Sample Category Title

EUR/USD Breaks Higher As USD/JPY Loses Bullish Grip

EUR/USD started a decent upward move above 1.1880. USD/JPY declined below 155.00 and is currently consolidating losses.

Important Takeaways for EUR/USD and USD/JPY Analysis Today

- The Euro found support and started a recovery wave above the 1.1850 resistance zone.

- There is a connecting bullish trend line forming with support at 1.1890 on the hourly chart of EUR/USD at FXOpen.

- USD/JPY is trading in a bearish zone below 156.00 and 155.00.

- There is a short-term bearish trend line forming with resistance at 154.65 on the hourly chart at FXOpen.

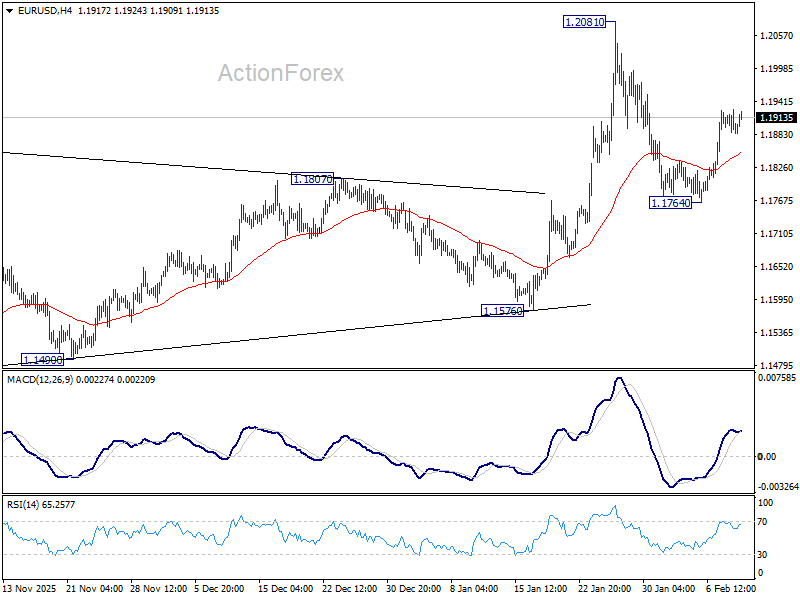

EUR/USD Technical Analysis

On the hourly chart of EUR/USD at FXOpen, the pair started a fresh increase from 1.1765. The Euro climbed above 1.1800 and 1.1850 against the US Dollar.

The pair even settled above 1.1880 and the 50-hour simple moving average. Finally, it tested the 1.1930 resistance. A high is formed near 1.1928, and the pair is now consolidating gains above the 23.6% Fib retracement level of the upward move from the 1.1765 swing low to the 1.1928 high.

Immediate support is near a connecting bullish trend at 1.1890 and the 50-hour simple moving average. The next area of interest could be 1.1835.

The main breakdown zone on the EUR/USD chart sits near the 76.4% Fib retracement at 1.1805. If there is a downside break below 1.1805, the pair could drop toward 1.1765. Any more losses might send the pair toward the 1.1720 low.

On the upside, the pair is now facing resistance near 1.1930. The next hurdle is 1.1950. An upside break above 1.1950 could set the pace for another increase. In the stated case, the pair might rise toward 1.2000.

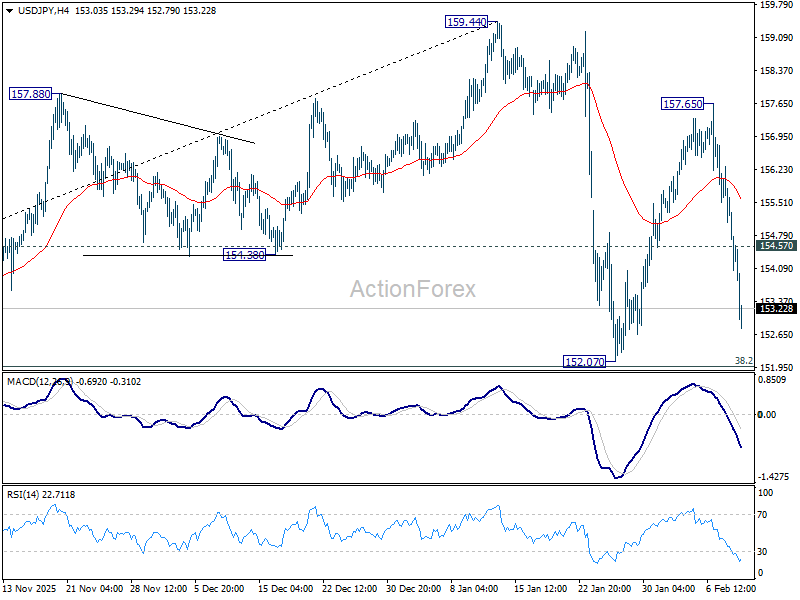

USD/JPY Technical Analysis

On the hourly chart of USD/JPY at FXOpen, the pair started a steady decline from well above 157.20. The US Dollar gained bearish momentum below 156.00 against the Japanese Yen.

The pair even settled below 155.00 and the 50-hour simple moving average. There was a spike below 154.50 and the pair traded as low as 153.34. It is now consolidating losses with a bearish angle. Immediate resistance on the USD/JPY chartis near the 23.6% Fib retracement level of the recent decline from the 157.65 swing high to the 153.34 low at 154.35.

There is also a short-term bearish trend line forming at 154.5. The first barrier for the bulls could be near the 38.2% Fib retracement at 155.00.

If there is a close above the 155.00 level and the hourly RSI moves above 50, the pair could rise toward 156.00. The next key area of interest is near 156.60, above which the pair could test 157.00 in the coming days.

On the downside, the first major support is near 153.35. The next key zone is near 152.50. If there is a close below 152.50, the pair could decline steadily. In the stated case, the pair might drop toward 150.00.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Chart Alert: Nikkei 225 Bullish Acceleration Intact Towards 60,000 in the First Step

Key takeaways

- Bullish momentum reinforced by politics: The Nikkei 225 extended its rally from the 6 February reversal low, supported by PM Takaichi’s snap election victory and a decisive parliamentary supermajority, making it the top-performing major global index over the past two sessions (+2.3%).

- Stronger yen not derailing equities: Despite USD/JPY falling on intervention fears, Japanese equities held firm. Domestically focused stocks are outperforming exporters, suggesting a stronger JPY is boosting consumer confidence and supporting internal demand.

- Acceleration phase intact toward 60,000: Technically, the short-term uptrend remains valid above 56,990 support, with upside targets at 58,932, 59,884, and 60,833–61,215. Momentum indicators continue to support further gains unless key support breaks.

The Nikkei 225 has continued to bask in the bullish limelight since last Friday, 6 February 2026’s minor bullish reversal low of 52,956, reinforced by the results of Japan’s lower house parliament snap election held on Sunday, 8 February 2026.

Incumbent Japanese Prime Minister Takaichi’s coalition party has managed to score a stunning victory in the snap election, surpassing the two-thirds majority of 310 seats, with Takaichi's Liberal Democratic Party winning 316 seats in the 465-seat lower house.

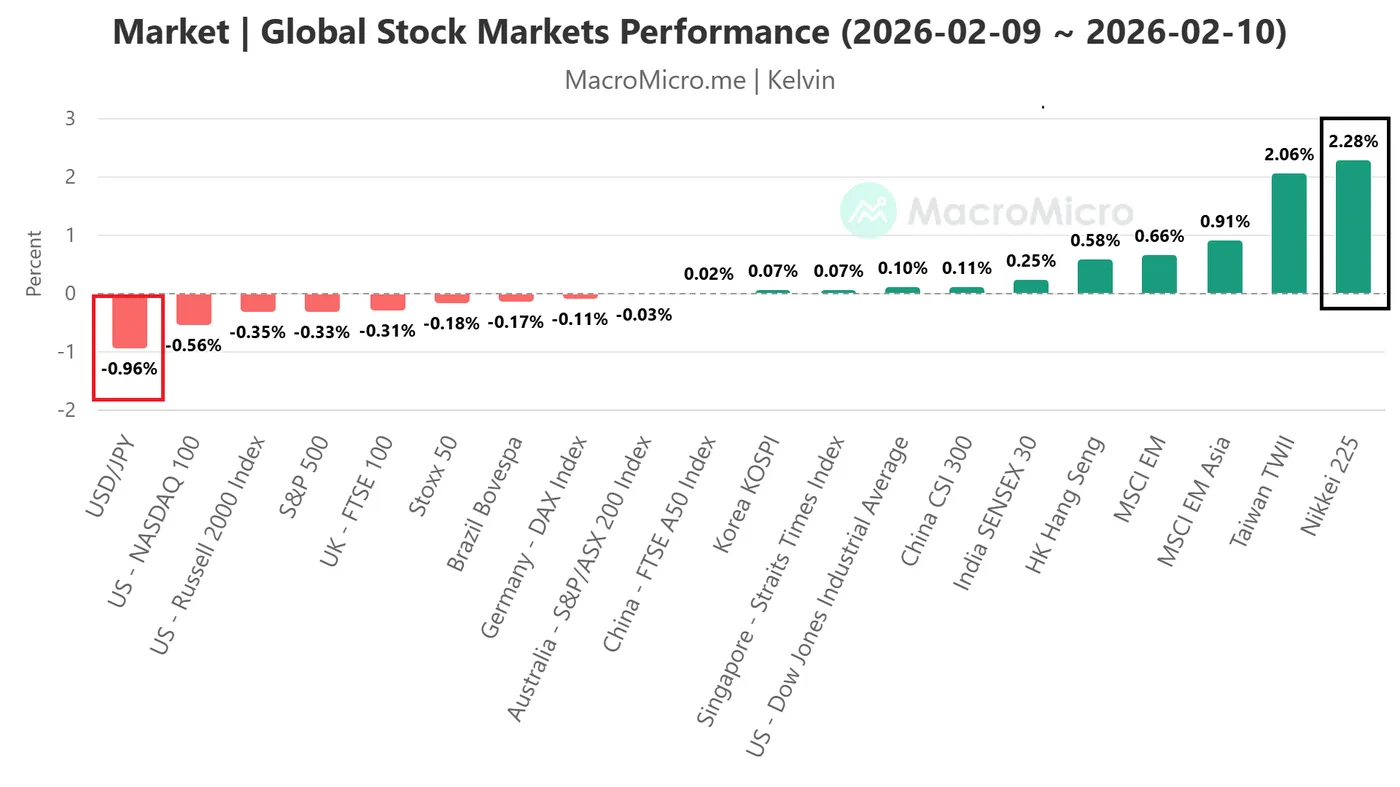

Nikkei 225 is the top performer among global stock markets over the past two days

Fig. 1: Global stock market indices with USD/JPY from 9 Feb to 10 Feb 2026 (Source: MacroMicro)

Since the start of the week till Tuesday, 10 February 2026, Japan’s Nikkei 225 is the top-performing major global stock with a positive return of 2.3%, surpassing the major US stock indices; Dow Jones Industrial Average (+0.1%), S&P 500 (-0.3%), Russell 2000 (-0.4%), and Nasdaq 100 (-0.6%) (see Fig. 1).

Interestingly, the renewed strength in the Japanese yen, where the USD/JPY shed -1% in the past two sessions due to fears of US-Japan joint intervention, is not having a negative feedback loop impact on the Nikkei 225.

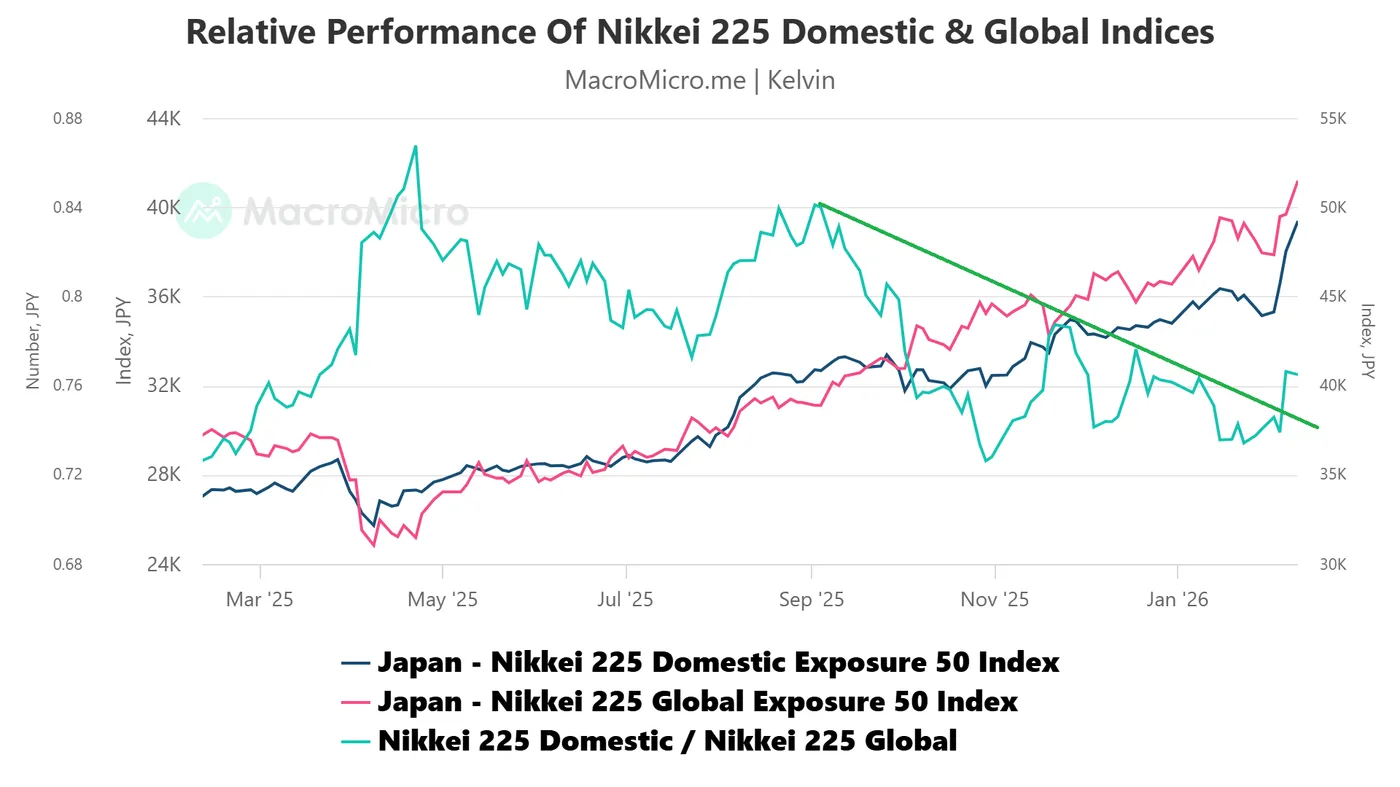

Japan’s equities with high domestic exposure are outperforming exporters

Fig. 2: Relative performance of Nikkei 225 Domestic Exposure against Global Exposure as of 10 Feb 2026 (Source: MacroMicro)

A stronger JPY is likely to negate the current higher cost-of-living squeeze in Japan, in turn, further boosting consumer confidence, which leads to an increase in domestic spending.

Within the Nikkei 225, stocks with a higher reliance on domestic Japanese sales are outperforming export-heavy names, particularly technology equipment and automobile manufacturers with greater overseas exposure.

Since 4 February 2026, the Nikkei 225 Domestic Exposure 50 Index (domestic sales) has outperformed the Nikkei 225 Global Exposure 50 Index (international sales), where its ratio increased to 0.76 on Tuesday, 10 February 2026, and broke above a 5-month descending resistance (see Fig. 2).

Hence, this counterintuitive observation suggests that a stronger Japanese yen is likely to be playing a supportive role at this juncture to maintain the bullish trend in the Japanese stock market (Nikkei 225).

Let's now look at the technical chart of Japan CFD index (a proxy of the Nikkei 225 futures) to decipher its short-term trajectory and key levels to watch.

Short-term trend (1 to 3 days): Minor bullish acceleration intact since 6 February

Fig. 3: Japan 225 CFD index minor trend as of 11 Feb 2026 (Source: TradingView)

Watch the 56,990 short-term pivotal support on the Japan 225 CFD index for the next intermediate resistances to come in at 58,932, 59,884, and 60.833/61,215 (Fibonacci extensions clusters).

On the flip side, a break and an hourly close below 56,990 negates the bullish tone for a minor corrective pull-back towards the next intermediate support at 56,096, and below it risks a deeper slide to retest 55,111/54,790 (the former range resistance from 14 January to 4 February 2026).

Key elements to support the short-term bullish bias

The hourly RSI momentum indicator has so far managed to hold at its intermediate support at around the 50 level after it exited from its overbought region on Tuesday, 10 February 2026.

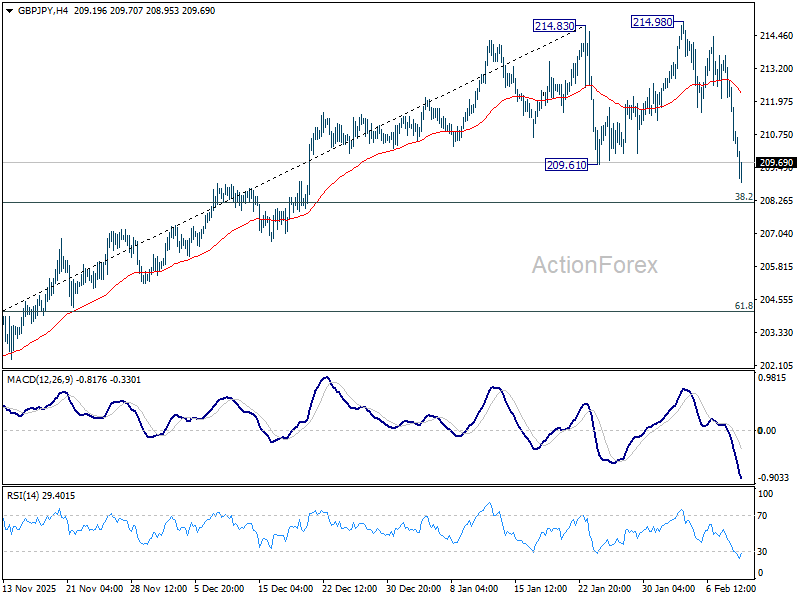

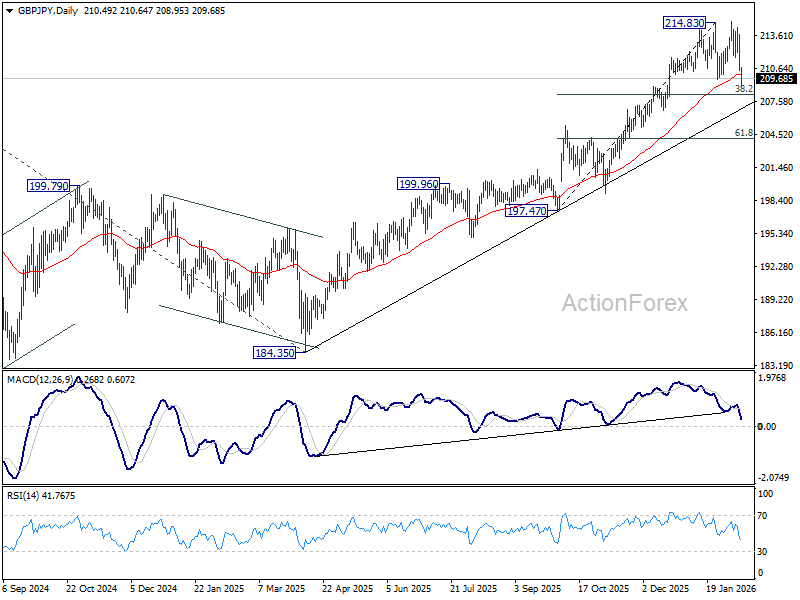

GBP/JPY Daily Outlook

Daily Pivots: (S1) 209.48; (P) 211.61; (R1) 212.73; More...

GBP/JPY accelerates lower and breached 209.61 support. But overall price actions from 214.83 are still seen as a consolidation pattern. Downside should be contained by 38.2% retracement of 197.47 to 214.83 at 208.19 to bring rebound. Break of 214.83/98 is expected at a later stage to resume larger up trend. However, firm break of 208.19 will argue that larger scale correction has already started.

In the bigger picture, up trend from 123.94 (2020 low) is in progress. Next target is 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. On the downside, break of 205.30 resistance turned support is needed to indicate medium term topping. Otherwise, outlook will stay bullish even in case of deep pullback.

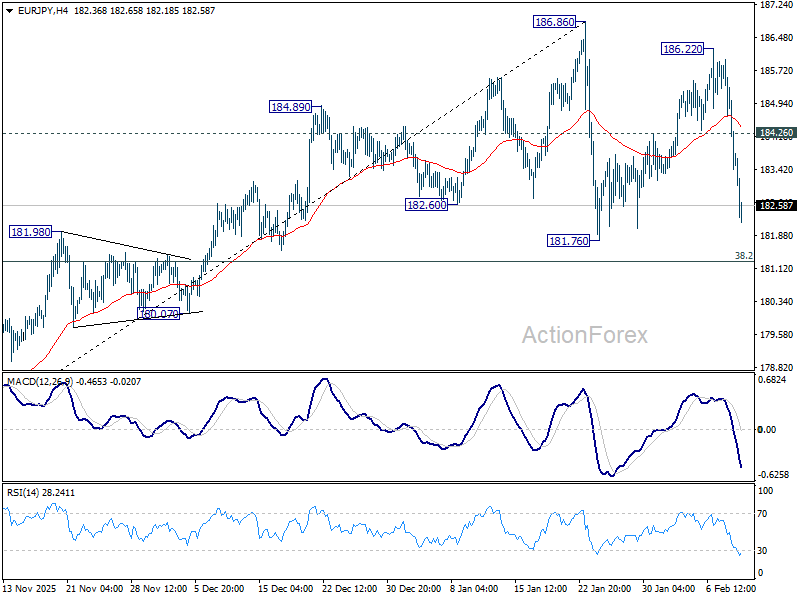

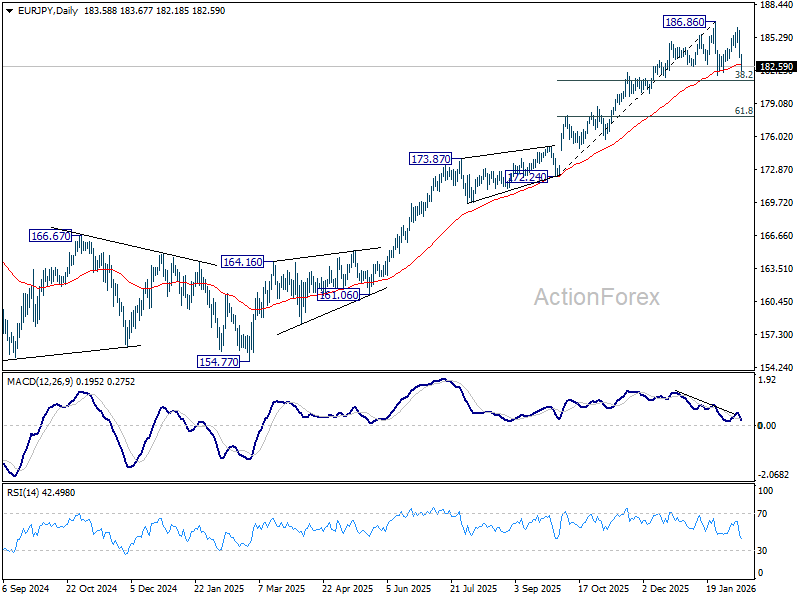

EUR/JPY Daily Outlook

Daily Pivots: (S1) 182.72; (P) 184.36; (R1) 185.27; More...

While EUR/JPY's current fall is steep, overall price actions from 186.86 are still seen as a consolidation pattern. Downside should be contained by 38.2% retracement of 172.24 to 186.86 at 181.27 to bring rebound. Break of 186.86 resistance is expected at a later stage to resume the larger up trend. However, sustained break of 181.27 will indicate that larger scale correction is already underway.

In the bigger picture, up trend from 114.42 (2020 low) is in progress. Upside momentum has been diminishing as seen in bearish divergence condition in D MACD. But there is not clear sign of topping yet. On resumption, next target is 78.6% projection of 124.37 to 175.41 from 154.77 at 194.88 next. Meanwhile, outlook will stay bullish as long as 55 W EMA (now at 174.22) holds, even in case of deep pullback.

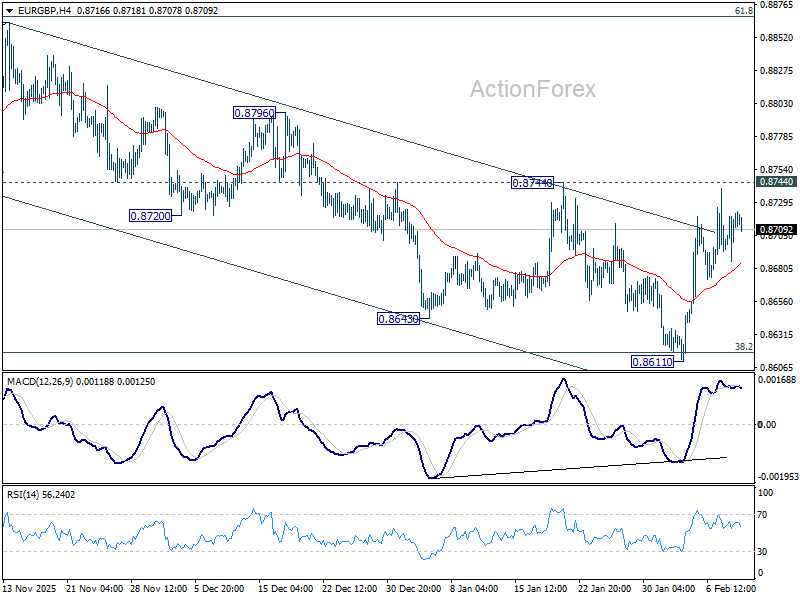

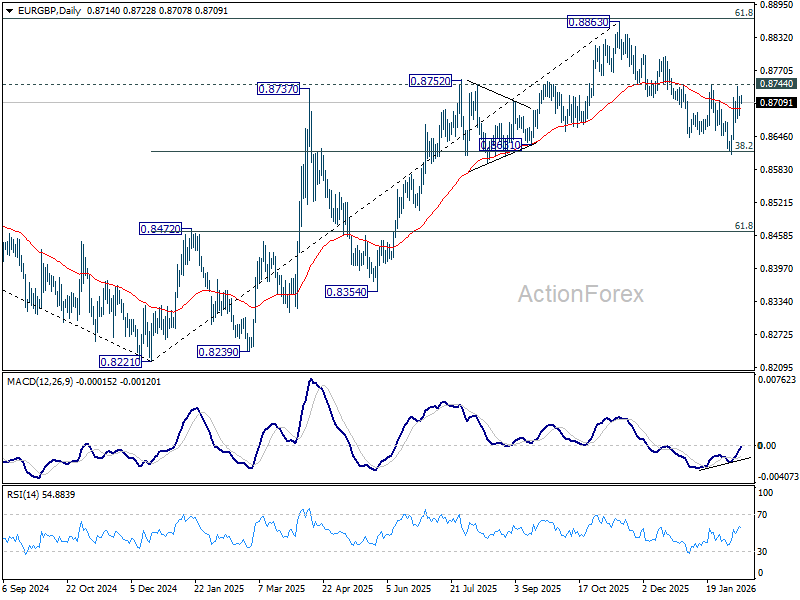

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8695; (P) 0.8709; (R1) 0.8731; More…

Intraday bias in EUR/GBP remains neutral for the moment. On the upside, firm break of 0.8744 resistance will argue that fall from 0.8863 has completed at 0.8611 as a correction. Further rally should be seen back to retest 0.8863 high. On the downside, sustained break of 38.2% retracement of 0.8221 to 0.8663 at 0.8618 will carry larger bearish implications and turn outlook bearish.

In the bigger picture, rise from 0.8221 medium term bottom (2024 low) is seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Sustained trading below 55 W EMA (now at 0.8629) should confirm that this corrective bounce has completed. In this case, deeper fall would be seen back to 0.8201/21 key support zone. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high). That should pave the way back to 0.9267.

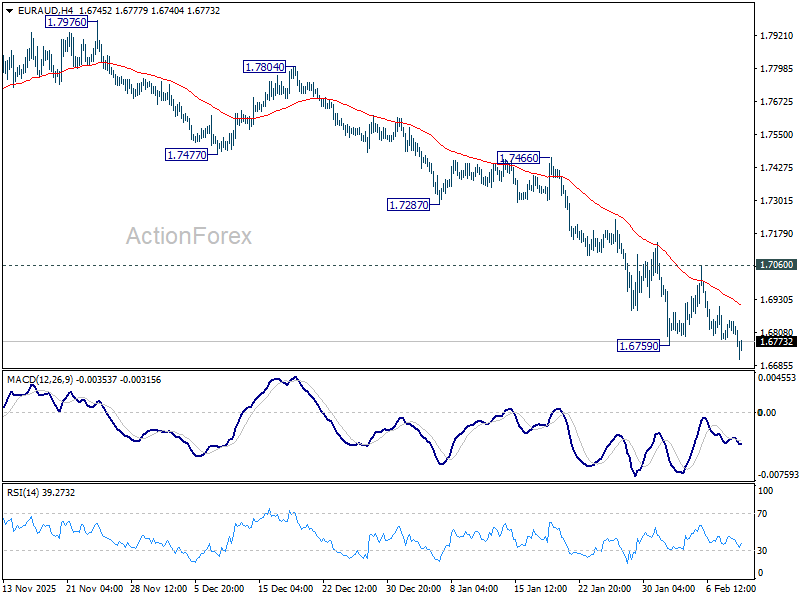

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6782; (P) 1.6818; (R1) 1.6848; More...

EUR/AUD's fall is resuming by breaking 1.6759 support. Intraday bias is back on the downside. Next target is 138.2% projection of 1.8554 to 1.7245 from 1.8160 at 1.6351. On the upside, however, break of 1.7060 resistance will indicate short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 1.8554 medium term top is still in progress. Sustained break of 38.2% retracement of 1.4281 to 1.8554 at 1.6922 will argue that it's already reversing whole up trend from 1.4281 (2022 low). Deeper fall would be seen to 61.8% retracement at 1.5913. For now, risk will stay on the downside as long as 55 D EMA (now at 1.7303) holds even in case of strong rebound.

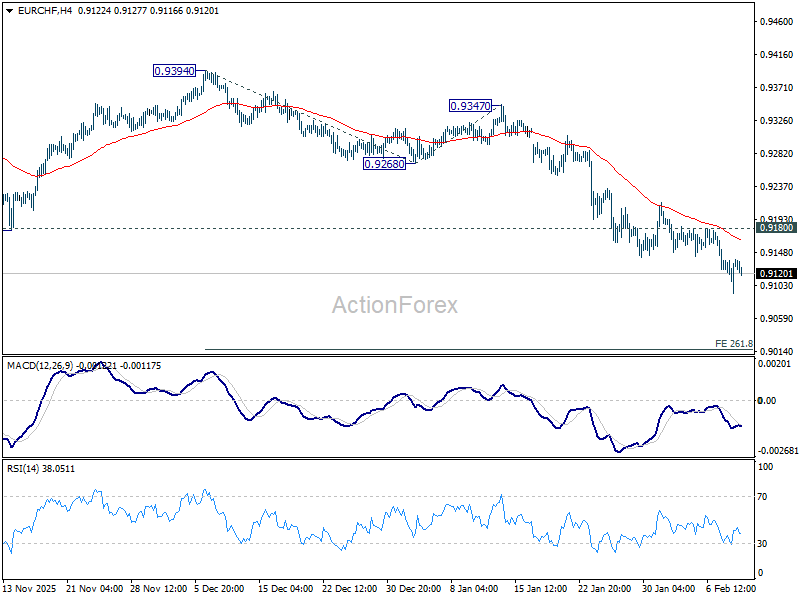

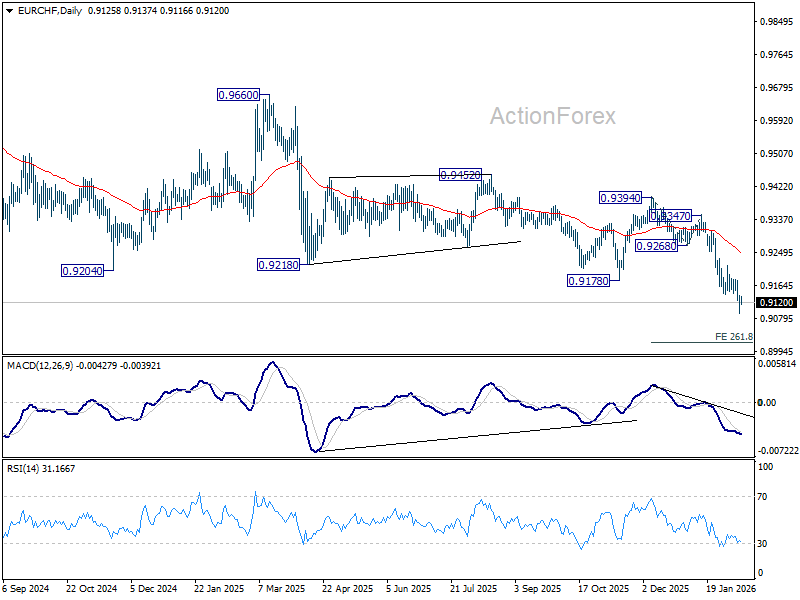

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9105; (P) 0.9125; (R1) 0.9155; More....

Intraday bias in EUR/CHF remains on the downside at this point. Current down trend should extend to 261.8% projection of 0.9394 to 0.9268 from 0.9347 at 0.9017 next. On the upside, however, break of 0.9180 resistance will now indicate short term bottoming, and bring lengthier consolidations.

In the bigger picture, down trend from 0.9928 (2024 high) is still in progress with falling 55 W EMA (now at 0.9334) intact. Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Outlook will stay bearish as long as 0.9394 resistance holds, in case of recovery.

Dollar in Defensive While Treasuries Rise Going into Possibly Pivotal Payrolls.

Markets

Some more disappointing data came yesterday on the heels of last week’s sub-par set of labour market data. US retail sales failed to grow at the end of last year, missing expectations for a solid 0.4% expansion. The Q4 Employment Cost Index meanwhile rose at the slowest pace since 2021. It may ease some of the remaining concerns at the Fed about upside inflation risks. US yields dropped between 3.3 and 7.4 bps in a market that was already on high alert going into the delayed payrolls (and annual 2025 revision) release today ever since Fed Waller’s “Zero. Zip. Nada.” speech flagged the risk of basically no employment growth throughout last year. Long end outperformance pushed the likes of the 10-yr yield below 4.2% support to the YtD lows. German yields dropped 0.9-3.7 bps in sympathy. Corporate bond markets were all about Alphabet’s massive (AI) financing spree in which a 10-times oversubscribed sterling centennial obviously drew the biggest attention. JPY stood out in FX markets, rallying against all major peers on continued hopes for a Japanese revival under PM Takaichi and her supermajority. JGBs by the way also gave the government the benefit of the doubt from a fiscal perspective by dropping 6-8 bps at the long end of the curve. USD/JPY closed near the intraday lows just north of 153. EUR/JPY neared the January troughs around 182. EUR/USD stabilized near 1.19, EUR/GBP bounced back above 0.87 with sterling’s grace period following PM Starmer’s survival apparently already ending.

Japan’s yen is extending this week’s rebound today but we should add that it happens in thinned trading with Japanese markets closed for National Foundation Day. The US dollar remains in the defensive while Treasuries (in the futures market) are rising going into what possibly are going to be pivotal payrolls. The January edition is combined with the annual revision of last year. The risk for 2025 is that the +/- 600k cumulative job growth is going to be wiped out and more: expectations are for a -825k downward adjustment. This is where Fed Waller and his repeated calls for rate cuts to support a weakening labour market come into play. The bar for January is set at a 65k job growth with unemployment stabilizing at 4.4%. There are nuances to today’s numbers, such as seasonal effects, deportation efforts (leading to lower employment but with less impact on the unemployment rate as the supply pool shrinks) and productivity growth (leading to GDP expansion despite fewer or even no hirings). But we doubt these will be given any consideration in the current circumstances. We see asymmetric market risks with the bigger reaction – a weaker dollar, front-end curve outperformance and potentially weaker stocks – in case of a downside surprise. Belgium takes center stage in European politics with the European Industry Summit today ahead of tomorrow’s informal summit to boost European competitiveness.

News and views

China’s January price data published this morning confirmed the deflationary tendencies. Consumer price inflation was reported that 0.2% M/M, reducing the Y/Y measure from 0.8% in December to 0.2%. Both goods price (0.3% Y/Y from 1%) and services inflation (0.1% Y/Y from 0.6%) eased, suggesting absence of demand pressures. Core inflation slowed to 0.8% Y/Y from 1.2%. Producer prices turned slightly less negative in a yearly perspective, ‘rising’ from -1.9% Y/Y to -1.4% Y/Y, the ‘highest’ level since July 2024. Prices of producer goods to some extent have improved due to higher raw materials costs. However, prices of consumer goods leaving the factory gate declined further (-1.7% Y/Y from -1.3%). The yuan this morning maintains its recent gains. At USD/CNY 6.91, the yuan trades near the strongest levels against the US dollar since May 2023.

Deputy Governor of the Reserve Bank of Australia, Andrew Hauser, warned that too high inflation remains a challenge for the monetary policy committee. Hauser assessed that the some of the recent rebound in inflation ‘reflects growing underling pressure about a pick-up in demand against supply constraints in the economy’. The risk is for higher inflation to persist, a scenario the RBA can’t allow to occur. The RBA last week raised its policy rate by 25 bps to 3.85% after (trimmed mean) core inflation rose further north of the 2-3% inflation target. Markets see an 80% chance for a rate hike in May. The Aussie dollar extended gains after the comments, with AUD/USD jumping north of 0.71, nearing the early 2023 top.

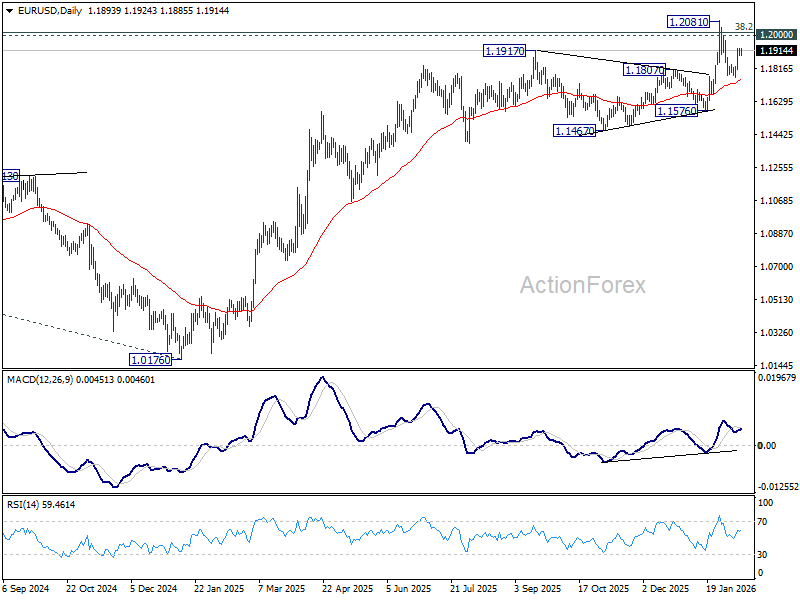

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1878; (P) 1.1904; (R1) 1.1920; More….

Intraday bias in EUR/USD remains mildly on the upside for retesting 1.2081 high. Decisive break there and sustained trading above 1.2 psychological level will carry larger bullish implications. On the downside, however, sustained trading below 55 D EMA (now at 1.1749) will raise the chance of reversal on rejection by 1.2 psychological level, and target 1.1576 support for confirmation.

In the bigger picture, as long as 55 W EMA (now at 1.1470) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.2581. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

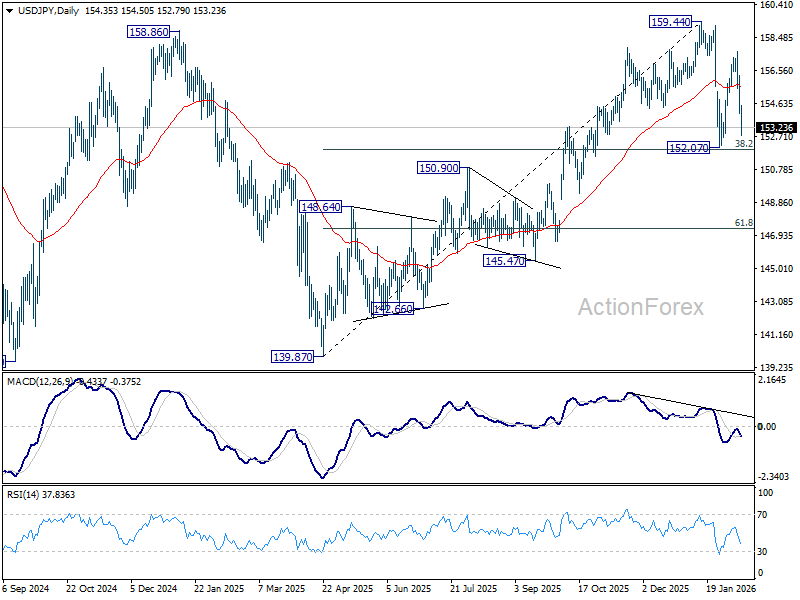

USD/JPY Daily Outlook

Daily Pivots: (S1) 153.53; (P) 154.91; (R1) 155.76; More...

Intraday bias in USD/JPY stays on the downside for 152.07 support. Price actions from 159.44 are still seen as a corrective pattern only. Hence, downside should be contained by 38.2% retracement of 139.87 to 159.44 at 151.96 to bring rebound. On the upside, above 154.57 minor resistance will turn intraday bias neutral first. However, sustained break of 151.96 will argue suggests that it's reversing the rise from 139.87 already.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 151.68) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.