Sample Category Title

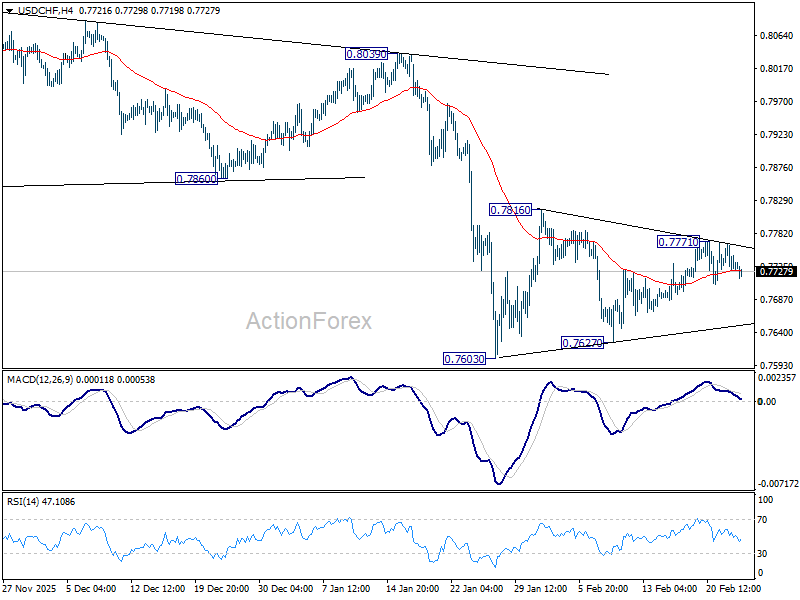

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7727; (P) 0.7746; (R1) 0.7762; More….

Intraday bias in USD/CHF remains neutral for the moment and outlook is unchanged. Consolidation pattern from 0.7603 is still in progress. In case of stronger rise, upside upside should be limited by 55 D EMA (now at 0.7828) to complete the pattern. On the downside, below 0.7627 will bring retest of 0.7603. Firm break there will resume larger down trend, and target 0.7382 projection level next. However, sustained break of 55 D EMA will indicate that a larger scale corrective bounce in underway and target 0.8039 resistance next.

In the bigger picture, down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8123 resistance holds.

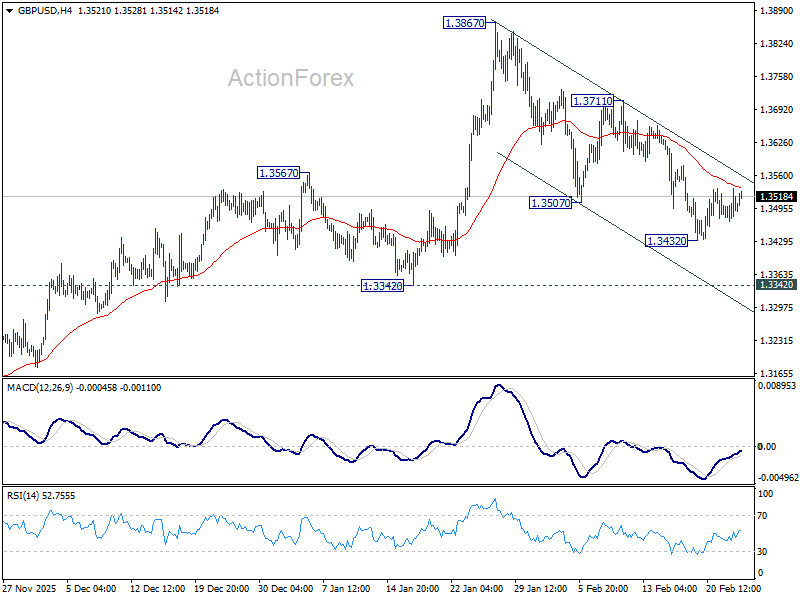

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3460; (P) 1.3498; (R1) 1.3527; More...

Intraday bias in GBP/USD remains neutral for the moment as range trading continues above 1.3432. On the downside, below 1.3432 will resume the fall from 1.3867 to 1.3342 support. Firm break there should confirm that it's already correcting the whole rise from 1.2099. However, break of 1.3711 resistance will argue that the decline has completed as a near term correction, and turn bias back to the upside for retesting 1.3867.

In the bigger picture, as long as 1.3008 support holds, rise from 1.3051 (2022 low) should still be in progress for 1.4284 key resistance (2021 high). Decisive break there will add to the case of long term bullish trend reversal. However, firm break of 1.3008 will raise the chance of medium term bearish reversal and target 1.2099 support next.

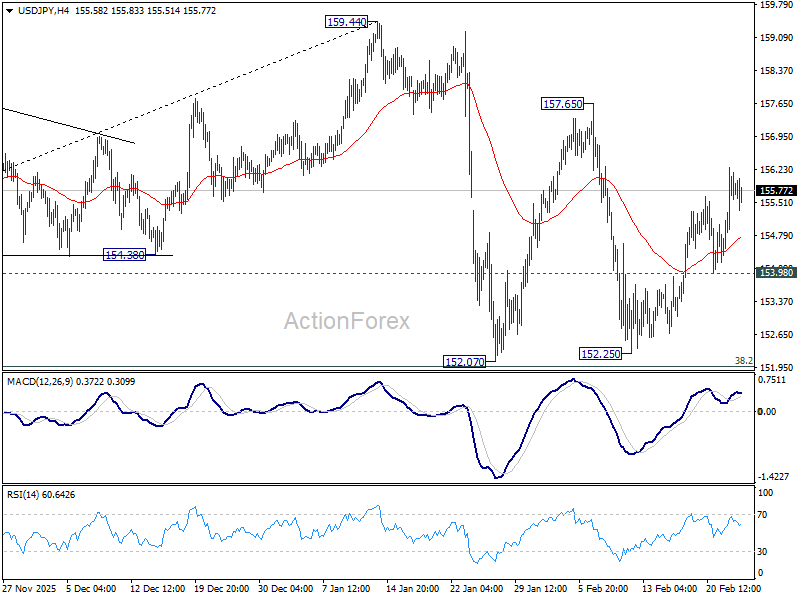

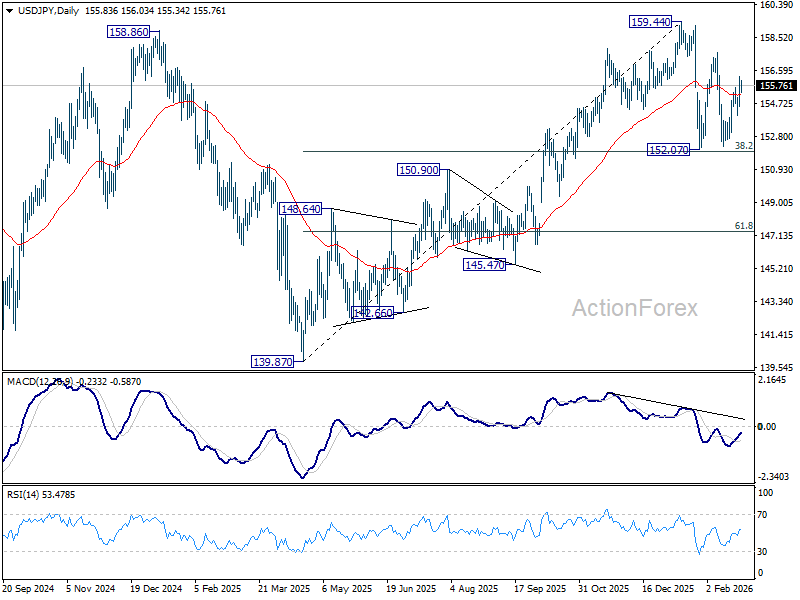

USD/JPY Daily Outlook

Daily Pivots: (S1) 154.86; (P) 155.57; (R1) 156.61; More...

USD/JPY's rise from 152.25 is still in progress and intraday bias remains on the upside for 157.65 resistance. Firm break there will target a retest on 159.44 high. On the downside, below 153.98 minor support will turn intraday bias neutral again first. Overall, with 38.2% retracement of 139.87 to 159.44 at 151.96 intact, price actions from 159.44 are seen as a corrective pattern. Also, rise from 139.87 is expected to resume through 159.44 at a later stage.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 151.93) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

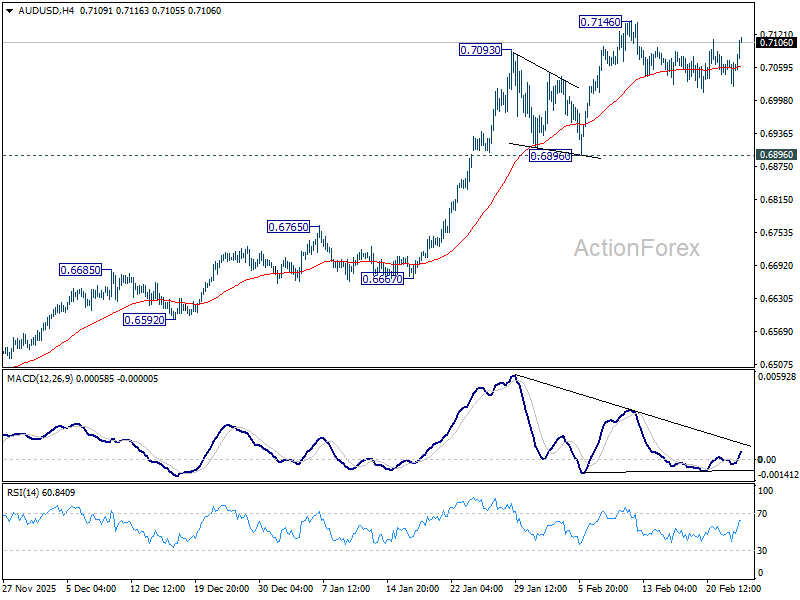

AUD/USD Daily Report

Daily Pivots: (S1) 0.7032; (P) 0.7053; (R1) 0.7079; More...

AUD/USD bounces notably today but stays in range below 0.7146. Intraday bias remains neutral first. Consolidations could continue and deeper retreat cannot be ruled out. But downside should be contained above 0.6896 support. On the upside, above 0.7146 will resume larger up trend to 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Further rally should be seen to 61.8% retracement of 0.8006 to 0.5913 at 0.7206. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.

Tariff Ruling: ST Pain, LT Gain?

The US Supreme Court recently ruled that the Trump administration cannot issue tariffs based on the International Emergency Economic Powers Act. This upends Trump’s current trade policy, as a majority of his tariffs are based on this ruling. The administration has other options. Following the ruling, Trump issued a blanket 15% tariff based on Section 122. As many countries faced higher tariffs than 15% before the ruling, the US effective rate tariff rate dropped from 16% pre-ruling to 13.7% post-ruling. In the future, the administration is likely to use a combination of Section 301 and 232 tariffs to bring tariffs back close to original levels (both require lengthy investigations). Though eventual tariff reimbursements and lower short-term effective tariff rates could provide a boost to the US economy, potential upsides are likely to be outweighed by the negative effects of higher uncertainty. That said, as the ruling constrains this administration and futures ones, US trade policy is likely to become more predictable in the longer run.

On 20 February, the Supreme Court finally issued a ruling in “Learning Resources v Trump”. The case revolved around whether Donald Trump could use the International Emergency Economic Powers Act (IEEPA) to set tariffs. In a 6-3 ruling, the Supreme Court ruled against the use of this law to impose tariffs on other countries. The Court noted that the constitution “gave Congress alone the power to impose tariffs during peacetime” and “did not vest any part of the taxing power to the executive branch”. As IEEPA only allows the president to regulate imports (and does not mention the word tariffs), it thus cannot be used to impose tariffs.

The decision is a blow to Donald Trump’s trade agenda. Most of his tariffs were based on IEEPA. Indeed, according to the Yale Budget Lab, the average effective tariff rate dropped from 16% to 9.1% immediately after the ruling. Though the Supreme Court ruling didn’t include a decision on reimbursements, many businesses will now be able to sue the government for tariff reimbursements. An estimated 175 billion USD was collected through IEEPA and could be reimbursed. These reimbursements, if received, would provide a mild stimulus to the economy, but would also exacerbate US budgetary issues.

Other options: Section 122

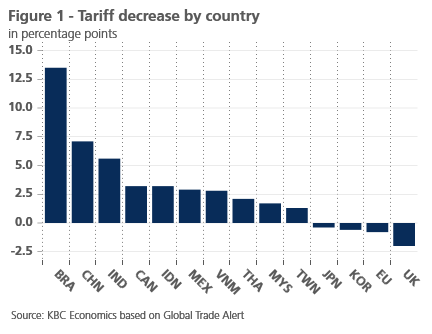

Though the ruling constrains Trump’s trade policies, the president has other options to impose tariffs without the need for congressional approval. He almost immediately invoked Section 122 from the 1974 Trade Act to impose a 10% global tariff. He announced a raise the day later to 15%. Section 122 allows Trump to impose tariffs on all countries to address balance of payments needs or to prevent a significant depreciation of the dollar. Section 122 comes with constraints, however. Congressional approval is needed after 150 days. Furthermore, 15% is the maximum percentage Section 122 allows to charge. As many countries faced higher tariff rates before the ruling, they will be pleased to see their effective tariff rate drop (see figure 1). Some countries such as the UK had faced a lower tariff before and will see a slight tariff increase. The effective tariff rate for the EU will also increase as fewer goods will be exempt from the 15% rate. Overall, as many countries see their tariff rates drop for now, the effective tariff rate falls from 16% before the ruling to 13.7% today.

Next options: Section 301 and 232

Though countries such as Brazil and China will be pleased to see their effective tariff drop, their relief is likely to be short-lived. The US administration is likely to use other options to bring effective tariff rates close to pre-ruling levels. Most likely is the usage of Section 301 from the 1974 Trade Act (which it announced it intends to do on most major trading partners). This allows the Trump administration to impose tariffs on a trading partner that has gained an “unfair advantage.” However, to impose it, a lengthy and cumbersome investigation normally needs to be done. In the first Trump administration, the investigation into China lasted more than six months.

On top of Section 301 tariffs, the administration will continue using Section 232 tariffs from the 162 Trade Expansion Act. These are tariffs that can be used to protect sectors where imports threaten national security (and also need investigations). They are already used for the car industry, steel & aluminum, kitchen cabinets, and upholstered furniture. Other sectors such as semiconductors are under investigation.

Economic consequences

The ruling will have a few economic consequences. First, as we mentioned there could be a mild stimulative boost from the tariff reimbursements. Second, the lower effective tariff will also likely be stimulative to US growth and lower US goods inflation. That said this effect is likely to be small as the effective tariff only declined by 2.3 percentage points. The drop is also likely to be short-lived as new Section 301 and Section 232 tariffs are likely to be imposed in the coming months.

The small positive economic boost from possible tariff reimbursement and temporary lower effective tariff rates is likely to be outweighed by the negative effect of continued trade policy uncertainty caused by this ruling. Indeed, as we argued last year (see Economic Opinion of 10 February 2025), tariff uncertainty can be as damaging as the direct effect of tariffs themselves as the uncertainty deters investment.

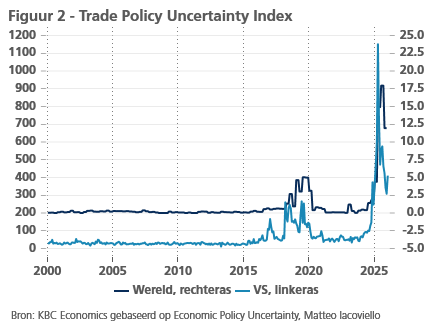

Following Liberation Day, trade uncertainty rose to an unprecedented high (see figure 2). Though it eased since, it remains at very elevated levels. The current ruling will keep uncertainty elevated in the coming months as the administration will gradually announce new Section 301 and Section 232 tariffs and several trade deals will have to be renegotiated.

That said, on the longer run, the Supreme Court’s ruling will lower trade uncertainty. As this administration (and future ones) cannot announce tariff increases on a whim anymore (given the need for investigations in Section 232 and 301), US trade policy is likely to become more predictable. This will eventually give investors some more certainty after a year of erratic trade policy making.

Nvidia’s Earnings Could Impress — But Not Reverse AI Worries

US and European equity markets rebounded yesterday as global investors digested the latest US tariff shake-up and the AI fear trade eased. LegalZoom, for example, which had been heavily hit by fears that Anthropic’s Claude could wipe out its business, jumped 2.5% from its lowest levels on fresh news that Claude unveiled features that could be integrated into the company’s products — making them more customizable and AI‑friendly.

That’s the brighter side of the medal: AI tools can enhance some of these software products — instead of replacing them — potentially helping these companies thrive alongside AI rather than disappear. The iShares Expanded Software ETF rebounded close to 2%.

The software stress is probably not over, but opportunities are clearly emerging.

In the Big Tech space, it was a good day too. Meta announced plans to buy AMD chips — a lot of AMD chips — to deploy up to 6 gigawatts of computing power. One gigawatt is roughly the output of a full-scale nuclear reactor and could power a small city. Meta is talking about the equivalent of six nuclear reactors — just for AI computing. Six gigawatts is enough to power 4–5 million homes. That’s the size of the deal Meta signed with AMD. The deal is worth tens of billions of dollars in revenue for AMD and pushed AMD’s stock price up by nearly 9% yesterday. That’s the good.

The bad is that Meta is spending money against investors’ will and taking on debt — something investors are growing increasingly uncomfortable with: more spending, increasingly on debt.

The ugly is that Meta is receiving warrants that would allow it to buy shares in AMD if the company hits certain performance targets. Meta could ultimately end up owning up to 10% of AMD. Again, the circular nature of AI deals attracts attention. Everybody’s hand is in everybody’s pocket, and if one of the companies stumbles, the whole group — increasingly running on debt — could wobble.

For now, Nvidia and AMD will continue to grow given the hyperscalers’ huge spending plans in AI infrastructure involving chips, despite investors’ reluctance. The risk is, what happens if the big spenders are forced — or decide — to spend less? Could a gap left by Big Tech be filled by smaller spenders? Time will tell. The world is migrating to AI, but the spending increase from outside Big Tech is obviously more granular.

Today, Nvidia will provide clarity on how many chips it sold last quarter and how much it earned. Q4 revenue is projected near ~$65.6–66.1 billion, which would represent nearly 70% year-over-year growth compared with $39.3bn earned in Q4 last year. Note that before the AI boom, this company’s quarterly revenue was around $6–7bn, and growth is expected to continue.

Now, all of this sounds great — but investors won’t just cheer the headline. Last quarter was a good reminder. Nvidia delivered strong top-line numbers, yet the stock didn’t fully ride the wave. Why? Because investors zoomed in on the details — specifically the widening gap between revenue booked and cash actually collected. And that matters in a world of rising leverage and massive AI capex. In this environment, investors don’t just want contracts. They want cash in the door.

So yes — Nvidia has built a track record of meeting and beating expectations in this AI cycle. But this time again, it won’t just be about revenue growth or EPS beats. The devil will be in the details — cash flow, receivables, margins and forward guidance. I’m afraid Nvidia alone may not be able to reverse the fears. Yes, AI spending remains strong, but investors are pulling back — not from Nvidia, but from its biggest clients. Given that hyperscalers make up almost 50% of Nvidia’s client book, the AI stress is likely not over just yet.

Broadly, Nvidia’s results will pretty much mark the end of the earnings season, and the numbers look strong. In Q4 2025, the S&P500 posted 13.2% earnings growth — its fifth consecutive quarter of double-digit earnings growth. Other good news is that the rally has spread to non-tech sectors as well, with the S&P500’s equal-weighted index mostly closing its gap with the tech-heavy, market-cap weighted version.

The S&P 500 looks toppish since the start of the year due to the AI fear trade — both in Big Tech and the software space. The latest AAII investor sentiment index confirms that the bears took the upper hand over the bulls for the first time since November — hinting that much of the selling may already be done. Still, the major US indices need technology to perform well, as the Mag 7 companies make up to a third of the index. Without their help, gains from rotation would be marginal.

Looking at the data, the Conference Board pointed to improved sentiment in February, while Home Depot warned that its customers — middle- and upper-income homeowners — are worried about housing affordability, job stability, and higher financing costs.

Meanwhile, Donald Trump, at the longest State of the Union speech ever, said America is “bigger, better, richer and stronger than ever before. ‘We’re winning so much…’” he added.

Alas, the US dollar weakened in Asia, pushing the EURUSD to the 1.18 level. The USDJPY retraced losses near 156, but Takaichi voiced apprehension regarding further Bank of Japan (BoJ) rate hikes— which could temper the impact of her expansionary fiscal plans aimed at boosting growth — and nominated two reflationist academics to join the BoJ policy board, suggesting that the yen will remain under pressure. Elsewhere, the AUDUSD jumped past 0.71 on stronger-than-expected CPI numbers, reviving Reserve Bank of Australia (RBA) hawks.

Today, euro area CPI figures are expected to confirm softening inflation that could allow the European Central Bank (ECB) to act if trade tensions flare and threaten economies. For now, the Stoxx 600 doesn’t look like it needs any help, trading near an all-time high, supported by stronger-than-expected economic data, and ignoring the fresh tariff uncertainty.

Trump Delivers Longest State of the Union Speech on Record

In focus today

In the euro area, the final January inflation data is released. We expect it to confirm the flash release of 1.7% y/y in headline and 2.2% y/y in core. As there were several changes to taxes in the different euro area countries in January (e.g. German VAT on restaurants) the HICP at constant taxes will shed light on the underlying inflation momentum.

In Norway, wage growth in both 2024 and 2025 exceeded the expected outcome from the central wage negotiations, so the wage statistics is getting more relevant. Today, the January figures will be published, and it will be interesting to see whether wage growth continues to decline into 2026, or whether lower unemployment also starts to lift wage growth. We expect that wage growth declined to below 3.5% y/y in January, but this is mainly due to base effects that will be partially reversed again in February.

In Sweden, although the Producer Price Index is interesting in its own right, especially given recent downside surprises to inflation, it is hardly a market mover and with an otherwise empty macro calendar the main events of the day will be the speeches delivered by the Riksbank's Per Jansson and Erik Thedéen.

Economic and market news

What happened overnight

In the US, Donald Trump's State of the Union speech, which was the longest on record at 1h47mins, touched upon many of past year's key policy issues but was light on actual forward-looking policy signals. He emphasized that US will never allow Iran to gain a nuclear weapon, but said he wants 'to solve the issue with diplomacy'. Trump repeated his earlier claims that he has ended eight wars in 10 months, and that inflation is now coming lower thanks to his policies, referring specifically to lower taxes as well as prices of electricity, health care and eggs. He emphasized that tariffs 'will remain in place' under alternative legal statutes, which do not require congressional action, but refrained from more direct attacks against the Supreme Court. We do not expect the speech to have a significant impact on financial markets, or Republicans' popularity in polling ahead of the midterm elections later in the year.

What happened yesterday

In the US, the Conference Board's consumer confidence measure rebounded modestly in February to 91.2 (cons: 87.0, prior: 89.0), though the indices remain at weak levels. Future expectations recovered, while the current situation assessment weakened further. The widely followed 'jobs plentiful' index also rose modestly, but remains at low levels compared to pre-covid.

ADP's latest weekly private employment growth estimate came in at 12.75k. This is a 4W rolling average until 7 February, up from a revised 11.50k last week. At face value, it suggests strengthening jobs growth momentum, marking the fastest pace of hiring since late November. This is equivalent to a monthly increase of over 50k jobs.

On US monetary policy, Chicago Fed's Goolsbee (non-voter) took a notably hawkish stance, emphasising the need to see clear progress on inflation before supporting further rate cuts. His dissent already in December to hold rates steady underscores his position as one of Fed's most hawkish participants. Atlanta Fed's Bostic (non-voter) highlighted the economy's resilience to last year's trade shocks and current AI-driven growth, supporting a 'mildly restrictive' policy, while cautioning that resurging inflation could warrant rate hikes. Markets are currently pricing a coin flip of a cut in June. However, we expect cooling real growth will prompt the Fed to resume policy easing already in June.

In Hungary, the Central Bank of Hungary cut its Base Rate with 25bp to 6.25%, as widely expected.

Equities: Global equities staged a rebound rally of 0.5% after Monday's sell-off, in what was largely a reversal of Monday's loss, albeit not to the full extend. S&P500 rose 0.8%, with Nasdaq 1% higher and Russell2000 1.2% higher. Stoxx600 was 0.2% higher. As the AI scare was not part of the trading session, IT, Industrials and Consumer discretionary was among the best performing sectors. Overnight, equities are higher in Asia, and US futures are up. Looking specifically at the south Korean Kospi, which is our preferred way to express the AI / tech theme, it is up 2.8% today, adding to the "relentless rally" it has been on this year and is up 45% year to date.

FI and FX: Positive risk sentiment dominated yesterday's session with stronger equities. Movements within foreign exchange and fixed income were relatively modest. European rates initially rallied in a curve flattening but the move reversed later in the day. US rates were roughly unchanged. EUR/USD trades a tad higher this morning at 1.180. In its State of the Union Speech, which was the longest such speech on record at 1 hour and 48 minutes, President Trump declared a booming economy and a "golden age" message at the same time as delivering several combative attacks on Democrats and the Supreme Court. Market reaction was complacent.

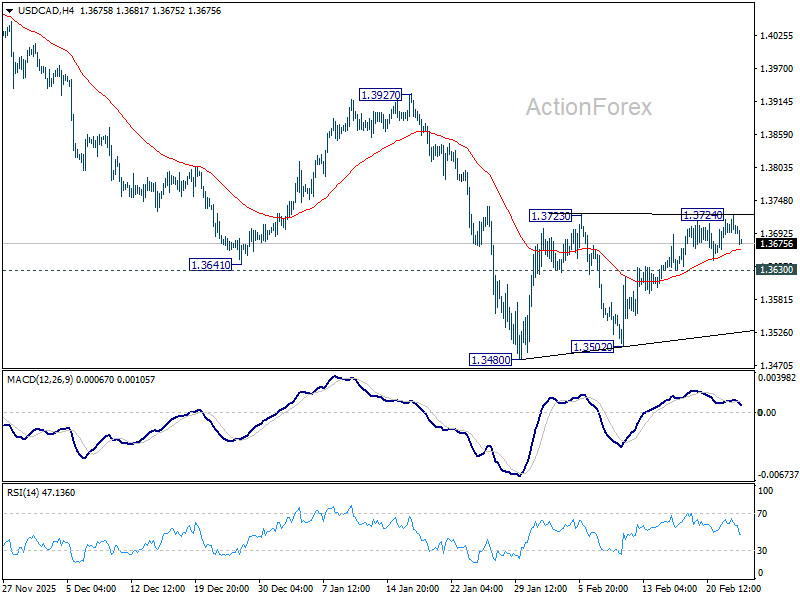

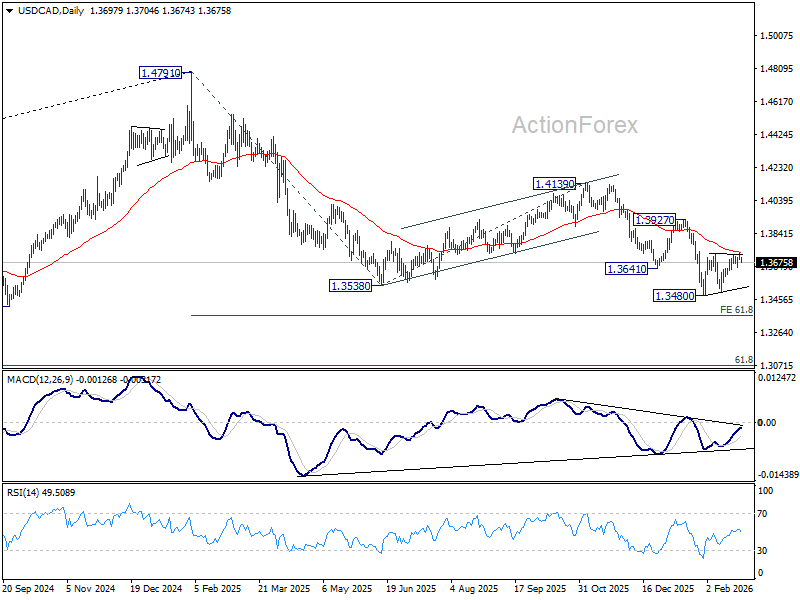

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3686; (P) 1.3705; (R1) 1.3719; More...

USD/CAD edged higher to 1.3724 but quickly retreated. Intraday bias stays neutral for the moment. Consolidations from 1.3480 is in progress and stronger rebound might be seen. But upside should be limited by 55 D EMA (now at 1.3733) to complete the pattern. On the downside, below 1.3630 minor support will bring retest of 1.3480 low. Firm break there will resume larger down trend from 1.4791 to 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365. However, sustained break of 55 D EMA will bring further rise to 1.3927 resistance and above.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. For now, medium term outlook will be neutral at best, until there are signs that the correction has completed, or that a bearish trend reversal is confirmed.

Dollar Slides as Asian Equities Scale Records; Risk Appetite Shrugs Off Tariff and Iran Tensions

Dollar fell broadly again today, pressured by renewed risk appetite as global equities pushed higher. The greenback struggled to attract safe-haven demand despite lingering geopolitical and trade uncertainties, with investors favoring higher-beta currencies instead.

Asian markets set the tone. Both Nikkei 225 and KOSPI hit fresh record highs, tracking the tech-driven rebound in the US overnight. Hardware and AI-linked names continued to draw inflows as dip-buying behavior dominated. The AI disruption theme remains ever-present in markets, but it has yet to spark a durable correction. Instead, volatility episodes are being treated as opportunities to add exposure rather than exit positions.

Trade and geopolitical risks continue to simmer in the background. Tariff uncertainty and elevated tensions with Iran have injected caution, but they have not derailed the broader constructive tone. Risk appetite may be tempered, but it is not reversing. Many analysts now place roughly a 50% probability on a US-led military strike against Iran. That risk has been reflected in higher oil and precious metals prices, yet broader asset classes show limited signs of stress.

Attention now turns to the next round of US-Iran talks in Geneva tomorrow. Diplomatic signals will be closely scrutinized, especially after President Donald Trump reiterated in his State of the Union address that negotiations are ongoing and that he prefers a diplomatic resolution.

On trade, Trump’s remark that tariff revenue could eventually replace federal income tax reinforced the message that tariffs are a structural pillar of his policy agenda. Markets increasingly see tariffs as permanent features rather than temporary tactics.

In currency markets, Aussie led gains, buoyed by improved sentiment and firmer domestic inflation data that strengthens expectations of another rate hike from the RBA in May. Kiwi and Sterling followed, also benefiting from the risk-positive backdrop. In contrast, Dollar languished at the bottom of the performance board, trailed by Loonie and Yen. Euro and Swiss Franc held mid-pack.

In Asia, Nikkei closed up 2.30%. Hong Kong HSI is up 0.42%. China Shanghai SSE is up 0.66%. Singapore Strait TImes is down -0.26%. Japan 10-year JGB yield is up 0.022 at 2.135. Overnight, DOW rose 0.76%. S&P 500 rose 0.77%. NASDAQ rose 1.04%. 10-year yield rose 0.004 to 4.033.

Australia trimmed mean CPI climbs to 3.4%, RBA hike seen inevitable

Australia’s monthly CPI for January came in hotter than expected, reinforcing expectations of further tightening from the RBA. Headline inflation held unchanged at 3.8% yoy, above the 3.7% consensus and marking the joint highest reading since mid-2024.

More concerning for policymakers, trimmed mean CPI rose from 3.3% yoy to 3.4%, also exceeding forecasts and standing at its highest level since Q3 2024. Core inflation has now been at or above 3% since July 2025, remaining clearly outside the RBA’s 2–3% target band.

Housing (+6.8%), food and non-alcoholic beverages (+3.1%), recreation and culture (+3.7%), were the largest contributors to annual price pressures.

Markets had already leaned toward a May rate hike, and today’s data does little to challenge that view. Some economists argue the RBA may be “a little bit behind the curve,” risking a scenario where inflation becomes entrenched and requires more forceful tightening later. With price pressures proving persistent, another rate increase is increasingly viewed as close to inevitable.

CPI supports AUD, but breakout pending; AUD/CAD bullish, GBP/AUD bearish

Australian Dollar strengthened following January’s stronger-than-expected CPI data, but the move has resembled a "steady climb" rather than a "breakout surge". While markets interpreted the firm headline and core readings as reinforcing the hawkish stance of the RBA, positioning remains measured.

One reason is that a May rate hike is already largely priced in. After the RBA’s hawkish increase earlier this month, traders had moved quickly to factor in another step. The latest CPI print confirms that narrative but does not materially extend it. For further upside momentum, markets would likely need to price tightening beyond May. That, however, may depend more heavily on the comprehensive Q1 quarterly inflation report due April, rather than the monthly indicator.

As RBA economic analysis chief Michael Plumb noted yesteday, it will take time to understand the properties and seasonal patterns of the new monthly data. For now, policymakers continue to place greater weight on quarterly measures, limiting the immediate impact of monthly fluctuations.

Global uncertainty also tempers enthusiasm. Ongoing trade tensions, fresh US tariff measures, and persistent US–Iran geopolitical risks act as a natural ceiling for risk-sensitive currencies like the Aussie.

Still, the broader tone for Aussie remains bullish. With inflation holding above target and core measures edging higher, the policy bias is clearly toward further tightening, keeping AUD underpinned on dips.

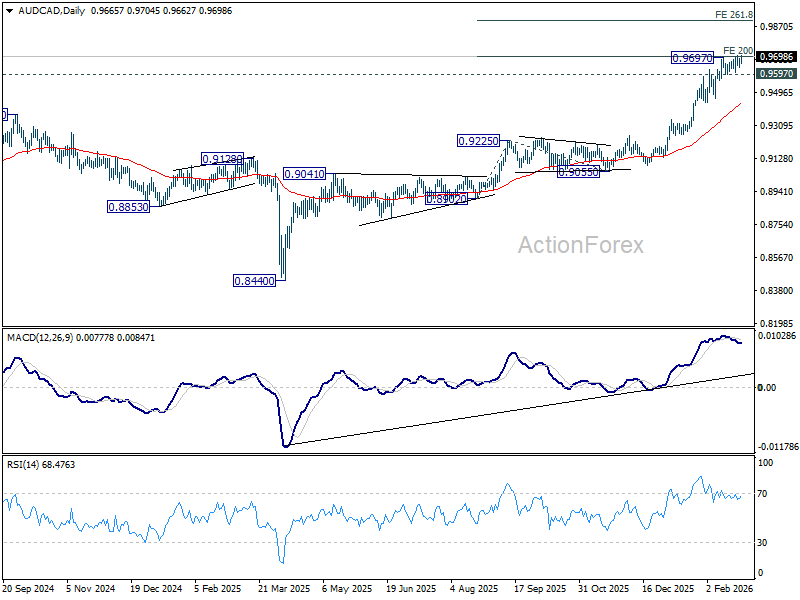

Technically, AUD/CAD has returned to test 0.9697 resistance level with today's bounce. Decisive break would confirm resumption of the broader rally from the 0.8440 (2025 low) and open the way toward 261.8% projection of 0.8902 to 0.9225 from 0.9055 at 0.9901.

However, failure to clear that resistance cleanly could invite consolidation. Break below 0.9597 support would would bring deeper correction to 55 D EMA (now at 0.9439) first.

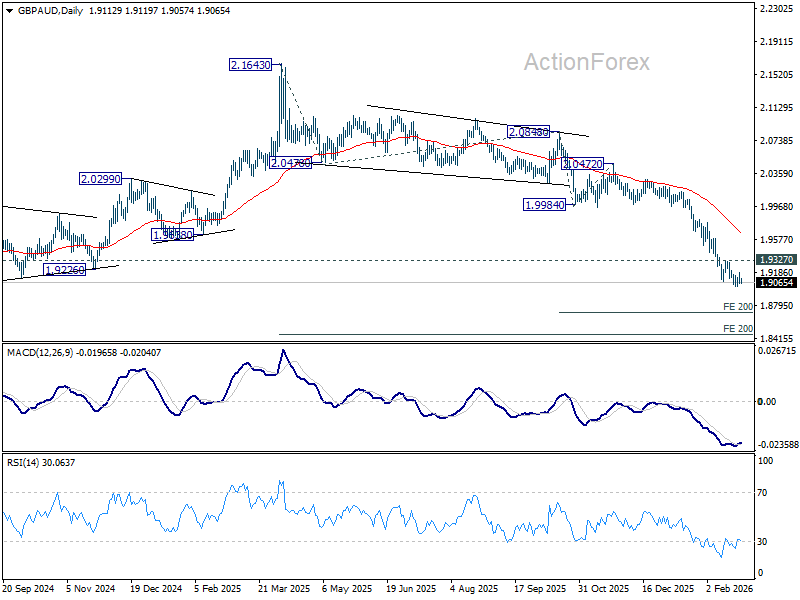

While GBP/AUD shows waning downside momentum as daily MACD divergence emerges, there is no clear sign of bottomg yet. The downtrend from 2.1643 (2025 high) high remains intact, with next target at 200% projection of 2.0848 to 1.9984 from 2.0472 at 1.8744.

However, firm break of 1.9327 resistance will indicate short term bottoming, and bring stronger rebound towards 55 D EMA (now at 1.9674).

Fed's Collins sees mildly restrictive rates on hold “for some time”

Boston Fed President Susan Collins indicated that the Fed is likely to keep interest rates steady “for some time”, pointing to improving labor market conditions and unresolved inflation pressures. In remarks delivered at at event overnight, she said employment data show “at least some more signs” of stability.

Collins argued that after 175 basis points of easing, policy is now only mildly restrictive and may already be close to neutral. Given that backdrop, she said it is “quite likely” the current rate range will remain "appropriate" while officials seek "more evidence" that inflation is firmly moving back toward 2%.

Turning to trade policy, Collins noted that the Supreme Court’s ruling against sweeping tariffs injects fresh uncertainty into the outlook. She warned that if companies have already passed higher import costs through to consumers, those price increases are unlikely to be reversed, potentially keeping inflation elevated.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3686; (P) 1.3705; (R1) 1.3719; More...

USD/CAD edged higher to 1.3724 but quickly retreated. Intraday bias stays neutral for the moment. Consolidations from 1.3480 is in progress and stronger rebound might be seen. But upside should be limited by 55 D EMA (now at 1.3733) to complete the pattern. On the downside, below 1.3630 minor support will bring retest of 1.3480 low. Firm break there will resume larger down trend from 1.4791 to 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365. However, sustained break of 55 D EMA will bring further rise to 1.3927 resistance and above.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. For now, medium term outlook will be neutral at best, until there are signs that the correction has completed, or that a bearish trend reversal is confirmed.

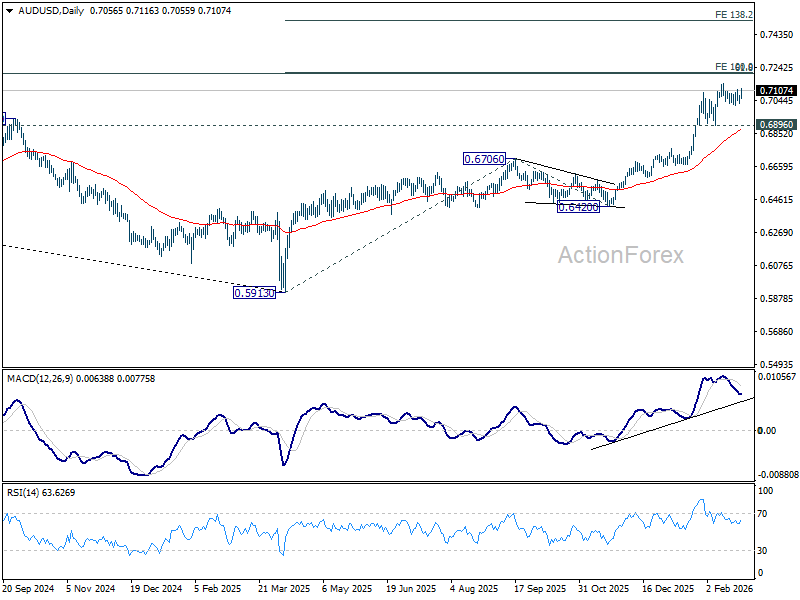

Chart Alert: AUD/USD Bullish Reversal at 20-Day Moving Average, Enroute to 0.7210

Key takeaways

- RBA may maintain hawkish stance: Australia’s core CPI rose to 3.4% y/y in January, above expectations. Markets are now pricing another hike in May, reinforcing a tightening bias.

- Yield spread favours AUD strength: The Australia–US short-term rate spread has widened sharply, supporting further AUD appreciation. The Aussie is already the best-performing major currency YTD, up 5.8% against the US dollar.

- Bullish technical setup intact: AUD/USD has formed a minor bullish base at the 20-day moving average. A break above 0.7110 opens room toward 0.7140–0.7210, while 0.7020 remains key support.

The RBA, Australia’s central bank, was the first developed nation central bank (other than the Bank of Japan) to kickstart a potential interest rate hike cycle, raising its cash policy rate by 25 basis points to 3.85% on 3 February 2026.

The decision marked the first-rate hike since November 2023, underscoring renewed cost pressures that intensified in H2 2025. Today’s hotter-than-expected core CPI data for January, which recorded a 3.4% year-on-year rise versus 3.3% y/y consensus and above December 2025’s print of 3.3%, is likely to strengthen the hawkish vibes in the RBA.

The latest 3.4% y/y print in Australia’s core CPI is the highest since September 2024 and continued to stay “stubbornly” above RBA’s inflation target band of 2-3%.

Short-term interest rate futures in Australia have started to price in a further rate hike by the RBA in May to increase the cash rate to 4.1%.

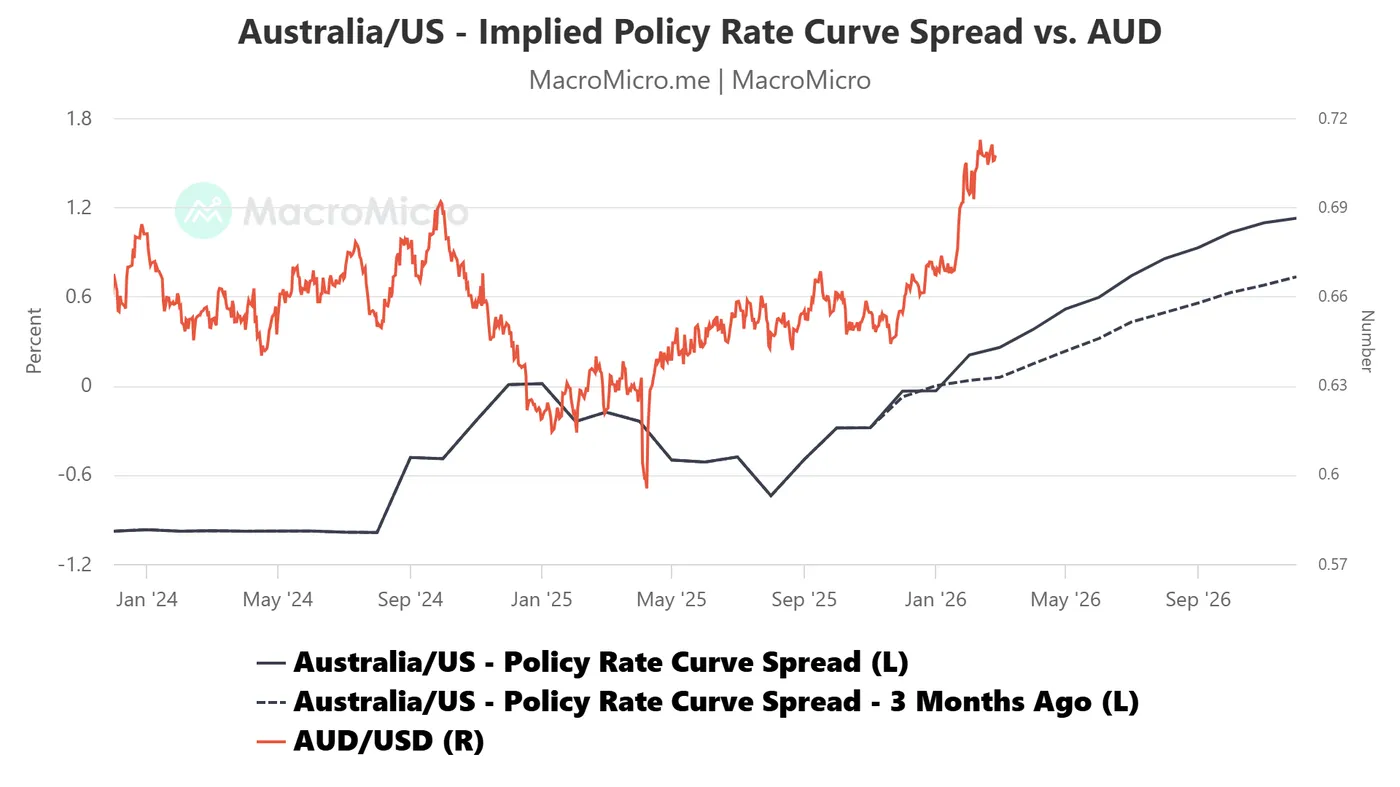

Monthly implied future policy interest rate curves spread suggest a hawkish RBA

Fig. 1: AU/US monthly implied future policy interest rate curves spread as of 25 Feb 2026 (Source: MacroMicro)

In addition, the spread between the monthly implied future policy interest rate curves for Australia and the US (derived from short-term interest rate futures) has risen steadily and shifted upwards (see Fig. 1).

The spread for May 2026 is now at 0.52%, a widening of 29 bps from 0.23% recorded three months ago. The current upward trajectory of Australia’s short-term interest rate premium over the United States’ short-term interest rates is likely to support a further strengthening of the Australian dollar against the greenback, which has a year-to-date positive return of 5.8% as of 25 February 2026 at the time of writing, the best-performing major currency against the US dollar.

Let us now focus on the short-term (1 to 3 days) technical trend and key levels to watch on the AUD/USD.

AUD/USD – Minor bullish basing has formed after a retest on the 20-day MA

Fig. 2: AUD/USD minor trend as of 25 Feb 2026 (Source: TradingView)

The recent retest on the 20-day moving average on 20 February and 24 February has formed a potential minor bullish basing formation for the AUD/USD, with its neckline resistance at 0.7110 (see Fig. 2).

Bullish bias with 0.7035/0.7020 key short-term pivotal support on the AUD/USD. A clearance above 0.7110 sees the next intermediate resistances coming in at 0.7140, 0.7175, and 0.7210.

On the flip side, failure to hold at 0.7020 and an hourly close below it negates the bullish tone to see another round of minor corrective decline sequence unfolding to expose the next intermediate supports at 0.6980 and 0.6907/0.6890.

Key elements to support the bullish bias on AUD/USD

- Minor bullish basing formation at the 20-day moving average.

- The hourly RSI momentum indicator of the AUD/USD has shaped a “higher low” above the 50 level, which suggests a potential resurgence of short-term bullish momentum.