Sample Category Title

Takata says BoJ should consider another “gear shift”

BoJ Board member Hajime Takata said in a speech that overseas risks, particularly around tariff policy, had been a key consideration when evaluating the timing of another rate increase. However, he said initial concerns over those external factors "have abated", clearing part of the uncertainty that had previously restrained policy action.

Domestically, Takata emphasized that Japan’s long-standing "the norm of prices not increasing easily has already been dispelled". Medium- to long-term inflation expectations have risen. Price increases now "have a greater tendency to generate second-round effects". He also cautioned that external shocks could produce greater-than-expected price surges.

Looking ahead, Takata highlighted expectations of a fourth consecutive round of wage increases in 2026, driven largely by base pay gains. In that context, he said the BOJ should prepare for another “gear shift” in policy and communicate under the assumption that the 2% price stability target is nearly achieved.

BoJ’s Ueda signals hike still possible in spring

BoJ Governor Kazuo Ueda signaled that a March or April rate hike remains on the table, stating in a Yomiuri interview that the central bank will continue raising interest rates if economic and price projections evolve as expected. "We will hold a policy meeting in March and April, so we would like to reach a decision by scrutinising data available by then," he said.

Additionally, Ueda noted that the BOJ does not necessarily need to wait for the quarterly Tankan survey release on April 1 to act, as it relies on a range of business and economic indicators. He also also rejected suggestions that the BOJ is behind the curve on inflation, arguing that underlying price pressures have yet to fully reach the 2% target.

Markets had earlier pared back expectations for a near-term hike after reports that Prime Minister Sanae Takaichi expressed reservations about further rate increases. Ueda’s remarks appear to have recalibrated those bets, bringing March and April back into active consideration as the BoJ weighs the impact of December’s hike on lending, investment, and consumption.

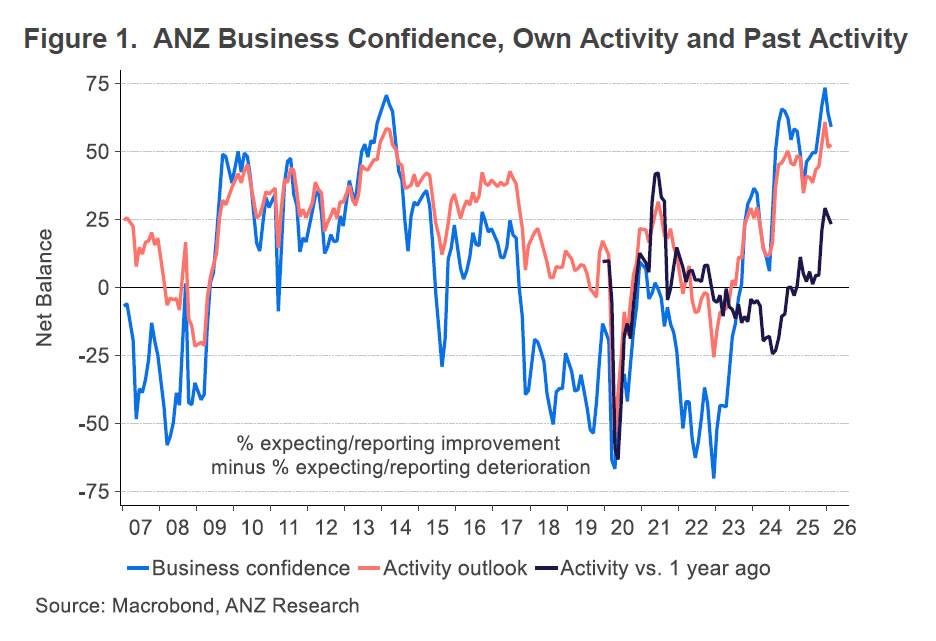

NZ business confidence falls, wage and price expectations rise

New Zealand’s ANZ Business Confidence index eased from 64.1 to 59.2 in February. However, the Own Activity Outlook edged higher from 51.6 to 52.6, suggesting firms remain broadly optimistic about their near-term operating conditions.

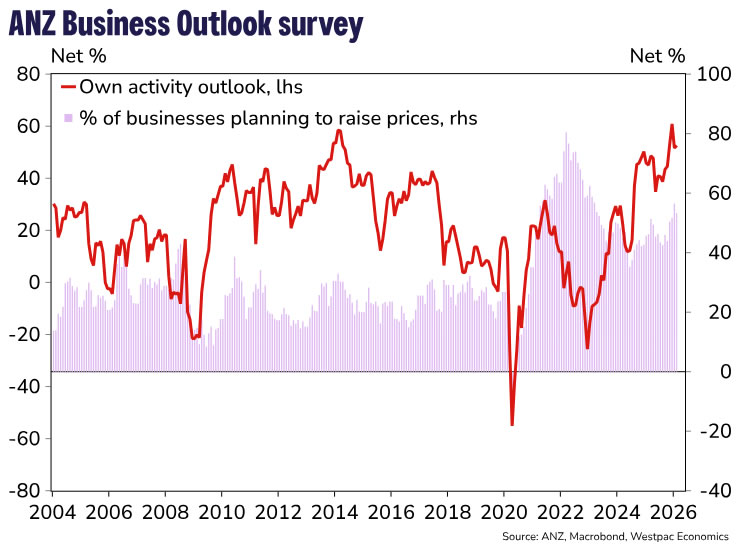

Beneath the surface, inflation pressures appear to be building again. The net percentage of firms expecting to raise prices over the next three months fell 4 points to 53%, partially reversing last month’s surge. Yet cost expectations remain elevated, with 79% of firms anticipating higher costs — the highest level since July 2023.

More notably, one-year inflation expectations rose from 2.77% to 2.93%, their highest level since July 2024. Wage expectations climbed above 3% for the first time since April 2024.

ANZ noted that pricing intentions are not consistent with widespread expectations of a steady decline in headline inflation this year. Although inflation is projected to return to the target band in Q1 and the RBNZ has expressed confidence in the disinflation path, the survey highlights ongoing upside risks.

First Impressions: NZ Business Confidence, February 2026

Business confidence dipped in February, though it remains at high levels. The recent signs of improvement in the economy have also come with the spectre of inflation and higher interest rates.

Key results, February 2026

- Business confidence: 59.2 (Prev: 64.1)

- Expectations for own trading activity: 52.6 (Prev: 51.6)

- Activity vs same month one year ago: 23.4 (Prev: 26.2)

- Inflation expectations: 2.93% (Prev: 2.77%)

- Pricing intentions: 53.3 (Prev: 56.5)

The ANZ business outlook survey for February showed a softening in confidence among New Zealand businesses. Given that confidence had already been running at a high level throughout 2025, the developments in the economy so far in 2026 have in a sense been unwelcome ones: signs that inflation pressures are re-emerging, and an increasingly clear message that the next move in interest rates will be up.

Confidence in the general outlook fell from 64 in January to 59 in February. Firms’ own-activity expectations did rise slightly, but the more detailed activity indicators (employment, investment, profits) were generally a bit lower.

A net 23% of firms reported that their activity was up on the same time last year. While this measure was also lower compared to February, it has largely held on to the gains that we saw in late 2025.

Perceptions about the ease of credit have fallen sharply in the last two months, and are at their lowest since July 2024. The RBNZ’s November Monetary Policy Statement, which signalled that OCR cuts were likely at an end, was followed by a sharp rise in term interest rates as the market began to consider the likely timing of rate hikes.

The inflation gauges in the survey were mixed. Expectations for inflation in the year ahead rose from 2.77% to 2.93%, the highest since July 2024. This measure typically responds to the last quarterly inflation print – in this case a higher-than-expected 3.1%yr, taking it outside the RBNZ’s target range. In contrast, firms’ own pricing intentions dropped back a little, albeit having reached a three-year high in January.

Interestingly, expected wage growth for the year ahead rose from 2.8% to 3.0%, the highest since April 2024. However, reported wage growth over the past year slowed from 2.8% to 2.5%. The wage questions are a relatively recent addition to the survey (from March 2022), so we don’t have a clear sense yet of how well they predict the official wages data. However, any evidence of rising wage pressures would be concerning for the RBNZ at this point, given its view that there will be a significant amount of slack in the labour market for some time to come.

Gold (XAU/USD) Bulls Eye Acceptance Above $5200/oz, Can NVIDIA Earnings Impact Haven Demand?

- Gold (XAU/USD) is trading above $5200/oz, fueled by geopolitical risks, trade uncertainty, and rising rate cut expectations.

- NVIDIA's upcoming earnings report is a critical sentiment test that could either increase safe-haven demand for gold or temporarily halt its rally.

- The technical outlook is bullish, aiming for $5300.

The price of gold has breached the $5200/oz handle with bulls eyeing acceptance above this level before further gains are possible.

The main drivers for Gold remain the Geopolitical risks as the US and Iran are set for another round of talks in Geneva tomorrow. This coupled with trade uncertainty and rising rate cut bets are forming the perfect cocktail for Gold bulls to seize the initiative.

OAU Share CFDs on MT5

State of the Union Speech

President Trump struck a hawkish tone in his State of the Union address. The President said that the economy is faring well and that the US is living in a golden age. He went further stating that lower interest rates will solve the housing problem, inflation is falling, wages rising and that the economy is roaring like never before.

Of course some of these claims may require a more critical look as we have become accustomed to President Trump making bold claims that at times do not pass a critical examination.

Regarding talks with Iran, the President made another bold claim that likely raised haven demand as he stated the Iranian Government is working on missiles that could reach the United States.

Detractors were quick to point out that this rhetoric was used to justify regime change operations in the past only for them to be proven false such as the case with Iraq in 2003 and Libya in 2011.

Either way, markets are on edge as the potential fallout from a US-Iran conflict could be huge as Tehran has threatened neighboring countries such as Jordan, the UAE and Saudi Arabia of strikes should they aid any US assault.

US dollar index retreats, aiding the Gold rally

The US Dollar index had been on a rally which appears to have run out of steam today. A host of US policymakers issued remarks today but rate cut expectations persist.

Kansas City Fed Jeffrey Schmid said that the Fed has work to do on inflation. However the dollar remained under selling pressure.

US Dollar Index (DXY) Daily Chart, February 25, 2026

Source: TradingView

After the US market closes today NVIDIA will be reporting earnings. This is a huge test for AI and valuations and one that could have a huge impact on sentiment.

A poor earnings report could lead to further safe haven demand and thus lead Gold higher. A positive release should see safe haven demand falter, at least temporarily and could lead to a drop off in gold prices.

The biggest data release this week from the US will come on Friday with the release of the PPI data. This could provide another glimpse into inflationary pressure that may hit consumers down the line and impact rate cut expectations.

Technical Outlook - Gold (XAU/USD)

From a technical standpoint, Gold is currently maintaining a bullish trajectory, but its continued upward momentum hinges on buyers' ability to gain acceptance above the $5200/oz handle.

If bulls are able to gain acceptance above this level the next challenge will be to break through this week’s resistance at $5,249/oz. Successfully clearing this threshold would preserve the current "higher highs and higher lows" market structure, potentially sparking a rally toward the $5,300/oz psychological milestone and the January 30 peak of $5,451/oz.

Conversely, failure to overcome the $5,249/oz barrier could trigger a bearish reversal or retracement.

In this scenario, the first line of defense for the XAU/USD pair sits at $5,150/oz. If that level fails to hold, the price may slide further toward the February 24 low of $5,093/oz.

A critical juncture for Gold and one worth keeping a close watch on.

Gold (XAU/USD) Four-Hour Chart, February 25, 2026

Source: TradingView (click to enlarge)

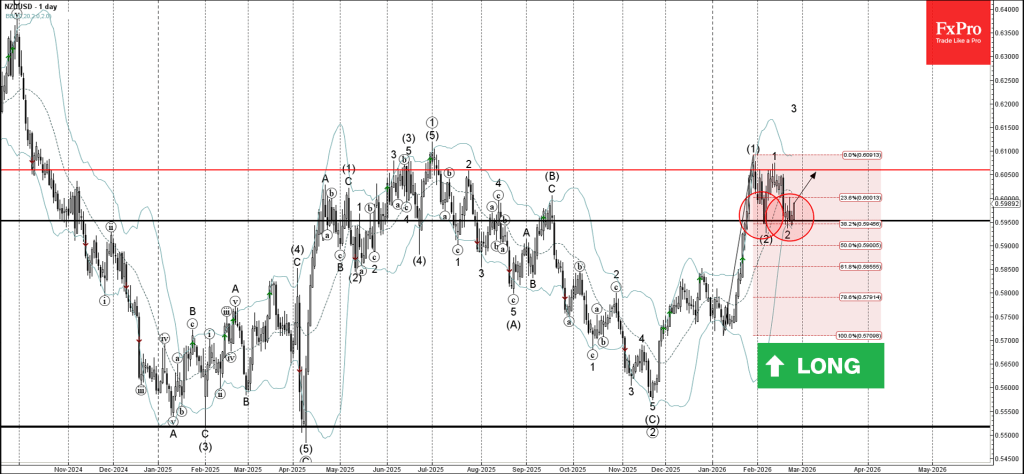

NZDUSD Wave Analysis

NZDUSD: ⬆️ Buy

- NZDUSD reversed from support zone

- Likely to rise to resistance level 0.6060

NZDUSD currency pair recently reversed from the support zone between the support level 0.5950 (which stopped earlier correction (2)) and the lower daily Bollinger Band.

This support zone was further strengthened by the 38.2% Fibonacci correction of the earlier sharp upward impulse from the start of January.

NZDUSD currency pair can then be expected to rise to the next resistance level 0.6060 (which stopped earlier impulse waves 1 and (1)).

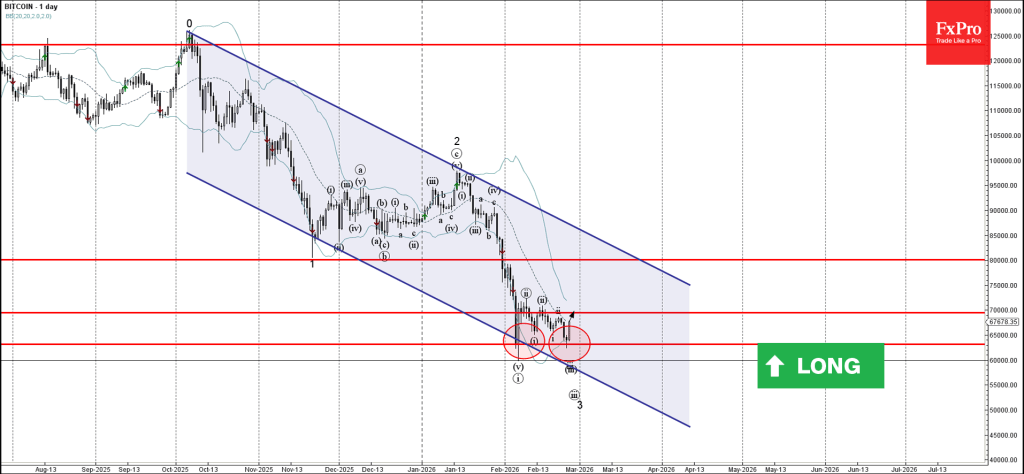

Bitcoin Wave Analysis

Bitcoin: ⬆️ Buy

- Bitcoin reversed from support zone

- Likely to rise to resistance level 70000.00

Bitcoin cryptocurrency recently reversed from the support zone between the support level 63155.00 (which stopped earlier impulse wave i at the start of February) and the lower daily Bollinger Band.

The upward reversal from this support zone is likely to form the daily Japanese candlesticks reversal pattern Morning Star – strong buy signal for Bitcoin.

Bitcoin cryptocurrency can then be expected to rise to the next resistance level 70000.00, that stopped the previous minor correction ii.

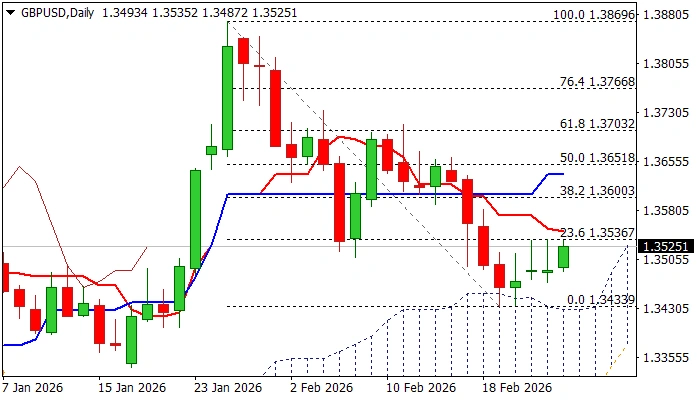

GBP/USD: Recovery Attempts Remain Capped for the Third Straight Day

Cable edged higher on Wednesday and retests the ceiling of near-term range in which the price holds for the third straight day.

Double-Doji candle (Mon/Tue) with longer upper shadows points to indecision, as technical studies remain mixed.

Rising daily Ichimoku cloud (spanned between 1.3428 and 1.3302) underpins, while diverging daily Tenkan/Kijun-sen after creating a bear-cross, pressure.

Solid resistances lay at 1.3536/48 (range top / Fibo 23.6% of 1.2869/1.3433 / falling daily Tenkan-sen) so far limit the upside, with sustained break here needed to generate initial bullish signal and open way for stronger recovery towards 1.3600 (Fibo 38.2%) and 1.3635 (daily Kijun-sen).

Conversely, violation of range floor (1.3470) and more significant 200DMA (1.3443) and daily cloud top (1.3428) would weaken near-term structure and risk continuation of larger downtrend from 1.3869 (Jan 27 top).

Traders also focus on the fundamentals as growing bets that the Bank of England may may opt for 25 basis points rate cut in March (the notion is supported by cooling inflation and improving signals about economic growth) and signals that Fed policymakers’ stance turns more hawkish, would make the dollar more attractive.

In such scenario, Sterling would lose traction against its US counterpart and probably return to broader downtrend (after violating key supports).

Res: 1.3536; 1.3548; 1.3600; 1.3651

Sup: 1.3470; 1.3428; 1.3390; 1.3338

Eco Data 2/26/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 00:00 | NZD | ANZ Business Confidence Feb | 59.2 | 64.1 | ||

| 00:30 | AUD | Private Capital Expenditure Q4 | 0.40% | 0.10% | 6.40% | |

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Jan | 3.30% | 2.90% | 2.80% | |

| 10:00 | EUR | Eurozone Economic Sentiment Feb | 98.3 | 99.8 | 99.4 | 99.3 |

| 10:00 | EUR | Eurozone Industrial Confidence Feb | -7.1 | -6.1 | -6.8 | |

| 10:00 | EUR | Eurozone Services Sentiment Feb | 5 | 7.5 | 7.2 | 6.8 |

| 10:00 | EUR | Eurozone Consumer Confidence Feb F | -12.2 | -12.2 | -12.2 | |

| 13:30 | CAD | Current Account (CAD) Q4 | -0.7B | -8.2B | -9.7B | -5.3B |

| 13:30 | USD | Initial Jobless Claims (Feb 20) | 212K | 211K | 206K | 208K |

| 15:30 | USD | Natural Gas Storage (Feb 20) | -52B | -36B | -144B |

| 00:00 | NZD |

| ANZ Business Confidence Feb | |

| Actual | 59.2 |

| Consensus | |

| Previous | 64.1 |

| 00:30 | AUD |

| Private Capital Expenditure Q4 | |

| Actual | 0.40% |

| Consensus | 0.10% |

| Previous | 6.40% |

| 09:00 | EUR |

| Eurozone M3 Money Supply Y/Y Jan | |

| Actual | 3.30% |

| Consensus | 2.90% |

| Previous | 2.80% |

| 10:00 | EUR |

| Eurozone Economic Sentiment Feb | |

| Actual | 98.3 |

| Consensus | 99.8 |

| Previous | 99.4 |

| Revised | 99.3 |

| 10:00 | EUR |

| Eurozone Industrial Confidence Feb | |

| Actual | -7.1 |

| Consensus | -6.1 |

| Previous | -6.8 |

| 10:00 | EUR |

| Eurozone Services Sentiment Feb | |

| Actual | 5 |

| Consensus | 7.5 |

| Previous | 7.2 |

| Revised | 6.8 |

| 10:00 | EUR |

| Eurozone Consumer Confidence Feb F | |

| Actual | -12.2 |

| Consensus | -12.2 |

| Previous | -12.2 |

| 13:30 | CAD |

| Current Account (CAD) Q4 | |

| Actual | -0.7B |

| Consensus | -8.2B |

| Previous | -9.7B |

| Revised | -5.3B |

| 13:30 | USD |

| Initial Jobless Claims (Feb 20) | |

| Actual | 212K |

| Consensus | 211K |

| Previous | 206K |

| Revised | 208K |

| 15:30 | USD |

| Natural Gas Storage (Feb 20) | |

| Actual | -52B |

| Consensus | -36B |

| Previous | -144B |

Sunset Market Commentary

Markets

US, EMU and UK yields today show a similar (tentative) bottoming pattern after a gradual, but protracted decline over the previous month. With no high profile data or event risk to drive intraday trading, nearby technical and/or psychological references are providing a point of reflection. A new rise in Japanese risk premia this morning maybe contributed to bond investors re-evaluating positions. Japanese yields jumped ( 30-y +7.6 bps) after a period of calm post the parliamentary elections. PM Takaichi recently was reported to ‘push’ the BoJ to be cautious on raising rates. Today, she nominated two new ‘dovish-labeled’ members to the BoJ board. Admittedly, the spill-overs to markets outside Japan were modest (US yield up 1-3 bps, EMU up +/- 1 bp, UK + 1-2 bps). Even so, in a broader perspective, some consolidation after this month’s bond rally makes sense. The US 2-yield since end last month eased from the 3.6 % area to test the October low (3.4% area) end last week. Similar story for the US 10-y yield declining from the 4.3% area to approach the 4% barrier (currently 4.05%). From a technical perspective, the move in UK yields was at least as significant, with the 2-y yield (near 3.60% from 3.77%) and the 10-y (4.33% from 4.6% area early this month) dropping below the 2025 lows. The Fed and the Bank of England are in somewhat of a similar position. Inflation is easing, but confirmation is needed for the both CB’s to further shave the policy rate towards a neutral level. Markets currently assess that it is mainly a matter of timing, not if. Softer labour market data also keep CB’s on alert to avoid unnecessary economic damage. Interestingly, EMU markets joined this broader move (EMU 2-y swap from 2.3% to 2.2%, 10-y from 2.9% to 2.75%) even as the ECB policy rate already trades at what is largely seen as a neutral level. The ECB guides that it is in a good place to assess incoming data and potential upcoming even risk. Still expected sub 2% headline inflation (January today confirmed at 1.7%) causes markets to err to the soft side (a bias we consider premature). The softening at the long end of the curve is a bit less evident. Fiscal risk premia, which often were a driver for curve steeping last year, for now moved a bit to the background. Recently, long term bonds (from time to time) again played a role as safe haven when geopolitical tensions and/or AI risk-off captured market headlines. This comes even as central banks also still have to make up their mind on how to react in case of e.g. higher unemployment due to AI productivity gains. A developing story, for sure. At least today, there was no reason for investors to add bonds due to safe haven considerations. After AI related uncertainty early this week, the EuroStoxx 50 (+0.85%) is setting a new all-time record (6168 area). US indices also open with gains of 0.3% (Dow) and 0.75% (Nasdaq), but haven’t returned to record levels yet. Nvidia results to be published after the US close this evening might be important in a market that is hyper-sensitive to AI-related news. Currency markets still are a bit disconnected for other markets. EUR/USD (1.1775) is holding a tight range in the 1.175/1.185 area. DXY gains marginally (97.95). A sustained break above 98.1 would (slightly) solidify the technical picture. The yen understandably underperforms (USD/JPY 156.7 from 155.9; EUR/JPY 184.55, from 183.55) as the PM Takaichi tries to ‘convince’ the BoJ on its ‘reflationist’ agenda.

News & Views

Czech producer prices fell by 0.7% M/M in January, faster than expected (-0.1%). On an annual basis, prices are 3% lower, coming from -2.1% Y/Y in December (and vs -2.4% Y/Y consensus). Prices of agricultural producers also decreased, by 1.6% M/M and by 5.8% Y/Y. Construction work prices were 0.3% M/M and 2.7% Y/Y higher and service producer prices in the business sphere decreased by 1% M/M to be up 3.6% Y/Y. Czech swap yields fell by 2 to 3 bps across the curve as money markets are still in doubt on the timing of the next rate cut by the Czech National Bank after the hawkish hold early February. The Czeck koruna is unnerved at 24.23.

A new analysis by Embuild Vlaanderen shows that the number of building permit applications for new homes and apartments in Flanders has dropped sharply since 2019. In 2025, only 11,727 applications were submitted—40% less than the nearly 19,600 applications in 2019. This decline continues a multi-year downward trend. The number of potential new housing units in these applications has also fallen significantly: from 73 776 units in 2019 to 41 157 units in 2025. Because not all applications are eventually approved or completed, the number of new homes that actually get built is much smaller. In 2025, according to Statistics Flanders, only 26,500 homes were effectively added. Embuild indicates that the housing shortage will intensify and that 600 000 additional homes will be needed by 2050.