- Fed rate cut bets return after ceasefire in Iran war.

- US PPI figures to test whether the Fed could resume rate reductions.

- ECB meeting minutes and UK data to test ECB and BoE expectations.

- Aussie traders await AU employment report and China’s GDP.

Dollar pulls back amid ceasefire in the Middle East

The US dollar started the week on the back foot on hopes that the US and Iran could work things out and end their conflict, and accelerated its tumble on Wednesday after headlines hit the wires that the two nations agreed to a two-week ceasefire, including the reopening of the Strait of Hormuz, through which one-fifth of global oil shipment passes. The White House confirmed that Israel was also on board for the ceasefire.

WTI crude oil dropped as much as 16% on the news and stocks skyrocketed as the news come just a day after US President Trump threatened massive attacks on civilian infrastructure, specifically warning that “a whole civilization will die tonight” if his demands were not met.

The ceasefire and the tumble of oil prices eased inflation fears, prompting investors to start speculating that the Fed may need to resume cutting interest rates following the truce. According to Fed fund futures, there is a nearly 30% chance of a quarter-point cut by the end of the year.

And that’s even after the minutes from the latest FOMC decision showed that a growing group of Fed officials believed that rate hikes may be needed to prevent inflation from spiraling out of control. Perhaps, with the ceasefire now in place, investors were convinced that the surge in oil prices will prove to be temporary as Fed Chair Powell highlighted in his remarks last week.

Focus turns to US PPI inflation data

Next week appears relatively light compared to the previous ones, with the only US releases worth mentioning being the PPI figures for March, due out on Tuesday, as well as the industrial and manufacturing production rates, scheduled to be released on Thursday.

A strong rally in the PPI figures could revive worries that the inflation problem may be more serious than initially thought as higher producer prices now could translate into stickier consumer prices in the following months. Thus, anything suggesting that prices could remain elevated for a while longer may convince investors to scale back their rate cut bets.

Having said that though, conditional upon the truce in the Middle East remaining in effect, this is unlikely to revive rate hike bets and thus, the dollar is unlikely to stage a meaningful recovery.

After all, although rate paths were lowered elsewhere as well, most major central banks are still expected to proceed with rate hikes, which marks a divergence between them and the Fed. The ECB is still expected to press the hike button twice this year, while 30bps worth of rate increases are penciled in for the BoE. The probability of a BoJ rate hike later this month remains a coin toss and there is a strong 60% chance for the RBA to proceed with the third consecutive quarter-point rate increase at its upcoming meeting in May.

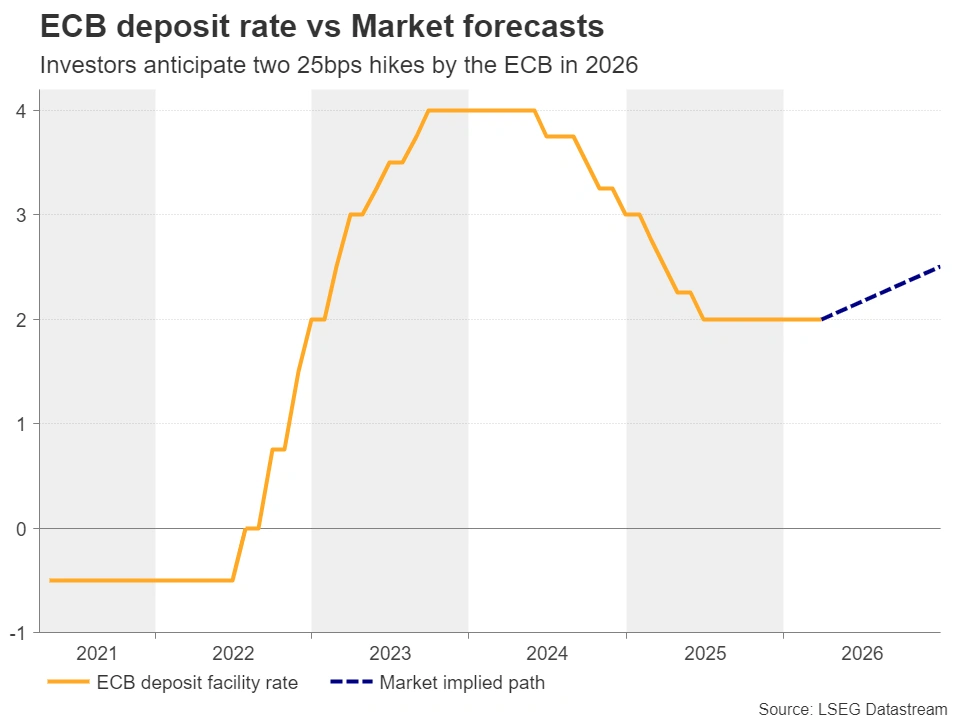

ECB minutes to reveal how willing officials are to hike rates

Speaking about the ECB, the minutes of its latest monetary policy decision, held on March 19, will be released on Thursday. At that meeting, policymakers kept interest rate unchanged but signaled they were closely monitoring growth and inflation risks from surging energy prices amid the war in Iran, adding that they were ready to adjust their strategy if deemed necessary.

More recently, ECB policymaker Dimitar Radev noted that Eurozone inflation expectations were at risk of rising more quickly and that the Bank should be ready to raise rates swiftly. This, combined with the flash CPI data revealing a jump in headline inflation to 2.5% y/y in March from 1.9%, allowed investors to maintain bets of around 50bps worth of rate hikes by the end of the year.

Therefore, euro traders will dig into the minutes to see how willing other policymakers were to shift to rate increases if the situation warrants so. Although the information could be deemed outdated, as the meeting took place amid an escalating war, an intense hawkish flavor could corroborate the notion that the ECB could consider raising interest rates even after the ceasefire, allowing the euro to continue gaining against its US counterpart.

Weak UK data could weigh on BoE hike bets

In the UK, the monthly GDP, the industrial and manufacturing production figures, as well as the trade data, all for the month of February will be released. Weak growth-related numbers even before the war in the Middle East erupted could prompt investors to question whether it will be wise for the BoE to proceed with rate hikes, especially amid a ceasefire.

Thus, receding rate cut bets could weigh on the pound, but with an even weaker US dollar, any pound losses may be more prominent on the euro/pound pair.

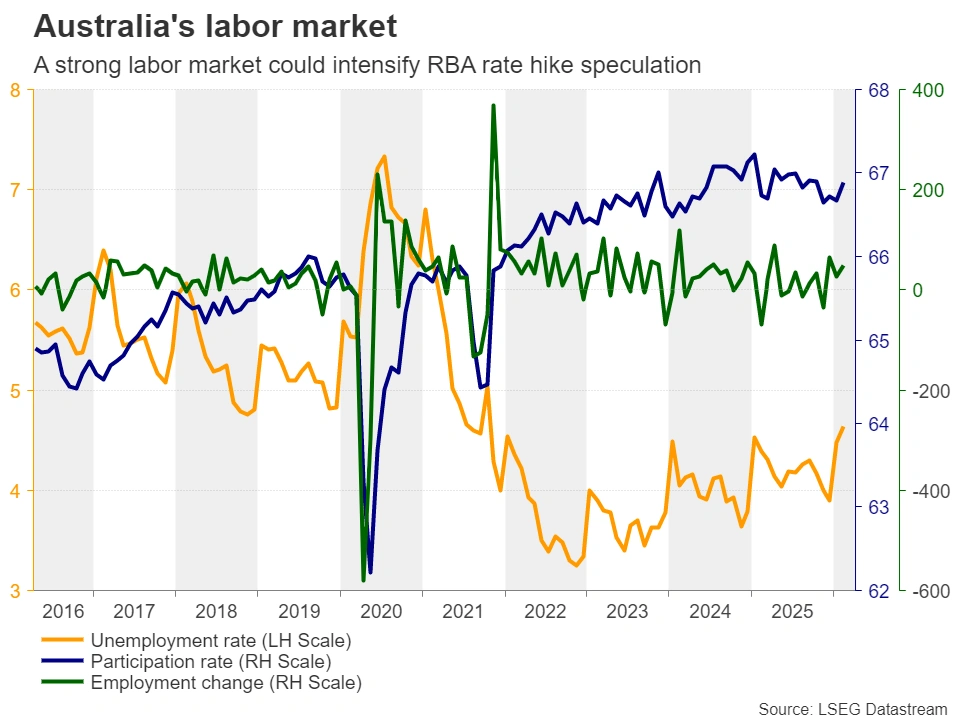

Australian jobs report and Chinese GDP to move the Aussie

The risk-linked aussie was among the currencies that benefited the most amid the truce announcement, surging as much as 1.75% on Wednesday. The increase in risk appetite and the still hawkish RBA rate expectations are very supportive variables for the currency. A strong employment report for March on Thursday could allow investors to take the probability of third straight 25bps hike by the RBA higher and thereby allow further advances in the commodity currency.

Aussie traders are likely to pay attention to Chinese data as well, as China is Australia’s main trading partner. During the Asian session on Wednesday, the world’s second largest economy will release its trade data for March. The GDP for Q1 is due to be released on Thursday, alongside the industrial production, retail sales, fixed asset investment and the unemployment rate, all for March.

Although trade tensions between the US and China have eased, the conflict in the Middle East and the spike in oil prices during the month of March may have left their mark on the Chinese economy, which is the world’s biggest oil importer. If the data suggest that China was able to withstand the pressure, the aussie may strengthen even more.

{kind=link}