Sample Category Title

Bitcoin and Ethereum Struggling to Rebound

Market Overview

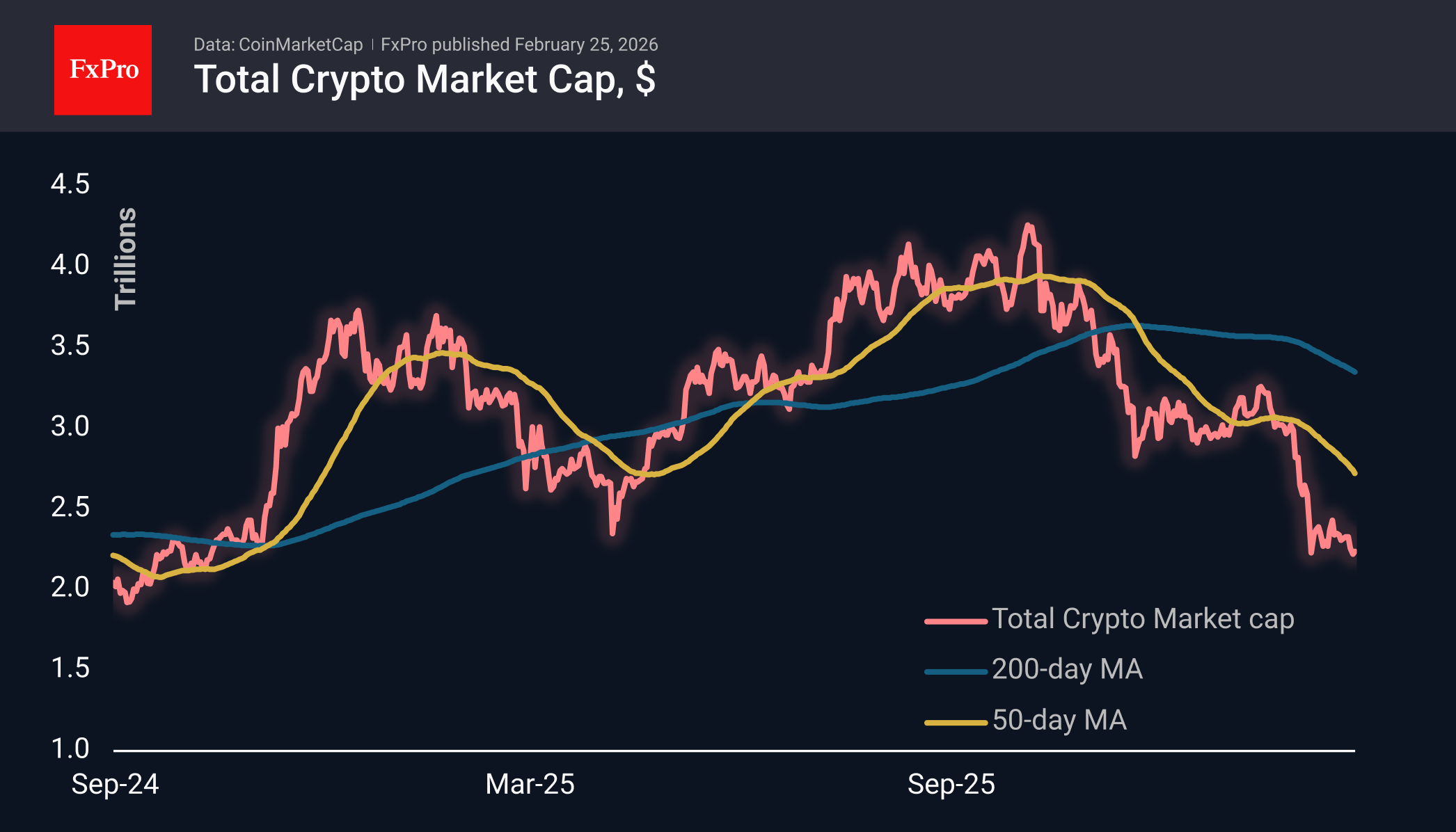

The crypto market capitalisation is up about 1% from yesterday’s level, rebounding to $2.24 trillion after plunging to $2.18 trillion on Tuesday. Once again, we are seeing a weak rebound after the dip, underscoring that bears remain in control of the markets.

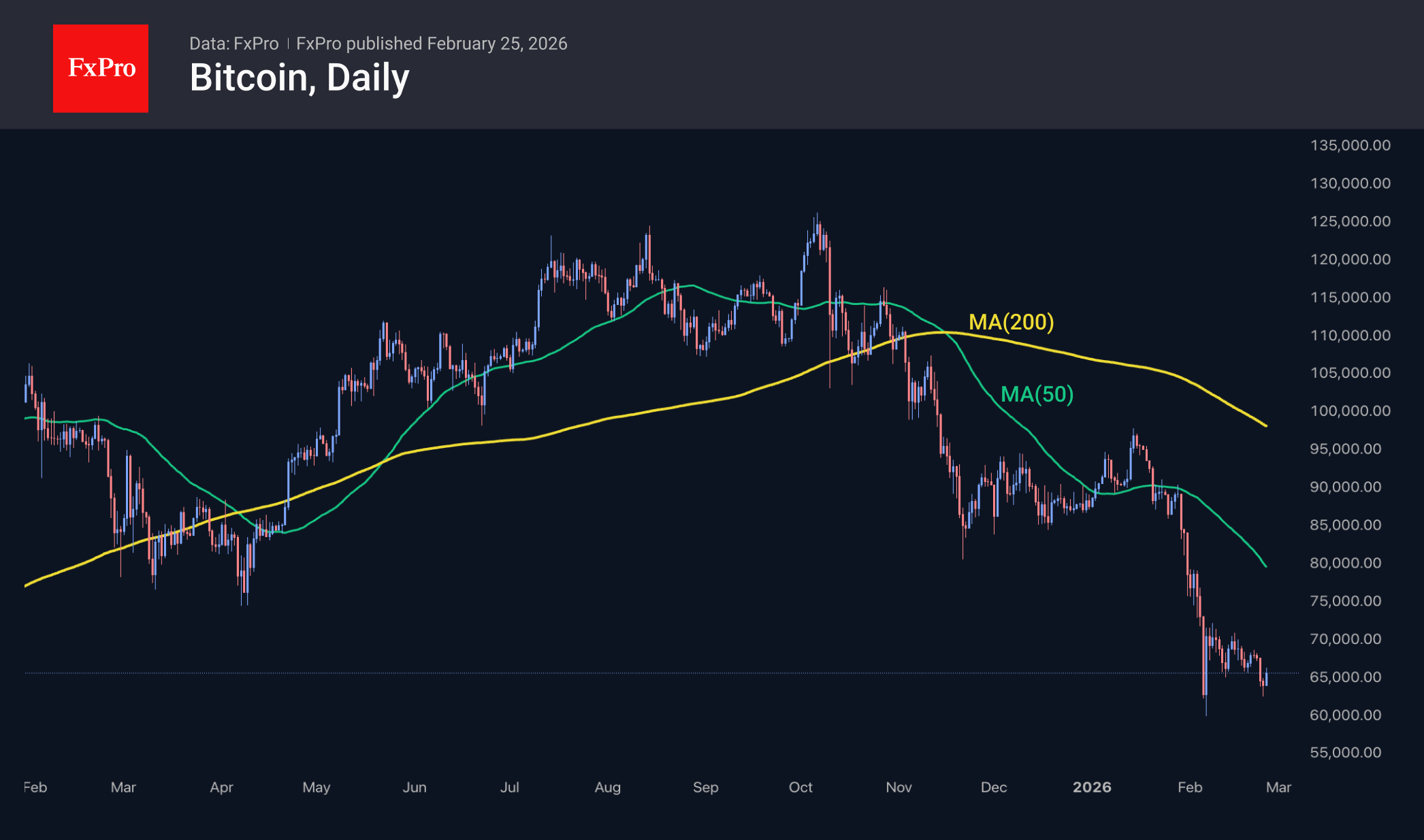

Bitcoin fell to $62.5K but had already rebounded to $65.5K at the time of writing. This looks like an attempt to form a double bottom. In the short term, it is worth acknowledging the local initiative on the bulls’ side, but this rebound has not yet broken the downward resistance that has been in place for twenty days.

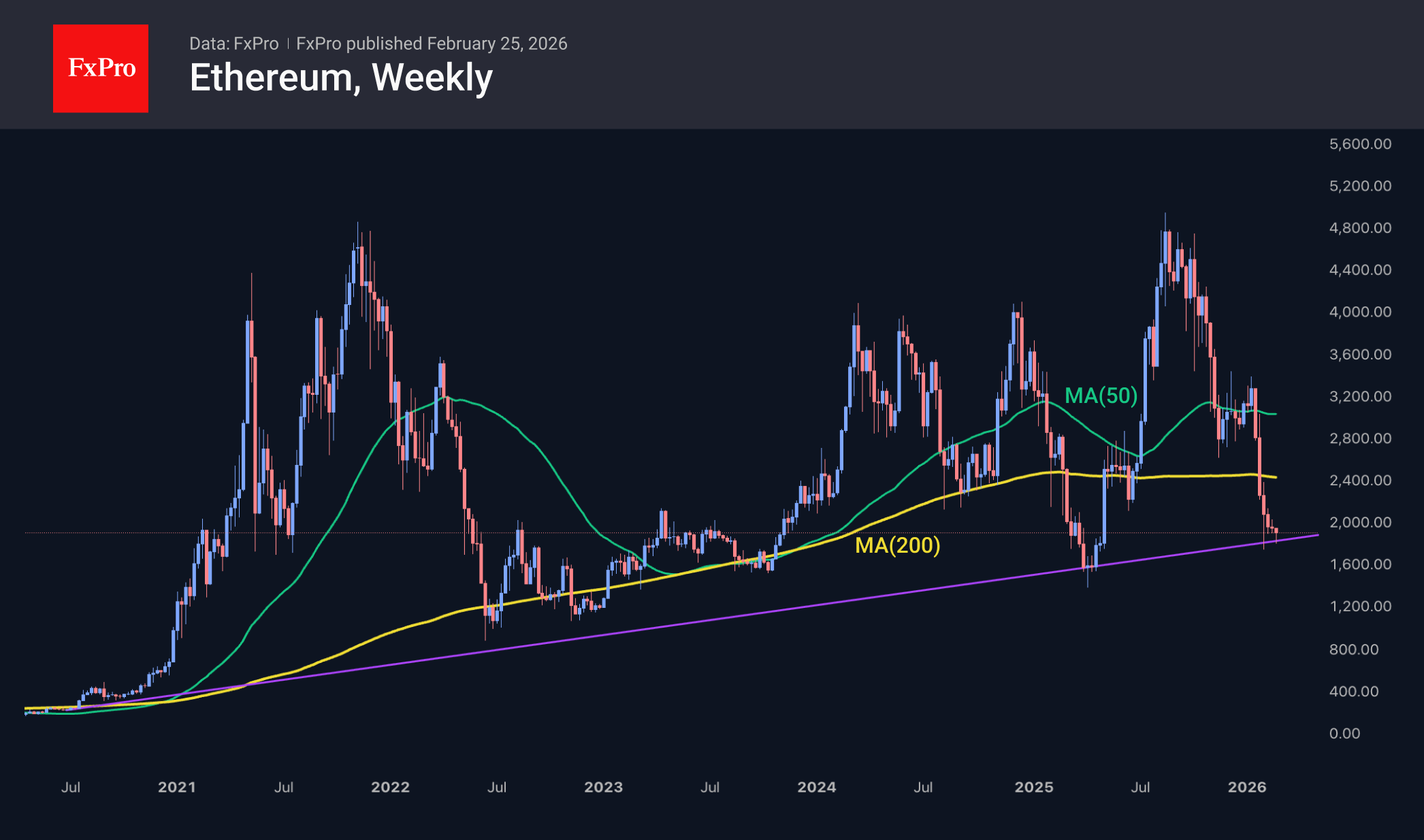

Ethereum is up 4%, outperforming many of its heavyweight competitors. Here, we also see an ongoing struggle at the long-term support level. In April last year, the second-largest coin by capitalisation was actively bought after falling below this line, but will it be able to do so again?

News Background

In the current environment, cryptocurrencies are losing ground alongside tech stocks, Wintermute notes. Capital is flowing from high-risk assets into defensive and tangible assets.

Global uncertainty is pushing investors into defensive assets, depriving the crypto market of liquidity. The stagnation in stablecoin supply has become a ‘significant obstacle’ for Bitcoin, Matrixport notes. Glassnode expects liquidity to recover in six months at the earliest.

If Bitcoin breaks through $60K, it could fall to the $50K–55K range or even to $47K, Bitrue predicts. In a negative scenario, cascading liquidations will accelerate amid deteriorating external conditions.

Cryptoquant has recorded a slowdown in BTC sales on the largest exchange, Binance, which offers hope for a short-term recovery. However, in the medium term, the bearish trend may continue.

Bitcoin is in its ‘adolescent’ stage of development — an intermediate stage between a speculative asset and a global store of value, according to Bitwise. Strategy founder Michael Saylor believes Bitcoin’s recovery could take two to seven years.

According to Onchain Lens, Ethereum co-founder Vitalik Buterin has sold 3,765 ETH worth $7.08 million over the past four days and 10,723 ETH since the beginning of February. The total proceeds amounted to approximately $21.7 million at an average price of $2,027 per coin.

The Arizona State Senate has approved the creation of a strategic reserve of digital assets. The fund is planned to be replenished with confiscated cryptocurrency.

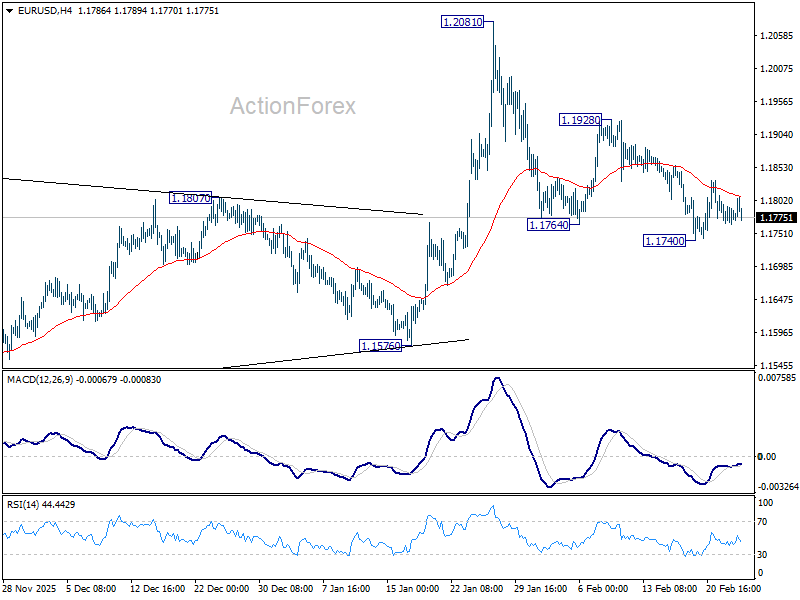

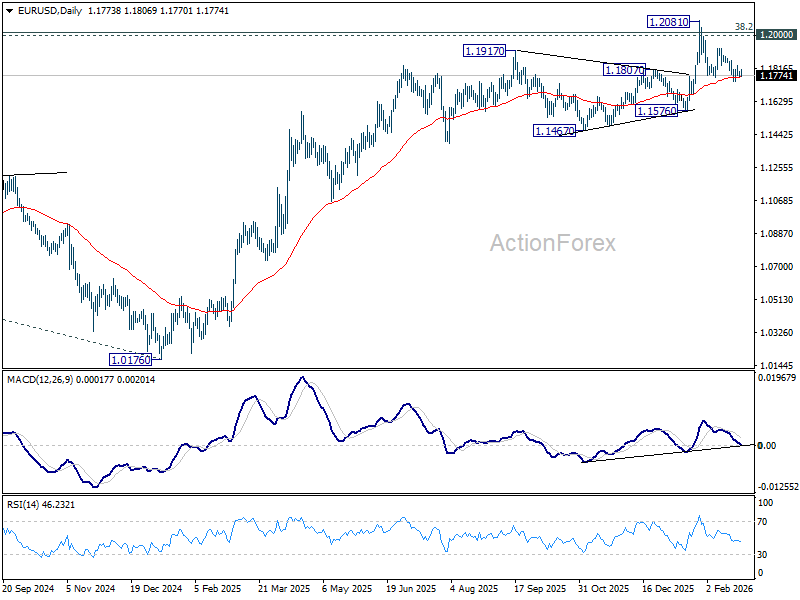

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1760; (P) 1.1779; (R1) 1.1791; More….

Range trading continues in EUR/USD and intraday bias stays neutral. Near term risk will remain on the downside as long as 1.1928 resistance holds. Below 1.1740 temporary low will target 1.1576 support next. Firm break there should confirm rejection by 1.2 key psychological level and turn near term outlook bearish. However, break of 1.1928 argue that fall from 1.2081 has completed as a correction, and revive near term bullishness. Retest of 1.2081 should then be seen next.

In the bigger picture, as long as 55 W EMA (now at 1.1494) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.2581. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

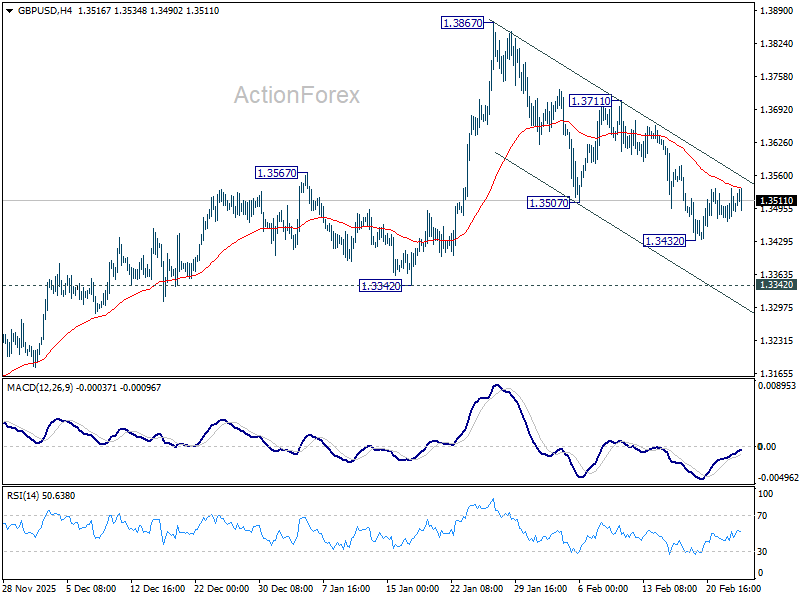

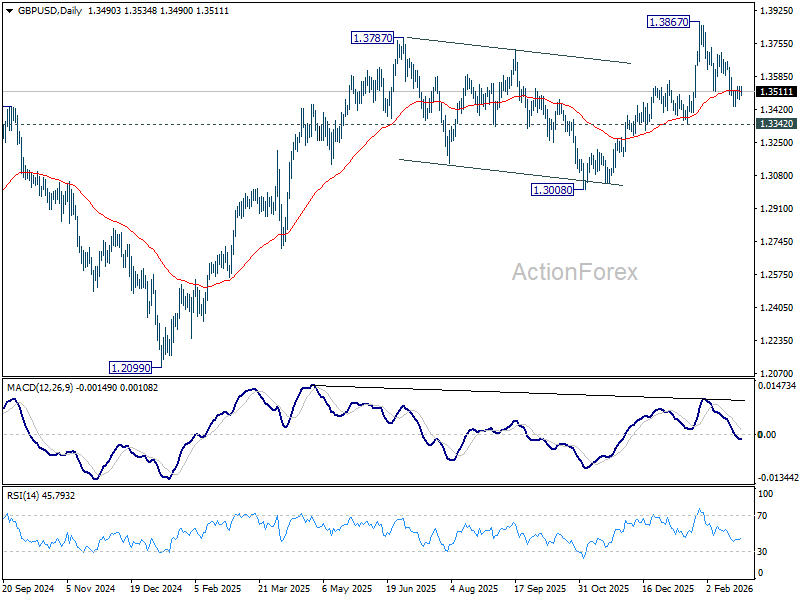

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3460; (P) 1.3498; (R1) 1.3527; More...

Range trading continues in GBP/USD and intraday bias remains neutral. On the downside, below 1.3432 will resume the fall from 1.3867 to 1.3342 support. Firm break there should confirm that it's already correcting the whole rise from 1.2099. However, break of 1.3711 resistance will argue that the decline has completed as a near term correction, and turn bias back to the upside for retesting 1.3867.

In the bigger picture, as long as 1.3008 support holds, rise from 1.3051 (2022 low) should still be in progress for 1.4284 key resistance (2021 high). Decisive break there will add to the case of long term bullish trend reversal. However, firm break of 1.3008 will raise the chance of medium term bearish reversal and target 1.2099 support next.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7727; (P) 0.7746; (R1) 0.7762; More….

Range trading continues in USD/CHF and intraday bias stays neutral. Consolidation pattern from 0.7603 is still in progress. In case of stronger rise, upside upside should be limited by 55 D EMA (now at 0.7828) to complete the pattern. On the downside, below 0.7627 will bring retest of 0.7603. Firm break there will resume larger down trend, and target 0.7382 projection level next. However, sustained break of 55 D EMA will indicate that a larger scale corrective bounce in underway and target 0.8039 resistance next.

In the bigger picture, down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8123 resistance holds.

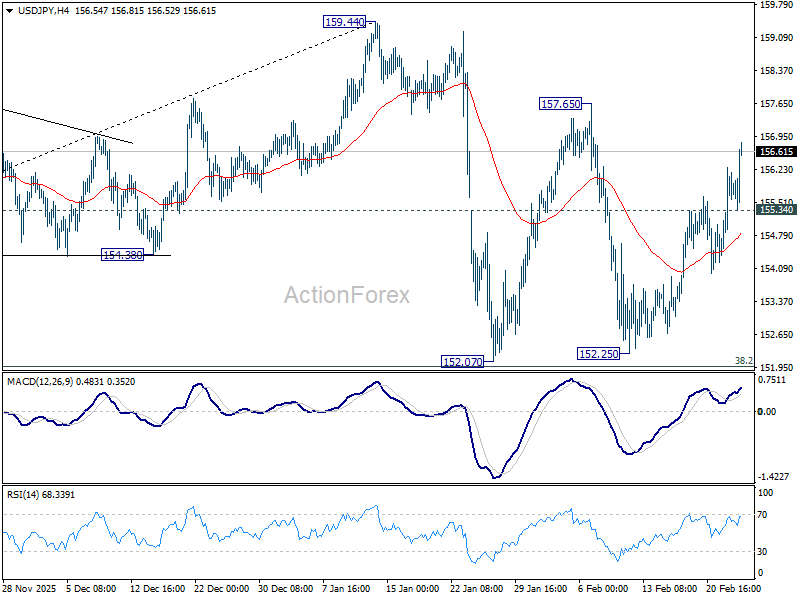

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 154.86; (P) 155.57; (R1) 156.61; More...

Intraday bias in USD/JPY stays on the upside as rise form 152.25 extends higher today. Firm break of 157.65 resistance will target a retest on 159.44 high. On the downside, below 155.34 minor support will turn intraday bias neutral again first. Overall, with 38.2% retracement of 139.87 to 159.44 at 151.96 intact, price actions from 159.44 are seen as a corrective pattern. Also, rise from 139.87 is expected to resume through 159.44 at a later stage.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 151.93) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

Risk-On Wave Pressures Yen, While BoJ Dovish Tilt Emerges

Yen is firmly back in its traditional inverse relationship with global risk sentiment. Today’s broad-based selloff in the currency moved in tandem with a powerful equity rally stretching from Asia to Europe. In Asia, the Nikkei 225 surged past 58,000 for the first time, while the KOSPI smashed through the 6,000 level in a decisive breakout. The move reflects strong tech momentum and persistent dip-buying behavior.

The strength extended into Europe. The FTSE 100, CAC 40, and Euro Stoxx 50 all hit fresh record highs, underscoring the breadth of the rally. Strong 2025 earnings from HSBC Holdings helped lift the broader European banking sector. At the same time, AI remains a tailwind. European technology stocks are benefiting from global capex optimism, with markets positioning ahead of Nvidia’s earnings due late Wednesday, seen as a key catalyst for the next leg.

Markets also appear to be shrugging off recent US tariff turbulence. While policy direction remains fluid, investors are treating trade tensions as a manageable structural factor rather than a trigger for de-risking.

For Yen, however, domestic factors are compounding the external pressure. Japan’s government nominated two academics viewed as strong stimulus advocates to the BoJ board. Toichiro Asada, a known reflationist, will replace Asahi Noguchi at the end of March, while Ayano Sato will succeed Junko Nakagawa later this year.

The shift in board composition could influence discussions around the pace and timing of further tightening. Although the BoJ is expected to continue gradual normalization, the probability of a hike in March or April has diminished. The central bank is likely to maintain its broader tightening path, but caution around timing now dominates expectations.

In FX markets, Yen is the weakest performer of the day so far, followed by Swiss Franc and Dollar. Australian Dollar leads gains on stronger CPI, though momentum was tempered by cautious remarks from RBA Governor Michele Bullock. Sterling and Kiwi follow, while Euro and Loonie sit mid-pack.

In Europe, at the time of writing, FTSE is up 1.00%. DAX is up 0.41%. CAC is up 0.42%. UK 10-year yield is up 0.031 at 4.335. Germany 10-year yield is up 0.011 at 2.721. Earlier in Asia, Nikkei rose 2.20%. Hong Kong HSI rose 0.66%. China Shanghai SSE rose 0.72%. Singapore Strait Times fell -0.26%. Japan 10-year JGB yield rose 0.034 to 2.147.

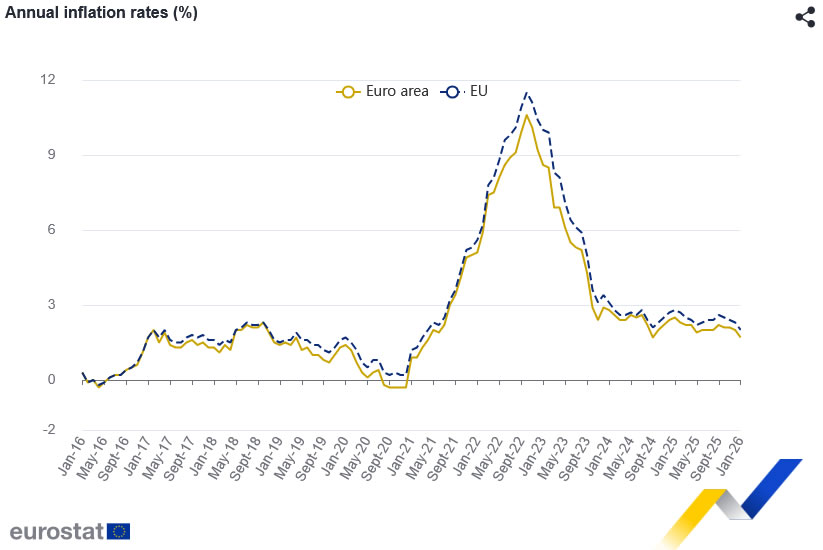

Eurozone CPI finalized at 1.7% in January, disinflation trend continues

Eurozone CPI was finalized at 1.7% year-on-year in January, down from 2.0% in December. Core CPI, which excludes energy, food, alcohol and tobacco, was also finalized at 2.2% year-on-year, slipping from 2.3% previously.

The breakdown shows services remained the primary driver in Eurozone inflation, contributing 1.45 percentage points to the annual rate. Food, alcohol and tobacco added 0.51 percentage points, while non-energy industrial goods contributed 0.09. Energy continued to act as a drag, subtracting -0.39 percentage points from overall inflation.

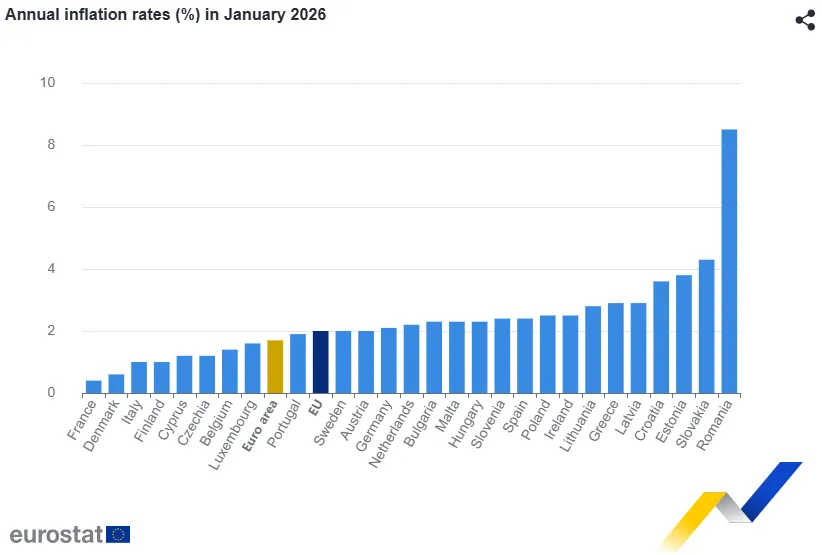

Across the broader EU, CPI slowed to 2.0% from 2.3%. Inflation declined in 23 member states compared with December. France (0.4%), Denmark (0.6%), Finland and Italy (both 1.0%) recorded the lowest rates. Romania (8.5%), Slovakia (4.3%) and Estonia (3.8%) were at the top of the range. The data reinforce the narrative of broad-based disinflation, though services inflation remains relatively sticky.

RBA’s Bullock tempers post-CPI tightening bets

RBA Governor Michele Bullock struck a measured tone in a fireside chat today, saying the Australian economy and labor market remain “a little bit tight,” while inflation is “a little bit elevated” but not "taking off again". The comments came after stronger-than-expected CPI data earlier in the day had fueled a sharp rise in rate hike expectations.

Bullock emphasized that it would take time for the RBA to determine its next move, adding that policymakers would "have to be patient” . Her remarks contrasted with the market’s earlier reaction, which had pushed the probability of a May hike from 84% to 95%, and lifted expectations of a third increase by year-end from 40% to 60%.

Following her speech, rate-sensitive markets pared gains, with traders dialing back expectations of rapid tightening.

Australia trimmed mean CPI climbs to 3.4%, RBA hike seen inevitable

Australia’s monthly CPI for January came in hotter than expected, reinforcing expectations of further tightening from the RBA. Headline inflation held unchanged at 3.8% yoy, above the 3.7% consensus and marking the joint highest reading since mid-2024.

More concerning for policymakers, trimmed mean CPI rose from 3.3% yoy to 3.4%, also exceeding forecasts and standing at its highest level since Q3 2024. Core inflation has now been at or above 3% since July 2025, remaining clearly outside the RBA’s 2–3% target band.

Housing (+6.8%), food and non-alcoholic beverages (+3.1%), recreation and culture (+3.7%), were the largest contributors to annual price pressures.

Markets had already leaned toward a May rate hike, and today’s data does little to challenge that view. Some economists argue the RBA may be “a little bit behind the curve,” risking a scenario where inflation becomes entrenched and requires more forceful tightening later. With price pressures proving persistent, another rate increase is increasingly viewed as close to inevitable.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 154.86; (P) 155.57; (R1) 156.61; More...

Intraday bias in USD/JPY stays on the upside as rise form 152.25 extends higher today. Firm break of 157.65 resistance will target a retest on 159.44 high. On the downside, below 155.34 minor support will turn intraday bias neutral again first. Overall, with 38.2% retracement of 139.87 to 159.44 at 151.96 intact, price actions from 159.44 are seen as a corrective pattern. Also, rise from 139.87 is expected to resume through 159.44 at a later stage.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 151.93) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

EUR/USD: Trapped at 1.1800 as Euro Area Inflation Cools Significantly… What Next?

- Euro Area annual inflation cooled to 1.7% in January 2026, the lowest level since September 2024.

- Core inflation, stripping out volatile items like energy and food, dropped to 2.2%, its lowest point since October 2021.

- The EUR/USD pair is struggling for direction around the 1.1800 handle, with its next move dependent on the US dollar's strength and central bank commentary.

EUR/USD has continued to struggle for direction around the 1.1800 handle. For the last 5 days EUR/USD has traded between the 1.1840-1.1740 handles with breakout not yet forthcoming.

Market participants had eyed the Euro CPI release as a potential catalyst for a breakout, however the data failed to inspire a bullish move for the Euro. The MoM inflation was actually worse than expected in the final number, dropping to -0.6% compared to the forecast of -0.5%.

Euro Area inflation at lowest level since September 2024

In January 2026, the Euro Area saw a notable cooling in cost pressures as annual inflation was confirmed at 1.7%, a drop from the 2.0% recorded in December.

This mark represents the lowest inflation level since September 2024, a shift that occurred alongside a significant strengthening of the euro, which surpassed the $1.20 threshold, its highest valuation in over four years.

This currency appreciation helped dampen price growth across several sectors; specifically, services inflation moderated to 3.2%, and the cost of processed food, alcohol, and tobacco slowed slightly to 2.0%. The most dramatic downward pressure came from energy prices, which plummeted by 4.0% in January, more than doubling the pace of the decline seen the previous month.

Despite the general downward trend, some sectors experienced upward pressure. Inflation for unprocessed food climbed to 4.2%, up from 3.5% in December, while non-energy industrial goods saw a marginal uptick to 0.4%.

However, the underlying trend remained soft, as evidenced by core inflation which strips out volatile items like energy and food, falling to 2.2%. This is a significant milestone, marking its lowest point since October 2021.

The slowdown was visible across most of the bloc’s major economies, though the intensity varied by country.

Source: EuroStat

What comes next for EUR/USD?

EUR/USDs next move may depend on the US dollar which has been seeing a resurgence of late. If this persists coupled with the low inflation the EU, EUR/USD could continue its grind lower.

Chatter from Federal Reserve policymakers yesterday aided the USD as they adopted a more hawkish rhetoric. Later in the US session we have a host of Fed policymakers speaking. Are we going to get a similar story to yesterday?

Tomorrow’s speech by ECB President Lagarde at the EU Parliament is the only potential domestic driver for the euro this week, ahead of flash CPI figures on Friday.

As much as chatter around the end of the ‘Trump trade’ has intensified, there are still concentration risks around the US which could hamper the US dollar and thus keep EUR/USD holding the line for now.

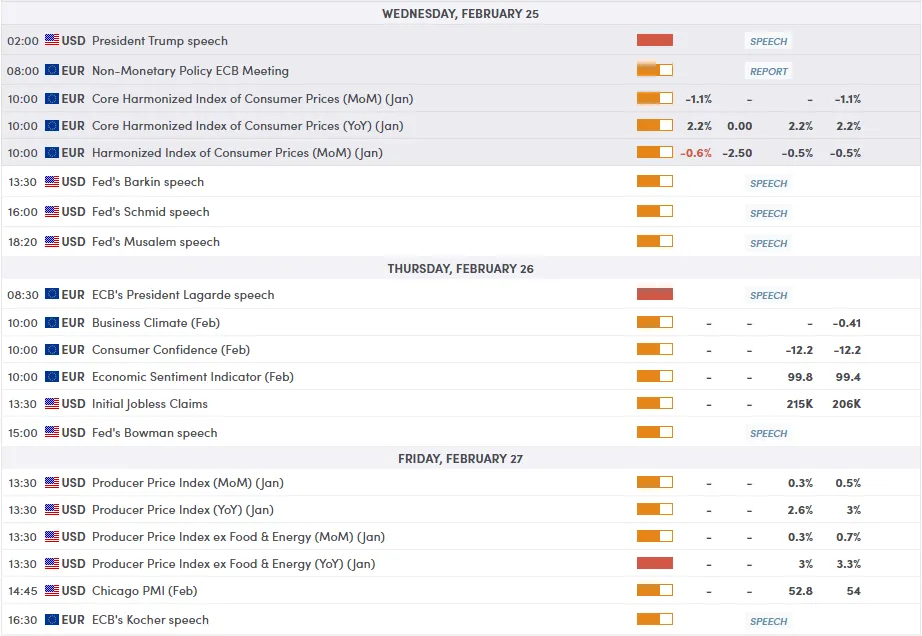

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Technical Analysis on EUR/USD

EUR/USD is currently in a consolidation phase following a significant rally and subsequent sharp rejection from the 1.2000 psychological resistance level.

Price action is currently being squeezed between a descending trendline and a key horizontal support zone with price right at the apex meaning a breakout is imminent.

This descending triangle pattern suggests that selling pressure is gradually increasing. However, the horizontal support at 1.1769 is holding firm for now.

The pair is trading slightly above its 100-day SMA. This moving average is sloping upward, suggesting that the broader medium-term trend still has a bullish bias, even if the short-term momentum is cooling off.

A few mixed signals but a breakout to the upside of the triangle pattern could facilitate a move higher as the 100-day SMA does hint a overall bullish bias.

Immediate resistance rests at the 1.1840 handle before the 1.1920 and 1.2000 psychological level come into focus.

A move to the downside may find support at the 1.1700 handle. The next target to the downside is the long-term ascending trendline near 1.1600.

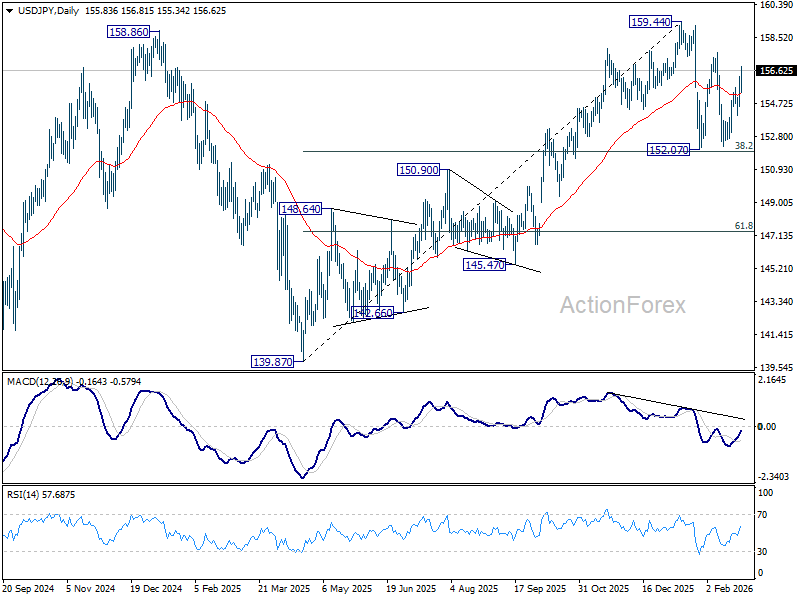

EUR/USD Daily Chart, February 25, 2026

Source:TradingView.com

RBA’s Bullock tempers post-CPI tightening bets

RBA Governor Michele Bullock struck a measured tone in a fireside chat today, saying the Australian economy and labor market remain “a little bit tight,” while inflation is “a little bit elevated” but not "taking off again". The comments came after stronger-than-expected CPI data earlier in the day had fueled a sharp rise in rate hike expectations.

Bullock emphasized that it would take time for the RBA to determine its next move, adding that policymakers would "have to be patient” . Her remarks contrasted with the market’s earlier reaction, which had pushed the probability of a May hike from 84% to 95%, and lifted expectations of a third increase by year-end from 40% to 60%.

Following her speech, rate-sensitive markets pared gains, with traders dialing back expectations of rapid tightening.

AUD/USD: Lifted by Higher Than Expected Inflation

AUDUSD jumped to two-week high (0.7116) in early Wednesday’s trading following release of Australian CPI data.

Inflation remained elevated and unchanged in January compared to previous month (3.8%; Core 3.4% - the highest in 16 months) beating forecasts (3.3%; Core 3.7%) and boosting bets for another rate hike, after the RBA raised interest rates by 25 basis points to 3.85% earlier this month, reversing its path after three rate cuts in 2025.

January numbers contribute to the central bank’s expectations that inflation would rise to 4.2% in the first six months of this year (Core inflation was expected to accelerate to 3.7%), as economic growth gains pace and the labor market remains tight.

However, subsequent relatively dovish comments from RBA Governor Bullock (signal that the RBA will likely stay on hold in March policy meeting) poured cold water on fresh bulls and pushed the price lower, to reverse about 50% of post-data advance.

Technical picture on daily chart remains bullish overall, as the price action holds in extended consolidation under new three-year high (0.7147).

Broader bullish structure is expected to remain intact while the price stays above 0.70 zone (psychological/recent range floor/near 50% retracement of 0.6896/0.7147 upleg).

On the other hand, loss of 0.70 handle would put immediate bulls on hold for deeper pullback that would unmask next trigger at 0.6870 (Feb 6 higher low).

Res: 0.7116; 0.7147; 0.7207; 0.7265.

Sup: 0.7043; 0.7000; 0.6975; 0.6896.

Eurozone CPI finalized at 1.7% in January, disinflation trend continues

Eurozone CPI was finalized at 1.7% year-on-year in January, down from 2.0% in December. Core CPI, which excludes energy, food, alcohol and tobacco, was also finalized at 2.2% year-on-year, slipping from 2.3% previously.

The breakdown shows services remained the primary driver in Eurozone inflation, contributing 1.45 percentage points to the annual rate. Food, alcohol and tobacco added 0.51 percentage points, while non-energy industrial goods contributed 0.09. Energy continued to act as a drag, subtracting -0.39 percentage points from overall inflation.

Across the broader EU, CPI slowed to 2.0% from 2.3%. Inflation declined in 23 member states compared with December. France (0.4%), Denmark (0.6%), Finland and Italy (both 1.0%) recorded the lowest rates. Romania (8.5%), Slovakia (4.3%) and Estonia (3.8%) were at the top of the range. The data reinforce the narrative of broad-based disinflation, though services inflation remains relatively sticky.