Sample Category Title

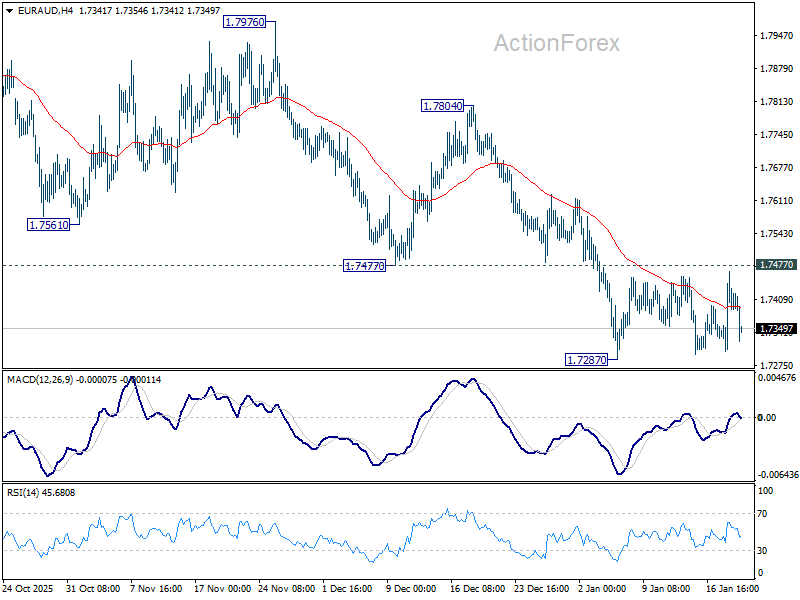

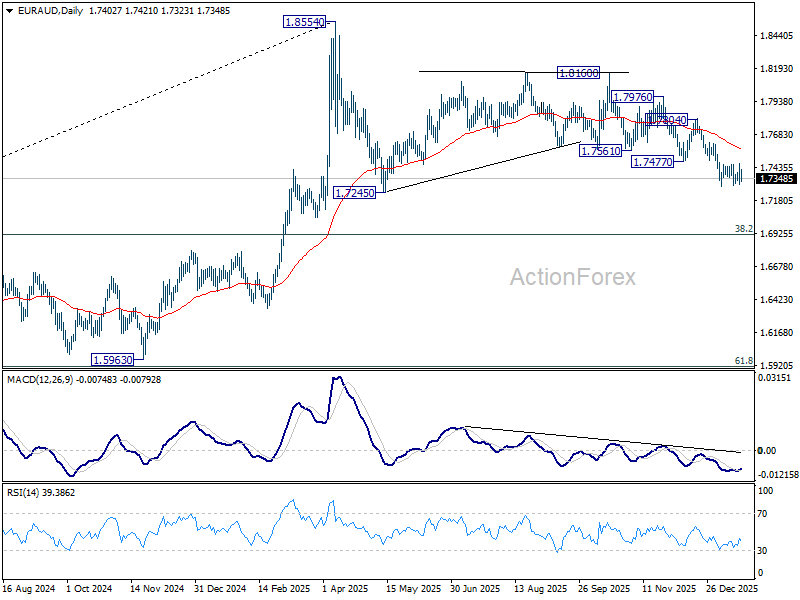

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7319; (P) 1.7394; (R1) 1.7479; More...

No change in EUR/AUD's outlook as range trading continues inside 1.7287/7477. Intraday bias remains neutral and further decline is expected. On the downside, break of 1.7287 will resume the fall from 1.8160. As this is seen as the third leg of the corrective pattern from 1.8554, deeper fall should be seen to 1.7245 support and below. Nevertheless, firm break of 1.7477 will indicate short term bottoming, and bring stronger rebound back to 55 D EMA (now at 1.7569).

In the bigger picture, the break of 55 W EMA (now at 1.7464) argues that fall from 1.8554 medium term top is correcting whole up trend from 1.4281 (2022 low). Deeper decline is in favor to 38.2% retracement of 1.4281 to 1.8554 at 1.6922, and possibly below. Risk will stay on the downside as long as 1.8160 resistance holds, in case of strong rebound.

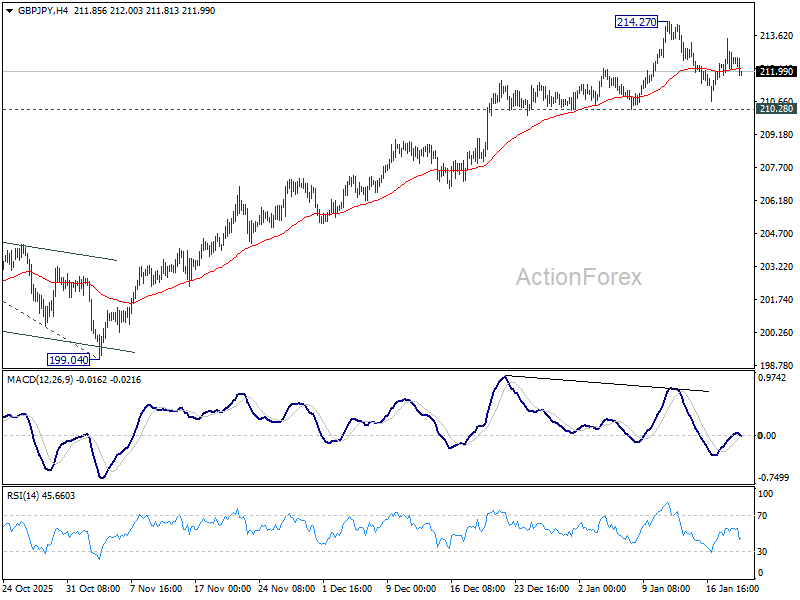

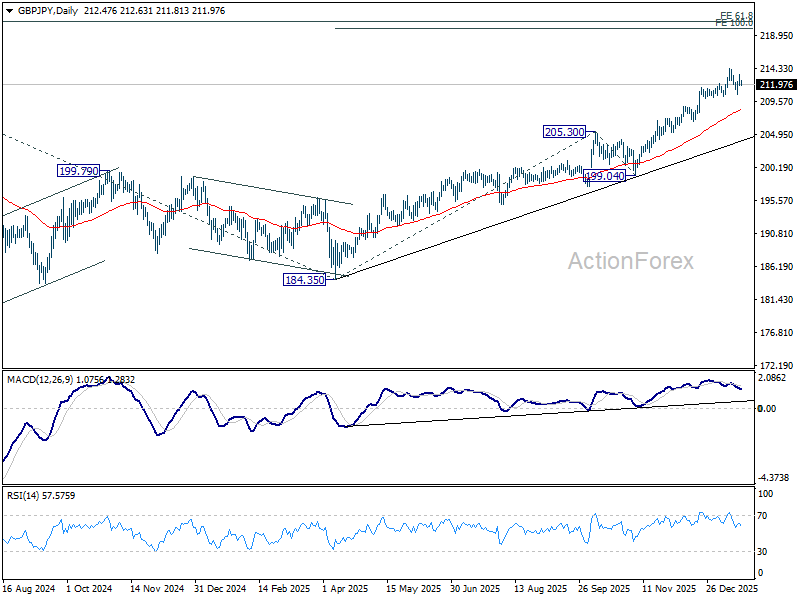

GBP/JPY Daily Outlook

Daily Pivots: (S1) 211.79; (P) 212.64; (R1) 213.44; More...

GBP/JPY is still bounded in range trading below 214.27 and intraday bias stays neutral. With 210.28 support intact, further rally is expected. On the upside, break of 214.27 will resume larger up trend to 100% projection of 184.35 to 205.30 from 199.04 at 219.99 next. Nevertheless, considering bearish divergence condition in 4H MACD, firm break of 210.28 will confirm short term topping, and turn bias to the downside for deeper pullback to 55 D EMA (now at 208.52).

In the bigger picture, up trend from 123.94 (2020 low) is in progress. Next target is 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. On the downside, break of 205.30 resistance turned support is needed to indicate medium term topping. Otherwise, outlook will stay bullish even in case of deep pullback.

Dollar Under Pressure: Tariffs and Geopolitical Risks Shift Market Sentiment

The US dollar continues to weaken after a period of short-term consolidation, amid rising tariff uncertainty and increasing geopolitical tensions. Statements by Donald Trump regarding the possible introduction of new tariffs against Europe have heightened market concerns about the consequences for global trade and economic growth, undermining support for the dollar as a defensive currency.

Additional caution is being driven by expectations of a heavy slate of US macroeconomic releases, including housing market data, inflation indicators, business activity figures, as well as speeches by Federal Reserve officials. In this environment, market participants prefer to reduce dollar exposure and act more selectively, awaiting new signals that could clarify the future path of monetary policy.

USD/JPY

At the start of the current week, the USD/JPY pair slowed its downward movement that followed the formation of a “dark cloud cover” pattern on the daily timeframe. For several sessions, price action has been consolidating within a narrow range of 157.60–158.50, although this sideways movement may soon come to an end.

A break below the 157.60 level could allow the downtrend to resume towards 156.80–157.00. Conversely, a sustained move above 158.50 may support a retest of this year’s highs.

The following events may influence USD/JPY price dynamics in the coming trading sessions:

- today at 11:00 (GMT+2): the International Energy Agency’s monthly oil market report;

- today at 15:30 (GMT+2): a speech by US President Trump;

- tomorrow at 01:50 (GMT+2): Japan’s trade balance (seasonally adjusted).

USD/CAD

Last week, USD/CAD buyers failed to overcome the key resistance zone at 1.3900–1.3930. Technical analysis points to the potential for a decline towards the 1.3750–1.3790 area, as a bearish engulfing pattern has formed on the daily chart.

Invalidation of the bearish scenario would require a firm break and sustained consolidation above 1.3900.

The following events may affect USD/CAD price action in the upcoming sessions:

- today at 15:30 (GMT+2): Canada’s Raw Materials Price Index (RMPI);

- today at 19:00 (GMT+2): the Atlanta Fed’s GDPNow indicator;

- today at 20:00 (GMT+2): the US Treasury auction of 20-year bonds.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

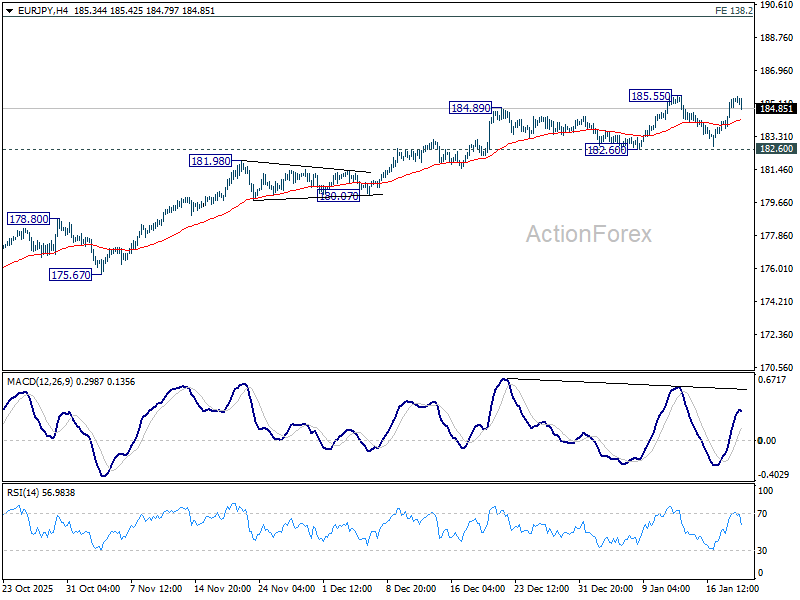

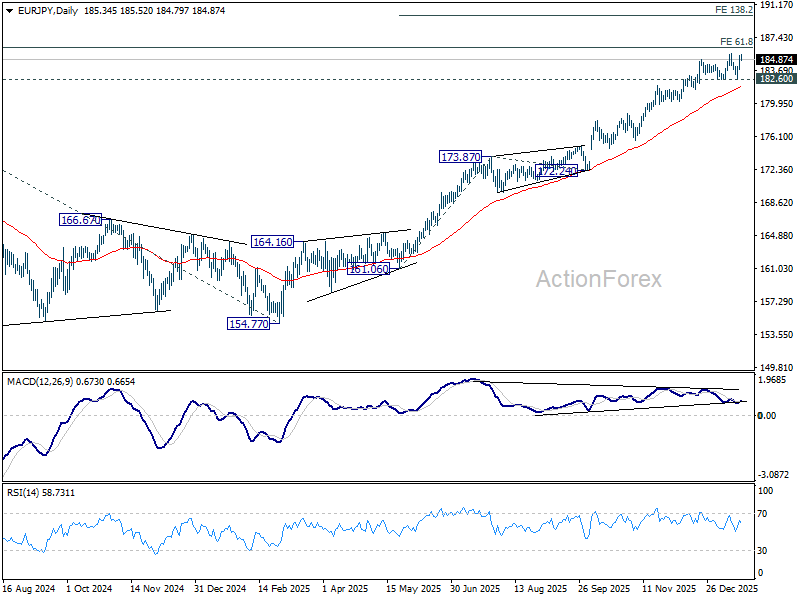

EUR/JPY Daily Outlook

Daily Pivots: (S1) 184.33; (P) 184.90; (R1) 186.02; More...

EUR/JPY retreated ahead of 185.55 resistance as range trading continues. Intraday bias remains neutral for the moment. With 182.60 support intact, further rally is expected. On the upside, break of 185.55 will resume larger up trend to 186.31 projection level. Firm break there will target 138.2% projection of 151.06 to 173.87 from 172.24 at 189.94. However, sustained break of 182.60 will confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 181.83) and below.

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. Considering bearish divergence condition in D MACD, upside could be capped by 186.31 on first attempt. Still, outlook will stay bullish as long as 55 W EMA (now at 172.58) holds, even in case of deep pullback. Sustained break of 186.31 will pave the way to 78.6% projection at 194.88 next.

Markets Catch Their Breath, Trumps Speech in Davos Now Key

Global markets appeared to stabilize somewhat today after the sharp U.S. selloff overnight, which saw the DOW suffer its worst one-day loss since October. That said, the underlying source of stress has not faded. Greenland-related tensions remain unresolved, with no visible path toward de-escalation. The current stabilization looks more like position-squaring, rather than renewed confidence.

For now, markets are simply catching their breath, awaiting the next catalyst. Attention has shifted to World Economic Forum, where US President Donald Trump is due to deliver a closely watched address later today. Trump’s speech comes amid soaring tensions between the U.S. and Europe over Danish territory Greenland, which Trump wants the U.S. to acquire. Markets are watching closely for any signal of escalation, moderation, or strategic ambiguity.

On Tuesday, Trump declined to specify how far he is prepared to go to achieve that objective, telling reporters bluntly, “You’ll find out.” He has previously refused to rule out military action and has threatened new tariffs on multiple European countries if they block the takeover bid.

Those threats have already left their mark on markets this week. The renewed risk of a transatlantic trade war pushed U.S. Treasuries sharply lower, while Gold surged to new record highs.

U.S. 10-year yield briefly breached 4.3% overnight, before settling around 4.295%. Speaking in Davos, Scott Bessent sought to play down concerns about the bond selloff. He said he was not worried about Treasuries, dismissing speculation that European investors were pulling back.

Asked specifically about Denmark, Bessent said its holdings were “irrelevant,” noting they amounted to less than USD 100 million, and added that Denmark has been selling Treasuries for years. He emphasized that the U.S. has seen record foreign investment in Treasuries overall.

Instead, Bessent pointed to Japan, arguing that the recent Japanese bond selloff following a snap election announcement had spilled over into global markets. He dismissed talk of European liquidation as originating from a single analyst at Deutsche Bank. Bessent added that Deutsche Bank’s CEO had personally contacted him to say the bank did not stand by the analyst report, accusing “fake news media” of amplifying unfounded fears.

Meanwhile, Gold climbed above 4,800, extending a powerful rally driven by tariff threats, geopolitical instability, falling real rates, and ongoing diversification away from the dollar. After a record 2025, Gold has entered 2026 with momentum firmly intact. According to analysts surveyed by the London Bullion Market Association, prices are increasingly expected to rise above 5,000 this year, citing lower U.S. real yields, continued Fed easing, and sustained central-bank diversification.

In FX performance terms this week so far, Dollar sits at the bottom, followed by Yen and Sterling, while Kiwi leads, followed by Swiss Franc and Aussie, with Euro and Loonie in the middle.

In Asia, Nikkei fell -0.41%. Hong Kong HSI rose 0.37%. China Shanghai SSE rose 0.08%. Singapore Strait Times is down -0.46%. Japan 10-year JGB yield stabilized and fell -0.056 to 2.288. Overnight, DOW fell -1.76%. S&P 500 fell -2.06%. NADSAQ fell -2.39%. 10-year yield rose 0.064 to 4.295.

ECB's Lagarde: Tariffs manageable, Trump's constant reversals more damaging

ECB President Christine Lagarde said she expects only a "minimal" inflationary impact from additional U.S. tariffs, arguing that Eurozone price pressures remain firmly under control. Speaking to RTL, Lagarde noted that inflation is currently around 1.9%, leaving little scope for tariffs to materially disrupt the ECB’s inflation outlook.

Though, she acknowledged that the impact would not be evenly distributed, with Germany likely more exposed than France given its export-heavy manufacturing base. However, Lagarde argued that Europe would be far more resilient if it focused on removing non-tariff trade barriers within the EU, strengthening internal trade and competitiveness rather than reacting defensively to external shocks.

Lagarde’s sharper warning was reserved for uncertainty, not tariffs themselves. Referring to renewed threats from US President Donald Trump, who has vowed to impose escalating tariffs on several European countries over Greenland, she said the "constant reversals" and unpredictability pose a more serious risk. Trump, she added, often takes a transactional approach, setting demands at “sometimes completely unrealistic” levels.

UK CPI rises to 3.4%, core holds at cycle low of 3.2%

UK inflation firmed at the end of 2025, with headline pressure coming in slightly hotter than expected. CPI rose to 3.4% yoy in December, up from 3.2% and above expectations of 3.3%, while prices increased 0.4% mom, pointing to ongoing near-term inflation momentum.

The upside in headline inflation, however, masked relative stability in underlying pressures. Core CPI—excluding energy, food, alcohol and tobacco—was unchanged at 3.2% yoy, undershooting expectations of 3.3%, and marking the joint-lowest reading since December 2024. Core inflation was last lower in September 2021, reinforcing the view that underlying disinflation progress, while slow, remains intact.

By component, services inflation edged up to 4.5% yoy from 4.4%, keeping the sector firmly in focus for the BoE, while goods inflation rose to 2.2% from 2.1%.

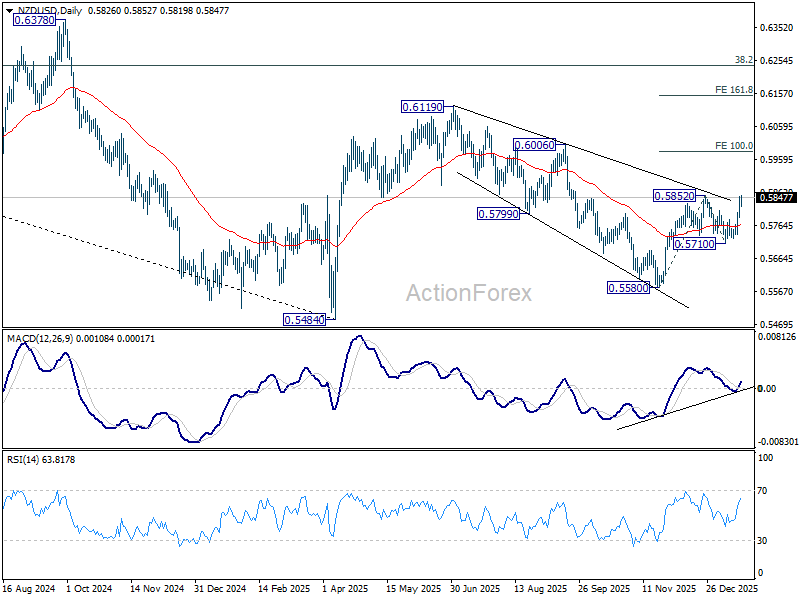

NZD/USD presses resistance Q4 CPI awaited on RBNZ hike guidance

NZD/USD has surged sharply this week and is now pressing key near-term resistance at 0.5852, as shifting global risk dynamics unexpectedly favor the Kiwi. With Dollar and Euro under pressure from Greenland-related geopolitical tensions, both New Zealand dollar and Australian Dollar have surprisingly emerged as relative safe havens, benefiting from stable domestic backdrops and distance from the dispute.

At the same, Yen remains under pressure, weighed down by an aggressive selloff in Japanese government bonds as markets price in post-election fiscal expansion. That divergence has left antipodean currencies unusually well-bid, along with Swiss Franc.

For Kiwi, attention now turns to New Zealand Q4 CPI, due Friday in Asia. The annual rate is expected to hold at 3.0%, right at the top of the RBNZ’s 2–3% target band. With the Official Cash Rate at 2.25%, markets broadly agree the RBNZ has completed its easing cycle. The open question is timing of the next hike, not whether one eventually comes. CPI overshoot would sharply pull forward expectations and offer fresh support to NZD.

That focus will intensify at the February 18 OCR review, the first major policy decision under new Governor Anna Breman. Markets will be listening closely to the tone of the post-meeting press conference for clues on whether Breman leans hawkish, dovish, or neither.

Technically, NZD/USD's dip to 0.5710 earlier this month was a little deeper than expected. But that didn't alter the overall structure. The corrective down trend from 0.6119 (2025 high) should have completed with three waves down to 0.5580.

Firm break of 0.5852 will resume the whole rally from 0.5580 and target 100% projection of 0.5580 to 0.5852 from 0.5710 at 0.6015. Decisive break of 0.6015 will solidify that NZD/USD is in an impulsive move that should be resuming whole rise from 0.5484 (2025 low) through 0.6119. In any case, outlook will now stay bullish as long as 0.5710 support holds.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 184.33; (P) 184.90; (R1) 186.02; More...

EUR/JPY retreated ahead of 185.55 resistance as range trading continues. Intraday bias remains neutral for the moment. With 182.60 support intact, further rally is expected. On the upside, break of 185.55 will resume larger up trend to 186.31 projection level. Firm break there will target 138.2% projection of 151.06 to 173.87 from 172.24 at 189.94. However, sustained break of 182.60 will confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 181.83) and below.

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. Considering bearish divergence condition in D MACD, upside could be capped by 186.31 on first attempt. Still, outlook will stay bullish as long as 55 W EMA (now at 172.58) holds, even in case of deep pullback. Sustained break of 186.31 will pave the way to 78.6% projection at 194.88 next.

ECB’s Lagarde: Tariffs manageable, Trump’s constant reversals more damaging

ECB President Christine Lagarde said she expects only a "minimal" inflationary impact from additional U.S. tariffs, arguing that Eurozone price pressures remain firmly under control. Speaking to RTL, Lagarde noted that inflation is currently around 1.9%, leaving little scope for tariffs to materially disrupt the ECB’s inflation outlook.

Though, she acknowledged that the impact would not be evenly distributed, with Germany likely more exposed than France given its export-heavy manufacturing base. However, Lagarde argued that Europe would be far more resilient if it focused on removing non-tariff trade barriers within the EU, strengthening internal trade and competitiveness rather than reacting defensively to external shocks.

Lagarde’s sharper warning was reserved for uncertainty, not tariffs themselves. Referring to renewed threats from US President Donald Trump, who has vowed to impose escalating tariffs on several European countries over Greenland, she said the "constant reversals" and unpredictability pose a more serious risk. Trump, she added, often takes a transactional approach, setting demands at “sometimes completely unrealistic” levels.

NZD/USD presses resistance Q4 CPI awaited on RBNZ hike guidance

NZD/USD has surged sharply this week and is now pressing key near-term resistance at 0.5852, as shifting global risk dynamics unexpectedly favor the Kiwi. With Dollar and Euro under pressure from Greenland-related geopolitical tensions, both New Zealand dollar and Australian Dollar have surprisingly emerged as relative safe havens, benefiting from stable domestic backdrops and distance from the dispute.

At the same, Yen remains under pressure, weighed down by an aggressive selloff in Japanese government bonds as markets price in post-election fiscal expansion. That divergence has left antipodean currencies unusually well-bid, along with Swiss Franc.

For Kiwi, attention now turns to New Zealand Q4 CPI, due Friday in Asia. The annual rate is expected to hold at 3.0%, right at the top of the RBNZ’s 2–3% target band. With the Official Cash Rate at 2.25%, markets broadly agree the RBNZ has completed its easing cycle. The open question is timing of the next hike, not whether one eventually comes. CPI overshoot would sharply pull forward expectations and offer fresh support to NZD.

That focus will intensify at the February 18 OCR review, the first major policy decision under new Governor Anna Breman. Markets will be listening closely to the tone of the post-meeting press conference for clues on whether Breman leans hawkish, dovish, or neither.

Technically, NZD/USD's dip to 0.5710 earlier this month was a little deeper than expected. But that didn't alter the overall structure. The corrective down trend from 0.6119 (2025 high) should have completed with three waves down to 0.5580.

Firm break of 0.5852 will resume the whole rally from 0.5580 and target 100% projection of 0.5580 to 0.5852 from 0.5710 at 0.6015. Decisive break of 0.6015 will solidify that NZD/USD is in an impulsive move that should be resuming whole rise from 0.5484 (2025 low) through 0.6119. In any case, outlook will now stay bullish as long as 0.5710 support holds.

UK CPI rises to 3.4%, core holds at cycle low of 3.2%

UK inflation firmed at the end of 2025, with headline pressure coming in slightly hotter than expected. CPI rose to 3.4% yoy in December, up from 3.2% and above expectations of 3.3%, while prices increased 0.4% mom, pointing to ongoing near-term inflation momentum.

The upside in headline inflation, however, masked relative stability in underlying pressures. Core CPI—excluding energy, food, alcohol and tobacco—was unchanged at 3.2% yoy, undershooting expectations of 3.3%, and marking the joint-lowest reading since December 2024. Core inflation was last lower in September 2021, reinforcing the view that underlying disinflation progress, while slow, remains intact.

By component, services inflation edged up to 4.5% yoy from 4.4%, keeping the sector firmly in focus for the BoE, while goods inflation rose to 2.2% from 2.1%.

Tensions on Japanese Bond Market Ease Somewhat

Markets

US President Trump’s key note speech at the World Economic Forum in Davos is scheduled around 2:30 pm CET today. In an opinion peace in the Financial Times, US secretary of commerce explained that the US administration isn’t going to Davos to uphold the globalist status quo, but to confront it head-on. “We aren’t going to Davos to blend in. We’re not asking permission or seeking approval. We are here to declare that the era of America Last has come to an end.” America first, although that doesn’t mean America alone. As long as you play ball with America of course. After his keynote speech, he’ll meet with EU leaders who hope to defuse the Greenland crisis or at least drop the tariff treats. An interview with CNBC is scheduled after European market close. Transatlantic relations hit rock bottom this week. Financial markets cramped, turning against US assets in general and selling off bonds and stocks in lockstep. Main US equity indices lost 1.75% (Dow) to 2.4% (Nasdaq) after reopening from the long weekend. EUR/USD closed at 1.1725 from a start at 1.1646. The US yield curve bear steepened with yields adding 1 bp (2-yr) to 8.2 bps (30-yr). The US 10-yr yield confirmed the technical break above 4.2%. Recall that the US administration in the aftermath of the Liberation Panic started moderating its aggressive opening gambits when long term US yields hit certain levels (respectively 4.5% and 5% area for 10y & 30y yield). It suggests that US rhetoric could remain hawkish going into the Feb 1st deadline for 10% tariffs on eight EU countries. We’re not yet inclined to step in and buy the dip already on US assets. On a sidetrack, we today follow the US supreme court hearing regarding President Trump’s Fed governor Cook. It boils down to the interpretation of firing board members “for cause”. That’s not formally defined but understood to mean because of serious malfeasance in office. Lower courts have ruled in favour of Cook, indicating a strict definition of “for cause”. A more expansive interpretation by the conservative supreme court hands the US president a strong precedent and harms legal protections against the independent US central bank. Such outcome is a wildcard for trading but would add fuel to the market fire.

Tensions on the Japanese bond market, another fire accelerator, ease somewhat this morning. The long end of the curve corrects 15 bps lower after this week’s violent JGB sell-off as markets fear that PM Takaichi might overdue it on the fiscal stimulus should her LDP party gain an outright majority in February 8 lower house (snap) elections. The Japanese FM tried to restore calm yesterday after Asian trading hours, suggesting that a sales tax cut proposal for food wouldn’t be funded by new borrowing. Japan’s second largest bank, Sumitomo Mitsui Financial Group, this morning announced plans to increase its Japanese government bond portfolio to as much as double the current JPY 10.6tn.

News & Views

In first public comments after becoming member of the MPC of the Polish National Bank end last year, Marcin Zarzecki agreed with the decision to leave to policy rate unchanged at 4% this month. He indicated that a return to interest rate cuts should only take place if the new projections clearly confirm that the disinflationary process is sustainable. Keeping rates at a reasonable level increases the anti-inflationary effectiveness of policy and solidifies the process of anchoring inflation expectations. Zarzecki even warned that soft incoming inflation figures shouldn’t automatically green light further easing as the MPC is focused on the inflation outlook. There as signs that there is some division within the MPC on the timing of further easing as other members recently left the door open for a Q1 rate cut. Zarzecki sees Governor Glapinski’s indications about the rate cut cycle bottoming out near 3.5% as a reasonable point of reference. The new MPC member also warned that an overly accommodative policy might limit the MPC’s ability to respond to potential external shocks, such as an escalation in geopolitical tensions.

Reuters reports that the German Government is in the process of lowering its GDP forecast for this year from 1.3% tot 1%. According to a draft report, also 2027 growth might be downwardly revised from 1.4% to 1.3%. The 2026 growth is still substantially higher compared to the 2025 outcome of 0.2% yearly growth. The revision might be included in the annual economic report of the Ministry of Finance that will be revealed on January 28.

The Greenland Chaos Will Remain the Main Course of the Week

An exotic blend of rising geopolitical tensions between the US and the EU — over Donal Trump’s willingness to buy Greenland — and a major selloff in Japanese government bonds, in the context of Japanese PM Sanae Takaichi confirming a snap election on February 8 in hopes of consolidating power and injecting more public money into the Japanese economy, rattled global financial markets yesterday.

The US 10-year yield flirted with the 2.40% level, while the 30-year jumped more than 25 basis points — a huge move — past 3.90%, and the 40-year pushed above 4%. Selling pressure eased and yields are lower this morning, but the violence of the move almost made investors forget about the US’ willingness to buy Greenland.

In FX markets, dollar and yen bears raced each other to see who could sell faster. Dollar bears were ahead, with the USDJPY fluctuating around the 158 level, while the dollar index fell the most in 10 days.

On the bond side, the US 10-year yield briefly traded above the 4.30% level, as investors continued to reduce US exposure, worried that:

- The US is becoming too aggressive for allies to continue viewing its government debt as a safe haven, and

- The exploding US debt pile is unsustainable — the good old US debt story — possibly amplified by fears that military spending must rise if the US becomes more assertive globally.

The bad news is that elsewhere, appetite for bonds didn’t look much better. European benchmark 10-year yields also rose, alongside growing cracks among European members facing differentiated US treatment over the Greenland story — only a handful being subject to fresh tariffs, not all of them.

We heard the German Chancellor say it is normal that the French react more because they are more sensitive to US tariffs, while Italy attempt to mediate the dispute — with little conviction from European peers so far.

The Greenland chaos will remain the main course of the week and will be served again today, as Donald Trump prepares to rock the boat in Davos. The rally in gold to $4’876 per ounce is a good indicator of how uncertain and tense markets have become.

I hope I am wrong — but there is a greater chance that the two sides of the Atlantic will not reach an agreement on Greenland in a single day. The UK and the Irish took almost a decade to reach an agreement on fishing rights; here, we are talking about an issue that could mark the beginning of the end for NATO. The implications would be huge — so huge that no one can fully grasp their extent. What we do know is that, either way, Europe will have to strengthen its defence. All members will need to set aside budgets for increased military spending in the coming years. Regardless of who takes the tariff or military hit today, tomorrow it will be someone else’s turn.

As a result, capital is flowing into European defence stocks, while at the index level, selling pressure dominates.

Across the Atlantic, market mood is no better. Major US indices gapped lower at the open of the holiday-shortened week — which is healthy. It is a sign that investors still care. The S&P 500 lost more than 2%, while the tech-heavy Nasdaq fell even more, on fears that tensions with the EU could finally push Europeans to tax US Big Tech companies.

This would add to the growing list of investor discomforts: circular AI deals, overleveraged investments, delayed ROI, rising metals prices, and higher memory chip costs. It is therefore unclear whether earnings will be enough to soothe nerves. Headline numbers will be tested, as investors dig into the details: has Nvidia converted receivables into cash? What are companies’ real cross-exposures in an environment where everyone’s hand is in everyone’s pocket?

Speaking of earnings, Netflix announced that it amended its offer to buy Warner Bros to an all-cash deal and reported Q4 earnings after the bell. The company narrowly beat earnings and revenue estimates. Ad revenue grew more than 2.5x year-on-year to over $1.5bn — something that could help soothe worries that OpenAI – which will shortly bring ads on its free chatbot - is not generating enough cash to match its massive infrastructure investment. However, Netflix shares fell in after-hours trading as Netflix warned of higher program spending and WB acquisition-related costs.

Looking ahead, we will keep an eye on the Greenland story — impossible to miss — Japanese yields, and upcoming earnings. The only certainty is uncertainty.

As a result, equity volatility is rising, and bond volatility — which had been falling due to strong demand for bonds of all kinds since last year — is likely to rebound from the lowest levels seen since Q4 2021.

Developed-market sovereign bonds no longer offer the diversification investors need in the current environment. They remain under pressure from geopolitical tensions that will drive higher security spending, at a time when debt levels are already unsustainable.

Where does capital go? Into gold, silver, copper, industrial metals, rare earths – hard commodities.

In short, investors are moving into anything tangible. What is striking is that Bitcoin has had little to no role in this flight to real assets. I would have expected stronger performance, but seemingly, the technology appetite weighs heavier than its 'commodity' status.