Sample Category Title

Canada: Higher Inflation in December Due to Comparison to GST/HST Holiday Last Year

Headline CPI inflation ticked up slightly to 2.4% year-on-year (y/y) in December, slightly above consensus expectations. The acceleration was driven by the comparison to lower prices during the federal government's temporary sales tax holiday a year earlier.

The temporary GST/HST exemption in December 2024 applied to spending on restaurant food, alcoholic beverages, toys, games and hobby supplies, children's clothing and some grocery items, such as potato chips and confectionery.

Not surprisingly, the biggest lift to headline CPI came from restaurant meals (+5.8 y/y), which were exempt from sales taxes the year prior. Prices at grocery stores were flat on the month, but up 5.0% y/y due to hefty increases for beef and coffee.

There was some offset from prices at the pump, where prices were down 13.8% from a year ago in December.

Service inflation rose to 3.3% y/y in December, likely boosted by restaurant meals, but shelter inflation continued to cool (2.1% y/y). Prices for owned accommodation are up only 1.3% y/y – the slowest pace in 12 years. This has been helped both by smaller increases in mortgage interest costs (+1.7% y/y) and falling homeowners' replacement costs (-1.6% y/y).

The Bank of Canada has focused on broader "underlying inflation" recently, but the official core inflation metrics (median and trim), both cooled further in December, running at 2.6% y/y on average. Zeroing in on trends over the past three months, trim and median inflation were running at only 1.5% and 1.9% (annualized), now below the Bank of Canada's 2% target.

Key Implications

Headline inflation in December's was boosted by comparisons to last year's GST holiday, but zeroing in on core measures shows inflation in Canada has cooled. Underlying inflation is still above the 2% target on a year-on-year basis, but it is getting a lot closer in recent months.

Overall, December's data is consistent with our expectation for inflation to moderate to the Bank's target over the next year, as past inflation problem areas, like rents, continue to cool.

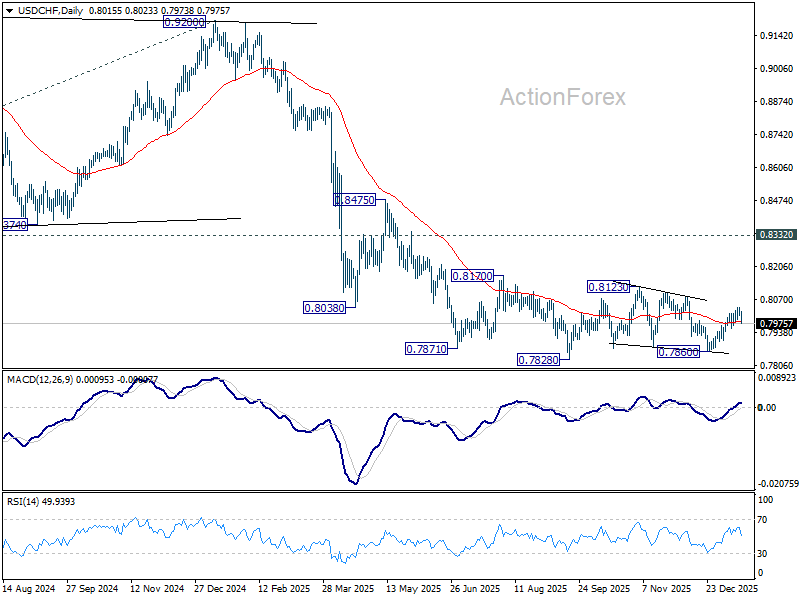

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8011; (P) 0.8026; (R1) 0.8045; More….

USD/CHF gyrates lower today but stays above 0.7954 support. Intraday bias remains neutral and another rise is in favor. On the upside, break of 0.8039 will resume the rally from 0.7860 for 0.8123 resistance However, break of 0.7954 support will argue that the rebound has completed, and turn bias back to the downside for 0.7860. Overall, corrective pattern from 0.7828 is extending.

In the bigger picture, price actions from 0.7828 are seen as a correction. Larger down trend from 1.0342 (2017 high) is still in progress. Break of 0.7828 will target 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

Europe Pushes Back as Greenland Tariff Threats Reshape Risk Outlook

Greenland dominated global headlines today as geopolitical risk surged back into focus. What had previously looked like an unusual diplomatic dispute escalated sharply over the weekend, forcing markets, governments, and corporates to reassess transatlantic relations and the risk of renewed trade war.

The escalation followed a pledge by US President Donald Trump to impose 10% tariffs from February 1 on eight European countries unless the United States is allowed to buy Greenland. Trump warned those tariffs could rise further, turning the dispute into a direct trade and political confrontation rather than a rhetorical standoff.

Greenland’s leadership moved quickly to push back. Prime Minister Jens-Frederik Nielsen said on Monday that the Arctic island would not be pressured by tariff threats. His comments followed weekend protests in Nuuk, where he joined demonstrators opposing U.S. efforts to take control of the self-governing Danish territory.

European capitals responded with unusual unity. Germany and France delivered a coordinated rejection of what they described as economic blackmail. German Finance Minister Lars Klingbeil said Europe would not allow itself to be coerced, while French Finance Minister Roland Lescure called tariff pressure between allies “obviously unacceptable.”

The United Kingdom struck a slightly more cautious tone. Prime Minister Keir Starmer warned that tariffs should not be used against allies, stressing that a tariff war is in nobody’s interest and that his priority was to prevent escalation rather than retaliate immediately.

Markets are now turning to the sectoral fallout. Europe’s automotive industry is widely seen as one of the most exposed, given deeply globalized supply chains and heavy reliance on manufacturing links across North America. Luxury stocks, which were largely insulated during earlier phases of U.S.–EU trade tensions, may not be immune this time. While demand from wealthy consumers tends to be resilient, the risk that tariffs trigger a broader economic slowdown could eventually spill over.

Europe’s pharmaceutical sector faces potentially more direct exposure. Medicines and pharmaceutical products represent the EU’s largest export category to the U.S., leaving the industry vulnerable should tariffs be applied broadly rather than selectively. Oil and gas could also face indirect pressure. Even if not targeted directly, weaker global demand expectations, softer crude prices, and higher supply-chain costs could weigh on the sector as geopolitical uncertainty rises.

On the policy front, EU governments are preparing a range of retaliatory options. These include tariffs on up to EUR 93 billion of U.S. goods and possible use of the Anti-Coercion Instrument (ACI), a framework approved in 2023 that allows far-reaching countermeasures beyond simple tariffs. The ACI is widely viewed as a “nuclear option.” It allows the EU to impose investment restrictions and limit the export of services, including those provided by U.S. digital giants, significantly broadening Europe’s leverage should confrontation deepen.

Elsewhere, political uncertainty is not limited to Europe. In Japan, Prime Minister Sanae Takaichi finally announced she will call a snap election on February 8, dissolving parliament this week. She framed the vote as a referendum on her leadership, saying she is staking her political future on securing a fresh mandate.

The election is centered on an aggressive fiscal and security agenda. Takaichi pledged a two-year suspension of the 8% consumption tax on food, alongside increased public spending aimed at boosting household demand and job creation. At the same time, her administration plans to unveil a new national security strategy later this year, accelerating Japan’s military build-up and lifting defense spending to 2% of GDP, a decisive break from decades of restraint near 1%.

In currency markets, risk-sensitive positioning reflected the uneasy backdrop. The Swiss Franc led gains on the day, followed by Kiwi and Aussie. Dollar lagged at the bottom, followed by Yen and Loonie. Euro and Sterling held mid-table.

Canada CPI rises to 2.4% in December tax effects

Canada’s inflation picture turned mixed in December, with headline pressure firming but core measures easing. CPI accelerated to 2.4% yoy, up from 2.2% and above expectations of 2.2%. According to Statistics Canada, the pickup in headline inflation was largely technical rather than demand-driven.

The acceleration was driven by base effects linked to the temporary GST/HST tax break that began in mid-December 2024. As exempt goods and services dropped out of the year-over-year comparison, this mechanically pushed headline CPI higher. That effect was partly offset by a year-over-year decline in gasoline prices. Excluding gasoline, CPI rose 3.0% yoy, up from 2.6% yoy in November.

Nevertheless, core measures offered reassurance. CPI median slowed from 2.8% to 2.5%, CPI trimmed eased from 2.9% to 2.7%, both below expectations. CPI common held steady at 2.8%. matched expectations.

Eurozone CPI finalized at 1.9% in December, regional gaps persist

Final inflation data confirmed that price pressures in the Eurozone continued to ease into year-end. Eurostat reported headline CPI at 1.9% yoy in December, down from 2.1% in November. Core inflation slowed modestly to 2.3% yoy from 2.4%.

Despite the overall cooling, inflation remained heavily services-led. Services accounted for +1.54pp of headline inflation, far outweighing contributions from food, alcohol and tobacco (+0.49pp) and non-energy industrial goods (+0.09pp). Energy prices continued to offset inflation pressures, subtracting -0.18pp.

At the EU level, CPI was finalized at 2.3% yoy, also easing from 2.4% previously. Disinflation was broad-based, with inflation falling in 18 countries, though dispersion remains notable. Inflation was lowest in Cyprus (0.1%), France (0.7%) and Italy (1.2%). Romania (8.6%), Slovakia (4.1%) and Estonia (4.0%) posted elevated readings.

China GDP growth slows to 4.5% in Q4, pressure builds for fresh stimulus

China’s economy slowed at the end of 2025, reinforcing concerns that headline growth masks deepening domestic weakness. GDP expanded 4.5% yoy in Q4, down from 4.8% in Q3, in line with expectations. For the full year, growth reached 5.0%, matching the government’s target, but momentum clearly faded as the year closed.

Officials were quick to acknowledge the strain. Kang Yi, head of the National Bureau of Statistics, described 2025’s performance as “hard-won,” citing persistent challenges from strong supply and weak demand—a combination that continues to weigh on private confidence.

Full-year investment data underscored the depth of the slowdown. Fixed asset investment fell -3.8% ytd yoy, marking the first full-year contraction since the 1990s. The property sector remained the biggest drag, with property investment plunging -17.2% and new construction starts down -20.4%, extending a downturn now in its fourth year. Private investment dropped -6.4%, reflecting weak profit incentives amid overcapacity and cautious households.

December activity data showed mixed signals. Industrial production rose 5.2% yoy, improving from November and beating expectations of 5.0%. But retail sales slowed to 0.9% yoy, missing 1.2% forecasts and reinforcing the message that consumption remains the economy’s main weak spot.

The Q4 slowdown increases pressure on Beijing to step up stimulus in 2026 to meet a growth target of 4.5–5.0%. Without a more decisive pivot toward households and consumption, growth is likely to settle in the low- to mid-4% range, forcing policymakers to confront one of the most persistent domestic demand slumps in decades.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8011; (P) 0.8026; (R1) 0.8045; More….

USD/CHF gyrates lower today but stays above 0.7954 support. Intraday bias remains neutral and another rise is in favor. On the upside, break of 0.8039 will resume the rally from 0.7860 for 0.8123 resistance However, break of 0.7954 support will argue that the rebound has completed, and turn bias back to the downside for 0.7860. Overall, corrective pattern from 0.7828 is extending.

In the bigger picture, price actions from 0.7828 are seen as a correction. Larger down trend from 1.0342 (2017 high) is still in progress. Break of 0.7828 will target 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

Canada CPI rises to 2.4% in December tax effects

Canada’s inflation picture turned mixed in December, with headline pressure firming but core measures easing. CPI accelerated to 2.4% yoy, up from 2.2% and above expectations of 2.2%. According to Statistics Canada, the pickup in headline inflation was largely technical rather than demand-driven.

The acceleration was driven by base effects linked to the temporary GST/HST tax break that began in mid-December 2024. As exempt goods and services dropped out of the year-over-year comparison, this mechanically pushed headline CPI higher. That effect was partly offset by a year-over-year decline in gasoline prices. Excluding gasoline, CPI rose 3.0% yoy, up from 2.6% yoy in November.

Nevertheless, core measures offered reassurance. CPI median slowed from 2.8% to 2.5%, CPI trimmed eased from 2.9% to 2.7%, both below expectations. CPI common held steady at 2.8%. matched expectations.

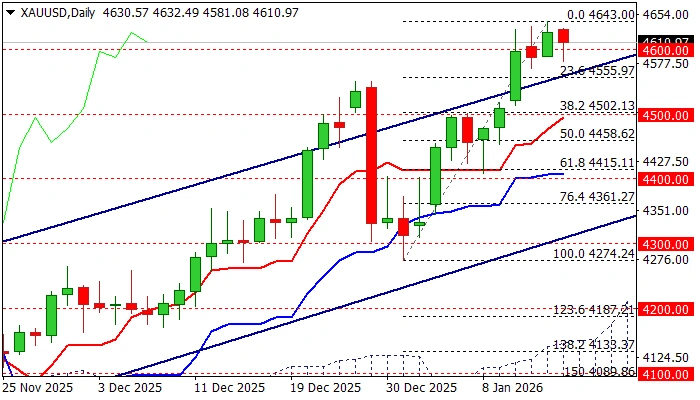

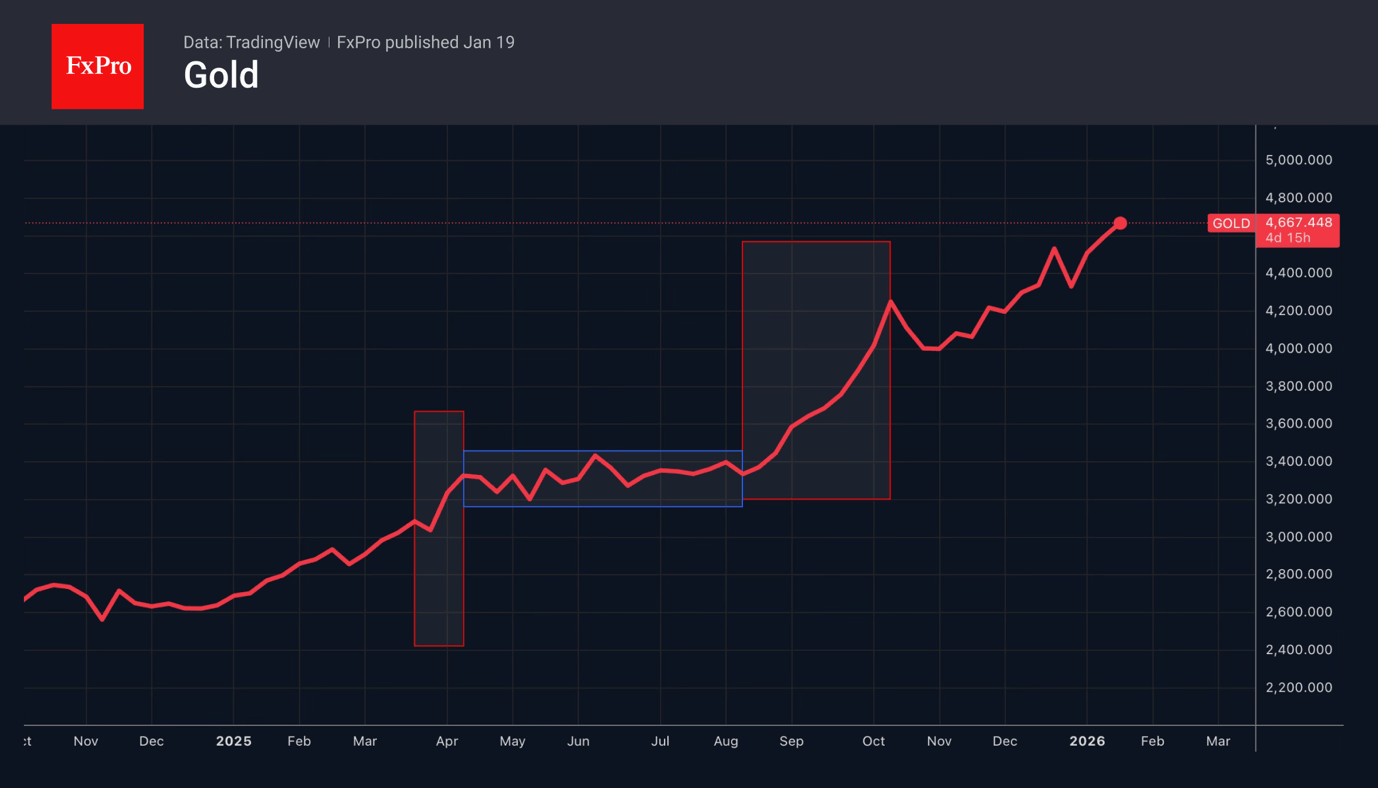

XAU/USD: Gold Rises to New Record High after Trump’s Latest Decisions Shocked Markets

Gold opened with gap higher and hit new record high ($4690) on Monday, after President Trump sent a series of shockwaves through the markets over the weekend by threats of imposing extra tariffs on several EU countries, with European leaders started preparations to retaliate that further escalated already heated situation over Greenland.

The western world entered new dimension of existing geopolitical crisis on growing risk of conflict between NATO allies, which adds to growing tensions over Iran, recent US attack on Venezuela and the war in Ukraine that enters fourth year.

Political divisions and clouded economic outlook for the most of developed economies, further clouds overall picture.

The latest developments (which were quite predictable to analysts) sparked fresh migration into safety of precious metals.

The price is establishing above $4600 level, despite weekly close marginally below here ($4596) with next round-figure barrier ($4700) now being under increased pressure (after early Monday’s rally stalled just $10 below this level).

Technical picture on daily chart remains firmly bullish, though with warning from overbought conditions that may pause rally for consolidation.

Near-term action so far holds within a narrow consolidation range above $4650, guarding session low ($4620) and psychological $4600 support, where dips should ideally find firm ground for fresh attempts higher.

Dip below $4600, on the other hand, would open way for deeper pullback and expose next strong supports at $4550 (former tops of Dec 26/29) and $4500 (round figure).

Res: 4700; 4721; 4761; 4800.

Sup: 4650; 4620; 4600; 4562.

Greenland as the Trigger of a New Trade War

- The Greenland dispute risks triggering a renewed EU–US trade war, with the US threatening tariffs of up to 25 per cent unless Denmark agrees to sell Greenland.

- New US tariffs would effectively dismantle last summer’s EU–US trade truce, despite legal uncertainty over their validity.

- Germany is particularly exposed: exports to the US are already sharply lower, and higher tariffs could significantly hit GDP.

- The conflict also weakens confidence in the US dollar, as markets fear long-term erosion of its global role due to politicised trade policy.

An escalation that goes beyond trade

A new trade dispute between the European Union and the United States, triggered by the conflict over Greenland, is sharply increasing the risk of a lasting deterioration in transatlantic relations. Donald Trump has announced plans to impose tariffs of 10 per cent on imports from eight European countries (including Germany and France) from 1 February, with the threat of raising them to 25 per cent from June. According to Washington, avoiding further escalation would require Denmark to agree to the sale of Greenland to the United States.

A trade agreement under question

If implemented, these measures would effectively dismantle the EU - US trade agreement reached last summer, which was designed to freeze the earlier tariff dispute and cap US duties at 15 per cent. The legal basis for new tariffs in the United States remains highly uncertain, and the Supreme Court is expected to rule soon on the validity of many existing measures. Nevertheless, past experience suggests that legal uncertainty rarely constrains the Trump administration’s use of tariffs as a political tool.

Security arguments or domestic politics

The official White House narrative frames the issue in terms of security, arguing that Greenland faces growing threats from China and Russia. This claim is weak, given that the United States already enjoys extensive rights on the island, including military deployments, base construction, surveillance of shipping routes and access to natural resources. It therefore seems more plausible that the escalation is driven by domestic political considerations, including the desire to divert attention from internal challenges and to cultivate the image of a president who expands US territory and influence.

A big risk for Germany

For Germany, the dispute comes at a particularly unfavourable time. Even after the introduction of reciprocal tariffs last year, German exports to the United States fell markedly. In November 2025, the value of German goods exports to the US was over 20 per cent lower than a year earlier. Estimates indicate that the current 15 per cent tariff regime could reduce German GDP by around 0.3 per cent, while an increase to 25 per cent - would deliver a significantly stronger negative shock.

Limited options for the European Union

The sale of Greenland has been firmly rejected by both Denmark and Greenland’s own authorities. Brussels may continue to pursue diplomatic de-escalation, for instance by offering a stronger NATO presence or expanded security cooperation. However, the scope for compromise appears limited. As a result, the likelihood of a renewed trade conflict is rising, ranging from a formal rejection of the existing agreement with the United States to retaliatory tariffs and, ultimately, the use of anti-coercion instruments against major US corporations.

The risk of escalation remains high

A major obstacle is the lack of consensus within the EU. While some member states and influential Members of the European Parliament favour a tougher response, others (less exposed to economic damage) see little benefit in reigniting the conflict. As a consequence, although diplomatic de-escalation cannot be ruled out, the probability of a renewed trade war has clearly increased. The dispute over Greenland may thus become the catalyst for a broader and more damaging economic confrontation, with particularly severe and long-lasting consequences for Germany and the European economy as a whole.

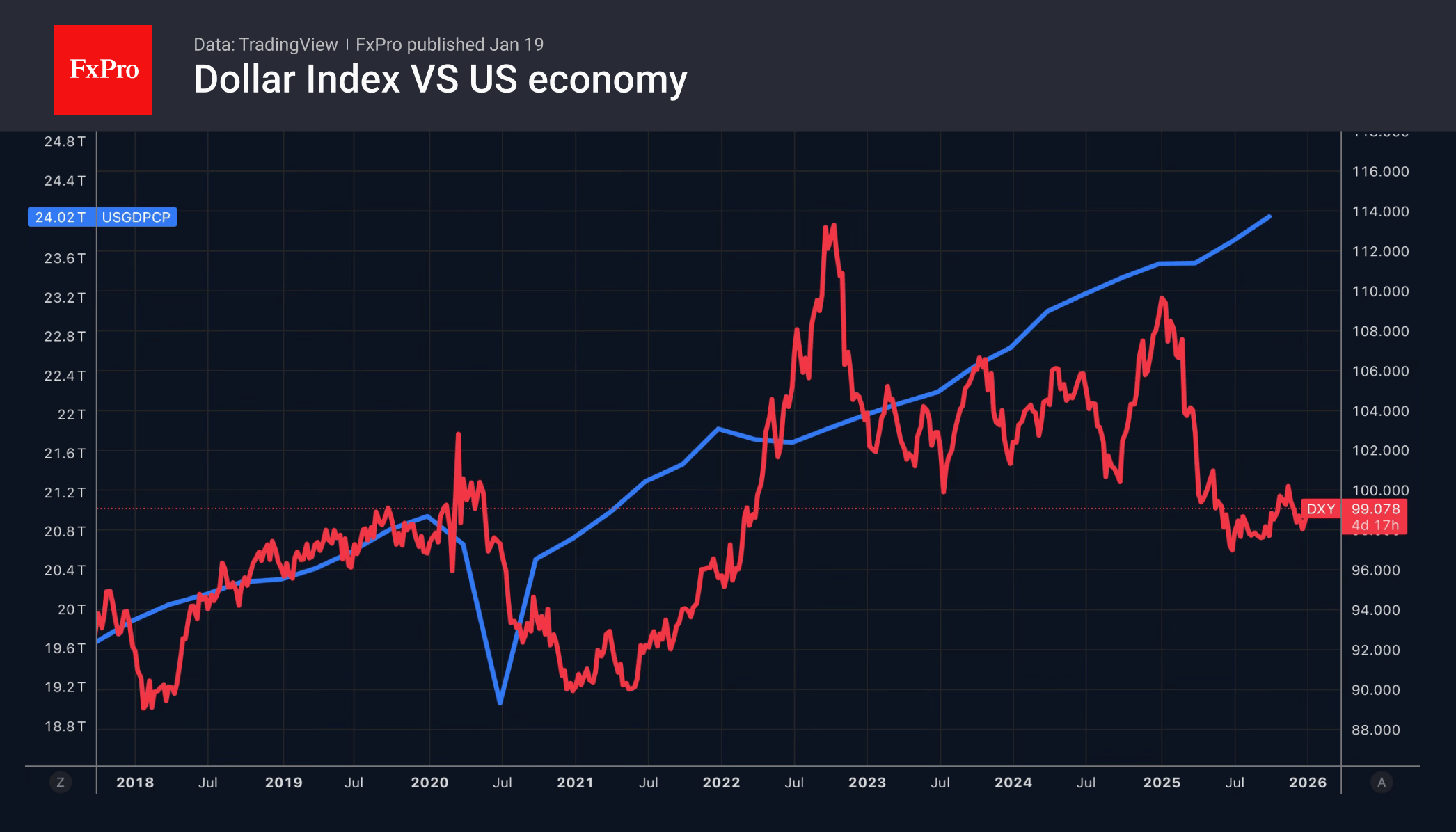

Dollar weakens as tariff threats revive structural concerns

Chart of the US dollar index, daily data, source: TradingView

The US dollar weakened today as markets reassessed the implications of Washington’s renewed tariff threats. Until now, the dollar had been supported by a slower-than-expected increase in trade barriers and by strong investment flows into new technologies, while investors assumed that any escalation would hurt Europe more than the United States. That sense of resilience is now being questioned. Beyond the immediate trade impact, markets are increasingly alert to the longer-term risk that more frequent use of tariffs and economic pressure could undermine the dollar’s role as the world’s dominant currency, encouraging trading partners to reduce their reliance on dollar-based transactions in order to limit political exposure.

European stocks slide on fresh US tariff threats

Chart of a CFD contract based on the DAX index, daily data, source: TradingView

European equities came under strong pressure on Monday after Donald Trump threatened to impose new tariffs on eight European countries. The Stoxx Europe 600 fell by roughly 1 per cent, reflecting broad weakness in trade-sensitive and risk-exposed stocks. National benchmarks also declined, with France’s CAC 40 down about 1.6 per cent, Germany’s DAX lower by around 1.35 per cent, and the UK’s FTSE 100 easing roughly 0.52 per cent, as investors sold off automakers, luxury names and other export-driven sectors.

Impact on US-EU tensions: Risk-off, US Dollar Subdued, Heightened Demand for Gold and Silver

Key takeaways

- Geopolitical escalation drives risk-off: Trump’s tariff threats against key NATO allies over Greenland have sharply intensified US–EU tensions, prompting EU retaliation plans and triggering a broad risk-off move across global equities, particularly in Asia and US index futures.

- US dollar weak, safe havens surge: Despite risk aversion, the US dollar failed to benefit as the “debasement trade” narrative took hold. Capital rotated into precious metals, with gold and silver surging to fresh record highs.

- Technical damage to equities, bullish momentum with metals: US Nasdaq 100 and European indices (DAX) show near-term technical breakdowns or mean-reversion risks, while gold and silver maintain bullish acceleration, reinforcing their role as primary geopolitical hedges.

“Tarriff Man” is backed with a vengeance. After the “capture” of Venezuela at the start of the new year via the forceful removal of Venezuela’s leadership and the seizure of oil assets to be placed under US control, Trump has set sight on Greenland next, the resource-rich Arctic territory under Denmark’s autonomous control.

Trump has escalated his confrontational foreign policy stance by deploying tariff threats against long-standing US allies within NATO, leveraging trade pressure in a dispute over sovereignty and control of Greenland.

Trump has threatened eight opposing NATO members over the weekend, including France, Germany, and the UK, with a 10% tariff from 1 February, rising to 25% in June, unless they agree to facilitate a US purchase of Greenland.

EU is in discussion of additional retaliation measures against US

In retaliation, the EU looks set to void the US-EU trade truce deal agreed last year, as France plans to push the EU to activate its most powerful trade retaliation tool, the anti-coercion instrument, to be used for the first time against the US.

All in all, EU officials have aimed to introduce more retaliatory measures, such as new taxes on tech companies or targeted curbs on investments in the EU, beyond the earlier suspended tariffs on 93 billion euros of US products, to counter the US’s pressure on Greenland.

To add fuel to the fire, key US White House officials have continued to back Trump, with the US Treasury Secretary Bessent reiterated that the US will not back down on taking over Greenland, citing that the EU is too weak to ensure its security.

The first reaction is a risk-off sentiment in today’s Asia session at the start of a brand-new trading week, where major Asia Pacific stock markets traded lower, including Japan’s Nikkei 225, and Hong Kong’s Hang Seng Index slipped by 0.6% and 1% in line with the intraday losses of 1% to 1.3% seen on the S&P 500 and Nasdaq 100 E-mini futures at the time of writing.

The US dollar does not benefit from this current episode of risk-off as the “debasement trade” narrative takes hold due to the latest US foreign policy towards its European allies, as traders shifted demand towards safe-haven precious metals. The US Dollar Index dropped by -0.2% intraday, while gold and silver rocketed by 1.6% and 3.5% respectively to hit fresh record highs.

Here are five intraday (hourly) technical setups on key cross-assets (Nasdaq 100, Hang Seng Index, Germany DAX, Gold & Silver) to watch as the trading session unfolds today in the aftermath of the US trade tariffs threat towards the EU.

Nasdaq 100 bearish breakdown below 20-day and 50-day moving averages

Fig. 1: US Nasdaq 100 CFD index minor trend of 19 Jan 2026 (Source: TradingView)

The price actions of the US Nasdaq 100 CFD index (a proxy of the Nasdaq 100 E-mini futures) have tumbled below its 20-day and 50-day moving averages, as well as the ascending channel support from the 21 November 2025 low.

These latest observations suggest that the earlier medium-term uptrend phase of the US Nasdaq 100 CFD index has been damaged and the likely control shifted back to the bears at least in the near-term (see Fig. 1).

Watch the 25,550 key short-term pivotal resistance (also the gapped down formed at the start of today’s Asian session and the 20-day moving average) to maintain the short-term bearish bias to expose the next intermediate supports at 25,133, and 24,870 (close to 76.4% Fibonacci retracement of the prior minor up move from 18 December 2025 low to 13 January 2026 high).

On the other hand, a clearance and an hourly close above 25,550 invalidates the bearish tone for a retest on the stubborn range resistance of 25,760/25,830 in place since 8 December 2025.

Minor mean reversion decline in progress for the Hang Seng Index

Fig. 2: Hong Kong 33 CFD index minor trend of 19 Jan 2026 (Source: TradingView)

The medium-term uptrend of the Hong Kong 33 CFD index (a proxy of Hong Kong’s Hang Seng Index futures) remains intact as price actions continue to oscillate above its 20-day and 50-day moving averages.

Right now, the recent three bearish reactions from its recent minor range resistance of 27,175 from 13 January to 16 January 2026 have skewed the bias for a potential minor mean reversion decline scenario to seek a retracement back to retest the area around the 20-day and 50-day moving averages (see Fig. 2).

Watch the 26,870 key short-term pivotal resistance to expose the next intermediate supports at 26,330, 26,220 (also the 20-day moving average), and even 26,045 (also the 50-day moving average).

On the flip side, a clearance and an hourly close above 26,870 negates the bearish tone for a retest on the 27,175 minor range resistance in the first step.

Germany's DAX broke below last week’s low, on track towards 20-day MA

Fig. 3: Germany 30 CFD index minor trend of 19 Jan 2026 (Source: TradingView)

The Germany 30 CFD index (a proxy of the DAX futures) gapped down and broke last week’s minor range support of 25,260.

The odds are now skewed towards a minor mean reversion decline towards its 20-day moving average and the medium-term ascending trendline in place from the 21 November 2025 low.

Overall, the medium-term uptrend remains intact with potential intraday weakness in the first step before a renewed bullish move materializes.

Watch the 25,260 key short-term pivotal resistance for a potential intraday drop to expose the next intermediate supports at 24,860 and 24,760/24,670 (also the 20-day moving average) (see Fig. 3).

However, clearance and an hourly close above 25,260 invalidates the bearish tone to seek a retest on the current all-time high area of 25,505, and above it sets sight on the next immediate resistance at 25,800 (Fibonacci extension).

Gold (XAU/USD) bullish acceleration mode

Fig. 4: Gold (XAU/USD) minor trend of 19 Jan 2026 (Source: TradingView)

The current price actions of Gold (XAU/USD) gapped up at the opening of today’s Asian session with a parallel bullish breakout above its former descending trendline resistance seen on its hourly RSI momentum indicator.

These observations suggest a potential minor bullish acceleration phase for Gold (XAU/USD). Watch the US$4,595 key short-term pivotal support; a clearance above US$4,684/4,687 near-term resistance opens scope for the next intermediate resistances to come in at US$4,720 and US$4,774/4,780 (see Fig. 4).

On the other hand, a break with an hourly close below US$4,595 negates the bearish tone for a minor corrective decline towards its 20-day moving average, exposing the next intermediate supports at US$4,560/4,550 and US$4,512.

Silver (XAG/USD) relentless uptrend remains intact

Fig. 5: Silver (XAG/USD) minor trend of 19 Jan 2026 (Source: TradingView)

Watch the US$86.26 key short-term pivotal support on Silver (XAG/USD) to maintain a potential direct intraday rise scenario for the next intermediate resistances to come in at US$94.60/95.81 and US$98.74/99.47 (also the upper boundary of a minor ascending channel) (see Fig. 5).

On the flip side, failure to hold at US$86.26 and an hourly close below it negates the bullish tone for a minor corrective decline towards the medium-term pivotal support area of US$81.70/78.84 (also the 20-day moving average).

Trade War Risks Resurface

- The US imposes tariffs on EU countries over Greenland.

- Gold rises to record highs following last year’s pattern.

Just as confidence in the US dollar began to return, Donald Trump dealt it two significant blows. The greenback coped with the first lawsuit against Jerome Powell. However, the White House’s introduction of 10% tariffs against several European countries, with the risk of them rising to 25% by the summer, forced the bears on EURUSD to retreat.

History now repeats itself. In October 2024, ahead of the presidential election, Wall Street Journal experts expected the US economy to grow by 2.1% in 2025. However, due to tariffs, they were forced to lower their forecast to 1.8% in April. Their January estimate for 2026 is 2.2%. The trade war between the US and the EU risks significantly reducing it. The absorption of import duties by Americans is fraught with a resumption of the cooling process in the labour market. This will force the Fed to return to the topic of easing monetary policy. It’s becoming clear why investors are buying EURUSD again.

The main reasons for the USD index rally at the start of the year were the Fed’s prolonged pause in its rate cuts, the wide interest rate differential and the gradual return of confidence. Investors value reliable places to park their money, especially the US Treasury bond market. High political control over central banks in countries such as Turkey has triggered uncontrollable inflation. If this experience is repeated in the United States, it will change the role of Treasuries in the global debt market and undermine confidence in the greenback.

The escalation of risks of a new trade war between the US and the European Union allowed gold to renew its record high with a sense of déjà vu. Precious metals reacted to the massive tariffs on America’s Liberation Day in April 2025 with a violent rally to new historic highs. Then, as TACO-trade, or ‘’Trump always chickens out’’ flourished, gold quotes entered a prolonged consolidation. It took Powell’s signals in Jackson Hole on more rate cuts soon in August for the precious metal to renew its growth.

Investors now have a good template to use against the backdrop of a potential slowdown in the US economy due to tariffs. However, this time the European Union may respond to the United States, which will result in a full-blown trade war.

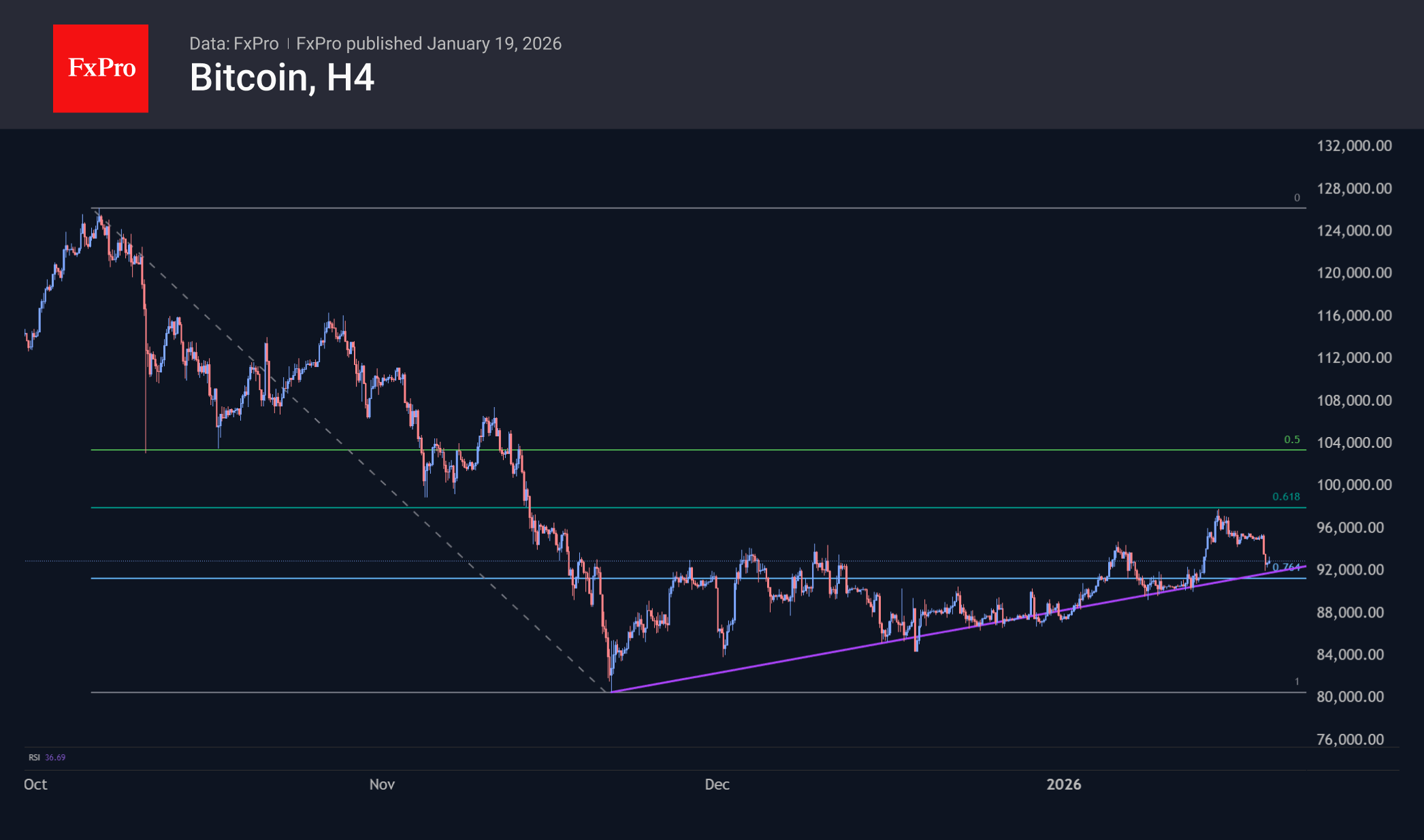

Crypto Fell Due to Risk Aversion, But Remained Within Consolidation

Market Overview

The crypto market cap fell by more than 3% on Monday morning at the start of the Asian session, following a sell-off of risky assets in traditional markets after mutual tariff threats between the US and the EU over the weekend. Interestingly, the crypto market, which traded throughout the weekend, ignored this news.

Bitcoin plunged 3.8% shortly after the opening of trading in Asia, reducing losses to 2.5% during trading in Europe. Bears are pushing their agenda, forming powerful downward momentum during the lowest liquidity. This allows them to form frightening candlesticks on the charts and trigger stop orders. Technically, the first cryptocurrency remains within the rebound range after the October-November sell-off. At the same time, the downward momentum has not broken the upward trend passing through the lows of November and December last year.

News Background

According to SoSoValue, net inflows into spot BTC ETFs amounted to $1.42 billion for the week, the highest since October. Since January 2024, total inflows have amounted to $57.82 billion. Net inflows into spot Ethereum ETFs in the US also rose by a notable $479 million for the week. The cumulative net inflow since July 2024 has been $12.91 billion. Inflows into the recently launched spot Solana ETFs in the US have continued for 12 consecutive weeks, with a total of $0.86 billion invested, which is less than the $1.28 billion that XRP ETFs have received over the past 10 weeks.

Ethereum user activity is breaking records. According to Etherscan, on 15 January, the number of addresses on the network exceeded 1 million, which is more than twice last year’s figures. At the same time, a new peak in daily transactions was recorded — 2.8 million.

According to Chainalysis, Iranian residents have sharply increased their purchases of Bitcoin amid a record fall in the national currency and mass unrest.

Bitcoin will collapse over the next 7–11 years, said Cyber Capital founder Justin Bons. In his opinion, BTC must either double in price every four years or significantly increase the volume of online commissions collected.

According to CoinGecko, over the past year, more than 11.6 million tokens have collapsed due to volatility and the collapse of the meme coin sector. The year 2025 set an anti-record, accounting for 86.3% of failed projects for the period from 2021 to 2025.

The monthly volume of payments using cryptocurrency cards has grown 15 times over the past three years, to $1.5 billion, according to Artemis.

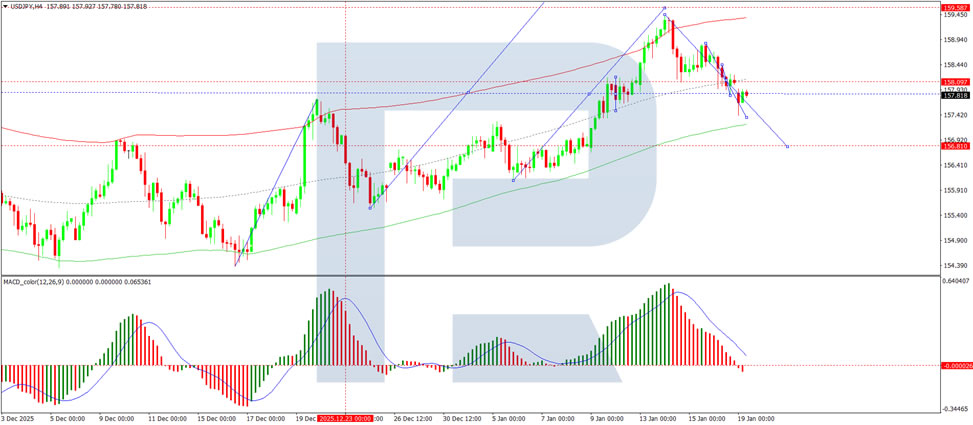

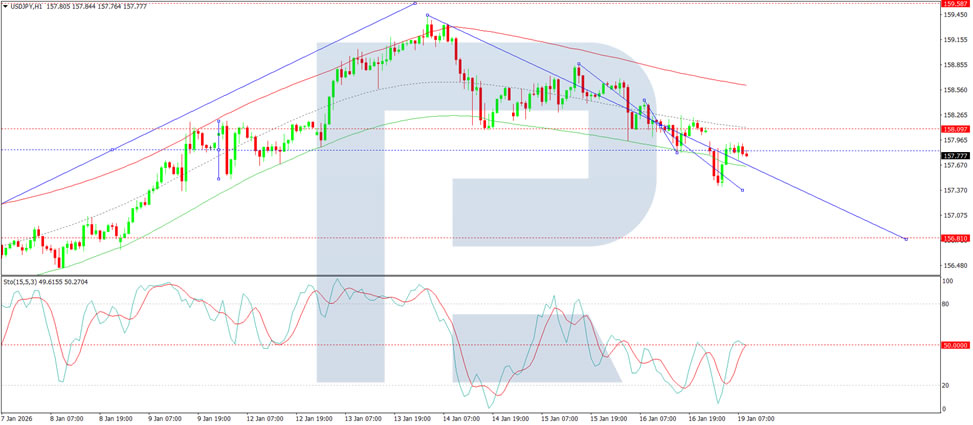

USD/JPY: Market Nerves Build Ahead of BOJ Decision and Political Tensions

USD/JPY is holding steady at 157.93 on Monday, with the Japanese yen attempting to strengthen amid volatile movements. Demand for defensive assets has increased as geopolitical and trade risks resurface.

U.S. President Donald Trump has threatened new tariffs against eight European countries in response to tensions over Greenland. These remarks have sparked backlash from European leaders and heightened market uncertainty.

Domestic attention is also focused on the upcoming Bank of Japan (BOJ) meeting, where the market expects the central bank to maintain its current policy stance. Investors are looking to June as a potential timeline for the first rate hike. Adding to the uncertainty, rumors about early elections in Japan are circulating. Prime Minister Sanae Takaichi may announce elections next month to consolidate his position and promote a more flexible budget policy. As part of his campaign, Takaichi is also considering temporarily suspending the 8% food sales tax to ease the burden of rising food prices.

Technical Analysis:

On the H4 chart, USD/JPY is consolidating around the 158.10 level, with the market recently breaking down from this range. A potential decline to 156.81 is in focus, with a rebound to 158.10 possible after reaching that level. The MACD indicator supports this bearish outlook, as its signal line remains below the zero mark and points downward.

On the H1 chart, a downward wave towards 157.36 is forming, with a possible correction to 158.10 before another decline to 156.81. This scenario is confirmed by the Stochastic oscillator, which shows the signal line descending towards the 20 level.

Conclusion:

USD/JPY remains in a consolidation phase, with the market reacting to both domestic and international uncertainties. Investors are closely watching the BOJ meeting and the potential for political developments in Japan. Technically, the pair is showing signs of short-term bearishness, with further declines possible in the near term.