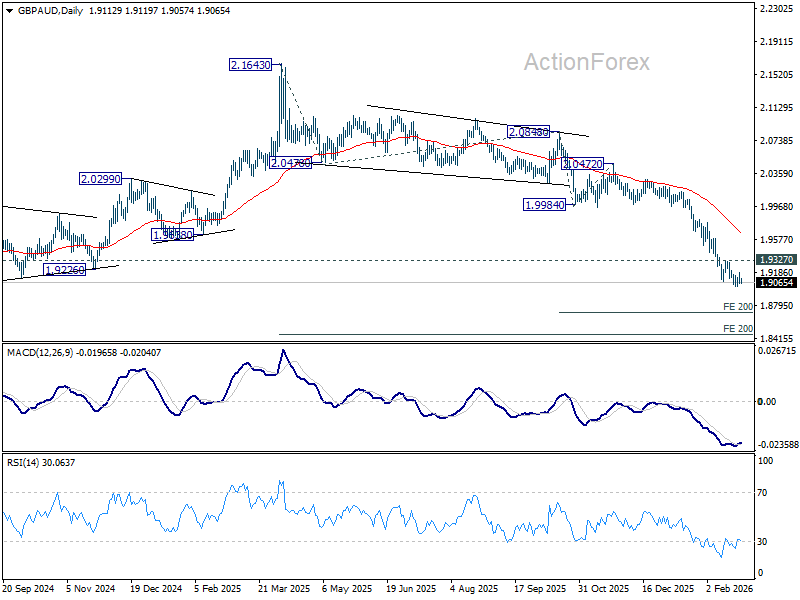

CPI supports AUD, but breakout pending; AUD/CAD bullish, GBP/AUD bearish

Australian Dollar strengthened following January’s stronger-than-expected CPI data, but the move has resembled a "steady climb" rather than a "breakout surge". While markets interpreted the firm headline and core readings as reinforcing the hawkish stance of the RBA, positioning remains measured.

One reason is that a May rate hike is already largely priced in. After the RBA’s hawkish increase earlier this month, traders had moved quickly to factor in another step. The latest CPI print confirms that narrative but does not materially extend it. For further upside momentum, markets would likely need to price tightening beyond May. That, however, may depend more heavily on the comprehensive Q1 quarterly inflation report due April, rather than the monthly indicator.

As RBA economic analysis chief Michael Plumb noted yesteday, it will take time to understand the properties and seasonal patterns of the new monthly data. For now, policymakers continue to place greater weight on quarterly measures, limiting the immediate impact of monthly fluctuations.

Global uncertainty also tempers enthusiasm. Ongoing trade tensions, fresh US tariff measures, and persistent US–Iran geopolitical risks act as a natural ceiling for risk-sensitive currencies like the Aussie.

Still, the broader tone for Aussie remains bullish. With inflation holding above target and core measures edging higher, the policy bias is clearly toward further tightening, keeping AUD underpinned on dips.

Technically, AUD/CAD has returned to test 0.9697 resistance level with today's bounce. Decisive break would confirm resumption of the broader rally from the 0.8440 (2025 low) and open the way toward 261.8% projection of 0.8902 to 0.9225 from 0.9055 at 0.9901.

However, failure to clear that resistance cleanly could invite consolidation. Break below 0.9597 support would would bring deeper correction to 55 D EMA (now at 0.9439) first.

While GBP/AUD shows waning downside momentum as daily MACD divergence emerges, there is no clear sign of bottomg yet. The downtrend from 2.1643 (2025 high) high remains intact, with next target at 200% projection of 2.0848 to 1.9984 from 2.0472 at 1.8744.

However, firm break of 1.9327 resistance will indicate short term bottoming, and bring stronger rebound towards 55 D EMA (now at 1.9674).

Australia trimmed mean CPI climbs to 3.4%, RBA hike seen inevitable

Australia’s monthly CPI for January came in hotter than expected, reinforcing expectations of further tightening from the RBA. Headline inflation held unchanged at 3.8% yoy, above the 3.7% consensus and marking the joint highest reading since mid-2024.

More concerning for policymakers, trimmed mean CPI rose from 3.3% yoy to 3.4%, also exceeding forecasts and standing at its highest level since Q3 2024. Core inflation has now been at or above 3% since July 2025, remaining clearly outside the RBA’s 2–3% target band.

Housing (+6.8%), food and non-alcoholic beverages (+3.1%), recreation and culture (+3.7%), were the largest contributors to annual price pressures.

Markets had already leaned toward a May rate hike, and today’s data does little to challenge that view. Some economists argue the RBA may be “a little bit behind the curve,” risking a scenario where inflation becomes entrenched and requires more forceful tightening later. With price pressures proving persistent, another rate increase is increasingly viewed as close to inevitable.

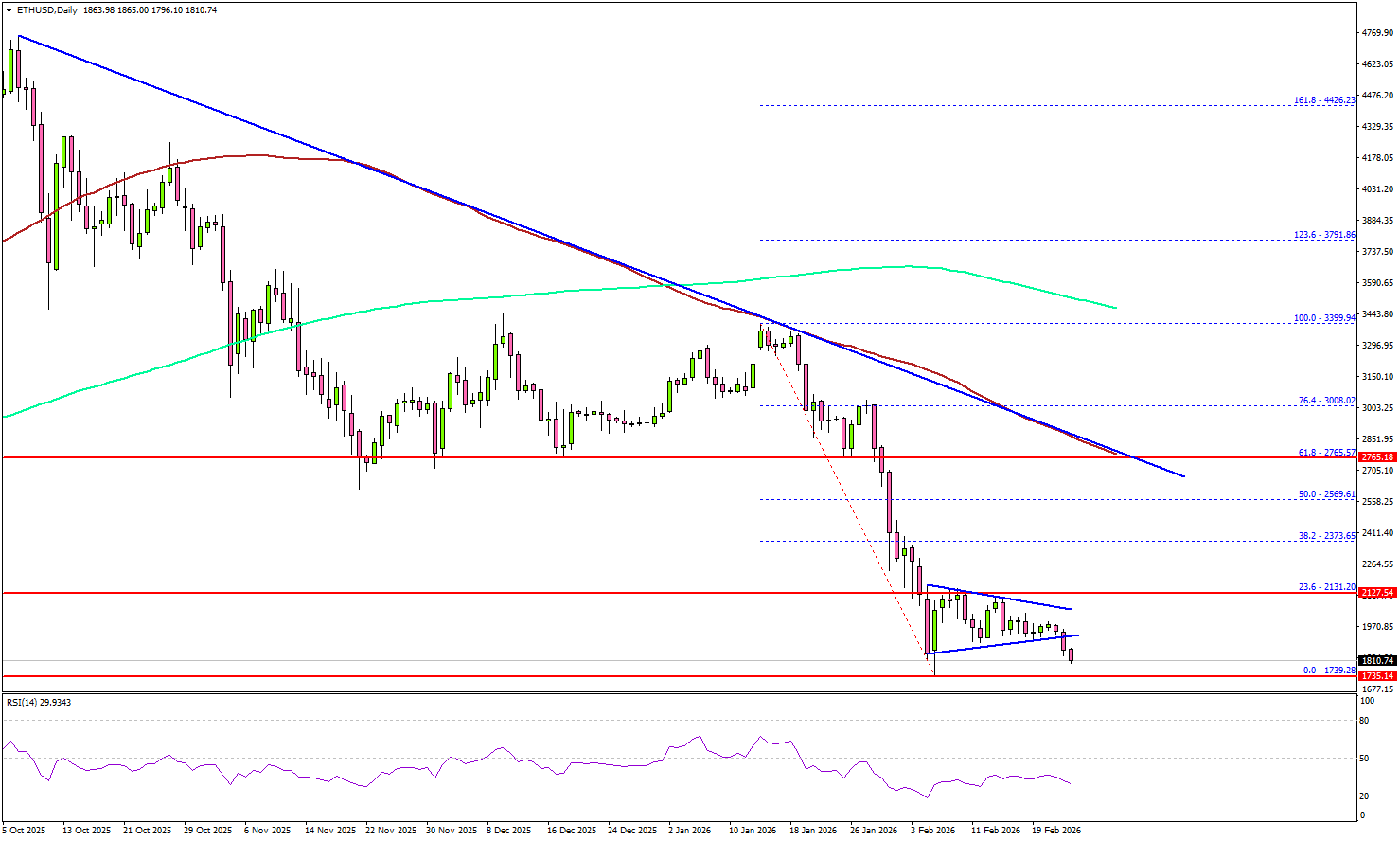

Ethereum Signals Bearish Risk, Downside Extension Now in Focus

Key Highlights

- Ethereum started a fresh decline after it faced rejection near $2,150.

- ETH could extend losses and revisit $1,750 or even $1,600.

- Bitcoin price gained bearish momentum after it broke the $65,500 support.

- XRP remained in the red zone and might dive to $1.20.

Ethereum Technical Analysis

Ethereum failed to stay above $2,000 and started a fresh decline. ETH traded below $1,950 and $1,920 to reenter a bearish zone.

Looking at the daily chart, the price failed to clear the 23.6% Fib retracement level of the downward move from the $3,400 swing high to the $1,739 low. It trimmed gains and traded below a bearish pattern with support at $1,920 on the daily chart.

On the downside, the bulls might be active near $1,750 and $1,740. The main support is now forming near $1,650, below which the price could slide toward $1,620. Any more losses might call for a move toward $1,500.

On the upside, the bears might remain active near $1,920. The first key resistance could be near the $2,150 level. The main hurdle for the bulls sits near $2,550 and the 50% Fib retracement level of the downward move from the $3,400 swing high to the $1,739 low.

A close above $2,550 could encourage the bulls to push the price above a key bearish trend line at $2,750 and the 100-day simple moving average (red).

Looking at Bitcoin, there was another bearish reaction, and the bears were able to push the price below the $65,500 support zone.

Economic Releases

- US Import Price Index for Dec 2025 (MoM) – Forecast +0.2%, versus +0.4% previous.

- US Export Price Index for Dec 2025 (MoM) – Forecast +0.2%, versus +0.4% previous.

- US Retail Sales for Dec 2025 (MoM) – Forecast +0.4%, versus +0.6% previous.

Fed’s Collins sees mildly restrictive rates on hold “for some time”

Boston Fed President Susan Collins indicated that the Fed is likely to keep interest rates steady “for some time”, pointing to improving labor market conditions and unresolved inflation pressures. In remarks delivered at at event overnight, she said employment data show “at least some more signs” of stability.

Collins argued that after 175 basis points of easing, policy is now only mildly restrictive and may already be close to neutral. Given that backdrop, she said it is “quite likely” the current rate range will remain "appropriate" while officials seek "more evidence" that inflation is firmly moving back toward 2%.

Turning to trade policy, Collins noted that the Supreme Court’s ruling against sweeping tariffs injects fresh uncertainty into the outlook. She warned that if companies have already passed higher import costs through to consumers, those price increases are unlikely to be reversed, potentially keeping inflation elevated.

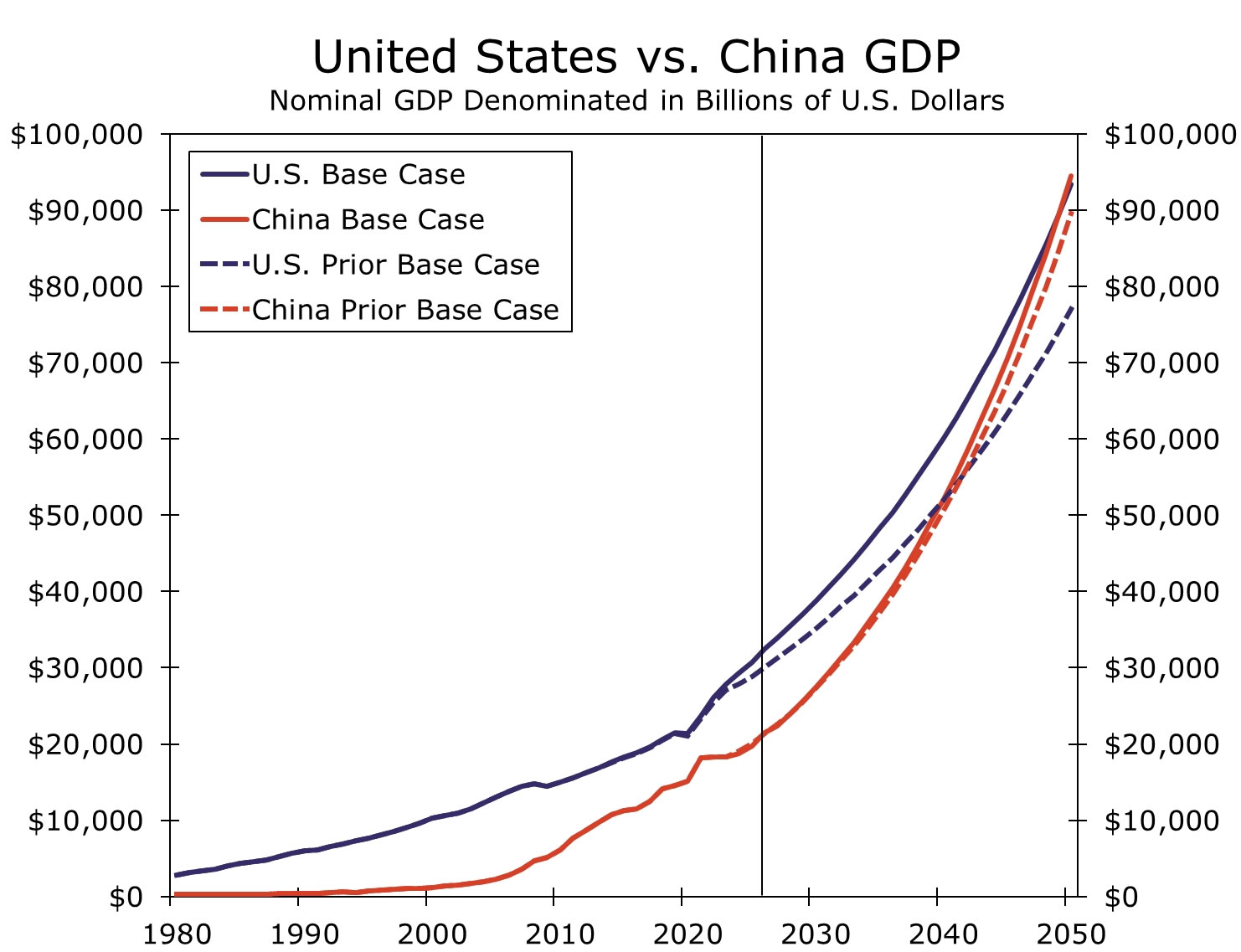

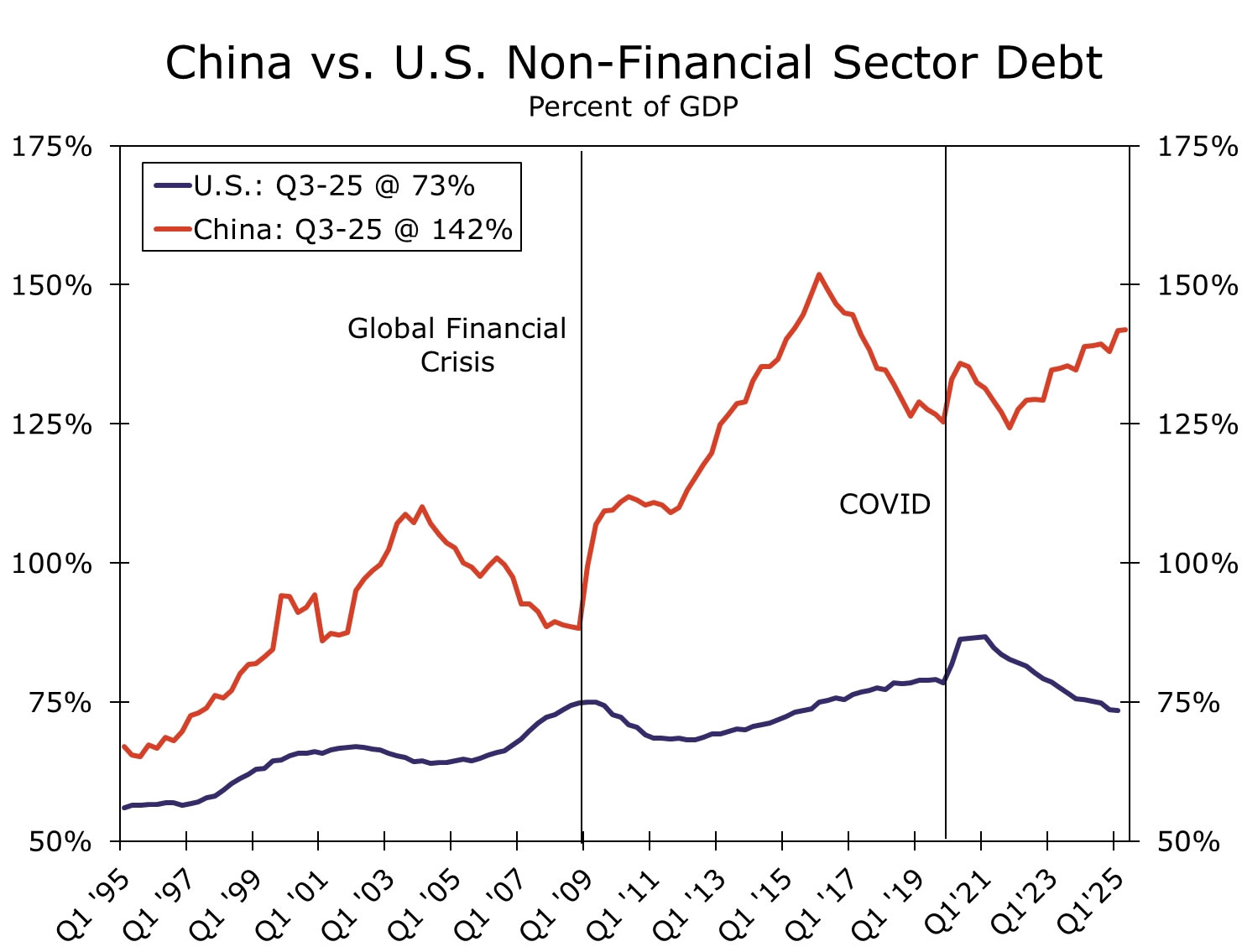

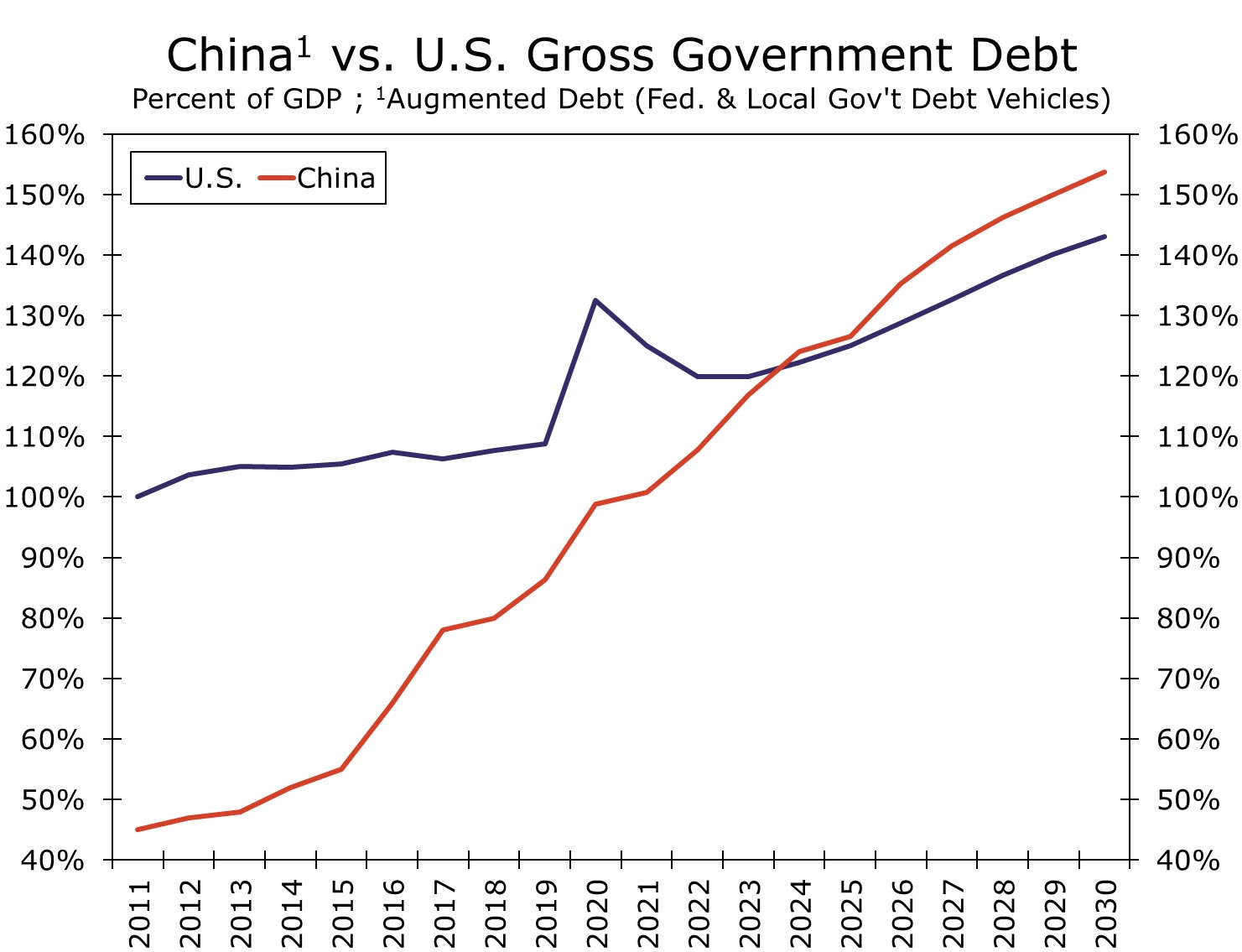

China’s Ascension to Top Economy Delayed… Again

Summary

China's rise to the world's largest economy is again delayed. We now estimate China overtakes the U.S. to become the largest economy in the world in 2049, pushed out from a prior estimate of early 2040s. Despite last year's resilience, the delay is a product of deteriorating underlying fundamentals that determine potential growth. China's population is smaller and older, deflation pressures are persistent, and rising private and public sector leverage re-introduces "hard landing" risks in China.

At the same time, fundamentals in the U.S. are on an improving trajectory and diverging from underlying trends in China. Just as worsening fundamentals will keep China stuck in second place for a longer period of time, improvements across potential growth indicators should set a solid foundation for long-term U.S. economic growth. "Hard landing" risks in China are not as apparent in the U.S., which also keeps downside risks centered in China.

Embedded in our 2049 estimate is also the view that the Chinese renminbi will strengthen going forward. We continue to believe Chinese authorities have fundamentally shifted the way FX policy is considered and set with a preference for financial stability as opposed to currency weakness. FX policy can change as domestic and external conditions change, and while our renminbi assumption is more constructive relative to FX forwards, should the renminbi trend in line with forward pricing, China's ascension to the top of the economic pedestal could come earlier than we expect, despite imbalances and structural impediments to sustainably high growth rates.

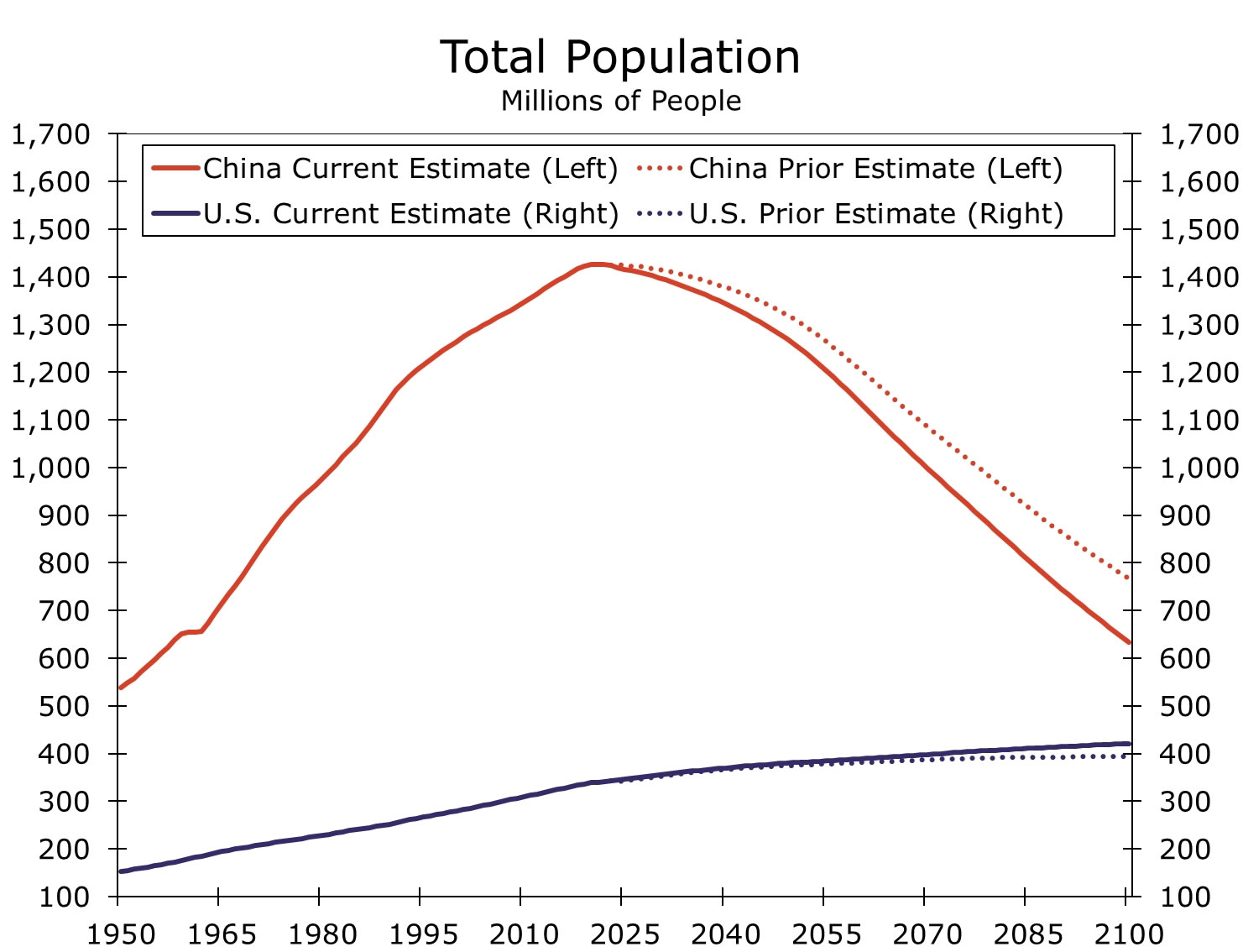

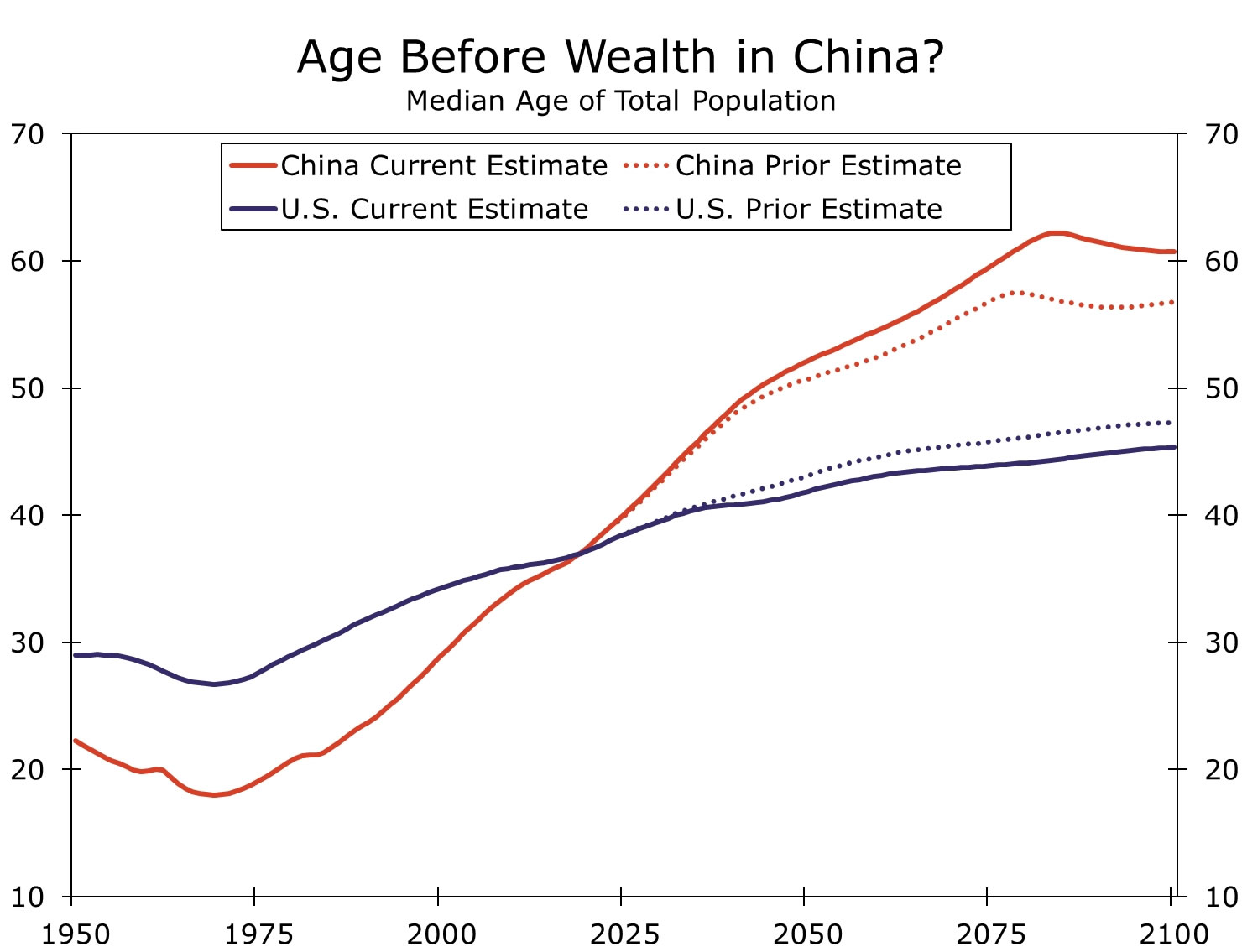

Demographics, deflation and debt are China's most pressing challenges. Each of which have contributed to slower growth over the years, and each of which have deteriorated recently. So much so that demographics, deflation and debt are likely to apply even more downward pressure on China's growth than we previously anticipated. On demographics, China's problems are known, although perhaps not fully appreciated is how China's population is now shrinking more rapidly (Figure 1) and aging quicker (Figure 2), according to the United Nations (UN). The UN now expects China's population to more than halve over the coming decades, a significantly quicker decline than prior forecasts. A similar dynamic exists for age as the UN now estimates China's population is getting older quicker than expected.

All else equal, a smaller and older labor force equals slower potential growth, and while the U.S. is far from setting the standard for ideal demographics, U.S. labor force trends are on a better trajectory than those in China. Population size is set to grow in the U.S. and that population is set to age at a less rapid pace. At least from a demographics' perspective, long-term economic growth should be more resilient in the U.S. than China, and population trends are a key input into our view that China's timetable for overtaking the U.S. is pushed out.

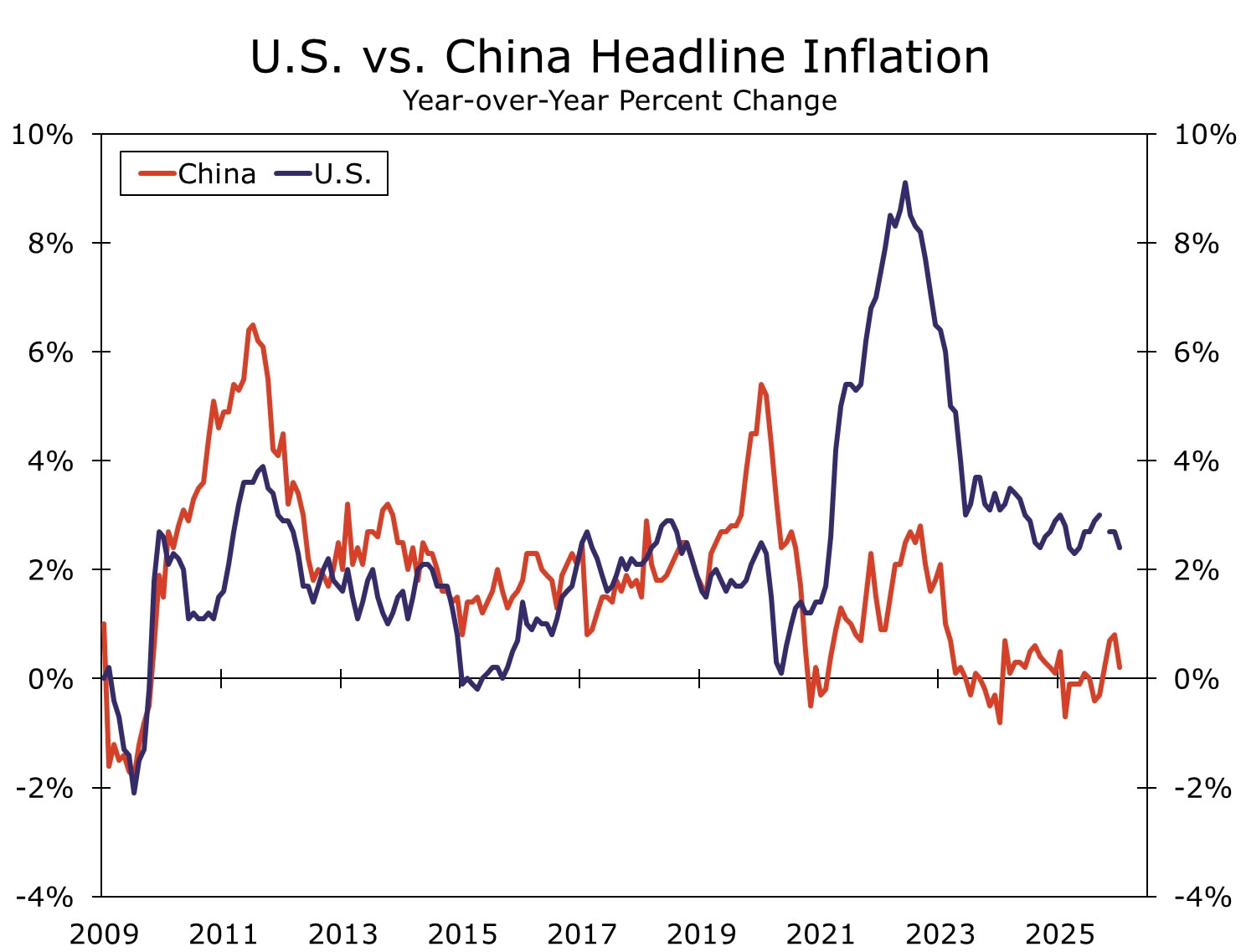

Diverging inflation trends between the U.S. and China also play a role in China lagging further behind the United States. We can point to multiple factors that generate deflation pressures in China (e.g., low consumer confidence, high household savings, sluggish domestic demand, real estate sector collapse), although just as influential are local manufacturers cutting prices to clear excess inventory (Figure 3). China's export price index is down ~15% from the peak in 2023, and while anti-involution policies have helped put a floor underneath prices, export prices remain suppressed.

Front-running tariffs catapulted China's share of the global export market higher, but if China wants to retain current market share, prices may be kept low and deflationary pressures could linger. U.S. inflation trends diverge from those in China (Figure 4). While above-target inflation in the U.S. can generate economic issues, for now, strong U.S. GDP growth combined with inflation pressures widens the gap between the U.S. and China.

Historically, an overleveraged private sector, not excessive public sector debt, has preceded rapid economic slowdowns and acted as catalysts for financial crises (e.g., Japan 1980s, EM Asia 1990s, U.S. 2000s). For China, the most pressing leverage problems still exist in the private sector, and after multiple failed attempts at deleveraging, China's private sector debt problems are intensifying. For the past few years, China's private sector debt burden has been rising and is approaching all-time highs. Corporate debt is likely to rise further now that "three red lines" policies have been relaxed, a decision that can not only pressure long-term growth rates but also re-introduces China "hard landing" financial crisis scenarios.

The trajectory of China's private sector debt burden is diverging from trends in the United States (Figure 5), leaving the U.S. economy on a more stable foundation for long-term growth. Whether a crisis unfolds in China or not, diverging private debt trends keep "hard landing" financial risks top of mind in China not the U.S., leaving downside risks to long-term growth more present in China. Also, for all we hear about U.S. government debt, China's public sector debt burden is larger, at least when adjusting for local government financing vehicles (Figure 6). Should private sector leverage issues spill over into the public sector, China has more acute issues, a dynamic that also delays China from catching up to the U.S., in our view.

The IMF suggests China may never overtake the United States... As far as comparing our growth and inflation outlooks, the IMF is more pessimistic on China's growth prospects, at least over the Fund's forecast horizon (i.e., the next five years). We—as well as the IMF—expect China's economy to be unable to sustain 5% growth rates going forward, but the IMF expects a more rapid economic deceleration. At the same time, the Fund is more optimistic that China will be able to reflate its economy to 2% in the coming years than we are. Although taken together, IMF nominal GDP forecasts are less constructive than how we see China's economy evolving. However, the IMF takes a less optimistic view on U.S. nominal GDP growth relative to ours. We both believe U.S. nominal GDP will hold steady going forward as opposed to trend deceleration in China, the IMF just holds a less optimistic definition of steady. If we extrapolate the IMF's relative views on China and the U.S. over a longer-term horizon, the IMF is inherently, based on our longer-term extrapolations, saying China will never overtake the U.S. as the world's largest economy.

...but the renminbi is the larger swing factor for China ascending to the world's largest economy. IMF forecasts, however, assume the Chinese renminbi holds steady around current levels for the foreseeable future. While the Chinese renminbi is not a particularly volatile currency, our base case 2049 estimate assumes China's currency gradually strengthens going forward as we believe China's FX policy is based on currency strength to promote financial stability (perhaps due to "hard landing" risks rising) as opposed to a historical preference for RMB weakness to support export competitiveness.

In our base case 2049 scenario, we assume RMB strengthens 1% per year going forward. We made this same assumption in our prior estimate for when China could overtake the U.S., so no change that distorts the analysis is coming from FX. We believe worsening underlying fundamentals, not RMB, are the driving force of China's delayed rise.

But while we assume RMB strength going forward, worth noting is that we still hold a less optimistic view on RMB relative to FX forward pricing. If we were to incorporate our baseline GDP and CPI forecasts with current RMB forward pricing, China could overtake the U.S. as early as 2038. Even if we were to use the IMF's GDP and inflation forecasts and adjust for FX forwards, China becomes the world's largest economy in 2039. In a scenario where the renminbi weakens, China moves further away from overtaking the United States.

Point being, just as much as underlying fundamentals play a role, so does China's currency. Typically, currency performance moves in line with economic fundamentals, but not necessarily when a managed currency regime similar to China's is in play. Granted, FX policy is not static and can change based on external or domestic factors, but if Chinese authorities are committed to financial stability and promoting the renminbi as a world's reserve currency at a time when the dollar is broadly depreciating, China's ascension could come a bit quicker even if underlying fundamentals are being eroded.

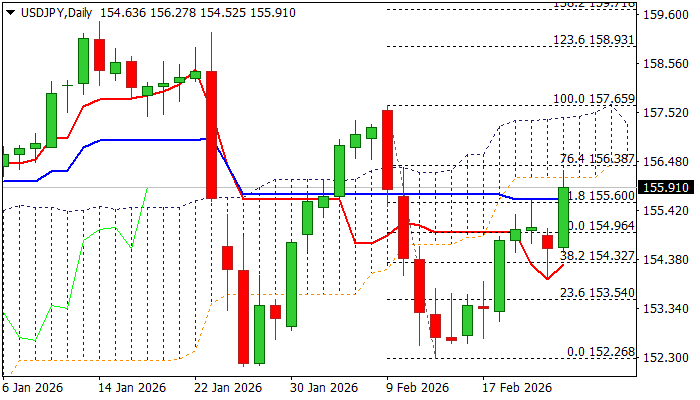

USD/JPY: Japanese Yen Falls Almost 1% on Fresh Monetary Policy Uncertainty

USDJPY jumped 0.9% on Tuesday after Japan PM Takaichi raised concerns about BoJ’s further interest rate hikes that collides with wide market expectations for increase in borrowing cost by 1% in the first six months of 2026 and the first action expected as early as April.

Fresh uncertainty about anticipated monetary policy trajectory deflated yen, which fell to the lowest in two weeks against the US dollar on Tuesday.

Tuesday’s rally generated signal of bullish continuation after rally from 152.26 Feb 12 low) paused for two-day shallow pullback, extension above Fibo 61.8% of 157.65/152.26 bear-leg (155.60) and cracking the base of daily Ichimoku cloud (156.13) adding bullish signals.

Bulls slowed after testing cloud base (seen by traders as good take-profit level after today’s significant rally), with overbought stochastic and north-heading 14-d momentum still holding under the centreline, setting stage for a pause.

Firmer technical picture and supportive fundamentals suggest that bulls may take a breather for consolidation and positioning for fresh attack at daily cloud (which is quite thick and may provide further headwinds), with stronger penetration into cloud to fuel hopes of full retracement of 157.65/152.26 fall.

Broken Fibo 61.8% (155.60) offers immediate support ahead of more significant 154.95 level (100DMA / broken Fibo 50%).

Res: 156.13; 156.38; 157.00; 127.40

Sup: 155.60; 154.95; 154.73; 154.32

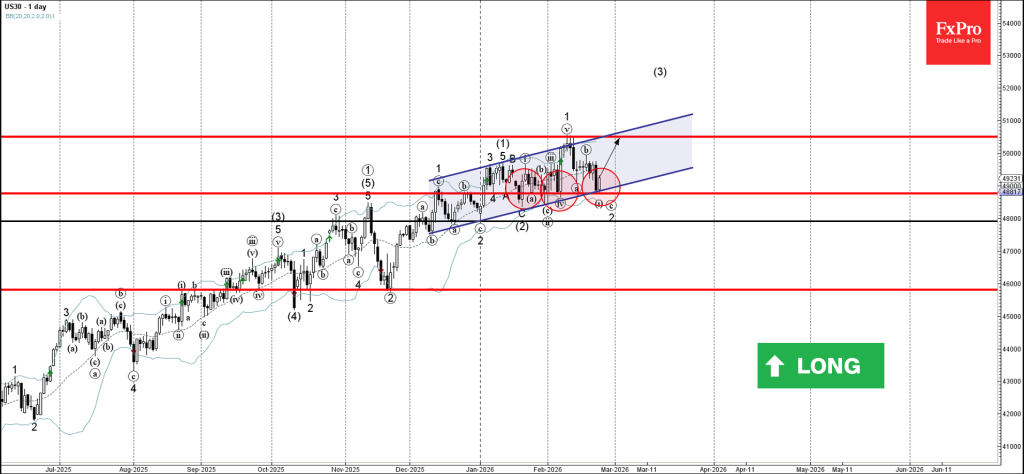

Dow Jones Wave Analysis

Dow Jones: ⬆️ Buy

- Dow Jones reversed from support zone

- Likely to rise to resistance level 50500,00

Dow Jones index recently reversed up from the support zone between the key support level 48760,00 (which has been reversing the price from December) and the lower daily Bollinger Band.

This support zone was further strengthened by the support trendline of the daily up channel from December.

Given the strong daily uptrend, Dow Jones index can then be expected to rise to the next resistance level 50500,00 (which stopped earlier impulse wave 1).