Sample Category Title

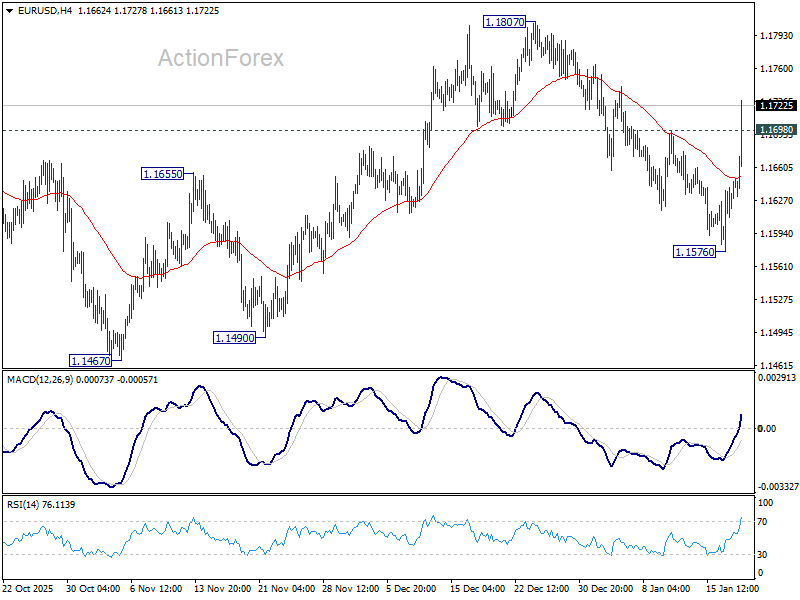

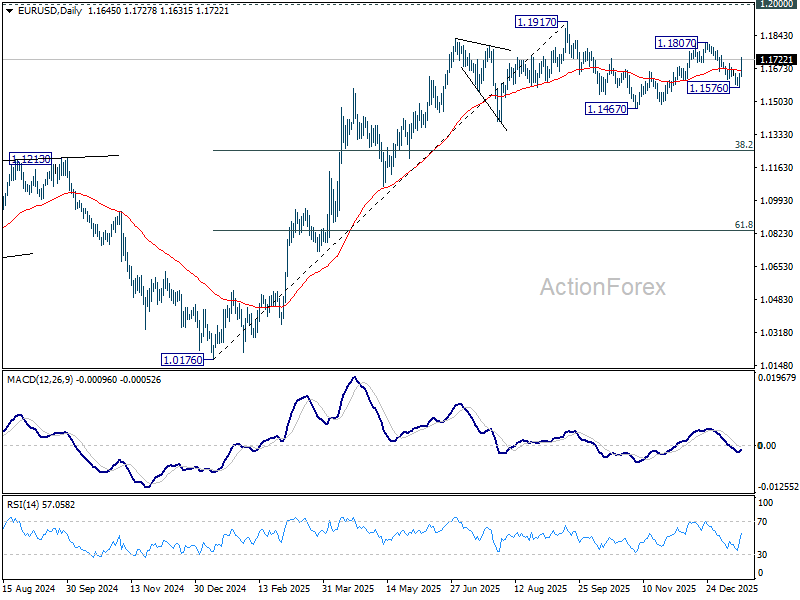

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1600; (P) 1.1625; (R1) 1.1670; More….

EUR/USD's solid break of 1.1698 resistance indicates that fall from 1.1807 has completed at 1.1576. Intraday bias is back on the upside for 1.1807 first. Break there will target a test on 1.1917 key resistance level. For now, risk will stay on the upside as long as 55 4H EMA (now at 1.1652) holds, in case of retreat.

In the bigger picture, as long as 55 W EMA (now at 1.1413) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will carry larger bullish implication. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

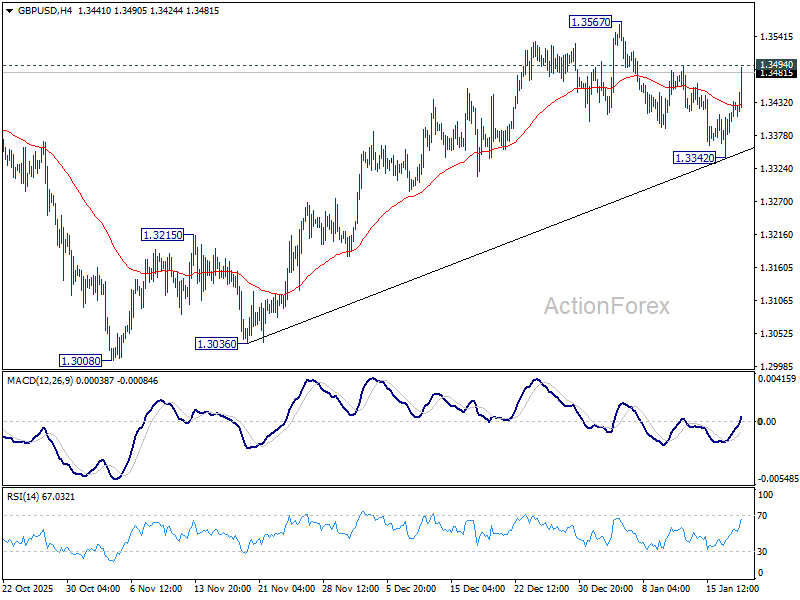

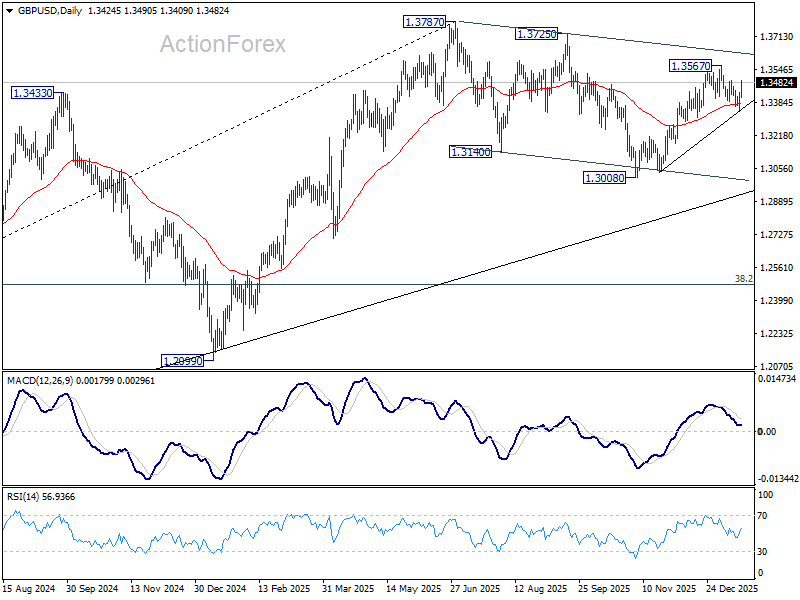

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3368; (P) 1.3402; (R1) 1.3460; More...

Immediate focus is now on 1.3494 resistance as GBP/USD's rebound from 1.3342 extends higher. Firm break there will suggest that pullback from 1.3567 has completed after drawing support from 55 D EMA (now at 1.3375). Intraday bias will be back on the upside for 1.3567 first. Break there will resume the rally from 1.3008 to retest 1.3787 high. On the downside, sustained trading below 55 D EMA will argue that the decline is another falling leg in the corrective pattern from 1.3787.

In the bigger picture, price actions from 1.3787 (2025 high) are seen as a correction to the larger up trend from 1.3051 (2022 low). Deeper decline could be seen as the pattern extends, but downside should be contained by 38.2% retracement of 1.0351 to 1.3787 at 1.2474 to bring rebound. Break of 1.3787 for up trend resumption is expected at a later stage.

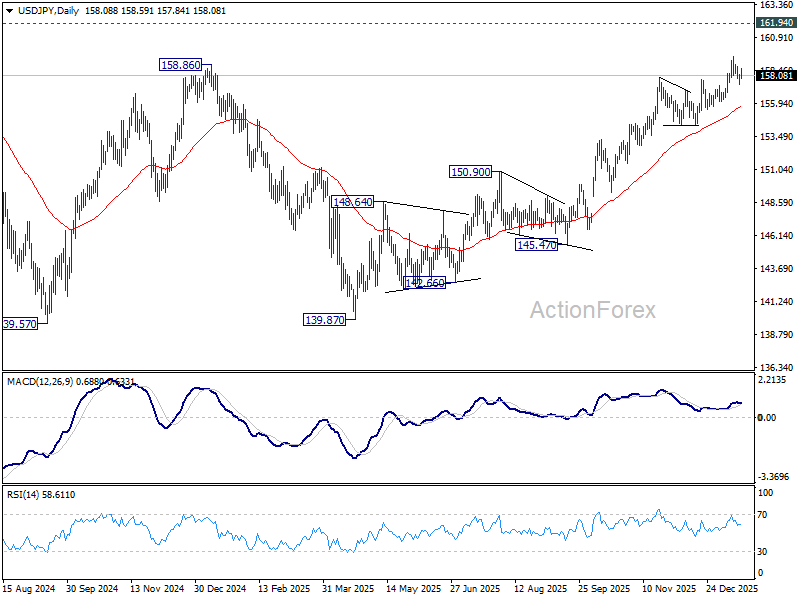

USD/JPY Daily Outlook

Daily Pivots: (S1) 157.64; (P) 157.91; (R1) 158.38; More...

Intraday bias in USD/JPY remains neutral and more consolidations could be seen below 159.44. Outlook remains bullish with 156.10 support intact. On the upside, break of 159.44 will resume the rise from 139.87 towards 161.94 high. However, firm break of 156.10 will confirm short term topping, and turn bias back to the downside for deeper pullback.

In the bigger picture, corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. Decisive break of 158.86 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 154.38 support will dampen this bullish view and extend the corrective range pattern with another falling leg.

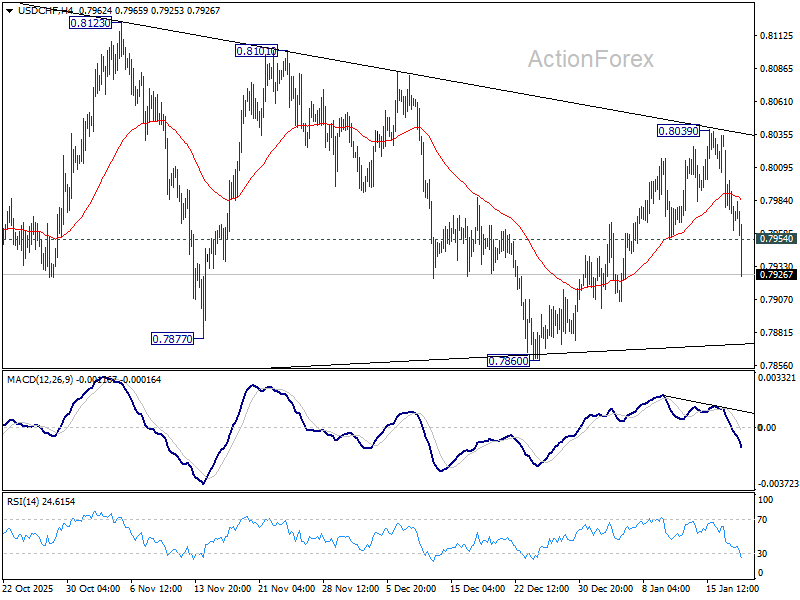

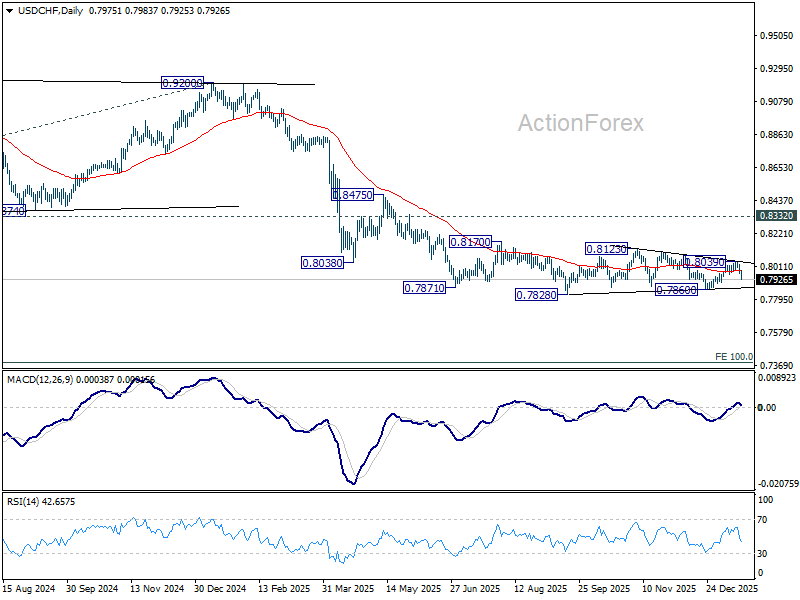

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7951; (P) 0.7987; (R1) 0.8012; More….

USD/CHF's fall from 0.8039 accelerates lower today and the break of 0.7954 support confirms that rebound from 0.7860 has completed. Intraday bias is back on the downside for 0.7860 support. Firm break there will argue that larger down trend is ready to resume through 0.7828 low. For now, risk will stay on the downside as long as 55 4H EMA (now at 0.7984) holds, in case of recovery.

In the bigger picture, price actions from 0.7828 are seen as a correction. Larger down trend from 1.0342 (2017 high) is still in progress. Break of 0.7828 will target 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

Dollar Slumps as “Sell America” Trade Reawakens

Dollar is under broad pressure today as markets return from Monday’s U.S. holiday with persistent focus on geopolitical risk. The move comes along with sharp rise in 10-year Treasury yield, which pushed above 4.27%, extending last week’s decisive break above the 4.2% threshold after nearly a month of failed attempts. Momentum now looks firmly skewed toward a test of 4.3%. At the same time, U.S. equity futures are broadly lower, pointing to a sharp downside open later in the session.

The combination of higher yields and falling stocks is not providing any support to Dollar, reinforcing the view that the market is questioning U.S. policy credibility rather than simply repricing rates. The selloff in the greenback has indeed accelerated through Asian and early European sessions. The combination revived talks that “Sell America” trade is finally gaining traction, reviving memories of the post-“Liberation Day” selloff last April.

At the center, US President Donald Trump has reignited trade tensions with Europe amid the Greenland dispute. The renewed tariff threats have reopened the debate over whether global investors should reduce U.S. exposure. The European Union has several response options. Beyond traditional retaliation, Brussels could activate the Anti-Coercion Instrument, an untested but far-reaching framework that allows restrictions on public tenders, investment access, banking activity, and trade in services. Its potential use is seen as a major escalation risk.

This matters because Europe is the United States’ largest external creditor, holding roughly US 8 trillion in U.S. equities and bonds, nearly twice the rest of the world combined. The key question is not whether Europe can sell, but what would push large institutional investors to start reducing U.S. exposure in size.

Tensions escalated further on Tuesday when Trump threatened 200% tariffs on French wines and champagne after President Emmanuel Macron was reported to be unwilling to join a proposed “Board of Peace” on Gaza. The remarks added a personal dimension to the dispute. Macron’s term runs until May 2027, with no option for re-election, but markets focused less on French domestic politics and more on the precedent of tariffs used as political coercion between allies.

At the same time, Yen selling is accelerating again, driven by a sharp repricing in Japan’s bond market. The 40-year JGB yield hit a record 4%, while the 10-year yield jumped above 2.3%, hitting the highest level since 1999. The moves followed Japanese Prime Minister Sanae Takaichi’s announcement of a February 8 snap election, reigniting fiscal concerns. Ultra-long yields are being pushed higher by both structural supply-demand imbalances and a renewed rise in term and risk premium as markets absorb a more expansionary fiscal stance alongside persistent inflation. This has revived the classic “Takaichi trade”.

On the FX scoreboard so far today, Yen is the worst performer, followed closely by Dollar, with both under heavy pressure. Loonie is the third weakest. At the other end, Kiwi leads gains, followed by Aussie and Euro, while Sterling and Swiss Franc sit in the middle of the pack.

In Asia, Nikkei fell -1.11%. Hong Kong HSI is down -0.25%. China Shanghai SSE fell -0.01%. Singapore Strait Times is down -0.12%. Japan 10-year JGB yield rose 0.082 to 2.353.

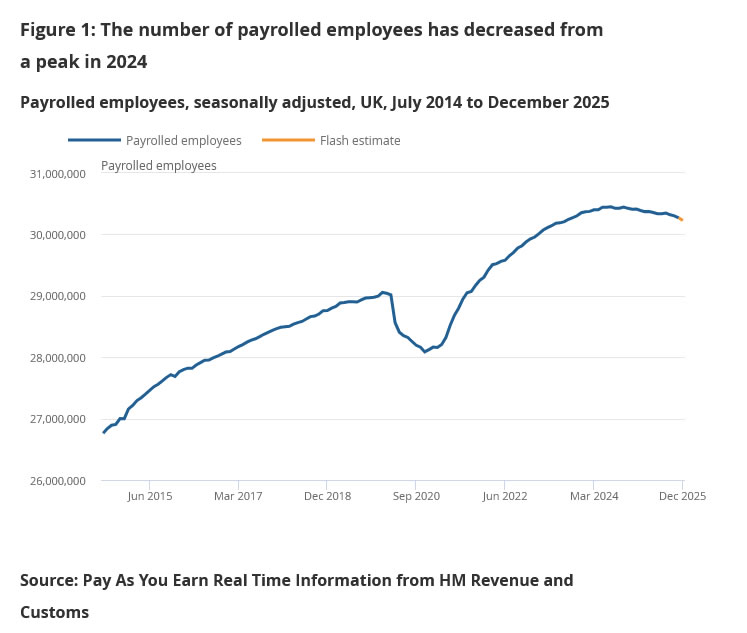

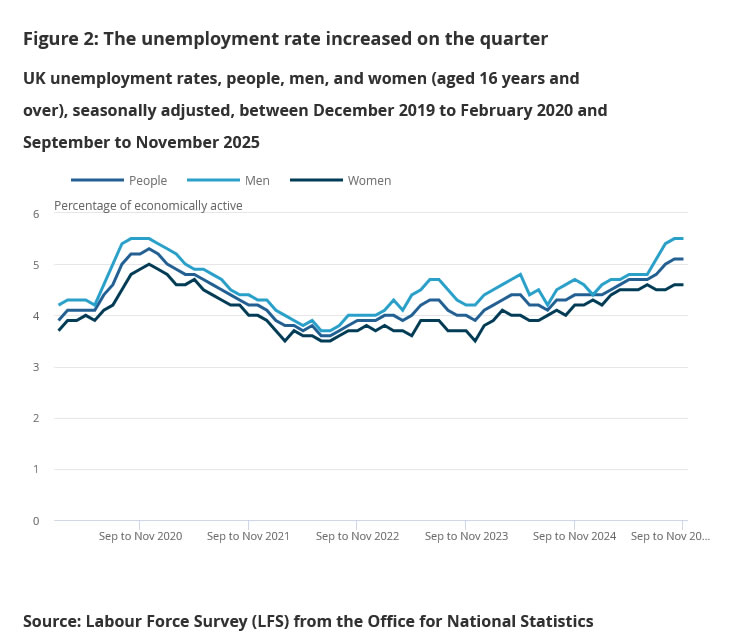

UK payrolled employment falls -43k, wage growth gradually eases

UK labor market data showed further signs of cooling in December, led by outright job losses. Payrolled employment fell by -43k (-0.1% m/m), while the claimant count rose by 17.9k, pointing to softening hiring demand as growth momentum slows.

Wage dynamics were mixed but continued to ease on a broader trend basis. Median monthly pay growth rose to 4.0% yoy from yoy, though this follows a sharp deceleration from levels well above 5% seen through mid-2025.

In the three months to November, unemployment rate was unchanged at 5.1%, suggesting labour slack is building only gradually. Meanwhile, average earnings including bonuses slowed to 4.7% yoy from 4.8%, while earnings excluding bonuses eased to 4.5% from 4.6%.

China keeps LPRs steady as policy shifts to structural support

The PBoC kept its benchmark lending rates unchanged, leaving the 1-year loan prime rate at 3.0% and the 5-year LPR at 3.5%. The decision was widely expected and reinforces the view that Beijing remains reluctant to deploy broad-based monetary easing despite slowing growth.

The policy stance reflects a clear preference for targeted support over headline rate cuts. The 1-year LPR continues to guide most corporate and household loans, while the 5-year rate anchors mortgage pricing. By holding both steady, authorities are signaling concern over financial stability and capital outflows, while relying on alternative tools to stimulate demand where needed.

Instead, the PBOC has intensified the use of structural monetary policy instruments. Last week, it cut rates on key relending facilities by 25bp, lowering the 1-year relending rate for agriculture and small businesses to 1.25%, effective Monday. By reducing the cost of central bank funding to banks, the PBOC aims to encourage cheaper credit for targeted sectors without reopening the door to broad leverage expansion.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7951; (P) 0.7987; (R1) 0.8012; More….

USD/CHF's fall from 0.8039 accelerates lower today and the break of 0.7954 support confirms that rebound from 0.7860 has completed. Intraday bias is back on the downside for 0.7860 support. Firm break there will argue that larger down trend is ready to resume through 0.7828 low. For now, risk will stay on the downside as long as 55 4H EMA (now at 0.7984) holds, in case of recovery.

In the bigger picture, price actions from 0.7828 are seen as a correction. Larger down trend from 1.0342 (2017 high) is still in progress. Break of 0.7828 will target 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

UK payrolled employment falls -43k, wage growth gradually eases

UK labor market data showed further signs of cooling in December, led by outright job losses. Payrolled employment fell by -43k (-0.1% m/m), while the claimant count rose by 17.9k, pointing to softening hiring demand as growth momentum slows.

Wage dynamics were mixed but continued to ease on a broader trend basis. Median monthly pay growth rose to 4.0% yoy from yoy, though this follows a sharp deceleration from levels well above 5% seen through mid-2025.

In the three months to November, unemployment rate was unchanged at 5.1%, suggesting labour slack is building only gradually. Meanwhile, average earnings including bonuses slowed to 4.7% yoy from 4.8%, while earnings excluding bonuses eased to 4.5% from 4.6%.

China keeps LPRs steady as policy shifts to structural support

The PBoC kept its benchmark lending rates unchanged, leaving the 1-year loan prime rate at 3.0% and the 5-year LPR at 3.5%. The decision was widely expected and reinforces the view that Beijing remains reluctant to deploy broad-based monetary easing despite slowing growth.

The policy stance reflects a clear preference for targeted support over headline rate cuts. The 1-year LPR continues to guide most corporate and household loans, while the 5-year rate anchors mortgage pricing. By holding both steady, authorities are signaling concern over financial stability and capital outflows, while relying on alternative tools to stimulate demand where needed.

Instead, the PBOC has intensified the use of structural monetary policy instruments. Last week, it cut rates on key relending facilities by 25bp, lowering the 1-year relending rate for agriculture and small businesses to 1.25%, effective Monday. By reducing the cost of central bank funding to banks, the PBOC aims to encourage cheaper credit for targeted sectors without reopening the door to broad leverage expansion.

The Tariff Hit

The week started on a sour note in Europe. With the US markets closed, European equities spent the session trying to gauge the Greenland risks: how serious is this, how far could it go, and where could it end?

Tariffs are obviously part of the story, and European companies with the highest exposure to US tariffs took the biggest hit. That familiar group from last year was back in focus — German carmakers, for example, and French luxury houses like Louis Vuitton, which slid more than 4% on Monday.

The US was closed, but futures traded down. Nasdaq futures underperformed S&P and Dow futures, amid concerns that Big Tech could become Europe’s target in the trade war.

US Treasuries joined Monday’s selloff this morning. The US 10-year yield jumped past 4.25% on renewed tariff uncertainty and rising rumours that Europeans could “weaponize their US assets” — yes, weaponize is the word being used — to retaliate against Mr Trump’s aggressive trade and geopolitical policies.

Europeans hold roughly $10 trillion in US assets: around $6 trillion in US equities and roughly $4 trillion in Treasuries and other bonds. Selling those assets would pull the rug from under US markets — and because Mr Trump is highly focused on Wall Street, it could maybe get his attention. But make no mistake: this would mean European investors — private and public — willingly accepting financial pain to punish the US. And right now, with a cost-of-living crisis, an ageing population, and a clear lag in technological progress, it’s hard to imagine investors voluntarily dumping their US holdings. Would you really give up your Nvidia shares to buy Louis Vuitton? Tough choice.

US futures suggest that Wall Street will follow Europe lower when trading resumes on Tuesday. Technology will be in focus — not only because Europe could retaliate by targeting US tech companies, but also because earnings season is about to get going, with Netflix reporting after the bell. Netflix is not an AI story and has lost relevance for broader market sentiment, but the rest of Big Tech will follow in the coming weeks.

Geopolitical risks are now being added to an already long list of AI risks: circular deals, over-leveraged investments, delayed returns on investment, and rising metal and memory-chip prices.

As I’ve been saying, if you like tech, there are plenty of tech stocks outside the US — and they’re doing just fine. The Korean Kospi index has risen in every single trading session since the start of the year. Every one of them. Memory-chip makers, in particular, are benefiting from supply tightness, which allows them to raise prices aggressively. Without memory chips, very little else in technology works.

And from a European perspective, one can’t help but wonder: could ASML — the only supplier of EUV lithograph— be “weaponized” too?

Beyond tech, one group stood out: miners — especially gold miners — as gold prices pushed to fresh highs. Gold is trading above $4’700 an ounce this morning, while silver is consolidating just below $95 an ounce.

Fresnillo jumped more than 6.5% in London to a fresh record high, adding over 250 points to the FTSE 100 on its own. Endeavour (another gold miner) and Antofagasta (a copper miner) added roughly another 150 points combined, helping the UK blue-chip index outperform its European peers.

There’s little doubt that if gold continues to rally — and it’s hard to see what would reverse it when the headlines are this absurd — mining stocks will likely keep rising. Buying gold as a way to defy the US has become a theme (the debasement trade).

But caution is warranted: some mining valuations are starting to look stretched. Fresnillo now trades on a P/E of around 76. This is not tech. Supply is limited, so most upside must come from price increases alone. A 76x earnings multiple simply doesn’t make sense. Endeavour’s P/E, at around 18, already looks elevated for a miner. For context, diversified miners like BHP, Rio Tinto, or Glencore typically trade on roughly 6–10x earnings, while precious-metal miners tend to sit closer to 8–15x. Above that, things start to look overheated.

Coming back to the uglier global questions: is this shaping up to be another TACO trade? Optimists argue that the Greenland saga is just another example of the now-familiar US negotiating tactic — punch first, talk later.

But when you consider the possibility of three more years of this, diversification starts to look like the obvious answer. Diversifying away from the US — and perhaps from US tech — might be prudent if this “Season of the Stupidest Trade War in the World History” pushes Europeans to lose patience and slap tariffs on US technology.

The problem is: where do you go? Let’s be honest, despite existing Asian alternatives, the US Big Tech’s appeal is hard to replicate elsewhere, and the deep integration and near-monopolistic nature of US tech services means Europe can’t really afford to lose them either.

Americans know — as well as you and I do — that if US tech were to leave Europe, there would be two choices: go with China - replace WhatsApp with WeChat and experience the joys of a mega-app — along with mysteriously disappearing messages? Or simply have no tech at all. No WhatsApp, no Word, no Excel, no social media. Back to SMS, MMS — maybe even fax.

My guess: a market selloff may be brewing, but a 15–20% pullback could once again be followed by another wave of TACO trades. Then we count down three more years, hoping the damage being done among Western allies doesn’t last longer than that.

Croatia’s Boris Vujcic Nominated as ECB Vice President

In focus today

In Germany, the ZEW indicator for January is released today. The assessment of the current situation remains low while expectations for future growth have improved slightly in recent months. The German economy started growing again in the final quarter of 2025 as fiscal spending is now finally kicking in. Therefore, we also see scope for an improvement in ZEW in January.

In the UK, the jobs report is released. Labour market data has been soft recently with job losses and unemployment edging higher. PMIs suggest the trend continues.

Economic and market news

What happened overnight

In China, the People's Bank of China kept the one-year and five-year loan prime rates unchanged at 3% and 3.5%, respectively. This was fully anticipated due to the stability of the 7-day reverse repo rate, which serves as a key policy benchmark. However, this could change soon, as the central bank has signalled further easing in 2026.

What happened yesterday

In the euro area, the EU finance ministers picked Boris Vujcic, Croatia's central bank chief, as the new ECB vice president succeeding Luis de Guindos on 1 June. While the European Parliament and ECB Governing Council must still be consulted before formal appointment, Vujcic is likely to secure the role, as finance ministers' decisions has historically been backed by the council. Competition for the six-member ECB executive board is highly political, with four positions, including the presidency, opening over the next two years. We anticipate that eurozone leaders will aim for a balanced composition of doves and hawks, similar to the current board. Vujcic, seen as a moderate hawk, may temporarily tilt the ECB's balance, allowing for a minor hawkish market reaction. However, given the consensus to keep the policy rate steady, we do not expect significant market impact.

In France, PM Lecornu confirmed plans to use article 49.3 to pass the 2026 budget without a majority in parliament. By passing the budget with article 49.3 the budget deficit in 2026 will likely be smaller than what would have been the result of a negotiation in parliament. After passing it with article 49.3, the government is going to face a no-confidence vote where the Socialist party will hold the pivotal votes in deciding the future of the government. All attention will thus be on comments from the Socialists leader regarding their voting intentions in the no-confidence vote. All else equal, a budget pass points to a tightening of the 10-year French-German government bond spread. However, this comes with the risk of a government collapse through a no-confidence vote.

In Japan, PM Takaichi called a snap election, pledging to suspend the 8% food levy for two years to ease rising living costs. Parliament will be dissolved on 23 January, and the election, set for 8 February, will decide all 465 lower house seats. Calling an early election may help Takaichi leverage public support and address the LDP coalition's narrow majority in the House of Representatives. The announcement sent the yield on the 10-year Japanese government bond to a 27-year high of 2.275%, as markets prepare for Takaichi to expand her fiscal policies if she secures victory.

In Sweden, surveyed money market CPIF inflation expectations for January dropped to 1.5% (prior: 1.6%) in one year according to Origo Group, reflecting the one-off impact from reduced food VAT tax. Two- and five-year expectations were roughly stable at 2.1%, which suggests that the drop in inflation this year is not expected to de-anchor longer-term expectations. In all, a good report for the Riksbank.

Equities traded lower yesterday, broadly in line with expectations. One notable exception was Asia, where markets ended higher despite the ongoing geopolitical escalation. Europe sold off, led by Denmark, which is fully consistent with Denmark being perceived as closer to the core of the current conflict. Importantly, this was not accompanied by a pronounced defensive rotation. The sell-off was broad-based. Yes, there was a marginal relative outperformance of defensives versus cyclicals, but nothing outside what could easily occur on any given trading day. Implied volatility measures moved higher, with both VIX and V2X. This is entirely textbook behaviour and underlines that investors are not necessarily pricing in a materially weaker economic outlook, but rather a more uncertain one. With VIX around 19, volatility is somewhat elevated relative to where we are in the economic cycle, yet still far from levels that would signal market stress. This morning, several Asian markets are again trading higher. European equity futures are marginally lower, while US futures are down around 1 percent, largely reflecting a catch-up to yesterday's move, as US markets were closed.

FI and FX: Market sentiment remains shaky amid the reignited EU/US trade war and the annual World Economic Forum in Davos. While aggregate market moves across asset classes all else equal have been relatively modest for a risk-off event, the "sell America" narrative is seeing a revival with a weaker USD, higher treasury yields (US cash market opening after yesterday's US holiday) and lower US equities. While long-dated government bond yields in Europe have been more stable or even risen slightly, European curves have generally bull steepened since the weekend as markets price in a larger potential impact on growth than inflation from the renewed trade war/Greenland concerns. Overall, Scandie FI has outperformed peers with especially short-end spreads moving lower.

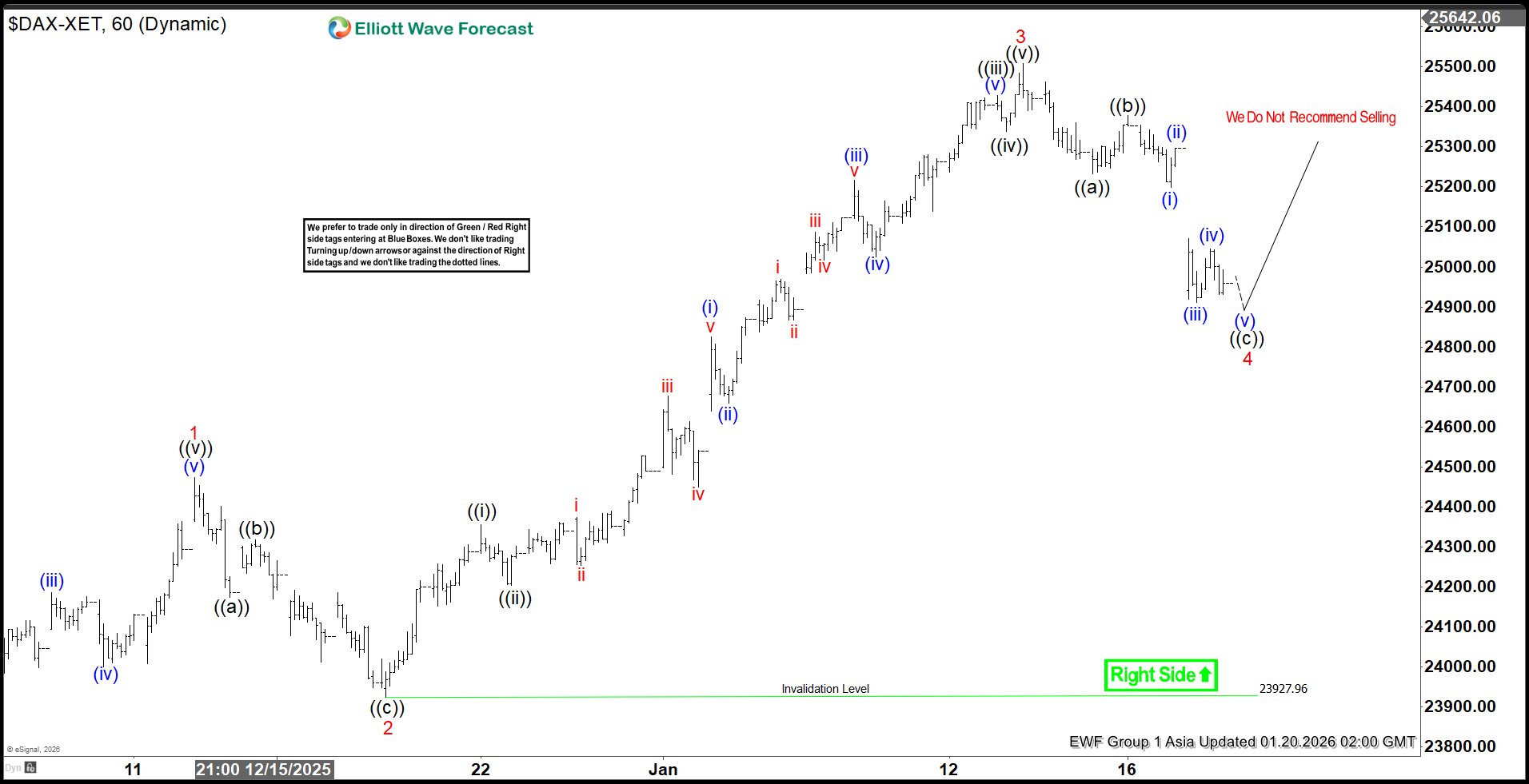

DAX Elliott Wave Outlook: Bullish Sequence Indicates Room to Rise

The DAX Index advanced in a clear three-swing rally from the November 21, 2025 low, reaching a new all-time high. Elliott Wave Theory states that a sustained trend typically develops in five waves, not three. The fresh high confirms strong bullish momentum, making it unlikely that the market would conclude its cycle with only three swings.

From the November low, wave 1 ended at 24,474.62. A corrective decline followed, with wave 2 finishing at 23,923.96. This pullback unfolded in a zigzag structure: wave ((a)) ended at 24,173.28, wave ((b)) at 24,318.30, and wave ((c)) at 23,927.96. The completion of this sequence marked the end of wave 2 at a higher degree.

The index then resumed higher in wave 3. From the termination of wave 2, wave ((i)) ended at 24,356.11, while wave ((ii)) retraced to 24,203.37. A strong rally in wave ((iii)) carried prices to 25,428.43. Wave ((iv)) corrected modestly to 25,338.30, and the final leg, wave ((v)), extended to 25,507.79. This completed wave 3 at a higher degree.

Currently, wave 4 is unfolding as a corrective phase. It is designed to adjust the cycle from the December 18, 2025 low before the next upward stage begins. In the near term, as long as the pivotal support at 23,927.96 remains intact, the expectation is for the decline to stabilize. Support is likely to appear in a three, seven, or eleven-swing structure, setting the stage for renewed upside momentum.

DAX 60 minute chart

DAX Elliott Wave video:

https://www.youtube.com/watch?v=OJp30YTw7Fs