Sample Category Title

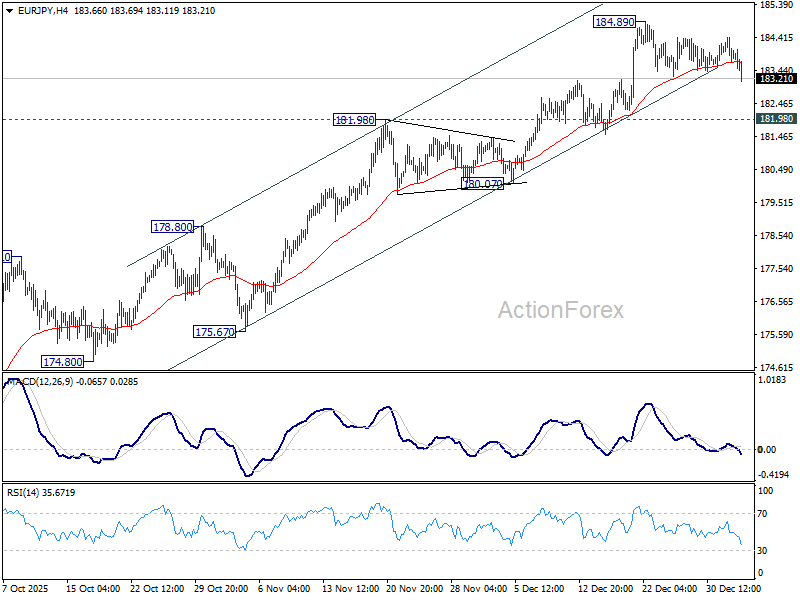

EUR/JPY Daily Outlook

Daily Pivots: (S1) 183.54; (P) 183.99; (R1) 184.26; More...

EUR/JPY dips notably today but stays well above 181.98 resistance turned support. Intraday bias stays neutral and further rally is still expected. On the upside, firm break of 184.89 will resume larger up trend to 186.31 long term projection level.

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. Considering bearish divergence condition in D MACD, upside could be capped by 186.31 on first attempt. Still, outlook will stay bullish as long as 55 W EMA (now at 172.16) holds, even in case of deep pullback. Sustained break of 186.31 will pave the way to 100% projection at 205.81 next.

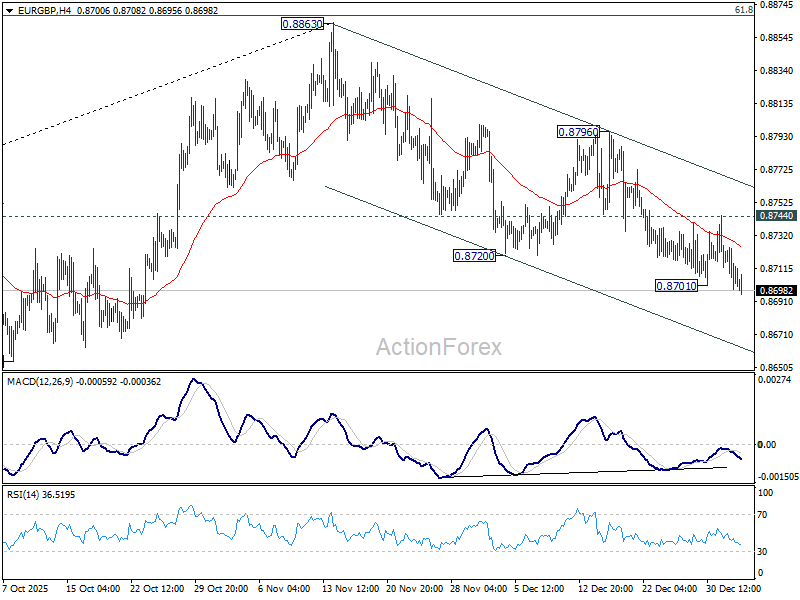

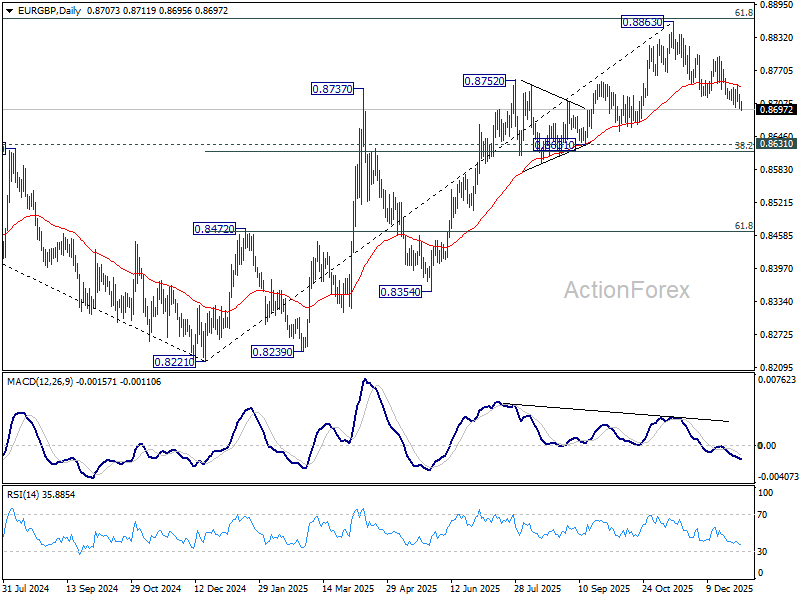

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8695; (P) 0.8713; (R1) 0.8726; More…

EUR/GBP's fall from 0.8863 resumed by breaking 0.8701 and intraday bias is back on the downside. Further fall should be seen to 0.8631 cluster support (38.2% retracement of 0.8221 to 0.8663 at 0.8618). On the upside, though, firm break of 0.8744 will indicate short term bottoming, and turn bias back to the upside for 0.8796 resistance.

In the bigger picture, rise from 0.8221 medium term bottom is still seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Sustained trading below 55 W EMA (now at 0.8617) should confirm that this corrective bounce has completed. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high). That should pave the way back to 0.9267.

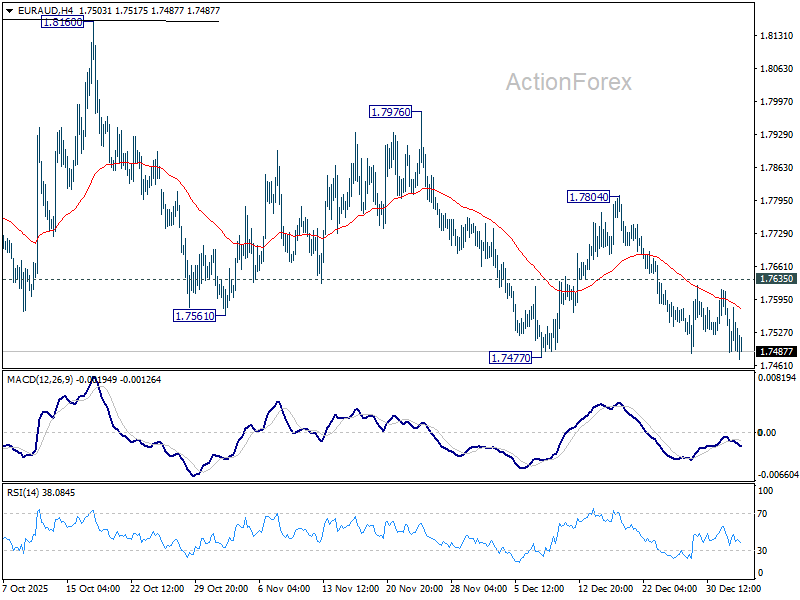

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7457; (P) 1.7540; (R1) 1.7590; More...

Intraday bias in EUR/AUD stays neutral for the moment. On the downside, firm break of 1.7477 will resume the whole decline from 1.8160, and target 1.7245 support and below. Nevertheless, break of 1.7635 minor resistance will turn bias back to the upside for stronger rebound back to 1.7804. Overall, corrective pattern from 1.8554 is still extending.

In the bigger picture, as long as 55 W EMA (now at 1.7472) holds, price actions from 1.8554 could still be a correction to rise from 1.5963 only. However, sustained break of the EMA will argue that it's already correcting the whole up trend from 1.4281 (2022 low). In this case, deeper decline would be seen to 38.2% retracement of 1.4281 to 1.8554 at 1.6922.

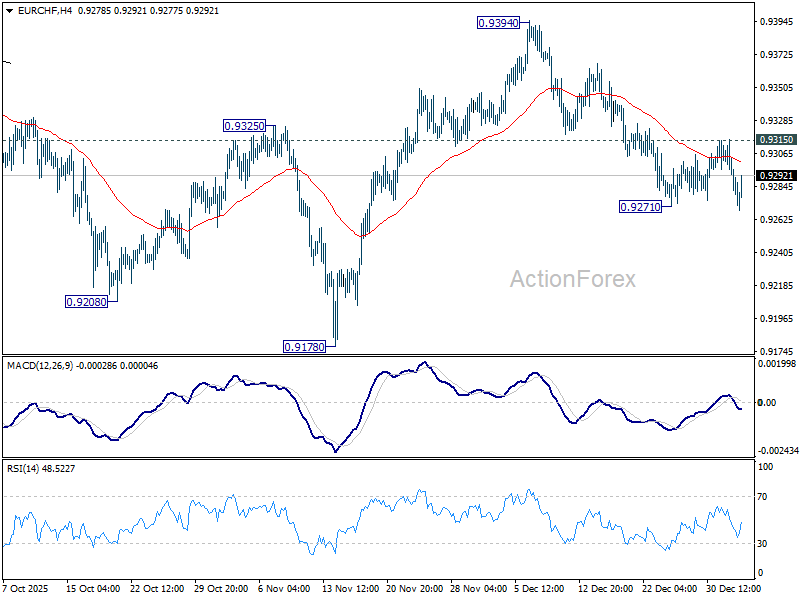

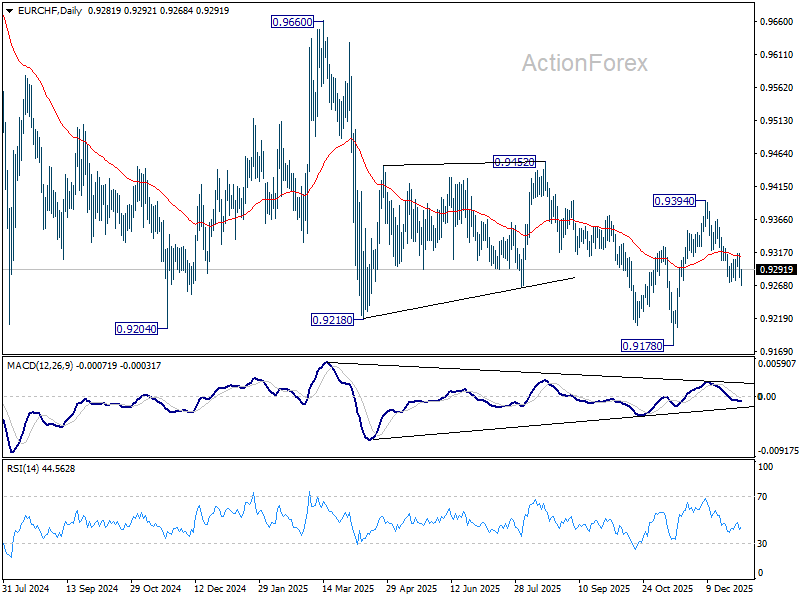

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9271; (P) 0.9297; (R1) 0.9312; More....

No change in EUR/CHF's outlook and intraday bias stays neutral. On the downside, firm break of 0.9271 will resume the fall from 0.9394. Next target should be a retest of 0.9178 low. However, firm break of 0.9315 will bring stronger rise back to retest 0.9394 resistance.

In the bigger picture, EUR/CHF has breached long term falling channel resistance as the rebound from 0.9278 extends. Considering bullish convergence condition in W MACD, sustained trading above 55 W EMA (now at 0.9366) will indicate medium term bottoming at 0.9178, and suggests that it's already in larger scale rebound. Further break of 0.9452 resistance will bring stronger medium term rally towards 0.9928 resistance next. Nevertheless, rejection by 55 W EMA will retain bearishness for another fall through 0.9178 at a later stage.

GBP/USD and EUR/GBP Struggle Near Resistance, Caution Builds

GBP/USD failed to climb above 1.3500 and corrected some gains. EUR/GBP is declining and trading below the 0.8725 support zone.

Important Takeaways for GBP/USD and EUR/GBP Analysis Today

- The British Pound is showing bearish signs below 1.3500.

- There is a key bearish trend line forming with resistance near 1.3470 on the hourly chart of GBP/USD at FXOpen.

- EUR/GBP is declining and showing bearish signs below 0.8725.

- There is a connecting bearish trend line forming with resistance at 0.8705 on the hourly chart at FXOpen.

GBP/USD Technical Analysis

On the hourly chart of GBP/USD at FXOpen, the pair started a fresh decline after it failed to stay above 1.3500. The British Pound traded below 1.3460 to enter a short-term bearish zone against the US Dollar.

There was a clear move below 1.3435. The pair even settled below 1.3430 and the 50-hour simple moving average. A low was formed at 1.3414, and the pair is now consolidating losses. On the upside, the GBP/USD chart indicates that the pair is facing resistance near the 23.6% Fib retracement level of the downward move from the 1.3502 swing high to the 1.3414 low at 1.3435.

The next key sell zone could be 1.3460 and the 50% Fib retracement. The main hurdle for the bulls might be near a bearish trend line at 1.3470. A close above 1.3470 could open the doors for a move toward 1.3500.

If the pair fails to recover, it could start another decline. On the downside, there is a key support forming near 1.3400. If there is a downside break below 1.3400, the pair could accelerate lower.

The next major area of interest might be 1.3360, below which the pair could test 1.3320. Any more losses could lead the pair to 1.3250.

EUR/GBP Technical Analysis

On the hourly chart of EUR/GBP at FXOpen, the pair struggled to gain pace for a move above 0.8750. The Euro settled below 0.8725 and started a fresh decline against the British Pound.

There was a clear move below the 0.8720 pivot level. The EUR/GBP chart suggests that the pair settled below the 50-hour simple moving average and 0.8720. A low is formed near 0.8696, and the pair is now consolidating losses.

Immediate resistance is near the 23.6% Fib retracement level of the downward move from the 0.8745 swing high to the 0.8696 low at 0.8705. There is also a connecting bearish trend line forming at 0.8705.

The next key breakout zone might be 0.8725 and the 61.8% Fib retracement. A close above 0.8725 might accelerate gains. In the stated case, the bulls may perhaps aim for a test of 0.8750. Any more gains might send the pair to 0.8780.

Immediate support sits near 0.8695. The next key area for the bulls sits at 0.8680. A downside break below 0.8680 might call for more losses. In the stated case, the pair could drop to 0.8650.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Forex Runs to Safe Havens

- Growing political risks in Britain are putting pressure on European currencies.

- Geopolitics are reviving investor interest in gold.

The rise in geopolitical risks against the backdrop of the kidnapping of Venezuelan President Nicolas Maduro by the US has increased demand for the US dollar as a safe-haven currency. Coupled with expectations of a prolonged pause in the Fed's monetary expansion cycle and political turmoil in Europe, this has allowed EURUSD bears to mount a counterattack and push the pair below 1.17.

The futures market estimates the chances of a cut in the federal funds rate at the January FOMC meeting at 17% and 48% at the March meeting. The Fed intends to sit on the sidelines until at least spring. This plays into the hands of the US dollar. It is strengthening against major world currencies amid a wide spread between US bonds and their European and Asian counterparts.

Moreover, there are signs of trouble brewing in Europe. Keir Starmer's approval rating has fallen to its lowest level among all British prime ministers in the last half-century. It is worse than that of Liz Truss, who is known for her quick resignation due to turmoil in the financial markets. As a result, the Labour Party is discussing a change of leader. Keir Starmer warns that his removal from power will plunge the country into complete political chaos and open the door to Nigel Farage, who is leading in the polls, for a new prime minister.

The rise in political risks in Britain is putting pressure not only on the pound but also on other European currencies. Following GBPUSD, EURUSD is falling off a cliff.

Politics and geopolitics are forcing investors to seek safe havens. The best option appears to be gold, which shone in 2025. The precious metal managed to rebound from local lows thanks to a spectacular operation by US special forces in Venezuela. Investors successfully bought up the dip in the XAUUSD pair. However, the market may quickly come to the conclusion that events in Latin America will have a muted impact on both the global economy and oil. Venezuela, with its production falling from 3.5 million bpd in the 1970s to 1 million bpd today, is only the 18th largest producer of black gold in the world.

If investors decide that the regime change in Caracas will not lead to turmoil, they will dump safe-haven assets. At the same time, pressure on gold may come from the strengthening of the US dollar amid a prolonged pause in the Fed's cycle of monetary policy easing.

The Australian dollar appears to be the favourite thanks to expectations of a key rate hike by the Reserve Bank and the Chinese economy's adaptation to US tariffs.

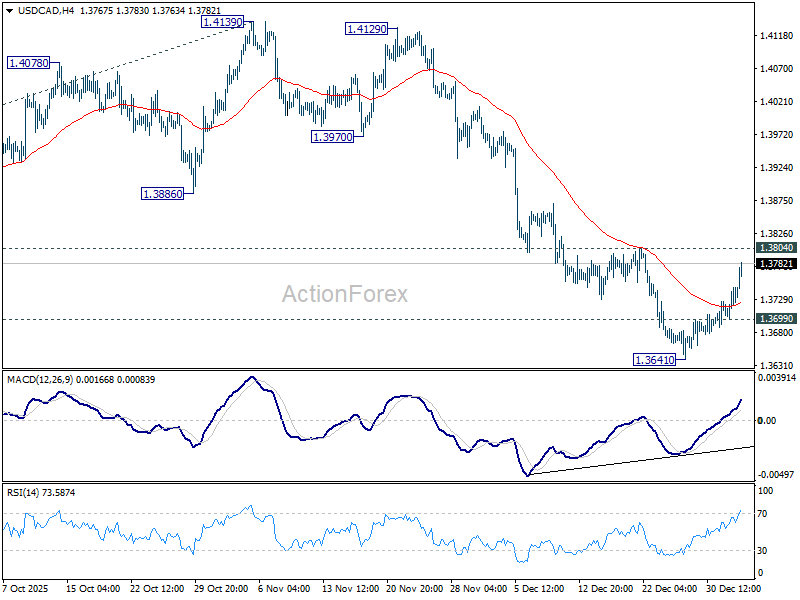

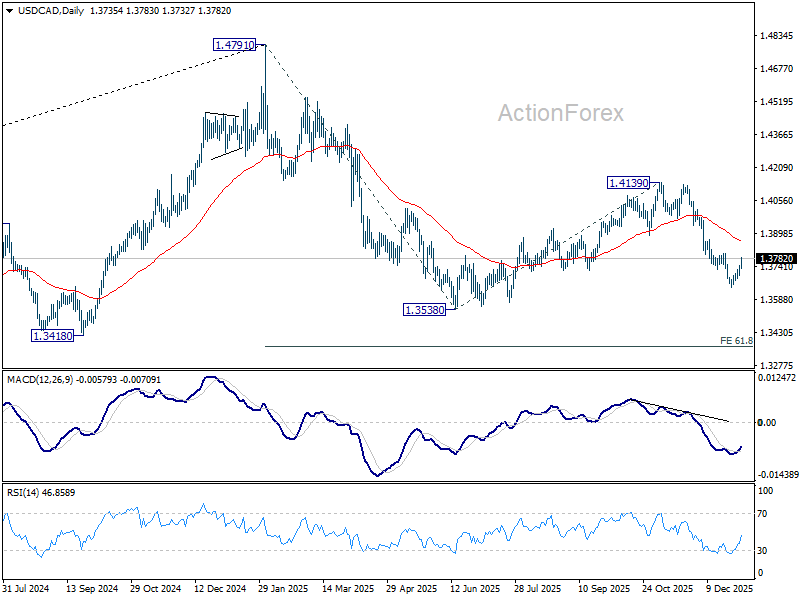

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3707; (P) 1.3727; (R1) 1.3754; More...

USD/CAD's rebound from 1.3641 extends higher today but still remains below 1.3804 resistance. Intraday bias stays neutral at this point. On the upside, firm break of 1.3804 will argue that fall from 1.4139 has completed. Stronger rebound should be seen back to 55 D EMA (now at 1.3864) and above. On the downside, below 1.3699 minor support will turn bias back to the downside. Break of 1.3641 will target 1.3538 low.

In the bigger picture, current development suggests that price actions from 1.4791 is developing into a deeper, larger scale correction. In the less bearish case, it's just correcting the rise from 1.2005 (2021 low). But even so, break of 1.3538 will pave the way to 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365. This will remain the favored case as long as 1.4139 resistance holds, in case of rebound.

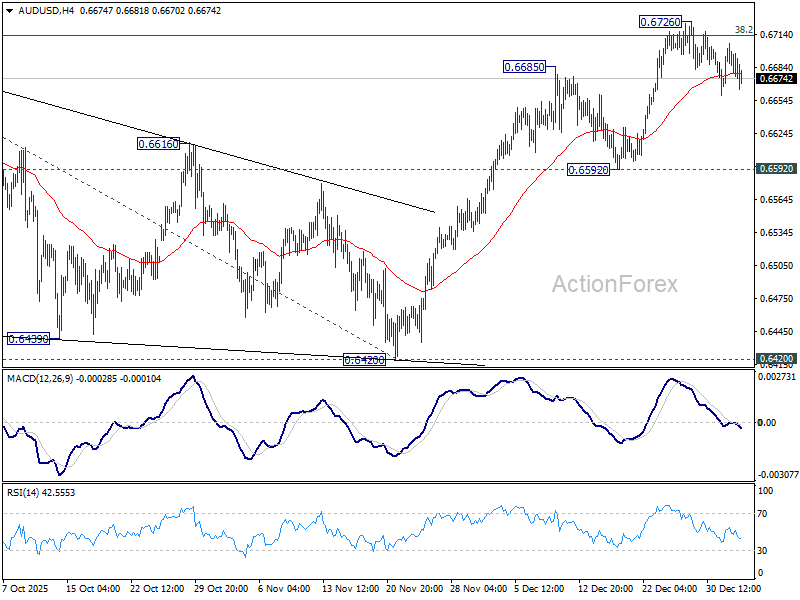

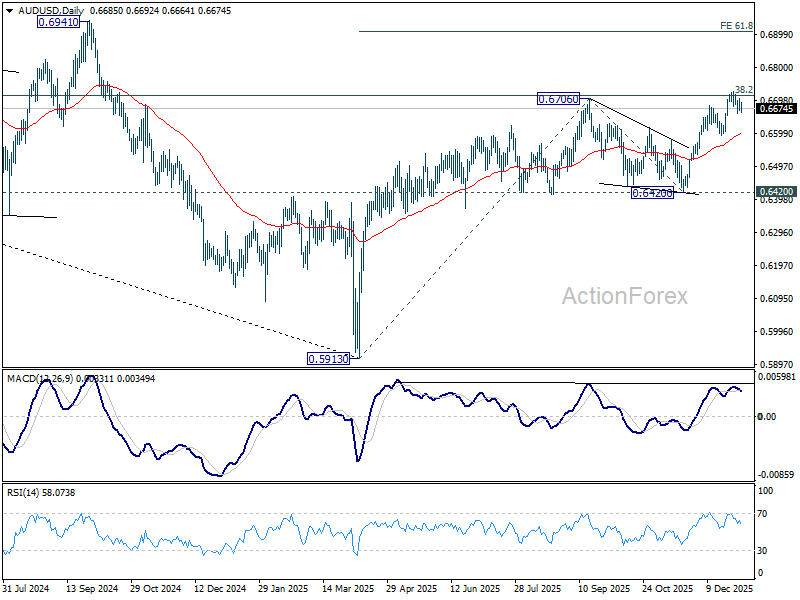

AUD/USD Daily Report

Daily Pivots: (S1) 0.6672; (P) 0.6690; (R1) 0.6712; More...

Intraday bias in AUD/USD stays neutral as consolidations continue below 0.6726. With 0.6592 support intact, further rally is expected. On the upside, sustained trading above 0.6713 fibonacci level will carry larger bullish implications. Next near term target will be 61.8% projection of 0.5913 to 0.6706 from 0.6420 at 0.6910.

In the bigger picture, the break of multi-year falling trend line resistance suggests that rise from 0.5913 is possibly reversing whole down trend from 0.8006 (2021 high). Decisive break of 38.2% retracement of 0.8006 to 0.5913 at 0.6713 will solidify this case, and bring further rally to 61.8% retracement at 0.7206. On the downside, however, firm break of 0.6420 support will suggest rejection by 0.6713 and retain medium term bearishness.

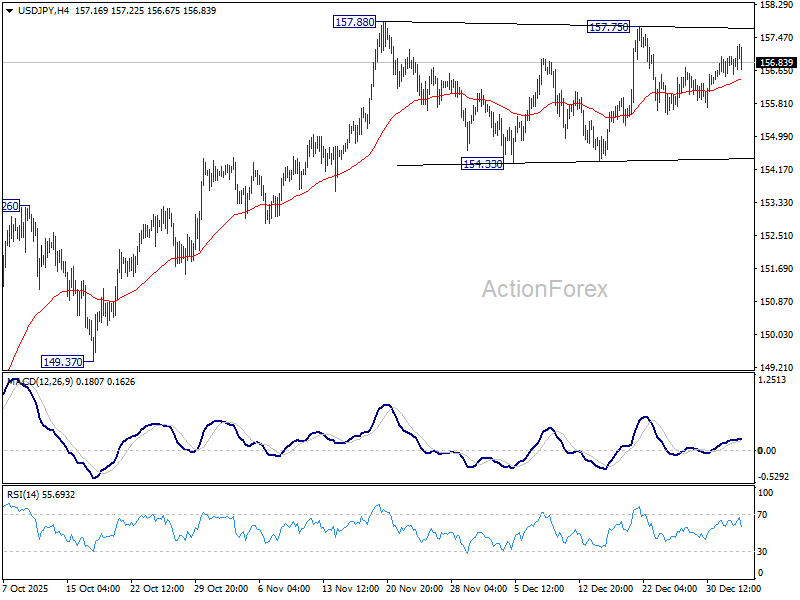

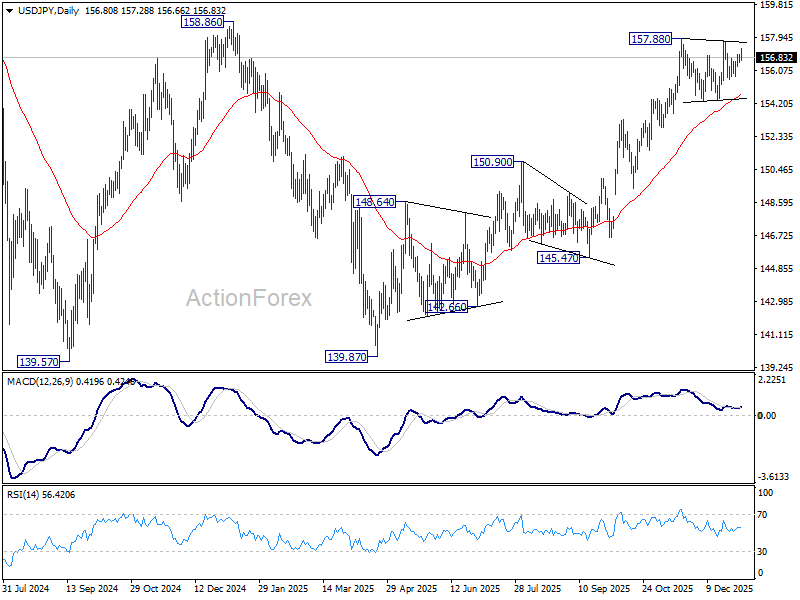

USD/JPY Daily Outlook

Daily Pivots: (S1) 156.57; (P) 156.79; (R1) 157.05; More...

Intraday bias in USD/JPY remains neutral as sideway consolidations from 157.88 continues. Another fall cannot be ruled out, but outlook will stay bullish as long as 154.33 support holds. On the upside, firm break of 158.85 key structural resistance will be an important medium term bullish sign. Next target will be 161.94 high. However, decisive break of 154.38 will turn bias to the downside for deeper correction.

In the bigger picture, corrective pattern from 161.94 (2024 high) could have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 150.90 resistance turned support will dampen this bullish view and extend the corrective range pattern with another falling leg.

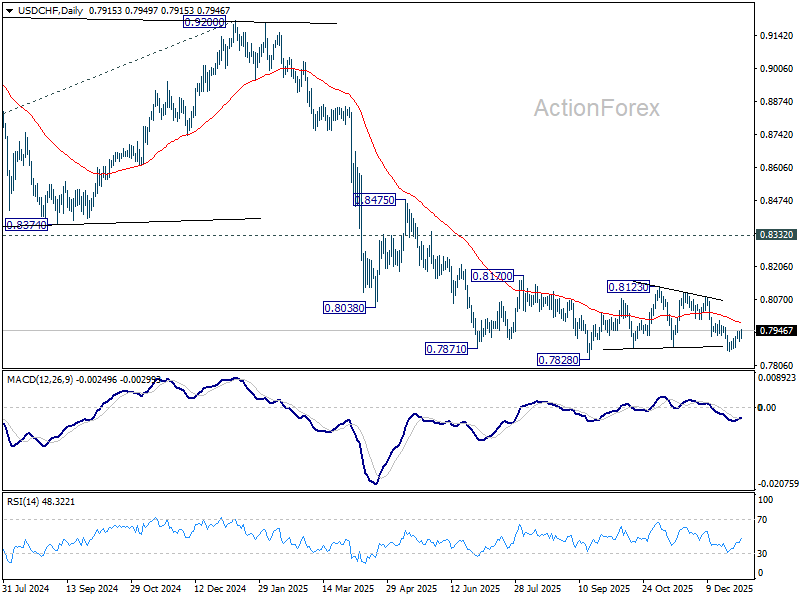

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7903; (P) 0.7922; (R1) 0.7943; More….

USD/CHF's rebound from 0.7860 extends today. But upside is capped well below 0.7986 resistance. Intraday bias remains neutral for the moment. On the downside, below 0.7900 minor support will turn bias to the downside. Break of 0.7860 will target a retest on 0.7828 low. However, break of 0.7986 will argue that corrective pattern from 0.7828 is still extending with another rising leg already in progress.

In the bigger picture, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low). Long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.