Week in Review: Markets Buoyed Ahead of FOMC Meeting

The week draws to a close with risk assets largely buoyed by the prospect of an interest rate cut from the Federal Reserve.

On Friday, the main US stock market indexes all moved slightly higher. The Dow Jones gained 236.46 points (a 0.49% rise), the S&P 500 increased by 31.44 points (a 0.46% gain), and the Nasdaq rose by 131.27 points (a 0.56% increase).

Looking ahead to next week, Federal Reserve officials are scheduled to have a significant debate: should they lower interest rates, or keep them steady? The core issue is that while prices remain difficult to control (stubborn inflation) and the job market is still surprisingly strong (resilient), some Fed members are hesitant to cut rates.

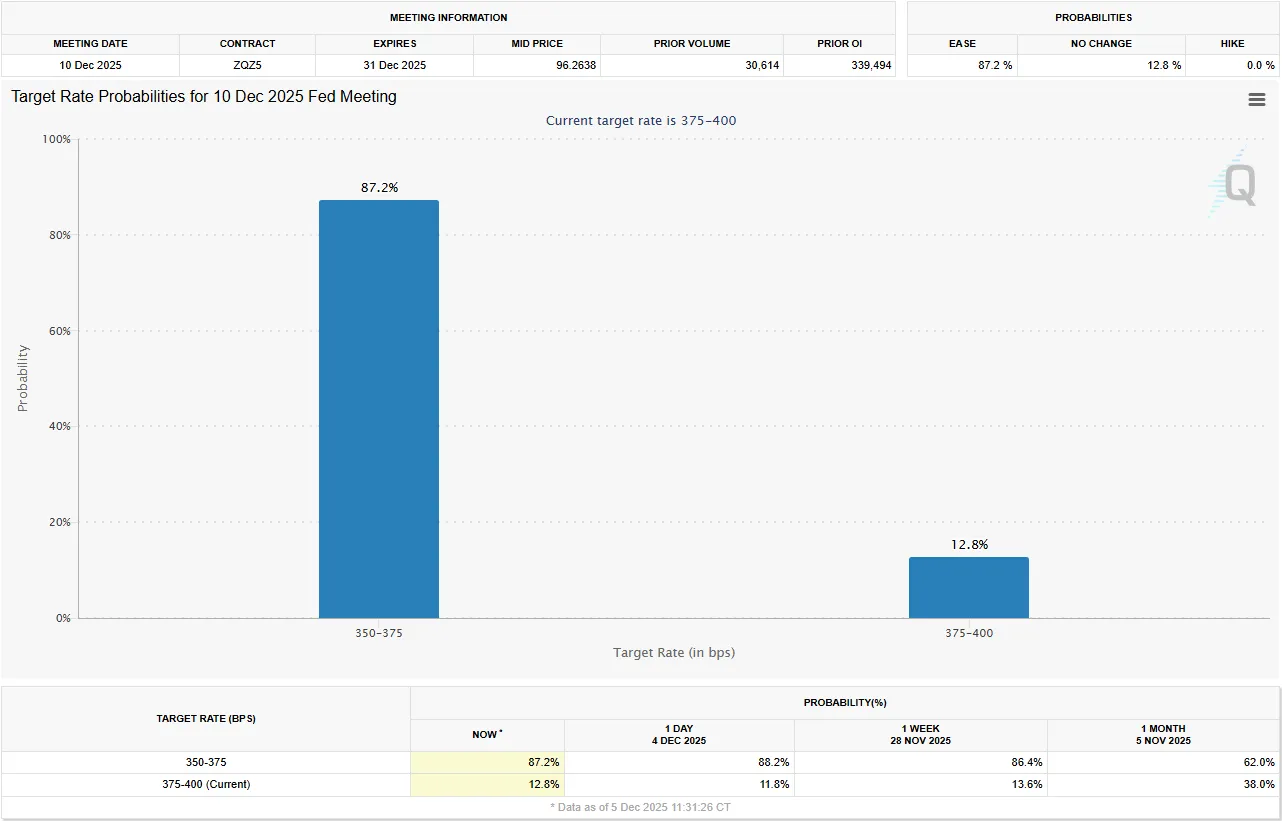

Other employment-related data still does not suggest a quick slowdown in hiring, which gives those who prioritize fighting inflation (the “hawks”) a stronger argument. Despite this internal debate, investors in the market still anticipate that the Fed will go ahead and cut rates by another quarter-point sometime by June 2026.

Source: CME FedWatch Tool

Heading into the decision, Wall Street indexes are all near all-time highs with the hope that the Federal Reserve meeting will serve as a catalyst for fresh all-time highs to be printed. Will such a move materialize?

How Did the US Dollar and FX Perform?

The US dollar was slightly weaker on Friday but generally stayed within its recent trading range against other major currencies.

The dollar’s strength index (DXY) dipped 0.2%, landing at 98.906, which is close to its weakest point in the past five weeks.

Meanwhile, the euro gained slightly, reaching 1.1651 against the dollar.

The Japanese yen remained mostly unchanged on Friday at 155.15 per dollar, taking a pause after recent days of strength driven by speculation that the Bank of Japan (BOJ) might raise its interest rates later this month. Reports from both Bloomberg and Reuters suggested that BOJ officials are indeed prepared to raise rates on December 19th unless there is a significant unexpected economic event.

The Canadian dollar strengthened by the most in six months against its US counterpart on Friday and bond yields jumped, as stronger-than-expected domestic jobs data boosted bets the Bank of Canada would begin raising interest rates next year.

Finally, the British pound (Sterling) also rose 0.2%, trading at 1.335 and nearing its highest level in six weeks.

The Week Ahead – Fed in Focus, RBA & BoC Rate Decisions Ahead

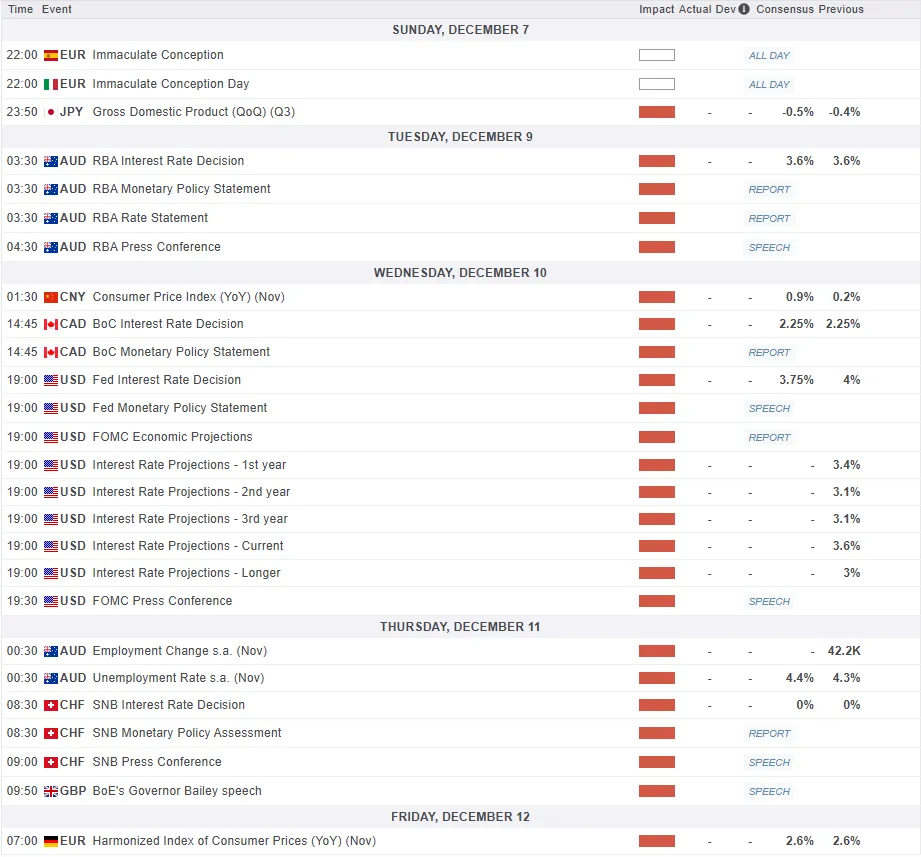

The week ahead will see market focus on the Federal Reserve rate decision. There is also rate decisions from Canada and Australia but given the stature of the US economy and its ability to affect overall market sentiment, the RBA and BoC decisions will likely be overshadowed.

Asia Pacific Markets

The Reserve Bank of Australia (RBA) is expected to keep its main interest rate unchanged at 3.6% next Tuesday. Since recent reports showed that both inflation and economic growth were stronger than expected, it’s now much less likely that the RBA will cut interest rates again. This suggests that the central bank might be finished with its current cycle of lowering rates.

China’s trade activity is expected to grow only moderately. Although the recent trade agreement and reduced tariffs from the U.S. should help Chinese exports, the way the numbers are calculated (base effects) will keep the growth rate low. For November, I forecast exports to grow by 3.3% and imports by 3.4%, resulting in a trade surplus of about $100.3 billion.

Separately, China’s inflation rate is predicted to continue its recovery, rising to 0.5% for the year, which is a positive sign after it recently moved back above zero. This is largely because the falling price of food is no longer dragging down the overall inflation number, and the prices of non-food items are starting to rise. While inflation remains quite low, it is important to prevent a sustained period of falling prices (deflation) to keep long-term spending and investment healthy. Since inflation is still low, it will likely not be a major factor in the People’s Bank of China’s interest rate decisions.

FOMC to Steal the Show

The Federal Reserve (US) is expected to cut its interest rate by $0.25\%$ this Wednesday. While some worry that new tariffs could keep prices high (inflation), the main reason for the cut is the growing concern about the weakness in the job market, which important Fed members have recently noted. Along with the decision, the Fed will release new predictions, which are likely to suggest only one more rate cut in 2026.

However, this long-term outlook might not significantly affect the market’s expectations which currently price in two or three cuts for 2026 because the composition of the Fed’s voting committee and leadership (including the Chair, Jerome Powell) could change drastically under the new administration.

Separately, Canada is likely to take a break from its recent series of interest rate cuts this Wednesday. Stronger-than-expected recent growth and employment figures support this pause, though we still anticipate one final cut early in 2026 due to ongoing trade risks with the US.

Finally, for the UK, I expect to see an improvement in the monthly Gross Domestic Product (GDP) data on Friday. The previous drop in September was mainly because a cyberattack stopped production at a major car company, but since that production has restarted, October’s GDP numbers should bounce back.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. GMT time (click to enlarge)

Chart of the Week – US Dollar Index

This week’s Chart of the week is the US Dollar Index (DXY)

From a technical perspective, the DXY has had a change in structure having taken out the November 14 swing low around the 99.00 handle.

Thursdays daily candle closed as a hammer offering bulls some hope. However, as has been the case of late any attempt at a bullish move has been met by swift selling pressure.

The period-14 RSI remains below the 50 mark which is a sign of bearish momentum.

Immediate support is provided by the 100-day MA which rests at the 98.58 before the 98.00 and 97.70 handles come into focus.

Upside resistance may be found at the 200-day MA around 99.51 before the 100.00 psychological level and the 100.61 level come into focus.

The Dollar Index trajectory may depend on the economic projections for 2026. Any sign that the Fed see more than one rate cut in 2026 could send the DXY sliding with a test of the YTD low a possibility depending on how dovish the Fed outlook is.

Alternatively, a hawkish stance could have the opposite impact. This would be similar to what we witnessed after the previous Fed meeting in October.

US Dollar Index (DXY) Daily Chart – October 17, 2025

Source:TradingView.Com (click to enlarge)

Be Nimble and Trade Safe.

, the S&P 500 increased by 31.44 points (a 0.46% gain), and the Nasdaq rose by 131.27 points (a 0.56% increase).){kind=link}