Sample Category Title

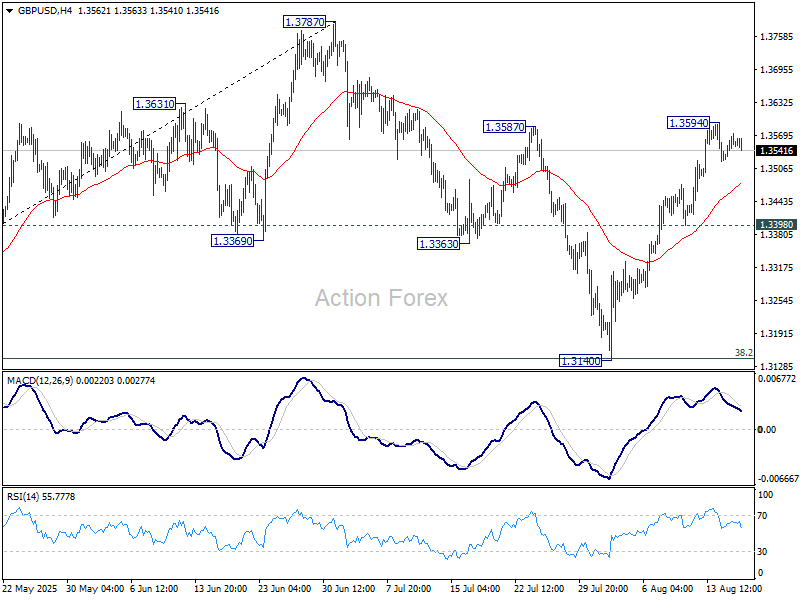

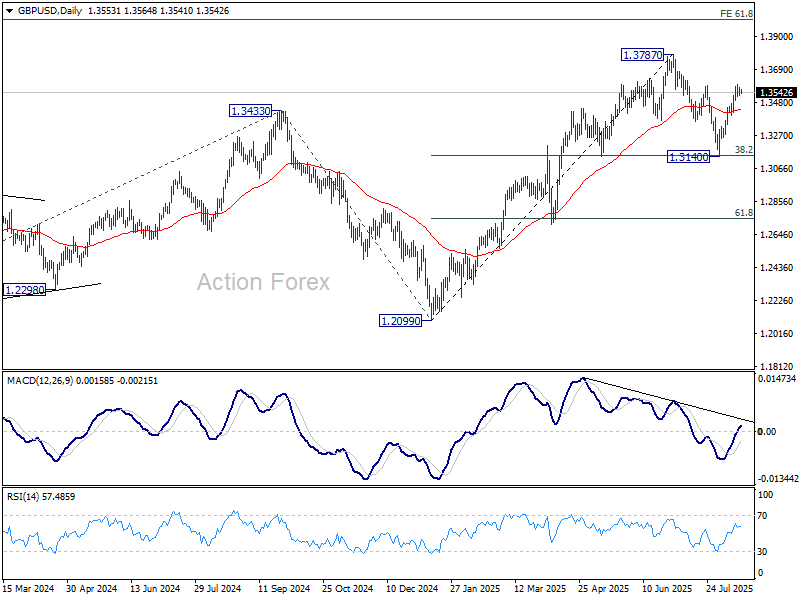

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3532; (P) 1.3553; (R1) 1.3581; More...

Intraday bias in GBP/USD remains neutral and more consolidations would be seen below 1.3594. Deeper pullback might be seen but downside should be contained well above 1.3398 support. On the upside, break of 1.3594 will resume the rise from 1.3140 to retest 1.3787 high.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3090) holds, even in case of deep pullback.

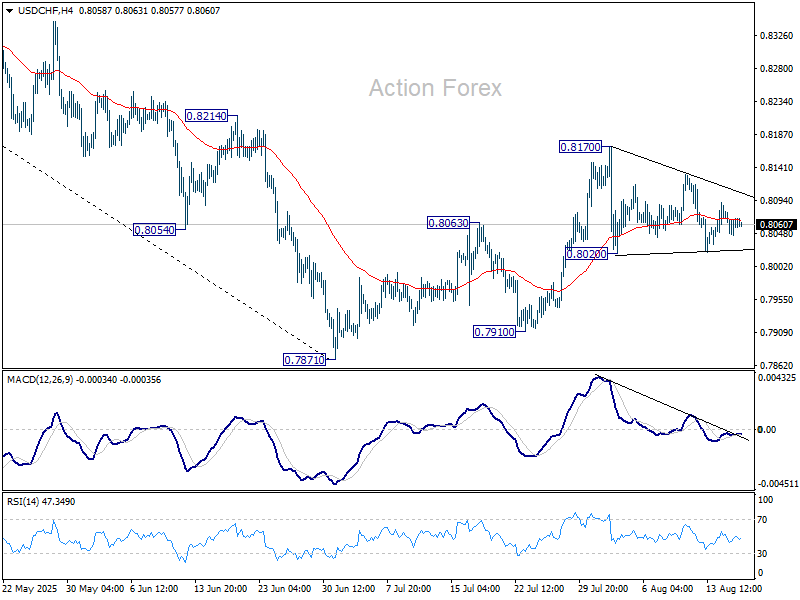

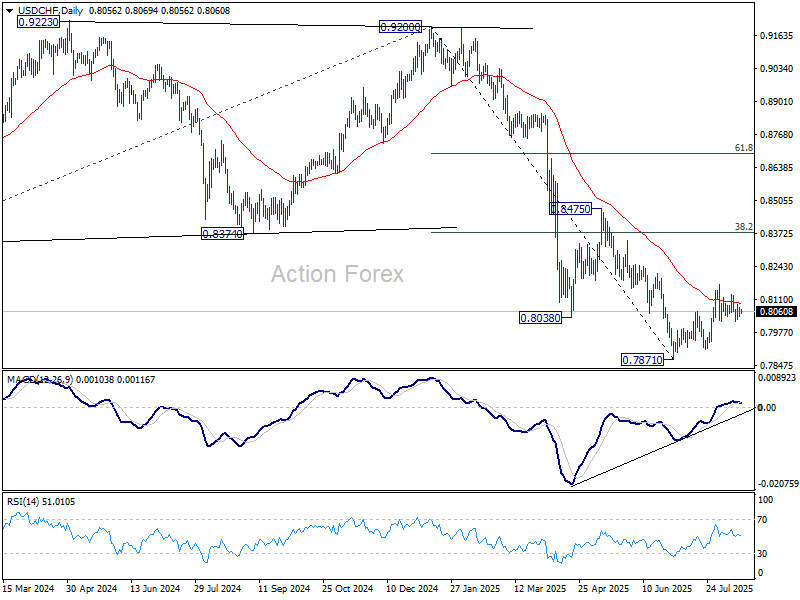

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7997; (P) 0.8040; (R1) 0.8110; More….

USD/CHF is still bounded in range trading and intraday bias stays neutral. On the downside, break of 0.8020 will revive that case that the corrective pattern from 0.7871 has completed, and target a retest on 0.7871 low. On the upside, firm break of 0.8710 will resume the corrective from 0.7871. Intraday bias will be back on the upside for 38.2% retracement of 0.9200 to 0.7871 at 0.8379.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

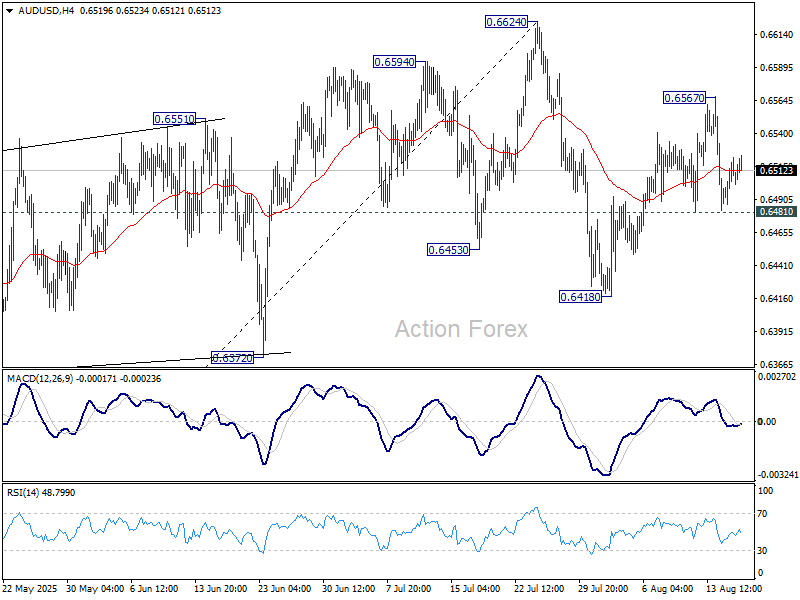

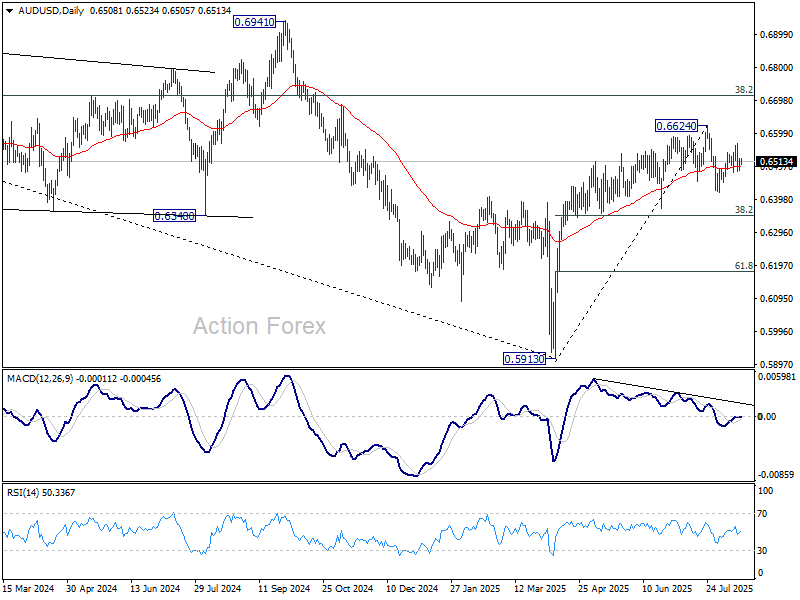

AUD/USD Daily Report

Daily Pivots: (S1) 0.6488; (P) 0.6506; (R1) 0.6525; More...

Intraday bias in AUD/USD remains neutral at this point. Overall, corrective pattern from 0.6624 should still be extending. Above 0.6567 will target 0.6624. On the downside, firm break of 0.6481 will resume the correction through 0.6418 to 38.2% retracement of 0.5913 to 0.6624 at 0.6352.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, even in case of another fall through 0.5913, downside should be contained above 0.5506 (2020 low).

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3797; (P) 1.3810; (R1) 1.3832; More...

Intraday bias in USD/CAD stays neutral for the moment. On the downside, break of 1.3720 will reaffirm the case that corrective pattern from 1.3538 has completed at 1.3878. Further decline should then be seen back to retest 1.3538 low. However, break of 1.3878 will extend the corrective rebound from 1.3538 with another rising leg.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

Hope Over Fears

Friday’s meeting between Trump and Putin seems to have gone smoothly. Details are scarce, but so far there are no signs of fresh tensions with Russia and no new sanctions on countries such as China and India that continue buying Russian oil. US crude opened the week with a gap lower but has since recovered part of its losses. Direction remains uncertain, though the absence of immediate stress is notable.

Later today Trump is due to meet Zelensky and European leaders to relay Moscow’s conditions for ending the war in Ukraine. Russia continues to demand territorial concessions, while Ukraine rejects this and instead seeks binding security guarantees from its allies. Hopes of progress are keeping oil bears encouraged — with risks that prices test below $60pb — but disappointment remains a clear possibility. The next hours will likely set the tone for crude.

From a macro perspective, ample OPEC supply and cloudy global demand — weakened by trade disruptions and subdued Chinese consumption — keep oil prices in a bearish medium-term trend. The IEA last week projected the largest ever global oil surplus, nearly 3 million barrels/day of inventory build, a pace even higher than during the pandemic. Bulls counter that US output may soon peak near record highs and soften, while a weaker dollar supports demand from emerging markets. Still, the bearish camp holds the upper hand in 2025, with geopolitics only triggering temporary price spikes.

Asian markets started the week higher: Chinese equities gained 1.5% and India’s Nifty 50 rose 1.4%, snapping a downtrend that began in late June amid tense US–India trade talks. Both nations would welcome any truce between Russia and the West, given their desire to maintain ties with both camps. European and US futures are also firmer. The yen is softer, while gold demand remains strong — showing investors are cautious ahead of Trump’s meeting with Zelensky. Material progress could spark further oil weakness, a rally across equities, and softer gold demand. Disappointment would bring oil bulls back, pressure equities (except defense), and lift gold toward its 50-DMA and record highs.

In Europe, equities extended gains last week to their highest levels since March, before tariff announcements. This suggests tariff risk is largely priced out. Earnings showed resilience: carmakers took the biggest hit (VW’s operating profit fell nearly 30% in Q2 due to tariffs), but most other sectors saw limited impact. The stronger euro helped reduce costs and temper inflation, giving the European Central Bank (ECB) room to stay supportive. Overall, STOXX 600 companies posted ~3% earnings growth versus expectations for a ~3% decline, and forecasts have since been revised higher. A Russia–Ukraine truce would add to the bullish case for European assets as investors look for diversification away from US markets.

In the US, indices hover near record highs as markets expect the Federal Reserve (Fed) to cut rates at its September meeting — potentially even by 50bp under political pressure from the White House. Attention now turns to Jerome Powell’s appearance at the Jackson Hole symposium this week. While the official theme is labour markets, investors will scrutinize any hint of September policy direction, especially after last week’s mixed inflation data: CPI showed limited price pressures, but PPI surprised higher. Treasury yields fell sharply after CPI, then rebounded on PPI, though remain below post-jobs data levels. The soft inflation backdrop supports equity valuations. Any progress on Ukraine peace talks could push global equities higher still. If not, any dip is likely to be quickly bought.

Trump-Putin Talks Falter Ahead of Zelenskiy’s Visit to the White House

In focus this week

Today, following the Trump-Putin meeting in Alaska, Ukrainian President Zelenskiy is set to meet US President Trump in the White House alongside a group of European leaders including EU commission president von der Leyen.

In the euro area, we look for final July inflation data on Wednesday, the PMI report for August on Thursday and the negotiated wages indicator released by the ECB on Friday. We will closely monitor the negotiated wages indicator, as declining domestic inflation is the biggest downside risk to our call of ECB holding rates steady for the rest of the year.

Across the Atlantic, the Fed is set to take headlines throughout the week, as the minutes of the FOMC's July meeting are released Wednesday evening. Then on Thursday and Friday the Fed's Jackson Hole Symposium will take place. This year's theme is "Labor Markets in Transition: Demographics, Productivity, and Macroeconomic Policy". The main focus of markets will be on Fed Chair Powell's speech on Friday afternoon. On the macro data front, August flash PMIs are due for release Thursday.

Economic and market news

What happened over the weekend

In the US, July retail sales came in strong at +0.5% (cons: +0.5%), while the June numbers were revised up from +0.6% to +0.9%. Control group sales, the 'core' group, came in at +0.5% m/m with solid sales reported among most sectors. While employment growth has slowed over the past months, solid wage growth continues to fuel consumption in the US. Meanwhile, US July industrial production grew -0.1% (cons: 0.0%) in July, while the June growth was revised up to +0.4% from +0.3%.

University of Michigan consumer 1-year inflation expectations rose to 4.9% (preliminary) in August from 4.5% in July. Inflation expectations declined from May to July, but the new tariffs appear to have caused renewed concerns in early August. Worries about inflation also fed into a weaker consumer sentiment which declined to 58.6 from 61.7 in July.

In Alaska, US President Trump and Russian President Putin met to discuss the war in Ukraine. The talks ended earlier than expected and were unsuccessful in making any imminent progress towards a ceasefire. Steven Witkoff, Trump's special envoy to the Middle East, said that Putin agreed that the US could provide security guarantees to Ukraine as part of a deal, which would, though, also likely require territorial concessions. Following the meetings, Trump decided to hold back on further sanctions against Russia as well as 'secondary tariffs' on countries buying Russian energy such as India and China.

Equities: Equities ended last week on a soft note, but the broader picture remains another week of gains. Under the surface, cyclicals underperformed defensives, but the real story was sector rotation - particularly a strong comeback in healthcare. We have highlighted the sector several times recently, and last week investors finally rotated back in: healthcare gained nearly 4% in Europe and more than 5% in the US, outperforming staples by 4% in relative terms. This was not a broad defensive theme, but a clear rotation story, partly reflecting easing tariff fears and the sector's prior underperformance. In the US on Friday, Dow +0.1%, S&P 500 -0.3%, Nasdaq -0.4% and Russell 2000 -0.6%. Asian equities are higher this morning, and futures in both Europe and the US are marginally in the green.

FI and FX: Risk sentiment soured through Friday's session as markets awaited the outcome of the Putin-Trump Alaska summit. Rates moved higher across regions with the solid US retail sales data and rising consumer inflation expectations adding to the move. Long-end bonds suffered the most with 30Y yields in Germany and France reaching their highest levels since 2011. EUR/USD drifted higher towards 1.17 on Friday as the USD broadly weakened, ending the week down around 0.4%. EUR/SEK and EUR/NOK rose as market sentiment worsened. Overnight, Asian stocks are trading modestly higher as focus turns towards the Trump-Zelensky meeting.

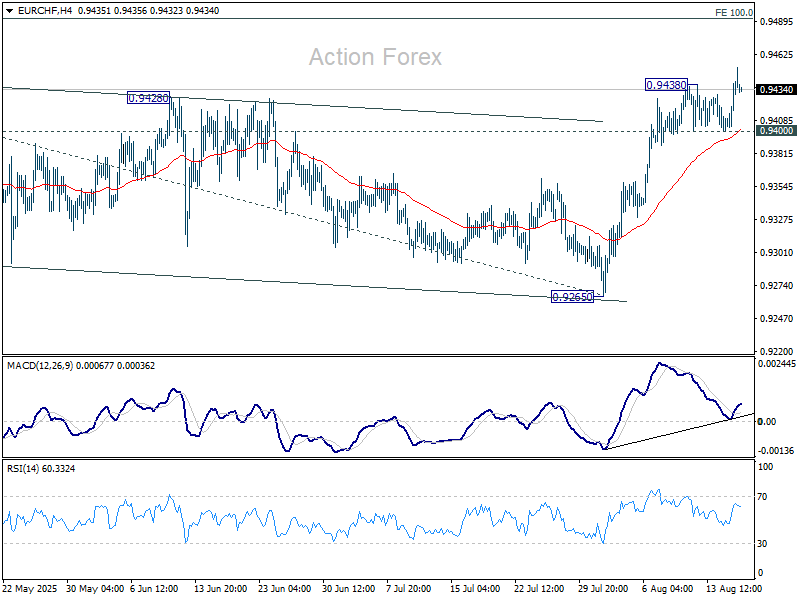

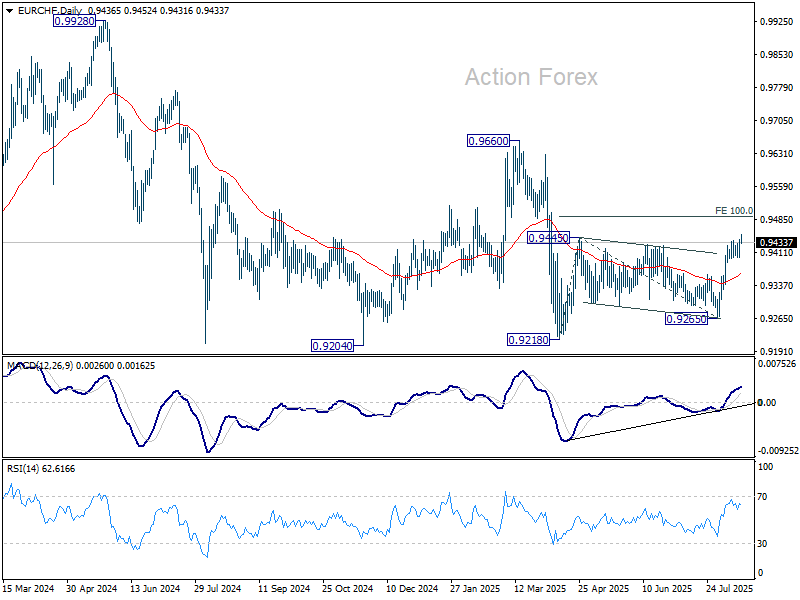

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9417; (P) 0.9431; (R1) 0.9457; More....

EUR/CHF's rally resumed by breaking 0.9438 temporary top and intraday bias is back on the upside. Rise from 0.9218 should target 100% projection of 0.9218 to 0.9445 from 0.9265 at 0.9492. For now, further rise is expected as long as 0.9400 support holds, in case of retreat.

In the bigger picture, the down trend from 0.9204 (2018 high) might still be in progress considering that EUR/CHF is staying well inside the long term falling channel. However, with bullish convergence condition in W MACD, downside potential should be limited in case of another fall. Instead, firm break of 0.9660 resistance will be an important sign of medium term bullish trend reversal.

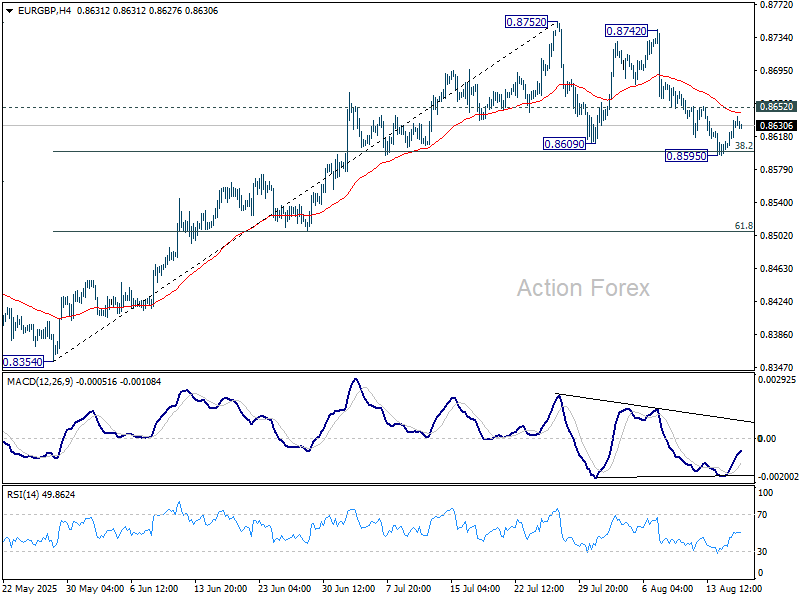

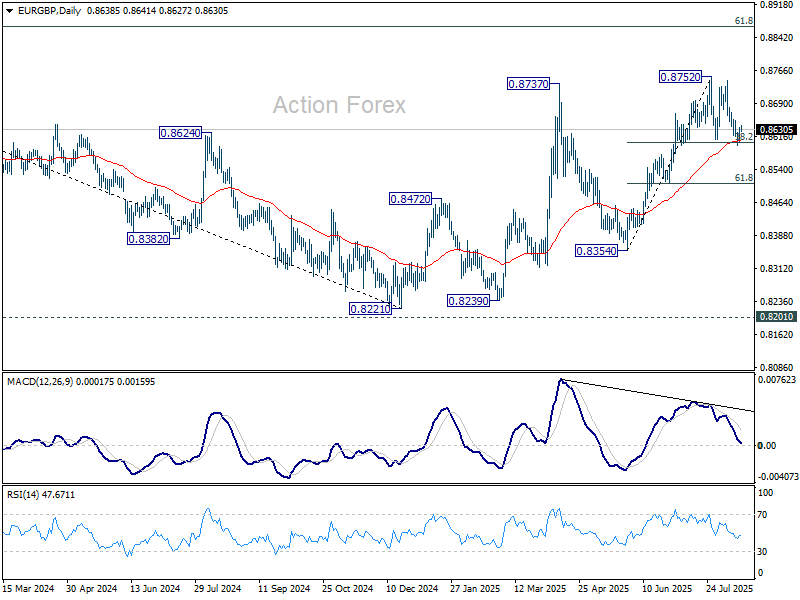

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8614; (P) 0.8626; (R1) 0.8648; More...

Intraday bias in EUR/GBP remains neutral for the moment. On the upside, break of 0.8652 will suggest that the corrective pattern from 0.8752 has completed after drawing support from 38.2% retracement of 0.8354 to 0.8752 at 0.8600, and retain near term bullishness. Intraday bias will be back on the upside for retesting 0.8752 high next. However, sustained break of 0.8600 will indicate near term bearish reversal and target 61.8% retracement at 0.8506.

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it's reversing the down trend from 0.9267 (2022 high). But even if it's a correction, further rise is expected to 61.8% retracement of 0.9267 to 0.8221 at 0.8867. This will remain the favored case as long as 55 W EMA (now at 0.8501) holds.

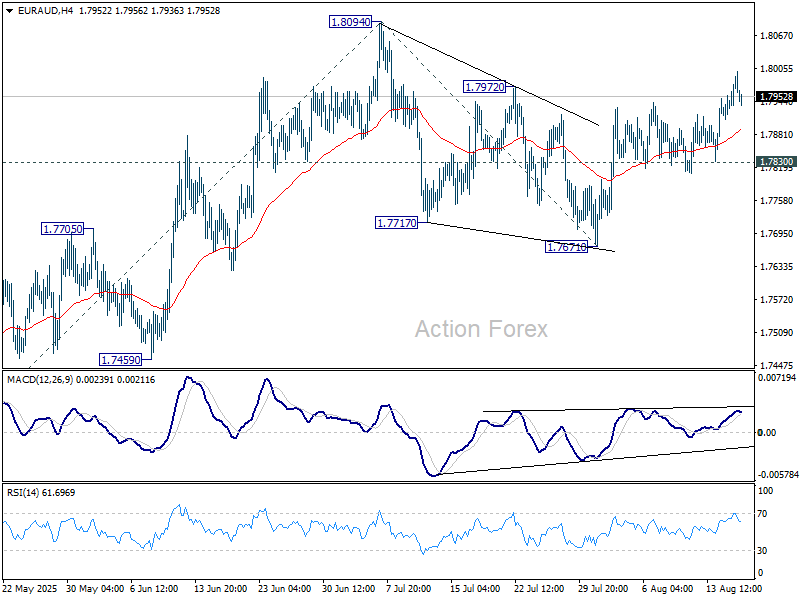

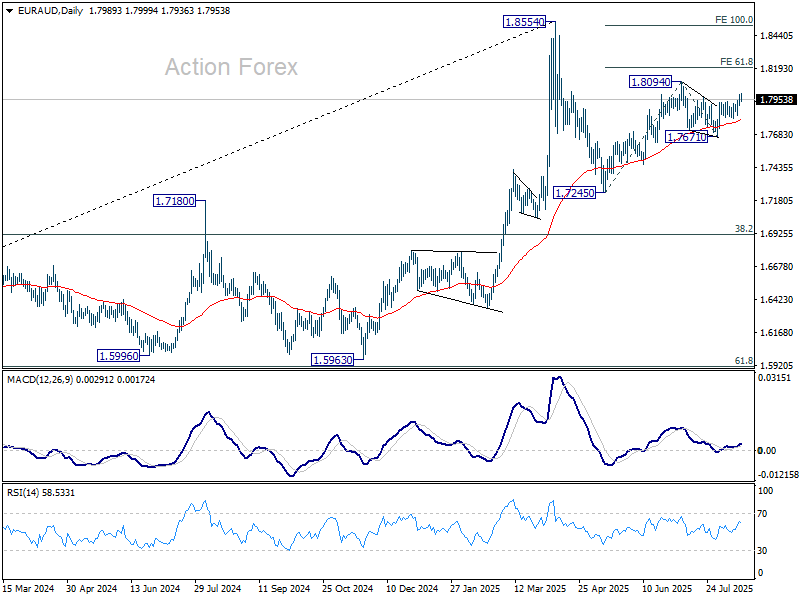

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7934; (P) 1.7963; (R1) 1.8017; More...

Intraday bias in EUR/AUD stays mildly on the upside for the moment. Correction from 1.8094 should have completed with three waves down to 1.7671. Further rally should be seen to 1.8094 first. Break there will resume the rally from 1.7245 to 61.8% projection of 1.7245 to 1.8094 from 1.7671 at 1.8196. This will now remain the favored case as long as 1.7830 support holds.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Such pattern could extend further with another falling leg. But even in that case, downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Uptrend from 1.4281 is expected to resume at a later stage.

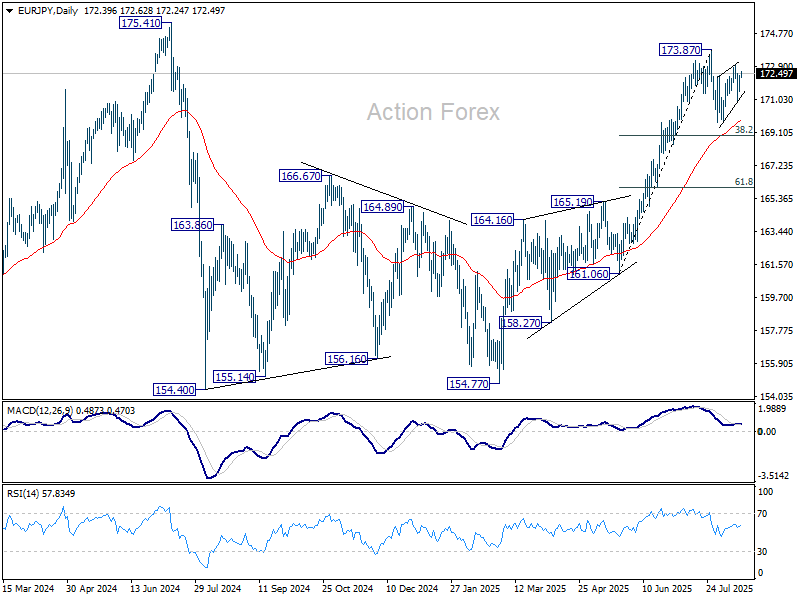

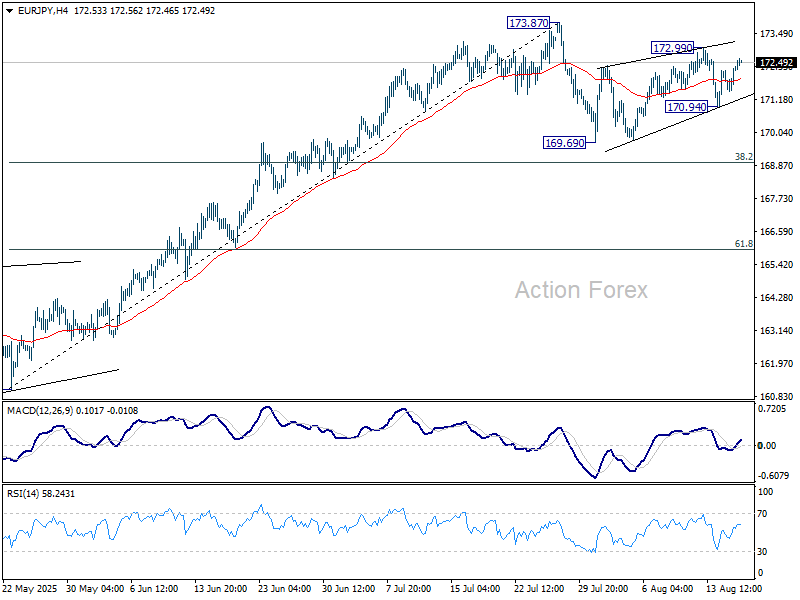

EUR/JPY Daily Outlook

Daily Pivots: (S1) 171.72; (P) 172.05; (R1) 172.59; More...

Intraday bias in EUR/JPY remains neutral for the moment. Corrective pattern from 173.87 is still extending, and break of 170.94 will bring deeper fall to 169.69 support. But downside should be contained by 38.2% retracement of 161.06 to 173.87 at 168.97 to bring rebound. On the upside, above 172.99 will bring retest of 173.87.

In the bigger picture, considering current strong momentum as seen in the rally from 154.77, corrective pattern from 175.41 could have already completed. Decisive break of 154.77 will confirm long term up trend resumption. Next target is 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. However, rejection by 175.41, followed by firm break of 55 D EMA (now at 169.87) will delay this bullish case.