- We expect the Bank of England on hold, but hawkish voices are growing louder.

- Data has come in on the soft side since the April meeting, but the inflation risks remain pronounced.

- Data releases ahead of the meeting could push more votes back in the hawkish camp but are not likely to change the hold decision.

Since the April meeting, data has supported our call for maintaining Bank Rate unchanged. That said, it remains too early to make any conclusions on inflation spillovers. We get fresh inflation and labour market data ahead of the meeting.

May PMI data suggest the economy came to a marked slowdown following a solid April print, as the service sector index took its steepest decline in four years. The manufacturing sector on the other hand remains quite solid with sustained growth in output and orders. Q1 growth was relatively high at 0.6%, although uncertainty on the seasonal pattern suggests momentum might be weaker. Retail sales reflected the deteriorating consumer sentiment in April with the biggest monthly decline in a year.

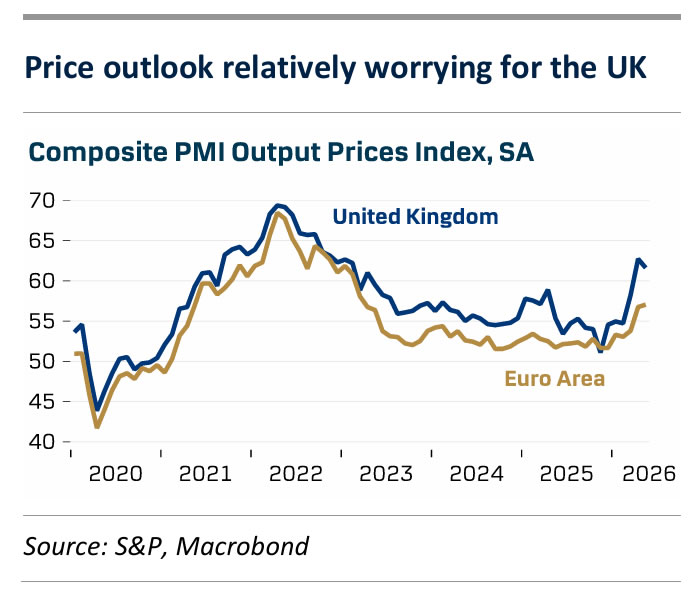

Job loss accelerated to -100K in April and the unemployment rate increased to 5.0%. At the same time, wage pressures remain on a weakening trend and according to the BoE decision maker panel (DMP), firms also expect slower wage growth going forward, which is key to the prospects of sustaining service inflation at acceptable levels. CPI inflation was lower than expected in April as core inflation continues lower. Producer prices, on the other hand, are on the rise and the PMI survey suggests businesses are raising prices, particularly in the manufacturing sector but also in service. Reported price increases are much steeper than in the euro area. According to the DMP, businesses largely expect compressed margins, though, suggesting more modest feed through of energy costs.

We continue to see Governor Bailey’s stance as the key to pin down the policy outlook. His remarks have been mostly dovish leaning as he has argued that allowing inflation to run above target is justified given the uncertainty about the impact of the Iran war on the economy and the weak pace of growth. We could quickly be back in a situation with a completely split MPC with recent hawkish remarks not least from Meghan Greene, who is more worried about second round price effects than what the official BoE risk scenarios imply.

BoE call. Hiking rates will have to be weighed against a considerable risk of exacerbating a looming economic contraction. We think it is most likely the BoE will remain sidelined for the foreseeable future, but the vote split could soon be back where only a slim majority stands in the way of hiking rates.

Market reaction. We will keep a close eye on the updated views of MPC members and the vote split. The relatively weak UK growth outlook and our dovish stance on BoE compared to market pricing weighs on our GBP call. We forecast EUR/GBP to move higher towards 0.89 on a 6-12-month horizon.

{kind=link}