Sample Category Title

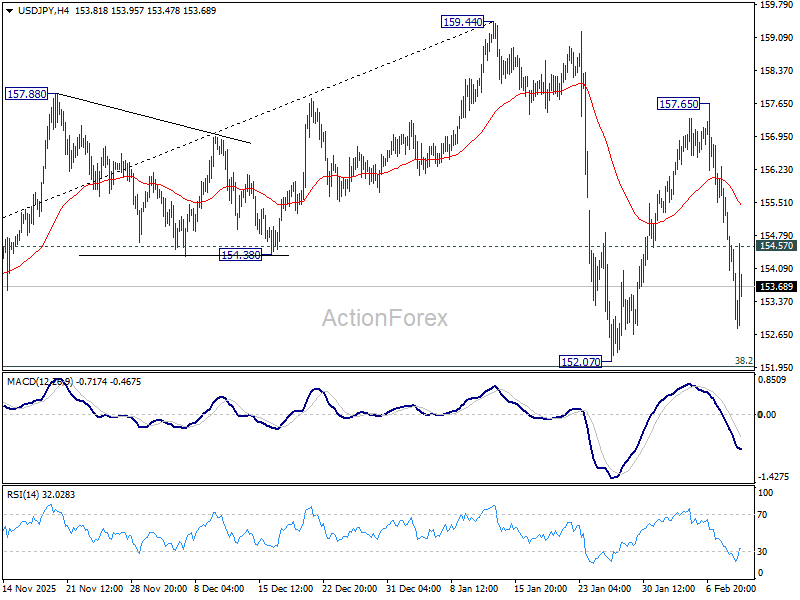

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 153.53; (P) 154.91; (R1) 155.76; More...

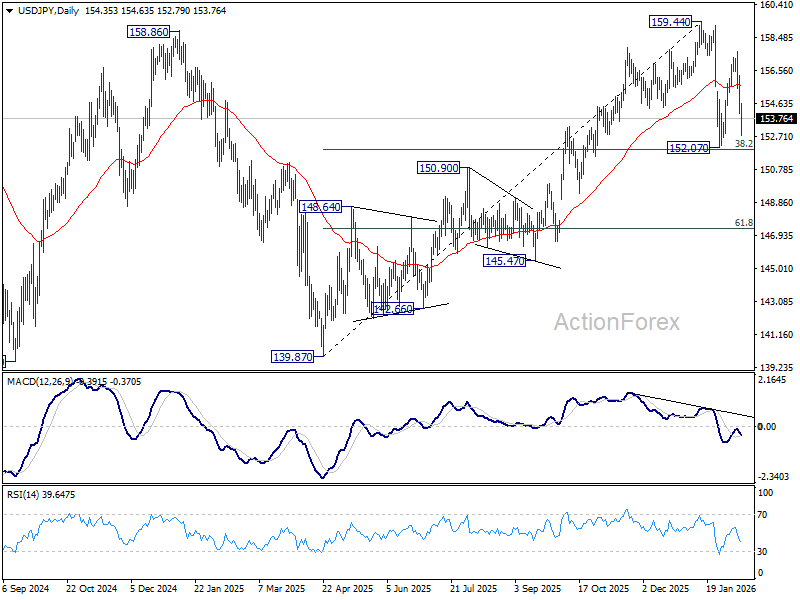

Intraday bias in USD/JPY is turned neutral first with current recovery. As noted before, price actions from 159.44 are seen as a consolidations pattern. In case of another fall, downside should be contained by 38.2% retracement of 139.87 to 159.44 at 151.96 to bring rebound. On the upside, sustained break of 55 4H EMA (now at 155.44) will bring stronger rebound towards 157.65. However, sustained break of 151.96 will argue that it's reversing the rise from 139.87 already.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 151.68) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

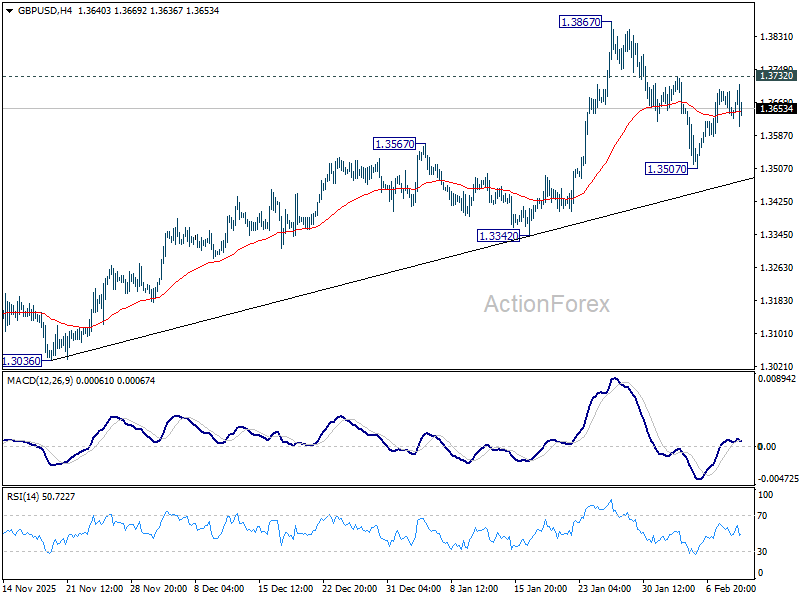

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3621; (P) 1.3660; (R1) 1.3682; More...

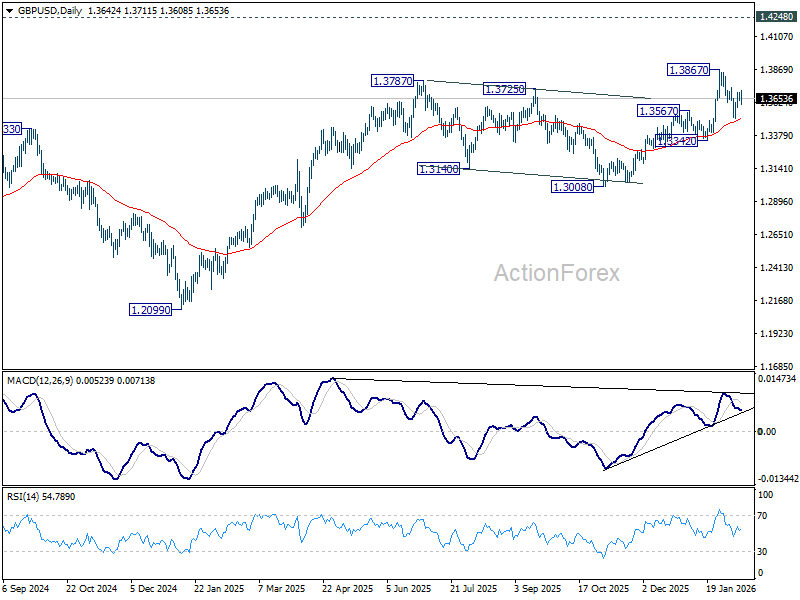

Intraday bias in GBP/USD remains neutral for the moment. On the upside, firm break of 1.3732 resistance will suggest that pullback from 1.3867 has completed as a correction at 1.3507. Retest of 1.3867 should be seen first. Firm break there will resume larger up trend towards 1.4284 key resistance. On the downside, however, sustained trading below 55 D EMA (now at 1.3497) will raise the chance of larger scale correction, and target 1.3342 support for confirmation.

In the bigger picture, rise from 1.0351 (2022 low) is resuming by breaking through 1.3787 high. Further rally should be seen to 1.4284 key resistance (2021 high). Decisive break there will add to the case of long term bullish trend reversal. For now, outlook will stay bullish as long as 1.3008 support holds, even in case of deep pullback.

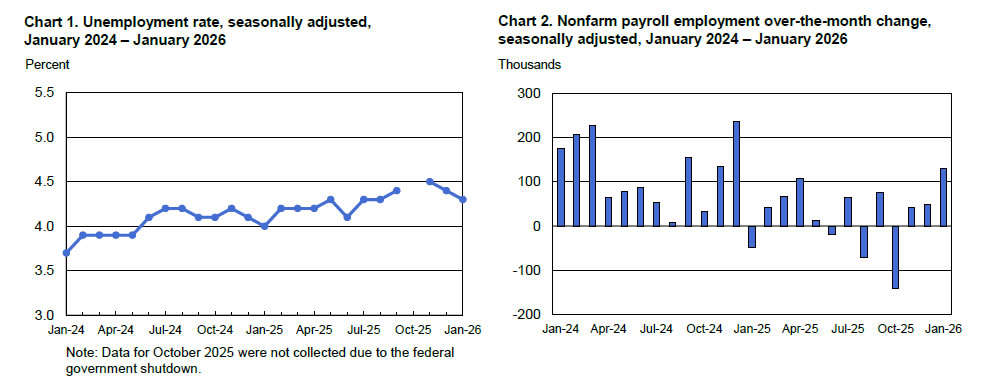

US: Payrolls Turn Meaningfully Higher in January, Unemployment Rate Ticks Down to 4.3%

Non-farm payrolls rose 130k in January, well ahead of the consensus forecast of 65k.

- This morning's release also included more comprehensive benchmark revisions, which are done annually to better align the establishment survey to the observed employment counts reported in tax filing data. The revisions showed that the level of employment as of March 2025 was lower by 898k.

- The Bureau of Labor Statistics also revised its seasonal adjustment factors (dating back to 2021) as well as the birth/death factors used to scale payroll changes up or down depending on the estimated rate of business formation. These revisions showed that payroll growth over the course of 2025 was revised lower by a total of 403k positions, though the bulk of the downward revisions were concentrated in H1-2025. In Q4-2025, payrolls were revised higher by 16k.

Private payrolls rose by a robust 172k in January, well above the 44k averaged over the prior six-month period. The bulk of January's job gains were concentrated in education and health care (+137k), while professional & business services (+34k) and construction (+33k) also chipped in. The federal government shed 34k positions.

In the household survey, a significant increase in civilian employment (+528k) eclipsed a smaller gain in the labor force (+387k), pushing the unemployment rate down a tick to 4.3%. However, the response rate was lower than usual last month because of inclement weather across much of the U.S..

Average hourly earnings (AHE) rose 0.4% month-on-month (m/m), following a smaller gain of 0.1% m/m in December. On a twelve-month basis, AHE held steady at 3.7%.

Key Implications

Well, that was unexpected! Not only did hiring activity turn meaningfully higher in January – with private payrolls rising at its fastest monthly pace in over a year – but the unemployment rate also ticked lower for a second consecutive month.

While we don't want to put too much emphasis on one data point, it would appear that the downside risks to the labor market have receded. Amid a backdrop of still elevated inflationary pressures, the Fed can be patient in its approach to further policy easing. Following this morning's release, Fed futures have pushed out the timing of the next rate cut to July (previously June), while the 10-year yield is up about 6 basis points to 4.2%.

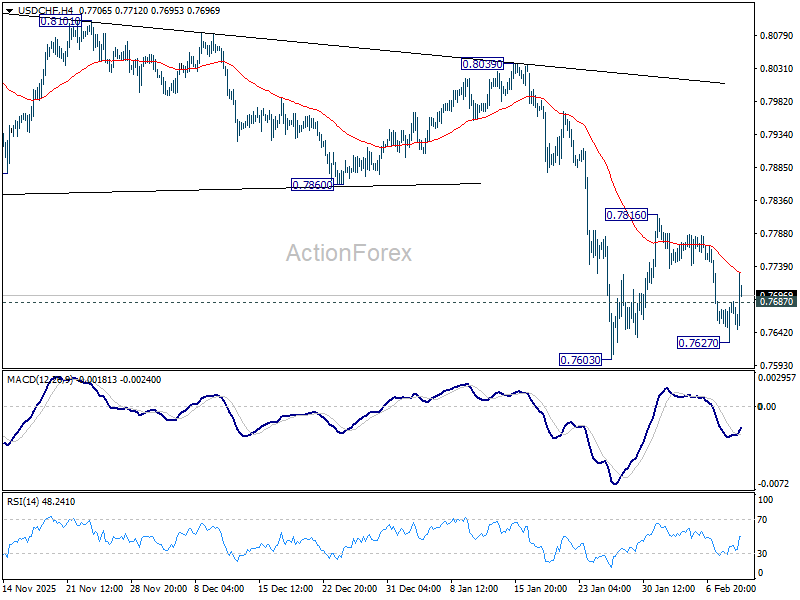

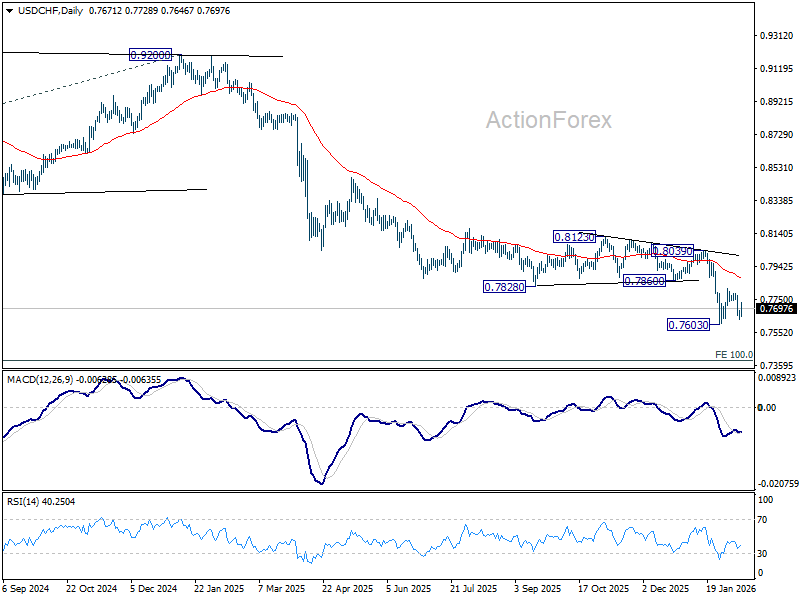

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7645; (P) 0.7666; (R1) 0.7704; More….

USD/CHF's recovery suggests that fall from 0.7816 has completed, and the corrective pattern from 0.7603 is extending with another rising leg. Sustained break of 55 4H EMA (now at 0.7730) will bring stronger rally to 0.7816 resistance. Though, upside should be limited by 55 D EMA (now at 0.7874). On the downside, below 0.7627 will bring retest of 0.7603 low.

In the bigger picture, larger down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8152) holds.

Blowout Payrolls Challenge Dovish Narrative, Dollar Rebounds With Uneven Momentum

January’s highly anticipated US non-farm payroll report delivered a decisive upside surprise, with job growth nearly doubling expectations and marking the strongest monthly gain since mid-2025. The data decisively push back against recent concerns that the labor market was deteriorating rapidly. Rather than rolling over, hiring appears to be regaining momentum at the start of the new year. The report suggests that underlying labour demand remains firm, even after a period of softer monthly gains through much of 2025.

For policy expectations, the message is clear that there is no urgency for the Fed to move again in March. Futures pricing for a rate cut next month dropped toward 5% following the release, effectively taking that meeting off the table. June remains the earliest plausible window for further easing, but that timeline still looks uncertain. Markets will need additional data before confidently reassessing the path beyond the first quarter.

Equities responded swiftly to the stronger tone. DOW futures jumped over 200 points in early trade, hinting that the index's record run could soon resume. S&P 500 may now be preparing for another serious attempt at the 7,000 psychological resistance level. Treasury markets moved in tandem. The 10-year yield rebounded strongly after sliding earlier in the week, though it remains unclear whether the move has sufficient momentum to decisively reclaim the 4.2% mark.

Dollar also firmed broadly following the release, though gains were uneven across major peers. The extent of the rebound will likely hinge on broader risk sentiment; if equities extend higher, risk appetite could limit safe-haven demand for the greenback.

Meanwhile, Europe faces renewed trade friction with China. A French strategy report proposed earlier this week either a 30% across-the-board tariff on Chinese imports or a 30% Euro depreciation versus the renminbi to counter a surge in cheap imports. The report, prepared by the Haut-Commissariat à la Stratégie et au Plan, warned that key sectors such as autos, machine tools, chemicals and batteries are under direct competitive pressure, citing sustained Chinese cost advantages of 30–40% and an “undervalued” currency. China responded sharply, with a social media account affiliated with CCTV warning of reciprocal tariffs, and investigations into French wine.

In currency markets, Yen remains the day’s strongest performer for now, followed by Aussie and Kiwi. Loonie is the weakest, trailed by Euro and Swiss Franc, while Dollar and Sterling sit mid-pack.

In Europe, FTSE is up 0.80%. DAX is down -0.22%. CAC is up 0.09%. UK 10-year yield is down -0.001 at 4.517. Germany 10-year yield is up 0.008 at 2.822. Earlier in Asia, Japan was on holiday. Hong Kong HSI rose 0.31%. China Shanghai SSE rose 0.09%. Singapore Strait Times rose 0.41%.

US NFP beats at 130k, unemployment rate dips to 4.3%

US non-farm payrolls surprised to the upside in January, rising 130k against expectations for just 66k. The gain was also well above the 15k average monthly increase seen through 2025.

Unemployment rate edged down from 4.4% to 4.3%, beating forecasts for no change, while the participation rate ticked up 0.1 percentage point to 62.5%. The combination suggests labor supply and demand both strengthened modestly at the start of the year.

Wage pressures also remained firm. Average hourly earnings rose 0.4% month-on-month, above the 0.3% consensus, with annual wage growth holding at 3.7% yoy. For markets, the report challenges expectations of rapid Fed easing and reinforces the narrative of a labor market that remains resilient.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7645; (P) 0.7666; (R1) 0.7704; More….

USD/CHF's recovery suggests that fall from 0.7816 has completed, and the corrective pattern from 0.7603 is extending with another rising leg. Sustained break of 55 4H EMA (now at 0.7730) will bring stronger rally to 0.7816 resistance. Though, upside should be limited by 55 D EMA (now at 0.7874). On the downside, below 0.7627 will bring retest of 0.7603 low.

In the bigger picture, larger down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8152) holds.

US NFP beats at 130k, unemployment rate dips to 4.3%

US non-farm payrolls surprised to the upside in January, rising 130k against expectations for just 66k. The gain was also well above the 15k average monthly increase seen through 2025.

Unemployment rate edged down from 4.4% to 4.3%, beating forecasts for no change, while the participation rate ticked up 0.1 percentage point to 62.5%. The combination suggests labor supply and demand both strengthened modestly at the start of the year.

Wage pressures also remained firm. Average hourly earnings rose 0.4% month-on-month, above the 0.3% consensus, with annual wage growth holding at 3.7% yoy. For markets, the report challenges expectations of rapid Fed easing and reinforces the narrative of a labor market that remains resilient.

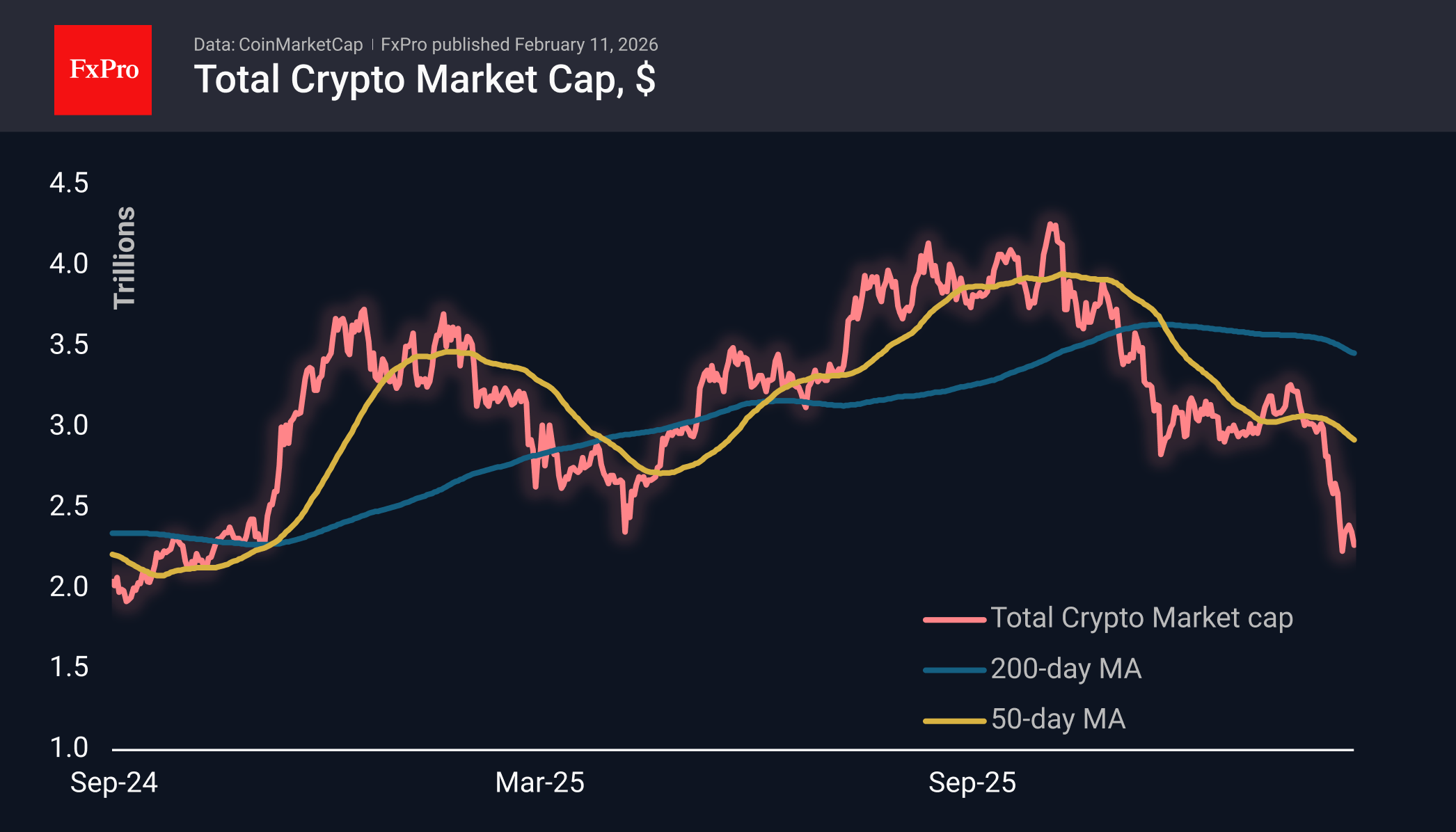

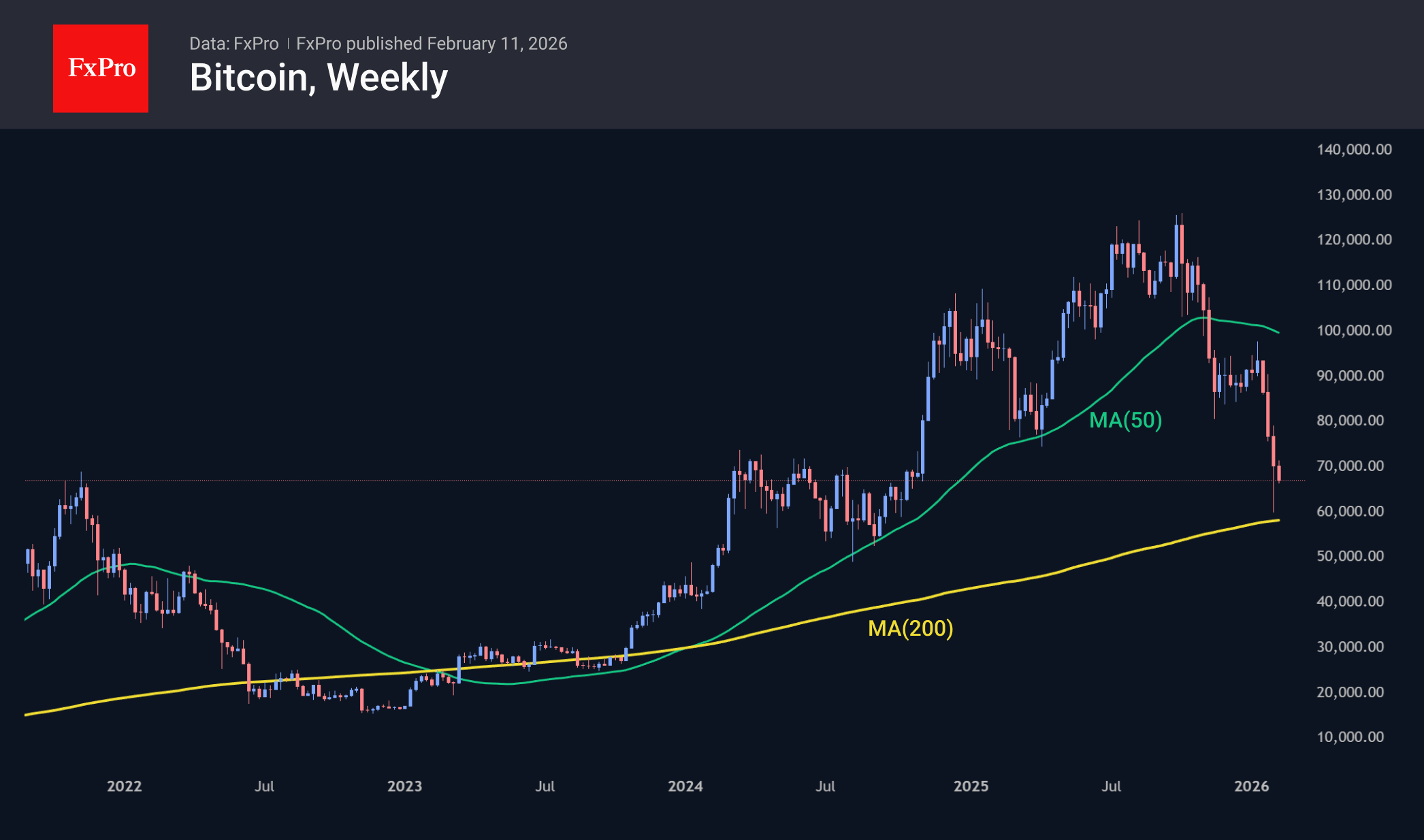

Crypto Market Still Has Significant Downside

Market Overview

The crypto market cap fell 2.5% in 24 hours to $2.27T. The market was below this level for several hours last Friday, the first time in the past year and a half. Trading remained stable in this range from March to November 2024. The rebound is losing momentum, increasing the likelihood of a retest of last Friday’s lows at $2.2T, potentially followed by a further 10% decline toward the $2.0T level.

Bitcoin has fallen below $67K, recording its third daily bearish candle. Of the more than 20% rebound from Friday’s lows, only slightly more than half remains. Excluding extreme slippage during illiquid trading, the next important support area is $63K, followed by $60K (a round level and recent extremes) and $58K, through which the 200-week moving average passes.

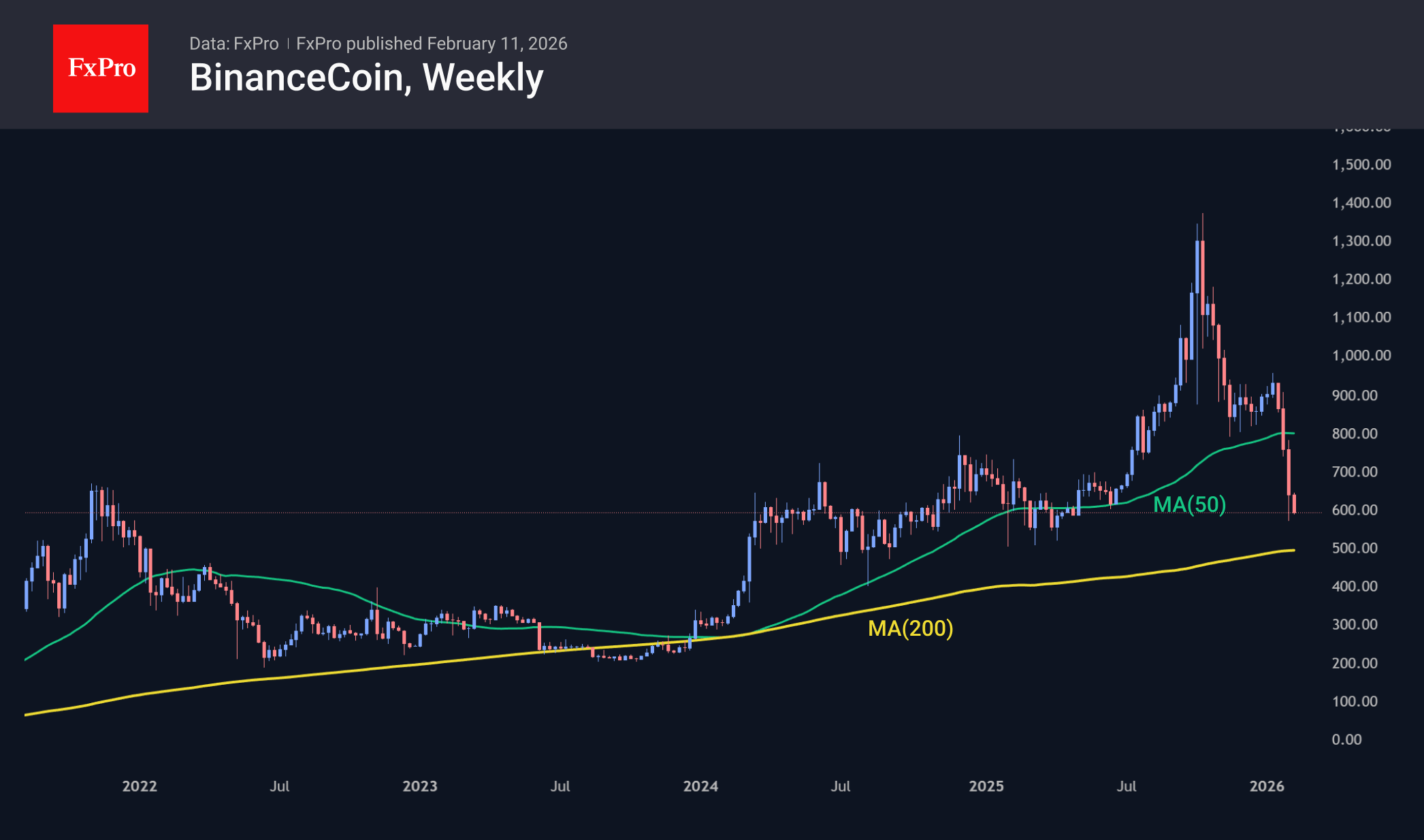

BNB has underperformed the broader market, losing nearly 6% in the last 24 hours and over 21% in seven days, roughly double the rate of decline of BTC and ETH. At levels below $600, this coin found itself in last year’s support area, from where it was actively bought on dips. But the technical situation is bleaker, as in 2025 buyers also found support on dips to the 50-week moving average, but this year bears pushed the price below that line at the end of January, after which we saw a heavy sell-off. This may only be a prelude to another 50% drop to $300.

News Background

According to CoinGlass, the Coinbase Premium index, which tracks the deviation of the BTC price on the US exchange Coinbase from the global average, has rebounded sharply, indicating a return of US investors.

However, there is no clear signal for a trend reversal yet. The Bitcoin futures market points to the likelihood of a further decline in Bitcoin. According to Amberdata, investors have not yet truly capitulated.

BitMine purchased an additional 40,000 ETH worth approximately $83.6 million. The company already owns more than 4.36 million coins and has fulfilled 72% of its plan to accumulate 5% of the ETH market supply.

According to CoinGecko, public DAT companies holding reserves in Solana faced unrealised losses exceeding $1.5 billion. The losses are concentrated among a small group of American firms whose shares have fallen by 59–73% over the past six months. However, the companies are not yet selling their assets.

EUR/CHF: Bears Take a Breather Above New 11-Year Low, Key 0.9000 Support in Focus

EUR/CHF is consolidating under new multi-year low at 0.9094 (the lowest since Jan 2015 when the SNB abandoned its minimum exchange rate policy of 1.20 CHF per Euro) that was hit on Tuesday.

Swiss franc remains well supported on ongoing safe-haven demand and continues to advance against its major peers.

Bears eye key supports at 0.9000 zone (psychological / Jan 2015 spike low) which could be reached soon, as overall environment remains supportive.

Tuesday’s Doji candle with long tail, points to growing bids which may pause larger downtrend for consolidation or possible limited correction, as daily studies are overstretched.

Technical picture remains firmly bearish and suggest that brief breather would mark positioning for fresh push lower.

Falling 10 DMA (0.9152) marks initial resistance, followed by more significant 0.9200 zone (Fibo 38.2% of 0.9289/0.9094 bear-leg / falling 20DMA) which should cap upticks.

Res: 0.9094; 0.9152; 0.9200; 0.9222.

Sup: 0.9116; 0.9094; 0.9050; 0.9000.

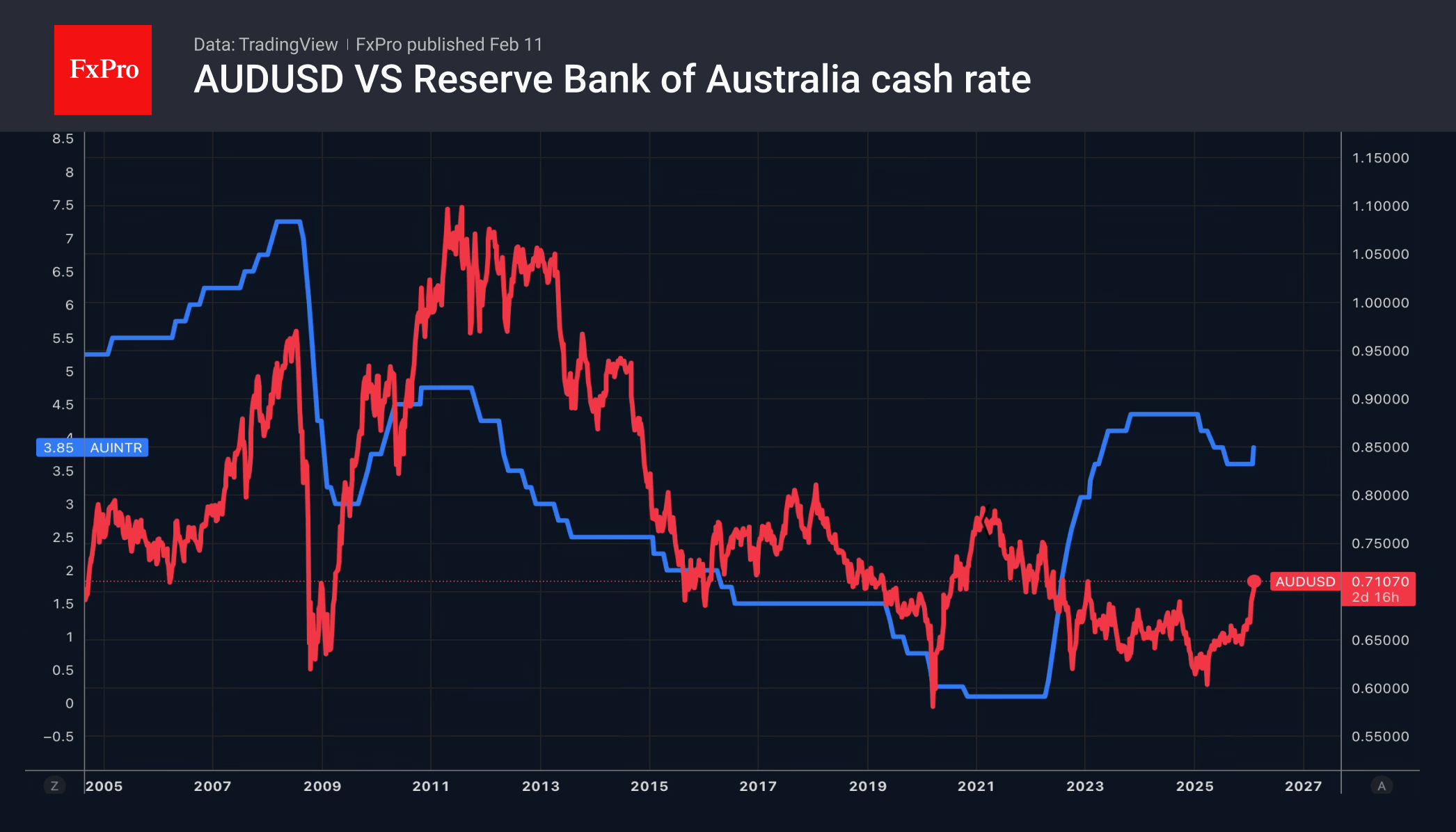

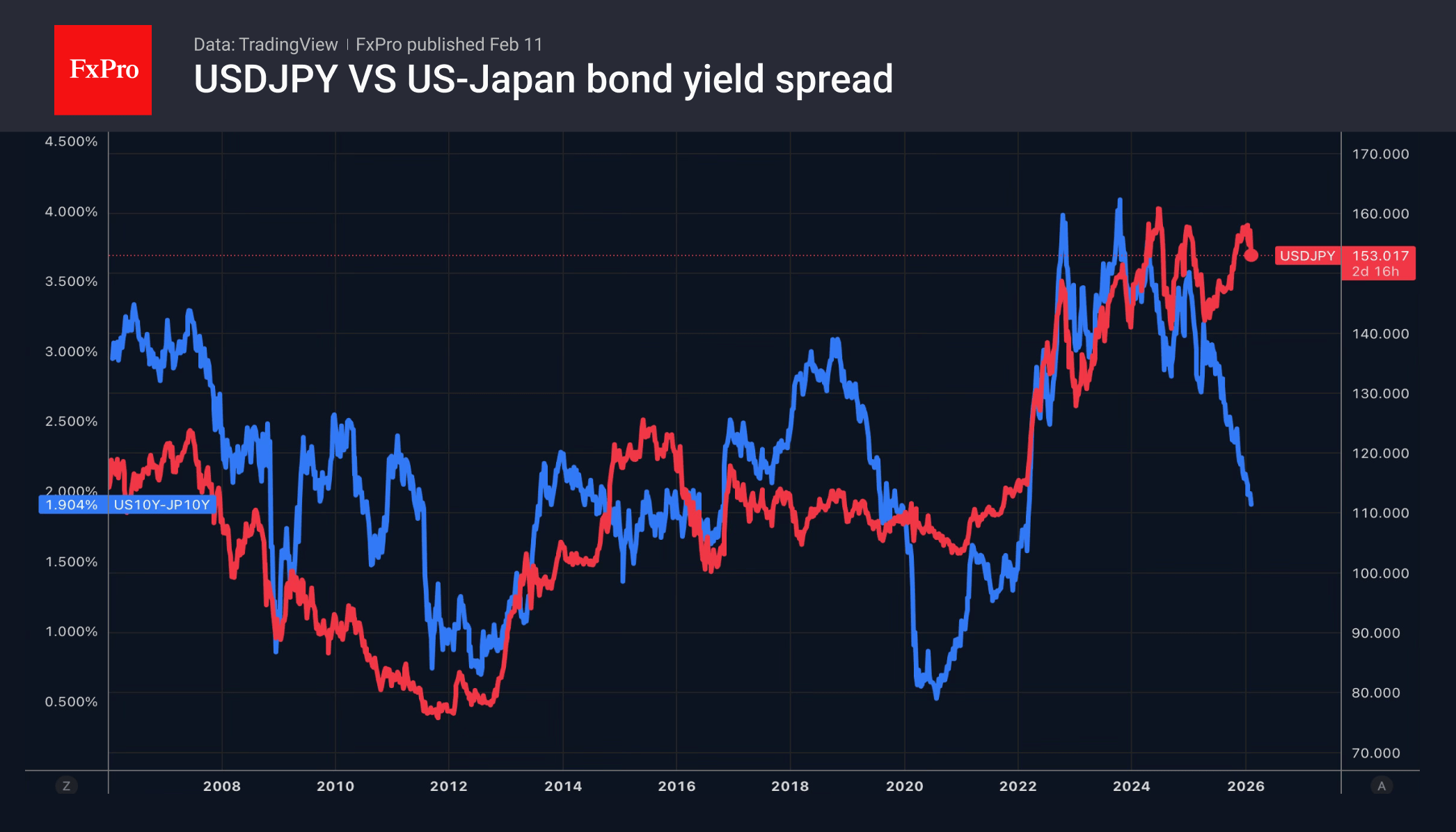

Forex Follows New Leaders

- AUD confidently leads the currency race.

- JPY is getting help from capital repatriation.

The US dollar has stalled amid anticipation of the important January labour market report. Non-farm payrolls are expected to add 69K, while the unemployment rate is set to remain at 4.4%. According to Dallas Fed President Lorie K. Logan, if hiring stabilises and inflation continues to slow, the current Fed rate level is appropriate for achieving the dual mandate. However, derivatives are anticipating two rate cuts this year, which is putting pressure on the US dollar.

The greenback was hit by retail sales, which failed to grow in December, missing forecasts of a +0.4% increase. Americans usually spend a lot at the end of the year, and their restraint exacerbates fears of a cooling labour market and raises the chances of a federal funds rate cut. The futures market gives a 42% chance for lower rates in April and 77% in June.

The US dollar’s downbeat mood was exploited by its Australian counterpart. The AUDUSD reached 0.71 for the first time in three years on hawkish comments from RBA Deputy Governor Andrew Houser, saying that inflation is too high. The Reserve Bank raised its key rate by 0.25 p.p. to 3.85% earlier this month. Westpac cannot rule out a repeat of this move in March. As a result, the Aussie is confidently leading the race among the 30 most liquid currencies on Forex.

The yen is attempting to compete with it in February. USDJPY is falling steadily after the parliamentary elections. The Liberal Democratic Party’s spectacular victory was initially perceived by investors as a path to fiscal profligacy by the government. However, markets now believe that Sanae Takaichi will be a fiscally responsible prime minister. If so, the repatriation of capital to Japan will lead to a strengthening of the yen. According to Nomura, USDJPY could catch up with the bond yield differential and fall to 150.

Gold continues to seek equilibrium and is trying to return to its old drivers after the rollercoaster ride at the turn of January and February. If gold is not helped by geopolitical factors, perhaps monetary policy will lend a helping hand? The increased likelihood of three, rather than two, Fed rate cuts in 2026 could be a tailwind for the precious metal.

Gold Climbs to a Two-Week High: Markets Await a Softer Fed Policy

Gold on Wednesday held above 5045 USD per ounce and traded near a two-week high. The quotes are supported by expectations of a softer Fed policy.

Growth intensified after weak US economic data. Retail sales came in below forecasts in December, pointing to a slowdown in consumer activity and fuelling fears of a cooling economy.

The market is now pricing in a higher probability of three Fed rate cuts this year than two weeks ago.

Investors are now awaiting the publication of US data on employment and inflation, which may provide additional signals about the state of the economy and the regulator’s next steps.

Demand from central banks remains robust. The People’s Bank of China increased gold reserves in January

Technical Analysis

The H4 XAU/USD chart shows that after a sharp collapse in early February from the 5550–5600 area to lows around 4400, gold has entered a recovery phase. The price has stabilised around 5000–5050 and is trading near the middle line of the Bollinger Bands. The bands are gradually narrowing, indicating declining volatility and the formation of consolidation following strong price swings.

On the H1 chart, the structure is more neutral. Quotes are moving within a narrow 5000–5080 range. The upper boundary acts as local resistance, while the lower acts as support. The market looks balanced, with attempts at a steady advance, but no pronounced momentum.

Conclusion

In summary, gold’s rally to a two-week high primarily reflects shifting market expectations towards a more dovish Fed, amplified by recent soft US retail data. While technical indicators show stabilisation and consolidation within a recovery phase, price action remains range-bound and lacks decisive momentum. The near-term trajectory will be critically dependent on incoming US inflation and employment data, which will either validate the current dovish repricing or challenge it. Sustained central bank buying and unresolved geopolitical tensions provide a structural floor, but for a breakout above the current consolidation, gold requires a clear catalyst from upcoming macroeconomic releases.