Sample Category Title

Sweden’s NIER Survey Takes the Limelight

In focus today

In Sweden, the February NIER Economic Tendency Survey will be released (at 9.00 CET). In January, it was nearly unchanged, with strong firm readings offset by weaker consumer confidence. For inflation, the survey's price plans will provide insight into import price trends amid a stronger SEK.

We will closely monitor developments in the US-Iran talks in Geneva.

Economic and market news

What happened overnight

In Japan, BoJ Governor Ueda signalled the possibility of rate hikes as early as March or April. Japan's government also nominated two academics seen as advocates of economic stimulus to the BoJ board, reflecting PM Takaichi's dovish policy stance. The yen traded near a two-week low yesterday, with USD/JPY trading around the 156-mark.

What happened yesterday

In the US, Trade Representative Greer outlined next step for tariffs, including Section 301, which allow tariff rates - also higher than 15% - to be imposed if investigations find foreign countries apply discriminatory policies against US commerce. Greer cited unresolved capacity issues in China as a reason for maintaining tariffs on China, Vietnam and others.

In the euro area, the final January inflation confirmed the flash print of headline at 1.7% y/y and core at 2.2% y/y, with a slight lowering of the estimates on the second decimal. Services inflation was weaker than in flash, but a less dovish impression emerges when adjusted for constant tax rates. Germany's VAT reduction on restaurants and other one-off factors thus contributed to lower services inflation, yet momentum remains consistent with recent months, reflecting decent underlying price pressure.

In Germany, the final Q4 2025 GDP release showed strong details of the 0.3% q/q expansion, driven by domestic demand. Private consumption rose as households spent more, lowering the savings rate to 9.4% from 10.4%, and worked more hours. Government consumption and construction investments also supported growth. The rebound this year looks promising, with expected real income gains and rising public investments.

In Norway, wage growth slowed to 3.1% y/y in January, as expected. This was mainly due to base effects that will partly reverse in February. However, the underlying trend seems to be declining, which should be good news for the inflation outlook. The trend adjusted LFS-unemployment came in unchanged at 4.5% in January, yet the more accurate NAV-unemployment is falling, signaling a tighter labour market.

In Sweden, the Producer Price Index increased by 2.4% m/m but fell -2.0% y/y in January. Import prices continue to decline due to last year's SEK appreciation. The pass-through to inflation remains limited. The monthly increase was driven mainly by electricity and water distribution, food products, and metals.

In oil space, the eight OPEC+ members are reportedly set to discuss a 137k bpd output hike for April at the 1 March meeting. This would mark a return to production hikes after a three-month pause. Saudi Arabia has activated a plan for short-term oil output and export surges, should a US strike on Iran disrupt Middle Eastern oil flows. Brent Crude is currently trading above the USD 70/bbl mark, as markets await the US-Iran nuclear talks today.

Equities: Global equities had another good day yesterday, rising 0.8%. S&P500 was up 0.8%, with Nasdaq 1.3% and Russell 2000 up 0.4%. Stoxx 600 rose 0.7%. The rally yesterday can either be seen through the 2026-laggard recovering or through the 'AI wave' lens with IT, financials and communication services in the driver seat, ahead of Nvidia's earnings report last night. After spiking well above 20 on Monday, the VIX gradually declined yesterday to just below 18 now. Asian equities are mostly in green overnight with Nikkei and Kospi setting new record highs, amid US futures being down.

Nvidia's earnings report came as the last of the big companies. While Nvidia in itself is not a forward-looking metric for the AI adoption, the solid beat on sales projection of 7bn to 78bn for Q1 shows the continued demand for chips. Also, the earnings beat per share of 9 cents to USD 1.62 shows the strong demand for their product. After an initial spike of 1.5% upon earnings release in the aftermarket, likely driven by the sales, the stock ended broadly unchanged in the aftermarket.

FI and FX: Yesterday's session concluded another day with an overall positive risk sentiment. Whereas credit spreads continued to tighten, movements in foreign exchange and fixed income markets can overall be described as small. EUR/USD lifted marginally and trades now at 1.182, and EUR/SEK as well as NOK/SEK closed the session almost unchanged, despite some intraday volatility. US treasury rates lifted by a couple of basis points, but the impact of the slightly softer than usual demand in the 5y auction did not result in any large reaction.

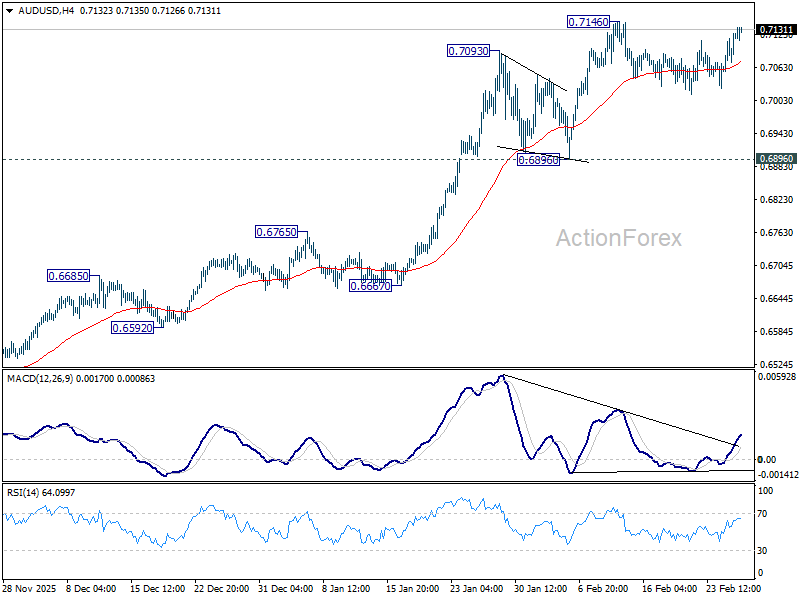

AUD/USD Daily Report

Daily Pivots: (S1) 0.7078; (P) 0.7102; (R1) 0.7148; More...

AUD/USD is still bounded in range below 0.7146 and intraday bias stays neutral at this point. Consolidations could continue and deeper retreat cannot be ruled out. But downside should be contained above 0.6896 support. On the upside, above 0.7146 will resume larger up trend to 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Further rally should be seen to 61.8% retracement of 0.8006 to 0.5913 at 0.7206. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.

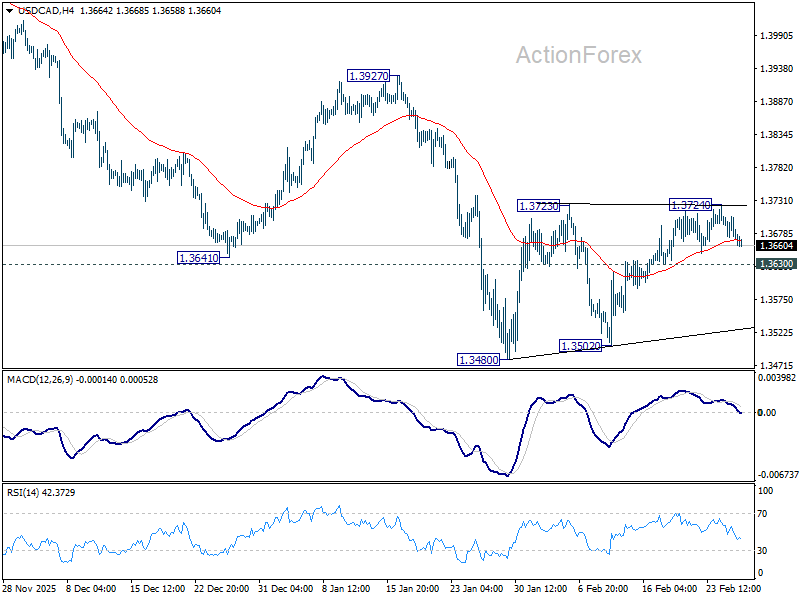

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3663; (P) 1.3685; (R1) 1.3698; More...

Intraday bias in USD/CAD remains neutral at this point. Consolidations from 1.3480 is in progress and stronger rebound might be seen. But upside should be limited by 55 D EMA (now at 1.3730) to complete the pattern. On the downside, below 1.3630 minor support will bring retest of 1.3480 low. Firm break there will resume larger down trend from 1.4791 to 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365. However, sustained break of 55 D EMA will bring further rise to 1.3927 resistance and above.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. For now, medium term outlook will be neutral at best, until there are signs that the correction has completed, or that a bearish trend reversal is confirmed.

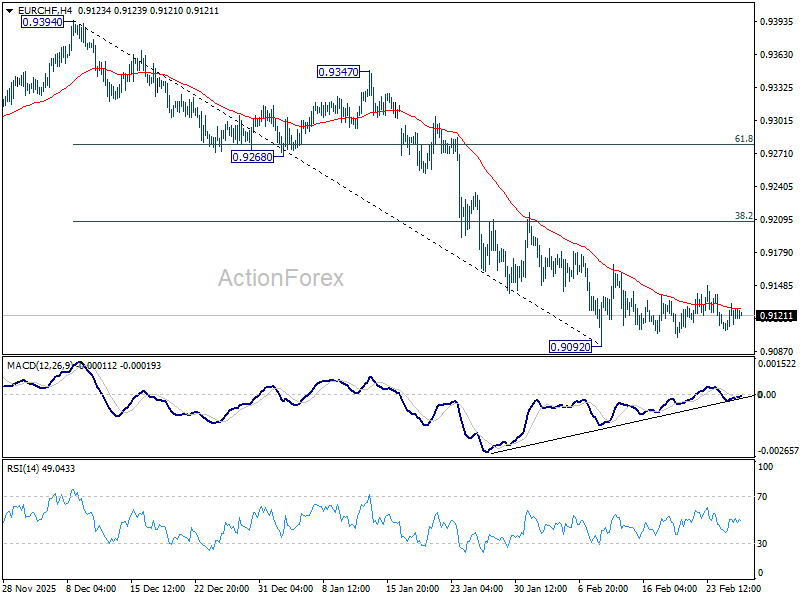

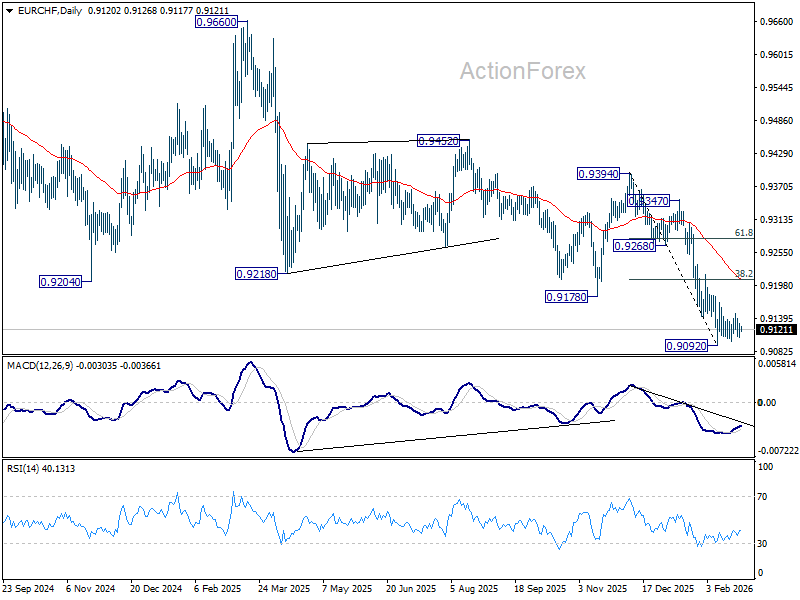

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9112; (P) 0.9122; (R1) 0.9136; More....

Intraday bias in EUR/CHF remains neutral as consolidations continue above 0.9092. Stronger rebound might be seen but upside should be limited by 38.2% retracement of 0.9394 to 0.9092 at 0.9207. On the downside, firm break of 0.9092 will resume larger down trend.

In the bigger picture, down trend from 0.9928 (2024 high) is still in progress with falling 55 W EMA (now at 0.9326) intact. Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Outlook will stay bearish as long as 0.9394 resistance holds, in case of rebound.

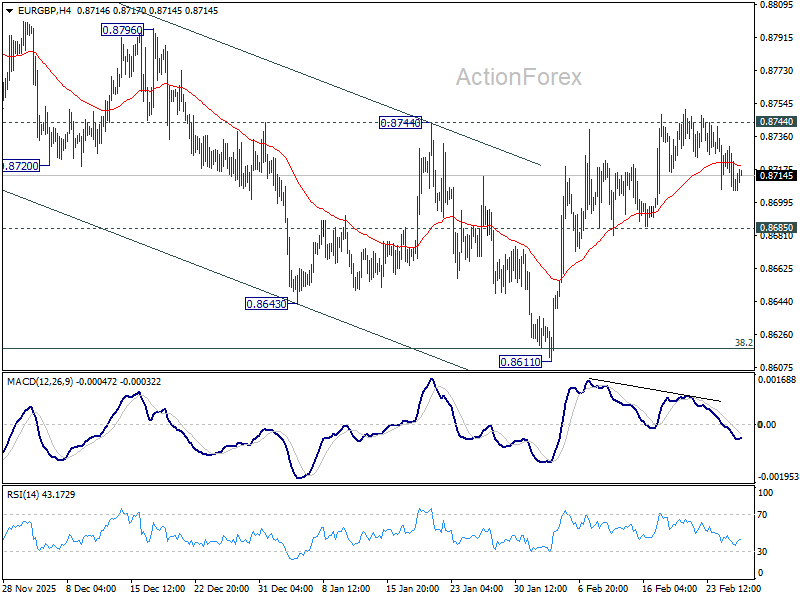

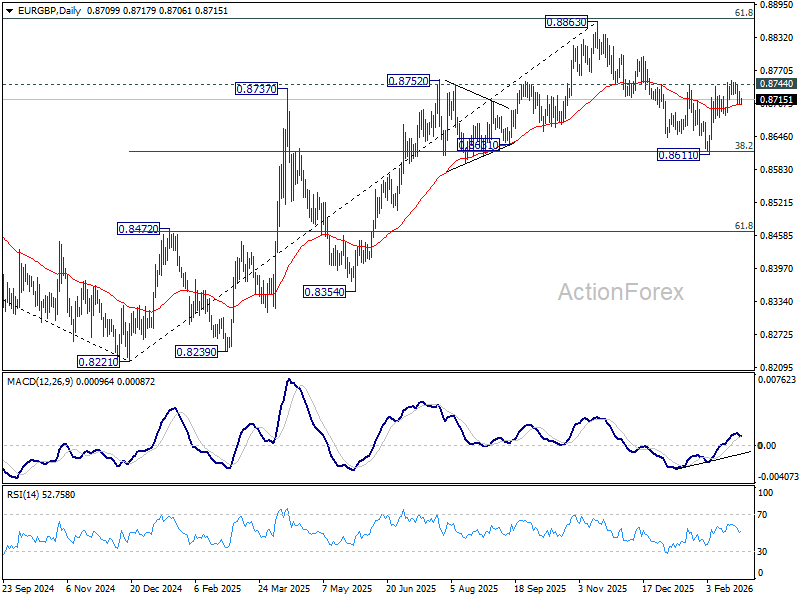

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8701; (P) 0.8717; (R1) 0.8725; More…

Intraday bias in EUR/GBP stays neutral and outlook is unchanged. On the upside, decisive break of 0.8744 resistance. should confirm that fall from 0.8863 has completed as a correction at 0.8661. Further rise should then be seen back to retest 0.8663 high. On the downside, break of 0.8685 support will turn bias back to the downside for 0.8611. Sustained break of 38.2% retracement of 0.8221 to 0.8663 at 0.8618 will carry larger bearish implications and turn outlook bearish.

In the bigger picture, rise from 0.8221 medium term bottom (2024 low) is seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Sustained trading below 55 W EMA (now at 0.8636) should confirm that this corrective bounce has completed. In this case, deeper fall would be seen back to 0.8201/21 key support zone. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high). That should pave the way back to 0.9267.

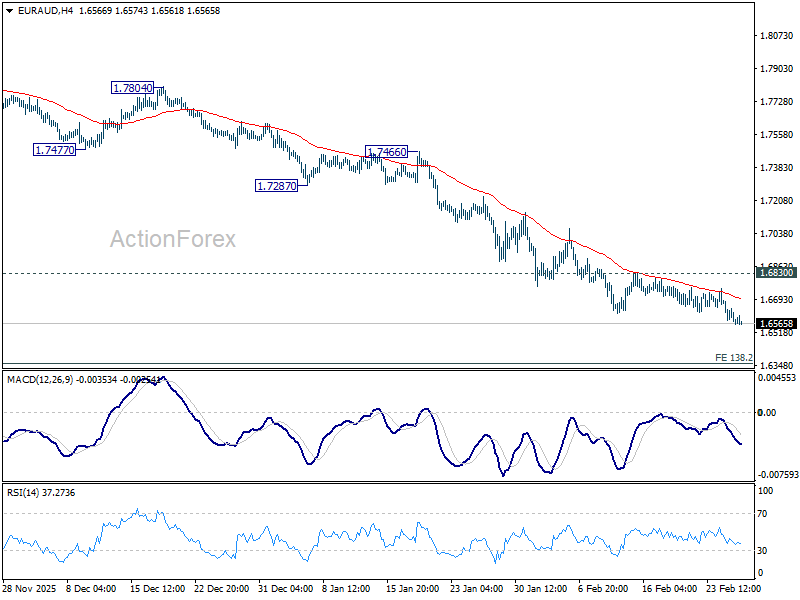

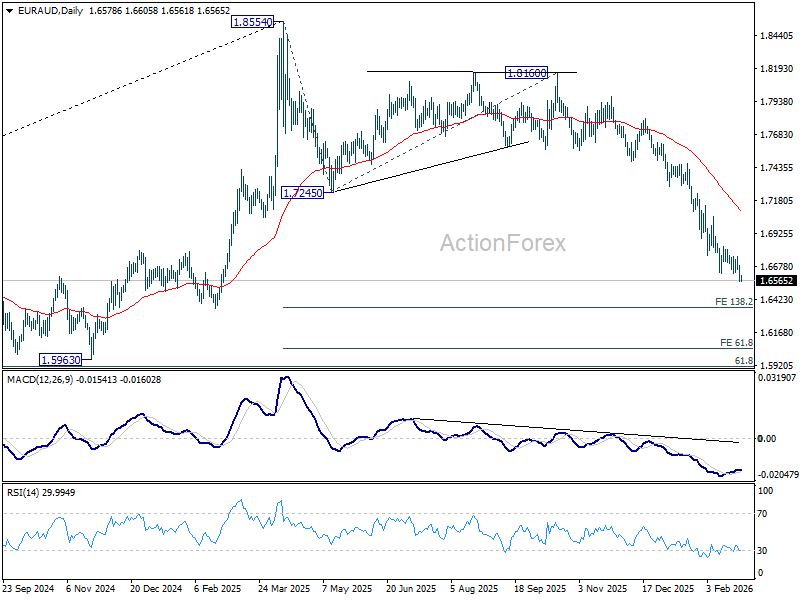

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6536; (P) 1.6612; (R1) 1.6654; More...

Intraday bias in EUR/AUD remains on the downside for the moment. Fall from 1.8554 is in progress and should target 138.2% projection of 1.8554 to 1.7245 from 1.8160 at 1.6351 next. Near term outlook will remain bearish as long as 1.6830 resistance holds, in case of recovery.

In the bigger picture, fall from 1.8554 medium term top is seen as reversing the whole up trend from 1.4281 (2022 low). Deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. For now, risk will stay on the downside as long as 1.7245 support turned resistance holds, even in case of strong rebound.

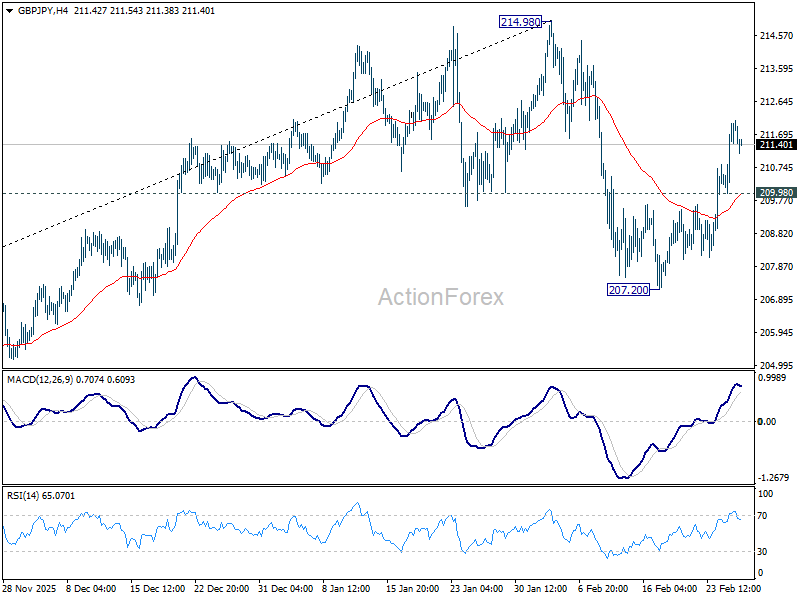

GBP/JPY Daily Outlook

Daily Pivots: (S1) 210.64; (P) 211.38; (R1) 212.76; More...

GBP/JPY's rebound from 207.20 is in progress and intraday bias stays on the upside. Pull back from 214.98 has completed as a near term correction at 207.20. Further rise would be seen to retest 214.98 first. Firm break there will resume larger up trend. On the downside, below 209.98 minor support will turn bias neutral. But risk will stay on the upside as long as 207.20 holds, in case of retreat.

In the bigger picture, current development argues that price actions from 214.98 might be a near term consolidation pattern only. That is, larger up trend from 123.94 (2020 low) is still in progress. Firm break of 214.98 will target 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. On the downside, though, break of 207.20 will revive that case that it's already in a larger scale correction.

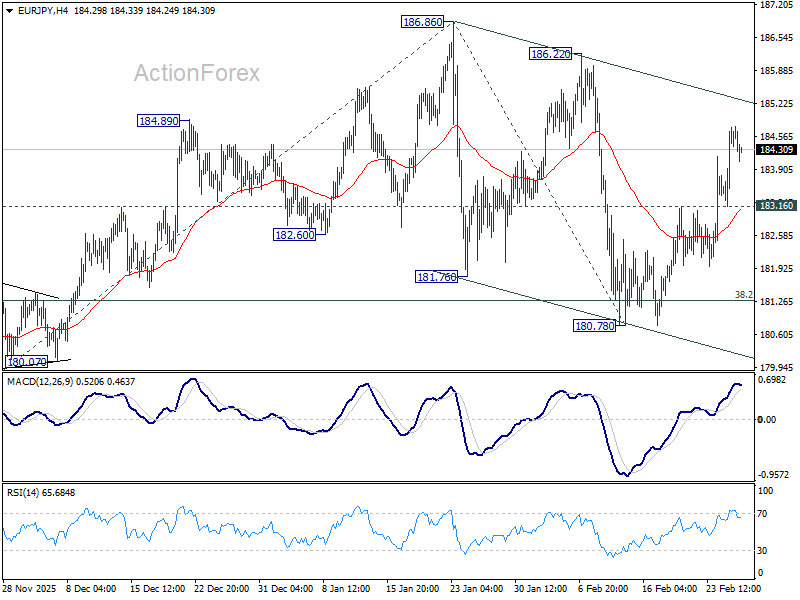

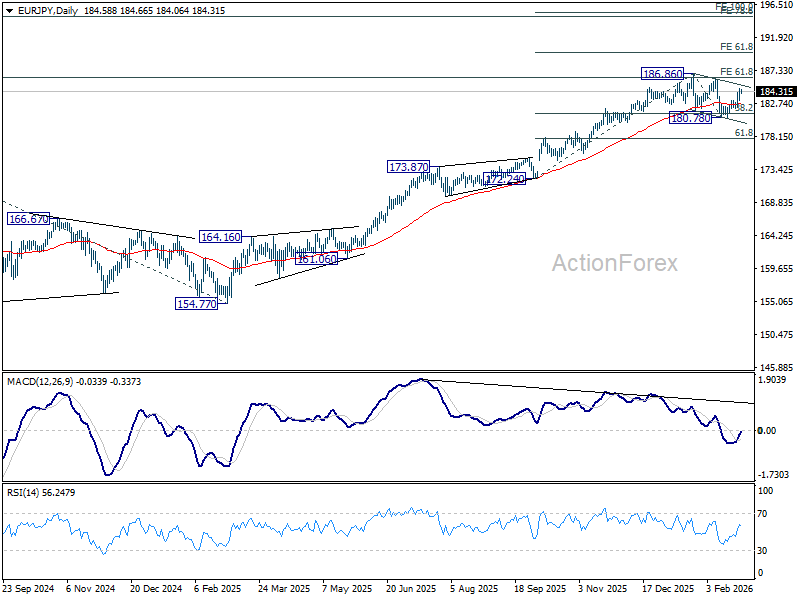

EUR/JPY Daily Outlook

Daily Pivots: (S1) 183.66; (P) 184.22; (R1) 185.24; More...

EUR/JPY's rally from 180.78 is still in progress and intraday bias remains on the upside for 186.22/86 resistance zone. Decisive break there will confirm larger up trend resumption. Next target is 61.8% projection of 172.24 to 186.86 from 180.78 at 189.81. On the downside, below 183.16 minor support will turn intraday bias neutral first. But outlook will remain bullish as long as 38.2% retracement of 172.24 to 186.86 at 181.27, in case of deep retreat.

In the bigger picture, current development suggests that price actions from 186.86 are merely a near term corrective pattern. In other words, the long term up trend is still in progress. Firm break of 186.86 will pave the way to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88 next. This will now remain the favored case as long as 180.78 support holds.

BoJ’s Ueda Talks Tough, But Political Reality Caps Yen Rebound

Yen recovered mildly today following hawkish comments from BoJ Governor Kazuo Ueda, who signaled that the bank will "scrutinize data" at the March and April meetings before making a rate decision. However, gains remain capped as Yen remains the week's laggard. While Ueda explicitly put a March hike on the table, markets suspect this is a verbal intervention to prevent a swift slide toward 160, rather than a definitive policy signal. Two factors support this skepticism:

- Political Friction: The Mainichi reported that PM Sanae Takaichi personally expressed disapproval of immediate hikes to Ueda last week.

- Reflationist Reinforcements: Takaichi has nominated Toichiro Asada and Ayano Sato—both staunch reflationists—to join the board on April 1 and June 30.

Pushing a hike in March would be a massive political gamble. It would be viewed as "front-running" the new board—a preemptive strike to lock in higher rates before Takaichi’s "dovish reinforcements" can take their seats. This would set Ueda on a collision course with a PM who just secured a historic landslide mandate.

Nevertheless, Ueda's comments still put April back as a more "diplomatic" window for the next hike. By then, Ueda can incorporate "Shunto" wage data and involve the first new member, Asada, framing the move as a data-driven consensus rather than a central bank coup.

Meanwhile, Dollar is also soft, weighed down by risk-on mood fueled by Nvidia's blowout earnings. CEO Jensen Huang pushed back on the "AI cannibalization" narrative, arguing that AI agents will not replace enterprise software but will instead use those tools to drive a "new industrial revolution." Equities responded positively, with focus now on whether the strong rebound in NASDAQ Composite and S&P 500 can extend into a range breakout.

Overall for the week so far, Yen remains the worst performer, following by Dollar, and then Loonie. Aussie is staying as the strongest, followed by Sterling, and then Swiss Franc. Euro and Kiwi are positioning in the middle. Overnight, DOW rose 0.63%. S&P 500 rose 0.81%. NASDAQ rose 1.26%. 10-year yield rose 0.015 to 4.048.

BoJ's Ueda signals hike still possible in spring

BoJ Governor Kazuo Ueda signaled that a March or April rate hike remains on the table, stating in a Yomiuri interview that the central bank will continue raising interest rates if economic and price projections evolve as expected. "We will hold a policy meeting in March and April, so we would like to reach a decision by scrutinising data available by then," he said.

Additionally, Ueda noted that the BOJ does not necessarily need to wait for the quarterly Tankan survey release on April 1 to act, as it relies on a range of business and economic indicators. He also also rejected suggestions that the BOJ is behind the curve on inflation, arguing that underlying price pressures have yet to fully reach the 2% target.

Markets had earlier pared back expectations for a near-term hike after reports that Prime Minister Sanae Takaichi expressed reservations about further rate increases. Ueda’s remarks appear to have recalibrated those bets, bringing March and April back into active consideration as the BoJ weighs the impact of December’s hike on lending, investment, and consumption.

Takata says BoJ should consider another “gear shift”

BoJ Board member Hajime Takata said in a speech that overseas risks, particularly around tariff policy, had been a key consideration when evaluating the timing of another rate increase. However, he said initial concerns over those external factors "have abated", clearing part of the uncertainty that had previously restrained policy action.

Domestically, Takata emphasized that Japan’s long-standing "the norm of prices not increasing easily has already been dispelled". Medium- to long-term inflation expectations have risen. Price increases now "have a greater tendency to generate second-round effects". He also cautioned that external shocks could produce greater-than-expected price surges.

Looking ahead, Takata highlighted expectations of a fourth consecutive round of wage increases in 2026, driven largely by base pay gains. In that context, he said the BOJ should prepare for another “gear shift” in policy and communicate under the assumption that the 2% price stability target is nearly achieved.

NZ business confidence falls, wage and price expectations rise

New Zealand’s ANZ Bank Business Confidence index eased from 64.1 to 59.2 in February. However, the Own Activity Outlook edged higher from 51.6 to 52.6, suggesting firms remain broadly optimistic about their near-term operating conditions.

Beneath the surface, inflation pressures appear to be building again. The net percentage of firms expecting to raise prices over the next three months fell 4 points to 53%, partially reversing last month’s surge. Yet cost expectations remain elevated, with 79% of firms anticipating higher costs — the highest level since July 2023.

More notably, one-year inflation expectations rose from 2.77% to 2.93%, their highest level since July 2024. Wage expectations climbed above 3% for the first time since April 2024.

ANZ noted that pricing intentions are not consistent with widespread expectations of a steady decline in headline inflation this year. Although inflation is projected to return to the target band in Q1 and the RBNZ has expressed confidence in the disinflation path, the survey highlights ongoing upside risks.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 183.66; (P) 184.22; (R1) 185.24; More...

EUR/JPY's rally from 180.78 is still in progress and intraday bias remains on the upside for 186.22/86 resistance zone. Decisive break there will confirm larger up trend resumption. Next target is 61.8% projection of 172.24 to 186.86 from 180.78 at 189.81. On the downside, below 183.16 minor support will turn intraday bias neutral first. But outlook will remain bullish as long as 38.2% retracement of 172.24 to 186.86 at 181.27, in case of deep retreat.

In the bigger picture, current development suggests that price actions from 186.86 are merely a near term corrective pattern. In other words, the long term up trend is still in progress. Firm break of 186.86 will pave the way to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88 next. This will now remain the favored case as long as 180.78 support holds.

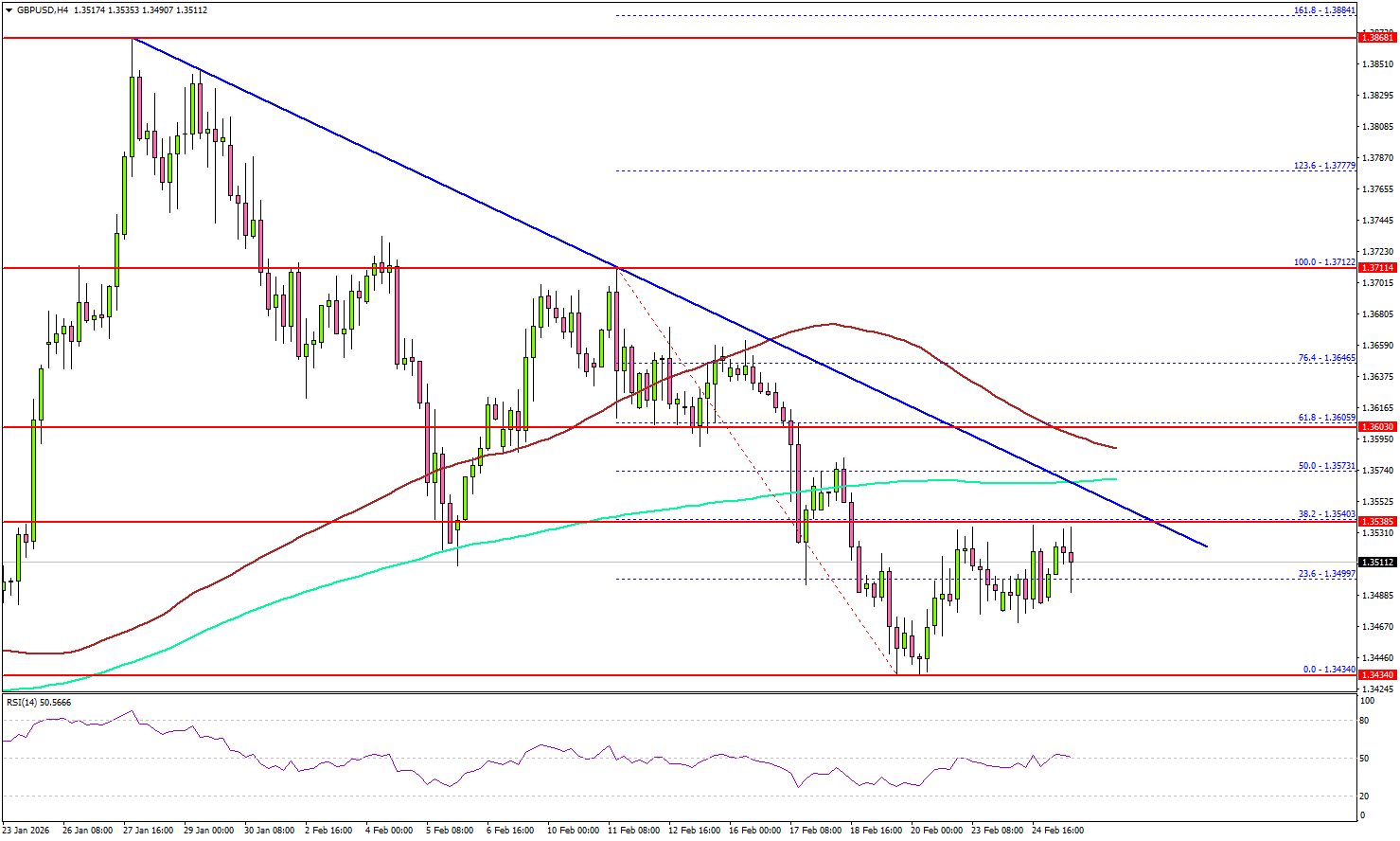

GBP/USD Upside Capped? 1.3550 Emerges as Major Hurdle

Key Highlights

- GBP/USD started a fresh decline from 1.3720 and dipped below 1.3600.

- A key bearish trend line is forming with resistance at 1.3550 on the 4-hour chart.

- Bitcoin recovered some losses and climbed above $68,000.

- Gold could aim for a fresh move toward $5,315.

GBP/USD Technical Analysis

The British Pound failed to settle above 1.3700 against the US Dollar. GBP/USD dipped below 1.3620 and 1.3550 to enter a bearish zone.

Looking at the 4-hour chart, the pair settled below 1.3550, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour) before the bulls appeared near 1.3430. A low was formed at 1.3434, and the pair started a recovery wave.

There was a move above 1.3500, and the 23.6% Fib retracement level of the downward move from the 1.3712 swing high to the 1.3434 low. On the upside, the pair is now facing hurdles near 1.3540.

There is also a key bearish trend line forming with resistance at 1.3550. The next stop for the bulls might be 1.3575 and the 100 simple moving average (red, 4-hour). It is close to the 50% Fib retracement level of the downward move from the 1.3712 swing high to the 1.3434 low.

A close above 1.3575 could open the doors for more gains. In the stated case, the bulls could aim for a move to 1.3600. The main resistance sits near 1.3720.

Immediate support could be 1.3460. The first major area for the bulls might be near 1.3435. The main support sits at 1.3400, below which the pair might gain bearish momentum. In the stated case, it could even revisit 1.3320.

Looking at Gold, the price is again moving higher, and the bulls could soon aim for a move toward the $5,315 resistance.

Upcoming Key Economic Events:

- US Initial Jobless Claims - Forecast 215K, versus 206K previous.

- BoE's Lombardelli speech.