- Oil and gas prices shoot up, upending rate cut bets as inflation fears return.

- Stocks tumble amid surging bond yields and stagflation risks.

- Markets increasingly price in a prolonged Iran conflict.

- Did Trump just shoot himself and the US economy in the foot?

Back to the 1970s

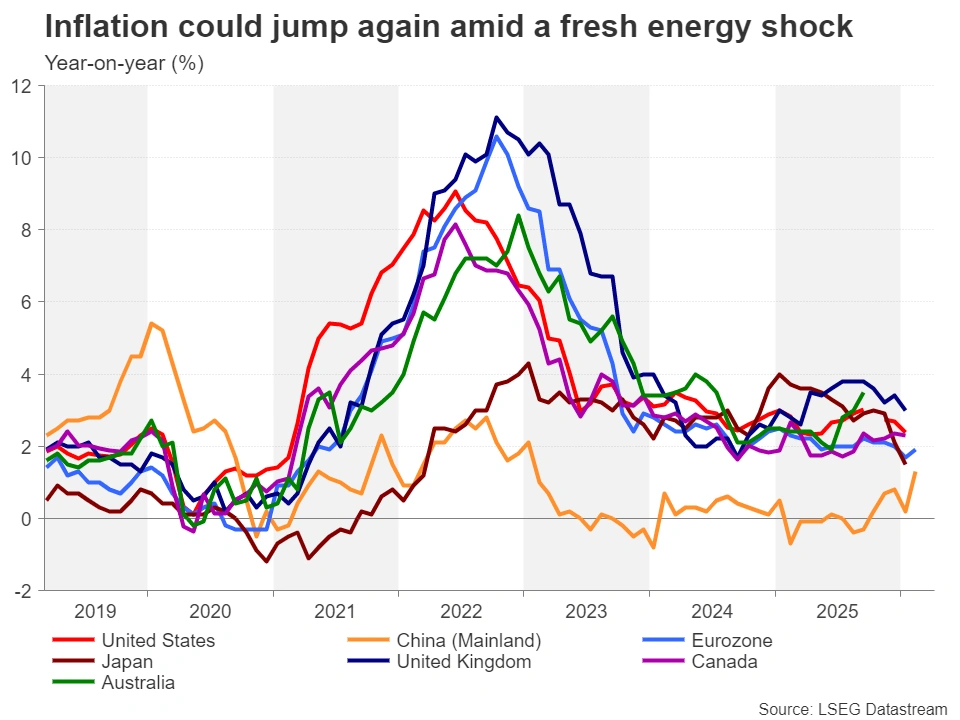

It’s only been a few years since Russia’s invasion of Ukraine triggered the worst energy crisis since the 1970s, and it’s looking increasingly likely that the world is facing yet another shock – the second one in less than a decade. All this is very reminiscent of the 1970s where inflation was rampant and economic growth was sluggish – a combination more commonly known as stagflation.

President Trump’s decision for the United States to launch joint miliary strikes with Israel on Iran may be going according to plan and “ahead of schedule”, but it’s had unintended consequences on global energy markets. America’s inability to completely stop Iranian drone and missile attacks on vessels passing through the Strait of Hormuz and guarantee their safety is not only halting shipments of oil and gas from the Middle East but is also having a crippling effect on production.

Key Oil chokepoint blocked

About 20% of global oil and gas supply is estimated to rely on the Strait of Hormuz for transit and with Arab producers such as Saudi Arabia, United Arab Emirates and Qatar unable to export, they have already reached their maximum storage capacities. What this means is that unless the Strait of Hormuz is opened for business again, which is extremely unlikely at this stage, production may soon come to a standstill.

Qatar has already ceased production of liquified natural gas (LNG) at Ras Laffan, which is the world’s largest LNG facility, while Saudi Arabia has started to reduce oil output. Oil and gas futures have subsequently soared, threatening a jump in energy costs for businesses that are still reeling from the price shock from the Ukraine war, and more recently, Trump’s tariff war.

From rate cuts to rate hikes

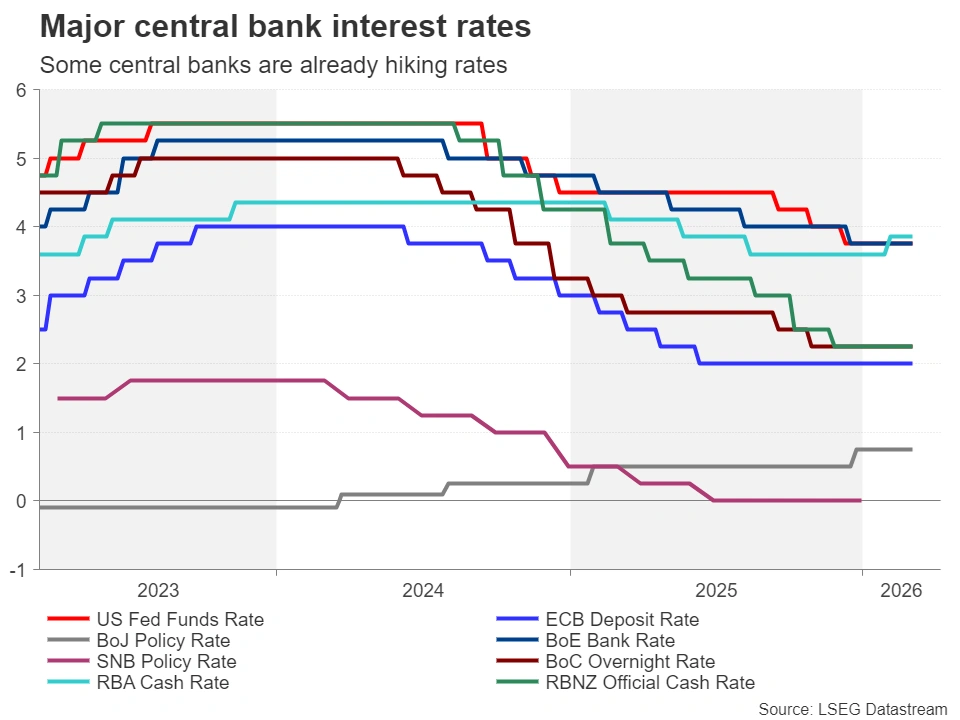

This is the last thing that central banks were hoping to revisit, as interest rates around the world have yet to return to their pre-pandemic levels. Although some central banks such as the Bank of Japan and Reserve Bank of Australia were on a tightening path well before the flare-up in Iran, others like the Federal Reserve and Bank of England looked set to cut rates by at least twice this year.

Even the European Central Bank, which has been on pause since last June, was moving towards a dovish bias before the outbreak of war amid declining price pressures in the euro area.

But hopes of additional rate cuts have now gone up in smoke, as policymakers are unlikely to signal fresh reductions in borrowing costs until oil and gas prices have peaked and they have some clarity on where inflation is headed. The most pressing issue for investors is that the White House doesn’t seem to have a clear end plan on Iran, casting doubts on Trump’s claim that the war will end “very soon”.

Iran’s neighbours can’t escape the missile barrage

Moreover, Iran has been carrying out counter strikes not just on US bases and interests in the region, but also against its neighbours, hitting their oil refineries and civilian targets such as Dubai airport. Hence, there is a high risk of further escalation, as Arab powers could decide to engage in direct military confrontation with Iran if Tehran continues to bomb them.

In the meantime, there is a growing risk of global fuel shortages from the ongoing blockage of the Strait of Hormuz. The problem is that even if there was a significant de-escalation in the war so that oil and LNG tankers started sailing again through the key shipping lane, it could take several weeks for shuttered production facilities to return to normal output. There’s also a danger that Iran and its proxies will not cease striking ships along Hormuz or other targets at every opportunity even with diminished capabilities after the US and Israel have stopped their attacks.

Fears of Energy crisis sparks market turmoil

Coordinated efforts for rich nations, such as the G7 countries, to release some of their strategic oil reserves may well end up being too little too late. It’s no surprise therefore that after a somewhat contained response to the onset of war in the Middle East, markets are now in full panic mode.

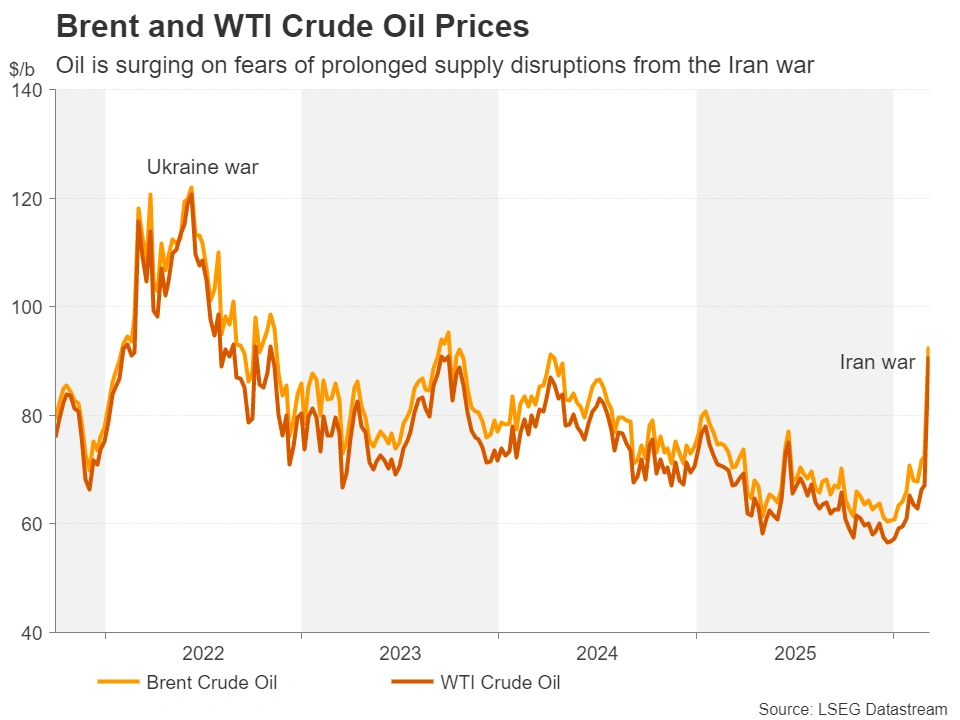

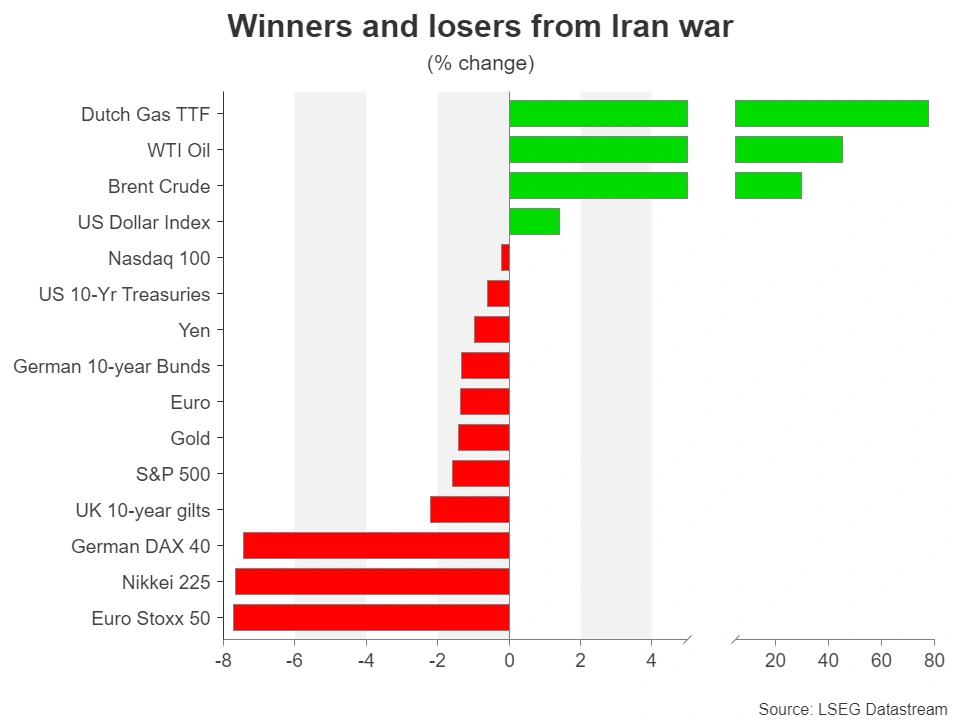

Both WTI and Brent crude futures spiked to almost $120 a barrel, while Dutch TTF futures – the benchmark for European gas prices – are up about 75% year-to-date.

Bond markets are starting to panic too, with government bond yields surging, signalling heightened fears of inflation. Global equities have slid to multi-month lows amid the renewed prospect of high inflation, high interest rates and talk of recession. Some of the hardest hit are Germany’s DAX and Japan’s Nikkei 225 indices. In both cases, the overreliance on gas and oil imports by Germany and Japan respectively, threatens to cause some serious pain for their exporters.

In addition, with debt jitters not fully subsided, some governments like in the UK are already considering the possibility of fresh financial support to households to help ease the burden of steeper energy prices.

Central banks once again face stagflation dilemma

What’s more crucial, however, is that even if a lot of these risks don’t materialize, the least that can be expected is that confidence in the major economies around the world will suffer a substantial knock, as this crisis comes hot on the heels of the unwelcome comeback of US tariff-related uncertainty.

Lower economic growth tends to strengthen the argument for rate cuts, but once again central banks find themselves in a dilemma of whether to boost growth or bring inflation under control.

Investors think inflation will take priority and have priced out rate cuts for the likes of the Fed and Bank of England, and priced in rate increases for the ECB, Bank of Canada and Reserve Bank of New Zealand. Oddly, rate hike expectations for the Bank of Japan have increased only modestly, possibly because of how an energy shock could impact the broader economy.

Will Trump keep the war short?

On the whole, it’s probably too early to predict how this latest crisis will unravel, as the US and Israel could end their military campaign within days, restoring safe passage through the Strait of Hormuz. Or, in the worst-case scenario, the war could stretch for several more weeks, dragging other countries into the conflict, with many predicting that we are on the cusp of World War III.

Most likely, however, Trump will not want to get too embroiled in the Middle East as a prolonged conflict risks pushing up energy prices permanently, which is not desirable ahead of the US midterm elections in November. The danger here is that a US pullout may not necessarily bring a resolution to the war.

{kind=link}